LIC is launching another health insurance related plan called LIC Cancer Cover (Plan 905) on 14th Nov 2017. This is such second health insurance product launched by LIC. Let us see it’s features, benefits, and review.

Many of you may not aware that LIC also offering one health insurance plan. I already wrote about this plan. Please refer the same at “Jeevan Arogya-Do you know this LIC’s Health or Medical Insurance Policy?“. This plan is comprehensive health insurance plan.

Now LIC is launching a disease-specific health insurance plan. This is called as LIC Cancer Cover (Plan 905). This is a non-linked (traditional), regular premium payment health insurance plan which provides fixed benefit in case the Life Assured is diagnosed with any of the specified stages of Cancer during the policy term (subject to certain terms and conditions).

Eligibility for LIC Cancer Cover (Plan 905)

First, let us look at the eligibility conditions to buy this product.

You noticed that the maximum coverage is Rs.50,00,000 only. Also, the maximum entry age is 65 years. You can buy this plan ONLINE. Policy can be assigned under as per Sec 38 of Insurance Act 1983.

Options in LIC Cancer Cover (Plan 905)

This product offers you two types of Sum Assured options. Also, your premium varies based on the option you choose. You have to choose this option at the time of buying this plan.

Option I – Level Sum Insured

The Basic Sum Insured shall remain unchanged throughout the policy term. Hence, the premium will also remain same throughout the policy period.

Option II – Increasing Sum Insured

The Sum Insured increases by 10% of Basic Sum Insured each year for first five years starting from the first policy anniversary or until the diagnosis of the first event of Cancer (whichever is earlier). On diagnosis of any specified cancer, all the claims payable shall be based on the Increased Sum Insured at the policy anniversary coinciding or prior to the diagnosis of the first claim and further increases to this Sum Insured will not be applicable

Hence, if you choose this second option, then the premium will not remain same throughout the policy period.

Benefits of LIC Cancer Cover (Plan 905)

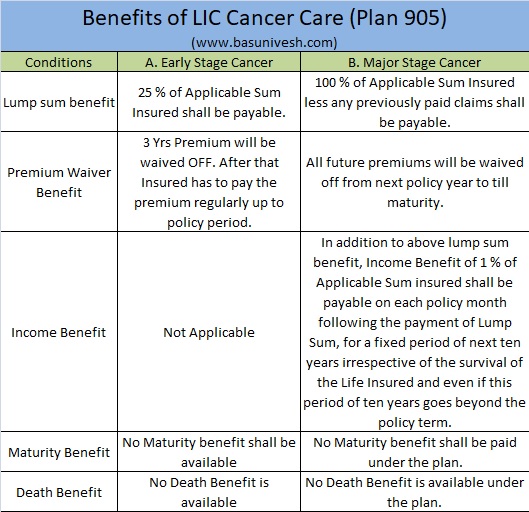

The benefits under LIC Cancer Cover (Plan 905) is divided into two stages. Do remember that this is disease specific. Hence, if you suffer CANCER disease during the policy period, then only you will get the benefits.

There is no Surrender Value, No Loan Facility, and No maturity benefit. There are two classifications of benefit.

1. Early Stage Cancer

Benefits payable on the first diagnosis of any one of the specified Early Stage Cancers, provided the same is admissible are as below.

(a) Lump sum benefit-25% of Applicable Sum Insured shall be payable.

(b) Premium Waiver Benefit– Premiums for next three policy years or balance policy term whichever is lower, shall be waived from the policy anniversary coinciding or following the date of diagnosis.

c) After 3 years premium waiver, insured has to pay the premium regularly up to the policy period.

Early Stage Cancer Benefit shall be payable only once for the first ever event and Life Assured shall not be entitled to make another claim for the Early Stage Cancer of same or any other cancer. However, the coverage for the Major Stage Cancer under the policy shall continue until the policy terminates.

