IRDA recently published the Annual Report for FY 2015-16. Let us find out the IRDA Incurred Claim Ratio 2015-16 and which is Best Health Insurance Company in 2017 in India.

Note:-I wrote the latest IRDA Incurred Claim Ratio. Please refer the latest post “IRDA Incurred Claim Ratio 2016-17 | Best Health Insurance Company in 2018“.

What is the meaning of Incurred Claim Ratio or ICR?

Incurred Claim Ratio or ICR is a ratio of the total value of claims paid or settled to the total premium collected in any given year. This can be calculated as Incurred Claim Ratio or ICR=(Total Value of Claims Paid/Total Premiums collected)*100.

For example, let us say Company ABC settled the total claim amount of Rs.90 Cr in the year 2015-16. In the same year, it collected Rs.100 Cr as a total premium. In this situation, the incurred ratio stands to be 90%.

This Incurred Claim Ratio is applicable only to non-life insurance companies. For life insurance companies, IRDA publishes Claim Settlement Ratio. I have already written a post on the same. You can refer it at “IRDA Claim Settlement Ratio 2015-16 | Best Life Insurance Company in 2017“.

What to judge from the Incurred Claim Ratio or ICR?

This is the one of identifying the financial health of non-life insurance companies.

# Incurred Claim Ratio or ICR more than 100%

It indicates that for every Rs.100 they collecting as premium, they are paying more than Rs.100 as a claim for a year. In simple terms, your income is Rs.100 but your expenses are Rs.100 or more. So instead of profit, they are into loss.

# Incurred Claim Ratio or ICR less than 100%

It indicates that for every Rs.100 they collecting as premium, they are paying less than Rs.100 as a claim for a year. Such companies are making a profit as your income is Rs.100 but expenses are less than Rs.100.

What it indicates that less ICR means the company is in profit or eyeing on profit. So either they may insure the less risky individuals or groups (customers rarely come forward for a claim) or rejecting the claims just to profit.

However, rejecting claims only on grounds to profit will not work out for any company. They have to look for reputation, future growth, and regular guidelines. Hence, simply for the sake of profit making, they can’t deny claims.

In my view, going with companies of high ICR or low ICR is risky. Hence, always choose a company which is in between both these points.

Remember once again, ICR is not main criteria in selecting health insurance. However, it is one among many criteria.

IRDA Incurred Claim Ratio 2015-16

Now let us concentrate on IRDA’s Annual Report for 2015-16. We will check the IRDA Incurred Claim Ratio 2015-16 and identify which is the Best Health Insurance Company in 2017 in India.

Here, I will divide the health insurance companies into 3 categories. One as public sector companies, second as private companies and the third one as standalone health insurance companies.

IRDA Incurred Claim Ratio 2015-16 for Public Sector Health Insurance Companies

Below is the data for the public sector companies.

There is a jump in ICR New India’s ICR. Last year, it was 98.78%. However, this year it is at 114.64%.

The Oriental Insurance’s ICR reduced from earlier 117% to currently at 114% ( a marginal).

IRDA Incurred Claim Ratio 2015-16 for Private Sector Health Insurance Companies

In below chart, I will show you the ICR of private sector health insurance companies.

I marked with red for those companies whose ICR is below 50% and above 100%. I marked with blue for those companies whose ICR ranges from less than 100% to 80%. I marked with green for those companies whose ICR ranges from above 50% to less than 80%.

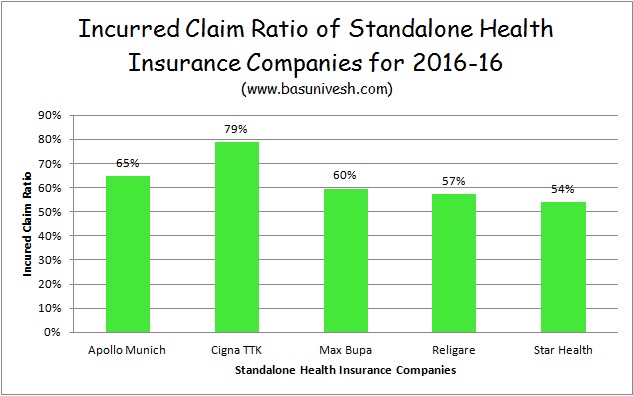

IRDA Incurred Claim Ratio 2015-16 for Standalone Health Insurance Companies

In below image, I will share you the IRDA Incurred Claim Ratio 2015-16 for Standalone Health Insurance Companies.

You notice that ICR ratio of all these standalone health insurance companies stands between 50% to 80%.

How efficiently General Insurance Companies handling Grievances of customers?

Above we saw the data related to their finance and how many claims they handled for FY 2015-16. Let us now concentrate on the numbers related to customers grievances. How many insurers resolved and how much pending?

In below image, I will show you the data of all General Insurance Companies Grievance Status for FY 2015-16.

Notice that in private sector companies, the worst customer grievance handling companies are Bajaj, ICICI, Reliance and SBI.

Whereas, in case of public sector companies, the numbers are worst (except United India). But all standalone insurers managed the grievances nicely.

Best Health Insurance in India in 2017 -Checklist to shortlist the product

Now we understood the financial health of insurance companies. Let us move forward and identify the points before selecting the health insurance.

# Coverage Amount-Concentrate on Sum Insured and think beyond the current hospitalization expenses. If premium costing you more, then fill the gap with the super top up plans.

# Buy early-Buying at the earlier age is best than postponing it. We don’t know the health issues. Hence, the insurer may reject your proposal. Hence, always buy immediately and never postpone.

# Understand the cover-Identify the features you want to cover. Covering all NOT POSSIBLE. Hence, try to identify the product which covers many illness.

#Individual or Family Floater-Decide whether you want to go for individual or family floater. It is always best to go for an individual if age of any one member of family is so high than the others. For example, in a family of 4 the oldest person’s age is 65 years and rest of other 3 members age is less than 50 years, then better to buy an individual plan for that 65 years old individual and rest 3 members can buy family floater.

Because the premium is fixed based on the age of oldest person also.

# Entry Age and renewable clause-Check the entry age and for how long one can renew it.

# Identify the company which covers existing diseases at early. Usually, all insurance companies have a waiting period 3-4 years for existing diseases. However, if your concern is to cover the existing diseases, then give first priority to this point.

# Check for room rent capping.

# Check for the co-payment clause. Higher the co-payment means lower the premium for you. Co-payment means how much you also have to pay in a total bill. If the co-payment clause states 20% co-payment, then for all bills claimed, you have to 20% and the rest 80% will be payable by health insurance company.

# Check for exclusions. If you feel the exclusions listed may be uncomfortable to you, then skip that product.

# Check for hospital network availability in your city or town. The cashless hospital benefit is better than producing the bills and waiting for claim settlement.

# Read carefully the wordings of policy brochure. If you have doubts on any feature, then try to clarify it NOW itself.

# Avoid all common features, which companies try to highlight.

# Check for No Claim Bonus company offers.

# Check treatment wise limit if any.

# Check the premium rates. Especially check the rates for older age rates as few insurers jump the rate drastically for older age coverage.

# Finally, if you feel the sum insured you opting is not within your budget, then go for sum insured according to your affordability and opt for a super top up plans.

