Which are the Top 5 Best Health Insurance Plans in India 2020? How to shortlist and what the cares you have to take care of before buying the plans? Let us do the review and comparison.

Along with Life Insurance (Term Life Insurance), Health Insurance is also a must product one must-have. While in the case of Life Insurance, you have to buy it only if you have financial dependents. , However, this is not the case with health insurance. All of us have to buy as we don’t know when we get hospitalized due to illness.

An exception to this is, if you created enough corpus for your hospitalization need, then you may not need to buy health insurance. But many of us simply ignore the hospitalization cost in our life. Even salaried not worry about buying separate health insurance (even though company providing).

Cost of hospitalization as per my understanding inching up at the rate of 10%. Hence, in many cases, it is impossible to fund the hospitalization expenses from our own savings. A week’s hospitalization in expensive cities like Bangalore may ruin your few years of savings. Hence, one must take it as a serious need and buy it.

Top 5 Best Health Insurance Plans in India 2020 – Checklist

Before jumping into shortlisting your Top 5 Best Health Insurance Plans in India 2019, you must understand what are the points you have to consider.

Before jumping into shortlisting your Top 5 Best Health Insurance Plans in India 2020, you must understand what are the points you have to consider.

# Sum Insured: When you look at the rate of inflation of hospitalization, you find that it is nearly around 8% to 10%. Hence, always try to go for a sufficient sum insured health insurance base plan. Consider the members you are including in the policy. Based on that you have to take a call on the sum insured you are opting.

# Daycare Treatment: Choose the product which offers the highest daycare treatment coverage. A few years back, to treat a few diseases, we need to get hospitalized for 2-3 days. However, due to advancements in medical technology, nowadays many treatments are converted into daycare treatments. Hence, it is important to understand how many daycare treatments the health insurance product covers.

# Room Rent Capping:-Nowadays many health insurance companies offering NO ROOM RENT CAPPING. You have to choose a product where there is no such capping.

# Definition of Hospital: Many of us ignore this important aspect that what is the definition of the hospital as per the health insurance company. There may be certain eligibility to consider which is a hospital. Hence, if you admitted to such an undefined hospital, then health insurance companies may deny the claim. For example, refer to THIS about what is the meaning of the hospital as per New India Mediclaim Policy.

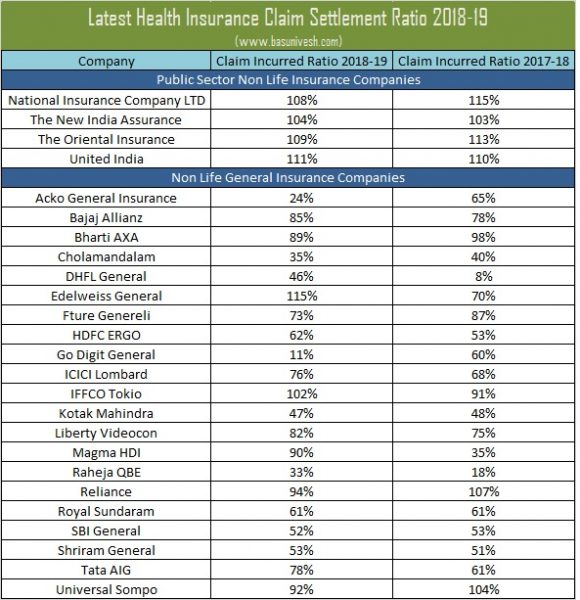

# Incurred Claim Ratio: You have to check the incurred claim ratio of Health Insurance Companies. Incurred Claim Ratio or ICR is a ratio of the total value of claims paid or settled to the total premium collected in any given year. This can be calculated as an Incurred Claim Ratio or ICR=(Total Value of Claims Paid/Total Premiums collected)*100.

For example, let us say Company ABC settled the total claim amount of Rs.90 Cr in the year 2015-16. In the same year, it collected Rs.100 Cr as a total premium. In this situation, the incurred ratio stands to be 90%.

This Incurred Claim Ratio is applicable only to non-life insurance companies. For life insurance companies, IRDA publishes Claim Settlement Ratio. But sadly many (even experts) complicate it.

If the incurred claim ratio of a company is more than 100%, then it indicates that for every Rs.100 they collecting as premium, they are paying more than Rs.100 as a claim for a year. In simple terms, your income is Rs.100 but your expenses are Rs.100 or more. So instead of profit, they are into a loss.

If the incurred claim ratio of a company is less than 100%, then it indicates that for every Rs.100 they collecting as premium, they are paying less than Rs.100 as a claim for a year. Such companies are making a profit as your income is Rs.100 but expenses are less than Rs.100.

However, rejecting claims only on grounds to profit will not work out for any company. They have to look for reputation, future growth, and regular guidelines. Hence, simply for the sake of profit-making, they can’t deny claims.

In my view, going with companies of high ICR or low ICR is risky. Hence, always choose a company which is in between both these points.

