Which are the Top 5 Best Online Term Insurance Plans in India 2020? What is the claim settlement ratio of these best term insurance plans? Let us choose the best term insurance plans in India by comparison with charts.

We have around 24 Life Insurance Companies and as of now, all insurance companies offer online term insurance plans. Hence, it is hard to shortlist the BEST among them. This post will help you in shortlisting the Top 5 Best Online Term Insurance Plans in India 2020.

What is Term Life Insurance?

Term Insurance is the type of Life Insurance. If death occurs of the policyholder during the policy period, then his/her nominee will receive the Sum Assured selected. If policyholder survives till the end of the policy period, then he/she will not receive any maturity amount.

This is the reason, these policies cost you very less and cover a large amount of life risk. This is the PURE LIFE INSURANCE. Hence, anyone who has financial dependents must buy this product immediately.

However, nowadays there are so many variants in Term Life Insurance. For example, the return of premium, Term Life Insurance up to 100 years of age, a variety of riders and a variety of claim payable options.

But instead of complicating your dependents, buy a simple plain term life insurance. Why you complicate your dependents when you are buying this is that this product’s benefit will come into picture when you are not here.

What are the advantages of online Term Insurance Plans?

Nowadays all Life Insurance companies offer you online term insurance plans. The advantages of online term plans are as below.

# It is convenient to buy as with the click of a button you can buy it.

# As there will not be any middlemen involved, the price is cheap than offline term insurance plans.

# You fill the proposal form on your own. Hence, an error of margin is LESS.

# Undue influence by agents is not there.

# Along with the discount of DIRECT purchase, if you buy through online then now life insurance companies will give you 8% on your FIRST YEAR PREMIUM. This is to promote cashless online transactions.

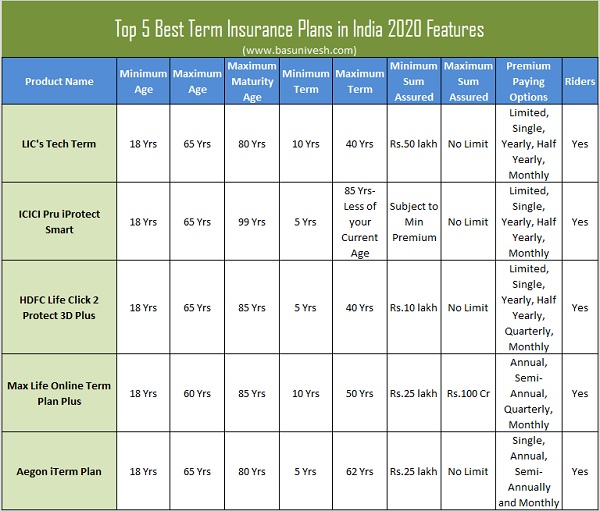

Top 5 Best Online Term Insurance Plans in India 2020

Now let us shortlist the Top 5 Best Online Term Insurance Plans in India 2020. How I selected the Top 5 Best Online Term Insurance Plans in India 2020?

# How old are the companies

# Claim Settlement Ratio

# Premium Cost

# Plan Features.

How old are our Life Insurance Companies?

Below is the chart which explains the age of all life insurance companies. I am comfortable with the company which is at least 15 years old.

You noticed that among 24 companies, around 14 companeis are around 15 years old. Hence, let us concentrate on these 14 companies. It does not mean that those who are less than 15 years are not trustworthy. However, I feel comfortable with the well eshtablished companies than exploring with new companies. After all Life Insurance is a long term contract.

IRDA Claim Settlement Ratio for 2018-19

I have already written a detailed post on this at “IRDA Claim Settlement Ratio 2018-19 | Best Life Insurance Company in 2020“.

However, for the better understanding purpose, I am putting the data again in this post.

You notice that among total 24 Life Insurance Companies, around 20 companies are in GREEN (Claim Settlement Ratio above 95%). Earlier it was 11 companies. Only three companies are in yellow (claim settlement ratio above 90% but below 95%) and one is in red (Less than 90%).

As usual, LIC tops the list. But don’t feel happy. Let us see the claim amount settled by individual companies to arrive at best companies.