2. Major Stage Cancer

Benefits payable on the first diagnosis of the specified Major Stage Cancer, provided the same is admissible are-

(a) Lump Sum-100% of Applicable Sum Insured less any previously paid claims in respect of Early Stage Cancer shall be payable.

(b) Income Benefit-In addition to above lump sum benefit, Income Benefit of 1% of Applicable Sum Insured shall be payable on each policy month following the payment of Lump Sum, for a fixed period of next ten years irrespective of the survival of the Life Insured and even if this period of 10 years goes beyond the policy term. In case of death of the Life Assured while receiving this Income Benefit, the remaining payouts, if any, will be paid to his/her nominee.

(c) Premium Waiver Benefit-All the future premiums shall be waived from the next policy anniversary and the policy shall be free from all liabilities except to the extent of Income Benefit as specified above.

Once a Major Stage Cancer Benefit is paid no payment for any future claims under Early Stage Cancer or Major Stage Cancer would be admissible.

If the life assured claims for different stages of the same Cancer at the same time, the benefit shall only be payable for the higher claim admitted under the policy.

If there is more than one Cancer diagnosed in an event, the Corporation will only pay one benefit. That benefit will be the amount relating to the stage of Cancer which has the highest benefit amount.

I will explain you the same in detail from below table.

You may feel somewhat confused by referring above table. Let me explain the same using the below image.

Do remember one thing again. THERE IS NO MATURITY VALUE, NO SURRENDER VALUE AND THIS POLICY IS NOT ELIGIBLE FOR LOAN.

Tax benefits of LIC Cancer Cover (Plan 905)

The Premium you pay towards this plan will be eligible for deduction under Sec.80D up to Rs.55,000 per year. Do remember that you will not be eligible to claim the benefits of premium paid under Sec.80C. (To know more about Sec.80D, refer my post “Tax Savings options other than Sec.80C for FY 2017-18“.

Review of the Premium of LIC Cancer Cover (Plan 905)

Premium calculated will remain unchanged up to 5 years ONLY. After 5 years premium may change according to the claim experience of LIC and if changed, it will then remain unchanged for next 5 years. (Any revision in premium will be calculated according to entry age of proposer at the date of commencement of the policy)

LIC Cancer Cover (Plan 905) – Definitions of the Cancer covered

I. Early Stage Cancer-

The diagnosis of any of the listed below conditions must be established by histological evidence and be confirmed by a specialist in the relevant field.

# Carcinoma-in-situ(CIS)

Carcinoma-in-situ means the presence of malignant cancer cells that remain within the cell group from which they arose. It must involve the full thickness of the epithelium but does not cross basement membranes and it does not invade the surrounding tissue or organ. The diagnosis of which must be positively established by microscopic examination of fixed tissues.

# # Prostate Cancer–early stage

Early Prostate Cancer that is histologically described using the TNM classification as T1N0M0 with a Gleason Score 2 (two) to 6 (six).

# Thyroid Cancer – early stage

All thyroid cancers that are less than 2.0 cm and histologically classified as T1N0M0 according to TNM classification.

# Bladder Cancer – early stage

All tumors of the urinary bladder histologically classified as TaN0M0 according to TNM classification.

# Chronic lymphocytic Leukaemia – early stage

Chronic Lymphocytic Leukaemia categorized as stage 0(zero) to 2 (two) as per the Rai classification.

# Cervical Intraepithelial Neoplasia

Severe Cervical Dysplasia reported as Cervical Intraepithelial Neoplasia 3 (CIN3) on cone biopsy.

II. Major Stage Cancer-

A malignant tumor characterized by the uncontrolled growth and spread of malignant cells with invasion and destruction of normal tissues. This diagnosis must be supported by histological evidence of malignancy. The term cancer includes leukaemia, lymphoma and sarcoma.

