Which is the best critical illness policy in India in 2019? Many of us have Term Life Insurance and Health Insurance. However, we never gave the importance to Critical Illness policies. Let us see the importance of having a Critical Illness policy and analyze which is Best Critical illness policy in India 2019 with comparison table.

Why we need Critical Illness Policy?

Your Life Insurance will come into picture when the insured die. Health insurance in other hand is “Indemnity” based insurance. This means the health insurance will indemnify the cost of hospitalization. Hence, health insurance will pay you the cost of hospitalization cost.

However, in a case of critical illness policies, they are called “Fixed Benefit” plans. Assume you are diagnosed with Cancer, and then irrespective of the cost involved in treatment, an insurance company will pay you the lump sum.

Due to diagnose of critical illness, you neither may die nor hospitalized but bedridden due to this critical illness. In such a situation, along with hospitalization, you have to bear your family obligations from your own pocket.

Also, in a case of health insurance, the benefits are defined like room rent cap or ICU cap. However, in the case of critical illness insurance, an insurance company will just pay you the lump sum.

The major critical illnesses are a heart attack, cancer or a stroke. Also, there are major chances that you survive after diagnosed with such critical illness. Hence, to compensate the work loss, financial burden of kids education and your financial commitments, you need a product which can compensate such losses.

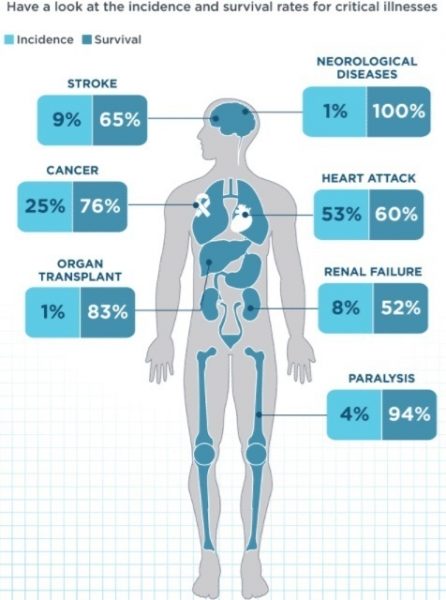

Below image will show you the possibility of survival % from the critical illness.

Source: – ICICI Lombard

Hence, we may say such survival after the critical illness will come with the COST. To compensate for this cost, you must have insurance.

No matter how good your health insurance is, there are deductibles, co-insurance payments, prescriptions that are no longer covered and exclusions. While you are recovering from critical illness, you’re not working. But that doesn’t stop the need to pay your household expenses, utility bills, EMIs towards home or car and your credit card bill.

Also, do remember that majority of health insurance products excludes the critical illness covers. Hence, it is important for you to have a critical illness.

It is not necessary for me to put some data which reflect the possibility of you and I may in future get such critical illness. Because now it is known fact that possibility is high due to our food habits, lifestyle and the stress we are into now.

Also, the medical inflation rising at an alarming rate of 10% to 12%. Hence, it is imperative for us to compensate such a high cost. We can’t pay all such costs from our own pocket. It will devastate our financial life and ruin us. Hence, it is a must for all of us to have a critical illness.

Best Critical illness policy in India 2019 -How to choose?

# Size of the cover-How much is the right cover? There is no such specific yardstick. But ideally, it should not be less than Rs.10 lakh. Also, few suggest having around 4-5 times of your annual income. But in my view, if you are capable of paying a higher premium, then go for higher cover. This will compensate your future medical inflation for certain year.

Ideally, I suggest the cover must not be less than Rs.10 lakh and also it must be around at least 3-4 times of your annual income.

# Illness covered-Higher the illness covered means higher the premium. Also, make sure that you must check different organs are covered than the same organs for different diseases covered. For example, a single disease may split into different cover and you may get fooled that the product is covered much critical illness.

# Definitions-The biggest task for all of us is to understand the medical terminologies. Hence, it is always best to consult a family doctor if you have doubt in this. Critical Illness policy turned to be complex for many of us because we can’t understand the medical words used in proposal or policy document.

Hence, it is a must to understand before jumping into buying.

# Sub-Limits-Insurers fix some sub-limits for each disease. For example, let us say there is a sub-limit of Rs.5 lakh for a critical illness of heart. If you diagnosed with this disease, then the insurance company will pay you Rs.5 lakh only. The policy will continue with a reduced amount of Rs.5 lakh.

# Renewal-You must always look for life long renewable products. Because the possibility of facing critical illness is high when you grow older. Hence, choose the product which offers you the life long renewability.

# Exclusion-You checks for the exclusions listed in the policy. Usually, the pre-existing diseases are covered after 3 years of the waiting period. The immediate cover of pre-existing diseases comes with a cost in higher premium. Hence, better to avoid.