Hope this much information is enough for you in shortlisting the health insurance product.

A simple, general question- If you were buying insurance for yourself, would you prefer public sector or private sector?

Dear Hitesh,

Good question 🙂 However, if I say my choice, then you too follow me? Each individual has a different view. Hence, I never give a SINGLE choice but OPTIONS.

1)What is the latest Grievances status of non-life insurance companies? Also, 2)how come public sector insurances have ICR of over 100%? 3)Do you personally think Apollo munich is a good company in terms of claim settlement? Policy bazaar & CoverFox are promoting them rapidly

(I used the sort option premium low to high and then compared it to the ‘recommended option’ & found that Religare was giving better features & lower premium than Apollo munich; Then how come they recommend it when both’s ICR are shit?)

Dear Hitesh,

I am writing on this with new IRDA annual report. Please for a while.

Dear sir

I have oriental mediclaim insurance since last 5 year. Now I would like to buy national insurance medicalim because the premium for oriantal insurance is very high compare to national insurance company medicalim. So my question is can I transfer my policy from oriantal insurance to national insurance ??..

Asif-You can use the Portability Option (Health Insurance Portability in India – Features and Process).

Sir, I want to buy Health Insurance from max bupa.Should i buy it direct from website or through agent by giving him some extra premium? One thing should I have to mention that my family members won’t be able to process any claim during emergency.

Bip- In that case better to go with an agent.

Thank you.

Hi Basavaraj,

First of all a great blog you have. I’ll be grateful if you can help can suggest few good health insurance policies for me to consider. The more I am reading the more I am getting confused.

Basically, I am 27 years old single person living in Bengaluru. So I want to cover my parents, My mother is around 52 years of age(arthritis patient for 7 years now) & my father is 55 years of age relatively healthy with diagnosis of high blood pressure.

What will be best for me, to go for individual plan for everyone? or separate plan for me and floater for parents?

Diwaker-Separate your insurance cover from your parents (for them family floater).

Which insurance is best suggested for Maternity / new birth related. I am about to get married. Seeing the money involved in new born baby, is it advisable to take any insurance policy which covers the complete cost. If I am expecting a baby after 2 years . Please advice

Sumit-Few insurers offer this. Check with them before going forward to buy.

Hi, Can you show the latest report ( 2016-17 claim settlement report)

Bharat-Refer my post “IRDA Claim Settlement Ratio 2016-17 | Best Life Insurance Company in 2018“.

I would like to take health insurance policy for me and my family. I am 51 years old covered by my company. Planning to take one in addition to existing to take care post my retirement. Please suggest. I prefer govt funded as I feel private ones take us for ride

sampath

Sampathkumar-Then you can opt any one among public sector companies.

Hello sir, I want buy health insurance to me and my spouse but getting confuse which company health insurance should I buy? Can you please help in choosing between Religare, cigna ttk and HDFC ergo .. online reviews are so confusing.. please help so that I can buy it at the earliest

Sadhana-What is your confusion?

Bad reviews is major concern.. on what ground should i chooses the company? Religare plan looks better than Cigna Ttk or HDFC ergo

Sadhana-Never depend too much on reviews. He, she or ME may have some hindsight or biased views. If plan features are matching your requirement, you are comfortable with company and premium is affordable to you, then go ahead.

Sir,

I have new india mediclaim policy for father (63)-mother(61), but now they have increased premium too much. I want to port policy. I am confuse between Appolo, Religare and Star health. Can you suggest which one to choose? most preferable to least preferable

Ankur-Hard to say BLINDLY.

Hi Sir,

I am having a Medical Insurance policy thru my company but I am looking to take personally one for my family(Self+spouse+daughter+father+mother). I have the following queries:

1) I checked online and have come to understanding to go for MaxBupa Health Companion.I would like to know the top 4-5 insurance companies which are good w.r.t. the claims settlement and other factors

2) As I understand taking separate policies for 3 of us and parents separately is good. What is your suggestion and which insurance is good for senior citixens

3) I am also looking for Term Insurance policy for myself. Pls suggest few options/insurers good in this field

4) What riders do we take for Medical insurance and Term Insurance plans.

Thanks in advance.

Ravi-1) Others factors and also the ICR is explained in above post.

2) Yes it is good.

3) Refer my post “Top 5 Best Online Term Insurance Plans in India in 2017“.

4) NO need to buy riders. Instead buy them separately.

Hello Sir,

I want to buy a Super top-up policy because my wife had diagnosed a neuro problem and my existing insurer Apollo Munich not exceed coverage from 3lac to 5lac or more. I had claimed in May 2017. And they told that its not possible in this or next year. My policy renewal date is 14th Jan, 2018 from Apollo.

I got the proposal from the Bajaj Allianz for Super Top-up and they said to cover pre-existing disease after 12 months (Policy Name: ExtraCarePlus). Except BajajAllianz, all are having 3 to 4 years waiting period in super top-up.

Can you please help me out here on this.

Thanks in advance.

Amit Gupta

Amit-If covering the disease is important for you, then go ahead with Bajaj.

Hi Sir,

Thank you so much for your reply.

Yes, the covering is most important to me but is there any question to ask to BajajAllianz except the 12month coverage.

If you have some questionnaire for me to buy this super top-up, kindly let me know as soon as convenient.

Thanks and regards,

Amit

Amit-Refer my post “Top Up Health Insurance Plan & Super Top Health Insurance Plan-What are they?“.

Hello sir,

If a disease found in current year, and if I increase amount or port insurance company then can that disease be treated as from previous insurance status? Like if my sum insured is 300000 and I renew to 500000, then can my disease which exists in 300000 can be treated in 500000 slab. Even in case of porting ?

Gautam-You are enhancing the cover. However, if you do not disclose about the disease during such enhancement, then it is not considered. You must be open and disclose all facts to the insurance company.

Hi sir, thank you for quick reply, but I have disclose my disease to insurance company.

Gautam-Better to disclose.

Awesome post Basu.. I almost read 100 comments so far.. I need ur expert opinion on 1 thing.. my mom’s, mines, wife’s and daughter’s age is 54, 32, 29, 17m respectively. Currently holding max bupa companion(30L family floater) since last 2 years (daughter not included). 2 years back I started with 25k premium followed by 32k and and now 35k. When I asked max bupa to add my daughter thy are asking 41k.

1. Now I am looking to split and port my policy. Also could not make up my mind between Apollo, icici Lombard, hdfc and star. Hdfc ergo is bit cheaper.

2. What is critical illness cover.. Do we necessarily need to take it separately

3. Also my major concern is, I don’t want my premium amount increasing every year like max bupa, what do u do in place of me..

[email protected]

Nikhil-Thanks 🙂

1) Choose among Apollo, ICICI Lombard or HDFC.

2) It covers specified critical illness. But hard to get the claims. I personally now own. But you have a family history, then you can own it.

3) The premium will increase based on age slab (but not yearly). Instead of a single family floater, I suggest you to separate your mother from your family floater.

Awesome.. thanku fr the prompt reply..

1. I definitely planning to take separate policy for my mom. Let’s c if I get portability for her.

2. I forget to ask about public sector vendors, I knw thy take time during claim bt bit reliable. But if person X has to choose between public sectors and individual players, and all has almost same features, what will ur opinion would be. ??

