There are around 24 Life Insurance Companies in India. All of these companies offer the term insurance product. How to shortlist the “Best Online Term Insurance Plans”?

Note-I published the list of best online term insurance plans in India for 2017 at “Top 5 Best Online Term Insurance Plans in India in 2017“.

Last year I wrote a post of “Best online Term Insurance Plans in India for 2015-A comparative list“. In this post, I concentrated mainly on Claim Settlement Ratio of IRDA for 2014-15. However, from now onward, I do not think the Claim Settlement Ratio is a most important and sole criteria in choosing your term insurance. Reason is, recently IRDA amended the Section 45 of insurance act. According to this, if the policy continued for 3 years or more, then insurance companies cannot reject the claim.

Note-I updated the claim settlement ratio of IRDA for 2014-15 in below post.

IRDA Claim Settlement Ratio 2014-15-Which is best Life Insurance Company?

This is a big turning event in the insurance industry. I explained in detail about this change in my earlier post at “Term Insurance-Claim Settlement Ratio no more a big criteria“.

So now how to choose the “Best Online Term Insurance”? It is pretty simple. No complication at all. Below I will share you how to short list.

1) How old is your insurance company?

Life Insurance is a long-term contract (especially term insurance). Hence, I will select the insurance company, which has been in this industry for more than 10 years. Why 10 years only? I feel comfortable with this number. Because privatization in insurance industry was done in the year of 2000. It means almost 15 years back. Hence, I look for a company which is at least 10 years old. I may be biased. However, this gives me some confidence on insurance company’s business existence.

I agree that we can’t predict the future. However, at the same time, we must look at history to predict our future. Here is the list of all insurance companies and how old they are.

Note-There may be an error of margin of around a year. Because some companies mentioned the IRDA approval as their start and some the actual start year.

From this activity, we noticed that around 12 companies are more than 10 years old. The rest of them are either 10 years or less than 10 years. Therefore, even though these new companies may be offering “Best Online Term Insurance” plans, but for my safety, I will stick to old companies.

2) Claim Settlement Ratio–

As I said above, claim settlement ratio is not a big priority now for the selection of insurance. However, it will give me an indication of how the company is aggressive about claim settlement. However, I again warn you that this is a raw data. It will not differentiate the claims based on products. You will not see how the LIC or some other companies settled endowment plans, term insurance plans, or ULIPs. However, you may feel some comfort and a tool to judge the insurance company. But not a sole criterion to judge. Below is the claim settlement ratio of all life insurance companies for the year 2014-15. I wrote a detailed post on the same at “IRDA Claim Settlement Ratio 2014-15-Which is best Life Insurance Company?“.

You notice from the above data that the companies which have more than 90% claim settlement ratio are around 9. I highlighted them with green. However, I highlighted Star Union Life with red even though it’s claim settlement ratio is showing at an impressive 94 %. Because it was a 7-year-old company. Hence, I feel a bit uncomfortable to go with.

Now we shortlisted the seven companies.

3) Cost of Term Insurance–

Now we have to list down all these seven companies premium rates to arrive at cheapest and affordable. Here is the list of premium calculated.

You noticed that LIC is the costliest one among all. At the same time, Kotak is offering the lowest premium. However, do remember that the above premiums may change based on your health condition or some other factors.

Note-I considered typical pure term plans. I have not considered any riders, benefit payout options or so.

- I considered typical pure term plans. I have not considered any riders, benefit payout options or so.

- The term I selected is 30 years. However, I suggest you to consider the time of insurance up to your working life. Life Insurance is not required during retirement.

- Never buy combo products, which offer riders or some death benefit payout options.

- Each of these facilities is not offered to you freely. They charge it for such offers. Hence, buy it only when you feel the features suit you.

- Buy accidental insurance separately from general insurance companies.

- Buy critical illness insurance separately from general insurance companies only if you have a family history of such diseases.

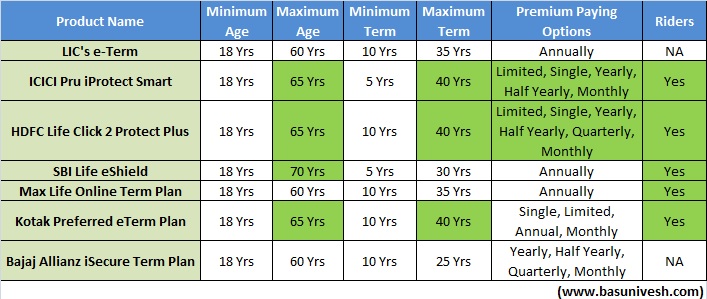

4) Plan features–

Let us go further and try to shortlist the plan which suits you. This time, we will look into the term of the plan. The minimum term and maximum term.

Finally, you notice that some of the best options like maximum age, maximum term and premium paying flexibility features are with ICICI Pru iProtect Smart, HDFC Life Click 2 Protect Plus, Kotak Preferred eTerm Plan and SBI Life eShield.

Please note that I am not against LIC or other companies. However, considering choices, features, flexibility, premium budget, and reliability, I chose below 5 term insurance plans as my choices of “Best Online Term Insurance”.

- LIC eTerm-Costliest but to those who feel that LIC is Government backed and safe.

- ICICI Pru iProtect Smart-Best with competitive price and features.

- HDFC Life Click 2 Protect Plus-Third Choice.

- Kotak Preferred eTerm Plan-Fourth Choice.

- SBI Life eShield-Final Choice.

You may feel biased. However, considering the factors, I feel these are “Best Online Term Insurance” plans to go. At the same time, I am not stating that my method of choosing is BEST. However, I tried my best to shortlist the products. Others may have a different opinion. Hence, chose the one which you personally feel comfort.

Note-We are not associated with any Life Insurance Companies to promote their products. There are no monetary benefits from any of the life insurance companies. It is purely an initiative to promote term insurance and make the process of choosing simple.

Hi Basu,

Have you written any article on the same for 2017 ?? like, “Top 5 Best Online Term Insurance Plans in India for 2017”

I am going to start term insurance. So can I follow this same post or wait for your 2017 analyze ?

Avik-Refer the same at “Top 5 Best Online Term Insurance Plans in India in 2017“.

sir

pure term insurance did not cover death due to accident . Is it cover death due to health problem like heart attack. Should not we go with accidental cover instead of term insurncae as their is more risk of accidental death .

Maninder-Who said that death due to accident not covered in term insurance?

Sir, I check various term insurance plans ,their are various options like “accidental death benefit rider” , i think i understand it wrongly. If term insurance covers accidental death then accidental cover is for cover disabilities due to accident ?

If i am wrong then please tell ( in short) what should we target to cover in term insurance plan( as u say pure term insurance) and accidental insurance.

thanks

one other query – is term insurnaces covers death due to health problem like heart attack.

Maninder-A typical normal term life insurance also covers the death due to the accident. However, by buying an accidental rider, you will get more benefits in case of death or disability (which you can easily buy it from general insurer than clubbing with life insurance). Yes, death due to heart attack is covered in term insurance if there were no such health complication during buying or insurer aware of the risk while issuing the policy. Death due to diseases at later stage due to any health reasons is very much covered in term insurance.

Dear Basu,

I always like your analysis and advise (nice graphical way of plotting data which helps arrive at a perspective quickly).

I Need your advice. I am currently subscribed to ICICI prulife Pure Protect – Elite from 2012 Jan. It is expensive compared to other policies in the market and ICICI seems to have ismart now which seems to have more RoI now.

Please help me with your expert advice on the following:

1. Is there any advantage on the length of subscription to a policy?

2. Do insurance companies provide a way to switch from one plan to other like insurance portability?

Looking forward,

Regards,

Venkata

Venkata-1) It seems offline term insurance. Hence, it is costly. Hence, better you check online alternatives. Once you got the new policy, then you go for cancellation of the existing one.

2) NO.

Hi

I just wanted to know if there is any effect of GST bill on term insurance. I mean if GST bill is implemented, then will there be any reduction in premium.

Srinivas-Let them implement the bill.

Sir, I want to do LIC e-Term policy. I rarely smoke .. i think 10 times during last year. Last time i smoke about 20 days ago. Now, If I apply for Non-smoker category and after medical test if I fail smoking test– What will happen?? Will they refund me the amount I paid or increase the premium to aggregate category?