Average Claim Settlement Amount of Life Insurance Companies in 2018-19

As I said above, the claim settlement ratio will not give you a clear picture of which type of products the insurance companies settled. However, we can assume the types of products they settled by looking at the average claim settlement amount of Life Insurance Companies in 2018-19.

Here come the results !! LIC stands in lowest with red in colour along with Life Insurance Companies like Bajaj Allianz, Exide, Future Genereli, IDBI Federal, India First, Max Life, Reliance, Sahara, SBI Life, Shriram, Star Union. What is it indicating?

It shows that, even though LIC settled the highest number of claims, the majority of such claims are less than Rs.2,00,000 Sum Assured. Hence, it is indicating indirectly that LIC’s claim settlement is mainly in the category of Endowment Plans but not Term Insurance.

Average Claim Rejection Amount of Life Insurers in 2018-19

Now let us go deeper into IRDA Claim Settlement Ratio 2018-19 and try to analyze the how much amount of claims they rejected. Here, I calculated average amount as I don’t have data to check the maximum and minimum amount.

The results are as below.

You notice that Sahara’s claim rejection amount is ZERO. The reason is that IRDA Annual Report itself mentioning it as ZERO. Then comes the LIC. LIC’s claim rejection is less because the quantum of claims it handles is HIGH but value is less. So no need to say that LIC done a great job here along with other players. However, you notice that as usual HDFC and ICICI tops the list.

Hence, the moral of the story is that DON”T RELY TOO MUCH ON CLAIM SETTLEMENT RATIO ALONE!!

Top 5 Best Online Term Insurance Plans in India 2020

Based on the IRDA Claim Settlement Ratio 2018-19, which are the Top and Best Life Insurance Company in 2020? I select a few based on the above data. You may differ in my view and come up with a different set of ideas. But these are my choices.

- LIC

- HDFC Standard Life

- ICICI Pru Life

- Max Life

- Aegon

Premium Cost of Term Insurance Plans

Now I will consider these 5 Life Insurance Companies premium only to arrive at best. The Insurance Companies which I shortlisted are as below

- LIC (Why? Because the oldest and Government backed mammoth)

- ICICI

- HDFC

- Max Life

- Aegon Life

Even you can consider companies like Bharti Axa or Tata AIA Life. However, I have to choose only five among 24 Life Insurance Companies. Hence, I have selected these 5 as per my choice and comfort with the companies.

Now I will consider an example of a person whose age is 30 years, Term of Plan as 30 years, Non-Smoker and healthy, Sum Assured Rs.1 Cr and yearly premium payment. I selected plain vanilla products without any riders or add-on features.

Many of you may be aware that last year LIC launched the new Term Plan by closing it’s old plan. I have written a complete details about this plan earlier and refer the same at “LIC’s Tech-Term (No.854) – Online Term Life Insurance Review”.

Now let us look at the plan features and decide which are the Top 5 Best Term Insurance Plans in India 2020.

Note:-Refer our latest mutual fund recommendations also at “Top 10 Best SIP Mutual Funds to invest in India in 2020“.

Few points to consider while buying term insurance

# Never rely on Claim Settlement Ratio

Claim Settlement Ratio is raw data. This data will not give you enough picture of what type of products the insurance companies settled. Hence, relying too much on this single data and selecting a product is not a good idea.

# Quantum of Life Cover

Ideally one must have at least 15-20 times of your yearly income. This is the basic calculation.

# Fill the data properly

Sharing data especially materialistic information must be accurate. If you are unable to understand anything, then immediately contact Life Insurer for the help. Understand the questions and fill only when you know what you are filling.

# Never allow someone to take over your decision

Never budge on the decision which is against your wish. If you are fully comfortable, then only go ahead and buy.

# Term of the policy

Ideally, it should be up to your working life. Because you retire when you are financially free. Hence, Life Insurance is not required during your retirement age.

# Splitting of Term Insurance

There are few who are apprehensive of relying on a single insurer. Hence, they try to split among few. But in reality, there is no logic in splitting. What is the guarantee that the all insurer will accept or reject the claim?

# Stay away from riders

Never combine Life Insurance with General Insurance requirement. You will get better-featured covers from general insurers regarding accidental and critical illness covers. Hence, simply avoid riders.

