IRDA published its annual report on 4th January 2018. Let us see the IRDA Claim Settlement Ratio 2016-17 and also which is the Best Life Insurance Company in 2018.

Note:-I published the health insurance data also. Please refer “IRDA Incurred Claim Ratio 2016-17 | Best Health Insurance Company in 2018“.

What is the meaning of Claim Settlement Ratio?

Claim Settlement Ratio is the indicator how much death claims Life Insurance Company settled in any financial year. It is calculated as the total number of claims received against the total number of claims settled. Let us say, Life Insurance Company received 100 claims and among that it settled 98, then claim settlement ratio is said to be 98%. Remaining 2% claims the Life Insurance Company rejected.

Based on this, we can easily assume how much customer friendly they are in dealing with death claims. However, I warn you that this claim settlement ratio is raw data.

It will not give you a clear picture of what types of products they settled. They may be Endowment plans, ULIPs or Term Insurance Plans. Hence, this is not a sole criterion in judging the performance of a life insurance company.

IRDA Claim Settlement Ratio 2016-17

Below is the IRDA Claim Settlement Ratio 2016-17 or up to 31st March, 2017. I differentiated the below table with colour code for your better understanding.

The same one I tried to show in a bar chart for your easy understanding. Here also I used the colour code and they are as below.

Green-Claim Settlement Ratio from 95% to 100%

Yellow-Claim Settlement Ratio from 90% below 95%%

Red-Claims below 90%.

You notice that among total 24 Life Insurance Companies, around 8 companies are in GREEN (Claim Settlement Ratio above 95%). Total 11 companies are in YELLOW (Claim Settlement ratio between 90% to 95%). Total 5 companies are in RED (Claim Settlement Ratio below 90%).

As usual, LIC tops the list. But don’t feel happy. Let us see the claim amount settled by individual companies to arrive at best companies.

Average Claim Settlement Amount of Life Insurance Companies in 2016-17

As I said above, the claim settlement ratio will not give you the clear picture about which type of products the insurance companies settled. However, we can assume the types of products they settled by looking at the average claim settlement amount of Life Insurance Companies in 2016-17.

Here come the results !! LIC stands in lowest with red in colour along with Life Insurance Companies like Sahara, Reliance Life, Exide and Future Generali. What is it indicating?

It shows that, even though LIC settled the highest number of claims, the majority of such claims are less than Rs.2,00,000 Sum Assured. Hence, it is indicating indirectly that LIC’s claim settlement is mainly in the category of Endowment Plans but not Term Insurance.

Average Claim Rejection Amount of Life Insurers in 2016-17

Now let us go deeper into IRDA Claim Settlement Ratio 2016-17 and try to analyze the how much amount of claims they rejected. Here, I calculated average amount as I don’t have data to check the maximum and minimum amount.

The results are as below.

You notice that Sahara’s claim rejection amount is less and then comes the LIC. LIC’s claim rejection is less because the quantum of claims it handles is HIGH but value is less. So no need to say that LIC done a great job here.

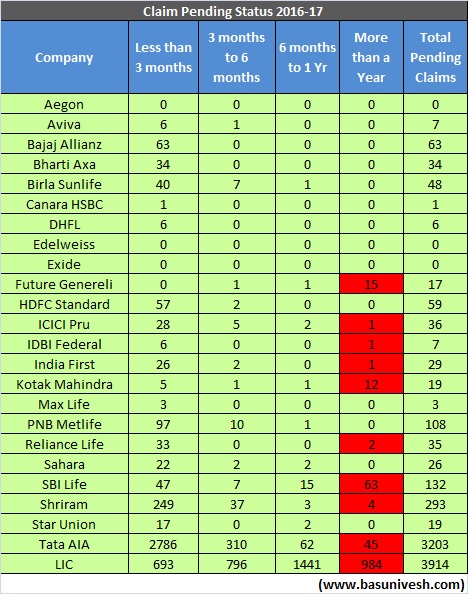

Claim Pending Status of Life Insurance Companies in 2016-17

The greatest fear for all of us is how fastly the Life Insurance Companies settle the claims. Let us now analyze the data of claims pending with Life Insurance Companies in 2016-17 and how old they are.

You notice that Future Genereli, SBI Life, Shriram and LIC are leading in pending the claims for more than a year. Reasons may be unknown to us.

Best Life Insurance Company in 2018

Based on the IRDA Claim Settlement Ratio 2016-17, which are the Top and Best Life Insurance Company in 2018? I select only five based on above data. You may differ in my view and come up with a different set of ideas. But these are my choices.

- LIC

- ICICI

- HDFC

- Aegon

- Max Life

Few important points before jumping into selecting of Life Insurance Companies

# Claim Settlement Ratio is raw data

As I pointed above, claim settlement ratio is just a raw data. It will not give us the specific data. Hence, never rely on this single data alone while shortlisting the insurance company.

# Concentrate on Product rather than company

Choose the product which suits your requirement and premium affordability. Declare the facts properly. Never hide any material facts. If all these you do, then an insurance company will have to accept your claim. Never give a room of suspicious on you to reject the claim.

# Section 45 of Insurance Act will guard YOU

According to Section 45 of Insurance Act “No policy of life insurance shall be called in question on any ground whatsoever after the expiry of three years from the date of the policy, i.e. from the date of issuance of the policy or the date of commencement of risk or the date of revival of the policy or the date of the rider to the policy, whichever is later”.

It says a lot. Even if you shared wrong information or hid some material facts, then also it is purely life insurance Company’s responsibility to dig deep and find out faults WITHIN 3 YEARS ONLY. After 3 years, they cannot question. Note the period of 3 years, it is from the date of issuance of the policy, or the date of commencement of risk or the date of revival of the policy or the date of a rider to the policy, WHICHEVER IS LATER. So let us say if you took the policy today and after a few years, the policy lapsed due to non-payment of premium. However, you thought to renew it again and paid all dues. In such situation, this 3-year period starts from such revival date, but not from the original policy issued date.

Read the complete details about this IMPORTANT act of Life Insurance in my earlier post at “Term Insurance-Claim Settlement Ratio no more a big criteria”.

# Disclose the facts Properly

While buying Life Insurance products, you must fill the proposal form on your own. Never allow any agent or Life Insurance Company representative to fill it. Disclose the facts properly without hiding anything. This will really help you in a big way. Also, it will not give any room for insurers to reject your claim.