Saurav-If they consider you in smoking category, then either they reject the proposal or hike the premium (even reduce the sum assured you proposed). If you not accept their proposal, then you have rights to reject it. Once you disagree, then they return the premium by deducting the medical examination cost and the tax on your premium.

Hello Sir,

If applicant dies after making online payment of premium & Medical examination is done but before policy paper gets issued & policy comes in force to applicant then premium paid will be refunded back to nominee on claim or not?

I checked this with Max Life Insurance & I have been informed by their call center executive that in such case premium will not be refunded back to nominee if applicant dies before policy issued.. Even he stressed that no other insurance company will refund back premium paid in such case & I can check with any Insurance provided !!

It was very surprising to know.. Please advice what is IRDA guidelines in this regard!!

Sachin-If policy is not issued and premium is accepted, then death occurs means they have to return the premium. If they NOT, then it meant that they accepted the proposal and they have to pay the SUM ASSURED. Don’t rely on these call center guys. Visit their branch and check personally.

Thnx for ur reply …

I also felt the same, but one never know about hidden T&C of these companies & when incident occurs, then you have no choice without accepting if it is mentioned so !!

I was about to finalize Max Life Term Plan, but now I am bit apprehensive about my decision. It becomes tough when you come across such incidents.

Kindly advice shall I go for Max Life or go for my next shortlisted options ( Kotak & ICICI ) ??

Sachin-If you are so apprehensive that accident may happen during this exluding period, then avoid it 🙂 Brother, please be positive. If you feel that it is a biggest negativity of that feature. Then simply switch to other insurer.

Hi Basavaraj,

Does LIC’s Amulya Jeevan cover death by accident?

Does LIC’s Term Assurance Rider- cover death by accident?

HDFC Click2protect Plus has an “Extra Life Option” which covers death by accident; doubles your SA- and your Premium on it increases by 3K Mark roughly. And would you call this as a Rider?

I still would want to add on a Personal Accident Rider from GI companies after shortlisting- as I digged a little to find out why you stress on Riders from GI Co’s and I understood its mainly due to variations in coverage. Thanks for that.

Karan-Yes Amulya Jeevan and Term Assurance Rider covers death. HDFC’s option is accidental rider.

Thanks Basu. So what I understand is that LIC Amulya Jeevan covers Death- Both natural and Accidental. Am I Right?

Karan-Not only LIC Amulya Jeevan but all insurers covers whether the death is natural or accidental. But only when you opt for rider, the rider benefit in case of accidental death will be added to claim amount.

Hello Sir,

I have Jeevan Anand and Whole Life Policy Limited Period each of Rs 5 Lac sum assured for 21 yrs premium paying term. i have paid 6 premium till date.

would like to know is it good to surrender and buy 1 term insurance as for above 2 policy my premium is Rs 42K. where as for same premium amount i will get Rs 2 Cr cover.

Also suggest me should i go for Surrender and take money back or keep it for paid up capital value.

thanks,

arun

Arun-Go ahead for surrender.

Hi,

I have processed term insurance with Max Life Insurance. I checked the above comparison and found that Max is fulfilling all the above criteria but still its not in your top 5 list. Any specific reason for not including it?

Abhishek-Check earlier comments. I already replied the same.

Dear friend, i already have (30 lac) term insurance i Aviva i life. now i want to take additionally 20 lac term plan for other Insurance company. is it possible. give me a suggestion.

Gnanasekaran-Why can’t you buy with same insurer?

Hi sir

I have taken home loan from hdfc.. Is it advisable to take insurance from hdfc.??

I needed to understand your opinion or concerns if any..

Regards

Kishan

Kishan-You are free to buy term insurance (to cover the debt) from any insurer of your choice.

WHY PREMIUM OF LIC IS HIGHER THAN OTHERS ???

Smit-It depends on the LIC’s actuaries price calculation. None can understand why it is at high.

sir , i am thinking in between icici/ lic/ pnb met life.

A) should i go for the riders or should i take individual policies for accidental or health

b) its very difficult to understand difference between terminal illness and critical illness

C ) main advantage in case of number of claims in lic 75k while incase of icici it is 8k. whats the reason other than gvt / pvt sector ? while in LIC riders are not included

Mandar-A) Don’t go for riders. B) Even for me too 🙂 C) It depends on mortality table they arrive at premium and also the profitability or other factors.

Basavaraj Sir,

As per my understanding, Terminal illness is a disease that cannot be cured or adequately treated and that is reasonably expected to result in the death of the patient within a short period of time. I think Insurance companies usually consider this time as 6 months. Entire Life Insurance Sum Assured will be paid in case of Terminal illness even before death.

Whereas a person with critical illness has a chance to survive and as it is available as rider/stand-alone policy, upon detection of critical illness, the lump-sum amount that is being paid can be used for the treatment and the person can get back his life.

BTW, rider in ICICI Term Plan is tricky. Kindly, avoid it.

Raghav-I know the definitions, but what I pointed is so many medical terminologies and rules make you to forget of claiming it.

Dear sir,

Let me know cheapest premium for term insurance for 1cr.

Age-46 yrs,male,20 yrs tenure.

If i take insurance today &died in two days,can my nominee gets full amount.

Sanjay-Visit the respective insurer portal and enter your data to get the premium rates. I can’t do for you by visiting all 44 insurer’s portals.

Sanjay … I was trying to do the same. The cheaper with good settlement ratio i could find were Max life and Tata. There are more cheaper u can try but i didnt selected them for xyz reasons.

I ultimately bought pnbmetlife due to spouse coverage.

Hi…Got a query regarding Term Insurance Plan- Nominee/Guardianship eligibility.

a) Wanted to check if the possible option can be selected while providing the nominee towards a term insurance, in the case of the nominee being a blood relative (Minor), can the guardian for the nominee be named as a Non-Blood relative /Non-family member? Any insights?

b) Some of the insurance companies like Max life insists that the guardian has to be a blood relative.

In such scenarios, where such an option cannot be provided, what is the alternative?

c)In case of incidents resulting in settlement of the insurance amount,

the minor will need to wait till he/she turns major?

TIA

Ramya-a) Even though nowhere it is written that appointee or guardian must be within a blood relation, but for their safety insurance companies may insist the appointee be within blood relation. Because nomination and appointee must always be within blood relation.

b) Yes, they are right. It is hard to say or strange that no blood relatives are there to appoint as guardian.

c) No, the appointee will receive the claim immediately after the death of insured. You have to create a will for instructing about the process of using insured claim amount until the nominee turn major.

Hi Vasavraj,

I am planning to take a term insurance plan with 1 CR cover. Could you please help me to decide from the below list-

Aegon Religare

Max Life Insurance

Kotak Life

Thanks

Bhaskar

Bhaskar-Please refer above post.

Hi,

I would like to take TATA AIA iSuraksha Supreme plan for 40 years tenure. My age is now 35 years old and premium is around 13K. Is my choice is correct?.

Vijay-If you are comfortable with premium and features of a product, then go ahead.

Basu , does any of the the above top 5 cover till the age of 80 years. It seems only ones like Tata AIA does and also AIA seems to have 96+ claim ratio success rate (as per thier website). I was thinking for one ICICI and Max life of 1 CR each. But seeing this AIA coverage till 80 yrs, I am thinking to take this also. Please advise, I am an NRI and 39 years of age and can manage upto 3 Cr term coverage.

Nadeem-Do you work up to 80 years of age? I think no, then why you need life cover post-retirement?

But wont my family get benefits in case of mishappening even between 75 to 80 years.

One more query please – I came to know that PNB gives option to include non working wife also in a term plan for husband. Please share your view if its good idea to go for it? Else my wife will not get any term plan until she is working.

If its something useful, is there any other term plan in market which offer similar options?

Hi basvaraj,

Finally, I have takrn pnb metlife as it has spouse coverage. Thnx for ur guidance .

Nadeem-Pleasure 🙂

Hi Basu,

I want to take a Online Term Insurance and after lot of analysis i short listed Max Life Insurance(Baisc vanilla plan). Earlier i believed that Online Term insurance does not consist Agent’s commission but i came to know that these plan also gave commission, companied treat it as assisted commission(It can be given to any individual agent or any other company which are know for policy comparison ).

So now i want to know how if i do not include any such person and fill complete form on my own then how i can get benefit which was about to given agent/company.

Thank you in advance and appreciate you initiative to aware people with out any business mind. You are doing really a great job !!!

Regards

Aditya

Hi,

Can pls suggest among Aegon, Aviva, Max Life. I want take 50 Lac term insurance.