Along with that, few plans specifically avoid few particular diseases. Hence, check the diseases that are excluded.

# Premium affordability-The more benefits you look for will comes with the cost. Nothing is at free. Hence, better you understand your requirement and plan accordingly. The premium will also increase as you grow older. However, if your purchased critical illness as a rider along with Life Insurance, then this will remain same throughout the policy period.

However, such riders come with limitations which sometimes may feel useless. Hence, even though standalone critical illness policies are costlier, better to go with them.

# Survival or waiting Period Clause-In critical illness policies, this is as per me is the BIGGEST drawback. Let us assume you today diagnosed with kidney failure, then these critical illness policies will accept the claim if you survived for certain period after the diagnose.

Let us assume your policy define the survival period as 30 days, then you must survive for a minimum 30 days after the first diagnoses of the critical illness. Then only you can make the claim. Assume the insured died before 30 days, then his nominee will not receive anything.

Do remember that this survival period differs for different diseases. Hence, better to check and know beforehand.

Along with that, there is a waiting period clause. It usually commences from the issue of the policy and around 90 days. Hence, an insurance company will not accept any claim if you diagnosed with a critical illness during this first 90 days of policy start.

# Claim Settlement Ratio-Even though it is hard to find the exact reasons for rejection of the claim, it gives you bit relief if you know the CSR ratio of your insurer. At the end of the day, CSR is a raw data which not point the reasons for rejection and delay in rejection. But give you some indication of how the company dealing the claims.

# Critical Illness as a RIDER or a Standalone-Many Life and Health Insurance products offer critical illness as a rider. They are cheaper than the standalone critical illness plan.

The biggest advantage of having a standalone critical illness is that the freedom to choose the coverage. Usually, in the case of Life and Health Insurance, you are not allowed to go beyond the sum assured or sum insured covered. However, in a case of standalone critical illness, you have the freedom to choose as per your comfort.

In a case of life insurance, the premium will remain same throughout the policy period. However, in a case of health insurance and critical illness insurance, it changes as you grow older (but in the case of health insurance in an age slab).

One more advantage of buying critical illness as a rider is that along with health or life insurance, your rider also gets renewed automatically when you renew both. However, in the case of standalone policies, you have to renew separately.

Nowadays few insurers offering you the disease-specific plans like Cancer Plan or Diabetic Plan. But in my view, it is better to go for plans which cover more critical illnesses than the single one or two. We don’t which critical illness we suffer.

However, when it comes to control and features, rider always comes with some restrictions. Hence, I prefer standalone critical illness.

Best Critical illness policy in India 2019 – Comparison Table

Now we understood what is the importance of critical illness policy and how to choose the best critical illness policy in India. Let us now look into the available critical illness policies in India and study the comparison.

Note:- I missed to update the Cigna TTK Critical Illness insurance policy details (Cigna TTK Lifestyle Protection-Critical Care Insurance Plan). They are as below.

The number of Illness covered-15 (Basic) and 30 (Enhanced).

Survival Period-Unable to identify.

Minimum and Maximum Cover-Up to Rs.3 Cr.

Minimum and Maximum Entry AGe-18 Yrs to 65 Yrs.

You notice from above table that Apollo Munich covers the maximum diseases but the survival period ranges from 30-90 days.

Also, for Religare and Star, the survival period is NIL. It means if the insured diagnosed with critical illness the next day of the policy issued, the insurance company will pay the benefits.

Star’s critical illness cover is costly. Because along with critical illness, it also covers hospitalization (like health insurance).

Considering the above facts, I assume Apollo, Max Bupa and Religare stands best with features and premium range and hence I consider them as “Best Critical illness policy in India”.

Income Tax Benefits of Critical Illness Insurance Policies

Premium paid by you towards critical illness insurance policies will be eligible for tax deduction under Sec.80D of IT Act. Do remember that this benefit is not available if you paid the premium through cash. Refer my earlier post for better understanding “Tax Savings options other than Sec.80C for FY 2017-18“.

Also, any claim amount you receive from critical illness insurance policy is completely tax-free for you.

Can we buy a critical illness policy?

The critical illness policy is the complicated product which defines many medical terminologies. It is hard for a common man to understand. Also, diagnosing of critical illness not enough. Even though your doctor diagnosed it, there is no guarantee that claim will be accepted. Because the insurance company’s own doctor has to diagnose and establish that you are suffering from critical illness.

Also, the definition of diseases is not so exhaustive. Hence, there is a scope that an insurance company may reject your claim on the benefits of doubts and no clear definitions.