Do the things properly which are in your hand. Rest HOPE for the best 🙂

Hi Basavaraj,

Could you please guide me on this.

***Fight against HDFC LIFE INSURANCE COMPANY*** HALLA BOL

Hi Team,

I have HDFC life term insurance policy to cover my home loan where critical illness is covered. I had major heart attack with 100% blockage on right artery on 29th October 2018 so gone through angioplasty. So i have submitted my critical illness claim to HDFC life insurance company in the month of December 2018.

I refute HDFC life statement that i had diabetes at the time of issuing me a policy so they have rejected my critical illness claim which has no grounds at all. No one has conducted my any medical tests from HDFC life before issuing me a policy then how they can say i had diabetes. My two other insurance companies i.e. Aegon Life and PNB metlife have taken all my tests before issuing me policy and now both have approved my critical illness claim within a month without any issue.

Now I am totally frustrated with this type of service from HDFC life,as i am a classic customer of HDFC Bank from last 15 years and they are giving me such service.I am a corporate employee with more than 3 lacs of employees in our company, so that i can spread this on our social forum. Social media is too powerful so they may definitely loose their business and eventually people will loose faith on HDFC life.I am not able to concentrate my job due to this issue also i am getting mental harassment due to this. I have already shared this on Facebook, Twitter, Linkedin, Instagram and Whattsapp.

Furthermore, I have already enclose a claim approval letters from Aegon Life and PNB Metlife to HDFC life for reference.

Notwithstanding that i have already submitted all the required evidences, it has now been 4-5 months since i raised my claim. This delay is unreasonable and it appears that we have now reached a deadlock. I have done all that i can do advance my claim but they have failed to deal with it adequately. My claim is dully covered by the policy and if i do not hear from HDFC bank within a week time then i may refer the matter to the financial ombudsman service without any further warning.

I looking for compensation as well as my critical illness claim approval.

My humble request you to look into the matter and do needfully in this on priority.

Thank you for your anticipated cooperation in this matter.

Please find my below details. Also sent legal notice of 1 CR for mental harrassement.

Loan Account. 402HPV57599009

Member Code / Master policy Number. PP000247

Consumer Court complaint No.0108155/2019

IRDAI complaint No.03-19-014947

Regards

Vikas Nhavkar

Dear Vikas,

The biggest MYTH with many of us is that we consider as if the ESTEEMED customer for Life Insurance company also if we have an account with their subsidiary bank. Do remember one thing that HDFC Bank is a different entity than the HDFC Life. Now coming back to the claim rejection, you have already raised an issue with IRDA. Better to wait for their process.

Dear Basavaraj, There is no response from IRDA and consumer court, they are saying file a police complaint against HDFC Life, I have already sent them legal notice of mental harassment even they are not replying to legal notice as well. Now i have raised my concern with Ombudsman team to proceed further.

Dear Vikas,

The best way is Ombudsman but not IRDA. If Ombudsman also not help you then drag them to the court.

Dear Basavraj,

Based on online research I am confused between TATA AIA and MAXLife for taking term-plan for 1 Cr.

I prefer TATA & AIA (100 yrs history)considering the brand name.

But TATA AIA claim settlement period is very high (one of the highest) in the above data on this site which bother me.

MAX has very good settlement period and is a decent brand too

Pls. suggest. what to chose.

Dear Niket,

Refer my latest post “IRDA Claim Settlement Ratio 2017-18| Best Life Insurance Company in 2019“.

I am 48, M, tee-totaller, Diabetic for 10 years. Looking for a Term Plan (online or offline) for 50 L or 1 Cr. Max. age coverage of atleast 80 or even 85 years. Let me know the best plan, potential risk, mitigation, claim ratio (online and offline), assured claim in case of any event.

Dear Shyam,

You are looking all benefits in a single plan. Do remember that they are into business but not for social cause. They first cross check your health issues and income. Based on that they issue the policy. Refer the above post properly and knock the doors of the insurer. By the way, do you need Life Insurance beyond your retirement age?

My age is 33 & I want to take a term plan for secure life. I have a medical history of angioplasty & already max life & icici decline my application for same reason.

Plz suggest me any insurance company with this medical history issue the policy?

Dear Amit,

Hard to say who will accept. Try your luck based on your comfort with companies.

Hi Amit, I have also gone through Angioplasty, so i inquired we will have to wait for 3 years to buy new policy.

Hi,

ICICI term plan is providing an option to complete premium within 5 years for a plan of 38 years. For payment tenure of 40 years, it costs Rs.7972/year. It costs Rs.30,924/year if paid payment tenure of 5 years.

If calculated this gives around 50% savings in premium for same benefits.

What is your advise on opting for short payment tenure ?

Dear Vikram,

If you can afford the premium, then go ahead.

Dear Sir,

I am planning to buy online term plan of 50L and upto 75 years.

also want waive of premium rider into my term plan.

I am confused between Aegon Life (6574/-INR Premium) Vs Edelweiss Tokio (7029/-INR Premium) Vs Max Life (7508/-INR Premium).

Please suggest which one is better ?

Thanks

Dear Hiral,

All are equally good and bad. Choose the one which is best suitable to you (comfort).

Dear Sir,

My name is Naman Vashishth. Age : 27 Year. Annual Income : 5 lakh Unmarried. I want to buy term plan of 1 Cr. which can give me cover upto 70 year. Which company do you suggest for me.

Dear Naman,

My suggestions are already listed in above post.

Very helpful article indeed. 1. Is it wise to buy Life cover with ADB rider and critical illness rider or would it be better to buy it seperately.

2. I am planning to buy Icici i protect with both these riders..however i have an option to buy TATA AIA critical plan separately.

Note: in life cover will stand reduced to the extent of CI payout with reduced premium thereafter.

What should i opt for?

Thank you.

Dear Tejas,

1) Buy them separately.

Thank you Sirji. Would be grateful if u can clear one doubt.

My Age is 45.

Can i take 3 policies as under:

1) 1.0 cr SA life cover of ICICI (40 yr) with 25L critical cover (30 yr). (34 Illness cover) and 100% ADB.

2) 1.0 Cr SA basic life cover of Tata AIA (35 yrs)

3) 25 L Critical Cover (15 illness 30 Yrs).