# Never heed the aggregators choice

Nowadays there are so many online aggregators. You may not know that they act exactly like insurance agents. Hence, never rely on their claim. Do your own research. If you are satisfied, then only go ahead and buy. Refer my post about the same “Beware of Insurance Comparison portals in India“.

# Know about Sec.45 of Insurance Act

After the recent clarification about Sec.45 of Insurance Act, the customer became king. It states “No policy of life insurance shall be called in question on any ground whatsoever after the expiry of three years from the date of the policy, i.e. from the date of issuance of the policy or the date of commencement of risk or the date of revival of the policy or the date of the rider to the policy, whichever is later.”

Refer the complete post at “Term Insurance-Claim Settlement Ratio no more a big criteria“.

# Review your life insurance cover

Buying Life Insurance of Rs.1 Cr or Rs.3 Cr is not a one-time affair. You must review your life insurance requirement at least once in the 5 years. If required, then you must increase the sum assured.

# Be cautious with premium payment

In case of term insurance, you have to be very cautious when it comes to premium payment. It is always better to opt for yearly premium payment and also if possible make it automated by the way of ECS. If policy lapses due to your negligence, then you have to undergo medical tests and all kinds of stuff once again. If there are any health issues, then the insurer may reject to renew the policy.

# Never go for Telemedical Examination

Recently one of my blog readers pointed that few Life Insurance companies insisting just Telemedical Examination by questioning about your health details in the phone (Refer-Can I buy Term Life Insurance with Telemedical Verification?).

It may be the easiest process for you and for life insurance companies. However, I feel suspicious of such kind of medical examination. Because in future insurance companies may find 100000 reasons to reject the claim on health ground.

Instead, I suggest you to go for medical examination. This will really clear the dust or doubt in your mind about future claim settlement.

Final Note:-The list of “Top 5 Best Online Term Insurance Plans in India 2020” is my personal choice and comfort with insurance companies and by verifying features. However, it does not mean that my selection will be the UNIVERSAL selection.

Hence, if you have a different opinion from my selection, then it does not mean you are buying the wrong product. My only concern here is not to shortlist “Top 5 Best Online Term Insurance Plans in India 2020”, but to give the gyaan which you must take into consideration before you shortlist your term life insurance.

Read our latest posts:-

- Never Compare Nifty 50 Index Funds Vs Active Large Cap Funds!

- Nifty 500 Multicap 50:25:25 vs Nifty 500: Which Is Best?

- 5 Important Investing Truths Most Investors Ignore

- Retirement Is Personal — Stop Comparing Net Worth and Move On

- EGR: The Gold Investment 99% of Indians Have Never Heard Of

- New Income Tax Act 2025: What Changed for You from April 2026?

Hello Sir,

Hope you’re doing well.

I have a question regarding life insurance for someone who’s living outside India – can this person continue having a term policy in India which he/she is already paying for even before moving abroad? What are the tax or other implications in such cases? or what is the right thing to do as discontinuing the insurance and buying it after few years may become a very expensive option?

thanks much

Dear Isha,

Yes, they can continue. Tax implication for what? Better to continue.

Hi,

Thanks for information.

What you suggest? Some of the company are providing limited payment option.

Can we go for that?

Like Policy for Upto Age 75 and Premium payment term for 15 Years.

Dear Chirag,

Regular premium is the best option.

Dear Sir,

Please let me know if the payout of Term plan is taxable for the nominees?

Regards,

Yash

Dear Yash,

It is tax-free.

Dear Sir,

Your analysis is comprehensive and an eye opener.

I have question regarding ‘Sec.45 of Insurance Act’ and Telemedical Examination.

If Telemedical Examination was done during policy creation and pay annual premiums for 3 years.

Still is there any chance of policy being rejected during claim due to Telemedical Examination ?

Dear Bora,

Yes, they can reject if they found that you hid some information.

Hi Sir thanks for detailed post, i am planning to purchase Icici pru term plan and their premium is 12000++/yearly without any critical illness benefit? so what if i suffer from any critical illness or accidental death and i didnt get any benefit from the policy..??

Dear Harsha,

Death due to critical illness or accident is also covered as usual.