LIC Cancer Cover (Plan 905) – Exclusions

Exclusions from all early-stage cancer benefits

# All tumors which are histologically described as benign, borderline malignant, or low malignant potential

# Dysplasia,intra-epithelial neoplasia or squamous intraepithelial lesions

# Carcinoma-in-situ of skin and Melanoma in – situ

# All tumors in the presence of HIV infection are excluded

Exclusions from all major-stage cancer benefits

A malignant tumor characterized by the uncontrolled growth and spread of malignant cells with invasion and destruction of normal tissues. This diagnosis must be supported by histological evidence of malignancy. The term cancer includes leukemia, lymphoma, and sarcoma. The following are excluded from major stage cancer benefits.

# All tumors which are histologically described as carcinoma in-situ, benign, premalignant, borderline malignant, low malignant potential, neoplasm of unknown behavior, or non-invasive, including but not limited to Carcinoma-in-situ of breasts, Cervical dysplasia CIN-1, CIN-2 and CIN-3.

# Anynon – melanoma skin carcinoma unless there is evidence of metastases to lymph 4 nodes or beyond;

# Malignant melanoma that has not caused invasion beyond the epidermis;

# All tumors of the prostate unless histologically classified as having a Gleason score greater than 6 or having progressed to at least clinical TNM classification T2N0M0

# All Thyroid cancers histologically classified as T1N0M0 (TNM Classification) or below;

# Chronic lymphocytic leukemia less than Rai stage 3

# Non-invasive papillary cancer of the bladder histologically described as TaN0M0 or of a lesser classification,

# All Gastro – Intestinal Stromal Tumors histologically classified as T1N0M0 (TNM Classification) or below and with mitotic count of less than or equal to 5/50HPFs;

# All tumors in the presence of HIV infection.

Waiting Period in LIC Cancer Cover (Plan 905)

A waiting period of 180 days will apply from the date of issuance of policy or date of revival of risk cover whichever is later, to the first diagnosis of “any stage” cancer. “Any stage” here means all stages of Cancer that occur during the waiting period. This would mean that nothing shall be paid under this policy and the policy shall terminate if any stage of Cancer occurs:

- At any time on or after the date of issuance of the Policy but before the expiry of 180 days reckoned from that date; or

- Before the expiry of 180 days from the Date of Revival.

Survival Period in LIC Cancer Cover (Plan 905)

No benefit shall be payable if the Life Assured dies within a period of 7 days from the date of diagnosis of any of the specified Early Stage Cancer or Major Stage Cancer. The 7 days survival period includes the date of diagnosis. The benefit under this plan shall be payable subject to fulfilling all of the below criteria:

- 7 days survival period from the date of diagnosis

- Signs and symptoms relevant to cancer should have been present and documented before death

- All investigations to confirm the diagnosis of cancer should have been done before the death of the insured.

- Satisfaction of the cancer definition as per the policy condition

LIC Cancer Cover (Plan 905) Review

As of now, I have limited information about this plan. Hence, I will not point out anything. Once I get the full picture of the plan, then I will review it again. However, as of now, I may share views.

- The biggest advantage to save the cost is, customers can buy this plan ONLINE. By purchasing it online, you can save the premium (7% of Tabular Premium).

- The premium will be less as this product acts like typical term life insurance where there will not be any maturity benefit, surrender value, paid-up value or loan value. Only in the case of event happening (in this product if you suffer due to cancer), insured will get the benefit.

- In case of identifying the major stage cancer, the benefits are much much better. Because you no need to pay the future premiums, 1% of applicable sum assured will be payable for the next 10 years (irrespective of the term of the policy left).

- Premium changes every 5 years. Hence, unlike endowment or money back plans where the premium remains constant, here the premium will alter based on the claim experience of LIC. Hence, if the premium is not affordable after 5 years, then you will end up with cancer cover.

- There are 180 days waiting period. Hence, the risk will not start immediately after buying the policy.

- Survival period of 7 days also applies to this policy.