Do remember that Claim Settlement Ratio or CSR applies to Life Insurance products and Incurred Claim Settlement Ratio applies to Health Insurance Products.

Let us now look at the latest Incurred Ratio of all Health Insurance Companies. Below is the incurred claim settlement ratio of Public Sector and Private Sector Companies.

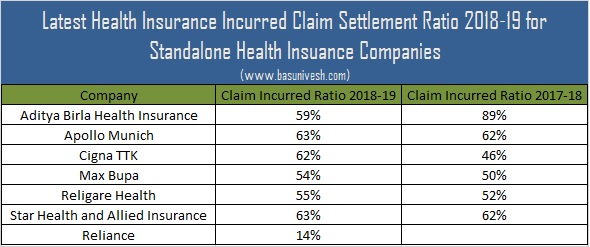

Below is the incurred claim settlement ratio of standalone health insurance companies.

# Buy early: Buying at an earlier age is the best than postponing it. We don’t know the health issues. Hence, the insurer may reject your proposal. Hence, always buy immediately and never postpone.

# Understand the cover: Identify the features you want to cover. Covering all NOT POSSIBLE. Hence, try to identify the product which covers many illnesses.

#Individual or Family Floater: Decide whether you want to go for an individual or family floater. It is always best to go for an individual if the age of any one member of the family is so high than the others. For example, in a family of 4 the oldest person’s age is 65 years and the rest of the other 3 members age is less than 50 years, then better to buy an individual plan for that 65 years old individual, and rest 3 members can buy a family floater.

Because the premium is fixed based on the age of the oldest person also.

# Entry Age and renewable clause: Check the entry age and for how long one can renew it. Currently, many insurers are offering life long renewal options. Hence, choose the one where you have the option to renew it forever.

# Waiting period: Identify the company which covers existing diseases early. Usually, all insurance companies have a waiting period of 3-4 years for existing diseases. However, if your concern is to cover the existing diseases, then give first priority to this point.

# Co-payment clause: Higher the co-payment means lower the premium for you. Co-payment means how much you also have to pay in a total bill. If the co-payment clause states 20% co-payment, then for all bills claimed, you have to 20% and the rest 80% will be payable by a health insurance company.

# Exclusions: Check for exclusions. If you feel the exclusions listed may be uncomfortable to you, then skip that product.

#Hospital Network: Check for hospital network availability in your city or town. The cashless hospital benefit is better than producing the bills and waiting for claim settlement.

# Policy Wordings: Read carefully the wordings of policy brochure. If you have doubts about any feature, then try to clarify it NOW itself.

# Common Features: Avoid all common features, which companies try to highlight.

# No Claim Bonus Offers: Check for No Claim Bonus company offers.

# Treatment wise limit: Check treatment wise limit if any.

# Premium: Check the premium rates. Especially check the rates for older age rates as few insurers jump the rate drastically for older age coverage.

# Super Top Up: Never rely on a base plan. Down the line, if your coverage is not sufficient, then go for Super Top Up Plans. They are cheap in nature compared to base plans. Make sure that your base plan and Super Top Up yearly renewal date should be almost close. There should not be a big gap in the dates between these two plans.

# Cashless is a facility, not a GUARANTEED feature:-It is just a facility to make sure hassle-free claim settlement. Hence, don’t think that this is your RIGHT.

Top 5 Best Health Insurance Plans in India 2020

Now let us jump into selecting the Top 5 Best Health Insurance Plans in India 2020 among those so many Health Insurance providers.

Here, my concentration is mainly on Day Care Treatments, Room Rent/ICU limit, Claim Incurred Ratio, and few basic features. Based on that I have selected the below products.

Note:-Refer our latest post on Top 5 Super Top Up Posts In India for 2020 at “Top 5 Super Top-up Health Insurance Plans in India 2020“.

Disclaimer:- Health Insurance actually depends on your age, family size, health status, and the particular feature you are looking for. Hence, my choice is based on certain generic considerations. It is always best to cross-check the product brochure before you jump into buying.

Also, I am not claiming that these are the ONLY BEST in India. If certain features are not suitable for you, then you can look for other products available in the market (but considering the above points which I have discussed).

Hope this article will help you in choosing the right health insurance for you or shortlisting the Top 5 Best Health Insurance Plans in India 2020.

Refer our latest posts:-

- The Dark Side of Compounding: How 2% Kills Rs.30 Lakh

- Flexi Cap Funds: Why Your 10-Year Return Chart Is Lying

- EPF Scheme 2026: EPF, EPS and EDLI Rules Explained Fully

- Financial Freedom Without Health? You’ll Regret It Later

- The Peltzman Effect: Why Playing It Safe Can Make You Poor

- Your Retirement Success Depends on Luck, Not Skill

Hi Basu sir,

I follow your blogs regularly and i have taken term insurances based on your blogs.