Dear sir ,

In term insurance policies it’s written that Death Benefit is the highest of

1. 10 times the annualized premium

2. 105% of all the total premiums paid as on date of death

3. Sum Assured

As for any term policy highest is always Sum Assured.Then why they write this ?Pls elaborate

Dear Rupesh,

It is not only for term insurance but for all the policies the standard format. Hence, you no need to worry.

hi sir…. i like your content……i have seen the individual claim ratio of ICICI in IRDAI ANUUAL REPORT 2018-19 it shows zero..but you have mention average claim rejection amount ratio is too high…so please clear my doubt

Dear Nirmal,

Please check the report properly.

Dear Sir,

I have a HDFC life insurance term plan. HDFC click to protect plus 3D plan bought in 2018.

In this policy’s proposal form I have not mentioned about my 2 personal accident policies and my 3 lapsed policies.

Because company’s executive told me that mention only about my existing term plan.

Now, what to do ? Will this information effect on my policy in future ?

Please clear my doubt.

Dear Nilesh,

You no need to mention about accidental insurance products and also for the lapsed policies.

Hi sir,

Can I buy PNB TERM PLAN

Please suggest

Dear Ramachandra,

If you feel the features and premium affordable, then go ahead.

Hi basu, I had purchased HDFC life click to 3D plus term plan through online mode but they had not asked me to take any medical. My age was 27 & am healthy. Now should I concern about medical test. If so what implications does it may have in future claims ?

Dear Sravan,

Don’t worry. If you disclosed the facts properly, then be calm 🙂

Hi basu, I have also made few mistakes.

1. I have a ULIP and is still active. I have not disclosed it. 2L worth

2. I also have SBI Life accidental insurance. I have not disclosed this too. 20L cover

I thought these are not term so no idea if I had to disclose. Now can I stop these two so that my disclosure will be correct. I am having 1cr cover in HDFC life simple vanilla from 2018.

Also should i buy any riders too ?

Am very much confused if I have to stop and restart a new policy. Now am 30 yrs old.

As per sec 45 of insurance act. I will be completing 3yrs by next year, so can I continue this policy if I stop these two existing policies ? Please guide.

Dear Sravan,

Exiting and retaining must be as per your requirement but not just because of Sec.45.

Dear Sravan,

Not disclosing ULIPs is a mistake but not accidental insurance.

Thanks basu, my ULIP is of 10 yr plan. I have already finished 8 yrs. It will be matured in 2 more years.. May I think After that My HDFC term declaration would be correct ?

What is the best solution I can do now. Please guide.

Dear Sravan,

My suggestion is to exit.

Sir,

I bought ICICI Prudential term plan in March 2020 through advisor of the company. But nominee dob, my phone no, and email id was not correct in bond I receive.

Due to lockdown I mailed them and get all above details corrected, Now all the details are corrected, and I have received mail from their customer care team.

But they are denying to send me the revised /updated policy, as per them I can use the email for reference.

The say no change in bond is possible after issue.

Please suggest should I discontinue the policy or any other solutions.

Please guide

Now

Dear Mohit,

They are correct. Bond can’t be changed but they can endorse on it.

Dear Basavaraj

Thank you for valuable information.

I am planning to buy a term plan and health plan for myself and husband now.

I have few queries for which please through your valuable thoughts.

– Currently myself and husband have a health plan of 7 lakhs (separately from employer). So we thought to purchase an additional 5 lakhs of family floater (we both are of same age) from companies which you suggested. Now that we have a child of three months. Please suggest if we can buy a separate policy or should we include in family floater.

– Secondly, we are planning to purchase term plan. As u suggested we are planning to go for plain product without riders like critical illness, However for critical illness especially for cancer, not sure if daily chemotherapies would be covered in regular health insurance plans. Please suggest on how should we secure ourselves for critical illnesses. Should we buy separate critical illness plans. If so would the premiums for such be high as age increases (unlike term where it is fixed based on current age). Kindly advise.

– Should we give importance to term plans where terminal illness benefit exists. I am planning to take term till 70 years of age. Is this reasonable?

– In summary, please advise on how should we plan buying health and term plans

Plan term plan of 1 cr

Health insurance sum of 7 lakhs of family floater 5 lakhs- will this suffice. Or should we increase considering critical illness (in case we do not purchase as rider in term plan)

should we consider going for top ups now or later as per need.

Please advise a plan for us

Thank you for your time.