- In case of increasing sum assured, even though your sum assured will increase each year by 10%, but such increase is restricted to “for first five years starting from the first policy anniversary or until the diagnosis of the first event of Cancer, whichever is earlier”. Hence, it will not benefit you in long run. You have to again buy one more such policy after such 5 years over to cover the cost of cancer treatment at that time.

- This is exactly like term life insurance but disease-specific. Hence, if you do not suffer from cancer during the policy period, then you will not get any policy benefits like typical endowment or money back plans.

- NO TPA involved here. Hence, the claim may be bit cumbersome and sometimes depends on how the concerned official will take it forward.

- Tax benefits under Sec.80D BUT not under Sec.80C.

- There are many cancer-specific insurance products available from general insurance companies. I am not sure why LIC entered into this field.

- A normal person finds it hard to understand the exclusions. Hence, hard for common man to relieve that they are protected from cancer disease.

- You can’t buy it for your family like general insurers provides you. You have to buy individually. This may create managing multiple plans and also cost may shoot up.

- If there is more than one Cancer diagnosed in an event, the Corporation will only pay one benefit. That benefit will be the amount relating to the stage of Cancer which has the highest benefit amount. This I think a hindrance to this product also.

- Also, early stage cancer can be claimed ONLY ONCE during the policy period.

What is mother had cancer and she died. Now if I want to take cancer cover, does LIC allows to issue policy to person like me, having cancer family history.? I saw that some private insurer is not accepting this .

Dear Sagar,

It depends on the underwriter’s decision. Please approach the LIC.

What is the Grace period of the policy to pay the premium after due date??

Ravi.

Dear Ravi,

To which policies you are asking for?

I am 44 years old, male. What medical tests i need to undergo for this cancer policy?

Dear Ajay,

It depends on LIC. Better you be in touch with your nearest branch for the same.

Does this policy cover all types of cancer which is happen to us bcoz in policy wrote tht if any cancer happen which is specified thn we get benefit so pls help me to get exclusions and limits of this policy so I can under stand this policy easily

Dear Mahesh,

There are specific categories of cancer mentioned and accordingly, they pay.

Hello,

My mother is 49 and she has Pemphigus Vulgaris disease. Can I take this policy for her ?

Does this policy cover all types of cancer ?

Dear Sreesha,

Eligibility fo your mother for this policy depends on LIC’s decision. Yes, it covers all types of cancer.

Im 33 years old, I was planning to buy a cancer policy for myself of 25 lakhs

after going through lot of information about it, I have shortlisted two policies

1) LIC Cancer Cover (15 Lakhs)

2) HDFC Cancer Cover (10 Lakhs Increasing Sum assured)

Query was regarding, Can I buy 2 policies for the cancer cover and claim them together

the reason being, the HDFC is providing me the policy term of 53 years where as LIC is offering me the maximum of 30 years of term.

So do you think its an viable option to buy two cancer policies for a longer duration.

Dear Avinash,

Yes, you can buy so. But I suggest to go with one.

Is this plan applicable after plan mature??

I mean life long benefit???

Dear Aneesh,

NO.

Hi Basu

Thanks for the review on LIC cancer cover. I have following questions:

1. Is a medical check-up required for this policy? I am 36, Male.

2. I want to insure myself and my wife under this plan. I understand I cannot be the proposer. So will it be possible for her to individually buy it online on her own…with her own login and other details?

3. What happens to the balance 75% after the 25% payout on first stage cancer diagnosis…?

Thanks in advance.

Dear Mandar,

1) Depends on case to case.

2) Yes, she can buy so.

3) Refer features once again.

Hi Sir,

Would you recommend a cancer protect plan apart from a critical illness plan? (Health insurance policy of INR 10 lakh is already taken)

Dear Kenneth,

Not required.

What is pre-existing condition?, I had thyroid infection a few months back , now it is recovered and am in good health , does it matter to apply for this policy, or pre-existing means only pre-existing cancers in this context?