Check for family history of your’s for such critical illness. If you found its necessary then go ahead. Because in many cases as per insurance companies, the critical illness which they define is hard for the individual to survive. Hence, he may end up with no claim but to pay the hefty hospitalization bills.

Buy enough health insurance. If you still feel shortage, then go for super top up plans. Create an emergency fund especially for such diseases.

Hence, I feel critical illness policies are bit complicated. Instead, I suggest enhance your health insurance and if possible go for super top up and create an emergency fund. Rest you have to decide based on your own family history.

Hello sir..

In case of riders with term plan critical illness benefit is paid from the sum assured of term plan which is supposed to be paid in the death event of candidate….

thereby decreasing the value of term insurance sum assured…

Should this not be the criteria of choosing option between standalone and riders bacause rider pay from candidates own money in a way…a

Dear Anubhav,

Your Term Life Insurance is required for a LIMITED PERIOD but your critical illness insurance is forever for you.

Dear Basu, I pray for your good health and all the blessings your readers have to offer. It goes without saying that your blogs have a multiplying effect through out India.

Dear NR,

Thanks for your kind words 🙂

Dear Basu,

Very informative article as always. Any specific reason to choose “Non life insurance” companies instead of life insurance companies. Or stand alone CI available only with this catogory companies.. pls clarify..

Dear Aravindan,

Life Insurance companies sell such a product as a rider but not as a standalone product. Hence, the features are limited and benefits are certain % of base life plan. Hence, it is advisable to buy as a standalone product.

hello sir

i am recently perches icici pru life insurance 50lc 50 years

and add for rider 3lac .it will be right a wrong sir

a fir take for separately critical illness insurance cover

please suggest sir

thanks kishor

Dear Kishor,

If you already purchased it then why the doubt now?

Hello Basu,

Could you please select top 5 from the given list as you had mentioned in https://www.basunivesh.com/2019/01/29/top-5-best-term-insurance-plans-in-india-2019/

Dear Anurag,

For me all are equal and based on that only I shortlisted. I never do a particular product suggestion.

Thanks Basu. Certainly a great blog. Quite great information is given which is essential to know before you buy any plan. Just one confusion here, I believe, Religare has stopped providing “Fixed Benefit” plans and started something like mediclaim covering 32 critical illness where, instead of fixed payment, the company will take care of all the expenses related to such illness. Would this type of plan be good in comparison to fixed payment plan?

Dear Prashant,

Thanks for your kind words. I am not sure about the change. However, if that is the case, then it is beneficial to the buyer.

I contacted the Religare Customer care. They dont have Religare Assure plan anymore.

I am all the more confused now, as they say that in the base plan they have critical illness covered (they dont have specific reference) but they say “any illness” . How is that possible. In addition to that they are also providing Critical Insurance plans for people who wanted a larger coverage for those particular critical diseases. I am confused.

Dear NR,

Why to stick to only one company?

Hi Basu,

Thanks for sharing detailed analysis on each plans. I don’t see criticare plan from edelwess. How is this plan compared to others. https://www.edelweisstokio.in/health-insurance-plans/criticare

Dear Laxmikant,

I have not listed this product because it is offered by Life Insurance Company. Here, I am concentrating on the products from non life insurers only.

Dear Basu,

I don’t see TATA AIA LIFE ci insurance figuring in the list provided. What is the major shortcoming because of which it doesn’t figure in your list?

Dear Anupama,

I am covering here NON LIFE INSURANCE COMPANIES but not LIFE INSURANCE COMPANIES PRODUCTS.

But what about Tata AIA Life Insurance Vital Care Pro? What i understand is that it is a critical illness insurance? I was planning to purchase this. Please advise.

Dear Anupama,

If you are comfortable with such offerings from LIFE INSURANCE COMPANIES, then go ahead. In plain, it looks good.

Dear Basu,

How is the ICICI PRU I PROTECT SMART term plan? I have planned to get this for 1 Cr with a term insurance for 85 yrs.

Dear Chayan,

Refer my latest post “Top 5 Best Term Insurance Plans in India 2019“.

Hi Basavaraj Tonagatti,

Can I have term policy with Basic Critical Illness Benefit (Lump Sum) in Aegon Life or any company why I have to purchase Critical Illness Policy?

Dear Makesh,

When you buy critical illness cover as a rider, then you will not get the exhaustive coverage. Hence, it is always advisable to buy it separately.

i have 2 company critical illness max bupa 10 lakhs and apollo munich optial vital 5 lakhs in case after year any Heart attack claim cover 2 company full amount payout?

i want to one more apply religare company 10 lakhs .So Any one illness claim in 3 company benefit full amount payout ? Total 25 lakhs

Dear Feroz,

Whether you can submit ORIGINAL documents to all 2-3 or 5 companies to prove your illness?