As all three have low premium compare to others.

Rahul-My choice is listed above. As per that Max is my choice.

Hi Basavaraj,

You haven’t specified your view on aegon and aviva.

I would like to know your view (either good or bad) on above two.

You reply is highly appriciated.

Rahul-To me all are equally GOOD and BAD.

Hi Basu,

Also I wanted to know if I take ICICI/HDFC,and pure term plan for 1 Cr,Is there any hidden exclusions that we sud be aware of??Or how to find what all exclusions are there which may interfere in getting 1 Cr to my nominee in an event of my demise??

Kishan-Check the policy features carefully. You will find any such exclusions. It is hard for me to disclose all on this platform.

Kishan, I have gone through all confusions as you have now. I can understand how it feels. I suggest you to fill the online proposal form of HDFC and ICICI and also any other insurance provider till the payment page. Try to keep all the options same such as Sum Assured, Policy Term, payment option. Check what is being asked specifically by every policy provider. HDFC may ask family health history irrespective of age whereas ICICI asks the same when your parents were below 55 and Max may ask upto 60. Same goes with your health history as well. It varies from person to person. Don’t hide anything but if one’s parents had some health issue after 60 then it need to be mentioned in HDFC but not in ICICI or Max.

As ICICI and Max are going aggressively in insurance business, you better prefer one of them. I have read few complaints that HDFC takes more time to issue policy. Anyway, Max is going to merge with HDFC. If you are in any of the cities where Max is providing its services then you take the policy immediately. Once policy is issued, you can move to anywhere. Nobody is bound to stay in the same place just because of insurance policy. You are free to live any where.

You can find the “Exclusions” in Brochure and Terms & Conditions. Its “your” policy, so you have to read yourself, not for you but for your loving family. Nobody will do that for you.

Hi Basu

I have taken home loan from HDFC.I dont want LIC as it is expensive and Max insurace as it is not so widely spread and since i am working in priviate sector I really dont know which place I wud be in next few years.So I feel ok with ICICI and HDFC.

1-Which one sud I choose?

2-for accidental rider,they say for just 4k, i can get 1 crore so is it crore extra they talk in addition to regular plan of 1 cr?

Regards

Kishan

Kishan-1) Both are good to me. You can choose anyone of your choice. 2) Don’t go for any riders. Instead, buy accidental insurance from general insurance companies.

I am planning to take pure online term insurance from HDFC LIFE CLICK 2 Protect plus (Life Option) .I am 34 yrs old Non-smoker NRI .I would be getting the Quote between 2 to 2.5 Crore for 24 yrs duration from HDFC Representative office in Dubai who is assisting me to get the insurance done and my medical test would happen in India (I will be traveling in Nov 16 to India ).

1 ) Could you please suggest which all points should I clearly ask them or get clarity from them so that I don’t fall in trap of any hidden conditions for this particular pure term insurance ?

2) After medical test in India is done would they hike the premium and would they maintain the same if medical report is more or less normal.

Regards,

SJ

Swapnil-1) There is no standard list which I too can share with you. But try to fill all proposal documents on your OWN. Understand all terms and conditions before signing the documents.

2) If medical report is normal (as per their norms), then there will not be any premium hike.

Hi Sir,

When I met the Sales person in HDFC Life Representative office in Dubai,he told me below things.

A ) Concerned Sales person would upload the term insurance documents online from his HDFC LIFE Representative Dubai office on behalf of me after taking all the documents from me.and he told me rates would be same like online done by me …My Question :- 1 )If the sales person does all the online, will this Policy of mine would be consider as online as per HDFC policy ?

B) As per the sales person since I am processing the claim from here and I a NRI, Taxes will not be applicable for the policy which would be considerable saving. Is this correct ?

Note :- For medical I will be going to India

Regards,

SJ

Swapnil-Check personally whether the price is same or not. Product is pure insurance one but not savings one. Check whether they are selling you term plan or any other endowment or ULIP.

Hi Basavaraj,

I wanted to buy Term plans to cover myself (39 years) & my wife for 1 crore rupees each. I am an NRI working in Dubai. I read your article & discussions which followed & shortlisted 3 plans:

1. Max Life Cover amount INR 15300 with option to add accidental coverage to tune of 72 Lakhs for just 4500 Rs more. This seems cheapest and some top performer in private market

2. ICICI Pru life – 16800 for only term insurance. Add ons wil cost more I guess. I understand your view is to go rider free. The riders looks very lucrative with 31 critical illness.

3. LIC – Govt and perhaps most secure. But charge twice. Do you see its risky to go with Max & ICICI in India

?

4. As an NRI, does any of above term policy is not applicable or give less benefits?

5. I want the same plan for my non-working wife. Will insurance company gives similar plan for non working people also?

Pls advise. And yes thanx a ton for such an informative article and facing and keeping criticism on you blog. God bless for your support on this ?

Thanks- Nadeem

Nadeem-1) You can go ahead. 2) But if you buy standalone critical illness insurance, then benefits will be more than this rider. 3) I prefer ICICI and Max over LIC. 4) I think ICICI and Max Life offers to NRIs but not LIC. 5) NO.

Hi Basavaraj,

Thanks for your quick response. Followup queries are:

1. Do you mean there is no term plan for non working woman?

2.is it better to buy 2 to 3 term plans of 50 lakhs each. Or just on of say 1.5 crores. What r the Pros and cons ?

BR

Nadeem

Hi Basavaraj, I am planning to buy term plan for myself and with a little bit of personal research and your in-depth analysis i have decided to go for Max Life term plan.

However i am troubled with two dilemmas, in your post MAX LIFE duration is 35 yrs only where as in their website the maximum duration of plan is 40 years.

Other dilemma is that needs your suggestion; is it wise to take accidental benefit or premium waiver rider when this option is already available with basic plan in Max life.

Kumar-Max Life may revised the feature. You can directly check at Max Life portal regarding maximum age. Never combine other insurance (like accidental or critical) with life insurance. Buy them separately.

Hi Sir,

My father has undergone major operation in Lungs when he was 48. Some part of Lung was removed which had carcinoid tumor. He is 67 now and healthy.

Now, while applying for Term Plan, I do not see any option related to Lungs in family history. I am not sure whether it comes under cancer or not. Will there be any problem if I don’t mention this. I am losing peace of mind due to this as I have to provide protection to my family. Please suggest.

Sanjay-No need to worry. Write a mail to the concerned Insurance company by quoting your proposal number.

Dear Sir, Thanks for sharing such important information about term plan. My age is 24 years and I request your advice on an insurance plan which can give me return on maturity as well death benefit.

Sharma-I will not suggest any plan which claim to be give you death benefit and return on maturity. SORRY…

Can you suggest me any good plan.

Sharma-If plan means term insurance, then they are listed above.

Other than Term Insurance.

Sharma-NONE.

Hi Basavaraj Tonagatti,

My Annual Income is around 6.4 lacs. I planned to take HDFC & ICICI Online Term plans of 50 Lakhs each (Total=1 Cr.).

1) Does the insurance companies accept it. They are saying that based on some underwriting, they will decide.

2) Does Term Plans of HDFC, ICICI covers Terrorist attacks, natural calamities, war etc.? They are not in their Exclusion List. Does that mean they are covered.?

3) As HDFC & Max are going to merge, which Term plan you recommend from both.? Max seems to be cheaper and better in other terms but if I take it now, it going to be handled by HDFC which in turn is a good company and one which I shortlisted.

Thanks & Regards,

Raghav

Raghav-1) Yes based on underwriting, they accept it. How can they upfront guarantee you that they accept your proposal?

2) If the reason of death mentioned by you are not in exclusion list, then why you have to worry?

3) As of now go with Max.

What you recommend now based on current situation.

Can we go ahead with Max life with lesser premium than HDFC ??

Manish-MaxLife.

Sir

I my age is 31 years and I want pension/retirement plan, I want to save Rs 5000/- per month (60,000 per year) up to attaining age 60 years.

Sir please suggest me any good saving plan/pension/retirement for long term i.e. 29 years ,60K per year saving so that I can get good return after 29 years which can be utilized for pension.

Avadhesh-This is not the right platform for asking. You can question the same in our BasuNivesh Forum.

Dear Basavaraj,

I was going for HDFC eterm plan but after knowing that HDFC and Max life are merging together and max life term plan is 15-20% cheaper than HDFC, do you suggest to go for Max life rather than HDFC?

