LIC is launching one more new plan on 3rd February, 2016. This is again typical endowment plan called Jeevan Pragati (Table No.838). Let us see in what way this will give you Pragati (Progress) in your financial life.

Few silent features of this plan are as below.

- It is non-linked endowment with profit plan. This means it is not an ULIP plan but a typical endowment plan or traditional plan.

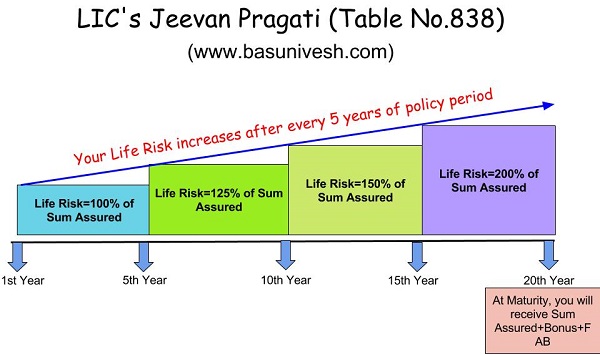

- The only additional feature of this plan is, the death sum assured increases after every 5th year. I will explain it in detail later.

The above information is suffice to say that there is nothing new in this plan. But the only added feature is that death benefit which increases during policy period.

Let me explain the same in below image.

You notice that this plan is unique only when it comes to increasing of life risk at every 5th year of policy period. Apart from this there is nothing much you can expect.

This is the information which is available at this point. However, I will update this post once I get premium chart and all details.

However, to know about how to calculate the LIC policies maturity values or return on your investment, read my earlier post “Video tutor-How to calculate LIC policies maturity amount and returns?“. You can also view the below video, where I explained about how to calculate LIC policies maturity amount and returns.

sir meri age 28 hai mein lic ki konsi polocy lun jo mere liye beter ho

Manoj-Term Insurance.

Sir First of all Thank You for doing a wonderful job by educating about financial planning.

I want to purchase a Term end policy. My age is 27 yrs, Monthly income 32,000/- in a Gov. Job.

Please suggest me a suitable Term plan for 50 Lakhs.

Should i go for any rider with it, like accidental or disability or critical illness etc.

Thank You

Ambesh

Ambesh-Refer my latest post “Top 5 Best Online Term Insurance Plans in India-2016“

Sir

would like to know good policy cover for life ( for home loan linked) for 58years age joint owner 49 years. Rs 50 Lakhs.

The premium payable for 5 years committed for 10 year term loan and cover.

ICICI Prulife initially quoted 69000 pa incl tax but after med test – diabetic increased the premium to Rs 1.20 L per annum. Feel it is too hight

pls suggest any other agency or policy

Srinivasan-I have not done any research on this front. Sorry.

dear sir

i am ram 41 yrs i need a lic policy for me please suggest

Ram-LIC policy for investment or insurance?

Sir the above video was helpful..can you share that excel sheet for looking into various premiums and the benefits..

Gowtham-Various premiums and benefits can be arrived at premium calculator available on LIC portal.

Dear sir,

I am confused by the way u are just getting term insurance policies ahead of endowment policies but i understand that some reason may be behind this…If endowment gives u returns both at your death and ur survival,and term plans only offers only on your death ,how it is better case ???can you explain..waiting for ur reply

Anesh-How much return? How much insurance? For how long your family survive on this insurance? Think and decide. I am not forcing you to buy anything.

Hi Basavaraj Tonagatti,

I have 3 LIC policy only.

1.New Bima Gold – 25,000.00/annum coverage 5 lakh started on 2010

2.Jeevan Chhaya – 72,000.00/annum coverage 13 lakh started on 2012

3.Jeevan Anand – 51,000.00/annum coverage 10 lakh started on 2013

Apart from that I have one Sukanya samriddhi account.

4.Sukanya samriddhi 50,000/annum started on 2015

I know these are very big mistakes done during my earlier days.Now I want to balance my investment and some I wanted to invest in SIP.

Kindly suggest me which LIC I can surrender with minimal loss and invest some in SIP.