Hi Basu,

The Critical ilness that comes with Max Life insurance term plan seems to be much more simplied. No complicated medical jargons used as inclusion and exclusion criteria. Their claim settlement ratio is also very good. Any comment on their term plan + Critical illness + disability plan ?

Thanks

Amartya

Dear Amartya,

But is is LIMITLESS coverage when it comes to critical illness rider?

Dear Basu,

the Critical Illness is 50% of Life coverage. I know this means buying additional life cover for many, which may not be needed. But the payment condition for Critical Illness is very simple here. There are multiple CI (e.g. ICICI ) which I couldn’t understand. I’m not sure in case of any disease, they will pay anything or slip thru the exclusion criteria.

Thanks

Amartya

Dear Amartya,

CI is a complicated product. It is just your chance of getting the claim. Because many definitions provided in CI Insurance are generic and huge possibility that they may deny the claim.

Hi Basu, what is your view on new “fg heart & health insurance plan” while comparing with the above CI policies? (It has in Option 2 – Covers 59 Critical Illnesses)

Dear Nitin,

Seems good but the maximum maturity age is 75 years, which I feel hindrance.

Hi Basu, would you advise to do SIP & get the fund to use for critical illness? There are so many clauses & conditions which seems the CI claim difficult to process at Insurer end.

Dear Ritesh,

Yes, that is the best solution. In fact I hardly suggest critical illness to my financial planning clients.

Good point. But I believe, if anyone is detected with critical illness at young stage, SIP might not be suffice to cover all expenses related to such illness. I hope your point of view is not based on the assumption that the one will be detected with critical illness at very later stage of life.

Sir, can you suggest a single plan for Health insurance with critical illness as a rider? Do companies offer such a plan?

Dear Umesh,

It is always best to separate health insurance and critical illness insurance rather than clubbing both.

Also, for Religare and Star, the survival period is NIL. It means if the insured diagnosed with critical illness the next day of the policy issued, the insurance company will pay the benefit

THIS STATEMENT IS INCORRECT.

SURVIVAL PERIOD MEAN THE DAYS YOU SURVIVE AFTER HAVING DIAGNOSED WITH THE DISEASE AND NOT AFTER ISSUING OF POLICY

Dear Nitin,

Please check correctly. As per me, in case of critical illness policies, this is the definition. You can cross check with insurance companies.

Hi,

Seems Nitin is correct.

Survival period means that Insurance benefit is payable, only if the Insured is alive for a period of more than or equal to 28 days from the date of the first diagnosis of the illness/medical event or undergoing illness related surgical procedure for the first time.

https://www.sbigeneral.in/SBIG/what-survival-period

Regards,

Harshit

I am 61yrs having gone engioplasty 10yrs back now fit to buy Ci only having no other medical insurance suggest best stand alone CI

Dear Aravind,

The best are listed in above post. Choosing the one is left with you.

How about ICICIPRULIFE Critical Insurance policy? There is no survival period required to claim and you apply for claim on your first diagnosis.

Is it true? Please suggest.

Dear Rajnikant,

Yes, it is true.

Hello,

During policy renewal, does base premium for critical illness policy changes with increase in age ? (there is no break in policy which is standalone critical illness policy)

Thanks

Dear Anil,

It may change based on your age.

Dear Basavraj,

Greetings ! Hope you are doing…reading through your blog and comments to queries, I have following to submit and request your advise

I am 52 years old, taking medicine for hypothyroid,BP and Diabetic. My family consists of wife (43 yrs), Son(17 yrs),daughter(13 yrs).

I have this April taken a ICICI Pru term plan for 50 lac upto 60 yrs, there is a Rs 36 lac term plan by company up to retirement age of 60 Y, have taken Star Health Insurance policy for Rs 5 lac for self ( was for family for last 4 years, converted to self) and Rs 5 lac for wife & children (wife can claim the tax deduction). Have taken a Rs 10 lac ICICI Lomabard CI for wife (father recently expired of cancer). My both parents are aged 88 & 77 and have age related problems.

Please advise on the CI standalone policy (recommended company) and amount that I should take.

Also need to know, about the policy for children to be cosnidered now or later for Term & Health or is it too early.

Any other comments based on above current policy status

Thanks for your attention to above.

Regards,

Hari

Dear Hariharan,

I usually not recommend any single plan or company. Regarding amount, better to take the cover of around Rs.25 Lakh+. Regarding your kids insurance, they need Life Insurance, if someone financially dependent on their income. Otherwise, Life Insurance is not required for them. Health insurance is required for them.

Hi

Can you pl suggest

1.which company/policy provide CI for kidney donor person?

2. Any healthy person having CI already before kidney donate, then if he/she donate kidney in future then is there any restriction for CI claim ?