3. Recently my agent was telling me about SBI insurance fr my mom.. He was saying that u ll get 3L sum assured and 7L top-up fr a fixed premium of 10-12k which will never increase. Have u heard about it by any chance and how trustworthy sbi is??

Nikhil-2) It is individual’s choice. Hence, I personally not comment.

3) I am not sure about product. May be he is trying to sell you one base plan and one super top up plan. Check the details with agent.

Hello Basavaraj,

Thanks for the informative article and keep up the good work. I am curious about one thing, the claim settlement ratios shown here seem to be completely different from yours:

https://www.policybazaar.com/health-insurance/general-info/articles/health-insurance-claims-things-you-should-look-before-buying-health-insurance/

Am I missing something?

Samik-I am not sure about their data. I fetched it from IRDA Annual Report and published. You can cross check with IRDA Annual Report.

Thanks. The given data is apparently for CSR and not ICR, which makes my original question look dumb 🙂

In the table above of Private Sector Insurance providers, would you prefer going with any of the ones marked in GREEN or BLUE?

Samik-I am inclined with Public Sector companies. But in case of private players, I am bit inclined with standalone players.

Thanks. Wishing you & your family Merry Xmas.

Samik-Same to you too 🙂

i personally have a very bad experience with Sriram G I (and few of my frnds too)

also, i found this article which might be useful.

https://timesofindia.indiatimes.com/business/india-business/new-india-assurance-tops-in-claims-settlement-ratio/articleshow/60431421.cms

BM-That is the reason, I usually avoid new entrants.

Good day

Looking at the customer grievance handling statistics Public sector looks worst.

Does this mean public sector is not good to buy and I should give preference to a standalone health insurance while choosing

Kindly guide me through.

Sachin-Public sector companies response may be delayed or negligence. But they are bit generous in accepting claim than private players (see the above data).

Hi sir,actually i have a health plan of cigna ttk in my 2nd year,just renewed for my 2nd year,my age is 28 now,i have sum concerns and worriers…is cigna ttk is well reputated? Or should i go for another health insurance compnay? I have a plan of 4.50 lakh with premium of 5076 rupees…. Now i always keep looking around reviews of cignattk…. Pls tell what shud i do now?

Kanwardeep-As of now, if there are no issues with the company, then why you are worrying about REVIEWS?

I feel it will not survive in future like lic…because this is a private company… And i dont see much talking about cignattk…

Kanwardeep-They can’t wind up their business as per their wish.

Thank you sir for clearing my doubts

Hi basav,

Thanks for really informative blog

Actually I want to port my mother’s Mediclaim policy, currently My mother age is 49 and we have new India assurance policy from last 2 years, someone suggest me to port this policy into royal Sundaram as the In this company no camping for room rent and some other features like no co payment option after the age of 60…

Can you please suggest should i go for private company or stick to public sector company or need to port into united health policy?

Please suggest looking for forward your response

Thanks

Rahul-If Royal Sundaram features looks good to your requirement, then go ahead as there is nothing called private or public. I am not sure of what prompted you to choose United in between. Hence, I can’t comment on this.

Hi

Thanks for sharing your views

No one has suggested the name of Royal Sundram, Just because of less premium i choosed this company, Even i am open for all other companies also

Please suggest the best company in private sector as per their claim settlement ratio

Regards

Rahul-Refer above post.

Hi Basav,

I didnt noticed roomrent cap in United india Super top upplan.

Which means, there is no roomrent cap or the room rent cap will berestricted on base plan.

https://uiic.co.in/product/health/Super-Topup

Naveen-Instead of assuming, it is better to cross check with company.

sir,

i wanted to opt united India but,1) it has no PPN network hospitals in nasik .so,, not fulfilling# Check for hospital network availability in your city or town. The cashless hospital benefit is better than producing the bills and waiting for claim settlement.

2)co payment clause( 10% for above 60 yrs)

3)less illness covered

what should i do?

max bupa is next choice,,,,,,,,,,but not being able to check for # Check the premium rates. Especially check the rates for older age rates as few insurers jump the rate drastically for older age coverage.

united or bupa ,,,,,,,,,,,which way??

pl guide.

thanks for all the help.

Nirmal-Call MaxBupa and get the quote and based on that you can decide.

Hi Basav,

A person have two insurance policies of 5 lakh(UnitedIndia) & 3 lakhs(Apollo) each from different insurance companies.

Here, both insurance companies have different featutres, Under United India policy domilicary treatment is not covered, and the customer went for claim amount of 2 lakh with United India.

Out of 2 lakhs excluding domicilary treatment the claim amount is approved of some 1lakh. Here the loss is 1 lakh to the customer.

So now is it possible to approach other insurance company to settle the remaining amount which is not covered domicilary teatment by united india though the claim amount is not crossed more than 5 lakhs?

Hi Basav,

1. Slow progressive diseases like BP, sugar or cancer is detected\contracted on 32nd day after serving initial waiting period.

Here, how the insurer would consider wether it is pre existing disease or permanent exculsion or has to server any waiting period?

2. What is the difference between Co-Pay and deductables?

4. what is “Any One Illness” ? link – https://www.andhrabank.in/english/ABArogayaadan2.aspx under Other features

Thanks in advance

Naveen-1) Hard to say and mainly depends on respective insurance companies.

2) co-payment is like for Rs.100 bill, you have Rs.30 and rest by the insurance company (if the co-payment clause is 30%). Deductibles is the amount you pay each year for eligible medical services or medicines before your insurance plan kicks in. For example, if you have a Rs.100 yearly deductible, you’ll need to pay the first Rs.100 of your total eligible medical costs.

3) It is explained in that link.

Yes its explained in the link but i am not getting what they r trying to say.

Sorry for my poor knowledge.

what is “Any One Illness” ? link – https://www.andhrabank.in/english/ABArogayaadan2.aspx under Other features

Naveen-A disease period of within 105 days of occurrence from the date of discharge from hospital is called as same disease. If disease appears after 105 days, then such disease is considered as fresh disease.

Thanks , ok.

what is the necessity of this feature, usually any patient can visti the hospital for his illness and admit in the hospital for 24 hrs or more than 24 hrs in a month multiple right .

why they mentioned like this as added feature.

Naveen-To avoid the claim for the same diseases.

Naveen-Refer my post on this topic “Multiple health insurance policies -How to claim from all?“.

SO here at any cost the sum insured should exceed from one insurer then only the contribution clause will be initiated with the next insure. this is very sad point, this is very bad . customer may not know which insurer to approach for 1 st claim so he will choose insured based on his comfort and situations, later he understands this will not covers and cannot approach the other insurer.

Ok i got it sum insured should be exceeded then only contribution clause will be initiated.

Is it posible to get the claim settled by the two parties WITHOUT EXCEEDING THE SUM INSURED, hospital and other expenses from one insured and other features like Domicilary treatment like second insurer? Bcoz, Here the domicilary treatment is not covered from first insurer so he approached the second insurer.

Plese ignore the above one.

here is the simple summary.

Ok i got it sum insured should be exceeded then only contribution clause will be initiated.