Prem-Better to go 🙂

Dear Mr. Basu,

Thanks for sharing very informative article on term Insurance.

In your article regarding Top 5 companies for buying term insurance plan based on certain criteria. Currently Max life also started giving term plan for 40years term as well as in quaterly, monthly mode payement.

Will your top 5 will now change based on new features max life is giving.

Also would like to know your views after hearing that HDFC life and Max life merger.

Now what should the customer chose between the two if anyone has to buy term insurance currently.

Manish-Now MaxLife turned into HDFC. So now again my recommendation holds good 🙂 No need to worry about mergers.

Hi Basu

I really like your elaborated informations that you put here…and point to point detail

But i have a query

I have taken Aviva I Life policy

How would you rate them…I didnt see you mentioning that in your column

Thanks in advance

Anil-If you already bought it, then don’t think too much. Stick to it.

Hi Basu,

Thanks for nice article. First time i got this detailed info about term insurance. Thanks to my friend who referred your blog. I am 41 yr Non smoker, NRI (India only on vacation)

1) Pls suggest policy term 25 or 30 which is preferable

2) For medical, i need to come to India (During vacation)

3) In case insurer survives after policy maturity, what could be the return against Sum Assured 1 cr.

Now interested to go ahead, expect your comments.

Kesavan-1) Term must be up to your working age.

2) YES.

3) NOTHING.

Thanks Basu,

Working age means, i can consider 15 to 20 yrs maximum as Policy Term with regular premium payment.

My understanding is correct?

Thanks

Kesavan-If your working age is 15-20 years, then term of term insurance also be 15-20 years ONLY.

Hi Basavaraj Tonagatti,

There are 3 Questions please reply both in detail

1) Is there any specific reason of not Choosing Max Life, Although It is slight cheaper ?

2) WRT term plans,Is there any difference between accidental death & Death ( off course leaving suicide & War apart) Or all type of death are covered?

3) I need accidental Insurance for my Wife(age 28)( since my all other things are taken care by employer) . Can you suggest best 2 plans considering – claim settlement ratio ; any type of death; least premium.

waiting for your response. Thanx

Manoj-1) I replied to similar comment in one of earlier comments. Please go through it.

2) Accidental death feature will also covers your disability also.

3) Refer my earlier blog post “Best Accidental Insurance Policy in India-How to choose them?“.

Hi Basu,

I see SBI Term insurance has second highest cost (nearly twice the cost of Max Life and Kotak), claim settlement ratio of less than 90% and is existent for 14 years (on par with most others greater than 10 years).

How did it find its place in the top 5 list.

You got to give me atleast one reason why its there ahead of many others.

Also I feel just to show you are not biased against LIC, you have included it in this top 5 list given the fact that they loot in term plan also.

Hi Mr Basu,

Between ICICI Prudential and Tata AIA, which one will you suggest for online term insurance for 1.50 crores, 30 years plan? How are the credentials of TATA AIA?

Pranjal-I listed my Top 5 in above post.

Hi How about New India Insurance company. Can we consider it?

Kamal-New India Insurance company not offers life insurance. It is general insurance company.

Great blog n good explanation for not going ppt beyond retirement age.

Bprayank-Pleasure.

hello sir. thanks for the article. it is very informative. i want to buy indiafirst life term plan because it is very cheap. but claims settlement ratio is verry very low for that company. i read in a website called mintwise that claim ratio is not fully reliable because of various factors like company age, and type of policies sold by company. then can i ignore claim ratio and buy indiafirst or other cheap plan? these companies are good companies, sir?

Mahesh-I not rely on any new entrant.

Very nice and informative article… Thank you for that!

Somehow PNB Metlife couldn’t make it to your top “7” companies after the 2nd round of filtering. I felt it satisfied all the 3 filtering criteria.

Is it so that you feel more comfortable or have more confidence on other 7 companies?

I am an NRI, 36 yrs old and looks like 2 top choices are PNB Metlife and HDFC protect. PNB Metlife’s premium is cheaper. Could you pls guide which one to go for?

Thanks & warm regards,

Amit

Amit-My choice is to do Top 5. If you short list of Top 7, then you can go ahead. As I said earlier and repeating once again, to me all are equally good and bad.

Actually I meant, as an NRI, I have limited options from the top 5.

Also I am confused why PNB Metlife couldn’t make it to top 7?

Amit-At the end which comforts you is matters MORE than Top 5 or Top 7 🙂

Hi Basu,

Thanks for all your article. It was very helpful. Could you tell us the reasons (which i may not know), why Max Life eterm plan which have less premium and is also best comparatively to ICICI prudential, HDFC life in many parameters, is not listed in this top 5? Please dont say that, if you comfortable with it go ahead. I would like to know what reasons you think bad about Max Life made you to not list under top 5.

Jeyraj-There is no biased reason to out Max from my list. I short listed from above creteria. It does not mean MaxLife is BAD. Premium varies based on thier acturies product design, company’s profitability margin and many more things.

Hi Basu,

According to the above criteria

1) How old is your insurance company?

ICICI Life–15 years

HDFC Life–15 Years

Max Life–14 Years

Don’t think 1 year big difference.

2) Claim Settlement Ratio

ICICI Life–93.80 %

HDFC Life–90.50 %

Max Life–96.03 %

Max Life has better claim Settlement ratio

3) Cost of Term Insurance–

According to your report

ICICI Life–8906

HDFC Life–10332

Max Life–7400

But When I checked in HDFC Life and ICICI Life websites, premium for ICICI Life and HDFC Life almost same for same setting Pure Life option. But in Max Life premium was ~2000 Rs less than these 2 and this gap widens when current age, term, sum assured increases.

So here too Max Life scores best

4) Plan features

Max Life:

Minimum Entry Age–18 Years

Maximum Entry Age–60 Years

Maximum Expiry Age–70 Years

Mode: Annual Mode only

So In Max Life only option given for paying premium is Annual. But Its advised by many pay premium annually to save premium cost, transaction charges. Doesn’t it look good. Why it was not highlighted in Green above?

Also, I want to add another 4 criteria’s

5)Solvency Ratio

As on 31st Mar 2015

ICICI Life–3.37

HDFC Life–1.96

Max Life–4.25

So here too Max Life scores best

6) Status of Grievance % Resolved during the Year

ICICI Life–99.50

HDFC Life–93.01

Max Life–99.98

So here too Max Life scores best and even ICICI Life

7) Status of Grievance Pending More than 30 days

ICICI Life–10

HDFC Life–2025

Max Life–0

So here too Max Life scores best and even ICICI Life

8) Claims Pending at the end of period 2014-15

ICICI Life–0.78 %

HDFC Life–2.26 %

Max Life–0.07 %

I have compared Max Life only with ICIC Life and HDFC Life because those are listed as top 2 private insurers in this list and it was advised to take Eterm with only 1 or 2 insurers, not to split much between insurers.

In all the above criteria only Max Life scores best. Also if you think nothing bad about Max Life, why its not in your list of Top 5. We all here reading your blogs hoping its unbiased. Whatever, we appreciate your efforts to help us to gain some knowledge about these financial planning for free.

FYI…I am not an agent or supporting any insurers. I already have 1 Eterm Inusrance with LIC for 50 Lakhs and looking for Private Insurers for 1 crore sum assured to save premium cost. I have almost decided to go with either ICICI Life or HDFC Life and Max Life was never in my list after reading your article. But after going through IRDA report, MAX Life looked better or approximately equal to ICIC Life or HDFC Life and so checked Max Life eterm plan premium which is almost 2000 Rs less from ICICI Life, HDFC Life for 31 year old, 30 year term, No Smoker, 1 Crore sum assured. This gap widens if age or sum assured is high.

I keep replying here, just because whoever read this article should not be misguided and they should know MAX Life also in top 5 to consider.

So According to my through research across many websites and blogs, below are my suggestion about Eterm plan.

Whoever feel comfortable only with Govt backed Insurer, Go with LIC, but ready to pay High premium almost 2 times of private insurer. Or split 1 with LIC, 1 with private, so on average will be less premium cost, at the same time you will feel comfortable.

Private Insurer Top 2:

1. Max Life eterm any option as per your nominee knowledge of managing Lump sum, else go with income option

2. ICIC Life Pure Life option (If you want Lump Sum),HDFC Life Income Plus option (If you want monthly income)

Maximum Expiry Age: 60-65 years or until you feel your nominee/dependents depend on your income (Go beyond 65 only if you marry late above age 40 or have below 5 year old kids @ age 45).

