Which are the Top 5 Super Top-up Health Insurance Plans in India 2020? You have the basic health insurance either from your employer or on your own. However, this base plan may not be sufficient to cover the cost of hospitalization. In such a situation the best way is to buy super top-up health insurance products rather than enhancing the sum insured from the base plan.

I have already written a post on which are my top 5 Best Health Insurance plans in India in 2020. Refer the same at “Top 5 Best Health Insurance Plans in India 2020“.

What are Top-Up or Super Top-Up Health insurance plans?

Top Up Health Insurance Plan

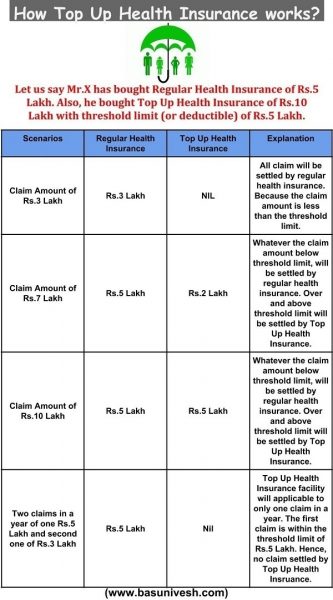

Top Up Health Insurance plan is a regular health insurance plan. But with a certain threshold limit (deductible) to it. For example, if the Top Up Health Insurance Plan offering you sum insurance of Rs.10 Lakh with threshold (deductible) limit of Rs.5 lakh. Then any health insurance claim arising more than Rs.5 lakh will be payable by this top-up health insurance. Below Rs.5 lakh claim must be settled either by regular health insurance or we have to pay from our own pocket.

Let us say Mr.X has regular health insurance of sum insured Rs.5 Lakh and top-up health insurance of Rs.10 lakh with a threshold limit of Rs.5 lakh. Suddenly one day due to health issues he got admitted to the hospital. The claim bill amount was Rs.6 lakh. His regular health insurance will pay Rs.5 lakh (as the maximum sum insured is Rs.5 lakh only). Who will pay the remaining Rs.1 lakh? As the claim amount is more than the threshold limit set by top-up health insurance, the remaining Rs.1 lakh will be payable by this top-up health insurance.

In the absence of any such top-up health insurance, Mr.X might be forced to pay the remaining Rs.1 lakh claim amount from his own pocket. I explained the different scenarios of how the regular health insurance and top-up health insurance will work in the above image.

Now you got an idea of where the Top Up Health Insurance will be handy, apart from regular health insurance plans. If there is more than one claim in a single year, then such a top-up plan will not be useful, as these top-up plans only applicable to one claim per year. If that particular single claim is above the threshold limit, then you get the claim amount from top-up plans. Otherwise, such top-up plans will not be useful.

Here in such a situation, super top up health insurance plan will come in handy.

Super Top Up Health Insurance Plan

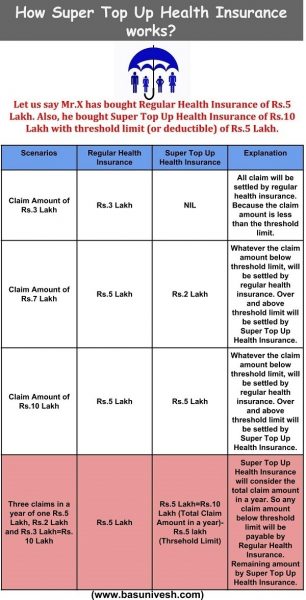

Super Top Up Health Insurance Plan works exactly like Top Up Health Insurance but with only one difference. In the Top Up Health Insurance Plan, there is a limit for a claim in a year i.e. single claim in a year. However, in the case of the Super Top Up Health Insurance Plan, there is no such limit.

For example, in the last scenario of the above table, if Mr.X has Super Top Up Health Insurance, then the remaining Rs.3 lakh might be settled by this super top-up health insurance but not from his own pocket.

Super Top Up Plans will consider the total claim amount in a year. Whatever the amount below threshold limit must be payable either by regular health insurance or from our own pocket. The remaining amount will be payable by super top-up health insurance plans. I tried to explain the same in the below image.