Best regards

Dear Rajani,

1) Better you include your child also and buy a family floater plan. Instead of going for base plan increment, better to go for super top up.

2) You have to buy separate critical illness plan.

3) Go for plain plan and restrict to around 60 years.

Dear Basavaraj

Thank you for the reply.

Do you also advise some good critical illness plans as well?

I understand that in critical illness plan, premium increases as age increases. Once a person gets identified with critical illness, lumpsum amount will be paid. In that case, should we buy another policy from then with high premium based on the age at that point of time. Please help me understand.

Thanks and best regards

Rajani J

Dear Rajani,

Wait for a day or two and I am writing a new post on that.

Dear Basavaraj

I read you article on super top ups. Does they not setting bigger claims.

It as mentioned in article as “But do remember that claim settlement may be cumbersome with Top Up Health Insurance Plan & Super Top Health Insurance Plan. Hence, it is better to increase your cover from the existing health insurance itself.”

In that case do you advise going for increasing base plan rather than buying super top up.

Dear Rajani,

It is not like that. To a certain extent, you can rely on base plans and later on super top up are must for you. I said so as cumbersome if both base and super top up are from a different companies.

Hi Basu,

ICICI providing different options to get money and accordingly set premium also

1. All amount together

2. Equal monthly income for 10 years

3. Some amount as Lumpsum and monthly income for 10 years for remaining amount

Is it good to select option 2 or 3 ? Or we should go for option one only?

Dear Divyanshu,

Stay away from such fancy options and stick to 1st one.

Dear sir,

I purchased term plan 50l each from Aegon life and Bharti AXA is it good?? Because as per my study’s with different insurance company these two are cost effective and also CSR is greater than 95%. Both Aegon and AXA is a reputed insurance company all over the world. So can you please suggest is it good for me.

Dear Debasish,

If you have already purchased, then stick to it.

Hi Basu sir, Nice blog and i had few questions,

1. Even though ICICI and HDFC has high claim rejection ratio..why are we shortlisting it? May be i missed something to understand.

2. Between HDFC or ICICI which one would be suggest?

3. Recently one of my friend went with ICICI he was ready for physical visit for medicals but ICICI said its not required and issued him policy is this act acceptable or can we demand of physical medicals?

4. If its not online way then would you prefer/suggest some other insurance companies?

Dear Sat,

1) They are well established then it’s peers.

2) For me both are good and bad.

3) Yes, it is better to demand.

4) All insurers are offering online. So not necessary to go offline.

Thanks a lot for replying Basu sir. You mentioned it both ICICI and HDFC have their own good and bad. Which would you suggest among these two as most preferred ones.

Dear Sat,

Both 🙂

One more question,

What’s you view or difference you can see about SBI Life insurance compared to other Max life and ICICI?

Please mention.

Dear Sudarshan,

For me all are equally good and bad. If you feel SBI is best for you, then please go ahead.

Dear Sir,

Thanks for sharing this must read article. This is a very informative post. I hope that I must read before to buy policy.

Recently on 2nd May2020. I bought term plan

-Company: Max life insurance

-Through: Policy bazaar

-Sum assured: 1cr

-Current age: 35 Years

-Policy Term: 40 (period of coverage in years) up to 75 years

-Premium Payment Term: 15 (period, in years, for which premium is to be paid)

-Premium Payment Mode: Monthly

Looking in to your suggestion in article, I guess I have to ask Policy Bazaar and Max life insurance to do changes in few terms such as,

-Policy Term: 30 (period of coverage in years) up to 65years

-Premium Payment Term: up till coverage i.e. next 30 years

-Premium Payment Mode: Annually

If they said no. I have option to cancel this policy too, within 30 days from the issue date of policy and ask them to pay premium back.

Please suggest.

Thanks & Regards,

Sudarshan

15

Dear Sudarshan,

Yes, but better you contact them immediately for these changes before they issue the policy.

Thank you sir for your reply.

I will try to contact them immediately. But just one question, I already read in your article still I want to ask. Is it ok to go with Max life insurance with policy bazaar? (As I already did it)

Dear Sudarshan,

Yes, no harm.

can we request all application details from term insurance company after issuance of policy so that we can detect any may have done by applicant .

Dear Singh,

NO.

Is irda mention the reasons under which companies rejected claims?

