Recently, ICICI Pru Life launched new online term insurance plan “ICICI Pru iProtect Smart”. This plan is called as one of a comprehensive term insurance plan in the market.

This plan I think combines all the features a term plan must have. Premium payment flexibility (Single, Yearly, Half-Yearly, or Monthly), Maximum Term of up to 40 Years, Riders like Accidental and Critical Illness, and a variety of benefit amount payment option.

Features of ICICI Pru iProtect Smart

Below are some silent features of this plan. You notice that accidental and critical illness riders maximum limit is not disclosed and I feel depends on individual cases.

- It is a pure online term plan.

- Coverage against death, terminal illness, and disability.

- Provides riders like accidental and critical.

- Special premiums for women.

- Covers s female organ cancers such as breast cancer and cervical cancer.

- You can enhance the sum assured at the later stage based on the increase in financial responsibilities, like your marriage, the birth of a first or second kid.

- Different benefits payout options.

- The surrender value is applicable only to Single premium policies. You can surrender policy and get the surrender benefit. This is calculated as-Surrender Value = (Single Premium*Surrender value factor/100)

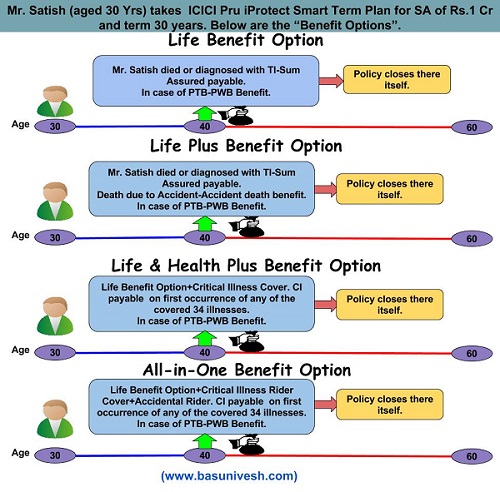

Benefit options of ICICI Pru iProtect Smart

First, let us look at the benefits options this plan provides.

- Life-Nominee will receive the benefit only in case of death of a policyholder, terminal illness of policyholders. Along with that, if the policyholder diagnoses with Permanent Disabilities (PD) due to an accident, then the future premiums are waived off. The policy will continue as usual without any premium payment from the policyholder.

- Life Plus-Along with “Life” option, this option provides you accidental rider benefit.

- Life & Health-Along with “Life” option, this option provides you critical illness rider benefit. It covers around 34 major illnesses. The list of this is available HERE. The policyholder will receive the full benefit irrespective of the actual cost of treatment. This benefit can be exercised only once during the policy period. Once the CI benefit paid, then the policy will continue as usual (without CI rider benefit). Please note that, if the CI benefit and death benefit (SA) opted are equal, then after the CI benefit payment, the policy terminates there itself. In addition, if the incident is covered under accidental rider as well as in CI rider, then policyholder will receive the benefit from both the features.

I tried to explain the same in a simple graphical way as below.

- I assumed that incidents of death or terminal illness occurred at 40 years of age.

- Critical Illness is equal to death benefits sum assured.

What is Terminal Illness?

It is an illness, which is highly likely lead to death within 6 months. It must be diagnosed and confirmed by medical practitioners’ registered with the Indian Medical Association and approved by the Company.

Death benefits payout options–

This plan offers three types of payout option of benefits. These are explained in below image.

ICICI Pru iProtect Smart premium illustration–

ICICI Pru iProtect Smart premium illustration–

Look at the premium chart once. You notice that the cheapest option is for “Regular Income” and costliest one is “Increasing Income”. Regular Income option is cheap because they keep the death benefit with them and pay you yearly for rest 10 years. However, Increasing Income is costliest-Because they have to pay 10% per year for 10 years with the increase in inflation at 10%.

If you wisely educate your nominee about how to utilize the claim amount, then your family will have control over money and they are capable of handling any emergency. However, in regular income and increasing income option, they don’t have control and further liquidity. In case of emergency, they can’t withdraw the additional money from this death claim.

Life Stage Protection feature–

Along with all these features, ICICI Pru iProtect Smart offers “Life Stage Protection” feature. You can increase the sum assured when you reach the important milestones of your life. The details are as below.

- Marriage-You can increase another 50% of additional death benefit available to original death benefit (maximum limit is Rs.50, 00,000).

- Birth/Legal adoption of 1st Child-You can increase another 25% of additional death benefit available to original death benefit (maximum limit is Rs.25, 00,000).

- Birth/Legal adoption of 2ndt Child-You can increase another 25% of additional death benefit available to original death benefit (maximum limit is Rs.25, 00,000).

The premium for this enhanced death benefit will be calculated based on the increasing sum assured and remaining policy term. This feature is available ONLY for LIFE OPTION.

My take on this plan–

- Don’t wait, but buy the PURE ONLINE TERM PLAN immediately.

- Each feature of this plan is charged indirectly. So never ever, think that it is a free add-on. However, think whether there is a necessity of adding features.

- There are many limitations in the case of a critical illness rider. Hence, I suggest to go for standalone critical illness insurance than buying as a rider. Buy this insurance only in case you have a family history of such diseases. It is one the complicated rider or insurance, which hardly understandable to the common person.

- In this plan, an accidental rider will be an option only in case of DEATH due to an accident. If you met with an accident, then maximum benefit you can opt is PWB and that too in case of permanent total disability. However, you will not receive any compensation if you are bedridden. This is the reason, it is always best to go for standalone accidental insurance rather than riders with life insurance. In case of standalone accidental insurance plans, you get benefits based on the disability %, which is not the case with accidental rider.

- Critical Illness option is payable only once during the life of the policy. Also, if your critical illness rider is equal to sum assured you offered in the basic plan, then after the payout of critical illness the plan ceases there itself. Therefore, at the later stage, you may have to survive without any life protection.

- In case of benefit payout options, I suggest to go for a lump sum and at the same time educate your nominee or family members of how to use the claim amount wisely. If not educate your family about how efficiently they can use the death claim, then it is WASTE TO BUY TERM INSURANCE. Because, in your absent anyone can trap your family and create a bad investment choice for your family. The two other options “Income” and “Increasing Income” options are good only if you feel that they can’t handle money and along with that they have enough emergency cash to meet any emergencies.

- The enhanced feature is only for marriage and up to 2 kids. What if you have other financial obligations like your spouse education, kid’s education, or some other financial goals? One will not enhance his term insurance only because of marriage and kids. But there are many other financial obligations which we can’t predict. The enhancing feature has restrictions on the sum assured and available with LIFE OPTION only. Hence, I think this just eyewash.

- Considering all these factors, what I feel is buy pure standalone lump sum payable term insurance. I think, ICICI launched this plan just to be in this competitive market as other insurance companies offering lots of add-on features to their term insurance plan.

I had purchased iprotect ismart policy of 5000000 at 10163 yearly. I am still going with it but some reviews in YouTube make me confused company’s credibility if they would fulfil my future unwanted requirement because so much confused exclusions are injected to escape their payment. Please make me confident with your valuable comment as you usually do.

Dear Subrata,

How can you compare your future death with the so-called Youtube experts examples of deaths and reasons?

Dear Basu

I am salaried person and already have term plan from icici and good going.

My wife is housewife. I like to buy term plan for her also but she is not earning member.

I checked with ICICI on this. They said they can give me term plan for my housewife based on my term plan but maximum cap would be 50% of the sum assured of my term plan.

This policy is issued under icici pru Smart term plan.

Just looking for your comment on this if possible.

Dear Naveen,

Do you need a LIFE INSURANCE for your spouse? If she is not working, then Life Insurance is a waste for her.

Hello sir,

I have seen two term insurance from icici pru iprotect smart POS and iprotect smart. Which one I can go. I am salaried person working in IT industry. Is waiver of premium is good to take for a term insurance . Please suggest.