Number of Term Plan & Number of Insurers: 1-3 Maximum…Plan to have More sum assured in the period of your child birth upto the age of 25-30 years old.

At What Age to take: 1 Term Plan– Before Marriage and another after Marriage. If you still feel under insured, try to increase sum assured of 2nd term plan. Take 3rd term plan only if you have availed loan.

These are my findings, suggestions for a salaried Middle class, May or May not work for you. Please decide according to your conditions and life.

Dear Readers ,

I just want to add one more criteria to see – Amount of claims paid in terms of benfit amount-

As per IRDA report 2014-15, the position is as under-

1. LIC—95.51%

2. Max life –93.59%

3. Star Union–91.54%

4. Sahara life — 89.86%

5. TATA AIE – 89.54%

The position of HDFC life–65.5% and ICICI is 79.56%.

This parameter can be taken to see that although the company has settled more claims but reduced the claim amount.

Any comments for above please.

Pranav-Claim amount of LIC is high than rest?? Check your data 🙂

Dear sir,

Pl download report from this link.

https://www.irdai.gov.in/ADMINCMS/cms/frmGeneral_NoYearList.aspx?DF=AR&mid=11.1

Annual report page no 127 & 128. I had rechecked for LIC it is amount claimed Rs 9480.49 crore and amount paid is 9055.18 cr, making it to 95.51%.

regards

Pranav-You devide that amount by number of claims paid. You will then get the average amount paid. Then you feel the heat.

I had checked & this is the output for amount paid per number of claims :-

amount paid in Cr No of claims paid amount paid / no claims

Crores

1. LIC – 9055.18 742243 0.01219975

2. HDFC – 263.52 11031 0.02388904

3. ICICI 352.86 11546 0.03056123

4. MAX 245.46 8786 0.02793763

5. SBI 305.40 13303 0.02295723

MAX life still looks better than HDFC.

Pranav-Now tell me who is best?

Basu-Although ICICI is paying avg claim amount of 3.30 lacs but point of worry is that average rejected claim amount is 11.47 lakh. This shows ICICI is reluctance for payment of higher claims.

Pranav-Check what type of claims are they and reasons for rejection.

Hi Basavaraj & Pranav,

Four months back, I decided to take HDFC Term Plan for 50 lakhs and ICICI Term Plan after few days. But as I had some doubts, I kept on postponing. I cleared those doubts with Sreekanth of Relakhs and however I see fall in HDFC Claim Ratio etc. and as a final option I checked your blog.

After reading your discussion, I just google’d about Max Life and came to know that Max Life & HDFC are going to be merged. Now, which Term Plan do you recommend.

Sanjay-Is corporate merger actually affects an individual? Don’t think too much. Just buy with the company which you feel comfort, affordable and features matching. People spend so much time on researching on a simple product called term insurance. Don’t do that, it is not a rocket science.

Jeyraj-First thing let me make it clear. I am neither for nor against any companies. Because at the end what matters to me is readers than insurance companies. Second thing, I have to short list 5 not more than that (as per the heading of post). So I did, but it does not mean that MaxLife is bad or rest of other companies are BAD. I am not here to promote any particular company. Look at the plan features, there others score more than MaxLife in few features. That is the reason I may left that.

But whether I pushed any particular company or product through this post? I stick to my unbiased views. At the end it is YOU who have to decide.

Now regarding number of term plans, do you feel 2-3 enough? There is a misconception among us that we stick to either one or two term insruance. But you must review your insurance at least once in a 5 years and based on that you must increase the sum assured. We all have mindset that if we have Rs.1 Cr, 2 Cr or 3 Cr insruance means it is enough. It is not the case. Hence, it is not worth to say that ONE must buy term insruance to the maximum of 3 only. It is continues process, which we must analye the requirement. The financial status of today is not the same of tomorrow. Future is uncertain, that’s why we bend at insruance. Am I right?? 🙂

Hi Basu,

So, you are saying that except plan features Max Life is best. So, Incase If you would like to, Please modify the article to put Max life in 2nd place (add condition whoever want to go for Annual pay option and entry age before 60). Would be helpful for those who will be redirected to this page while searching for online term plan. Let them decide based on their eligibility. Not many will read all these comments. Please remember that these kind of article influence decision for those who have less information about Term plan, feel lazy to go in depth, even if you mention disclaimer “its upto you to decide in the end”.

And for Maximum number of Term plan, I said 3 because we should take maximum sum assured in 1 or 2 term plan and don’t split with myth of if 1 insurer rejects, other will approve. Of course if one feels under insured, they should take many more, I’m just suggesting to club it within 3 if possible.

Jeyraj-Instead of modifying the Top 5 list, I keep all data as it is. Let the readers decide. If they felt features best of MaxLife then they can opt it. At the end of the day, I short listed based on all creterias which I gone through. I have not hid any report just to hide MaxLife. But put it openly to all to decide on their own.

I agree about splitting. One must not split. But at the same time, buying any insurance is not ONE time issue.

Very informative. Thanks

Dear sir,

Nice article and discussion. Am 37yrs old NRI staying in Bahrain. I am looking for 4cr term insurance policy. Max Life, icici, birla said they don’t provide nri cover. I dont know about hdfc. How is aegonreligare and metlife. Is it good? Kindly suggest. Thank you.

Sudharsan-HDFC provides insurance to NRIs. Both Aegon and Metlife are good. You can buy.

Hi Basu,

Thanks for your reply. whatever the reasons, it would be just excuse. According to the report, if many grievance (large gap compared to other insurers, only 93.16 % resolved) is pending more than 30 days shows the customer service is not good, right? it means something wrong in their customer support (either inadequate support persons to resolve or unwilling to settle the claims…etc), atleast as of now. when we shortlist insurers this also does matters, right?

Jeyraj-You can ASSUME, but can’t say exactly of what happened.

Hi Basu,

If we consider claim settlement ratio by assuming all are genuine claims, we should also consider Grievance resolve percentage assuming all are genuine Grievances. Also, we should consider How many claims pending more than x number of days, average claim settlement days, how many Grievance pending more than x number days.

Jeyraj-Do you feel always delay may be due to insurance companies? What in the cases where insured family submitted for claim, but not provided sufficient documentation?

Hi Basu,

Take an Example…Out of 2 candidates, one scored 95 % and other scored 90 %. Who will you select? will you look in to the personal reasons in depth of the second candidate while shortlisting? will you take risk of selecting 2nd candidate over first by assuming/listening to his reasons for not scoring.

Jeyraj-I replied to your all questions. Now it is YOU to decide of which is BEST. I am not here to promote or degrade any companies. I hope you checked the plan feature option of the above post. Also, do keep in mind that IRDA data about insurers is RAW onw, judging your company based on that is a biggest MISTAKE. 🙂

Hi Basu,

We all are forced to rely on IRDA report including your blogs, many other blogs, websites…etc. Do we have any other option?

Jeyraj-I don’t have second opinion on that. But what I am saying is, don’t rely too much on this data alone. It is RAW data.

Mr Jeyraj,

Why you are promoting Max life so much???

Leave it with users to decide what is best, with whom they should go. Browse google and you will see n number of websites promoting some brands and nobody care to answer or resolve doubts. If Basu is doing his part you should appreciate it instead arguing. Take some time and get you website/blog rolling with information and then see if you can answer each and every query as he is doing….

Humble request!!! Appreciate rather than criticising, we understood your opinion, thanks, now leave on us to decide what is best!!

One more thing, I am not a friend or hold any kind of relation with Basu, I am just trying to understand investment through his website & user comments from a week so….

Sai-Thanks for sharing your view. This is the reason I never promote any particular company or product.

Don’t get upset or demotivated, as you must be knowing from comments there are lots of follower and listeners of yours than distracters. Nobody in world give advice free of cost. If it is made available there would be people around to felt jealous.

We truly admire your work, research & opinion. Your opinion gives a reason to think, to follow or not to follow it all depends on individual. Atlast market is subject to risk.

Sai-NONE can demotivate me. I started this blog in December 2011 and running it continuously without PAUSE.

Could you tell us the reasons (which i may not know), why Max Life eterm plan which have less premium and is also best comparatively to ICICI prudential, HDFC life in many parameters, is not listed in this top 5?