See from the above table where I highlighted the last row with a different color. Here Super Top Up Health Insurance Plan will come into handy than regular plans or Top Up Health Insurance Plan.

Features of Top Up Health Insurance Plan & Super Top Health Insurance Plan

- No restriction to have Regular Health Insurance-There is no such restriction that you must have regular health insurance to buy either of these two. If you have regular health insurance, then below the threshold amount will be settled by the regular plans and above threshold claim amount by either of these two.

- Can buy from different insurers-You can buy regular health insurance from one company and top-up plans from a different company.

- Cheaper than Regular Health Insurance Plans-Due to threshold limit or deductible clause, these plans are cheaper than regular health insurance plans.

- Both Individual and Family Floater Plans Available-Exactly like typical regular health insurance products, such top-up plans will offer you to an individual or to a whole family.

- Come with regular exclusions-Regular exclusions also applicable to top-up plans like existing diseases or dental care. Hence, check out for exclusions in detail.

- Tax Benefit-Exactly like regular health insurance products, you can claim the tax deduction under Sec.80D of IT Act.

- Works on reimbursement base-Before settling the claims under top-up plans, insurers first check whether the below threshold limit amount of total claim bills paid from a policyholder or not. They will not bother whether the below threshold amount is from the policyholder’s own pocket or from his regular health insurance. Then only any dues of above threshold limit settled by top-up plans. Hence, you may say that getting cashless benefits from the top-up plans is difficult.

- No NCB (No Claim Bonus)-These plans usually not offer any NCB benefits.

Who can buy Super Top Health Insurance Plan?

If your health insurance is negligible and budget is your problem, then definitely you can this of buying Top Up Health Insurance Plan & Super Top Health Insurance Plan. Because they are cheap. But do remember that claim settlement may be cumbersome with Top Up Health Insurance Plan & Super Top Health Insurance Plan. Hence, it is better to increase your cover from the existing health insurance itself.

If you plan to increase your health insurance cover, then first try to compare the premium of top-up plans with regular plans. Go for top-up plans only in case you feel cheaper than going for regular plans.

Usually, minor claims are more frequent than huge claims. Hence, you may end up forgetting the features of such top plans. Hence, make sure that you know the details regularly and it’s applicability.

Top 5 Super Top-up Health Insurance Plans in India 2020

The best strategy while choosing the Top 5 Super Top-up Health Insurance Plans in India 2020 is to have both the base plan and super top-up plans within the same company. This creates easy claim processing. The second important aspect you have to choose is both the base plan and super top-up plans commencement date should be as nearer as possible.

Considering all these aspects and my earlier Top 5 Best Health Insurance Plans in India for 2020, I am recommending below super top-up plans as my Top 5 Super Top-up Health Insurance Plans in India 2020. However, it doesn’t mean they must be your BEST.

# HDFC ERGO Optima Family Floater

Sum assured options that are available include 5/7/10 lakhs. Aggregate deductible options include 1/2/3/4/5/6/7/10 lakhs.

In a family floater policy, a maximum of 2 adults and a maximum of 2 children can be included in a single policy. While the family may include self, spouse, dependent children and dependent parents, the 2 adults in a family floater can be a combination of self, spouse, father or mother.

The premium for a family (2 Adults (45 Yrs and 35 Yrs to 44 Yrs) +1 Child (below 16 Yrs) for Sum Insured of Rs.10,00,000 and deductible is Rs.7,912 (Including tax)

You can visit their page here for more details – Optima Super Family Floater.

# HDFC Ergo Super Top-up Plan

The name of the HDFC Ergo’s Super Top-up Plan is “my: health Medisure Super Top-up”. Sum assured options that are available for an aggregate deductible of 4 lakhs is 6/11/16 lakhs. Sum assured options that are available for an aggregate deductible of 5 lakhs is 5/10/15/20 lakhs.

You can opt for a sum assured of 20 lakhs with 5 lakhs deductible by paying a premium of Rs. 5,200 per annum. (For a family of 3 members).

The premium for a family (2 Adults (45 Yrs and 38 Yrs) +1 Child (below 16 Yrs) for Sum Insured of Rs.20,00,000 and deductible Rs.5,00,000 is Rs.4,400 (excluding tax).

