What is the applicable latest Post Office Small Saving Schemes Interest rates Apr-June 2018? The government announced the interest rate for PPF, Sukanya Samriddhi, NSC, KVP Interest Rates Apr-June 2018. Let us see the changes applicable with effective from 1st April 2018.

Earlier the interest rates used to be announced on yearly once. However, now from 2016-17, the rate of interest will be fixed on a quarterly basis. I already wrote a detailed post on this. I am providing the links to those earlier posts below.

- Post Office Savings Schemes -Changes effective from 1st, April 2016

- Premature closure of PPF account – New Rules 2016

Based on these new changes, now onward interest rate will be declared on a quarterly basis. The earlier quarters (FY 2016-17 and FY 2017-18) interest rate can be viewed in my earlier posts “Interest of PPF KVP NSC SCSS and Sukanya Samriddhi for April-June 2016“, “PPF and Sukanya Samriddhi Scheme interest rate July-Sept 2016“, “PPF, Sukanya Samriddhi, NSC, KVP Interest Rates Oct-Dec 2016”, “PPF, Sukanya Samriddhi, NSC, KVP Interest Rates Jan-Mar 2017“, “PPF, Sukanya Samriddhi, NSC, KVP Interest Rates April-June 2017“, “PPF, Sukanya Samriddhi, NSC, KVP Interest Rates July-Sept 2017“, “PPF, Sukanya Samriddhi, NSC, KVP Interest Rates Oct-Dec 2017?. and “Latest Post Office Small Saving Schemes Interest rates Jan-March 2018“.

Below is the timetable for change in interest rates for all Post Office Savings Schemes.

As per the schedule, Government announced the interest rate applicable to all Post Office Savings Schemes from 1st April 2018 to 30th June 2018.

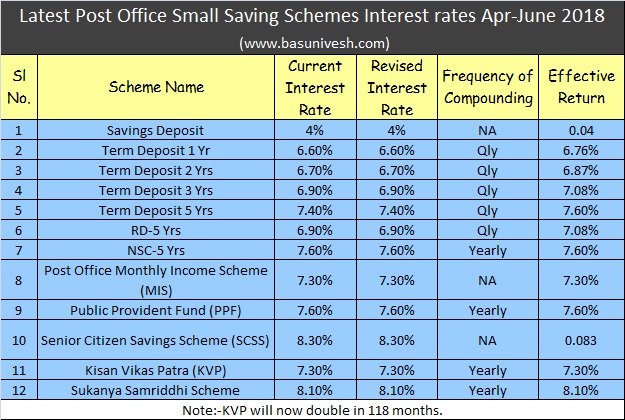

Latest Post Office Small Saving Schemes Interest rates Apr-June 2018

Just to quickly recap, last quarter, Government reduced around 20 BPS or 0.2% for all its schemes (except Savings Account interest rates, SCSS).

However, for this quarter, Government maintained the same interest rate. Hence, below is the latest Post Office Small Savings Schemes interest rates Apr-June 2018.

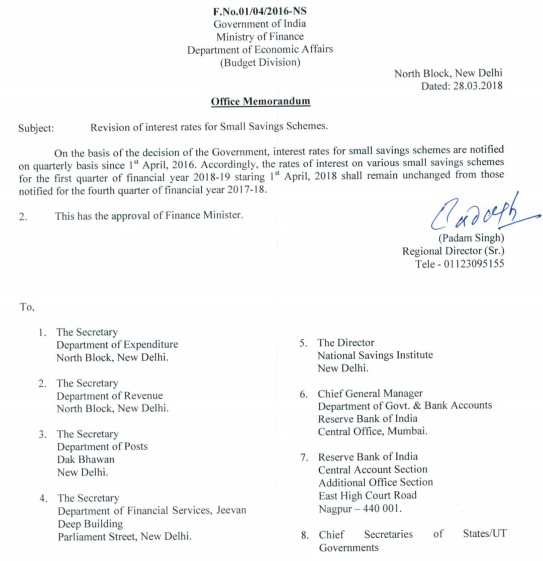

Below is the notification in this regard from the Ministry of Finance.