Dear Sammy,

Yes, pre-existing means related to cancer only.

Sir i am suffering form DVT and liver problems so can i get this policy and what is the emi.

Dear Seema,

It is hard to say so. Because the decision depends on the underwriter of the LIC.

Hi Basu,

I have already got this policy last year. Now in case I go abroad for a couple of years to work and there is no change my citizenship, will this policy still be applicable for me?

Dear Subhasis,

YES.

Hi!

Can a person consuming alcohol occassionally take this policy? Also if there is family history of cancer, is it possible to take this policy?

Thanks

Dear Anshu,

Yes, such alcoholic and family history of cancer person can take this policy. However, the final decision is left with LIC underwriter.

Hi Basavaraj,

I was checking the premiums of this plan and ICICI Heart + Cancer care for my wife. The premium for this plan came to 9369, where as for ICICI it was 7000. The only difference is for this policy the 1% of SA paying period is 10 years, where as for ICICI it is 5 years. I was unable to figure out the exclusion criteria for both these policies. Could you compare the exclusion criterias for these policies. Any other comment is also welcome.

Dear Amartya,

They usually define exclusions in a generic way. However, my suggestion is to go with LIC.

Hi Basavaraj,

Thank you very much!

Another question – can I go for LIC for a moderate SA at the moment now, and at a later stage, when I’ll have some more spare cash buy another one from some other insurer.

Thank you

Dear Amartya,

You can do so.

Hi,

If the claim get settled after diagnosis of cancer, is this amount taxable under income tax provisions, if yes, under which section and how much

Rohit-It is tax-free.

sir,

if one persons (man) sister suffered breast cancer,can he take cancer cover policy?

Aneesh-She has to take it on her name.

Hi

Do you have any review on the Max Life Insurance’s “Cancer Insurance Plan”? and its benefits and drawbacks?

Thanks

Ganesh

Ganesh-NO.

Sir breast cancer is covered or not in LIC cancer cover plz clarify.

Babita-I think NO. But I am not expert to understand those medical words. Hence, suggest you to cross check with LIC Branch before proceeding.

dear Basavaraj

please help me to get a good health policy [family floater plan] for my family having wife + 2 kids with s.a. for 7.5 -10 lacs

I am from kolkata , my age is 47 yrs, wife 39 yrs , 2 kids 9 yrs+14yrs

regards ……

Tapas-Refer my post “IRDA Incurred Claim Ratio 2016-17 | Best Health Insurance Company in 2018“.

Can I apply for this on behalf of my father who is being diagnosed for cancer? It’s a major stage cancer.

Anshuman-Try your luck.

Dear Basavaraj,

Ltl bit confusion in 1% Payout Condition, please clarify if you can.

so the 1 % of sum assured will get pay on monthly basis or it will calculate as yearly and divide in months payout.

like an example if we take 10 Lakhs sum assured then payout will be 10000 p.m straight forward or it will 833 per month (10000/12).

Kindly reply.

Regards,

Deepak

Deepak-It is 1% on monthly.

Whether LIC’s Cancer cover plan can be allowed to the children whose parents are suffering from Cancer?

Ashim-It can be but purely left with LIC’s underwriter decision.

Article didnt clearfy that should i go for hdfc cancer care or lic cancer care for each 30 lakh?? Which is the best one? Lic or hdfc…

Kanwardeep-It depends on individual’s choice.

WHICH HAS LESS EXCLUSIONS….AS WE CANT UNDERSTAND THEM…WHAT IS WHAT..? PLS TELL IF WE CONSIDER EXCLUSIONS ON BOTH POLICIES WHICH ONE SHOULD I CHOOSE???

Kanwardeep-Hard to say and list them in a single post. You have to dig it.

Im 27, i want to take policy for future, agar hdfc or lic mein cancer care leni ho to aur claim lene k waqt jo asaani se claim de de……pls answer in just one word…. Kaun si lu??