3. Any person with kidney failure but not yet Dialyses, is any company provide CI or Term insurance considering waiting period also?

I hope u will suggest my queries

Dear Devaraja,

1) There is no such DONOR SPECIFIC CI.

2) Donating is an individual wish and not considered as CI. I am not sure why you are considering KIDNEY DONATION WITH CRITICAL ILLNESS.

3) NO.

Hi sir.

Im a govt bank emp.my bank provides 4lakhs health insurance for me and my family. My confusion is should i go for another family health insurance or top up insurance. Plz suggest

Munna-First go for another family floater on your own. If both employer provided and your own health insurance not sufficient in future, then go for super top up.

But employer provieded insurance and family floater we avail only one right another one will be wasted

Munna-Yes, you have to claim anyone. But in case of sudden job loss, the one which you have will be handy.

Thnx for the information

I have come across Aditya Birla Critical Illness Plan where Plan 2 covers 50 illnesses and survival period is only 15 days. What is your view on this? Please go through the brochure and advise.

Avinash-Is it RIDER or Standalone?

Standalone

Avinash-Birla is a Life Insurance Company then how can this product be standalone product??

This is from Aditya Birla Capital. Here is the link: https://www.adityabirlacapital.com/healthinsurance/#!/activ-secure-critical-illness

Avinash-Aditya Birla is act like middlemen. I need the product name.

Hi,

I came across Kotak Mahindra Critical Illness Plus Benefit Rider which covers 37 illness and Survival period is only 30 days. Just wanted to know if you left it out for any specific reasons.

Thanks

Praveen

Praveen-Is it the rider of Life Insurance Product or standalone critical illness product?

Yes, it reads “KOTAK CRITICAL ILLNESS PLUS BENEFIT RIDER”.

It is a rider only plan. Need to opt with a base plan of course.

Praveen-But this post is for the standalone products.

Religare is not much big company , may not survive in future also what is the claim settlement ratios of these companies can u plz comment.

Rahul-Sadly such separate settlement data for Critical Illness is not available.

Dear Mr. Basavaraj,

It was really informative reading your comments on various insurance related issues.

I am 51 and my wjfe is 45. My family has a history of heart related ailments and my wifes family breast cancer related. I have a family floater for 10.00 Lacs and also intend to purchase a plain vanilla term plan for 75.00 Lacs.

I also had an angioplast a few months back. Should we both go for separate CI plans, say of 15-20 Lacs each ? Will my recent angioplasty be a deterrent for insurance companies in offering me a CI plan.

Your advise shall be highly appreciated.

Thanking you with warm regards.

ANAND MENON

Anand-Considering your health complication, yes it is best to go for critical illness cover. Regarding issuing of the plan, it is purely insurance companies decision.

Dear Mr. Basavaraj,

Thank you very much for your advice.

Since the decision for a CI is now confirmed, please also advise ” Should I go for a plain term plan plus a separate CI plan” OR opt for a “Term plan with a CI rider” . Please share your thoughts from the utility point of view keeping aside the commercial considerations.

Thanking you and looking forward to hear from you.

Best Regards

Anand

Anand-Go for a plain term plan plus a separate CI plan.

Is there separate CI plan available in the market? I think there are few, but premium increases/chnages every year/three year?

Binod-Refer above post for the plans available currently.

Hi Sir,

First, thank you for the very useful article.

My company provides a mediclaim policy of Rs.2 Lakh/year base cover for family members and an additional family floater of Rs.14 Lakh/year. Also it includes personal Accident coverage up to 6 times the annual income. It takes care of critical illness as well for more than 15 diseases, financial support for cancer treatment and many other benefits also.

I have taken a term plan. I’ve the following questions.

1. Is the health insurance coverage decent enough?

2. Except the base & floater cover, my family is not covered for critical illness or accident coverage.

Do i need to go for separate critical insurance policy for my family?

3. As per my company policy, retired employees also can choose to continue the coverage after some revision…

Is it ok to continue with this coverage post retirement?

Jayakumar-1) There is no specific yardstick to say that whether this much is sufficient or not. But relying totally on employer provided insurance is not a good sign.

2) You must have your own health and accidental covers (if need then critical).

3) What if they change this policy at later stage?

sir , i Want to take term plan – is joint ( me and my wife) term plan possible OR Joint Health Insurance ?

And which is more needed / important in today’s scenario & WHY ?

Ranobir-You want to take Term Life Insurance then why you are questioning about health insurance? Health is entirely different than term life insurance. Each product has its own need.

Hi!

Thanks for the wonderful blog. It is really helpful.

Most of the companies are private. What is the extent of risk coverage against closure / merger / winding up of such companies? That is, what happens if the company shuts down during the coverage period. What kind of protection do the consumers have for the remaining period of the insurance?