Is it possible to get the claim settled by the two parties WITHOUT EXCEEDING THE SUM INSURED? Here hospital and other expenses from one insured and other features like Domicilary treatment with second insurer? Bcoz, the domicilary treatment is not covered from first insurer so he approached the second insurer.

Naveen-I got it. But you will allow to approach another insurer when the limit exceeds. You can’t approach different insurers for different treatment claims.

Thanks Basav.

Naveen-I understands what you are intending. But it is hard to say that you cover this expenses and other expenses I will claim it by another insurer.

Thanks

HI Basu,

I am 30 years old, i want to take health insurance policy with star health(as it is a stand alone compnay) and my purose is to cover the maternity benefit. could you please suggest on this.

Venu-Check whether the policy covers maternity benefits or not.

After reading the your report and comparing the ICR ,it can be said that Government owned insurance companies fulfilled the easily if we compare with standalone and private health insurance cos. May in gov cos. we face some problem because the online facility is limited and also there are TPA ,but we get money and that is the last thing. What you say Sir?

Biplab-I too agree 🙂

So , can we prefer gov health insurance companies ? Actually I am worried about paperwork during claim in gov cos. Will that be a big issue ? I am thinking to buy Cigna ttk for first year , if I won’t satisfy with then simply I will change it to new India health insurance company. Is it good decision or I am thinking wrong?

Biplab-There may be a service issue. But a bit relief.

Thanks for prompt reply , you are really helpful. Please answer my last question , “””” I am thinking to buy Cigna ttk for first year , if I won’t satisfy with then simply I will change it to new India health insurance company. Is it good decision or I am thinking wrong?”””

Biplab-If you are doubtful of CIGNA, then why not buy public sector company from first year itself?

Because Cigna ttk or Apollo etc have many additional features which are absent in public cos. Also Oriental , new India are giving mediclaim policy whereas private cos are giving health insurance , so which is better mediclaim or health insurance?

Biplab-If features are attractive to you, then go ahead. Also, may I know the difference between “MEDICLAIM Policy and Health Insurance”?

Hi Basavraj,

1. Is it possible to convert bank health insurance to individual policy means open market insurance?

2. what is second opinion and anyone illness? I read in google but i coulnt able to understand.

I am asking question like mad, sorry for that.

Naveen-1) Yes few insurers provide this facility if you are porting within same insurer. Hence, better to check with your insurer.

2) May I know where you found this?

Hi Basav,

I am planning to purchase Supertop Plans for my family I have few queries regarding the same.

1. Super top plan works WITHOUT Base/Parent insurance plans or not ?

2. If it works how to follow the process for claims?

3. If base insurer is rejected what happens to super top up (will it be rejected or accepted).

4. Say multiple indicidual policy(family of 3, say person 1 5l from lombard , person 2 from apollo munich and person 3 from new india ) from differ company

Can one super top will plan work for all (assuming purchase from United India) clubbing all three. If yes any specialised process need to follow.

5. what is threshold 15 lakh e.g 5l is threshold so Sum Insured is 20lakh or 15L?

Usually u are the one who stuck in my mind regarding the health insurance queries. Thanks in advance

Naveen-Refer my post “Top Up Health Insurance Plan & Super Top Health Insurance Plan-What are they?“.

I have gone through your airtcle thanks a lot many of my queries has been cleared.

1.I understand that Super top up plan works after deductable limit paid.

So here my question is, if the claim amount is 10L and deductable limit is 3l , do the insurer settles 7lakhs?

2. Say Base insurance is from Lombard and supertop up if from United India Insurance.

If base insurance is rejected what happens to super top up plan(will it be rejected or accepted).

3. Say multiple individual policy(say person 1 has 5l from lombard, person 2 from apollo munich and person 3 from new india )

Do one Super Top up Family plan will work for all the said policies. Scenarios :- Individula 1, individual 2, individula 3 and Supertop(Individul 1, 2, & 3)

Naveen-1) YES.

2) It is separate and not linked to base plan. Whether you pay the base amount from your own pocket or from the insurance company is up to you. Hence, they may or may not accept the claim (based on the situation).

3) Refer my post “Multiple health insurance policies -How to claim from all?” (http://www.basunivesh.com/2016/05/06/multiple-health-insurance-policies-claim/)

OMG too many technica/logical terminology and huge workaround is needed. Thanks for sharing the article of multiple insurance policies. i didnt know this earlier.

I guess I have confused you or i didnt asked in proper way.

Family consists of theree has 3 policies(Individual ploicy) from different insurers.

Say Mom 5 L (apollo), dad5L(lombard) and son 5L(United India) and for all three is it possible to take one SUPERTOPUP(Family Floater) ?

Naveen-If individuals have their own separate policies, then it is not issue with super top up plans. You can still go and buy it.

Ok thanks, Again I am framing.

here I am not purchasing 3 super topup policies for each individual only one Super Top up family floater Policy for 3 individuals . this will work right? Bcoz united super topup policy is very cheap and affordable so only asking again. sorry for that.

Naveen-For buying super top of a family, there is no such rule that you must own a health insurance (either single or family floater). It is up to you of how you pay the base payment. Hence, you can go ahead and buy.

Thanks a lot Basavaraj:)

Thanks for your patience in advance., You have already answered me for this question.

Which scenario is correct.

I know scenario 1 will work , but not sure about the scenario2.

scenario 1

————

mom-> individual Lombard-> 5l SI -> Super top up Individual(United) 15 = 20L SI

Dad-> individual Apollo -> 5l SI -> Super top up Individual(United) 15 = 20

Son-> individual Religare-> 5l SI -> Super top up Individual(United) 15 = 20

Total = 60 Lakhs(5+5+5+15+15+15)

Total Ploicies = 6 Policies(3 individual(Apollo,Lombard,Religare) and 3 supertop up(United))

Total Premium policies to pay = 6 Ploicies

Scenario 2

———–

mom-> individual Lombard-> 5l SI -> Super top up FAMILY FLOATER(United) 15 = 20L SI

Dad-> individual Apollo -> 5l SI -> Super top up FAMILY FLOATER(United) 15 = 20L SI

Son-> individual Religare-> 5l SI -> Super top up FAMILY FLOATER(United) 15 = 20L SI

Total = 30 Lakhs(5+5+5+15 bcoz only 4 policies)

Total Ploicies = only 4 Policies(3 individual(Apollo,Lombard,Religare) and ONLY ONE supertop up(United))

Total Premium policies to pay = only 4 Policies(3 individual(Apollo,Lombard,Religare) and ONLY ONE supertop up(United))

I am doing analysis and planning to reduce the premium cost and also at the same time trying to get high sun insured.

Bcoz, 90% of claims falls under below 5Laks and once in full moon day claims will cross above 5Lakhs

those are major operation or critical illness etc. so individual policies for each and one family floater super top.

Please see the Scenario 2 premium will be paid only for 4 policies for which SI is 30 lakhs

wheareas in scenarion 1 premium will be paid for 6 policies and and the sum SI is 60 lakhs

Naveen-I understood your point. But here in first scenario you are paying high and ending up with higher sum assured also. Personally, I separate old age people from clubbing with young age. This saves a premium.