I want to know that because if we can reduce those mistakes or errors while buying insurance.

Sir can I know why anyone should purchase directly with life insurance company instead of policy bazzar ??

Dear Singh,

Sadly IRDA data will not share such information. Policybazzar acts like middlemen as they are the aggregator. Hence, obviously they may influence my buying right (for their profit)?

hi which one to buy from aegon and bajaj?

Dear Kaushik,

For me both are fine.

I have purchased Maxlife term insurance online worth Rs.88 lakhs 2 yrs back. I wanted to increase it to 1 correct this year,however ,Maxlife doesn’t give option to increase sum Assurance,will have to buy new policy again.My questions are-1) Should I purchase new policy in Maxlife or lic tech term for 1 CR??? or 2) should I buy 2nd policy worth Rs.25 lacs in above mention companies??? Plz help

Dear Anand,

No insurance company will provide the facility to enhance from the existing life insurance. Hence, you have to buy a new one from the same insurer.If your need is Rs.1 cr and you already have 88 lakh policy, then buy another Rs.12 lakh from the same insurer.

But Maxlife and all other companies provides insurance of minimum 50 lacs.What should I do then?

Dear Anand,

If you don’t want beyond Rs.1 Cr, then opt other insurers.

Sir to my previous query, any reason to your statement to opt for a regular premium than a limited premium option?

Dear Anup,

It is not FREE and it cost you if you consider the time value of money.

Hi Sir,

I want to by 1CR policy for the next 32 years, is it better to go for 7years payment term with ICICI or 10 years payment term with Maxlife ?

Which would be cheaper and by what percentage cheaper than other?

Dear Anup,

Why not a regular premium than a limited premium option?

My salary is 18 lacks per year and have house loan 40 Lacks with 20 year term out of 2 year completed.

I am looking to buy term insurance and below are my questions,

1. How much should be the SUM ASSURED?

2. he age limit shall be 60 or 65?

3. which company i have to choose and why?

4. Is rider is necessary? if yes which one?

5. through which channel i have to purchase? i.e by POLICY BAZAAR or Direct insurance company’s portal. ( Eg. Tata AIA, ICICI, HDFC ergo etc…) and online or offline…

6. is it advisable to purchase 2 term insurance? If yes -why? If no – why? the reason is premium is getting higher when we go for higher sum assured… For Example pls see below,

I took ICICI IProtect to analysis and found as,

For SA 2 crore & 60 age premium is in POLICY BAZAAR as 20152 & ICICI PRUDENTIAL as 17130 ( Diifer is 3022 )

For SA 4 crore & 60 age premium is in POLICY BAZAAR as 59278 (see 3 times!!!) & ICICI PRUDENTIAL as no data

why can’t we go 2 x 2 crore which saves approx Rs 19000 as per policy bazaar data?

Could you pls help?

Dear Ram,

1) I already answered to this.

2) It should be up to your working age.

3) Refer above post.

4) Already answered in the above post.

5) Directly with Life Insurance companies.

6) Why???

I think I have answered all your questions in above post. Take the pain to read once again.

Hi,

Iam 41 years old (used to smoke till 2018 and stopped). Iam perfectly healthy, have taken up a full body checkup on March 2019. I want to buy a term insurance with return option (return of premium upon maturity). Hence can you please suggest some good options? Thanks so much.

Dear Venkatesh,

My options are already listed in the above post.

Hi,

I had bought term plan of ?50 lakh from hdfc in 2012 at the age of 32 years. Last year I wanted to increase my life cover to ?1 crore, but couldn’t do as it was told from hdfc to apply for freshly. Then I decided to go with the insurer who offers the same cover with lower premium and good claim settlement ratio compared to others. Therefore, I bought ?1 crore term plan last year with disability rider of ?50 lakh from Aegon with the thought that I will discontinue with hdfc. Now I have dilemma whether I should exit the hdfc or should continue with both keeping in mind the need to increase of cover in future.

Dear Gajanan,

If your Aegon Life Insurance is sufficient for you, then you can continue HDFC.

Surprised when you say don’t go by claim settlement ratio. Ultimately if claim is not settled what purpose does the policy serve? You seem to try and find reasons to belittle the efforts of LIC. If the policies are small in size, that is not worth settling? Or do you mean that claims of only big cases are worth analysis? Strange analysis-i would even call it biased.