Arindam-Refer my post “What if your Insurance Company goes bankrupt?“.

Hi Sir,

Am 25 years old and want to buy a term plan. My confusion here is :

1) Should I buy a simple term plan with SA 1 Cr or

2) SA + CI + Accident benifit

If you suggest me to go with point 1, then do I have to buy the separate CI plan.

3) difference btwn CI along with term insurance VS independent CI

Thanks in advance 🙂

Charan-Go with 1st. Refer my post “Best Critical illness policy in India – Comparison Table“.

Thanks Sir,

do I have to buy the separate CI plan.

Regards

read your post thoroughly and made clear about how CI works and various ways to get one. Thanks

For Plain Term Insurance, am confused between the following companies:

1) Aegon 1 Cr for 80 years

2) MAX 1Cr for 65 years

3) LIC 1Cr for 60 years (Permium is very high)

Can you please help me choose any one from above and reason for the same.

Thanks in advance and Regards

Charan-Do you need Life Insurance beyond your working age?

Sorry, but I don’t know how to decide. Thanks

Charan-Yes.

This is the best article over critical illness. Sir, can you please put some detail on CSR of different companies in this case

Gyan-Sadly CSR for Critical Illness policies not available.

Hi Basavraj,

I am a 35 year old Software engineer working in a MNC. My Company has provided a Group Mediclaim insurance of 8 lakh and Group Accidental assurance of 50 Lakh. I do have a basic term plan also. I have one confusion now. Should i buy critical illness plan for me and my wife now? Or Should i buya personal mediclaim policy for my family first and then look for critical illness plans. Do you advice personal mediclaim policy, even if employer provides it?

Raj-First buy your own family floater health insurance and then look for CI.

Thank you very much, I will definitely look for family floater health insurance first.

What would you recommend – A topup Family floater or regular Family floater Plan? Is it good idea to convert the topup into regular later on?

Raj-A small amount of base plan is must. Hence, opt for regular family floater.

Hello sr

Sr if I have some critical Illness and after that I have bought a term insurance with critical illness rider policy,.So sr after how many days it will cover to me.

Vikas-Please check the policy document.

Good morning sir, can you please tell me

1) What are the added advantage of critical illness cover versus health insurance cover.

2) Is there a difference in the premium amounts.

3) Kindly suggest sir.

Shradha-It is hard to explain everything in a comment section. But refer above post properly. You notice that health insurance covers all diseases and there is no special benefits apart from hospitalization. However, in case of critical illness, it is CI specific.

Very good post! I currently have a term insurance from HDFC (50 Lacs + regular income) from past 3 years (paying 15,800/year) Very good post! I currently have a term insurance from HDFC (50 Lacs + regular income) from past 3 years. When I bought this policy I had no idea about riders and now I am regretting that I did not choose a Critical Illness Rider. My current policy is expiring by this month end and I was thinking of letting it lapse and buy a new Term insurance + Critical illness. However, right now for my age (male, 34, smoker- 1Cr+25L CI benefit), the premium is coming to almost 36,000/year. I am not sure what to do.

1) Should I let my current policy let go and buy a new one with CI rider? I am currently paying 15800/year.

2) Should I buy a separate CI policy and continue my existing 50L term policy?

3) Should I just drop the idea of buying a CI policy considering it’s complex nature and thousands of clause from there insurance companies?

I am a noob in field of insurance and your inputs will be really helpful.ay. When I bought this policy I had no idea about riders and now I am regretting that I did not choose a Critical Illness Rider. My current policy is expiring by this month end and I was thinking of letting it lapse and buy a new Term insurance + Critical illness. However, right now for my age (male, 34, smoker- 1Cr+25L CI benefit), the premium is coming to almost 36,000/year. I am not sure what to do.

1) Should I let my current policy let go and buy a new one with CI rider? I am currently paying 15800/year.

2) Should I buy a separate CI policy and continue my existing 50L term policy?

3) Should I just drop the idea of buying a CI policy considering it’s complex nature and thousands of clause from there insurance companies?

I am a noob in the field of insurance and your inputs will be really helpful.

Also what are your views on Policy term? I mean till what age we need term insurance? Considering we’ll not be working post 60 Years?

Binod-1) Let it continue.

2) If you have family history of such CI, then go ahead. I personally not fond of CI.

3) I already replied.

Thanks for responding Basavaraj! Really appreciate it. Could you please edit my comment above as I mistakenly copied and pasted the same content twice while posting it the other day. It’s kind of looks odd! 🙂

Binod-It’s alright 🙂

Dear Sir,

Can you suggest any Critical Illness plan which covers Ulcerative Colities and Colon Polyps Cancer?