Yeah you are too smart, your suggestion is nice.

Hi Basavraj,

I want to buy a Health Insurance for self (36), wife (36) and son (8). I hold a company insurance of 5 Lac and want to buy additional insurance of 5 Lac. Wanted to understand which companies are good to go. The premium from Royal Sundaram is showing almost 25% less than Apollo Munich and Max Bupa and features are also better or similar to these. Please suggest which one should I go for. Also wanted to understand if companies having TPA are Ok or we should go for Non-TPA companies.

Anshum-In that case you can stick to Sundaram. TPA or Non-TPA is irrelevant nowadays. Because companies which not provide you TPA service, have their own in house claim settlement service.

Thanks a lot Basavaraj…Just 1 more thing….I am not sure why premium of Sundaram is less than that of Apollo or Max……Do you have any info about the services of sundaram?

Anshum-It is purely a business call. Hence, none aware of why the premium is high or less.

Thanks a lot for the Insight !

Hi.I want to ask that my husband is 31 Nd I 29, want to buy a mediclaim.But the issue is I hv gone through an surgery of fibroid last year.So I think it will consider as pre existing disease.

Which co. will suits us, as currently I am checking with Star health FHO.

I hv not rec’d my answer

Suman-Hard to say which company SUITES TO YOU. But check for the comprehensive cover by referring above post. Then short list the company and disclose all facts. Then only you will come to know whether they issue the policy or not.

I am sorry if I have missed this but in the graph for public sector companies why is United in red? Assume United is UIIC?

KDS-Higher the claim settlement than the premium the company received shows the company is under loss for that particular year as expenses overtook than income.

Ok would that not apply for New India and Oriental too?

KDS-Why not? But United India’s ratio is high. Hence, I highlighted with red.

Ok I was wondering if there was a reason for having blue for New India and Oriental when United was red considering all have higher expenses

KDS-Both fairer than United.

Hi Basavaraj,

I have few queries on Personal Accidental(PA) insurance, here are

1. is it mandatory to reveal income proof for personal accidental(pa) insurance?

bcoz, the insurance company is issuing the policy to max sum insured upto 8 to 10 times based on theincome. my requirement is omre than the income.

2. while going for claim , do insurance company catch and reject the claim ?

3. if they catch , how they will catch, do you have any idea regarding this?

Thanks in advance

Naveen-1) Yes, because they need to understand the actual financial loss in case of an accident.

2) May be.

3) At that time they may ask you to submit income proof.

Thanks Basvraj,

I am planning to take PA Ploicy around 20 to 25 L for my parents.

My father is earning money from multiple sources eg. 1. giving money to people by getting small interest

2. Administrator and account of unregistered small finance comp 3. Partner of unregistered small finance comp 4. Giving the farm land for lease and earns money from it.

So, here how to estimate the income and how to show the income proof, he didnt file any it returns.

As per Govt records he is a farmer, Could you please help me with this kind of typical situation, how to get policy as the SI(20 to 25L) and how to show income proof tomorow to make sure not to reject the claim.

Naveen-The income which is accountable and shown for IT return is the proof you can show.

Thanks

Hi,

Thanks for such an informative post. Kindly help me answer the below query:

Is the room rent limit in government health insurance companies tend to increase after some time, may be after 5-7 years, considering inflation, etc. Or it stays the same for life long, let’s say even after 25-30 years.

Sachin

Sachin-It will remain same. To enhance such cover, you have to increase the sum insured.

Hi.

i am 34 years old.my wife 29,1 kid-2 years. i have diabetes and high BP. my wife and kid has no pre existing disease. my mother(57y) has thyroid & rheumatism.my father(64y) has BP,sugar,heart problem & kidney problem etc..i want to take medi claim policy for all.how do i split it.which policies will be ideal for my requirements.

Rishi-Your parents in one plan and your family in one plan. Refer above post for selecting.

hi sir

thanks for the quick response.my father has many health issues..my mother has no complexity..if i am clubbing them in one health insurance wont it be more expensive?? what should be the ideal approach??

Rishi-In that case, it should be better to separate them.

Good afternoon Sir,

I’m Sushovan, 33, unmarried, govt employee from Bengal. I’ve no medical problems except cold related nausea. I’ve gone through your post and other comments posted here. And found public sector insurer are more reliable than private sector. But I’m confused about some basic points and requesting you for clarification..

1) Whether should I buy ‘health insurance’ or ‘mediclaim’ policy? (I want to lessen the burden of my pocket in the period of treatment)

2) Is National Insurance most reliable than others in public sector category?

3) Mom, 50,stays with me. She has some medical problems. I’m going to marry soon. So, which one is better, ‘individual’ or ‘family floater’ ?

4) According to claim settlement ratio, which company should I choose?

5) Is there any provision of maturity and refund of money (like lic) if no claim is made say for 5 yrs or more?

6) Can I add my future wife or babies later in my individual plan?

.. Sorry for asking so many questions.

Thank you.

([email protected])

Sushovan-1) What is the difference between health insurance and mediclaim policy? As per me, both are same.

2) How can you judge this?

3) Individual for her.

4) I already explained in above post.

5) NO.

6) YES by converting to family floater.

First of all thank you for your suggestions. With references from your reply

1) Heard that ‘Mediclaim’ covers only hospitalization cases where as ‘health insurance’ covers other than hospitalization cases also. Is that true?

2) I’m not judging. Just confused what policy to buy. Want your suggestion.

Thank you again.

Sushovan-1) I am not aware of that. As per me both are same.

2) May be due to public sector.

Thank you for your valuable comments and suggestions. Have a great day.

Sir I want to take a policy in which new born baby should cover from 1 St day as already I have a bad experience about it when my first son was born after born he went to icu and now he is with us , so for the prevention I want to have insurance cover so that this should not happen next time .will you please sujjest me the best plan for this in which room rent cap is substantial, and the feature of this is also there . My age is 34 and I want policy for my wife 28 and for my son 3 months with above facility

Request to suggest the best

Regards

Asif

Asif-I understand your concern and pain. But sadly no insurer will take such risk.

Sir max Bupa heart beat silver plan agent says that in maternity cover there is limitation but the new born will be covered from day first .your view sir on this he is saying right or wrong .or should I take any other public company policy plz suggest

Regards

Asif

Asifthussain-Yes it is true.

For comparison of policy in premium could you suggest other than max Bupa heart beat silver plan so that comparison could be made sir and best could be taken

Regards

Asif

Asif-Better you visit individual portals and compare than relying on comparison portals.

Name of more plan which gives cover from day 1st to new born .,then only I could compare sir , their are lot of policy please suggest some so that it is easy to compare regards

Asif

Asifhussain-You have to dig by each individual product of each insurer if you want to nail this specific major criterion for buying insurance.

I have purchased Apollo Munich health insurance policy for my parents after health check up They have charged 2500rs extra because of high body mass index. I want to know that I should pay or not because If I choose HDFC Ergo for my parents no medical check up required there and In hdfc I get 5 L premium instead of 3 L premium that I get in Apollo. Should I cancel my policy and should go for hdfc? Can you suggest me?