Dear Murali,

Surprised that you are unable to understand the CLAIM SETTLEMENT RATIO. Check the average claim settlement amount the LIC settled. It is least. This indicates that LIC settled mainly traditional plans but not big amounts. If LIC really did its best, then Insurance today may not be SOLD product but a BUY product. Also, all of us might have a proper life insurance to protect our family (when I say proper, the ideal coverage should be at least 15-20 times of yearly income).

Desr Basav

I am stuck with an unwelcomed technaility being used by the insurer in calaculation of the sum insured in my case and medical tests postponement in my wifes case.

As we see it, the insurer doesnt want to to offer that product which has been discontinued for sale 2 days after we paid for it and ideally they shud honor the committment already given but they are trying to give one reason or the other which defies all logic for it . I need your advise and would seek a way i contact u asap pls.

Dear Nikhil,

Is that product so great that you have to FIGHT? Just move on to new product or some other insurer. Don’t waste your time on this.

Mr.Basavraj,it seems to be as if you’re insisting people to go for online purchase of insurance plans,discrediting the effort and the pain put by the Agents of various insurance companies in procuring business for insurers since the inception of the concept of insurance on earth. Insurance is a subject matter of solicitation,hence Agents always take care of the customer’s interest before closing any plans. Please remember one thing that need for insurance is established only when an agent approaches the prospect. Hence don’t encourage the online policy sales affecting the livelihood of lakhs of Insurance agents associated to the industry.

Dear Arijit,

I can understand your anger 🙂 We have to make a society to change from agent approach to prospect to prospect to buy directly. Come out from that mindset and accept the change.

Dear Basavaraj,

I am 37 years wants to buy term insurance as I am a occasional smoker like 1 -2 sticks in a week I am trying to quit that also, should I opt for smoker’s option or should I go for non smoker category.

As in Aegon there is an option to update in your plan once you leave smoking.

Also do they consider smoker’s or non smokers category based on last one year?

Dear Amit,

Better to consider yourself as a smoker.

Hi..

I am 34 years old, smoker, married & 01 kid with 18 lacks yearly package

I am looking to buy term insurance and shortlisted as below using policy bazaar with key factors as Sum assured 2.20 crores until age of 85 years ( i.e 51 years coverage)

Tata AIA maha raksha supreme ( yearly premium 48026)

Bajaj alliance smart protect goal ( yearly premium 34254)

Could you pls guide me which one will be wiser and why?

Thanks in advance…

Dear Ramkumar,

Do you need Life Insurance up to your 85 years of age?

Very good information it will help any individual to know and take a clear decision on buying any of the term policy. I would suggest pls share more frequently these kind of information on regular basis to educate individuals to aware of policies. Great to read and surely read your info henceforth Mr. Basavaraj

Dear Rajashekhar,

Pleasure 🙂

Hi, i had taken ICICI i protect smart insurance for 80 lakhs coverage in 2019. Along with this, taken critical illness cover of 18 lakhs. But later I came to know that term insurance should be plain life insurance . So , i would like to know from you that it is ok to have both in single life insurance.

Dear Ravindra,

You already purchased, then why worrying now? Calm down 🙂

Which is best for Term Plan LIC or HDFC Life?

Dear Mangesh,

Both are good.

Hi Basu, I’m 42 and taking 40 yrs term insurance for 2 CR in TATAAIA. My medical is done. I can pay the premium by any of the below options. Can you suggest which one I should pick?

176056 * 5 (pay annually only first 5 years, )

98176 * 10 (pay annually only first 10 years)

85432 * 12 (pay annually only first 12 years)

37760*40 – (Pay annually Every year till the end of the coverage)

65136*18 – (Pay annually for 18 years and stop when I turn 60)

Dear Amar,

Opt “Pay annually Every year till the end of the coverage”.

I’m 30years old (occasional smoker) planning to take a joint term insurance policy for 1cr +50 lakh with my wife (working) and have thought to move forward with Bajaj Allianz for a total of 70years with the joint annual premium of 14k, what is your thought on this.

And is it suggestable to go with waiver of premium addon?

Dear Karthik,

Why JOINT?

I have submitted the proposal for TATA AIA term plan.Now after reading your article, I feel that I should go for Maxlife.