1. Any chances you will be writing blog on health insurances for 2024.?

2. I need a suggestion sir, For my parents aged 70 and 78 I am confused between niva bupa or star.

3. For self and my family (ages 40, 35 and 13) confused between HDFC ergo, Niva Bupa or star.

We all are having corporate group insurance planning to buy outside slowly come out this.

Can you guide or suggest as you do eveytime please.

Dear Satish,

1) Sure will write.

2) Better to avoid both and stick to old players like ICICI or HDFC or PSUs.

3) Better to go with HDFC or Niva.

Hello Basu,

Are there any good health insurance for my 7-yrs old autistic daughter?

Thanks for your reply.

Raja

Dear Raja,

I am unsure of such specific cover. But try with the same insruance companies which I have listed above.

Basu.

Sorry.

I was talking about 80DD.

M i eligible?

Dear Rekha,

Under Section 80DD, the major conditions are as below.

1) Dependent means – Spouse, Children, parents, brothers, and sister of the individual.

2) Such dependent should be disabled a person. Disability means – a disability of not less than 40%.

If both above conditions are satisfied, then you can.

HELLO BASU,

I’M Married , government salaried women… Because insufficient salary of my husband, i am paying expenses occurred on medical condition of my father and mother in since last FY.

M i eligible to claim those medical expenses occurred in my ITR u/s 80D?

Dear Rekha,

Medical expenses can’t be claimed under Sec.80D as it is meant for insurance premiums.

Dear Sir,

I needed one clarification from your end .

what is the catch of “Single Pvt room” capping ? Like Star health policy mentioned in that their policy wording.

Dear Venkat,

It means that if you opt for a single private room, then there may be a certain limit to it.

Waiting for your detailed review sir

Dear Sumanth,

Sure.

Dear Sir,

Thanks for the reply.

Can I also request you to confirm the ideal Sum Insured for general public (not high networth). As it is recommended to take Super tops with health insurance and most of the Super Top ups have a deductible maximum of 5 Lakhs. So, does that mean is it enough to take 5 Lakhs SI and then a Super top-up? Will Super top have the policy coverage as base policy when taken from same insurer or will it have its own policy T&Cs. Will super top-ups be cashless when base policy is also from same provider ?

If Super top-ups have the same policy terms as base policy then it makes sense to go with 5 lakhs SI. But again why would an insurance lose business by explicitly selling Super top ups with only max deductible of 5 lakhs (i have only investigated HDFC & ICICI).

Initially I was planning to take 10 Lakhs SI and then a super top-up but all the Super tops from HDFC and ICICI have deductible max of 5 lakhs. So, does it make sense to go for high SI when taking a Super top-up

Dear Sumanth,

Ideally around Rs.5 lakh base plan is fine with super top up of at least Rs.25 lakh. Yes, majority of super top ups offer the same features which the base plan offers.

Can you please compare HDFC Ergo Optima Restore vs Optima Secure. Optima Secure has double the benefits of restore for same or a slight increase in premium. HDFC secure has the below add-ons in comparison with restore and these are lucrative benefits

1) Protect benefit – Complete non medical expenses (68 listed in policy) are covered [Ex: gloves, masks, pads etc which a general insurance will not cover

2) Secure Benefit – 100% on SI on buying or renewal (10 lakhs cover becomes 20 lakhs by default). Applied every year and no carry over.

3) Plus Benefit – On Renewal without a break, 50% of the Base Sum Insured under the expiring Policy will be added to the Sum Insured subject to max of 100% of SI. Any amount unutilized in the current Policy Year will be carried forward to the subsequent Policy Year

(Again 10 Lakhs cover becomes 15 lakhs by 1st year and 20 lakhs by 2nd year renewal). No strings attached and even if insured claims in previous year

3) Restore Benefit – Instant addition of 100% Basic Sum Insured on complete or partial utilization of Your existing Policy Sum Insured during the Policy Year (irrespective of any benefits used). The Total Basic sum insured will be restored only once to all Insured Persons for all claims under In-patient Benefit during the current Policy Year.

4) NCB – 10% of SI for no claims in previous years (this is 50% in Optima restore but hardly makes a difference with above benefits which are more permanent in nature as once claim is made that 50% is reduced)

5) Ayush Benefits (not in Optima Restore)

6) No sublimit

With all these benefits as 10 Lakhs SI is worth below

SI – 10 Lakhs

Secure Benefit – 10 Lakhs

Plus Benefit (after 2 years) – 10 Lakhs (carry over unutilized if claims made)

Restore benefit – 10 Lakhs

Total = SI + Secure + Plus+ Restore = 10 + 10 + 10 + 10 = 40 Lakhs (for premium of 10 Lakhs ??)

I have read the policy document comparing with optima restore. So what is the catch here ? Am I missing anything and the policy is too good to buy and I do not find any such policy in market. Am i missing anything.

