HDFC Life Sanchay claims 8% to 9% Guaranteed Addition and also the guaranteed maturity benefit of 220% to 325% of the Sum Assured depending upon the policy term. One of my blog readers noticed this and shared with me for review. Let us see what is the truth.

Note:- HDFC Life recently started a new version of this plan in the name of HDFC Life Sanchay Plus. I have written a detailed post on this. You can refer a below link for the same.

HDFC Life Sanchay Plus – A GUARANTEED TRAP!!

It is one of the traditional plans which is not related to stock market. In such a situation how can a product generate 8% to 9% GUARANTEED ADDITION?

Let us see the key plan features. They are listed as below.

- Guaranteed benefits payable on maturity provided all due premiums have been paid.

- Guaranteed benefits will vary by policy term in a range of 220% to 325% of the Sum Assured on Maturity.

- Premium payment for a limited period of 5, 8 and 10 years.

- Flexibility to choose policy terms ranging from 15 years to 25 years.

Eligibility to buy HDFC Life Sanchay

Below are the eligibility conditions to buy this product.

HDFC Life Sanchay Benefits

# Guaranteed Additions (GA)

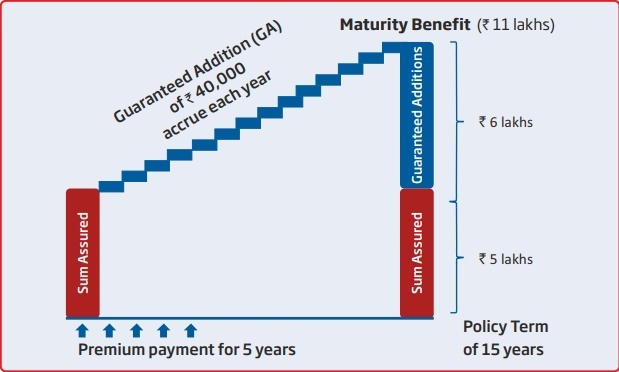

The plan offers guaranteed additions as a percentage of Sum Assured on Maturity accrued at a simple rate for each completed policy year, throughout the policy term.

These Guaranteed Additions are payable at Maturity or Death whichever is earlier, subject to all due premiums being paid. In case of surrender, the surrender value of Guaranteed Additions will be payable.

Policy Term-15 Yrs to 19 Yrs-GA 8%.

Policy Term-20 Yrs to 25 Yrs-GA-9%.

# Maturity Benefit

If policyholder survives till the end of the policy period, then he will receive the below benefits.

Sum Assured on Maturity (which is equal to Basic Sum Assured)+ Accrued Guaranteed Additions. This according to HDFC Life varies from 220% for 15 Years policy to 325% for 25 years policies of Sum Assured.

# Death Benefit

If the death of the policyholder occurs during the policy period, then his nominee will receive below benefits.

Sum Assured on death is higher of the below.

a) Sum Assured on Maturity

b) an absolute amount assured to be paid on death, which in this case is equal to the Sum Assured on Maturity

c) 105% of premiums paid

d) 10 times Annualised Premium

HDFC Life Sanchay – Reality check of 8% to 9% Guaranteed Addition

As I said earlier, two things are highlighted by HDFC Life to sell this product. The first one is 8% to 9% Guaranteed Addition and second is Guaranteed maturity benefit of 220% to 325% of the Sum Assured depending upon the policy term.

Let us check the reality now. For this purpose, I took the same example of what they showed in their product brochure.

Ramesh, a 35-year-old individual, invests Rs. 1,14,877 annually for 5 years in the HDFC Life Sanchay. He chooses a policy term of 15 years. His Sum Assured on Maturity in the plan is Rs.5,00,000. He will receive a guaranteed maturity benefit of Rs.11,00,000 at the end of the policy term. Below table illustrates his benefits in the plan.

Now as per HDFC Life ‘s claim, Ramesh will definitely receive 8% GA per year without fail till maturity. Also, the maturity benefit is obviously 220% of Sum Assured.

So is it a GREAT product? Let us cross-check the reality by using the IRR formula and find out the actual returns from this plan.

You noticed that the actual returns are just 5.11% but not the 8% to 9%. Then why returns showing less?

# The premium in this plan is hefty but sum assured is less. Hence, the returns are less. Because your returns are linked to the sum assured you opted.

# The GA what HDFC Life will declare yearly will not earn any interest further. They just keep that money with them and will pay you back either at maturity or death.

# Even though 8% or 9% GA and 220% to 325% of Sum Assured at maturity will look fancy, but the reality is that this plan not gives you more than 6% returns.

Conclusion:–

The 8% and 9% GUARANTEED ADDITION may look you fancy to jump into investment. But when you check the return on investment, then you will see that returns are not more than 6%.

Also, one more fancy thing what HDFC Life did is that to claim 220% to 325% of Sum Assured as a maturity benefit. This at first glance looks so attractive. But the reality is something different.

Refer our other posts related to HDFC Life-

- HDFC Life Pension Guaranteed Plan – Should you invest?

- HDFC Life Click 2 Protect 3D Plus Review and Benefits

- ULIPs Vs Mutual Funds – How HDFC Life is misguiding !

good work…

HDFC Sanchay plus Guarantee Return for the 5/15 policy with premium of 10L per year for 5 yrs and at the maturity on 15th yr, maturity amount is 1,12,15,155 (1.12cr) with IRR of 6.92% is this any good ? Please help me with your views as I felt this is just little above FD (1% more) and USP is that it’s tax free blah blah blah. Please help me understand this better. Thanks

Dear Kapil,

I have already replied to your email.