In IRDA Annual report 2014-15, Why HDFC standadrd Life have 2025 Grievance pending more than 30 days which is very high compared to other insurers of same size?

Jeyraj-That you better ask HDFC. It is just report. Reasons not disclsoed.

Hi Basavaraj,

Is there any problem going with Max Life? There is almost Rs 2000 of difference in annual premium between ICICI Vs Max Life. Why there remains a huge difference in premium like LIC, ICICI or MAX? Do they factor the premium on the basis of claim received?

Nitsh-Claim settlement and Premium fixing are two different things. So don’t combine both. If you feel Max Life is good for you, then simply go ahead. No issues at all.

Hi Sir, My name is venkat. My age is 32 yrs and Im diabetic. Same was disclosed to hdfc for the term plan click2protect.I opted for 1 cr term plan for 33 yrs(till 65yrs) along with cancer care, accident and critical illness riders. Now after medical examination they have increased the initial premium which was Rs 2500 to Rs 3600 claiming medical diabetic conditions. Should I go ahead or reduce the premium by removing the riders and opting for only 1cr death benefit ? Will taking riders separately have any big benefit in terms of insurance premium amount and cover ?Its almost a month having applied and only now they have comeback on this. s it worth going with premium mentioned ?Is there any diabetic specific rider plans which will help ?

Sir premium mentioned below is monthly

Venkat-Don’t go with riders. Buy them separately. Better to go ahead with that premium, if you feel the premium is affordable for you.

Hi Basu,

Very Nice article, Please keep sharing your well versed knowledge.

Can you please give me a suggestion.

Im 36 years of age,smoker. Earning 8.5L p.a, I want to take a Term Plan of 1.5 Cr for 30-40 years. Companys include multiple option n riders, Accidental, CI, extra life, monthy income etc. Here I got confused.

Wheter its good to go for it.

Or if i take 75 Lac Term plan and 75 lac some investment plan. if so please suggest some company to go for it.

I think HDFC life, ICICI Pru life, MAx life, Bajaj Alianz, which one to go for from your view point.

Smoker : Yes

Annual Income: 8.5 Lac

Entry Age: 34 Years

Term : 36 years (Till 70 Years)

Ideal coverage: 1.5 Cr (18 times of Annual Income)

Rider: WAIVER OF PREMIUM ON DISABILITY

Premium:

Max Life 28,983/- p.a 39 YEARS

PNB Metlife 28,800/- p.a 34 YEARS

ICICI iprotect-smart : 29,289/- p.a 30 YEARS

HDFC click-2-protect 36,877/- p.a 30 Years

Which one to go for? Please suggest

Pradeep-Go for plain term plan than any riders or payout options. First, understand how much insurance you need and for how long. You claim to be looking at Rs.1.5 Cr term insurance and suddenly for Rs.75 lakh insurance. Also, be specific of term..in your case there is a gap of 10 years in assumption.

Dear Mr. Salian,

ICICI Pru iProtect Smart is the ONLY term plan that offers life cover along with health cover for 34 major illnesses like Cancer, Heart Attack, Kidney Failure & more.

In case of permanent disability all future premiums will be waived off. You can also opt for double coverage with accidental death benefit cover.

To know more about this plan, please visit the below link and fill in your details and we will have one of our experts assist you.

Link: goo.gl/QH8lpG

Regards,

Team ICICI Pru Life

http://www.iciciprulife.com

Dear Sir,

I just filled the ICICI term insurance application online today. I received a PROPOSAL CONFIRMATION pdf in the email . It mentions that MEDICAL TEST DETAILS – NO MEDICAL TESTS AS PER INITIAL UNDERWRITING.

Does it mean, they will not conduct the medical test ? If so should I insist for medical test ?

Regards,

-Santosh

Santosh-They may insist you later. But go only if they conduct the medical test. Otherwise, simply reject.

Ok Thanks.

Let me see what they are going to do . In the worst case, if they do not do medical tests, how to reject ? The payment is already made through credit card.

Regards,

-Santosh

Santosh-You can send them a mail and they will refund it (excluding the taxes).

Question:

After taking Policy, why they will ask for Medical test again. If they don’t do it while taking the policy

Pradeep-Whether the policy is issued??

i have to take a term plan of 75 lacs but i am confused regarding PNB Metlife and Max Life because i require Total Disability and Monthly income. Both have different policy like monthly payment, different term years and claim settlement ratio.

Suraj,

I have very bad exp with PNB metlife personally. I guess Max will be good.

I am moving to Max from PNB.

Hi Suraj,

you mentioned like u had very bad exp with PNB metlife.please let me know the reason and it that some thing related to claim or something else..?

Krishna-If it is realted to claim, then how can he be replied?? Just imagine 🙂

Suraj-Why you are looking for those riders?

Hello sir,

1. Want to select term insurance to secure the home loan of 25 lac for 25 yrs period, my age 34 yrs, non smoker. Want safe term plan. What can be best one?

2. Is it good to assign term insurance policy to home loan banker?

Thanks for information provided in above blog, really helpful.

Sandeep-1) My best are already listed above.

2) Better not.

Dear Sir,

Thank you very much for your valuable suggestions.

I think considering all aspect I should go for policy term till 60 Yrs and 3Cr of SA for ICICI Pru iProtect Smart.

However I did a basic comparision on premium amount between age 60 Yrs and 70 Yrs, I found both premium payable is almost same with not significant change in SA.

i.e.

Till 60 Yr age ( 19Yrs) – SA – 3 Cr. – Premium -35,836/-

Till 70 Yr age ( 29Yrs) – SA – 2.2 Cr. – Premium -35,743/-

Do you feel, the option-2 is good ? You loss 80L SA and get 10 Yrs coverage. Does it make sense ?

DOB – 20-JUN-74

Regards,

-Santosh

Santosh-Do you feel insurance required after your retirement (Hoping you retire at 60 years of age)?

Dear Sir,

I have decided to go for term insurance from ICICI prudential i.e ICICI Pru iProtect Smart after reading your blog and doing some research online.

My personal details :

DOB – 20-06-74 , NON-SMOKER, ANNUAL Income – 25L (after tax), service – IT industry, one kid 6 yrs age

1. What should be duration . I know your advice is to take till retirement. You know in IT industry it is difficult to predict retirement age. Also you get fired from job at anytime. If one can continue till 50-55 age it would be great achievement. Should one choose till 55 or 60 or 65 age?

2. What is the amount one should take . Should I go for 15-20 times of annual income or just 1 Cr ?

3. Your advice of taking separate accident cover and critical illness cover from general insurance company is appreciated. However should I take these insurance. How to decide whether it is required for me or not ? If so what coverage amount is appropriate ? What are the good plans from general insurance companies ?

4. As per your suggestion, I am taking the vanilla term insurance of ICICI Pru iProtect Smart.

Kindly see if you can answer these quieries.

Regards,

-Santosh

Santosh-1) 55 yrs. 2) Better beyond 20 times. 3) Yes, you must buy them. There is no such yardstick like life insurance about the quantum of these insurance products. 4) Good..carry on 🙂

Thanks a lot Sir.

Is ICICI’s Payment term (Limited option) good ? Say your policy term is for 30Yrs, but you pay premium till 25 yrs ?

Or Regular option is better ?

Regards,

-Santosh

Santosh-I prefer regular payment.

Dear Sir,

Is there any difference if we take term plan from policybazar portal and directly from ICICI prudential portal ? I entered my details in policybazar and they are almost forcing me to take from their portal. Is there any difference in premium or any other issue ?

Regards,

-Santosh

Santosh-Premium wise there may not be changes. But yes, they earn from this selling. Don’t fall to their trap.

Dear Santosh,

We are happy to know that you have decided to cover your life with ICICI Pru iProtect Smart term insurance plan.

You can purchase this plan by visiting: goo.gl/QH8lpG.

Please fill in your details in the link above and we will have one of our experts assist you with your concerns.

Regards,

Team ICICI Pru Life

http://www.iciciprulife.com

Dear Sir,

Your blog is one of best source of knowledge. I went through it thoroughly and also your answers to the queries. I have decided to go for ICICI term insurance. However I have few questions, which I have e-mailed you with personal details. Kindly see if you can reply the same.

It would help me to take a decision fast.

Regards,

-Santosh

Hello Sir

Greeting for the day! How are you doing ?

Dear Sir, I am 25 years (11/12/1990) old self employed (business) & Non Smoker with no medical back history.