You can visit their page here for more details – my:health Medisure Super Top-up

# ICICI Lombard Super Top-up Plan

The name of ICICI Lombard’s Super Top-up plan is “Health Booster”. Sum assured options available include 5/6/7/10/15/20/25/50 lakhs. Aggregate deductible options available include 3/4/5 lakhs. There are 3 options that are currently available – A, B and C

The premium for a family (2 Adults (45 Yrs and 38 Yrs) +1 Child (below 16 Yrs) for Sum Insured of Rs.20,00,000 and deductible Rs.5,00,000 is Rs.4,587.

You can visit their page here for more details – Health Booster

# Max Bupa Super Top-up Plan – Health Booster

The name of Max Bupa’s policy is “Max Bupa Health Recharge”. Sum assured options that are available include 5/7.5/10/15/25 Lakhs. Aggregate deductible available is 1-10 lakhs in the multiples of 1 lakh.

The premium for a family (2 Adults (45 Yrs and 38 Yrs) +1 Child (below 16 Yrs) for Sum Insured of Rs.25,00,000 and deductible Rs.5,00,000 is Rs.3,292 yearly.

You can visit their page here for more details – Max Bupa Health Recharge.

# Liberty Insurance Super Top-up Plan

The name of Liberty Insurance’s Super Top-up Plan is “Health Connect Supra”. Sum assured options available include 3-100 lakhs. Aggregate deductible options available includes 2-40 lakhs in the multiples of 1 lakh.

The premium for a family (2 Adults (45 Yrs and 38 Yrs) +1 Child (below 16 Yrs) for Sum Insured of Rs.20,00,000 and deductible Rs.5,00,000 is Rs.5,372 yearly (Option 1).

You can visit their page here for more details – Health Connect Supra

# Star Health Super Top Up Plan

The name of Star Super’s Top-up plan is “Star Super Surplus (Floater) Insurance Policy”.Sum Assured available under the Gold Plan includes 5/10/15/20/25 Lakhs. Aggregate deductible options available include 3/5/10 Lakhs.

The premium for a family (2 Adults (45 Yrs and 38 Yrs) +1 Child (below 16 Yrs) for Sum Insured of Rs.20,00,000 and deductible Rs.5,00,000 is Rs.5,7,30 yearly (Gold Plan).

You can visit their page here for more details – Star Super Suplus

# New India Assurance Super Top-up Policy

he name of the New India Super Top-up Plan is “New India Top Up Mediclaim”.

You can visit their page here for more details – New India Top Up Mediclaim

# Oriental Insurance Super Top Up Plan

The name of Oriental Insurance’s Super Top Up plan is “Oriental Super Health Top UP” Sum assured options that is available is in the range of 3-30 lakhs. Aggregate deductible options available is in the range of 3-20 lakhs.

You can check the premium amount by clicking on the link here – Oriental Insurance Super Top Up

After going by all the features, I am suggesting my Top 5 Super Top-up Health Insurance Plans in India 2020 as below.

Conclusion:-Considering the Covid-19 issues and the way hospitalization cost increasing in India, it is always better to have proper health insurance coverage (even though your employer providing). Hence, instead of buying Rs.20 lakh to Rs.25 lakh base cover, the wise decision is to have a combination of the base plan and super top-up plans. Do remember that the plans above shared are my choices and it does not mean they are the best. If you have differences of opinion, then you are free to choose the plan as per your choice.

Refer our latest posts:-

- The Dark Side of Compounding: How 2% Kills Rs.30 Lakh

- Flexi Cap Funds: Why Your 10-Year Return Chart Is Lying

- EPF Scheme 2026: EPF, EPS and EDLI Rules Explained Fully

- Financial Freedom Without Health? You’ll Regret It Later

- The Peltzman Effect: Why Playing It Safe Can Make You Poor

- Your Retirement Success Depends on Luck, Not Skill

Hi Basu sir. Do you suggest to go with Niva Bupa in 2024 as its no more called max bupa now. OR after this change over do you remove from your above list.?