REASON being: Only ICICI offers 34 illness along wIth ADB cover. Premium for 1 cr SA of TATA is lesser. And hence the combo.

My worry being: would both Icici and Tata will pay on diagnosis of critical illness? Any issues I might face at the time of claims if i take such a combination?

Would really be thankful if you can guide me on this.

Best regds

Tejas

Dear Tejas,

What is the reason of combining Life with Critical Insurance?

Icici covers more than 25 lacs of critical cover only if its a part of a term plan. In a standalone plan their limit is 25 lacs.

But i get your point… I should rather take 25 Lac of Critical cover from Icici and Tata each separately…and the term plan separately. Got this. But would both companies honour my Critical care claim at the same time or can that be a problem. If it can be a issue wouldnt i be safe taking 50 L critical with icici term plan with 34 illness cover?

Dear Tejas,

Treat the claim separately for Life and Critical Insurance. Who honor or who not, depends on many things. Do you think there is any GUARANTEE of honoring your claim if you took both with same insurer? Why I am saying for separate is that standalone critical cover always gives you exhaustive features which is not possible with riders (because they come with so many limitations).

You are so right. Thank you for your support on this matter. Though Hdfc has a rider which waives of Entire premiu upon diagnosis of any of 34 illness BUT Will go for it seperately. Really appreciate your feedback.

sir namaskara iam subrahmanya frm kundapura my age 45 i confused in lic term insurence and private term insurence pls advise me i for term insurenes private or govt pls

Dear Subramanya,

You can buy either from LIC or from Private insurers. Both are equally good and bad. Don’t do so much research.

Dear sir,

Your articles are most informative. Please continue.

Kotak life is claiming that their claim settlement ratio is 99.4 %. Is it correct?

Dear Sivaji,

Please cross check the same either with my data or IRDA’s Annual Report.

Hi sir, I have completely disclosed all the medical details while taking the policy. My doubt is like health status might change at anytime after taking the policy I might get hypertension or diabetes after some years. Is it advisable to keep the company posted about my health details, will company increase premiums incase if I disclose the details. Please let me know. I am asking because incase tomorrow they should not reject the claim based on non disclosure of the facts.

Dear Satyam,

Not required. Because they need your health status only at the time of policy issue.

Hi,

I’m planning to take term insurance. i see huge difference for smokers and non-smokers. i’m smoker and planning to take term insurance as non-smoker to minimize the premium since as per IRDA SECTION 45 if the policy completed for 3 years there are no issues in claim settlement process even though if i hide material facts.

2) Kotak mahindra is offering term insurance for 1 crore without medicals so i’m planning to take that since i’m aware of sec 45.

3) As per sec 45 insurance companies have a right to do medical tests within 3 years but not sure how kotak is offering term plan without medicals.

plz let me know u r thoughts

Dear Kittu,

Sec.45 of Insurance Act does not mean you hide anything as per your wish and buy it and let insurance companies accept it. Please read the section carefully. It is not you who will be under trouble but your dependents for your just one mistake.

Sir, I have a Birla Sun Life insurance dream ULIP policy which I am paying regular premium since 2008. In 2016 I have taken max life term cover for 50 lacs. Recently I am getting attracted towards ICICI or aegeon because they are offering terminal illness benefits. But I cannot have three policies together. So planning to surrender Birla policy and take one more new policy from ICICI or Aegeon Religare. What do you suggest sir, is it advisable to stop 10 years old ULIP policy. In dialemma, please guide

Dear Satyam,

If you are looking for then why the ULIP for you?

My age is 31. I have term plan of Max life with Rs 50 lakh coverage since 2015. I am thinking to increase coverage to 1cr. Is it good idea ?

If yes, what should i do ?

should not renew existing and take 1Cr new plan?

or

keep renewing existing and purchase new 50 lakh coverage ?

If purchasing new 50 lakh then it should be beneficial to purchase from same insurer or different insurer?

Please advise

Dear Kumar,

Many of us have the biggest misconception that buying Life Insurance is the one time vent. It is not like that. You have to review it once in 5 years at least and if your liabilities or responsibilities are increasing, then you must enhance it. If you are OK with the current insurer, then go ahead with them only. Otherwise, take the additional coverage from other insurers of your choice. Better to stick to the same insurer.

Thank You

I have taken an aegon life insurance policy. While filling up the policy I have filled up my annual salaried income as 4,00,000 instead of 3,77,000. This after speaking to aegon customer support that my income is 3,77,000 but i needed a 1cr cover. They advised me to fill up my income as 4,00,000 as I am a salaried individual and also as my age is very low (26 yrs). While sending them the document my annual income cleary shows as 3,77,000. They assured me this would not create any problem in the future. What is your take?

Dear Clayton,

Yes, they are right. Don’t worry.

Dear Sir

What happens when insured person buys a term insurance policy while on job. After few years , leave the job and then dies. Would it create any issue in settlement.

Dear Rajesh,

Not at all. Because they need your financial status only at the time of issuing the policy.

Hello sir, one question I want to ask that in term insurance claim in natural death ,there are additional requirements of hospital doctor’s statement and discharge summary’s ,test reports for past illness . Why so ? Is there post claim investigation by private agency’s ? What is procedure,.

Dear Ratan,

Such investigation is not ONLY with private sector companies, even LIC also performs extensively when they have a doubt and especially if it is early claim (death within 3 years of policy commencement).

Sir,

Thank you for such a nice article and explanation. You are saying that Aegon is one of the best life insurance company as IRDA Claim Settlement is above 97 percent, and it is ranked above SBI life. But, if you look at the number of policies for AEegon is mere 588 vs 17,610 for SBI life or other companies. Isn’t 588 very low number data point to conclude that Aegon is a good insurance company?

Dear Tanmay,

I never said any particular company is BEST. Also, above companies are just shortlisted but not ranked. Above that, as I already claimed, CSR is just a raw data. Hence, never rely too much on this single data.

Hi Sir,

I am looking for a health insurance for my mother age 44 years, few weeks back i have done medical health check from rockland hospital (full body) , Hythroid is the main issue that has been detected, for thyroid she has been taking medicines since 8-10 years. And about the Hypertension is normal 110/60. she was also taking medicine for the same since 8-10 years, but now doctor said, that no need to take any medicine and no need to declare for the hypertension.

so what to do. & for insurance company i am confused b/w (1) Religare (2) ICICI lombard (3) star Health.

so please suggest

Dear Pramod,

Better to declare the conditions. Let the insurance company decide.