Request your help please……

Patel-Hard to point any particular.

Dear Basuji,

Could you please review the icici pru “smart health cover” plan ?

The premium for women seems to much lower than for the men. Can you discuss the pros and cons for the plan ? Shall I go for this plan for my wife (age 33).

Regards

Amar

Amar-No harm, you can go ahead.

Dear Sir,

What is your take on ICICI Prudential Critical Illness Plan? Is it recommended?

Regards,

Neo

Neo-Hard to comment and suggest you BLINDLY without knowing your need.

dear Basu ji

I was having Critical Illness plan from Bharti Axa. When I started my critical illness plan two year back my premium was 5200 with tax and everything. Then I paid my second premium 5200 with tax and everything. And now on 3rd premium they revised it by 50 increase with tax and everything. The premum becomoes 8183. Then I have a talk with their representative. He explained me that my age band has changed therefore they are re doing the premium amount. Then i asked him If I after 5 years I cross my age band again my premum will be increased he says yes..

then i asked him wheter IRDA approved this thing his answer was not strainght. Then i informed him i will not renew this policy.

what is your say.

Jnbarc-Usually it happens so. If you are not sure, then cross their plan feature or premium. It changes based on age band.

We are a family of 3, myself and my husband and 6 yr old child. We have taken the Apollo munich optima restore, which is a family floater with multiplier benefit. Basic sum insured is 10Lakhs. Which I believe also includes critical illness. I on the other hand have a family history of cancer and would like to go for a stand alone cancer policy for myself. Would you be able to advise some good options for the same.

Bhawna-Check with LIC’s Cancer Care.

Is it a good strategy to buy two critical insurance policy from different vendor.

Like one from Max Bupa and one from Religare.,

Since Religare offer Nil survival period and Max Bupa has 30 days of survival period.,

Suppose a person require 50 lacks of critical insurance cover – would it make sense to break 50 between Max Bupa and Religare. Do you see any impact for later during claim process if person survive more than 30 days – does applicatant allow to claim SA from both companies.

Could you clarify.

Thanks

Prashant

Prashant-The more diversification in insurance means more work for you to get the claim and run behind insurance companies.

Yes bit of more work for claim processing. but is it allow to claim from two insurance product ?.or either of one can be claim ?.

Prashant-You can claim at both sides.

i have 3Lakhs base insurance policy with 7 Lakhs super top up policy duducted 3Lakhs . does i required any critical illness policy?

Subrata-If there is a family hisotry or critical illness, then better to go for.

Hi Basu

I am looking for disability insurance as I am freelancer professional. Is critical illness and disability are similar in coverage ? If not then what are best disability insurances in India?? What should be optimum coverage ?

Regards

Sandeep-Both are different. You have to buy accidental insurance. Refer my post “Best Accidental Insurance Policy in India-How to choose them?“.

My sense is the simplest is the best. critical illness plans are complicated and expensive. Despite paying huge premium there is no guarantee of getting the money. The medical terms and conditions are beyond our understanding. It is better to go for term plan with large cover. the premium is low. besides, some insurers pay a part of sum insured on terminal illness. I do not dispute but in case of critical illness like cancer the survival rate is not much.

Sanjay-I value your views.

hi mr basu

i here to enquire about any critical care policy in india for pre existing dieses

cardio

Ravi-Har to say. But based on above post approach the companies of your choice.

sir i want purches CRITICAL ILLNASS POLICY .. BUT I AM TOBACO USEING ANT HEALTH INSURANCE COMPANY GIVE ME CRITICAL ILLNESS PLAN ???

Shantanu-It depends the insurance company. Better you disclose the details and let them decide.

Your understanding of survival period is wrong. It refers to the period you need to survive after diagnosis of the illness and not the period between buying the policy and detection of illness.

Amit-May I know where I mentioned that survival period is between buying the policy to the detection of illness?

I’ve read the terms and conditions of the policies but Illness including cancer , heart etc are excluded with a condition in all , how in the world one can know which type of cancer can happen or which grade of heart attack can happen to someone ? can you find out and tell us all which is best as per terms and conditions of exemption of illness disease.

Rahul-It is hard to define medical terms for an individual.

I know that’s why I asked u to do as courtesy to me and fellow readers , there are many terms and conditions like cancer not covered it…blah blah blah 4 cm, 2 cm, etc. etc. which I don’t understand It’s in medical terms not in general like lung caner, blood cancer covered etc . so I’m requesting you to find out which one is best for us as we’re planning to cover to uncertainty and any disease can happen so i would like to buy the policy which covers most of diseases and has less terms and conditions of disease.