Please help decide as you would also not need a super top off with this policy. What would be the use of top-up for this policy ? As we are getting 40 Lakhs for 10 Lakhs premium (not much higher than other policies having 10 lakhs SI just 10% increase)

Also, will super top have the same coverage as base policy ?

Dear Sumanth,

Let me write a detailed post on this.

Sir, HDFC Ergo Optima Restore Vs Optima Secure – looks like HDFC came up with new health insurance policy – Optima Secure. Which one is best among these two? Kindly advise..

Dear Babu,

Yes, Optima Secure is eye-catching with some gimmicks. You can opt that.

Sir,would you like to write a post on small case? There are lot of advertisements happening around smallcase. Fees seem to be bit high.

Your opinion is highly appreciated.

Thanks

A Banerjee

Dear Banerjee,

I am not an expert in direct stock reviewing. However, avoid anything which costs you a lot and creating NOISE.

Dear Sir,

Is it required to declare fresh illness during renewals of health policies ?

Dear Amartya,

No, not required.

Dear Sir,

I’ve a Bandhan Bank Group health Insurance by HDFC Ergo. I wrote few PED in the application form, but they they didn’t mark any PED in the policy. Though in the policy document the photocopy of the form is there. Few good thing s about the policy is there were only two premium slabs under 45 and a 45plus (when I purchased it from Apollo Munich, going forward this may change I guess). Also there is no room rent capping.

Shall I continue this existing policy or get some other policy ?

Dear Banerjee,

If a photocopy of the policy showing your filled PED details, then no need to worry.

Sir, give some valuable inputs regarding newly introduced Maxbupa reassure plan. Actually, i am planning to buy the HDFC ERGO optima restore but this reassure policy really catching my eyes with unlimited restoration benefits . Your thoughts please.

Dear Arijit,

You can go ahead.

I am 41 years old. I need a mediclaim for me, my wife whose age is 36 years old and she is Diabetic for last 2 years and my one son whose age is 4 years and also a separate policy for my mother whose age is 61 years. Need a mediclaim of Rs 5 lakhs for me, my wife and my Son and needs Rs 3.00 Lakh mediclaim for my mother separately. My mother is physically fit. Please suggest which companys mediclaim to take.

Dear Pradeep,

Refer the above post.

Hi Sir,

I have new india floater mediclaim policy. Sum assured: 12Lakhs, TPA – HITPA. I am single (age 28) and I have my mother (age 58 no pre-existing diseases like BP and Diabetes) and myself covered under the policy. I was earlier covered under New india assurance – TCS group health insurance. I ported it to new india floater mediclaim policy last year as I switched from TCS to Infosys. My policy renewal will be in April 2021. I have 4L free of cost health insurance provided for me (my wife and children in future) by my current employer.

Should I convert my family floater to individual cover(individual policies for me and mom)? Last year premium was 34K. Opting for individual covers will reduce the premium?

My father who died 2 years back was covered under my earlier TCS policy, I had good experience during his hospitalization but the TPA was Mediassist. Do I have to worry about TPA change?

Can you please provide details about what is comprehensive insurance? I have been hearing comprehensive insurance is best even though premium is higher.

Dear Rajnesh,

Buy separate health insurance for you and your mother. Don’t buy as a family. Comprehensive means having lot of features as per the INSURANCE COMPANY 🙂

Hi Sir,

I enquired with new India assurance , they are not allowing to convert to individual cover. What can i do?

Dear Rajnesh,

In that case, better to have your own base and super top up.

Sorry sir, I am not clear. Are you asking me to reduce my family floater Sum insured amount and take a super top up plan? Can you tell me super top up plan name from New India assurance?

Dear Rajnesh,

I am not saying you to reduce your family floater. But insisting you to go for super top up.

Thank you for the clarification sir. I enquired with New india assurance and they don’t have a super top up plan. Shall I take super top up from another insurance provider and keep this base cover?

Dear Rajnesh,

Yes, you have no option but to take it from different insurance company.

Hello Rajnesh,

This is completely off-topic, but curious to know how to do TCS group policy to individual? I am also on the same boat.

You can contact mediassist, they will provide you contact number of new india assurance person. You have to provide TCS policy details to new india assurance along with a letter from HR. You can port only within 30 days from last day in TCS. If possible take screenshot of the policy details from tcs mediassist portal.

sir

Can you tel som insurance cover for fertility frequently & pregnacy

Dear karthica,

If you are employed, then many group insurance cover this cost. I don’t think you have to buy a special one for such costs.

sir

not employed .

kindly advise .

Dear Karthica,

You can check with HDFC ERGO Easy Health Family Floater.

Dear Basavaraj,

I am looking for your expert advice on choosing right health insurance plans for my family. I am searching fr a health insurance plan for my family( me+wife+one son + mother (69 years)) . I am currently having my company insurance covered everybody of sum insured 15 lakhs. Can you please advice me which plan would be sufficient for me and how to select super top up plan

Dear Nikhil,

For your family (You, Spouse and kids), you can refer the above post. For your mother, suggest you to buy from PSU Insurers.