Best Regards

Amiya

Amiya-Surrender all policies which completed 3 years.

Thank you for you response.

What is the next step? Kindly suggest how to invest 2lakh/annum in different direction for better return?

And what about sukanya samriddhi?

Regards

Amiya

Amiya-First create your basics. Buy term insurance, health insurance, accidental insurance and create an emergency fund of at least 6-12 months household expenses. Then think about goals.

Hi Basavaraj,

Thank you for your suggestion.I am working with an MNC and already have company provided health insurance for family.

My age is 35 yrs now and my goal is to achieve at least 1 Cr within 15 yrs. Regarding investment plan I am planing to invest in SIP mutual fund.

Kindly suggest how can I achieve this?

Amiya-This is where all do mistake. What if from next year onward your company stopped to provide you health insurance? How you get covered once you retire or during out of job periods? You must have your own health insurance. Regarding your expectation of Rs.1 Cr target amount after 15 years, if we assume equity investment returns as 12%, then you need monthly investment of Rs.20,000. However, do remember that the current value of Rs.1 Cr not be same after 15 years.

Hello sir,

This product will not give more than 6-6.5% return over a 20 year policy period (like any other Endowment or money back plans from LIC)

Suppose if this product doubles investment over 20 years (like any other LIC plan) in case of regular investment plan, IRR works out be around 6.22%.

However, my question is can ULIP give a better return?

I still believe there is a merit to consider ULIP instead of traditional plans. There is every possibility that over the next 20 years, Indian stock market will give better returns (inflation beating that is). In that case can I expect to get 3 times of my original investment? IRR works out be 9.60% in that case. I believe yes.

I know that to materialize the same, fund should generate CAGR of 12% p.a. over a period of 20 years. However, I think it is possible given India’s transformation from being a developing economy to developed economy.

Investing through mutual funds will give even higher returns. However, for people who are ready to take risk but are obsessed with “Insurance” can certainly give try to ULIP instead of traditional plans which have lost their relevance.

Thanks

Ritesh-Hard part of ULIPs are, you don’t have control over your portfolio, less liquidity, no track record of fund or fund manager.

dear sir plese tell me which instrument gives guarantee 8 to 9% interest risk free, tax free etc

Gopala-Timeframe?

Respected Sir, I have noticed that from ur discussion about jeevan Anand or jeevan pragati is not benefited for people, so please inform me which is better for young people like 23years old from Lici.

Swajan-LIC’s online term insurance plan 🙂

Hi Basavaraj,

Many thanks for putting your thoughts over this plan.

I have noticed you criticizing (and not condemning) almost of the LIC’s plans (again no disrespect to you here), you have always given logical and mathematical reasoning to support your views.

Has there been a plan in LIC’s history which you think in true sense is a product that has benefited an investor?

Over the years I have heard much about the plans like Jeevan Saral and new Jeevan anand from my colleagues.

I am not a fan of insurance products as such and have always look around for better mutual funds to invest rather investing in ULIP or other insurance products.

Regards

Durgesh

Durgesh-Again the Jeevan Saral and Jeevan Anand are under my criticism. The only products which I love in LIC are it’s online term insurance and Jeevan Akshay VI.

Hi

Hope you are doing great!

Could you please advise about Kotak Platinum Unit Linked Insurance Plan?

Regards

Pranav

Pranav-It is typical ULIP plan, look at the charges. They are high, less liquidity and no past track record to believe that it perform well. Hence, stay away.

ok thanks . Could you please suggest any ULIP

Pranav-STAY AWAY.

Dear Sir,

Thank you so much for knowledge sharing.

Vaishali-Pleasure.

Thank you.

I came to know this site about 15 days back. So far i read almost 70+ articles.

After readying all this information, I came to know that how much I was illiterate in Finance.

This is one of the best sites I have come across in my life.

Thanks again.

Chandrasekhar-Pleasure to know that and I request you to spread with awareness among others.