Kanwardeep-For me all insurers are equally good and bad. However, if you are looking for readymade TIPS, then sorry.

Sir, eligibility of assignment is mentioned under Eligibility conditions of the plan and Ins.Act is mentioned as 1983. If it is not allowed then rectify both.

Achla-Yes, sorry and thanks for correcting.

Hi,

I had cancer about 10 years ago. It was hogdkin beginning stage. I completed 12 sessions of Chemo and have had perfect health since.

Is there any medical, critical and life insurance that I can apply for? I’ve tried but most companies reject.

Thank you

Dylon-Hard to say but you can try your luck.

There is one plan from star health for cancer patients.

Insurance Act 1938 section 38 allows assignment of policy ,please recify.

Achla-This plan as per me not eligible for assignment.

Very nicely explained a useful product so that a layman can also understand d pros n cons and raise the queries as per his requirements.

Achla-Pleasure 🙂

Which is the best cancer care plan among icici Lombard heart and cancer care, HDFC cancer care and lic cancer care. Also let me know which plan covers breast cancer too

Pankaj-I prefers LIC.

Dear Basu,

Please let me whether oral cancer and or breast cancer is covered or not under this policy

Regards

Anurag-In my view YES.

Basavaraj Tonagatti Sir,

SIR YOU HAVE VERY WELL EXPLAINED THE PLAN, I HAVE CHECKED THE PREMIUMS.

PREMIUMS ARE REASONABLE.

INCOME BENEFIT IS THE MOST ATTRACTIVE FEATURE.

A VERY GOOD PLAN LAUNCHED BY LIC OF INDIA.

THANKS SIR

Mohan-Yes, but I have only one concern that how LIC handle the claims. Otherwise, a better featured plan.

Does this policy cover endometrium cancer (EIN – Endometrial Intraepithelial Neoplasia)

Saravana-I think it will cover. But still, suggest you to discuss the same with LIC Officials.

Hello Sir,

Is the LIC Cancer Cover (Plan 905) is applicable to person already diagnosed with breast cancer?

Ashwini-It is not sure from LIC features. Hence, better you propose with LIC and let them decide.

No, Star Health Cancer care policy you can check it out

hi,

thanks for the information,

i am looking for critical illness policy not only cancer but there may be multiple illness covered.

i have gone through Ipru’s critical illness policy is it good? or there may be other options available.

Thanks,

Sandeep

Sandeep-Refer my blog post “Best Critical illness policy in India – Comparison Table“.

Hello sir

I want to know which policy in the market is protected for cancer cured person.

I mean who’s cancer was cured from 7/8 years ago.

Jayesh-Hard to say and you have to propose and based on that they will issue.

Thank you for the informative article.

I want to take this policy, but the lic link is not loading when i click the option for new cancer cover plan.

Is the LIC website always like this? I am thinking I will take this plan through an lic agent.

DO you know how much the cost diffrence in rupees may be ? I saw you mention something about 7% , does that mean if my premium is 10000 online , then I will pay 10700 if I pay through the agent with no other extra charge ?

Thanks for reading my long post.

Sany-May be portal is in Maintainance mode. Better to try on Monday or Tuesday and I suggest you to buy it ONLINE.

Thankyou Mr. Basavaraj, you have elaborated each points in a very easy way.

Rajkumar-Pleasure 🙂

Thankyou Sir, Its very useful Plan.

Hello Basavaraj

Greeting ..! very useful information.!!!

If the mother or father of the family died in cancer , is it possible their children to buy this policy?

some of the other policies are not allowing it

Thanks in advance

Michael-It is hard to say so. Because it is purely the decision of LIC’s underwriter’s decision.

Basu,

May i know who is LIC’s underwriter..?

Can you please elaborate it ?

Thank you for the prompt reply

Michael-It is their officials who do the underwriting job (in each branch level). Hence, hard to say who is for whole LIC.