Dear Dileep,

Let them LAUNCH 100000 VARIANT products 🙂 Go with simple Term Life Insurance without riders.

Hi sir, My doubt is if a person has taken the icici I protect smart term plan, if that policy holder immediately dies in the same year.Does his nominee can claim? what are the minimum premiums had to be paid in such case?

Dear Sravanthi,

YES, the nominee can claim. Even if the single premium is paid and the policy is issued, then the nominee has a right to claim.

I bought icici iprotect smart life term plan a year ago. Recently i checked my documents and it has four different plan .life. life plus. Life health. All in one. I belong to Life . I am bit confused whether life policy covered against death due to accident. It shows no to accident death which means if i die on accident my nominee wont get nothing based on this policy. Please clear my doubt as I want to cancel this policy.

Thank you

Dear Jos,

Who said death due to accident not covered?

Sir I have already taken ICICI Pru i smart term plan of 85Lakhs of 85 years of age . In this policy category shown Non Medical .

Any medical tests not completed till today . Please give me suggestion

Thanking you sir

Dear Ganapathi,

What suggestion you looking for when you already purchased it?

Sir I have purchased ICICI term policy but not completed medical tests .

Dear Ganapathi,

If you are uncomfortable, then better not to proceed.

Hi Sir,

I am taking a home loan if Rs4450000 in HDFC, they are asking me to take insurance for the same, insurance name is HDFC flexi grow. Yearly premium is about 120000, can i go with that? Please advise, i dont have any idea about that.

Dear Shiv,

Stay away from such dangerous people and products.

I have already taken I care 2(term insurance) with 59lakh sum assured with premium 25487 from 2012 (total term 30 years) till my age of 71 years.now they have advised me to change the policy to I protect smart with premium 58000 for 5 years with policy term 37 years.my present age 48 . will it be good to change?

Dr.Shaji,

Stay away from such SELLING tactics.

Dear Sir

Your blogs are very nice. Can you please give your opinion on Edelweiss Tokyo Zindagi+ term insurance plan.

This company is pretty new. Is it advisable to go for a term insurance with this company. Your comments will be very much helpful.

Dear Srinivasan,

It is better to go with well established.

Please don’t get bluff and spend your energy with ICICI iProtect Smart term plan. Their management is worst to response and bluff you with no valid reason.

In my case, they reject my application -OB10963288 based on my past medical history which I clearly stated in application form and provided most medical reports. The worst part it – they send me 37 KM for USG test one way and no major difference in my old and new USG observation.

If my medical condition is so worst to process my application further, they should reject it in first instance rather ICICI made me go through all this medical process.

As far as learn from term plan market, diabetes, high/low bp are more severe conditions and they accept such cases with high premium. However, my premium was low 3.75 lakhs for 10 years for 1 CR term plan. So, might be they won’t get benefited in my case and simply rejected.

Please don’t spend your energy and money with them. They are worst, energy-sucking and pain giving players in market.

Dear Geeta,

Sad to hear your bad experience. However, this may not be considered as company specific. If the underwriter feels there is a risk, then they may load the premium, reduce the sum assured or reject your proposal. Hence, better you search different option.

Can you pls elaborate, how CI rider is complicated?

Does it mean, I will face problem in opting money if I am diagnosed with critical illness?

Dear Akash,

The definitions are mainly in generic and many terminologies are hard for the common man to understand. I am not saying that just because of this, you will face the issues at the time of claim. But what I am pointing is that to understand it well.

hello

i am confused between icici pru life and max life term plan

which one is best ?

Dear Mangesh,

Both are fine to me.

I wanted to know which term plan is better among ICICI and Max?

I am using ICICI Bank services for last 9 years and quite impressed with their service and also had positive review from 2-3 friends about I Protect plan. But Policy Bazaar insurance advisor also mentioned about Max term plan as the CSR is 98.3% with lower premium. I also checked and it looked good. But when going through reviews on internet, negative reviews exist for both and more for Max Insurance.

Now I am confused.

Dear Rakesh,

Two things I think you missed here. ICICI Bank is an entirely different entity with respect ICICI Pru Life. If your banking experience with ICICI Bank is excellent does not mean the same experience with ICICI Pru Life. Second thing, Policy Bazaar act like an online aggregator, if you buy using their portal (even though it is ONLINE Term Life Insurance), they get certain benefits. Also, to list the product on their portal they charge a certain fee to the Insurance Companies.

Hence, I am suggesting you first understand the CONFLICT of interest in the industry then believe on anyone. For latest updates, you may refer my post “Top 5 Best Term Insurance Plans in India 2019“.

Thanks Basu for your reply and the information. I read you article on ‘Top 5 Best Term Insurance Plans in India 2019’.

I understand that both the entities are different. What I was trying to convey was ICICI as a group which makes ICICI PRU also reliable.

About Aggregators- even if they get commission from Insurance companies, does this impact anything at insurer end in Term Policy. As per their version, they are helpful with the process and also at the time of claim settlement.

You mentioned ‘Aegon I-Term ‘ in best 5. But number of policies and Benefit amount is very less in comparison to other 4. Does this matter? But other criteria are good enough.

ICICI was good enough in all criterias. I was confused because of some negative reviews by customers.

Dear Rakesh,

If you trust the ICICI group, then go ahead with ICICI but never be in the false trap the aggregators will help you in cliam settlement process. They are not for social service. Whether the negative reviews by customers are GENUINE or what? Whether you cross checked?

Hi sir…. I took icici life insurance…. In medical it shows nicotine test positive….. Why they ask now extra premium…. Pls reply me clearly sir

Dear Arun,

It is completely underwriter’s decision. You have only two options either to accept or move to some other insurer.

What documents are required for ICICI prudential term plan? Are the documents different for NRI?

Dear Sanjay,

Check with the concerned insurer.

Dear sir,

I brought ICICI pru I protect smart policy. 2.5 lack instalment per year. Whether my decision is correct to go with this policy or any better option available. ?

Dear Shree,

I recommend one thing always, NEVER COMBINE INVESTMENT WITH INSURANCE.

Hi,

I have taken ICICI i protect smart plan. I am confused whether it is a right decision ? Kindly guide

Dear Sheetal,

What prompted you to doubt on your own decision?

Never get into such useless products. If you have surrender option without much loss than you should exit. Advisors/agents are just pushing to make quick money..stay away..

Hi Basavaraj,

I am not sure whether my previous question was posted here or not, so i am repeating my question.

Which one would you prefer between Aegon, HDFC and ICICI for term insurance and considering same features in all 3. I know by premuim wise Aegon is less expenesive, but I would like to know which company among above mentioned is most reliable or hassle free while settling the claims?

Thanks,

Janardhan

Dear Janardhan,

I have replied to your email.

I need to buy to separate term plan for me and my housewife, with maximum coverage yr. I am in dilemma which company to select?

Kindly suggest

Dear Suman,

Do your wife really need a LIFE INSURANCE? The ideal coverage should be around 15-20 times of your yearly income. Refer my post “Top 5 Best Term Insurance Plans in India 2018“.

she was a banker but after marriage she has quit her job. Now no company is ready to give term plan bcoz she has no Income proof.

What if I take only SBI general personal accident insurance of rs.1000 for 20 lakh

Dear Suman,

Accidental Insurance is different than normal Life Insurance. Please read the features before jumping into buy.

Dear Suman,

Yes, to buy Life Insurance one must have a certain income.

does ICICI prudential pay base amount in case of accidential death incase of Life Plan?

Dear Dhrumil,

YES.

Hi Basavaraj…

Hope you are doing well!!

I am planning to buy a health insurance policy , friend of my suggest for ICICI I Protect Plan, I am in dielimma , kindly suggest .