Hi,Sir

I have taken a term plan of one of private insurer and i have not disclose my family health as mom is suffering so many deases like diabities,High BP,kindney infection.

So will it affect at the time of claim.

Pls suggest.policy issued

Subham-If you hid the health issues of your mother during policy issuing time, then it is your fault. Better to disclose the same immediately.

Sir

I planning for taking a term Plan.i found many of companies in joint venture form. I have 2 queries

1. What happen if joint venture will separate in future after taking term plan. Will they bound to continue policy, if yes then which format. Whether one company will take full responsibility or they will share on 50-50basis.

2. Suppose Joint venture discontinued and both companies decided to close down the insurance business completely. Then what will happen with insured person as they paid premium many years. Whether they need to take new term plan from another companies or is there any Government implications to save their customer to get rid of this anonymous situation.

Sheetal-Refer my post “What if your Insurance Company goes bankrupt?“.

Dear Sir

Please confirm if I take max life insyrance policy today for my father and by chance in case aomething happens within 1 year,Then will I get a claim or not.?

Sheely-There are MILLIONS of reasons for that SOMETHING HAPPENS, then how I or Max Life can guarantee you on that??

Thanks for the articles and prompt responses..As I just started reading your posts and seems very good for me..It is very helpful if you clarify my questions which are pointed below.

Me and wife are in our 29 th age and we don’t have any life insurance policies till now..My wife is NRI and have an annual salary of 15 lack..Now I resigned my job and left India to abroad to find a job where my wife works. So my doubts are:

1) At this point of unemployment, can I get coverage of 1cr which i presume? Else is it best to take Insurance to wife with a sufficient coverage?

2) Wife is arguing for an Endowment plan as she aiming for a return in future. So which is better TERM or ENDOWMENT Plan ?( as stated she is having salary of 12 lack /annum(government job) and liabilities about 60 lack till now)

3) For me, does it s a better idea to take insurance after having a permanent job and salary?

4) As NRI, are there any issues or conditions to take online or offline insurance in India?

5) Do you have any suggestions or instructions for us while choosing policy for such NRIs?

6) Is there any problem will face at the time of settlement of claims to us or our nominees?

7) Do we benefitted under policies while abroad?

Albin-1) If you have last 2-3 years IT Return proofs, then you can buy it. Else, yes your wife has to buy.

2) Term.

3) As per Life Insurance concept, if someone financially dependent on you, then you must have it. Else, it is not required.

4) Nothing such but check which companies offer to NRIs.

5) No special points to select.

6) Hard to say BLINDLY.

7) Life Insurance is the concept of loss compensation tool rather than benefitting tool.

THANK YOU SO MUCH..

Hello sir i want to buy an online term plan of ICICI. i am interested in it because it has several features such as critical illness.. accidental benefit rider etc. which neither LIC nor SBI life has.. But my relatives are saying to take policy from a govt. company as private companies such as ICICI etc.. trouble later on during claims settlement and so they cant be trusted. Should i go for govt. name or feature loaded ICICI term plan?

Raghav-I will not differentiate between public and private sector companies. For me all are equally good and bad.

AS COMPARED TO LIC ?? WHETHER PVT COMPANIES WILL PAY CLAIM??? @40 YRS AGE PVT TERM PLAN COSTS 20K A YEAR AND LIC COSTS 50K A YEAR… !! DO U THINK WITH AGE 75 .. ANOTHER 35 YEARS PRIVATE COMPANIES WILL BE ABLE TO PAY CLAIMS?? AND ARE THESE REJECTION ON DEATH CLAIMS ?? OR ALL CLAIMS INCLUDING MATURITY AND OTHER CLAIMS FOR OUTSTANDING CLAIMS AS SHOW ABOVE??

IF 20K IS PAID FOR 35 YEARS THEN TOTALLY 7 LAKHS IS PAID IN 35 YEARS… AND MOST LIKELY OUT OF 100 PEOPLE 70 WILL DIE.. HOW WILL INSURANCE COMPANY PAY CLAIMS??

I’M COMPARING ICICI PRU .. HDFC CLICK TO PROTECT AND TATA AIA TERM PLAN OF 80 YEARS..??

WILL THESE 3 COMPANIES GENUINELY BE ABLE TO PAY CLAIMS???

DO U THINK TERM PLAN IS A SUSTAINABLE MODEL FOR PVT COMPANIES?? AND DOES SECTION 45 GUARANTEE DEATH CLAIMS AFTER 3 YEARS??

OR WILL THEY INCREASE THE COST IN FUTURE??

YOUR VIEWS?? AND WHICH IS THE BEST TERM PLAN IN PVT COMPANY??

Kunal-Do they accept claim??-YES and NO and depends on the claim and to me all insurers are same.

Do you need life insurance when you are 80 years of age?

Premium is always fixed and there is no escalation of premium in middle.

Hi,

I want to conf that term plan ofexide life insurance good or not to buy because they gave cash back of full amt if nothing mishapped. Is to. Buy or fake? They gave it with written.

Is exide life good compny or not. No other compny give money back in term plan,

Pls guide

Kundan-Return of the premium option in term plan is the WORST feature. Rest you have to decide.

Dear Sir,

Why do you term the Return of premium option as the worst?

I am planning to buy TATA AIA sampoorna raksha plus plan which includes return of premium at the end of maturity.

Please help.

Regards,

Laxman Selvam

Laxman-Check the premium difference and something called TIME VALUE OF MONEY concept.

So do you mean to convey, if I invest the premium-difference amount elsewhere, I might end up with a higher return( considering at least 5-6% growth for around 30 years) than the one offered by the premium return policy?

And also how’s TATA AIA as a plan on a whole?

Laxman-They are into business and not for social cause. Hence, each facility will cost you. My selection is listed in above post.

Hello sir

I want to purchase Bharti AXA life insurance . So Bharti AXA company is good or bad.

Pankaj- If you already shortlisted, then what is the doubt?

Aegon life insurance is offering me policy without it’s hard copy

So it is safe to buy the same through online

Ashvani-Yes. But share that softcopy with your family without fail.

Sir my confusion is that which one I should go with icici Prudential or Aegon life insurance

Please suggest

I have budget issue also

Ashvani-For me, both are equally good and bad.