Hi Basu

The premium as compared to other plans are very high.

Pls put a comparison table with hdfc, ICICI and future generalii

Ajay-May be high but for lot of us it is RELIABILITY.

One of the common cancer for women is breast cancer which seems to be excluded here.

Could you please confirm on this.

Manish-May be but I am not sure of technical terms of what and in which category they consider it.

Great Post! Thanks for sharing Features, Benefits, premium etc of LIC Cancer Cover (Plan 905).

Rajiv-Pleasure.

In 90s there were two policies Ashadeep and Jeevan Asha where some diseases were covered including malignancy. Theses policies fall under endowment and the claim settlement ratio under these policies is good. The claims are processed by LIC staff in consultation with DM. Nobody should be worried about claim settlement as the people in LIC are quite experienced.

Manoj-I know about both policies. But do anyone or any agents sold those policies saying they also cover such diseases??? Even if agents were told, how many claims arrived with such diseases??

Dear Sir,

I have studied the brochure of HDFC cancer care, Star Cancer care policy. Among the said policies and LIC cancer care, I felt LIC cancer care is very reasonable in cost, coverage is good and exclusions are reasonable. Waiting period in HDFC is 48 months, which is 6 months here. Preconditions in HDFC is much more than LIC. Star brochure is little confusing, it states that it covers persons diagnosed with cancer. Waiting period is the most dangerous clause and you should always observe that in any cancer care policy Sir. According to the policy, patient should NOT be diagnosed of cancer or cancer causing lesions during Waiting period.

Sir, it feels like this policy of LIC is far better than HDFC cancer care, but premium is costly, but in reliability LIC is good i feel.

Sir, OVERALL you have analysed this policy very nicely.

regards

RAJESH PAI

Rajesh-I agree most of your points. Also, when you compare the existing plans, this plans holds good. No doubt in that. My only concern is how fastly the LIC settle the claims. Because this plan is not Life Insurance. Rest of all features are good to me.

Dear Basavaraj,

Can you please suggest which Cancer Insurance Policy in the market has the widest cover available for (a) Individuals (b) Family Floater

Thanks in advance for your help

Sunbir-Check with general insurers or standalone insurers. Like many critical illness insurance products by default covers cancer insurance. This I feel exhaustive than going for separate cover for each such major diseases.

do we have to go though medical check up to take this policy i want to take this for my parents age 65 & 62

how can i take this

Rohit-Check underwriting rules with the LIC Branch.

No Need for any medical check up for any age upto age 65

sir My sister in law thirumathi kannambal is suffering from second stage THROT AND LUNGS CANCER,and taking Treatment in Madurai Rajaji Hospital Since from2012, and now took FLUOROURACIL injection,ip500mg per week,HIS date of biorth is 03-02-1959.she is living with his mother at door no8-16/1,senbagamalar 11 street,viswanathapuram ,madurai 625014 and his cell no is 9842954644.kindly inform 1.can she eligible for major stage cancer cover [plan905],if so how much primium to pay. 2.whom i contactfor taking policy[he should come to her house for Dioganus the canser] 3.By this relation ,shall i be the proposer and his son as nominee,and document required 4.Regarding policy whatare all the documents required. thanking you for replay

Jeyaseelan-Sad to hear about your sister-in-law. In my view, LIC will not issue the policy as she is already suffering from cancer. However, if you want to try, then contact the local LIC Officials.

100 percent correct

Sir how come tax benefit of ?50000 u/s 80D.

It is 25,000

Rajwant-I said up to the maximum of Rs.55,000. Refer the link I shared for better understanding.

This policy is no doubt a good policy. But what will be the premium ? Premium charts may pl be provided.

Also Star Health has launched same policy. We have to ascertain the benefits first.

Pinak-You will get the premium chart on LIC portal. But in my view, without a second thought I may say that LIC premium will be costlier than Star. But you may go with LIC as a reliable insurer.