Hi,

I am 37 yrs old and my wife is 31. I am planning to take a insurance cover and have short-listed two:

1) Apollo Munich – Easy health (family floater) – it gives NCB of 10% for each claim free year upto 100% of SI.

2) Max Bupa – Companion (family floater) – it gives NCB of 20% for each claim free year upto 100% of SI and no reduction in NCB in case of claims.

Ignoring the premium part, based on your experience which policy would you recommend.

Nitin-Is the major concern for you is NCB or plan features? In my view both are fine.

I am regular reader of your blog.

I am 29 year old, my wife is 25 year old and my daughter is 8 months old,

i want to need medlclaim with cover of 3 lacks.

i want to go with public sector but all policies with public sector companies has room rent limit, that i dont like.

so i have to go for private company.

my questions are as follow:

1. Is anny compny is public sector has policy with no room rent limit with 3-4 lacs SI

2. In private i have figure out Apolllo, cigna TTK, royal sundaram, Religare , which is best from above?

3. we are planning one more baby after 2 years, i think pregnancy takes 15-20K and i can suffer easily right now, so i dont think take special plan that covers maternity by paying high premium to only cover pregnancy because most of has 2 year + 9 month waiting for it.

Please suggest me.

Thanks

Vishal-1) As per me NO.

2) To me all 🙂

3) It is waste to buy maternity cover policies.

Thanks for reply.

Can you pleaese suggest me based on which compnay is good in case settlement and which not hike premium after claim made,because there is many company starts with low premium and after claim made it increase premium.

AS you have large experience and large customer so you can any ideas about that.

Vishal-IRDA recently warned all insurers that premium can’t be raised due to claim in particular year.

I am 25 year old and wife is 23 year old.

My wife is suffering from migraine.

Please suggest me health insurance company.

Should i go for public sector companies or private?

Nilesh-It is hard to say which company is best and which one will issue the policy when there are health issues already facing. Check with public sector insurers.

Hi Sir, I want to take a health insurance for me (age 29) and my wife (age 24) which includes critical illness as well, actually i want to have the cover of around 30-35 lakhs for any worst scenario.

I searched a lot and found out the below option fine:

1 family floater health insurance base plan of 5 lakhs plus super top of 20 lakhs plus a critical illness of may be 10-15-20 lakhs.

Company i have not decided yet, but thinking of Apolo Munich or Max Bupa for the base and top up plan and for critical illness Religare.

Is the above options are fine or if not then please suggest any modification from your side.

Thanks in advance.

Abhishek-Please go ahead. But in my view MaxBupa may costlier than Apollo.

Nice artucle.

I have few questions.

1) I am 25 now running tata aig medi prime of 4lacks coverage for 3 years now. Will I be able to merge the plan with my future wife ? As she is also going to opt for the same plan, she is 24 now.

2) will there be any option of merging two same policies and make it a family floater?

3) is there any company which is covering 100% of any helth issues including opd? (Excluding Critical illness, hiv and plastic surgery etc)

Sayantan-1) Currently I think you are holding individual plan. If you try to add your wife, then you have to buy family floater. They will not merge in the same plan.

2) NO.

3) NONE.

Hi, is there a claim settlement ration for general insurance companies also available. Like Vehicle insurance

Gaurav-Yes, check IRDA annual report.

Sir, I (38 yrs old ) have purchased Star health optima last year 14/09/16, 2A+2C for R’s. 11880/- of SA R’s.50000/- .On that time my agent said that premium will be same up to my age 45 but, during renewal this year he says I have to paid Rs. 15287/- and as per him C.Gov.increase the premium. Pls help what should I do? Am I quit or renew ? My agent is right or wrong ?

Abhijit-For your information, Govt in no way have rights to increase your premium. It is purely insurance company which has rights to increase. Govt may increase taxes but not premium. Check the reasons with Insurance company directly than relying on an agent, then decide.

Hello Sir,

I hope you are doing well…

I want purchase medical policy for my parents. My father age is 55 and my mother age is 50. I have selected two company policy for 5L Cover. First HDFC ERGO-Health Suraksha With Regain and ECB and Second Apollo Munich-optima restore

Premium for hdfc is 21500 Rs approx and for Apollo is Rs 25300 but I am confused which company has good claim settlement

Can you help me which one is best?

Saurabh-Don’t rely too much on claim settlement. Go ahead which comfort you.

Why not to rely on claim ratio ?

Rishabh-Is it provides product-specific like an endowment, term life insurance or ULIP claim settled ratio? Is it gives you the clear picture for rejection? The answer is NO.

Dear Basavaraj,

First of all thank you for writing these blog posts. You are doing a great service to lot of people. I am very impressed with the efficiency at which you follow up queries !… and I think this is the right place I might find answers to my questions 🙂

I would like to buy health insurance for my parents (father-56, mother-54). Since they are reaching 60 and my mother is having Hypertension, I decided to go for individual plans. Father is healthy.

1) Is it wise to go for individual plans for each one?

2) Per your analysis in this post, I applied for MaxBupa Health Companion for my mother an mentioned her condition with symptoms (online form asked them) as “Headache and Anxeity”. The application got rejected stating “Decline reason- Known case of headache and anxiety”. I had also honestly mentioned that her father was a Hypertension patient too and that his demise was due to heart attack. Is it too bad to be honest while applying for health insurance?

3) In your answers you recommend going for Public sector companies for parents. Though the incurred claim ratio is high for them, how is their service and customer support?

4) Is it better to take 10 Lakh cover or 5 lakh cover + 10 lakh super topup (with 5 lakh deductible)?

Many Thanks!

Ravi

Ravi-1) Yes, 2) Being honest is not bad but you are saving yourself from future claim rejection scenarios. Hence, if one company rejects the proposal, then approach the another one. 3) In my view, it is safe to go for the public sector. 4) Better Rs.5 lakh base plan and Rs.5 lakh super top up.

Thanks Basavaraj, best wishes !

Sir my age is 37 my wife is 34 my daughter is 5 and my son is 2 yrs old. My son is a cardiac patient and his open heart surgery is done.

1. Is there any insurance company who can give him policy?

2. If not then should I buy family plan for me, my wife and daughter or individual plan for all three?

3. I’m a customer of canara bank and they are having a tie up with Apollo munich. Should I buy it from bank as bank is offering low premium or i should buy directly from Apollo munich?

4. Is it worth buying a policy from bank?

Somebody has also asked you the same question (3) but you have posted a link there and I couldn’t find my answer in that link also.. please I request you to kindly answer my question.

Thanks Naveen

Naveen-1) Hard to say. You have to knock each insurance company of your choice and then wait for their reply.

2) Even if buying family plan with hiding the health issues of your kid may not use as they may reject claim if in future your kid get hospitalized due to ailments related to existing one. Hence, disclose facts properly (if you want to go for family floater) and let insurer decide.

3) Such products come with limited features and not aware how long the bank tie up with the insurer. Hence, better to avoid.

4) I already answered.

SIR , I WANT TO BUY TRAVEL CUM MEDICAL POLICY FOR MY DAUGHTER GOING FOR FURTHER STUDIES

IN USA ,PLEASE CAN YOU SUGGEST WHICH INSURANCE COMPANY IS BEST WITH RESPECT AFTER

SALES SERVICE , FOR SETTELING CLAIM

Amit-Refer my earlier post “Best Travel Insurance in India-Product Comparison” (it may be old post but help you in shortlisting).