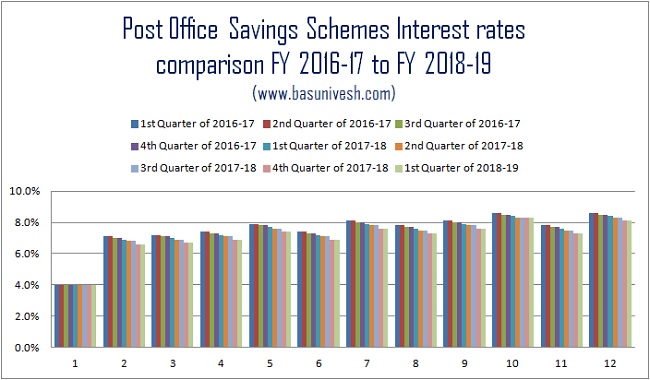

Post Office Small Saving Schemes Interest rates trend FY 2016-17 and 2018-19

Below is the interest rate trend for FY 2016-17 and FY 2018-19.

You notice that only savings account interest rate is same for almost two years. Rest of all products interest rate slowly reduced.

Refer our earlier posts related to Post Office Savings Schemes-

- All about Public Provident Fund (PPF)

- How to open PPF account online in ICICI and SBI Banks?

- PPF and NSC for NRIs – Amendment Rules 2017

- PPF Account for Minor and Wife – Rules, Tax Benefits and Tricks

- How to encash or withdraw NSC bought from different Post Office?

- NSC-Accrued Interest taxation and way to reduce it

- Post Office Monthly Income Scheme or MIS – A complete guide

- Premature closure of PPF account – New Rules 2016

- PPF withdrawal rules & options after 15 years maturity

- Public Provident Fund -20 unknown facts

- 15 Rules of availing Loan against PPF (Public Provident Fund)

- How to transfer PPF Account from Post Office or Bank to another Post Office or Bank?

- Excel PPF Calculator-Calculate goal, loan or withdrawal amounts

- PPF-Loan and Withdrawal

- PPF-When to contribute to get higher returns?

- All about Kisan Vikas Patra (KVP)-2014

- Sukanya Samriddhi Account -When to invest to earn more returns?

- Sukanya Samriddhi Account-An investment scheme for your girl child

- Post Office Senior Citizen Scheme (SCSS)-Benefits and Interest Rate

- NSC and KVP in e-mode and Passbook mode from 1st July 2016

- How to transfer NSC from one person to another?

- India Post Help Centre and a Toll-Free Number 1924 features

What is interest rates for second quarter means from July to September 2019.

Dear RG,

As per my knowledge, it is not yet declared. Once it is declared, then I will write a new post soon.

So till that time the Q1 rates will be only applicable?

Dear RG,

No, they will announce may be today night or tomorrow early morning.

Dear Sir, thanks for your blogs. Great insight.

Quick question : When there is change in interest rates, as informed it is now quarterly effective FY 2016 – 2017, does it impact the existing investment ? For instance, I had started the RD 34 months ago. Will this change in interest rate impact the RD rate which was offered 34 months ago ? Require some clarity on this.

Dear Edgar,

For RDs, FDs, SCSS and MIS, the interest is applicable which they offer during the time of booking it.

Sir on 11.4.18 I invested one lac in NSC , now the rate of interest in NSC is 7.6 % . If I calculate the maturity amount comes 145200.66 but in my nsc pass book it shows 144232.00.

Kindly advise us what is right.

Ashok-Contact the Post Officials for the same.

NSC interest calculeted yearly & you calculated half yearly

Rajinder-Check properly.

Super-As of now there are no such offerings of Infra Bonds.

Which would be better sukanya samridhi plan or investing in mutual fund for similar tenure with fixed amount to be invested every month.

Rajiv-You are comparing an apple with orange. Don’t differentiate them as one is debt product and another is equity. You need both in right proportion to reach your financial goals.

Thanks for sharing this valuable information.

you are doing a great job.

Manisha-Pleasure 🙂