Thanks

PC

Dear Pallabi,

What is your dilemma?

My dielimma is ,should i go for ICICI I Protect Plan or any other health insurance plan which is available in current market , pls suggest .

Dear Pallabi,

Why you are mixing Life Insurance with Health Insurance??

Hi,

I am a NRI. i would like to take icici iprotect (all in one) for my wife (she is currently working in india. if i take insurance for her now, and if she become a NRI after two years is policy cover her as NRI?

if anything happen while in abroad (CI or accidental death) is policy will cover?

Regards

Dear Prince,

Yes, it covers. However, it is best to inform your insurance company for such residential status change.

Hi Basavaraj.. Thank You for such a good article. You are suggesting that we should take a basic life option plan and for riders like terminal illness and accidental death, we should go for a separate general insurance plan. I am a bit confused here.

Let’s say a person has opted for life benefit option (where no riders are involved) and that person dies due to any illness or an accident. Will his nominee will still get the sum assured due to death caused by TI or accident (even when he has not taken accidental death rider) ??

Thanks in advance 🙂

Dear Ashish,

YES, nominee still get the death benefit.

What does PTB-PWB Benefit from chart means?

Venkatesh-Terminal Illness Benefit and Premium Waiver Benefit.

Thanks Basavaraj!

I have a term plan which i took in 2013.i just want to knw if Section 45 of Insurance amendment act is applicable on this policy also?

Ajay-YES.

If i take critical illness of 25lacs and isurance of 1crore. And after 2year if i get to know that i got cancer or somethng like this, will icici ipru will cover in early stage or they only give in last stage wen insurer going to die within 6month??

Eshan-This is what they claim “In life & health option, if the life assured is diagnosed with any one of the 34 Critical illness mentioned below, the life assured will be paid the critical illness benefit amount immediately at the first diagnosis stage without any medical bills.”

I am having ICICI PRU I CARE POLICY OF RS 30.00 LACS WHICH IS HAVING A TERM TILL I ACHIEVE AGE OF 60 YEARS. NOW I WANT TO TAKE I PRU IPROTECT OF RS 50.00 LACS WITH A TERM OF 40 YEARS. MY CURRENT AGE IS 34 YEARS AND I AM EARNING ANNUAL SALARY OF RS 8 LACS P. A. PLEASE INFORM IF I CAN TAKE NEW POLICY AS WELL AS CONTINUE MY OLD I CARE POLICY.

2)ARE MEDICALS REQUIRE IN IPROTECT PLAN FOR AMOUNT OF RS 50.00LACS? I AM EJOYING I CARE TERM PLAN SINCE 2013.

Ajay-If you have no issues with ICICI, then go ahead with ICICI itself. Yes, they do medical examination again.

For term policies i heard that companies ask for medical check up at regular interval (3-5 yrs) .

and based on the result the premium is also changed.

is it true??

Giri-FALSE.

thanks

Sir,

Is the Death caused by earthquake, flood or due to any other act of god covered under Accidental Death benifit rider ?

Jewel-In general YES. But better to cross check with the insurance company.

Sir, I am in a job profile of traveling to different countries, If I have died in other foreign countries will these policy covers.

I am a employee in India and salaried in India but I travel around the world

Prasanth-YES. But you have to inform about the nature of your job while buying the policy.

Hi Sir,

Does ICICI Pru lifeprotect’s base plan i.e life option covers death due to accident. If yes then what is the use of separate accidental rider. Example: If someone has opted for life option only for 1cr cover and he/she dies due to road accident, will it be covered under basic plan or do we need to opt for additional rider.

Which term plan is good amongst ICICI, Lic, HDFC and MAX. I am very confused between them.

Sonali-Sonali-All life insurance policies cover death due to accident also. However, in many cases, person meet with an accident but not die. Instead, he get bedridden due to disability. In such a situation, based on the condition of the insured, accident benefits will be payable (if you opted for accidental rider). Hence, accidental rider offers benefits which are extra than ONLY death.

For me all are good. Hence, choose the one which is BEST to you.

Hi sir

Iam 24 years old. I want to take term plan with 75lac in one company for 36 yers, another 25lac from different 15 years is it good to take insurance from two companies

Ram-Why you thought to split?

Hi ,

Is it better to buy LIC eterm or ICICI standalone term plan. The credibility point of view LIC is better and premium is lesser in ICICI. So which will be the better choice or any other company to choose.

Anand-To me both are best.

Hi Basavarj,

Hope you are doing good. I’m looking for one Health Insurance plan and gone through few plans but couldn’t decide which is the best one to buy. Could you help me decide in buying one?

Dilip-Refer my post “IRDA Incurred Claim Ratio 2015-16 | Best Health Insurance Company in 2017“.

Thanku very much sir

Hello sir..

I have taken this icici term plan 6 months back.but I mistakenly forgot to declare one of my previous endowment policy in the proposal form..

Can this be declared now??

Or will I have to break the policy and then again have to declare about that undeclared policy..?

Sir,Please also clear, whether it is true that after 3 continuous premium payment, insurance companies have to pay the death claim, irrespective of the fact that customer has revealed? or concealed some facts??

Gairi-Better to share it NOW. It is true about 3 years cluase. But it does not mean that you hide and let insurer find the facts.

Hello, you mention that its good to buy this plan as a pure online term plan and that its better to buy the Accident and Critical Illness separately. Can you kindly inform about a couple of good policies where Only Critical can be purchased. Also any suggestions for Accident only policies (it seems that the got Medical assueres like New India and United have a 10 lakh cap on accident and it cant be increased beyond that. Their covereage of accident seems comprehensive, it will be great to have a similar with a higher coverage)

Ajit-You can check those plans from General Insurers and standalone health insurance companies.

Hi Basavaraj

Does this plan cover, death in other countries. I am in a job profile which requires me to travel to different countries ?

Also, does it cover death due to Aeroplane crash ?

I know, these are rare scenarios, but just want to make sure, whether it is covered or not ?

regards

Harsh

Harsh-For safety purpose, it is best to inform the insurance company about your such travel. Air crash is covered under term insurance as it is an accidental death.

Hi Sir,

I am looking to buy term insurance. Age 29 yrs Non Smoker Female. I have seen term insurance plans of PNB MetLife and Max Life Insurance. PNB executive visited my home and he suggested to buy standalone term insurance which is similar to what you advise. The premium of Max is lesser than PNB Metlife for pure term insurance. Claim settlement of PNB is very much lesser as compared to Max Life. Please suggest how much impact really does the claim settlement ration make?

Thanks

Priyanka J

Priyanka-In that case why not go with Max?

Hi

What so you mean by standalone Term plan ? You mean its better to take Only Life Option ?? which covers Death benifit and terminal illness +waiver on premium on permanant disability ?

Please suggest !! Thanks in advance

Gowtham-Buy a pure LIFE INSURANCE from the LIFE INSURANCE PRODUCT. Rest of features can easily be available from General Insurance with much enhanced features.

Hi,

thanks for all the insights that you have provided in your site. It’s awesome.

which is a good critical illness policy(looking to cover me & my wife) that we can opt for for a coverage of 20L?

Thanks for your help.

Bharath-There is no specific one. However, you can check with public sector companies or standalone health insurers.

dear sir i like to know that which kind of death is acceptable to get benefit. or its any kinde death?????

plz help me to find out this plan

Ajay-There are millions of reasons for death, I can’t list all of them. But for particular product, while buying you can check for exclusions.

Dear Sir,

Can you please answer me? If I take a all in one for policy term of around 30 years since that is max, post 30 years is it possible to renew for another 15 years since the max is 75 years? the adviser told me that it is possible to extend the term but I am not sure

Example

Now – Age 30 – Poilicy starts

Later – Age 60 – Policy ends (since it is 30 years max for all oin one )

Max is 75 at exit

Is it possible to renew from Age 60 to 75 ?