Morning sir, I want to purchase term insurance but I am confused Between two companies Aegon life and icici Prudential and I also have budget issue so please suggest which one is better.

Ashvani-What is your confusion?

Sir My Age Is 29 and I want to purchase term insurance but I am confused between ICICI Prudential and Aegon Life so please suggest me from which I should go with?

Also I have budget related issues

Plz reply accordingly

Ashvani-What is your confusion?

Will you suggest a best policy with Sum insured 5 or 3 lakh with lowest premium and maximum coverage especially day care

Sir I have heard that royal sundaram is pathetic in customer service and settling claims ..

Your 2016 2017 list does not reveals the company too .I am confused ??

Aditya-If you are doubtful, then change your insurer. As simple as that.

Hi sir is royal sundaram health plan is a good one .Or I should switch to other one .

Aditya-If the premium is affordable to you and plan features suitable to you, then why to switch?

Sir I mean to say I am planning to buy an insurance policy from royal sundaram. ?

How is the performance of this insurer ??

Aditya-I already told that. If plan features and premium is affordable to you then go ahead.

Sir, Good morning

Agar claim settlement ratio me Birla 95% se niche hai to Birla Sun life ki policy kharidne me koi problem ho sakati hai Kya….our LIC wale bolate hai ki Private company to ham kis had tak bharosa kar sakate hai.

Nitin-You can buy Birla product if you are comfortable with features and premium.

Sirji

I am 43 yrs old and my wife is 40 yrs old. We both are working. Currently i have hdfc term plan for 50 lakhs.

There us no insurance for my wife. I am confused whether we both should be insured or my insurance is good enough.

It would be great if you can advise me on this.

Pravin-If someone is financially dependent on her income, then you can buy the Life Insurance in her name. Otherwise, Life Insurance is not required for her.

Thanks a lot for clarifixation.

Pravin

Sir, Maine December 2018 me hdfc 3d term plan 50 lacs k liye hai. Meri age 32 years hai. Mere pass already aegon ki 50 lacs ki policy 2015 se hai. Hdfc ne mera medical nhi kiya aur policy issue kardi hai. Maine kabhi smoking aur drinking nhi ki hai. Aegon walo ne to medical test Kiya tha but hdfc ne nhi Kiya . Koi problem to nhi hogi hdfc ko lekar plz zaroor bataaein mehrbaani hogi

Sajid-If you disclosed everything properly, then you no need to worry.

Thanks a lot, sir

HELLO SIR GUDEVENING, my current age is 56 years old. My annual income is 5 lacs annual. what is criteria basis for term life cover insurance according to income, if some want more insurance cover than, is it possible or not?? Plz

Ratan-The ideal cover should be around 15-20 times of your yearly income+existing liability.

I am a recently recruited probationary officer at SBI, 29 years old, one of my staff members, who sells insurance basically is recommending me SBI LIFE, but reading the IRDA reports I am having second opinion. Should I choose LIC or Aegon over SBI Life, since I am an employee will I get some advantage as compared to others for term insurance?

Anonymous-No such advantage fo being an employee. Because SBI Bank is a different entity than SBI Life. Choose the one which comforts you.

hello sir , i am a 55 yrs old , i purchased a hdfc life term policy for 50 lac for 15 yrs upon my 5 lacs income ,but just after 2 months i again buy a icici prulife 50 lacs cover for 20 yrs , but in this second policy icici pru, i did not disclose about first one hdfc life policy . should i now i disclose to icici prulife for first one hdfc life policy? what i do now ? icici prulife will accept my disclosure now for first one policy or not

Ratan-You have to inform to ICICI Life about HDFC Life Insurance. But you no need to inform to HDFC Life about your ICICI Life Insurance.

HELLO SIR GUDMORNING, THANKS for reply. If I disclose to ICICI prulife about my previous hdfc policy, is ICICI Prudential will accept to it or not?? . I afraid about that either they will cancel my policy because I state 5 lacs annual income in proposal application, I want that my Nominee will be not face any issue in claim procedure, plz guide me

Ratan-It is better to disclose and clarity. If they reject then you have the option to buy from others. What if you hide and they do not accept the claim after your death?

HELLO SIR I HAVE DISCLOSED OR INFORM TO ICICI PRULIFE ABOUT MY PREVIOUS HDFC LIFE POLICY ,THEY REPLY BY BELOW FOLLOWING

Dear Mr. Ratanlal Acharya,

We refer to your email dated 28/02/2018 for ICICI prudential policy number 21640264.

As per your Existing policy details shared with us post issuance of the policy, we would like to inform you that we have verified the revised details shared by you and we confirm that there is no change in the decision and policy terms and condition will remain the same. Hence we would like to convey you that we have accepted the policy with the necessary details shared by you.

We look forward to supporting you through a life of financial security.

Further, We thank you for choosing us as your preferred life insurance provider and hope that you are enjoying the benefit of security that our policy offers you.

However you can retain this email for future reference.

Hope we have been able to address back to your concern.

Ratan-Then let it be.

I am an 27 year individual. Looking for term insurance, shortlisted PNB-metlife Mera Plan and HDFC life(Extra Life). Both almost matched 95% features, even premium. Only difference stands is coverage years. HDFC says till 67 years (ideally), PNB at that premium says around 82 years (ideally). Let’s say taking in count ideal retirement age of 60 years.

2 question to be answered.

– Is term insurance be taken till 70+ years?

– Secondly, as per above IRDA data. PNB stands way behind than HDFC. Plus, recent outlook of PNB-Bank fraud (though a govt PSU), I am really doubting on it.

Satbir-1) Not required.

2) Better to go for HDFC.

Hi Basavaraj…Any specific reason for not going beyond 65-70?, is it only because of premium amount (in my case it’s around 12l) has to be paid after retirement (here, we are not sure about source of income after retirement)….

Secondly, I felt PNB offering better features than HDFC, you might have a clue on PNB…Just worried about their claim settlement ratio.

Satbir-Do you need Life Insurance when NONE financially dependent on you? When you retire, then practically none depend on your INCOME right?

Yeap!!! that’s correct…Thanks a lot Basavaraj for prompt response….

Was looking after HDFC life….Found many health relate riders…are they should be taken as part of term insurance, I mean those health riders are generally part of health insurance, isn’t?…They, is there a use case for health riders in term insurance?….