While calculating returns on LIC policies about which you are not satisfied about, you take into consideration the whole premium . Insurance premium can be separated into 3 parts- service tax, risk premium, investible corpus. LIC’s return on investible corpus is 7-9 per cent and that’s not really bad considering the fact that there is a lot of liquidity in LIC products.

Mazibar-Why commenting in different name? Take my reply to your same comment but with different name 🙂

Bibek-Is it? Anything that goes from my pocket is investment to me. At first we must consider this as an insurance product. Second thing, may I know how you calculated which claims 9% returns? Liquidity in LIC product? Let me share one real life experience. A husband of an LIC agent took Rs.45 lakh endowment plan. Premium is Rs.3,60,000 per year. Now let me know when he will at least be able to get what he paid+5% return on it. This is how LIC products sold in India-9% good return for long-term INVESTMENT, GUARANTEE and HIGHLY LIQUID.

While calculating returns, you take the whole premium into consideration. But the fact is, the total premium is divided into 3 segments 1. service tax. 2. risk premium. 3. Investible corpus LIC gives more than 7 per cent to 9 percent returns on the investible corpus which is is no way a bad investment considering the fact that there is enough liquidity in LIC products.

Bibek-Is it? Anything that goes from my pocket is investment to me. At first we must consider this as an insurance product. Second thing, may I know how you calculated which claims 9% returns? Liquidity in LIC product? Let me share one real life experience. A husband of an LIC agent took Rs.45 lakh endowment plan. Premium is Rs.3,60,000 per year. Now let me know when he will at least be able to get what he paid+5% return on it. This is how LIC products sold in India-9% good return for long-term INVESTMENT, GUARANTEE and HIGHLY LIQUID.

Yes LIC’s returns on the investible corpus are around 7-9 percent. Mazibar and I are of this view.. You take into consideration the risk premium as well which is not invested in the market. The service tax amount is the amount to be deposited in the Govt’s exchequer. Mortality rates go up with increaing age and you are aware about it. You must have heard that when Health Plus table no 901 was launched, not all the premium paid qualified for sec 80 D. In fact , the investible corpus qualified for sec 80 c. In my discussion with the Actuary dept., I culd learn how liquidity affects the rate of return. The actuary also apprised me with the fact that when you calculate returns on insurance products you must deduct he risk premium. Yes, it is true, returns on LIC products range between 7-9 per cent.

Bibek-By changing name as Bibek and Mazibar, you can’t hide your IP address, which is one and same. Why you are commenting with two different names? Wait for evening, I will come up with reality of this plan 🙂 When I being an investor consider my whole premium as an investment, it is left with LIC to disburse according to their wish, it is not my business friend 🙂 Hence, I consider the whole premium for my return expectation. In all products there are expenses, if according you I calculate, then I have to deduct that expenses then arrive at return on investment.

Hello Basavaraj,

I don’t have any specific question about this policy.

You are doing a wonderful service and i thank you for that. The moment i heard about Jeevan Pragati policy , i entered your site and there i have the information about it. You are so up to date with the present market and for sure there will be thousand others like me getting benefited.

Thanks

Santhosh

Santhosh-Pleasure to know about it 🙂

Hi,

Nice details. I have couple of questions, listed below

1) how is it different from Jeevan Anand.

2) After maturity, will it pay SA in case of death like Jeevan Anand.

3) My age is 30 Years. I want to take it for 21 years. What will be the premium for 10 lacks.

Chandrasekhar-1) In Jeevan Anand your life risk will be same throughout policy period. Also life risk in this plan stops at maturity or at death. In case of Jeevan Anand after maturity the life risk continues without any further premium payment.

2) No, after maturity there will not be any benefit. Policy ceases there itself in Jeevan Pragati.

3) Just read my review, if you feel the return of 5% to 6% is great earning for long term investment, then go ahead.

New Jeevan Anand (815) is the Best Compare to Jeevan Pragati (838)

Baburam-HOW?

Hello sir,

Great thanks for continuous sharing your knowledge. Thank god, LIC rejected BIMA GOLD policy for me.

Bipin-Lucky you are 🙂