Rahul-It is hard to do for me as digging each of their definitions (if not clear then contacting them separately) and explaining the same in detail.

ok thanks buddy but if you don’t mind can u tell which one have u taken for yourself as I’m damn sure you’ve done all the maths before buying , so if u don’t mind can u share the details which one you’d bought.

Rahul-For your information, I am not having any critical illness cover as I know very well that getting claim is tough and understanding the clauses even to fight for the claim is the biggest risk. Instead, I created the corpus to compensate any such eventuality on my own.

Dear Sir,

what is meant by ‘corpus to compensate’. Will you please give the details so that I too can follow that?.

Thanks in advance

Raj-Compensate the cost of illness.

Hi Sir,

I am planing to take critical illness plan please suggest which plan is best and which company

Anuraj-Refer the above post.

Sir

Very enlightening post.

Would like to ask if exclusions are same in these policies. Do all policies cover pre existing diseases/ conditions after 48 months . Or do some policies completely exclude pre existing conditions.

Secondly congenital is one area I have less under standing.

Third I was going through Apollo Munich optimal vital, but found something confusing. Kindly read the last paragraph regarding waiting period.

EXCLUSIONS

TERMS OF

RENEWAL

OTHER

BENEFITS

HOW TO AVAIL

BENEFIT UNDER

THIS POLICY

• All illnesses & treatments within the first 90 days of the cover.

• Any pre existing condition will be covered after a waiting period of 48 months.

• Any critical illness in presence of HIV infection and / or any AIDS.

• Congenital internal and external diseases, defects or anomalies.

• Abuse of intoxicant or hallucinogenic substances like intoxicating drugs and alcohol.

• War or an act of war or due to a nuclear, chemical or biological weapon and radiation of

any kind.

• Any treatment arising from pregnancy (including voluntary termination), miscarriage,

maternity or birth (including caesarean section).

Please refer to the Policy Wording for the complete list of exclusions.

• Lifelong Renewal – We offer life-long renewal unless the insured person or any one

acting on behalf of an insured person has acted in an improper, dishonest or fraudulent

manner or any misrepresentation under or in relation to this policy or the policy poses a

moral hazard.

• Grace Period – Grace period of 30 days for renewing the policy is provided under this

policy.

• Maximum Age – There is no maximum cover ceasing age in this policy.

• “”””””””Waiting Period – The waiting periods mentioned in the policy wording will get reduced

by 1 year on every continuous renewal of your Optima Vital policy. “””””””

Saurabh-All policies cover existing diseases after 48 months usually. But I suggest you to check the exclusion clause properly. What is your doubt in Apollo exclusion list?

Waiting periods in the policy will get reduced by 1 year on every continuous renewal.

This means the 48 month waiting period?

Saurabh-Now while taking policy it is 48 months, after a year it get reduced to 36 months and so on. What is confusing here?

DEAR BASU, IS THERE ANY PRE MEDICAL CHECK UP AND AGE ELIGIBILITY CRITERIA FOR CRITICAL ILLNESS POLICIES? PLEASE CLARIFY.

Giriprasad-Yes, based on your age each insurer follow some rules for medical check up and also there is a restriction of the maximum age of entry.

Thank u dear basu for info

Is portability allowed. I have family floater with IFFCO TOKIO with 10 lakhs critical illness cover and 10 lakhs for normal medical.

So now want to top up to 50 lakhs for critical illnesses. Is this possible

John-Yes, exactly like health insurance policies, you too can use portability option for Critical Illness policies.

i have 3 company critical illness plan

1.Max bupa 10lakhs

2.Apolla munich 5 lakhs

3.Max bupa 15 lakhs

Any claim heart diereses 5 lakhs expenses i am claim 3 company payout 5 lakhs total amount 15 lakhs correct or not ?

Feroz-Yes, as the critical illness is fixed benefit product.

Hello Sir, Could you throw some light on the below plan from ICICI – Heart and Cancer coverage… is it worth buying..

https://www.iciciprulife.com/health-insurance-plans/icici-pru-heart-cancer-health-insurance-calculator.html?UID=2399

Also compare the available health insurance plans in the market..

Suresh-These plans are illness specific. Hence, better to avoid and buy a comprehensive plan.

Dear Sir,

An excellent article. Sir, what is the basic difference in Critical Illness and Individual Comprohensive Mediclaim policy? i feel if you have the latter , it will cover critical illnesses too. secondly, there is no question of insurance company doctor certifying critical illnesses in mediclaim, as Hospitalization is the only criteria.

“Buy enough health insurance. If you still feel shortage, then go for super top up plans. Create an emergency fund especially for such diseases”.

Sir, this is the take home message and golden words of this article. You have rightly pointed out. Hatsoff to you.

regards

RAJESH PAI

Rajesh-Yes, your understanding is correct regarding critical illness and mediclaim policy. Thanks for your kind words.