Hello Sir,

Very nice article. I am interested in buying a policy for myself and family. I am new and I don’t understand the terms written in the policies properly. Can you please tell me a website/blog name where I can easily understand these complicated policies? I don’t understand the parameters on which I should choose one policy. Very confused. Please help. I will be very thankful to you for the same.

Ritesh-The parameter to choose a plan is also explained in above post.

Some says that public sector health insurance company has good claim settlement ratio rather than private sector.

so can u kindly let me know for this. which should i do?

Rai-Data is in front of you.

Sirji,

I am 45 years old central govt. officer. I have my wife aged 31 and two sons aged 13 and 10. I live at Tribeni (712503), West Bengal (Kolkata Suburb). I have chosen Cignattk for my firstime family floater health insurance. Is it a good company? I will proceed further after your reply.

Madhu-You already purchased. Hence, you no need to worry and continue.

Oh! No. I have selected only. Will buy if you suggest so

Madhu-I am not blaming or pointing you 🙂 I know you want to understand whether you are doing correctly or not. But I can’t name any particular product as universally best. Hence, I suggest you go through the points and procedure I explained in above post in choosing the product. Based on that you select. In that, if the insurance product you already short listed is OK, then go ahead.

Hello Sir,

Myself Lokesh, in June 2017 I planned for taking health insurance for my parents aged 54 and 53. They both have some medical history and due to which Max Bupa had rejected the application. I tried to contact other companies but right now I am in touch with Cigna TTK who ensure that they might consider providing health insurance but waiting period will be of 3years after the Medical examination and also there might be a loading.

Now, I am confused should I go with it or not as Maxbupa had rejected and Cigna is providing so not sure they will process my claim after 3 years or they are going to reject it (if any).

Can you please help me to sort it out?

Lokesh-But it is better to have something than NOTHING right?

Dear Sir

I am porting from New India Assurance mediclaim to Apollo Munich health insurance(Optima restore). I am an irregular smoker(but not a complete non smoker) and have social dinking habits which I have mentioned in the application form. I find in their policy wordings that injury or illness arising out of use of tobacco or alcohol are excluded. I contacted the company executive/agent for a clarification of this wording since this, according to me, is a dichotomy. However, I could not get proper clarification except that this is as per IRDA guideline(I could not get hold of such IRDA guideline though) and that I need not worry since I have already declared my habits. The New India Assurance policy wording mentions illness or injury arising out of use of alcohol/narcotics etc. as excluded. I wish to know whether they can reject a claim for diseases which may be attributed to use of tobacco/alcohol but not necessarily arising out of the use of the same, based on their policy wordings as well as based on the declaration submitted by me. An early advice is sincerely solicited since my free look period is coming to an end by 07.07.17

Regards

Arindam-It has clearly mentioned that illness arising out from alcohol or narcotics. Hence, any future claims arising due to your drinking habits will not be acceptable for claim.

hello Basavaraj Tonagatti sir

i follow your web site from past 1 year really helpfull project thanks for such grateful effort

my question is

1. star mediclaim give joint replacement cryosurgery after continuous period 2 year oprat policy (when port policy bajaj to star)

2. i confuse between cigna ttk & universal sompo mediclaim

please help me sir and any friend also he expert in question

Thank you in advance

Pradeep-1) Whether this surgery is an issue with you?

2) What made you confuse between these two?

hello sir for replay

1. actually that problem face my mother (she 51 years old ) from past 2 to 3 month ……i plane to do surgery next renewal after july 2018

my previous policy was bajaj just portability with star (star told me wecover after continuous 24 month only in when portability case )

please make sure is it right???

note – because no any preexist diseases mention on bajaj policy…

2. i confuse between cigna ttk & universal sompo mediclaim (this policy take for me age is 31 years old)

Thank you sir

Pradeep-1) Refer my post on portability of health insurance “Health Insurance Portability in India – Features and Process“.

After going through the comments, i am now leaning towards public sector companies. I was earlier thinking of buying Religare. But now second thoughts.

Yathiraj-Go ahead.

I am planning to buy a health insurance for family – Myself (36 yrs), Wife & 1 Kid. Done some research. Looking for advice which one should i choose. I have a corporate heath insurance with 3L SI. I wanted to choose a policy with 10L SI. All the public ones have high premium. I looked at Oriental & New India. Also, they have TPAs for claim settlements as they are GICs. In private, i liked the features of Max Bupa & Cigna ttk. Particularly, both of them have same features almost like restore benefit, no room rent limit, Bonus. Cigna also pays OPD of Rs.2000 unlike Max Bupa. But Max Bupa has a bigger network hospital. Cigna’s premium comparatively to Max Bupa is very less i.e. almost 5K to 7K less depending on the product. The only thing i dont know is how does Cigna increase its premium YoY. Max Bupa increase 1 to 2% as they say. I am inclining towards Cigna but again their hospital network is not very wide in India. So, dont know if it is right decision. If network is not very good, i have to pay from my own pocket and then reimburse. Then, the whole purpose of insurance is lost as i cant pay a big amount myself and then claim. But Max Bupa premium is also very high. So, i am not sure. Even if i go for 5 L SI + 5 L Top-up in max Bupa, premium will not decrease much than Cigna. Also, am i going in right direction by ignoring public ones? No choice there as there premium is way too high. Can you pls advice?

Dinesh-Insurers will not increase your premium year on year. But based on the age slab of the oldest person in family floater plans. Also, if you are comfortable with Cigna TTk and features matching your requirement, then go ahead.

Hi Sir,

I am 32 years old, i didn’t yet enrolled any health insurance ? Can u suggest me good health cover for floater and Individual.

1. Which secttor health insurance is better? a. Public b. Private Partnership c. Private Standlone.

2. In public secotor cashless facility available ?

3. Can i go for high sum insured or low sum insured ?

4. if low SI the cover will be low , inthat case, is there is any way to increase the SI?

Naveen-1) Public or Standalone.

2) YES.

3) That depends on your capacity of premium payment.

4) You can go with affordable sum insured and then if you feel higher requirement, then go for super top up plans.

Thanks Bhasavaraj,

Could you suggest me which one can I go- Individual or floater. If I take individual later can I enroll any of the parents or family members into the policy?

Thanks in advance.

Naveen-If you are an individual, then stick to an individual plan. If you are a family person (wife and kids), then better to go for a floater. However, don’t combine your parents into your insurance. Buy them separately.

Thank you Bhasavaraj,

I have gone through public and private sector health insurance company plan quotes. In my a analysis almost all the premium rates are similar and the facilities and coverages covered are also similar. Here my question is why should one prefer public sector, Bcoz, public sector service will be bad and private sector services will be good I feel alike? Can you help clarify in this regard.

And, can you differentiate public and private sector companies. With strong valid points.

Thanks in advance and sorry for asking many questions.

Naveen-But public sector companies may be generous in claim settlement than private sectors. Also, the hospital cost may be different for a private and public sector. Hence, I suggested public sector.

Thank you Bhasavaraj.

Hi Basavaraj,

I am planning to take health insurance plan for my parents , whose age is 60 and 48 respectively.