I have started business from November 2014. Now i am earning 13 to 15 Lakh per year (Profit)

I want to purchase Term Plane. In the same regards, i want to know first, but it online or off line ?????

I need 1 Cr Sum Assured for the bad time.

Sir, please suggest with which company should i go ?? & Also suggest with which plan should i go ???

I want to also know that it would be better to buy rider for accidental or should i purchase separately ???

No back ground history for critical illness. so should i test my self before buying the plan ???

Hope to have your valuable reply at the earliest.

Regards

Sushil Sharma

SRI Equipments

09013940134

Sushil-The products are listed above. Buy anyone, but don’t buy any riders. Instead, go separately with general insurers.

Thanks for all your effort in helping people in unbiased way. really appreciate your initiative.

My wife has eterm plan from Max life for 1.2 crore. I want to do the eterm from a company from whom settlement is easiest but at the same time don’t want to pay too much (LIC listening?). I am confused between which eterm plan is best for me, in term of settlement. Could you please tell on basis of your experience that which one will be better is my situation. Preferably, I am interested in eterm plan from company other than Max life because we don’t both husband and wife but your suggestion is very helpful for me to decide. I have two questions

1) I am confused between LIC, ICICI and max life. Could you please rank them for me please?

2) If I want term plan of 1 crore, Can I take 50 lakhs LIC for 27 years (retirement) and another 50 lakhs from ICICI (35-40 years) to reduce the overall cost?

Many Thanks for your suggestions in advance.

Prem

Prem-1) My order of preference is as you mentioned. 2) If cost matters you, then go with ICICI.

Dear Mr. Basavaraj,

Kindly suggest

1)whether I can go for 50 lacs with LIC and 50 lacs with ICICI. is this acceptable to both the company and is there any impact in claiming the amount in event of misshaping with insured person. Any kind of risk is associated with this.

2) In your comments, you mentioned that accidental death benefit rider should not be clubbed with term insurance. I want to know why. Any risk that they don’t pay that or any other risk as cost wise, it looks ok. and with respect to other rider like critical illness, I am not much worried looking into medical history.

3) Can my wife ( Non working) be also included in either of cover with me in LIC or ICICI.

Thanks in advance for nice suggestions in this forum.

Regards,

Deepak Gupta

Deepak-2) There is no risk but you can get the accidental insurance at much cheaper rate by general insurers.

3) Included in the sense?

Dear Basavaraj,

Kindly let me know whether LIC or any other Insurer will increase premium if in between the policy term if one is found to be have some illness.

Deepak-In between they will not. If they have to increase then they will increase it at initial stage itself.

Dear Prem,

At 93.80%, we are happy to share that our claim settlement ratio is one of the highest in the private life industry. You can read more about our claim process and philosophy by visiting: goo.gl/SzgDJn

If you have any further queries about this plan or want to purchase the plan, please visit: goo.gl/QH8lpG and fill in your details and we will have one of our experts assist you.

Regards,

Team ICICI Pru Life

http://www.iciciprulife.com

Hi Basu,

I am 33 and smoker,

I am planing to bay Max life term Insurance plan for 1.5 cr. witch is the bast way to bay term plan online or offline.

If Required, Please give me a right product term insurance plan company name.

your valuable feedback is appreciated.

Thanks & Warmest Regards & Respect,

Virendrakumar Masani

Virendra-Online is best. You can go ahead with Max Life.

Hi,

I’m a graduate student studying in USA and also working as research assistant. It’s been more then 1.5 years that i’m staying abroad.

Currently, i’m in India for a short trip and thinking to buy ICICI insurance term plan. I need your suggestions on following points:

1. Do i come under the category of NRI or Resident Indian for insurance buying purpose?

2. Is ICICI term plan a good option?

3. Since, i’m a student and i do get salary in USA, will there going to be any issues with income to be shown for term plan purpose? Can a student buy insurance?

4. I worked in India for 3.5 years before moving to USA, so i do have ITR for all those 3.5 years.

Vijay-I replied to your question in FB message.

Dear Vijay,

We are glad to know that you have considered protecting your family with ICICI Pru iProtect Smart term plan. iProtect Smart is the ONLY term plan that covers your life along with 34 major illnesses like Cancer, Heart Attack, Kidney Failure and more. With this plan you can opt for a critical illness cover of up to Rs. 1 Cr, you can avail the entire critical illness cover on first diagnosis of the listed 34 illnesses.

To know more about this plan you can visit: goo.gl/j26BOj and fill in your details and we will have one of our experts assist you with your queries.

You can also leave us a message on our Facebook page and we will have a call back arranged.

Regards,

Team ICICI Pru Life

http://www.iciciprulife.com

Hi Sir,

i am Ram Mohan from Hyderabad, i am planing to start TERM POLICY in this year.

i searched so many policies in online and asked my well-wishers. But i didn’t get proper response.

Can you please suggest GOOD and Suitable policy for me..

Ram-They are listed above.

Hi,

I am 36 and non-smoker, recently AEGON team contacted for term insurance and looks some thing good. But I am in confusion whether I can go or not to take it. Premium wise they are less than HDFC and ICICI.

Any your valuable feedback is appreciated.

Siva-If you are comfortable with company, premium and features of plan, then go ahead.

Hi Sir,

That is Confusion, I have. I don’t know any thing about the company. And they are saying that their clime ratio for the year 2015 to Sept 2016 it is 92% and Premium wise it is very less when I compared with HDFC and ICICI. But I am not expert in this Term Insurance area and absolutely it is funny to ask any one experience since they may not alive to know . So Only experts can share their feedback since they will in this market.

And please consider this is my sincere request and Advise the best term policy and I will blindly go through it.

Hope you understood my situation.

Siva-I listed them above.

Hi I am 32 year old non smoker and have purchased pnb metlife mera term plan with 92% settlement ratio however in your opinion it is not in top 5. I am still in free look period. Should I look on other companies? As the premium was also low and product was good I bought it. Pls suggests.

Kunal-Stick to it and continue.

Hi Basa Sir,

I was tricked by Metlife that the SA will be 1.5 cr however they added the same in variable and SA they made is 1.04.

I have read the document carefully and inquired that MISS SELL the policy to me. I did not agree on any other letter ahead they were trying to provide me explaining that SA will be 1.5 cr. I asked for 100% premium reimbursement.

Not sure if they will do it.

I now want to select Icici and Max where premium of Max for 1.5 cr is 13,900/- and ICICI is 15,341/- both inclusive of taxes. Basic term plan lumsum pay.

What you suggest?

Kunal-I am not able understand of why MaxLife reduced the sum assured to Rs.1.04 Cr.

hello sir,

I want to invest my savings in SIP.Which SIP plans are good to make 50lakhs in 10 years.I can invest from 5k – 10k per month and can you tell me about equity ??

Sharmin-SIP is the way of investment but not a product. Also, your question needs lengthy guiding. Hence, request you to raise this in our Blog Forum.

Thank you for such an informative article. Really helped me in my decision.

I’m 27 and I am thinking of buying HDFC click2Protect Plus with a cover of 1 Cr and the Accidental Disability Rider.

However, you’ve mentioned “Never buy combo products, which offer riders or some death benefit payout options.” and “Buy accidental insurance separately from general insurance companies.” So, I just wanted to know if it’s wise to buy AD rider also or just the basic term plan. And in case, just the basic plan, could you kindly advise why you would not recommend AD rider with it?

Ankur-AD with rider will have lesser features. That’s why I recommend to buy it separately.

Alright. Thanks again! 🙂

Hi Basavaraj,

This is a great article for anyone who has no idea about Term insurance as it clears most of your doubts and queries related to term insurance. Going by your analysis or whatever I have read so far on other portals one thing is for sure that the fight/confusion/inclination is more towards either LIC or ICICI with Pros and Cons on both sides.

I am a 33 year old male who earns 10L p.a. and already investing 1.5 L a year in life insurance, accident insurance, medical insurance, ppf, etc. Now which of the following scenarios is most viable

1) Buy a term insurance (till 75 years) of say 1cr from LIC and have my wife and my child as the nominee – in this case for how many years will I have to pay annual premium amount, is it 42 years (75-33) or 35 years from now?

2) Buy individual term insurance of 50L each for me and my wife and have the other one as the nominee along with the child. This will cover us both for our given life terms and in turn our child as well. So does it makes sense to buy two individual policies of 50L? If my wife decides to leave her job then in that case I will anyways pay the premium for a 1cr policy (in reference to point 1). The only drawback here could be the rise in premium since we will go for individual 50 L policy rather than a single 1cr one

Please provide your expert guidance as my final decision rest on the resolution of these two queries.