Dear Satish,

You can go ahead.

sir,

Could you please suggest few good Super top up Insurance plans in 2023 for (2A+1C) family floater? I have base policy (family floater) for 10L.

Planning to take super top up for 30L (deductible 5L). Is this a good idea or should i have lower deductible?

Thanks in Advance.

Best regards,

Harsha

Dear Harsha,

Deductible should be ideally equal to the sum insured of base plan. Regarding products, you can check with ICICI or Niva.

Dear SIR,

Kindly suggest your opinion ….

I have, HDFC ERGO Optima restore (Base -10 Lakhs) & HDFC ERGO Medi sure super top up (20 Lakhs)

I am looking to increase my Super top up policy up to 50 Lakhs, but my existing HDFC ERGO Super top up policy is providing maximum 20 Lakhs.

In this case , What I have to do ?

Dear Venkat,

You have no option but to choose a different insurer for this purpose.

Dear Basu,

In my salary slip in “DEDUCTION” part,my employer has shown these three deductions(every month)-

(1)Medicine

(2) NPS contribution by employer

(3) NPS contribution by employee

I have clearity about NPS contributions.

But Deduction for medicine I can’t understand,as my employer hasn’t shown anything in 80D….

So plz tell me how to claim this “Medicine Deduction” deducted each month by my employer.

Thanks.

Dear Archana,

Without clarity from the employer for the purpose of the deduction is not a wise way to show the same in the deduction.

Thanks for good article..

If someone is covid postive in 6 month before without any symptoms and complications, will these top 5 suggested supertop plan cover covid hospitalisation with immediate effect or needs waiting period of 2,3 years??

Regards

Dear Gyanendra,

Obviously, there will be a waiting period.

Hi, first of all thank you for enlightening us. My query is, if anyone have opted for hdfc ergo optima restore plan for 10lacs on family floater basis, what will be the deductible amount to look for the super top up plan? Upto sum insured of 10lacs? But as per their website the deductible started from 4-5 lacs, not beyond that. Bit confused.

Dear Arijit,

Usually, it should be equal to your basic sum insured. Maybe HDFC not offering more deductible. You can check with others.

Dear Sir,

What is your take on 1Cr policies sir, with increasing medical cost and treatment methods do they deliver what they promise in proposal, can you provide a write up it will be very helpful.

Dear Vijayan,

They come up with high deductible. They know that the probability of crossing such deductible is low. Hence, they are offering. Once down the line if they start to experience the cases, then they may increase the premium.

Hello Sir,

Very informative article. How does the claim settlement process work in case of someone using the base cover as well as the topup and are to submit original medical expenses with different health insurance providers?

Dear Prosenjit,

You can submit the duplicate copies if you submitted the originals to base company.

Thank you Sir. Can you suggest which super topup plan can I consider among the following?

1. ICICI Lombard Health Booster

2. Bajaj Allianz Extra Care Plus

3. Max Bupa Health Recharge

4. Tata AIG Medicare Plus

Thank You

Dear Prosenjit,

My choices are explained above.

Our office provided Mediclaim(3kakhs) needs to submit the original bills. For a claim of 5 lakhs, balance 2 lakhs can be availed from super top up health insurance but do it requires to submit this original bills again with them ?

Dear Bhaskar,

Yes.

I have a health policy from care insurance

I have individual policy

My wife and my son have floater policy

Want to buy super top up.

Questions

1) Can I buy floater super top up with with my whole family? If yes how deductible consider for the same?

2) Can I buy 2 super top up from liberty insurenc e ?

1 is deductable 5 lac and sum assured 5 lac

2nd is deductable 10 lac and sum assured 50 lac

If this is possible than i can increase a floter cover to 60 lac with small premium

please help

Dear Vihar,

It is better to buy the Super Top Up from the existing base plan provider. You have to buy a family floater Super Top Up and the deductible is equal to the base plan sum insured.

Hi. This is. Avery good article. In did now know about super top up plans before.

I’m 40 with wife and 2 kids. I have just 4lac heal insurance from my office.