Muthuraman-Yes you can take. But do you feel insurance required after 60 years of age? Do you feel the premium be same as that of today? Will the company issue easily as it is today?

Hello Basavaraj,

Your article is informative and to the point. Thanks for your post.

I have a query.

I have bought LifeOption+Regular Income type on Jan’16. Can I change the policy to LifeOption+Lumpsum from Y’17 onwards?

Manjunath-I think change not possible in middle.

HI MR:BASAVARAJ,

Great Article,

Can you please let me know whether this policy is available for Non Resident Indians ?

Thanks

Thomas

Thomas-It is not clear from the information they provided. Hence, I suggest you to directly contact ICICI Life.

Hi Mr.Basavaraj,

The branch manager says it is open for NRIs also, but nowhere it is mentioned anywhere in their site.Polizybazar guys also say it is open.Bit confused! Thinking of going ahead with hdfc one which clearly gives the option to mention your residence status.Please advise.

Thomas-First check whether the option of mentioning your residential status is available in proposal form or not. If it is there then go ahead with ICICI iteslf.

HI BASAVARAJ SIR,

IN THIS I PROTECT SMART PLAN WITH INCOME OPTION, THEY WILL KEEP 90% OF MONEY WITH THEM. SO MY DOUBTS ARE

1. WILL THIS YEARLY INCOME TO THE NOMINEE IS TAXABLE? BECAUSE IT IS DEATH BENEFIT IT SHOULD NOT BE TAXED RIGHT?

2. WON’T THERE IS LOSS OF BANK INTEREST TO THE NOMINEE? EVEN IF THE NOMINEE IS FINANCIALLY ILLITERATE, HE CAN KEEP FD AND AT THE PREVAILING RATE OF 7% FD INTEREST LOSS WOULD BE AROUND 31 L TO NOMINEE IF SUM ASSURED IS 1 CR. THEN INCOME OPTION MAY NOT BE THE RIGHT OPTION, I BELIVE

KINDLY SHARE YOUR THOUGHTS SIR

REGARDS

DR RAJESH PAI

Rajesh-1) It is tax-free.

2) Yes, that is why I advised not to opt this feature.

Hi Basavaraj,

Need some advise w.r.t Term Insurance plans. I am in the lookout of taking a Term plan till the age of retirement at least. Do you think ICICI term plan would be a good option.? Some points on which I seek your advise are:

(A) What are the ifs and buts if I take an accidental rider along with the term plan?

(B) What is your take on critical illness and terminal illness. I mean under which situation, ICICI can decline the claim? They say for a 50L cover, no medical is required. Its only required for a 1 Cr. covered. Does that mean that if I take a 50 L cover and at a later date some disease is detected, they can come up saying that it was not declared at the time of availing the policy and therefore, the claim is rejected.

(3) What are the hidden risks in permanent disabilities in this Plan?

Request your advise on the matter.

Sandeep-A) You will end up with less featured accidental insurance.

B) There are many reasons for decline. How can I list them all?

C) Hidden Rules??

Ok. But what would be the important ones like that cannot be neglected??

Sandeep-Many..How can I list all probabilities??

I can understand. What would be your suggestion then if I have to take a Term plan. Which would be the best one in term plans i.e. having less risk features?

Also would you kindly suggest which plan can be availed for accidental insurance?

Sandeep-Refer my latest post “Top 5 Best Online Term Insurance Plans in India-2016“.

Thanks for the information. However, my doubt is:

Assuming I take a pure ICICI term plan with only death benefit option and no riders such as Accidental or Critical Illness. Now say after 10 years, I expire due to an unfortunate accident leading to death. My understanding is as death has occurred (due to whatsoever reason), the insurance company has to pay the SA to the nominee.

I am just trying to understand the actual picture. Under this situation, is there a possibility that the insurance company may decline the claim stating that as the death was due to accident, nothing will be paid. If that is the case, then what would be the meaning of ‘natural death’.

Kindly advise.

Sandeep-When Life Insurance will come into picture? When a person dies. So they have to give. However, accidental insurance will come into picture as an additional tool especially when death or disability. Don’t confuse both.

Hi Mr. Basavaraj,

Just to conclude, a last question which should hopefully clear all my doubts. ICICI says that for a 50L term cover, no medical is required. However, the same is required for a 1 cr. cover.

My doubt is if there is already the option for online self-declaration, is there any requirement of undergoing a separate medical from a clinic. Would the self-declared online medical suffice enough as a basis to take up claims at a later date or a separate medical is advisable?

Sandeep-The more you declare and prove your healthy status the more it will BENEIFT you and your dependents. Hence, why to worry for medical tests?

Mr.Basavaraj,

You adviced to go for ‘Stand alone PA policy’ instead of Rider, but on accident the amount recieved will be double the insured. So Why shouldnt I select PA Rider for a small additional premium ?

FYI, I have my family insured in Star Health which will help for Accidental Hospital Expenses.

Ramdas-Check the typical accidental insurance product with this rider feature. You will come to know the difference 🙂 Star health (in my view health insurance) will come into picture when a person hospitalized. But what if the person neither dies nor hospitalized but bedridden in home??

Nice article. 1. Will there be a diff in premium, if I buy online or buy from agent?

2. I’m diabetic from 4 years, can I declare it so that all illness related to it can be covered in future?

Saral-1) YES. 2) Yes, you have to declare.

Hi Basavraj

Recently I buy ICICI Pru iProtect Smart SA 50lac with premium 6925.00/- yearly, term 40 years through ICICI agent. My concern is that I told him about my medical condition that I have some BP problem and I am hepatitis B+ also and I am taking regular treatment for this. But he didn’t declare while filling it online, and also there is no medical requirements needed by ICICI Prudential. Please suggest me should I contact ICICI and told them about my medical problems, my policy is in free look period, and if I hide this medical fact after 5 year if there is any condition of claim, will ICICI Prudential reject claim by saying that insured hide the facts (however I read INSURANCE AMENDMENT AC 2015 that if a policy is in force for continuous 3 years than a Insurance company can’t deny the claim)

Your suggestion require

Thanks

Karan Giri

Karan-The biggest mistake you did is allowing him to fill the form. They do it just to close the target. Their concern is to close the sale. They not bother about the difficulties your nominee faces in case of claim. If the policy is in free-look-in period, then better to inform them at the earliest about your health issues.

Thanks for your advise, I will get in touch with company asap.

I am not going for fraud, but will you please let me know about INSURANCE AMENDMENT ACT 2015. Just want to know my right if I am paying my premium regularly

Karn-Your understanding about act is correct. But what I am saying is do the things properly and why to be in doubt.

I am an nri . Afet few years i will be obtaining usa citizenship . am i eligible to apply for this iprotect insurance

Akshay-Yes. But if your are obtaining USA citizenship after few years, then buy for that short period only.

Dear Sir,

Thanks for clearing my doubts regarding investment in private sector,

May I ask you one more thing , Is Terms Plans are really required or can go with my ongoing LIC policy ?

Mayuresh-If someone financial depending on you, then you MUST have term insurance.

Hi Basu sir,

I am 25 yrs old unmarried. I had opted for ICICI Pru iProtect smart on 29/09/2016. Below are the details of my plan:

Plan cover is Rs. 1,000,000.00

Tenure is 40 yrs.

Benefit option is Life plus

Payout option is Lump-Sum

Kindly advise if i should decrease the tenure to 30 yrs, as i had read previous comments regarding the funda behind tenure.

Thanks for sharing such a wonderful blog with us as it has helped a lot.

Thambahadur-It’s OK for you as your age is 25 years and your term ends when you are 65 years. Maximum you can reduce the tenure to 35 years.

Thanks for your prompt reply.