Thanks . Can you please advice if super top up plan need to be added for my family

Dear Nikhil,

Yes, ideally one must have around Rs.5 lakh base plan and around Rs.25 lakh Super Top Up with a deductible equal to base plan.

can the base plan and super top up plan be taken from same company or different one ? DO you have your article for PSU insurer top list ?

Dear Nikhil,

Better both base plan and super top up plan from the same company. No, I have not written a post on PSUs.

Hello sir,

Thanks for the blog,

How is some of the companies are offering 1crore health insurance with same or similar premium, like Aditya birla , Religare and Max. Can you please write on this

Dear Dileep,

It is their decision to offer based on their actuaries or business module. It is hard to judge why they are cheap or costly.

My mom who is 57 yr old have iffko Tokio individual health insurance policy since 3 yrs(without any claim).1)Can I switch to maxbupa policy???( since iffko Tokio customer care service is very pathetic)

2)Does she has to undergo medical checkup while buying makeup?

Dear Anand,

If you have such a huge issue with the current insurer, then switch. However, yes once you move to MaxBupa, they may ask for a medical examination due to her age factor.

Hi ,

Just i have taken a health insurance family floater for 4 members from Axis -TataAIG named group medicare for 10lakhs with premium 18500.

Anybody has any idea about this insurer, how is teh policy.

please suggest as my free lookup period is under progress,.

Dear Bina,

It is a group policy, not a family floater policy. If the tie-up with the bank over, then you left with no insurance. Better you check with the health insurer that whether you can port it to family floater if the tie-up of bank and insurer ends.

and sadly I can’t even port or stop this insurance…as buying another insurance seems impossible at this point for him (borderline diabetes/heart patient) 🙁 would buying a new policy with a public limited company make sense at this point?

Sir, please share your valuable comments on Union Health Surksha by Union Bank Marketed by Religare one should buy it or not as premium is very less and with no health checkup.

Dear Sanjeev,

Better you buy on your own than the insurance offered by banks.

HI Basavaraj Garu,

My age is 35 now, Health family floater plan is needed for 2 adults – (Me & wife) + 2 kids – (son & daughter). I am looking for policy of Rs. 7.5 lacs to 10 lacs.

I have a big confusion in choosing the Family floater health insurance in between HDFC Optima Restore, Max Buppa Health Companion & ICICI ihealth protect…

I have finalized above three but unable to choose one. Please suggest me which one i have to go with. (Please don’t say all are good).

Thank You

I was in the same situation.

I bought one for me and one son from hdfc and wife and 2nd son from max bupa.

Dear Sir,

Indeed a very informative blog with crisp, to the point articles. I ended up reading scores of articles over a few days!!!

Sir, in the top 5 mentioned health insurance plans none are from the public sector or standalone health insurance companies.

Can you please suggest what are the pros and cons, in general, between the public, private and standalone health insurance companies? One observation is the private players offer many more benefits at relatively lesser premiums. Are, we as end users, safe in the long run in-case the private companies somehow collapse?

Dear Puneet,

Don’t generalize in that sense. All are EQUALLY GOOD AND BAD. You have to choose the product which is BEST suitable for YOU.

Dear Sir,

If the health insurance policy has Restoration of 100% Sum Insured benefit and if Super Top-up policy is also taken then how will this work?

Example –

Case (1) Base Cover 5L with Restoration of 100% Sum Insured benefit i.e. 5L + 5L. Super Top-up of 5L with 5L Deductible

Case (2) Base Cover 5L with Restoration of 100% Sum Insured benefit i.e. 5L + 5L. Super Top-up of 5L with 10L Deductible

Dear Puneet,

It all depends on the deductible.

Dear Sir,

I have taken Religare for my father in 2016 and as he’s a diabetic and a heart patient for over two years now due to which I couldn’t port the plan from religare to Star/Max Bupa. Not sure I can still port to any public or pvt insurance for him? Please advise. As of now, I also have the employer insurance cover for my parents. But I would like to also purchase a stand alone plan for my mother (age 57) and myself (age 37) – what do you suggest? Should I go with individual or group policy with a pvt/public company?

Thank you so much for your guidance!

Dear Isha,

Considering your father’s health status, I suggest you to continue the same policy. Regarding you and your mother, better to buy it separately.

thank you Sir… do you suggest pvt or public for mom? I have employer insurance and it is from United India… I can probbaly go with a pvt company for myself between the top 5 suggested by you…

Thanks much

Isha

Dear Isha,

For your mother, I suggest public sector companies and for your requirement, private sector.