That too, health riders comes with a clause saying “post 30 days of diagnostic and the person should be alive after 30 days”…

Satbir-Buy critical illness riders separately from general insurance companies and buy life insurance only from life insurance companies.

Well, thanks for the prompt reply..Any specific reasons for it?.

1) Does buying health riders as part of health/general insurance has more advantage over term insurance providing health riders? Can you highlight any?

2) I was thinking of adding only disability rider and removing others. I think that works.

Satbir-1) Yes, they provide you additional freedom to choose the coverage of sum insured. Refer my post “Best Critical illness policy in India – Comparison Table“.

2) Even that also be purchased separately as an accidental insurance.

Thanks once again for prompt reply.

Your blog is really good for clearing off queries with prompt replies.

Sir, Aegon Religare or SBI Life? Wgich one is the best term plan, in view of low premium rates & high claim settlement ratio? Pkz guide.

Ravi-Aegon.

Hi,

Thank you for the details. Based on your analysis, i just wanted to know your view as to why Aegon is in 5th place despite having no claims pending and having claim settlement ratio of more than 97%?

I am planning to take Aegon iTerm insurance plan which insures upto 80/100yrs and the premium is very less compared to similar plans for similar insurance term from other companies. Any views on it?

I am 27 years old in good health condition.

Thank you.

Akshay-Don’t say it is at 5th place, but say as it is one among top 10.

hello

kindly advice me i am salary person,i want take IRDA exams. will you provide details how to attended exma

Prakash-Knock any Insurance company of which you want to become an agent.

Hello sir,

I am a government servant insured under group insurance scheme of state government and premium is also deducted every month, in this case shall I have to disclose this scheme while taking term insurance plan.

Shashikant-Better to disclose as you are paying the premium.

Hi sir,

I am 34 years old and planing to take term policy for 35 years. Plz suggest me one good company in that 5 list which covers all like critical illnesses increasing sum assured accidental Beni fit etc., which has options of coverage in case of god act war terrorism and susuide also.

Chaitu-Buy the plain term plan without riders. You can refer my earliest post “Top 5 Best Online Term Insurance Plans in India in 2017“.

Hi Sir,

Thanks, I have gone through your post and decided not to go with riders. but w.r.t terms and conditions, can you plz suggest which one is good. Also let me know if it is better to take policy with limited payment option like one time payment or 5 years payment with policy term for 35 years.

Chaitu-Hard to explain each term for you. However, if the premium is affordable for you, then go ahead for limited payment option.

Thank you sir, 🙂

Hi Sir,

I plan to take a Term policy from MAXLIFE insurance for 30Lakhs. I stopped smoking completely for the past 2 years. I am not a alcoholic. Will the smoking habit in the past impact my term policy creation?. Will they ask me provide any medical test?. Please advise

Mani-If you really stopped smoking from past 2 years, then it will not affect your insurance buying. Yes, a medical examination is mandatory.

Sir i am 33years old.want to take a term plan 25lakhs for 17 years.which offline plan would be best for me.i prefer offline rather than online.please suggest.

Himadri-May I know the reason for choosing OFFLINE option?

Sir my family is not comfortable with online services.in online term plan claim is also made in online.

Himadri-Claim Settlements is not ONLINE for online plans.

Thank u very much.sir should i go for like term?

Himadri-I only suggest Term Life Insurance in the categories of Life Insurance.

Thank you very much!!!!.

I want to take an online term plan but I have hesitation because company will settle the claim or not in the event of death.

Parasuram-If you are so HESITANT then create a wealth so that in the event of your death, your financial dependents may not suffer any financial burden.

MY DATE OF BIRTH IS 22-09-1966 ,I WANT TO TAKE TERM INSURENCE . FOR YOUR ATTENTION HEAR I AM DISLCLOSING THAT I AM DIABETIC SINCE LAST TEN MONTHS AS WELLASALCOHOLIC AND SMOOKER(OCADSIONALLY) I WANT TO OPT FOR SA-50L FOR24 YEARS THAT IS UP TO THE AGE OF 75YRS. PLEASE SUGGEST THE BETTER FOR ME.THAÑKS.

Ambastha-It is hard to get at this age with such health complications. Try your luck with insurers of your choice.

The above claim settlement ratio data shown is only for individual policies sold or both individual and group policies.

Nikhil-Only for individual.

Nice article sir! I have a query. I have recently purchased SBI Life term policy. At that time I had ICICI pru life term policy which was in Lapsed condition. The same was disclosed as Lapsed in SBI Life application. SBI Life policy is issued and is now in force. Now my question is Can I now reinstate ICICI life policy? If I reinstate ICICI policy, Do I need to inform SBILife? If I don’t Inform SBI , Can my claim be rejected as wrong discloser or supresion of information? After 3 years (Sec 45) Can my claim be rejected on the same reason? Kindly clarify my queries. Thanks a lot.

Pavan-You declared the status as it was while buying plan. SBI Life was not insisted you to inform them whenever you either reinstate the lapsed policy or buy new one in future. Hence, you no need to worry even if you reinstate the lapsed policy.

Thank you very much sir for valuable and prompt reply.

Impressive artical for how to claim our insurance money in various insurance company and detail analysis of companies and compare with data.

I purchased online term insurance plan 4 years ago. At that time my annual income was x lacs. So i took term insurance for Sum Assured for 10x lac. Now my salary is doubled.

My question is

1. Is is possible to increase the Sum Assured now within the same policy? (or)

2. Discontinue the present policy and start a new one as per my current annual income? (or)

2. Continue the present policy and Purchase another Term insurance with another insurance company for the difference SA?

Kindly advise which is better and economic?

Chandra-1) NO.

3) Better to buy the new one with continuing the existing one.

Hi.Thanks for the valuable information. I already have a BSL Term Insurance Plan that has been in force for the past 3 years. However owing to the low CSR coupled with the lackadaisical customer/agent service I was contemplating switching over to ICICI/HDFC for their high CSR. Much to my dismay, a LIC agent informed me that they are all sailing in the same boat and it makes sense to only take a LIC Term policy. I am 38 years old and have a family of 3 dependents excluding myself. Would request your advice if it makes sense to switch insurance companies at this juncture. Thanks.

Malcolm-Never rely on the agent who is claiming so about LIC. I suggest you to continue the existing one (if you declared all facts properly).