I was thinking of getting a personal health policy from Lombard for 10L SI. But after reading this article, I’m thinking should user super top-up and get total cover of 20L. So does it make sense to go for 10L heath cover floater and 10L for super top-up or should I go for 5 lac health cover and 15 lac super top up. Apart from the difference in premium, will there be difference the two?

Dear Kumar,

There is no such a difference apart from the premium.

Dear Basavaraj,

I have employer coverage for me and parents with base policy as 10Lakh. Now, if I take super-top of say 20 Lac, when is the 20Lac be useful? Let’s say I make a claim of 10L and exhaust the base policy. Then if my mother needs to make claim, will super-top cover or not? Or, does the deductible mean it should be exhausted by the same member? Please clarify.

Dear Ranganath,

Each hospitalization should cross the deductible amount, then only Super Top Up will come into picture.

Hi Basu

Great article

I have an employer provided base plan for 5L and my wife also has employer provided base plan for 5L . We have 2 Kids. Should we go for another base plan or we could just consider a super top up?

Dear Bhaskar,

Better you must have your own base plan also.

Ok. Thanks Basu for the reply. I am 40 without any existing diseases. As you are suggesting base plan , would you suggest taking a bank group policy(premium is lower) or a retail plan (higher premium)?

Dear Bhaskar,

Retail plan.

Hi Sir.I want to buy a Max bupa ReAssure health insurance plan.

Is it a good plan ? Any better policy better than this ReAssure plan ?

Provide me All the details .

Dear Kumar,

What prompted you to choose this product?

Hello Sir, How is the performance of Liberty Insurance’s ” Liberty Health Connect Supra” plan you suggested? I am seeing on their website that it’s providing world-wide coverage health cover, which means in any world-class hospital around the world we can have our treatment, and the company will pay for it? Will it be cashless worldwide coverage or we will have to bear the cost upfront and they will provide reimbursement? What is Liberty Insurance’s Claim settlement ratio, ICR (Insurance Coverage Ratio), claim settlement amounts (if they have disclosed) anywhere? According to IRDA, which company has the highest claim settlement ratio in Super top policy, does IRDA even have such data? Because as far as I know IRDA only reports data of ICR and not Claim Settlement ratio and that too its releasing data on a health insurance policy, do they specifically release data of Super top policies too? How is Liberty Insurance in comparison with ICICI Lombard or HDFC Ergo or Star Health Insurance in terms of customer service, hassle-free claim process, claim settlement? Is there any co-pay clause like say after passing 80 yrs, is there any co-pay? I dont want Co-pay hence asked.

Dear Hemant,

I suggested Liberty mainly for those who are looking for large sum insured in the super top up. As of now, no issues with the product. Don’t rely too much on ICR. It is a raw data.

Hi Basu,

As always, thanks for a detailed post. It clarified a lot of things for me. Quick question for you — I have Religare insurance (base) of 5L and planning to go for super top of 20L. I understand it is better to have same insurance provider for easier processing of claims. Since I did not see mention of Religare, wanted to know any pitfalls of Religare insurance

Dear Sachin,

Nothing like that. You can go ahead with Religare.

Hi basu.

I have a hdfc ergo family floater policy ( optima restore) of rs 3 lacs ( 6 lacs practically since the 3lac SA will get restored once the basic 3lac amount finishes in a year ). I am planning to take additional 14 lac super top up cover . How much will be the total cover now – 20 lac ( 3+3+14 ) or 8 lac (14-6)

Dear Naveen,

If you are planning to buy Rs.14 lakh coverage of Super Top Up, then the maximum coverage is Rs.14 lakh ONLY. While buying you have to declare the deductible (usually sum insured of the base plan).

Hello Mr. Basu,

In HDFC Ergo Super Top up plan with deductible of Rs. 5 lakhs and SI of Rs. 20 Lakhs, there is a mandatory co-pay of 10% after 80 years of age. Although, considering my age (43 years) that is too far, but as I am considering Super Topup in view of rising medical expenses in future, I have a question: Can that mandatory co-pay portion be paid/adjusted using the NCB (if available) in the base policy at that time? I have asked customer care executives of my base health insurance company, but they were also not able to give any satisfactory answer on this. Please suggest. Thanks in advance.

Dear Vishal,

As per me, you can’t adjust the same with NCB.