Dear Sir,

Iam 33 years, I never invested in private policies,so now making mind to buy this ICICI iProtect smart term plan,but bit confuse about few point as it is term plan, what after few year if company closed or plans are closed or changed what will happend to my invested premium.

Please help me out to clear my mind.

thanks

yours reader

Mayuresh-Refer my old post “What if your Insurance Company goes bankrupt?“.

Thank u so much Sir, It clears my mind.really thankful for your help.

Hello Basu Sir

I am 25 year old and planning to buy a term insurance plan . Suggest me which will be best ??

Rahul-Refer my earlier post “Top 5 Best Online Term Insurance Plans in India-2016“.

Dear Sir,

I am looking for a Term Plan for my father aged 55, I almost made my mind to buy either ICICI i Protect Plan or PNB Metlife. But recently a few guys asked me to avoid going with Private Players and go only with LIC as CLAIM SETTLEMENT is the Top Most Priority. Kindly suggest as I don’t want to delay a good decision of investing in Term Insurance or else the plan might get dropped.

Further if a situation comes that after analysis of Medical Reports and Form Disclosures The company does not want to accept the offer and doesn’t issue the policy. Will they refund me my first Premium amount.

(Note: Proposed is Tobacco User, Diabetic and Does have Cholesterol Problems, Is a Businessman with Annual Income of around Rs.3,50,000)

In light of the above kindly suggest which company’s Term Insurance Plan should I buy.

Sidharth-As your friends about the exact data of claim settlement ratio of LIC’s for term insurance products. NONE know the details. Simply airing the views. So don’t heed to such half truths. Go ahead where you feel comfort (LIC, ICICI or PNB). Yes, if proposal not accepted, then they refund the premium amount.

Dear Sir,

What is the maximum policy period for term insurance in India?

Csrao-It depends on product feature. I can’t analyze all products and point you. First choose the company and you will come to know.

hi sir, till now i don’t have any insurance, right now i would like to take two plans

1) investment plan ( max investment 30-35k PA)

2) life plan including critical medical plan

right now my age 38yrs. so pls suggest a good plan for my future

3) i would like to take a child plan too for my son in law, is it possible? if Y pls suggest a good plan and his age is 7yrs

Jagan-Never run behind these insurance plans for investment.

Pls suggest a investment plan and one for child plan

Jagan-Buy first term insurance. Secure your life first. Then based on timeframe of goal diversify your investment in debt and equity. For both debt and equity, you can choose mutual funds and start investing.

Jagan-Your comment is simple, but answer will not be. It is hard to guide your whole life financial planning on this platform.

Hello Sir,

Is medical exam required for ICICI Pru iProtect Smart. I took this policy 2 months back via online. i received welcome kit also but not receive any call or email regarding medical examination. Kindly confirm.

Bhupenddra-Whether you received policy number and policy bond? If so, then they issued it without medical examination.

Thank you so much for writing such a detailed article and I have followed you on Google plus to keep getting updates from you.

I have few questions to ask and I hope you would help me with those:

1. If my wife is a foreign citizen then can she be my nominee if I take this policy?

2. What will happen if I survive the entire term of policy without any terminal illness or death?

3. I didn’t understand the meaning of lump sum plus benefits. Lets say I die at 59 and my cover is 1 crore then how this payment will be made to my nominee along with any other benefits or they will only receive the assured amount of lump sum only.

4. On their website they are giving illustrations talking about payment for 10 years so if lump sum will be paid then what is the meaning of installments.

Thank you for your help.

Khalid-1) Yes. 2) Nothing will be payable. 3) Your nominee will receive the lum sum available in term insurance and rider benefit option in case of your sudden death. 4) It is the Income or Income-raising options, which I already explained in above post.

Thank you so much for the reply.

Hi Basu, am a 46 yr old unmarried female. Does icici pru iprotect is a suitable option for me.

Sudha-What is your requirement?

I am looking for an insurance plan that gives me coverage well into my old age. Since i may not be in a position to pay premium after my retirement, i prefer limited pay option.

I work for a private firm.i dont have any other policies except the mediclaim policy (coverage 2 lacs) provided by the employer

Sudha-If you are looking for INSURANCE, then why can’t you opt for term insurance?

Sir I am 22 year old unmarried guy.I am working in defence service,sir can you please suggest me which term insurance company should I go with.20years or 30 years which is best for me.

Abhishek-Refer my earlier post “Top 5 Best Online Term Insurance Plans in India-2016“.

Hi Basu sir,

I am planning to buy term insurance from LIC or ICICI. I dont have my permanent house , Currently iam in rent house and all all my addressproof, are in this address, My other LIC Policy is also in the rent house address. In future I might change this rent house.

Will there by any issue to get claim by my nominee, for any address issue. My same question allpies to SSA and PPF scheme

Ravi-You will not feel any claim issue due to address change. But it is always better to change address whenever you change your location.

Dear Ravi,

We are glad to know you have considered our term insurance plan iProtect Smart to protect your loved ones.

You can purchase the plan online by visiting: goo.gl/QH8lpG

Regards,

Team ICICI Pru Life

http://www.iciciprulife.com

Dear Abhishek,

We can have one of our experts contact you and address your concerns.

Please visit: goo.gl/QH8lpG and fill in your details and we will have a call back arranged for you.

Regards,

Team ICICI Pru Life

http://www.iciciprulife.com

Hi Basu,

First of all thanks for this article.

I want to buy ICICI pru smart i protect (Life option) but have few questions:

1. Whether to buy this term plan online or offline (through employee, only Rs. 200 more i need to pay for offline). Is their any commission that he will receive during claim settlement in case of my unfortunate death if i opt for offline.

2. Agent informed that the amount received by nominee in case of my unfortunate death will be tax free, Is this correct?

3. Agent informed me that once i buy the term plan they will send someone to collect the sample for medical examination. Is this the right way they are following for a insurer to get medically examined or this is just a formality they are doing, because he was even ready to accept my enrollment with medical examination and i insisted him for medical test. Can you put some light on this.

4. I have read somewhere (not able to recall) that insurer are actually covered after two year of completion of any insurance term plan i.e. if one die before the 2 year tenure of any term plan the nominee will not get anything even if they have always paid the premium on time.

When i asked about this to agent he said that in ICICI pru smart i protect, insurer will be covered within seven days after medical examination and only in case of suicide within 2 years will not be covered and rest all the cases are acceptable & after 2 years all the cases of death are considered. What is your comment on this.

Thanks,

Parbinder Rawat

Parbinder-1) It is online plan and you have to buy it online. Agents receive commission when you pay premium but he will not receive when policy arrive for death claim. If they are offering it for offline also, better to go for ONLINE.

2) YES.

3) It is correct process for ICICI.

4) Your information is completely wrong and agent’s information is partially. Your life risk starts after the policy commencement date but not after 7 days of medical examination. Suicide clause apply for 1 year but for 2 years.

Is this plan covers suicide?

Rahul-Yes, after a year of buying.

Dear Parbinder,

If you wish to buy this plan online, you can visit: goo.gl/QH8lpG and fill in your details and we will have one of our experts assist you.

Regards,

Team ICICI Pru Life

http://www.iciciprulife.com

Hi Raj,

Good evening.

I took this plan (ICICI Pru iProtect) in below format: –

50 Lacs Life cover + 50 Lacs Accidental Insurance + 10 Lacs Critical Illness cover

Please advise is this good as I took for 30 years.

Took the advise from a Certified Financial Planner – Mrinal Mohindra.

Please let me know, if I could continue in this policy.

Regards

Hari

Hari-If you already took it then what is your doubt? In my view combining life insurance with accidental and critical illness insurance is bad thing. Also, you mean to say that you opted offline plan?