Thanks a ton. Will do so as all facts were declared properly.

Hello Basavaraj,

I am planning to buy LIC online term plan for SA 50L. However I came across option of alcohol intake. I am a occasionally drinker (once in a month). But there’s option of daily intake only (30ml/day,60ml/day etc).

So what should I select there non alcoholic or lowest one(30ml/day).

i have hepatities b should any company will give term insurance, should i disclosed it to insurance company and if i have not disclosed then after 3 year can they reject my claim, how is aegon i thinking about it.

Ajay-You must have to disclose it. Issuing policy to you is completely insurance company decision. Hence, I can’t say anything on this. If you intentionally HID, then YES, they may reject the claim even after 3 years.

Insurance amendment act 45 can’t protect in this case even after 15 years?????

Ajay-Insurance Act 45 does not protect each every false claim (if intentionally made) to acquire a policy. That act made to protect genuine buyers but it does not mean I can declare anything and get it protected after 3 BLIND YEARS of Life Insurance Company.

What is your view on edelweiss tok io life insurance. Products

Priya-I already shared my views in above post.

Sir, how can I become an mutual fund Agent?

Harish-Contact AMFI or any of the Mutual Fund Company.

Dear Mr. Basavaraj,

Your claims ratio analysis is incomplete as it just talks about the individual business claims. You haven’t included the Group Insurance claims which form a significant portion of Life Insurer claims. In Group Insurance, there is minimal underwriting as Lives are insured basis enrollment in a group member policy holder like Group Loan Protection, Group Term Life etc. These schemes should also be analysed on claims settlement. Any insurer who has better group claims settlement here may actually be a preferred one as it has the right intent on creating a superior customer satisfaction. Hence, please don’t miss including the group claims along with individual claims for perfect analysis. All the best !

Amol-So as per you if the group claim settlement is BEST then that company is BEST? How be the Group Insurance judged with Individual Insurance? How can you arrive at an assumption in that way? For me as a life insurance buyer, always look for how the individual life insurance products claims are settled rather than PRODUCT TYPE B.

Hello sir,

I had file my itr of 2016-17 with my previous bank account details but my bank account has been closed, now my new bank account has been opened. so how can get update my bank account details & how can get my tds return?

please assist me.

Punam-You have to update the same in IT portal.

Hi Basu Sir,

Very well written article. Fully agree with your opinion, but beg to differ with you in one company. HDFC life, I was unhappy last year also and i am unhappy this year also. This is the fifth continuous year, HDFC life

Average Claim rejection amount is very high and its standing like kutub minar in the graph, plotted in this article (tallest among all). they have marginally increased their claim settlement ratio this year. thats all. I still feel HDFC life does NOT deserve 3rd place in your list. Sir, any particular reason why Canara HSBC is not in top 5? i feel they are doing lot better now a days.

regards

Rajesh-I know that HDFC slowly loosing it’s grip in the market due to the above data. But changing view immediately within 1-2 years is not good. I look for another 1-2 years, then we can judge. Because there may be many reasons for a particular year to deviate from the past data.

Canara HSBC is indeed a best company. But as I pointed, I look for 1-2 years and then take a call and above that I am bit biased towards existing old companies than the new entrant.

Not the correct way to read and interpret the data.

Avg Claim Amount settled and Avg claim amount rejected in incorrectly read.

Companies mentioned in the graph do a minimum term insurance of 25Lakhs

Hence Average claim amount settled and avg claim amount rejected will be not be lower than 25L

Dear Tarun,

How can you assume that the minimum insurance they did is 25 lakh types of insurance only?

Minimum Basic sum assured offered by private players is 25L and above.

Dear Tarun,

It does not mean that majority of policies issued by them will be Rs.25 lakhs right?

Good attempt. But the ranking given at the end has spoiled the effort. LIC has a benefit of 50+ long years which makes max claims as non early, most of them endowment plans, less SA, so obviously would look best.

It would be helpful if same data is published for Term and non term separately with break up of early and non early claims. That will help customers know best companies to buy insurance.

Santosh-Sadly IRDA not publish such Term Life and Non Term Life data.

Sir recently I have joined in Kotak life as advisor can I successfully build my career pl guide

Githa-It is hard to say anything BLINDLY.

Please provide me with your mail id

Imran-Reason?

The aegon company is very bad company they are rejected claim of filing claim time

Jivraj-Reasons for rejection??

The policy buying time i submitted all documents with income proof of itr but policy holer was dead early and policy is in force .i am claim the company and they are rejected my claim

Jivraj-I need the reasons for rejection. It is mandatory that you have to provide income proof while buying the policy.

Hi sir

I am an insurance agent and atn holder of mutual fund.I would like to recieve updates from you regularly.how can I?

Raka-Great to know about you. You can use the widget which is available at right hand side (in desktop version) where it is mentioned as “Signup to receive blog posts via Email”. Provide the details asked there, confirm your subscription. Then you will receive the blog posts directly into your email.

Can u give the actual term plan claim settelement report.

Ravi-Sadly IRDA does not publish such data.

Very informative article, thank you.

Sir,

Is there any health Insurance in India that occurs the treatment for the Rheumatoid Arthritis?

Manimekalai-Check with respective health insurance company.

Hello sir,

My question is that if I filled two years ITR file in this financial year then after how much time I can file the ITR for 3rd year.

The gap of that two years’ ITR and 3rd year ITR?

Rewanand-There is no such gap mentioned. If you have not filed then you can file it NOW.

But someone said that there should be a 10 months gap between last 2 and 3rd ITR.

Then What should I do?

Rewanand-Why not relying either on me or someone? Directly contact IT Helpdesk and ask them. As per me, there is no such rule.

Rewanand

if you ask in my case i had filed 2 year ITR at a time in Dec and the current year ITR which ended in march by APR so the gap was only approx 4 months and there were no rejections or disputes, however you need to look out only that all the relavent document to be inline, only to justify in case if your file is been picked up for audit.

also if you are a high net worth tax payer then better to have all the credentials in your position for at least 1 year. because they may pick up for audit any time

And sir I need your help…i have a policy of national insurance…my mom got hospitalised in July last year…TPA was sent a bill of 187000 but they didn’t approve 67000 giving invalid reasons…I’ve read the policy wording very very carefully…infact I read the lists of non- payable items… presently I train students for Competitive English…. I’m great at reading sections and clauses… I’m pursuing ICWA inter and have done CA Inter….I went on IRDAI site but they closed my grievance without valid reason…I wrote them a very detailed mail with reference to sections and clauses as given in my policy wording…but all went vain…sir should I apply to ombudsman…I want you to proof read my detailed article if possible… I’ll mail it to you… kindly provide your mail id…

Anurag-Surely you can approach Ombudsman if you are not satisfied with Insurance Company and Regulator.