Hi Basu,

I am 40 yrs old with no health issues or insurance.

Now, I am planning a family floater health insurance for 4 (Myself, wife and 2 kids).

I can bear cost of few lakhs towards health urgency of my own.

I am thinking of getting Super top plan for 20 lakhs, with deductible that can be managed by me.

Can you clarify?

1. Is it ok to take super top up without base plan?

2. Will it cover Corona?

Dear Pappu,

If you feel few lakhs no issues, then you can go with the super top-up directly. However, my suggestion is to have at least 25 lakh coverage. All health insurance products cover the Corona related hospitalization.

Thanks Basu. I will take 25 lakh super top.

In case base plan is mandated while taking Super top plan, can I take Arogya sanjeevani as base plan?

Dear Pappu,

You can.

Thanks Basu.

what is Arogya Sanjeevni?

Dear Isha,

Refer the post “Arogya Sanjeevani Policy – Standard Health Insurance Features and Benefits“.

Sir, in your top health insurance list royal sundram was there but it was not included in super top up list any reason for that ?

Dear Sanjeev,

The criteria change when you buy super top up. Don’t compare both in same basket.

How is max bupa premium increase compared to other providers since they are giving (5+95) 1 cr insurance very cheap. I getting family floater (2 adults + 1 child) for 18k

Dear Vaibhav,

Usually, the premium will increase based on the age slab. They can increase the same yearly.

I don’t have any base plan can I take only super top up plan and premium of plan will same every year or change

Dear Rajesh,

Then who will pay the deductible? If you don’t have the base plan, then you have to pay it from your own pocket. Premium changes based on the age group. Once you fall under the next age group, then the premium will increase.

Hi Basu,

Whether a person can take 2 individual super top up policies ?

Also please confirm if we have a 20 lac base policy, then should we go for 20 lac deductible or lesser than that ?

Dear Venkat,

Yes, one can have multiple policies. It is better the deductible should be equal to base plan.

Dear Basu,

If the super top up cover is for 20 Lakhs with 5 Lakh of deductible , will this cover 20 Lakhs or 15 Lakhs after the 5 Lakhs which can be met through the base policy

Regards,

Somyajit

Dear Somyajit,

It is like Rs.5 lakh base plan+Rs.15 lakh super top up=Rs.20 lakh cover.

I have 15 lacs base cover from my regular plan and now if i purchase super topup plan of 20 Lakhs with 10 Lakh of deductible. What will be my overall cover . Is it 25 lakhs or 35 lakhs cover.

Suppose i get the claim amount say 28 lakhs for a year by multiple claims. Will i complete get cover from both regualr and super top up plans. Please explain

Dear Kalai,

The total coverage is 20 lakh ONLY.

If there should be an occurrence of no Base Medical coverage plan how might the last situation where you have featured the last line with an alternate color will be thought of? would you be able to please intricate?

Dear Updated Ideas,

If you don’t have a base plan, then you have to pay it from your own pocket.

Hi Basu,

In the current pandemic scenario, I have following questions:

1. Will these “Super Top-ups” cover Covid-related claims as well?

2. If yes, then, which is better between “Super Top-ups” and “Corona Kavach”?

Dear Mahesh,

If you feel the base plan and super top up cover is sufficient, then I don’t think having COVID cover is necessary.

Hi Basu

We have a family floater health plan in my wife’s name and now I want to compliment it by buying a super top up plan in my name. Is there anything wrong in this schema?

Dear Praksh,

Nothing wrong.

What is wrong with Tata Medicare super top up?

Dear Alok,

Nothing wrong 🙂 As I stressed, always better to have both base and super top in the same company and also whatever my Top 5 must not be universal. If you are comfortable with features, then go ahead.

What are the points to be considered if we are opting for Super top up from different insurer? How cashless claim works in super Top up?

Dear Dilip,

Super Top Up works like normal health insurance and same procedure is usually followed for claims.

Dear Basu,

In case of no Base Health insurance plan how would the last scenario [where you have highlighted the last row with a different color] will be considered. can you please elaborate.

Thanks

Viswanath

Dear Viswanath,

You have to bear it from your own pocket.