1. Could you please suggest me wether to go for 1. mediclaim ploicy +super topup or 2. critical illness plans?

2. what is critical illness ploicy comparing to health insurance plans is it same

Naveen-As the age difference is high between your parents, better to buy separate health plans to them.

1) Better to separate.

2) It covers specific critical illness than the normal illness.

Sir just wanted to know that I want to have a health insurance floater plan for my family. Myself and my wife. Should I go for public or private sector companies….plz suggest me as I am clueless regarding this…

Ayan-Better public sector.

Thanks sir…..for your prompt reply.

I’m 34 years old a state Govt employee with 2kids am having apollo Munich optima restore for the past 4 years paying around 24000 per 2 years I’m not sure to take any cancer plan online can u guide me.took term insurance for 500000 from lic and having endowment plans from lic.

Rahul-Why you felt that you need cancer plan?

As we grow older there is chance to get that disease so I thought of can u further enlighten

Rahul-If you fear of such diseases, then better to take separate critical illness cover.

pls suggest a combination of two insurance plan which fulfill these two character -(Fixed or Defined benefit plans+Indemnity benefit plans).

Ankit-Defined benefit will be in case of annuity plans. Indemnity against what? What is your requirement?

Hello sir My father is 63 years old and I am having religare care health insurance for him from the last 4 years. The problem is with the premium here. They were increasing premium every year citing some reasons. last year the premium was around 21000/-. This year it went to 25000/-. The reason they were citing is many number of new day care procedures are added, so that’s why we have to charge more premium. Is this case the same for every health insurance company out there? There should be some cap on increasing the premium. Is religare the best policy now? on paper the features look very good.

Rajbharath-If you are uncomfortable with their premium capping, then better to port with public sector companies.

Could you please guide us also about health insurance by Punjab national bank.. how are these health insurance plans provided by banks? shall I go for it’s family floater. Me (33), my wife and daughter (4).

Thanks and Regards.

Ranjeet-I will not rely on such plans. Reason is, if the contract between bank and insurer for any reason ENDS, then we will be out of insurance.

Thank you. If possible kindly suggest me a good health insurance plan that i can opt for. I am a 34 years old government servant. I want a plan that will cover my wife as well as my daughter (4 years old). I know you cant directly endorse a particular plan here. But it will be a great help as I am really unsure on selecting one for me. If anyhow it is possible to let me know on my email id: [email protected]. Thank you.

Ranjeet-Check with public sector companies.

Thank you 🙂

Sir,

Thank you very much for guiding us to take the calculated decision with respect to Investments/Insurance etc.

I am 32 years old (Smoker) and hold an ICICI Lombard Health Policy for 3 years. I have covered my wife under the same plan for the sum insured of Rs 3 lacs. We now have a daughter which is 12 months complete now and want to include her in the same policy with the new sum assured of Rs 5 lacs.

Need your advise as to whether continue with ICICI Lombard with Sum insured of Rs. 5 lacs at this stage OR i should decide to switch the company OR enhance my sum assured.

Thanking you in advance.

Shirish

Shirish-If there are no issues with ICICI, then why to switch? You can include your daughter. Regarding enhancing of sum insured, it is you who has to take call. If at all you feel the hospitalization cost in your stay not suffice, then instead of enhancing the cover, I suggest you to go for super top up plans.

Thank you very much for your valuable advice. My concern is that the advisor states there is no room rent capping in ICICI Lombard. He explains that one can use room and nursing charges of whatever available in hospital, as in with sum insured of 3lacs one can even use the higher category room if hospitalised. Is it true ?

Shirish-Instead of doubting, let him show the product brochure to clear of what he is claiming. No oral confirmation.

THANKS FOR THE VALUABLE INFO.

Dear Basavaraj Sir,

Very informative article. Thanks to you. Sir, kindly share your valuable openion on Group Health Insurance schemes provided by banks such as CAN MEDICLAIM, SYNDAROGYA etc. They offer good cover at very less premium, and also covers parents upto 80 years. Are they worth buying sir? why they are offering coverage at less premium? any hidden agenda or costs involved sir? Please throw light on these sir.

regards

RAJESH PAI

Rajesh-Let me dig on this data.

Pension plans – Bharti Axa Samriddhi (investin 1Lfor the next 10 years) – to get a pension of Rs.16k (2l approx.) for lifelong.. your opinion sought..age44; female;

Basically looking for a retirement plan to give monthly income of rs.40k..your suggestions..

Liz-It is a typical endowment plan which I think wrongly sold as Retirement Plan. It fetch you around 5% return. How can you sustain with such low return for your retirement corpus? Stay away from such dummy products.

sir i have been in star health policy from past 3 years and no claim till know,this month i have an renewal but some one says that their investors are exiting from this company so shall i go with company or any other please clarify

Can I take multiple health insurance? I already have Family floater of New India company worth 3 lacs. My age is 30 (Non-smoker/tobacco) and I am planning to buy from private sector like Max Bupa or Apollo.

Also please let me know am I right on this decision? If possible can you please suggest which company is better?

Peter-Yes, you can buy multiple health insurance product. Refer my earlier post “Multiple health insurance policies -How to claim from all?“.

Sir, since 8 years I am staying in Qatar.

I want to invest some amount in mutual funds for my retairement and now my age is 48

Maximum 10 years I can invest at 3Lakhs per annum.

I need your suggestions for my financial planning. Till now i did not invest in mutual funds.

How to proceed.

Srinivasa-Refer my post “Top 10 Best SIP Mutual Funds to invest in India in 2017“.

Respected sir, thnx for information, im a customer using religare care family floater plan super ncb,policy due next month, i wantto know is this good to stay with religare or should i go with cigna ttk, religare offering super ncb 150%, i always follow your guidance, please suggest me, i know u may say choice is urs, no one is perfect, but just wanna go with ur suggestion, didn’t claim last year, 10 lakh cover going to 15 lakh as per ncb religare, please suggest… Or any other suggestions. Thnk u sir

Dr.Anand-You continue the existing one.

thnx sir for ur suggestion, im grtful to u

Hi Sir,

I would like to share my personal experience.

I have Religare care family floater policy for Rs. 10 Lakhs. It came for renewal in December. Religare has increased premium by around 12% in October 2016. While making inquiry about premium increase, Religare representative informed that IRDA allows health insurers to increase premium every 3 years according to claim experience and increase in medical inflation and Religare has increased premiums after 4 years (Since inception in 2012)

However, one has to accept that Religare have markedly improved product features in modified Care Version -2 such as increase in number of day care treatments, Compulsory medical examination age increased from 45 years to 50 years, Annual health check up for all insured members covered by policy, in-built optional PA cover, optional OPD cover, Non alopathic treatments (Ayurveda, Homeopathy, Unani ), Maternity cover for SI of Rs. 50 Lakhs and above etc.

Hence, I have continued with Religare even after revision in premium.

Thanks

Ritesh-But as per IRDA rule, they can’t increase premium based on earlier claim.

Sir religare is the worst.they are giving me wrong answers on mail.where should I report.religare is most cheating company .

Laxmi-What wrong answer according to you they gave?

Very informative.

Keep up the good work