Hi Raj,

Thanks for your response. As per advice of agent I have considered taking below in format given above. I paid a premium of INR 12,500. My doubt is whether taking this policy for 30 years is good or should I shift to another term insurance plan given by other firms (HDFC or LIC) next year.

Hari-Restrict your term of policy to your retirement age.

Dear sir, kind regards.i need your help, and below is my plan details,

Product Name : ICICI PRU IPROTECT SMART

Sum Assured/Modal Income (in INR) : 10000000

Premium Payment Term(in Yrs) : 20

Policy Term (in yrs) : 25

my question is,

1) if i survive more than the policy term of 25 years, what maturity amount i will get

Nandakumar-It is pure term life insurance plan. There will not be any maturity value.

Dear Sir, I am Mangesh , working in Kuwait, started my LIC policies immediately after my marriage (since 2008, INR 6284/month, 5 nos. policies for me n my wife, since 2012 for 1st daughter, 4 nos. of policies – INR 35000 annually, since 2014, 3 nos. of policies, for second daughter 34000 annually). Now I came to know that these can not be investment not insurance all together, hence I have closed all policies in last 3 – 4 months and bought HDFC term insurance of 50 Lakhs. Surrender value is very nominal compared to what i paid to them.

What will you suggest, could you please tell me any other option to minimize this loss?

your help in this is highly appreciated, sir.

Mangesh-If you already closed the plans, then why you are worrying now?

Hello Basu,

Thanks for the nice blog post on “Term Insurance”.

Other then the queries in comments, I would like to ask on “Death Benefit”(DB).

What is the definition of DB here?

Does it means

– Accidental Death

– Death by any Health problem

– Death by Natural Calamities like Flood, Earthquake

Budh-Here DB stands for all the death reasons you mentioned.

Dear Sir,

My name is Vijay Karun. I am looking for the health plan. I have already LIC life insurance plan of 8 Lakh and 2 Lakhs of PLI. Should have I take this ICICI I protect smart term life insurance or I have to go for the pure health plan.

if I go for the ICICI term plan, how is the claim settlement ratio. Please help me to get out of this confusion. or if possible please guide me on the other best health plan.

Vijay-Never combine health and life insurance. Buy pure term insurance. If you are comfortable with ICICI, then go ahead.

Dear Mr. Vijay,

Thank you for your interest in ICICI Pru iProtect Smart. Please fill your details in this link and we will have one of our experts call and assist you with the plan: goo.gl/j26BOj

Regards,

ICICI Prudential Life Insurance

Hi Basu,

I am 36 yrs old. Family has good Cardiac History (2 generations affected by cardio attack and Diabetic)

As per your previous discussion, I have taken personal accidental insurance for 1 cr(New India Insurance) and term insurance for 1 cr(ICICI).

Now I want to take pure critical illness insurance. What is the best company?

Please guide me.

Thanks in advance.

Narender

Narender-Personally I am not fond of critical illness. Because there are many restrictions to it and complicated product. However, you can check with few public sector companies.

I compared some and found that this CI rider here somewhat covers 34 CI which is comparatively more than the other players and thinking to go with it. Have one clarification.. If is have opted for a 20L CI..Is this only one time claimable ? i.e. In the first CI requirement, say only 5L is required and claimed, then i have a requirement for another 10L after 4 yrs, are they claimable or it closes in the first claim itslef ?

Hello Basu, any advice on this take ?

Rajesh-You can take plain product without any additional features or riders.

Rajes-Refer the product Boucher fully. Because I am not fan of combining insurance with investment.

How can I get insurance & health indutance in a one plan . I have already invest 18000p/anum in insurance and 8300 in mediclaim …. and 2000 p/m in sip can i get any thing better than that

Amod-It is not possible as per recent IRDA regulation. Refer my latest post on the same “Health Insurance Regulations 2016 – 5 changes you must know“.

Hi Basavaraj,

This was an interesting read. Need your advice on my situation. I am a software professional 35 years old. Married and have a 2 year old girl. I have two term policies

1. LIC Amulya Jeevan – 50 Lakhs – Started Feb 2011 – Term 35 years – Yearly premium – 19,400 – Medical check up done

2. ICICI Pru iCare – DB – 1CR , Accedental DB – 50 Lakhs. Start Date – Nov 2012 – Term 30 Years – Yearly premium – 16,800 – No medical check up was required

On the investment front I am purely dependent on PPF and NPS also EPF. What would be your suggestion on the

1. Taking any additional policy for death cover? Any recommendation? – ICICI iProtect smart

2. Any suggestion on investment avenues?

Regards,

Kumar

Kumar-1) Your further insurance requirement depends on your income and financial liabilities. Ideally you may calculate like 15-20 times of your yearly income as the insurance coverage.

2) Investments guidance can’t be made over comments. Also, I don’t know much about your financial goals, then it is hard for me to guide and dangerous for you to follow on my such recommendation.

I just came across your blog few days back and after going through it, I found it informative and unbiased. Would like to have your advice:

I’m a 40 Yr old Non Smoker healthy male with two kids. I want to protect my family in event of my death, i.e., If I die suddenly, they get regular monthly income (since they are not literate enough) until death of my spouse. Can you suggest me any product? Any help would be highly appreciated. Thanks

Rajat-Don’t rely on such products. Instead buy a term insurance which pay the lump sum. Educate your spouse of how to use it in your absence. They can buy immediate annuity plans to get such cash flow for life long.

Ok, I’ve seen you applaud LIC term insurance a lot despite the fact that they are costly. What is so special about LIC Terms insurance? while there are many other providers offering same coverage at significant lesser premium? Can you honesty advice about a Term insurance product available in the market. I’d like to go through complete health checkup to avoid any risk in case of claim. Thanks in advance…

Rajat-The simple answer is there in your comment itself. LIC not at all ready to issue a single policy where they found health issues and all, but the same is not with others. Private players are aggressive in building their business. For your information, I am neither supporting LIC nor against it. It is purely your call. But I safely go with existing players than aggressive new entrant. Rest is left with you to decide 🙂

Hi Basvaraj,

I was doing some research for a Term plan and thanks to you that now i am clear about going for a Pure term plan.

But, i still require a suggestion on the company, i was suggested by a friend that i should go for 2 Term plans out of which one should be LIC which is little expensive but does all the checks and another with something cheaper like Max life which also has a good claim settlement ration. With LIC clearing my claim in case of death, there will be no option left with Max life to deny.

Also, while choosing a brand which is not Indian, do we have to take any cautions or it’s all covered by IRDAI?

Regards

Sandip

Sandip-On which world there was rule that if LIC accept the claim then other insurer or Max Life must accept it? There is no logic in splitting. Go either with LIC or the private insurer. Including LIC all are equal under law of insurance. So you no need to worry.

Thanks Basavaraj.

I also read some articles on Google+, very hepful. All the best to you.

For term Insurance, simple pain ones with no add ons, I am confused between ICICI, HDFC or LIC. My relative is the India head of Aviva Life Insurance and he has suggested to go for LIC irrespective of it might by charging 7k to 8k higher

Sidharth-Then go ahead with LIC.

Sir I have family history of cancer, hypertension, diabetes. I am 30 yrs male, annual income 8lakhs, married, no kids yet. I want to take 1cr life plus 30lakh Critical illness rider for 30yrs term. I have checked best separate Critical illness mediclaim is Religare Assure which gives maximum 20lakh with increasing premium every 5 yr and in 20 yrs the cumulative premium is 5lakh approx. Where as in icici I am getting 30lakh CI for 30yrs at 3 lakh(10000*30) cumulative. Shud I go for it?

Anubrata-Don’t combine Life Insurance with Critical Illness insurance.

I have a separate simple term plan of 1 crore. I shall keep that. I want to go for this CI rider because it is much cheaper than other CI mediclaim. For 30 lakh cover for 30 yrs I have to give 3 lakh cumulative whereas the best possible CI mediclaim which is giving max 20lakh cover for 20 yrs costing me 5lakh. I am a doctor. I have read both policy wordings. Is there any reason why you are suggesting not to go for it? What problem may happen?