Hello Sir,

thank you! I got to know that Religare has now increased premiums for all policies citing increase in services/treatments on the Care plan. I have been paying almost 27K/per year since 2016 along with underwriting charges (for Dad’s borderline diabetes) and this year they have increased it to almost 29k 🙁 is this even allowed or the right thing to do by companies?

regards

Isha

Dear Isha,

They can increase the premium and sadly you can’t question it. Only load based increase was not possible.

thank you Sir…it’s sad we cannot do anything about such random increase in premiums…:(

Hello..

Thank you for your reviews..

I was comparing HDFC ERGO Optima restore and STAR heath comprehensive policy..

Both have almost similar features..However premium for Star Health policy is less across most individual as well as family floater policies..

1. So I wanted to know your opinion on Star Health Comprehensive Insurance policy..

2. Also wanted to know any specific reason for not including it in your top 5 list..

3. These policies have plans of 25, 50 lacs..The premium are proportionally reasonable..So is it good to take such large sum policy ?

Thanks in advance..

( I want to buy a family floater plan with amount of about 25 or 50 lacs)

Your articles are really helpful always

Dear Dhaval,

If you are concentrating on premium then you can go ahead. But check for the checklist points I shared before jumping.

Sir

How is Digit Health insurance? It provides coverage for mental illness as well as for Alzheimer’s, Dementia,etc. This is a compulsory exclusion in all the five insurance companies recommended above (as on date) and in most of other companies also, What is your opinion about digit health insurance

With regards

Satheesh Rao

Dear Satheesh,

I hardly trust the new entrant.

Great Article sir. Cleared many of my doubts – shortlisted HDFC Ergo/ICICI/MaxB.

I would like to have some clarifications please…

1) Does any of the listed policy have wellness program? If so what are those benifits?

2) Do they reimburse amounts if we sumbit bills such as that we spend on Gym/year? If so what is the limit and any conditions like can be claimed only with their tie-up associates?

Dear Saravana,

1) These are insurance products not wellness products. Please stay away from such products even if someone is offering you.

2) Great…I think you are expecting too much from health insurance 🙂

Not my expectation, but informed. I just came here for confirmation. Thank you 🙂

Dear Saravana,

Don’t rely on hearsay. Check the policy document or product details.

Dear Sir

In your last years list Religare Care appeared. It is mentioned that due to certain management issues you have dropped Care. I have the Religare Care policy maintained for last six years without a claim. Is it prudent to port it to Max Bupa / royal sundaram. kindly advise me

With regards

Satheesh Rao

Dear Satheesh,

Better to port.

Dear Basunivesh

Firstly thanks a lot for this valuable information.

Please help me understand the latest max Bupa 1cr policy. I am not sure on why this is coming with very less premium for so much of sum assured.

Does this policy has one crore sum assured or does this plan has built in top up plan?

Please advise if we should such types.

Thank you.

Dear Rajani,

This policy is a Super Top Up health insurance but not a normal health insurance. The risk usually starts from a certain amount to 95 lakh. Hence, they are cheap. For a better understanding of that product, refer my latest post “Top 5 Super Top-up Health Insurance Plans in India 2020“

Dear Basavaraj

Thank you for the reply.

In that case, I understand it would be better not to have a clubbed policy (regular plus top up) and buy separately a top up or super top up as needed. I mean it would not be a good option to buy Max Bupa 1 cr policy which includes both. Kindly advise.

Dear Rajani,

You have to buy separately as base and super top up.

Dear Sir,

Thank you for this guide. I had a few queries.

1) Do you have a preference between HDFC Ergo Optima Restore and ICICI Lombard Complete Health Insurance?

2) Does HDFC Ergo My Suraksha Silver differ from Optima Restore?

3) Do you suggest a women-specific policy for female family members? What is your opinion on such policies such as my:health Women Suraksha Essential plan?

Thank you.

Dear Kenneth,

1) Both are good products.

2) Yes, slightly in features.

3) I usually not suggest it.

Basu Sir,

I was in a Tier 1 company for past 14 years, and no planning to move into a more Niche skill based start up. That means I am forced to take up a Cover on my own (vs previous company sponsored one for 5 Lakhs). So, as usual I came to your blogs for an easy summary and hassle free pick up. Thanks for all your blogs which always helps us to save our time spend on analysis. Keep up your good work. This is very helpful for people like us.

1) How different is Health insurances when compared to mediclaim (Or both are same) ?

(Kindly ignore the below question if Health Insurance and Mediclaim are one and the same).

2) As I prefer to have a 5 Lakh coverage similar to my previous employer (they term it as Medical Benefits), would you suggest to go with one of the 5 Health insurance companies you suggested (or to a Mediclaim policy if both are different to retain same kind of coverage that my previous employer provided).

Dear Balaji,

1) Let me write a detailed post on this.

2) Yes, go with the above suggested.

Thank you Basu sir. Recently came to know that ICICI has a group health care for all its customers from Lombard. Which has all coverage similar to ICICI Complete. But has an 10% discount rate as it is a Group coverage. Can you suggest if I can opt Group policy instead of Complete ? Or would there be any catch being Group policy?