If you don’t mind can you say the clause which led to difference and the reason stated by insurance company for rejecting 67k claim amount.

Hi Basavaraj, Nice and informative piece of study. Have you done a similar one for Health Insurance. If yes request provide the link to the same. Rgds, Colonel Raj Singh

Colonel Raj-I will do the same soon.

I read whenever you post…and I share your articles too…plz tell me what does the 2016-17 mean? Does it mean from January to Dec…or April to Mar?

And plz publish your article on current year’s medical incurred claim raito….

Anurag-It is for FY 2016-17.

It means till April 2016- March 2017

Anurag-Yes, this is what I already mentioned in above post also.

Hi, it awesome analysis of data provided by irda, great job.

I had buy Aegon life term plan, so it comes under Aegon Religare or what?,? Pls give your opinion.

Prabhat-Yes, it will be under Aegon Religare.

Aegon Religare is now Aegon Life. The data reflected is for Aegon Life and has nothing to do with Religare.

Kirti-What BIG mistake does it creates? For your information, even IRDA report also still mention the company as Aegon Religare Life but not AEGON LIFE. Can you knock IRDA at first and then me?

There is no blame game here. So you can stop being defensive. There are just 3 instances of Aegon Religare and all other mention Aegon Life in the report. This comment was just to clear confusion of the readers of your blog. I believe as an influencer you too wish to give out the correct info and not follow the inaccurate path. All in good faith I believe.

Kirti-“There are just 3 instances of Aegon Religare and all other mention Aegon Life in the report.”-Then first you must ask IRDA as a regulator to give the correct name to YOUR INSURANCE COMPANY. I just follow what IRDA reported 🙂

It has nothing to do with Aegon Life being my employer or not. This conversation

is just to clear the confusion YOUR article created in the minds of YOUR readers about Aegon Life. Once again, you don’t have to be defensive, I am just helping people understand, we do value our customers a lot. And yes, I appreciate and thank you for sharing such an insightful article. 🙂

Kirti-Let READERS decide who is helping in what sense 🙂 Because I already mentioned in our FB chat in the morning itself that I changed from AEGON RELIGARE to AEGON LIFE. But still, you want to HELP the customers 🙂

Yes, because even after that, one of your readers had some confusion. Was just trying to answer that. 🙂 And we ALWAYS want to help our customers, no two-ways about that. 🙂

Kirti-Wooow Ageon and Aegon employees!! Then can you reply to the one more reader’s blame that AEGON, where he mentioned that how the claim was rejected? Please follow up with that reader and let me know the outcome and reasons for rejection 🙂

Mr. Anubhav, you can opt for the limited premium payment with the long term INSURANCE plan. TATA AIA LIFE giving you the TERM INSURANCE up to age of 80 years with the premium paying term of only 10 years.

Regards

Umesh Verma

Sr. Life Planner

TATA AIA LIFE INSURANCE

Umesh-Do you think one need Life Insurance up to the age of 80 years?

Premium of Term Insurance , will it be coverd in Tax benifit.

Nandkishor-Yes, you can claim for deduction under Sec.80C.

Thaks a lot Sir.

Very useful aricle

Hi Basu,

I am 32 year old male working in IT field and my wife is also working. I have a son 1.5 yrs old.

I just wanted to know your views for how long i should take term insurance. I contacted one of the agent and he told me to take max 40 yrs term plan. But i feel i should go for 28 year term plan (32 Age +28 = 60 yr age) as i feel i will be having no liabilities when i will be reaching 60 -62 years & it would be waste to pay the premium. My son would be earning by that time.

Though everyone has its own thinking but just wanted to know your opinion whether i am thinking on the right track or should go for premium for years after 60 years of age.

Actually i might be missing something in my thinking which i wanted to discuss – why its beneficial to pay premium when i would be retired?

Anubhav-You are on right track but not YOUR ADVISER.

Hi Basu,

i have a doubt for ICICI & HDFC term insurance (life option – the simplest plan in both). Suppose if i take a cover of 1CR then both policies say that it will give 1CR to nominee in case of death but both policies have extra rider for accidental death. So it means both policies with life option will not cover accidental death? and it covers only natural death?

Regards,

Nicolas

Nicolas-YES. If you oped for the accidental rider, then the additional sum assured is payable in case of death due to the accident.

Hi Basu,

Thanks for the response. Actually my doubt was if i am not opting the accidental rider then the basic plan covers the death due to accident (Sum assured amount)?

Regards,

Nicolas

Nicolas-YES very much.

I have lic bheema policy but not paid premium for 3 years, if I repay total amount now can I claim the total three years amount under 80c for current FY.

Ram-Yes you can claim the tax benefits under Sec.80C. Because deduction under section 80C is available on payment basis.However, late fee or any penalty must not be considered for deduction.

Mr. Basu, who are you to decide ‘LIC has not done great job’? The avarage claim satellment ration(amount) is small as LIC is selling policy in every segment and even the poorest class of society which your so called BIGGER TICKET SIZE companies are not doing. You comparing service of train with plane?

I am sure you might have been rejected in an interview of ASISTANT by LIC OF INDIA!

Dear, Compare financial products only not company. Its not your job

Punit-It is not me who is judging, but IRDA data reflecting, which I just shared 🙂 It is you to decide or the buyers to decide which is BEST to them. Hence, cool down!! Rejected for an interview of LIC??? If you prove that I at least applied for any JOB of LIC, then I give up this profession else can you give up your profession??

It is not ME but you indirectly comparing company (LIC) with others. So please correct your views at first 🙂

Excellent article. Very helpful. Thank you!

Nithin-Pleasure 🙂

claim repudiated is not analysed. Its crucial parameter.

Abhay-Sir, I provided those numbers also in the first image. Also, the claim repudiated is definitely reflected in claim settlement. Hence, I thought of just share information. Let me know your views.