Anubrata-Check properly about standalone critical illness policy features to the rider option of this plan. Don’t rely only on premium. You notice the difference.

I think ICICI pay entire CI benefit but they will reduce your Sum Assured by CI Benefit amount. Lets say, you have Rs.1 Crore Term Plan with 30L CI Rider. If you are diagnosed with CI then they will pay you 30L lump sum amount but your Sum Assured will be reduced to 70L instead of 1 Crore. You are paying extra amount for CI Benefit but it effects the Sum Assured.

If you take CI Policy separately, then you will get 20L on diagnosed and Term Plan will continue with Rs.1 Crore.

That might be the reason, CFPs recommend Pure Term Plan.

Sanjay-Yes, rightly pointed.

sir I m 30 year old,unmarried… I want to take icici eterm plan…but I have one confusion….. as m not married, so I can’t make nominee to my wife/child…if I make my mother as nominee,will it not be hectic for my to be wife to claim,in case my mother n I pass away unfortunately???

Ram-You can change nomination at any point of time. It is not a big deal.

thanks a lot sir for clearing my doubt…

one more doubt sir…I HV taken lic jeevan anand already because I was trapped in agent’s luring ,and have paid 3 premiums of 30000 each.

can I surrender this???

will it be worthy to close as I have paid 90000 already???

please clear sir…

can u also tell around how much will be surrender value???

Ram-Continue LIC Jeevan Anand if you feel 5% to 6% return is fine for you. Otherwise, strictly think of coming out of this plan at the earliest.

The policy is not available to NRIs. The ICICI people wrote to me when I inquired and confirmed that.

Sanjay-Thanks for your updates.

I think this information is wrong and bit confused now

..I had wrote to their email id @[email protected] whether it is available for NRI..Today they have replied and it is attached here for ur reference. So pls advice me , 1)can I go forward icici with this? or

2)Should i got with Max that having same parameters what i believe like Icici but they clearly specifies ‘Online term plus ‘ plan for NRI too on their website.

3) I like to opt Pure term plan with out riders.

I heartily appreciate you Sir for Writing articles like this.

below i sharing Icici team reply.

”

ICICI Prudential Life Insurance Co. Ltd

8:30 AM (26 minutes ago)

to me

Dear Sir,

Greetings for the day!!!

We refer to your email dated 23/04/2018.

We would like to inform you that you can apply for Term plans as NRI (Non Resident India n ) post fulfilling the below mentioned requirements:-

1. To apply for the plan you must have the residential proof of India n address.

2. The product is also available Non Resident India n s however the payment would be accepted in INR only.

3. You must be in India while buying a policy.

4. You can buy the plan mentioning your Permanent India n Residential Address.

5. While applying for the policy you have to fill the NRI questionnaire

Passport copy is mandatory to be submitted

Further, we request you to kindly revert us with contact number so that our sales team will contact you.

Thank you for giving us the opportunity to serve you.

Yours Sincerely,

Navin Sinha

Customer Service Team

ICICI Prudential Life Insurance Co. Ltd.

———————————————————-“

Albin-Then why not go ahead?

If I buy a term insurance for 50 lakh with critical illness rider of 5 lakh. & used critical illness once. Then after some years natural death occurred then what will be the benefit for nominee.

Sunita-Nominee receive the sum assured opted under the term insurance plan.

Hi Basu,

This is a nice informative website. I am planning to buy 50L ICICI iProtect term plan. I chew PAN 3-4 a day for last 10 years. Do I need to buy the term plan as a tobacco user ? Do I need medical test before buying term plan.

Sekhar-Better to inform. Yes, insurance companies insist you to undergo medical test before issuing a policy.

The premium amount is same as non-tobacco user upto 49L in ICICI iProtect plan.

In order to save some premium amount, Should I buy two term plans from ICICI of 49L each from ICICI iProtect .

Please advise.

Sekhar-You can, if you manage multiple issues.

Sir,

I want to do term insurance with accidental and terminal illness benefit for my mother 53 yrs old.

She is a housewife.

Will insurance provider give term insurance?

Should i go for icici- iprotect SMART?

Manojit-If she don’t have income of her own, then no company will provide her insurance. Also, think twice of whether term insurance really required to her?

Sir,

Myself Ganesh and i want 1 crore life insurance policy which one is better , plz suggest me

Ganesh-They are listed in my old post “Top 5 Best Online Term Insurance Plans in India-2016“.

Thanks Basavaraj Tonagatti Ji for your kind & eyeopener suggestions regarding term plan.

On the same line i want to know how to choose a Health Insurance Policy ??

In your opinion what are the best policies available in the market ???

Kislay-I recently wrote a post on how to chose a health insurance plan. Please go through it “Best Health Insurance Company in India-Based on IRDA 2014-15 Incurred Ratio“.

Hi Sir,

I got flash adv during login on to ICICI bank, that was no medical upto 49.90 lakh.

While contact on ICICI bank, JMC House, Ahmedabda, their representative told that depending on underwriter about after providing the details. So is it fair or have you any suggestion.

I have plane for 50 lakh, also what will be better as per your personal.

Amitkumar-Don’t buy a term plan WITHOUT MEDICAL. It creates lot of opportunity for insurance company to reject the claim.

What should be the ideal max term year for this policy.

If i am 38 now ,how much term year should i opt for.

Agent suggest to go for the maximum term.

Also,Say if i retire at early age can my children continue to pay the premium for this policy to get the benefits.

Sachin-Ideal term must be up to your working age. Insurance is not required during your retirement.

I have been insured with a term insurance as suggested.

My Wife is a house wife ,should she have a term insurance too ?

If yes, what should be the sum assured and the tenure.

Regards

Sachin

Sachin-If she is not earning, then no insurance company will offer term insurance to her.

Thank you

Dear Sir,

It is an eye opening for me. Thanks for sharing the information

I would like go for Single premium with Rs.1.5 crore with lump sum. it is advisable to for single premium ?. And also after policy term of 20 years , by gods grace if i am surviving then can i change to Increase income ?

Thanks

Raja

Raja-It’s your wish or comfort to choose the premium paying option. I can’t say anything on that. But I feel it is best to opt for regular premium. You can’t increase either in middle or at end.

There is no Maturity or Survival benefit. ? If I am alive after the policy term I will not be getting the lump sum amount ?

Hi Basu, I took ICICI PRU I care 2 option 1 for 1.5 cr last year and the premium is due next month. The premium amount is Rs. 22,000 (inclusive of taxes). No riders was opted. Now this new policy from ICICI shows a premium of 17,000 for 1.5 lac for same tenure of 30 months. Is it advisable to discontinue the first one and go for this one without any riders.

I asked the insurance official to mandatory do the medicals last time, as I got a murmur (which is purely functional) and they did tests in 2 different hospitals, confirmed and offered the first policy.

Sarin-Better to stick to your old one. But if there is a difference of Rs.5,000, then think seriously. However, don’t cancel the first one without the issue of second one. Chaning frequently due to new offerings is not good.

Thanks Basu

Can u pls advise ..which term insurance is better hdfc i protect with disability rider or icici i protect smart with critical illness rider ..i am 34 year old and want term insurance..want 1 crore sum assured

Shikha-Buy either HDFC or ICICI but without riders.

What is the meaning of the follwing tersm in the Policy Term benfit options ” Regular Pay / Limited Pay / Single Pay “

Sachin-Regular pay means you pay the premium throughout the policy period. Limited pay means let us say the term of policy is 15 years, but you can chose to pay up to 10 years only. But policy period will be up to 15 years. Single pay means, instead of paying it on yearly, half yearly or quarterly basis, you pay the premium at once at the start. Policy will continue as you opted. No headache of paying the premiums year on year.