Dear Balaji,

Better to stay away from such luring products and discounts.

Sir, thanks for the insights. I was thinking of buying a plan, either Religare NCB Super or ICICI LOMBARD. Which one to select as Religare plan seems to have more benefits with 150% NCB. Also I will buy the Super top up from ICICI as it is better priced. Please suggest!

Dear Abhishek,

I suggest ICICI over Religare.

Hi sir & other blog readers,

We often face claim rejection from our health insurance provider. Here is pdf which contains few cases which went upto ombudsman level .

The idea here is to prevent us from NON Disclosure of information.

This is weapon that i found insurance companies are using to deny the claim.

I hereby urge all readers to read the pdf and basu sir to throw light on this. May be by writing a article

The pdf is available at below link ( insurance ombudsman) website:

http://ecoi.co.in/GIC/mediclaim/Individual%20Mediclaim%20-Gen27.pdf

http://www.ecoi.co.in/GIC/mediclaim/Individual%20Mediclaim%20-%20General26.pdf

Hope this document will help people know about the clauses and they become much serious about the declaration on form and not leave form filling to agents or executives who blindly tick NO to all medical questions …

Thanks,

Will post more links as i get.

Dear Vinay,

Thanks for sharing this vital information. That is the reason, understanding the features in detail is very much important.

Thanks Sir

Yes indeed understanding the features in detail is of utmost importance.

Hi Basavraj,

I am Planning to Take the Health Insurance for my Family. Can you please suggest Plans as per y requirement.

Star Comprehensive

HDFC Optima Restore

Max Bupa Companion

ICICI Lombard General Insurance

Nations Insurance

(Any Government Insurance Preferred)

On the Below Basis I am analyzing the Policies:

Quick Claim

No Co Pay and Private AC Room

Should I Take Individual or Family Floater

Dear Ravi,

My choices are already mentioned above.

I am having apollo munich /hdfc ergo optima restore plan for me and my husband with a coverage of 10 lacs. Now I want to switch to max bupa. Which health plan of max bupa will be good for two adult and one child? Should we increase sum assured amount? Kindly advice as I had chosen the term plan based on your advice.

Hi

i read almost all of your articles and found this very informative.

I had few questions.

Suppose i have hdfc ergo 2 lakhs policy ( group ) from company. In this scenario if i take HDFC ergo 3 lakh base( individual) plus 7 lakh super top (Family floater) ..would it be wise choice,?

or should i buy super top from company other than HDFC ergo to diversify the risk of claim rejection.?

in case of claim i heard group policy should be used first ad then personal policy . In this case since all is with ERGo it will be fine.

But in case i changed my company and lets say my insurer is icici lombard (group). How will this process work if i go for claim on group policy first and then Personal policy with HDFC ergo 3 lakh base( individual) plus 7 lakh super top (Family floater) ..

please advise.

Dear Vinay,

I usually suggest both base and super top up should be within the same company to avoid procedural difficulties. You can’t control your employer and their choice. But you can control your choice of being within the same company health insurance. Hence, control what you can.

Thank you sir for reply…

I am planning to go with HDFC Ergo with base and super top up plan from HDfC ergo as per above list.

I will probably go for 5 lakh base plus 15 lakhs super topup (still exploring) ..considering the medical inflation in years to come.

Can you please suggest :

1. How much amount of base + super top up cover should i opt for considering inflation and rising medical cost in years to come. ?

2. Shall i opt for critical illness policy in Health insurance itself or preferably take it as a rider (25 lakhs) in term plan ( I am planning to take max life term 1 cr after reading your article) … I already have aegon life 1 cr term cover ..

3. Considering above planning , i assume that base+ super top up plan will help me cover medical cost and inflation …Meanwhile 25 lakhs critical illness plan along with term insurance will be buffer for any unforeseen circumstances (both medically and otherwise)

Please advise ..

Thanks

Dear Vinay,

1) Ideally around Rs.5 lakh base plan and up to Rs.25 lakh super top.

2) Yes, you can but separately.

3) Yes.

Thank you sir…

i must say your blog is must read for all information before buying any policy (health or life).

I have already shared your blog with my friends ..

This blog should be probably in top searches when someone searches for health and life insurance .

Keep sharing knowledge !!

Dear Vinay,

Pleasure 🙂

Hello Sir,

I am single as of now and planning to get married in next 6 months. Kindly suggest, if I should buy individual health insurance now or family floater after 6 months.

Secondly is there an impact on premium of (individual policy + addition of one more member) vs family floater for 2 member. Kindly guide. Thanks

Dear Abishai,

If you are covered for these 6 months, then better to wait for your marriage. Otherwise, buy now. Yes, suggest you to go for family floater than an individual.

Unfortunately I am not covered hence a bit critical to ask.

Can you answer the later part of question also with some numbers if possible as it will help me in taking a decision?