You are 100 percent not correct ,

LIC PREMIUM IS LESS THAN STAR

LIC BENEFITS ARE MORE THAN STAR EXCEPT ONE BENEFIT WHERE STAR GIVES POLICY EVEN TO AFFECTED PERSONS OF CANCER WITH ELIGIBLE TERMS BUT LIC PROVIDES ONLY FOR HEALTHY AS PER ELIGIBLE TERMS.

STAR GIVES MAXIMUM 5 LAKH AS SUM INSURED .LIC GIVES FROM 10 LAKH UPTO 50 LAKH

Sreeramkumar-Forget about to whom they give. I am neither franchisee of LIC or Star. Hence, I neither defending LIC or Star. Check Star premium they have the trick always to reduce the premium by infusing UNKNOWN co-payment clause. Hence, they offer at cheap.

Star health insurance

Cancer care and LIC cancer cover both not same coverage

Cancer care giving to cancer cured patients, its cover if insured get cancer again lump sum paid, and also cover regular cover for all disease. Normally cancer patients deny policy from insurer, policy covers relapse of cancer and mediclaim

Narayan-If Star providing coverage to cancer patients also, then at what COST?

As far as the LIC is concerned the claime settlement percentage is high.

At the same time the proposer should have thorough knowledge about the features and benefits of the Plan.

Sankarasubramanian-Claim settlement is HIGH only in case of endowment and money back plans but not in handling health-related products.

The claim settlement position in LIC ,both in Maturity claims & death claim is very good.Since the TPA is not roped in for settlement of claim, the claims will be solved without hassles,provided the very condition of contract of good faith is satistified. Since variety of illnesses are not being covered, the policy holder will be in a better position as regards the type of cover he can opt for.Otherwise, on many occasions the claims are rejected for operation of exclusion clauses,the life assured not being properly informed.

Dipak-Claims may be settled fast. But will LIC equipped the staff to handle such immediate settlement cases. Such products are not like typical Life Insurance Products.

Claim settlement will be assisted by Divisional Medical Referree, who’s a highly qualified doctor. Don’t worry about LIC’s ability to handle claims portfolio

Sreedhar-I am not worrying about LIC’s ability nor against this policy. But handling Life Insurance claims is different than handling the claims of such products. As you said, it will be assisted by DM Referree, it again consumes time as low-level officials have to wait for the process consent at top level.

I think it’s a very useful plan covering special disease like cancer. LIC’s claim settlement ratio is very good in comparison to others. Thanks sir for providing so good information.

Laxmi-LIC’s claim settlement is good by accepting the claims mainly of Endowment Plans. Hence, you can’t generalize and say that LIC is capable of handling such high-cost immediate result plans. LIC has to equip the team to handle at ultra speed.

The claim will be settled by LIC officials and not TPA is boon. As lics death claim settlement ratio is very high where the investigation is done by officials.

Ambatkar-Is the death claim settlement is same as claim settlement in this case? Whether you checked the average claim settlement Sum Assured of LIC?

Great day to you Sir.Under early stage cancer(optionA),only 25% is payable on diagnosis and three years premium stands waived.what will happen to 75% of SA? Whether it will be given for onward treatment if the same could not be cured at an early stage.If not what is the use of paying further premium? Please clarify.

Maala-Good question. But as of now, no clarity. However, the life risk will continue up to maturity and during that period, if you diagnosed with major stage cancer, then the facility will be applicable.

What will be the annual premium for a 65 yr. male under option 2 ?

Das-Wait for the launch on 14th.

Thank you for information on this new policy. It will be really helpful for us readers when you update your opinion and advice on this policy and compare it with other available options once you assess new information as and when available.

Surya-Surely I will.

Since Medicaid policy cover cancer also.Do we need to buy it separately ?

Anjni-It may or may not based on policy exclusions. Also, the typical health insurance will not suffice such high-cost diseases. Hence, insurance companies launching standalone products.