Thanks,

Vishal Marathe

Vishal-1) It is 42 years.

2) If your wife is not an earning member, then LIFE INSURANCE is not required for her. You must treat individual’s requirement. The question here is whether Rs.1 Cr suffice or not. Decide and act.

1) so even after my retirement I will have to pay that amount?

2) So your are saying go with only one term plan rather than splitting them in half for me and my wife?

Vishal-1) As term ends, your premium payment stops there itself.

2) I am saying understand your requirement buy based on that. Understand your wife’s requirement and buy for her. Don’t say Rs.1 Cr insurance I need. Let me split between me and my wife.

Very informative article.

I have query regarding the term plan taking from two different insurance comapnies…

Is it advisable instead of taking one policy take 2 policies from different companies.

eg instead of taking one insurance policy of 1 Cr. from ICICI prulife should i take one policy of 50L from ICICI prulife and 50L from HDFC life.

Thanks & Regards,

Deepa

Deepa-Better to stick to one insurer. There is no logic in splitting.

Thanks to aware us regarding Term Insurance.

I am working in private sector while my wife is a govt employee. I am looking to buy a term insurance of Rs 50 lakh. Should i purchase term plan for both or is it better to have one term insurance policy. for whom should i buy term insurance . if we buy term insurance then why we need other accidental insurance ? whether term plan doesn’t cover it?

Pl suggest

Thanks & Regrds

Vaibhav

Vaibhav-You both are working and both of your income really affect each other’s financial life, then you both MUST buy a term insurance. Ideal coverage must be around 15-20 times of yearly income. Term insurance will come into picture when the insured person die. However, if you met with an accident and turn to be disability, then accidental insurance will come into picture.

Thank you very much for suggestion..

Did you write any post related to Accidental insurance. pl provide web link of same.

Vaibhav-Refer this post “Best Accidental Insurance Policy in India-How to choose them?“.

Dear Sir,

i asked to Kotak and ICICI for term plan …ICICI representative had suggested to add critical illness rider. But i am not going to add this as you suggested above.

Pl advise which company is best as there is no major difference in term of premium.

what should be the tenure for term plan? upto 60 yrs age or 70 yrs

Thanks & Best Regards

Vaibhav

Vaibhav-My choices are listed above. You have to restrict the tenure up to your retirement age.

Sir please suggest which mode is best to

how nominees should receive the payout

Lumpsum

regular income

increasing income

please revert

Vaibhav-The best option is to get the claim at once as lump sum.

Hi Sir,

I purchased a term plan from Kotak, Sum assured is 75 lakhs. As per your suggestion i have purchased it for 30 year i.e upto my retirement age. For above criteria premium is 6782 rs. and if I purchase it for 40 year means upto 70 years of my age then premium would be apprx 7700 per month. Sir Dont’t you think if i am paying 30 K + 77 K=1.07 lakhs extra to company than it would be more beneficial as there is more chances to die before 70 years and in this case our child would get benefit of Rs 75 lakh & I have to pay only 1.07 lakhs extra. This is my opinion.

I need expert (Your) advise.

Please suggest.

Best Regards

Vaibhav

Vaibhav-What if you buy it for 80 years of age (just an assumption)? Try to cover your risk but never try to benefit from term insurance.

Ok sir as per your opinion it is not good to increase tenure.

Sir can you please guide what is the loss if we increase the term.

I agree that we should try to cover risk but never try to benefit from term insurance. But if family member can avail benefits why we should avoid long term.

Can you write a short note.. I am still very confuse.

Vaibhav-Just calculate the value of your sum assured planning to buy with the term of 30-40 years with inflation of 6% (minimum). Then you will come to know the current high value of insurance so small during your retirement.

Hi sir

KOtak issued me policy withour any medical examination.

I asked to them for medical checkup then as per kotak there is no need of any medical.

Should i make any objection or is it ok

please advise

Regards

Vaibhav

Vaibhav-It is better to go with medical examination. If they say not required, then skip the insurer.

I have already paid my premium.. today i asked to kotak life insurance..

Kotak has already dispatched the policy document without any medical..

Now as per your suggestion i should cancel this policy..and select other insurer.

Vaibhav-You can cancel the policy even now too. Once you receive the policy document, then immediately cancel it (within 15 days free-look-in period).

Hi SIr,

Ok sir i will cancel it if they don’t agree for medical examination..

Sir what is disadvantage for customer if insurer issue their policy to customer without any medical examination..

Please revert.

Best Regards

Vaibhav

Vaibhav-They will have many reasons to reject claim based on health issue and non-disclosure of the same from you.

OK Sir,

Today i again discussed with KOTAK life insurance regarding Medical Examination but Kotak is not ready to do.

Then I discussed with Max life insurance for new term plan (in case of skipping KOTAK), they are also saying same that it is not necessary to do medical examination and Max also can’t commit regarding medical examination. It seems they will also not do Medical if i will go with Max.

Kindly suggest what should i do..

You above stated that IRDA amended the Section 45 of insurance act. According to this, if the policy continued for 3 years or more, then insurance companies cannot reject the claim. then why should we worry if insure doesn’t do medical examination.

Please revert.

Best Regards

Vaibhav

Vaibhav-You no need to worry. But still be in safety net 🙂

🙂

Now what is your opinion?

Skip the KOTAK or contniue

but in case of skipping, which company will commit that they will provide Term insurance after Medical only.

Please guide sir.. Now i have limited time for cancellation of policy.

Thanks & Regards

Vaibhav

Vaibhav-I am not saying to skip. But I am saying it is SAFE to buy with medical examination. You can check with other insurers by calling them directly and providing details like your income, age, sum assured you are going for and term. If they are ready to issue with medical examination, then go ahead. Not a big issue.

Dear basavaraj

I am 47, non smoker, wants to buy term insurance which I never thought till I read your blog.

Employed in private firm.I know I am late but still can I buy considering my age?.

I am bit confused when I check online, I want for 10 year(premium payments) but it shows 60 years, does that mean even if I pay for ten year term, the policy will be in force until 60yrs. age? Some web sites show more than that.

Kindly clarify.

Appreciate your guidance.

Saleem-There is the difference between premium payment term to policy term. Please check it with the particular product you want to buy. For example, if the premium paying term is 10 years and policy term is 30 years means you have to pay the premium only for 10 years. After that you no need to pay anything. However, policy will be for 30 years term and feature will continue till 30 years of term. Hope you got clarity now.

A big Than Q Basu sir……

Hello

I am 33 years old. I have Birla Sunlife Protector Plan for 2600000 which increases Sum Assured by 10% every year for 30 year plan. I pay around 13000 per year as premium. I have paid the premium for 3 years. Last time I purchased the plan I bought it as there was some rider benefits. Am I paying high premium for the sum assured of Rs. 3500000. Please advise if I should opt out and buy ICICI term insurance plan with higher sum assured for the same premium I pay.

Vinay-If you feel the heat of premium, then you can switch. But make sure that you have policy issued in your hand by ICICI, then cancel Birla insurance.

Hello Basavaraj

Thanks for the reply. What is your whole opinion on the Birla Sunlife Protector Plan I have right now. Is it a good product where in the Sum assured increases by 10% every year while the premium remains the same. But the negative side of this the sum assured is not great multiple of my current annual income. Am I paying high premium for the low sum assured.

Vinay-The catch here is the yearly 10% increase in term insurance coverage is already factored in your premium, which you are feeling that they are increasing the cover without extra premium. If you feel you are underinsured, then you must increase.

Hi Basavaraj,

I am 33 year old and non smoker and I am confused to choose best term plan for my self.

I am confused in between Lic eterm plan, icici an hdfc. Please suggest ..which on is best for me.

Rohit-To be all 3 are best. But check your budget and decide.

Hi Basavaraj,

Thanks Basavaraj, for qucik reply.

I think , I can afford icici and hdfc now. So I Should take accidental benifts, it will helpfull or not. And one more thing, I should two term plan with different companies, one for long periods and second for less period. Or form one company only.

Please suggest.

Thanks

Rohit

Rohit-Then go with either of the one. Yes, accidental insurance is must, but don’t combine this with life insurance as rider. Buy separately. Why one for longer period and one lesser period?

Hi,