Dear Abishai,

If you are not covered, then better buy an individual policy immediately. Once you get married, then you can add your spouse by converting the same into family floater. When you add a member to your individual plan, then it is no more considered as individual plan but a family floater.

Sir, I have a Health Insurance policy Religare Care for me and my wife for Rs.10 Lakh since 2016. 1. Can I continue with the same or should I port it to some other company? 2. Is it possible to port to some other compnay? 3. Can I shift to Arogya Sanjeevani in the same company i.e; Religare for Rs.5 Lakh?

Dear Vasavan,

Better to port.

Sir, Can you please suggest some companies to which I can port in the order of preference?

Dear Vasavan,

I have already mentioned in the above post.

Hi Basu,

A big fan since many many years of your blogs. They have helped me to learn and judge in picking up products.

Ques 1) I am looking for a health insurance for my father aged 66 yrs. I see you have been supporting PSU for this. Any reason I should prefer PSU over HDFC Ergo Or ICICI?

PSU’s have capped limit on most of the services, then how is it beneficial?

Ques 2) For my mother aged 56 she has been with Religare Care, but I do not seem to like now as there is a copay clause and growing premiums. Would you suggest moving to HDFC ergo or ICICI or PSU considering I am looking peace of mind if and when required?

Thanks!

Dear Vivek,

1) Generosity in claim settlement than private players. However, if the offering of sum insured is not sufficient, then you can look for the products like Star.

2) Better to move to PSU.

I came across Max Bupa’s 1Cr Super Saver plan which has the premium equal to insurance premium of 15-20lakhs. Is there any loophole there? Looks too good to be true. Any idea?

Dear Rahul,

The Sum Insured is Rs.1 Cr. Don’t go for any fancy features. Look for the basics which I shared above.

Hi Basavraj,

I have been detected with Ankylosing Spondylitis (auto immune condition) which is under control from past 1.5 years, have applied for various prominent companies for health insurance but all were rejected.

I am 29 years old and married.

Could you guide for companies/plan which provide health insurance to us? As i have faced too many rejections.

Dear Amit,

It is hard to say that you go with this company and they accept it. It is at the end of the day left with insurance companies.

I am thinking of going for National & New India Assurance plans, it has certain limitation but they might accept my proposal.

Do you have any information about PSU General insurance company feedback?

Dear Amit,

Obviously they are bit liberal than private players.

Dear Basu,

Though the possiblity is not high,. its better OK to have cover when some insurance is available to get it covered.. I need your suggection on the crediblity of that insurance company since it is not familiar as such.. thanks..

Dear Rajiv,

I usually go with established companies. You may feel I am biased. However, I always look for stability.

Dear Basu,

Thanks for the very informative details on health insurace . I have question on stand alone cancer plan provided by Future Generali which covers baby from 1 year where no other company have such product for kids on cancer coverage. Since you mention go with established one , i need your thought about that company crediblity.

Dear Rajiv,

Do you think the probability of getting critical illness for baby is HIGH?

Dear Basavaraj,

Thanks for the great analysis.

Just wanted to know if you included Religare Care-Super NCB plan in this analysis. If so, I was curious to know in what repect it falls behind these 5 plans.

I personally have Religare Care plan. Based on you input, I would like to reanalyze the plans before I renew this year.

Thanks.

Dear Shyam,

Due to certain issues with management (not directly with Religare Health Insurance), I am not recommending this product.

What is your opinion about Religare?

I am a customer of religare since 2015. If switching from religare would be a good choice in present scenario, plz suggest. No claims yet so far.

Dear Souorajit,

Due to certain issues with management (not directly with Religare Health Insurance), I am not recommending this product.

Star health comprehensive policy is the best policy, claim settlement ratio is the also very good.

Dear Gautam,

Then, please buy. My BEST must not be YOUR’S BEST. Hence, if you are comfortable with the company, product feature and premium, then go ahead and buy.

Surprisingly you have not included any Star Health plan, any reasons?

Dear Baldev,

Yes, it is not surprisingly but cautiously 🙂 The Reason is I personally experienced their horrific claim process. Usually, all insurers follow a similar claim settlement on cashless benefit (interaction between hospital and insurers). However, this particular Star company’s representative must visit the hospital. Interact with patient and give the report to the company. Then the process will be initiated. Because of this, I was forced to extend for another day. Just because of their sheer slowness. I am not sure now they follow the same rules or not. But delay in claim settlement process means a BIG NO for me.

Good article , regards to Cigna Vs HDFC , liked HDFC Optima as this has no copay like Cigna once you cross age 60. Cigna will however waive Co pay if policy holder pays extra for waiver

Dear Shashidhar,

Thanks and if you liked HDFC over Cigna, then you can go ahead.

What are you Views on Cigna Pro health plus?? The features and cost are better than HDFC optima restore and Surakasha. Any specific reason for not including Cigna?

Dear Sanjay,

I go with established than the new one.