Kindly inform me that other than being a relatively newer company which other factor stopped TATA to be included in your Top 5 list. Plz help

Dear Amit,

If you liked Tata product, then there is no harm in going there. It is my comfort and choice I shared. Above that, if you already purchased, then why second thought?

Have read your article. Thank you for graphical representation, it came handy. A couple of months ago I ( Male,30)switched from Lic’s Anmol Jeevan to Edelweiss Tokio’s online term plan. Have I taken a risk?

Regards.

Dear Saurav,

If you already purchased, then calm down.

Will the term insurance plan prices increase in May 2020 post lockdown? I am 28 should I buy immediately a Term insurance before may 2020?

Dear Rahul,

Who told you about such rumors?

Sir i am 31 years old government employee and have bought the HDFC TERM insurance plan online for 55.00 lacs. I thought they will do medical check up but did not. Instead they asked me to fill up medical form online asking for my medical history which i gave.

I told HDFC why did not you conduct physical check up, but they told we know when it is necessary. Now i got the policy bond also through online.

But i have one doubt whether the tele check up was safe, i mean in future after my death the HDFC should settle the claim without any problem to my family.

Dear Danish,

If you disclosed everything properly, then no need to worry.

can we request physical medical test later after issuance of policy? Because their may be any medical condition which we did not know without medical.

Dear Man,

After issuance of the policy? NO.

During this lockdown, policy bazaar is ready to give term insurance without any medical tests. What is the risk involved in it?

Dear PP,

Never take hasty decisions. They are hungry for BUSINESS and why you have to be a scapegoat?

Why to buy additional term insurance from the same company??

Is there a problem if I buy from other insurers as of now it’s advisable not to keep all the eggs in same basket.

Dear Navin,

A simple logic. The more diversification in Life Insurance, the more work for your dependents (when you are not here). Keep it simple. There is no logic in DIVERSIFICATION OF INSURANCE.

Can I go with Aegon and Bharti – AXA ??

Dear Debasish,

Please read my post again.

I have an HDFC term life cover. I pay annual premium. Can I increase the sum assured ? How do I do it?

Dear Rath,

It is better to review your Life Insurance coverage requirement and based on that you can increase it. You can’t enhance the coverage from the same existing Life Insurance. You have to buy one more plan from the same company. I suggest you to buy the term life insurance from the same company.

life insurance company asking that is their any application rejected earlier. If we forget about any application rejected to tell them . Can they reject claim on basis of that.

Dear User,

Yes, maybe. But how can one forget such vital information?

Their was two applications more than year ago .they asked about them only on call not in online form. I just remembered about one policy that time and they also asked about that policy like they see it on some cibil like system and they not enquired about rejection reason of other policy that I forgotten. Also I does not have any cancellation proof of second policy.

So can I update such details after issuance of policy??

Dear User,

Yes.

Dear sir , I have applied for one term insurance but due to lockdown they are unable to conduct physical medical and then I applied for other company term insurance through policy bazar which is based on tele medical. The second insurance company representative asked me to cancel my first application before they procide for further process of underwriting after telemedical.

Should they insist me to cancel my earlier application before issuing policy ?

Dear Reader,

They can’t insist on you so. Also, why you are SO EAGER to buy immediately? Let the lockdown over, then complete the process.

It is laughable condition , I have already wanted to purchase insurance but delayed it and when applied for the insurance it is delayed due to lockdown and somewhat to have cover during pandemic. Their was in the news also that IRDA is going to increase premium , can you tell about something about that..

Policy bazzar was also mentioning that earleir. One from the earleir term insurance rejection is not accepted by me as they have offered me reduced cover even after perfect medical but due to salary. So I think I have to also mention that rejection in my further application for insurance. Thanks a lot to you for your informative articles

Dear User,

IRDA will never increase the premium, it is the companies which increase based on their actuaries and business profit. Whether the insurance companies increase the premium or not, not sure. But who is spreading this UNCONFIRMED news don’t know.

Various news websites published that from april irda is going to increase premiums as they are not revised premium from various years. the policybazzar flashed this news till mid april that premium gona increase in few days. Did not know how they are saying that?

Dear User,

I consider all of them as rumors until and unless there is confirmed news from the insurance companies.