Hi,

Thanks a lot for this review..i was looking for one.

Being an NRI ,am i eligible to join this plan? Whether my physical presence in India is needed for the activation ?

please advise.

Vishnu-They have not mentioned anything special about NRI eligibility. Therefore, I suggest to contact ICICI directly. Yes, your physical presence is required as you have to undergo medical test and KYC process.

Hi Basavaraj,

I am interested to buy this plan, but have one confusion.

hope it get clear here……

That’s, in case of successfully completion of this policy term (let say 30 year) and i am still alive.

Now what i will get in end……?

Mohit-NOTHING. Because it is a TERM INSURANCE PLAN.

my annual gross income is 6.84 lakh and my annual net payable income is 5.28 lakh….plus i have outstanding house loan of 10.6 l…now my question is what should be, my sum assured for term 30 years. my age is 31 years…thank you

Anil-You can calculate on your own by visiting ICICI Portal.

thank you for your reply..but in that calculator it ask for annual income..annual income should be gross annual income or take home annual income???

Anil-Better to mention total income.

Hi Basu,

Thanks a ton for this review. Really appreciate it.

Regards,

Sreehari

Sreehari-Pleasure 🙂

Hi Basavaraj,

Really nice write up with all details and comparison.

I have a monthly income (take home) of 70,000/- rupees and I wish to take a cover for 1 CR. I felt LIC plan is bit costly with a premium of Rs.17000/- per year with no riders.

. I somehow liked ICIC iProtect smart which gives 1 CR cover + waiver of premium for PD & Rs, 20 lakhs critical illness rider for a yearly premium of Rs.17500/-

Do you think this is a good move to go ahead with mixed options which gives cover + riders?

PLease help.

Thanks,

Vivek

Vivek-In my view select plain LIFE PLAN.

Okay, thanks. Can you suggest me please best options for standalone plans separately for CI and accident policy?

Vivek-You can check my post “Best Accidental Insurance Policy in India-How to choose them?“. Regarding CI, better you opt only in case you have family history of CI.

Why only in case of family history?

Also, heart attacks are very common. It mentions heart attack. Are there very specific clauses to it?

Dear Amit,

The diseases definition mentioned in Critical Illness Insurance are just generic and hence more probability to reject. I personally not suggest.

Dear basavraj,

I wish you a very happy new year…

I am 23 years old and was trying to educate myself on investment and insurance. I found your blog very useful and informative.

In this blog You have preferred a standalone pure term plan and a seperate accidental insurance plan, but my doubt is when I chose life plus plan of pru life I am covered for both natural death/terminal illness and accidental insurance also. Then why go for a separate accidental insurance….?!

Please suggest. Thank you

Aditya-In Life plus plan, they provide you benefit only when the death due to accident. But if the person be bedridden due to accident?

but the “term plan” actually has death cover for death caused by any means like natural or accident, right ?

thank you.

Aditya-Yes. But when you buy accidental riders, then you will receive additional amount equal to accidental rider amount you opted (apart from sum assured).

Thank you basavaraj.

Just what I was looking for! Thanks a lot Basu, your article cleared many of my doubts.

Sanjay-Pleasure 🙂

Very Informative , thanks for sharing .

Could you get chance to review and comment on PNB Metlife “Mera Term Plan”.

I am considering the option in that where they payout lumpsum + monthly income with 12% increase every year .

I have to choose from HDFC , ICICI and PNB Metlife for 1 to 1.5 Cr .

Any advice will be helpful.

Thanks

Numchar-No need to review. It is just a regular term plan with some payout options differently and also joint life option. Buy pure term plan.

brilliant artcle Sir, as per the need of hour. Can you please list some more term insurance plan with disability and critical illness riders available in the market and compare them. Regards.

Abhishek-Don’t go with term insurance which offers riders. Buy the plain one. Purchase critical and accidental insurance separately from general insurance companies.

Thanks a ton Mr Basavaraj…Even I am having similar line of thought as yours of not mixing term insurance and critical illness. You article has clear my doubts.

I have taken LIC eterm of 1 cr each for myself and my wife. Yes it is costly but peace of mind negates that.

Also would like to thank you for such a great blog.

Have learned a lot from this blog.

Regards

Gaurav

Gaurav-Pleasure to know your leap 🙂

Thanks for the information…..Can you please suggest list of insurance companies offering standalone critical illness policy.

Vikas-All general insurance companies offer critical illness policies. Please check the individual companies.

Thank you for the information….Very informative blog.

In ICICI pru, what is the difference between death benefit / Terminal illness benefit and Accidental death benefit of1.00 crore,

Does Accidental benefit cover under Death benefit ?

Shalem-Death Benefit-Death due to natural or accidental causes. Terminal Illness Benefit-Explained above. Accidental death benefit-Death due to ACCIDENT ONLY. Yes, accidental death benefit cover under death benefit.

So that means Life option covers both natural death or death due to accident? Then why do we go for Life-plus option which include accidental death benefit?

Vasanth-In life option, death due to natural and accidental both are covered and nominee receive the sum assured ONLY. In case of Life Plus Option, in case of accidental death, nominee will receive SA+Accidental Rider Amount. That is the difference.

Satshri akal sir ..I’m ramnik from punjab..sir I was working in private engineering college . I worked for 6 months and left the job bcz I got govt. Job.my EPF was deducted for 6 months. Now what is the procedure to get that. It left job in Dec. 2006 .thanks

Ramnik-You can transfer it to current EPF. But use the right platform to raise your doubts. If unsure of where to ask, then use our Forum.

Thank you for the information….Very informative blog.

However i am still confused about Standalone Accidental Insurance Plan and Standalone Critical Illness Insurance Plan.

Could you please give some advise about these plans??? Which are the options available with ranking??

Loyit-You can check about Critical Illness from the respective general insurance company portals. Regarding Accidental Insurance, I already wrote a post on this. Please go through it “Best Accidental Insurance Policy in India-How to choose them?“.

Hai Basavaraj Sir, Good evening.

Am interest to buy ICICI Pru iProtect Smart scheme. If I buy online on monthly basis any medical test are there.

My age is 33

Dear Dileep,

Whether you pay it on monthly or yearly, you have to undergo the medical examination.

Thank you for the information

I want to go for Term insurance policy soon.

Was looking at various insurance options and came across this article.

Is this one of the best term insurance policy available in market at present.

What about LIC term insurance policy in comparison with this ?

Could you suggest which are good

1.Standalone critical illness insurance

2.Standalone accidental insurance

Thank you

Sachin-If you want to buy this product, then simply opt for plain term insurance (without any riders and payout benefit options). I am not saying it as a best. But at the same time, compare the premium and if you are comfort with insurance company, then definitely go ahead. LIC’s term insurance is currently the costliest online term insurance. However, if you have inclination towards LIC, then go ahead.

1) and 2) There are may in market. Check with general insurer and you requirement.

As I understand a person should have following three policy to safe guard in future :

1. Term Insurance

2. Critical Illness Insurance

3. Accidental Insurance.

Would you suggest or provide any link to your article if you have already written on Best available plans for item 2 and 3.

What amount you suggest in each category or distribution of premium in each category ,is there any rule or calculator for the same.

Thank you in advance for your usual advise .

Sachin-I wrote a post about accidental insurance selection. You can read it at “Best Accidental Insurance Policy in India-How to choose them?“. Regarding critical illness, it is exhaustive list and one can’t say easily which one is best. You have to opt based on your family history and so many clauses. For accidental insurance, my suggestion should be around 10 times of your yearly income. For critical illness, it depends on the illness they cover and the current expenses of such diseases. Rather than distribution of premium, concentrate on how much and which cover you need.

Well understood.

Thank you