Dear sir, I’ve paid a total of 65K in HDFC Life Sanchay for past 5 months, and if I discontinue, fund will be lapsed and will lose my money. I was misguided by an agent to take this policy along with HDFC Click to wealth.

He claimed maturity amt will be 60 to 64 lacs. Currently Im paying combined premium of 25k per month

Policy term 15 yrs and paying term is 5 yrs.

Should I let go the 65 K and start an SIP? Investment is my priority. What should I do?

Dear Athul,

If you are OK with forgetting what you paid, then go ahead (I Know it is painful to say so).

Which is the best policy for investment with good returns? Can you please suggest

Dear Shraddha,

How can I say BLINDLY without knowing your actual requirements?

Dear sir I joined this plan in 2014. Should I leave it asap I paid 1 lakh premium for 5 years

Dear Aj,

Better to surrender.

HI

I have received the same plan offer from the Bharti AXA Life Elite Advantage.

Representative is offering to me pay annually 50,000 Rs and i will receive after 12th year 55000 upto 5 years and 13,00,000 after 12+5 years. OR i can receive the lumsum amount after 12th year approx 13,21,000Rs.

Please help me to understand is it good policy plan so i can go with it.

Dear Avnish,

if you are fine with your long term investment returns of around 5% to 6%, then go ahead. Otherwise, NO.

Hi,

The illustration i received for 12 year term has 6 year premium paying term with SA of Rs. 452,243. At the end of 12 year one gets Guarantted 196% of SA (i.e. Rs. 886,396) + Loyalty Addition of Rs. 434,153 (Rs 36,179 every year till policy term). Which makes total GA of Rs. 13,20,544 (i.e. IRR of 8.5%). Is there something which i am missing on calculating the returns ?

Dear Raj,

Do your own research. If this product generates you guaranteed 8.5% in the current scenario, then this is the 8th wonder of the world.

I have followed your formula in excel but i am not getting, i believe i am missing something

kindly let me know how you got 5.7 % investment.

Dear Avnish,

Refer above post again.

Hello

I received an benefit illustration for jeevan sanchay with following details. You pay amount each year till year 6 . After 12 years you get amount 14.68 return. I checked online the irr is coming 9.39, which is pretty good and probably highest for a guaranteed plan. Please confirm or point out anything that I may have missed.

Just to clarify, the amount 14x you get after total 12 years from your initial investment.

Dear Chinmay,

God blessed to that guy who showed such exaggerated returns.

Dear Chinmay,

If this product giving you 9.39% IRR, then please go ahead. WONDERFUL PRODUCT ON THIS EARTH. But whatever I shared above is as per their claim. Rest left with you as it is your money.

Sir maine hdfclife sanchay plan le liya hain sum assured 108961 aur quarterly 7838 premium hain 5 yrs premium paying term hain aur 10 yrs ka maturity hain to kitna amount milega maturity ke bad unke hisabse to 8% milega

Dear Kishor,

Refer above post to know how much you can expect. Never trust the SELLERS. Do your own homework.

Thank you for your help

Hdfc life representative saying if you invest 1lakh annually for 10 years then along with all the benefits of sanchay they will give medical insurance of 5 lakh for 5 members for 36 years. 36 years is the policy tenure. I asked why they giving health plan, they saying this is direct plan so commission is being passed to hdfc ergo for health insurance. Should we rely on it. They saying if you don’t get all these on bond then you can cancel the policy.

Dear Naveen,

Let him give all these in writing. Because as per me, it is against IRDA and can be punishable.

Thanks Basasvaraju, Please let me know how you have calculated the ROI.

Dear Manish,

I explained the same in the above post.

Also they have given me a commission benefit of 20% i.e. 10k return on every premium paid of 50k till 5 years. Kindly suggest

Dear Rahul,

A simple question to you, if they are so confident about their product, then why they are luring you by sharing the commission, which is against the IRDA rule?

Dear Sir,

I recently took this policy with the premium of 50K p.a. 5 years premium paying term and 15years policy term. Sum assured as per the policy is 214950/- plus GA of 8% pa on sum assured at maturity. They also included a medical insurance of 2.5 Lac in the first year of the policy and if not claimed in the first year than the medical insurance would be 5 Lac( for four members including me) till the tenure of the policy.

Could you suggest if it’s a good deal or shall I surrender the policy as I still have 30 days to surrender without any penalty or charges.

Dear Rahul,

MEDICAL INSURANCE with this policy? Someone I think in a big way cheated you. Please cross-check the facts properly.

Hi Basu

1. GST is 4.5% for 1st year and 2.25% for the subsequent years. You have taken 4.5% for 5 years in the table.

2. Also the premium payable is for 5 years. You have shown 16 years in the IRR table

Dear Ajay,

1) Yes, GST is as you said. But I have considered the premium exclusive of GST (as per HDFC website).

2) Yes, you will receive the maturity benefit once you complete the 15th year and that is on 16th year beginning. Hence, the calculation is correct.

It is really a bad plan without any benefit. The sum assured is less than what we pay as premium and percentage addition will be sure less than 8 %. So it is just art of fooling. Do you advice , it wise to surrender policy and get the refund even if we are in loss? There is no benefit of keeping hard earned money to company where they will not give any benefit.

Dear Entaz,

As it is a typical endowment plan, coming out is also not so easy 🙂

Bakwas plan – worst service

Aap verify karwa do or payment kar do fir uskey baad yeh log bhul jayengay ki aapko koi paper ya service bhi deni hai. Inka email ka bhi answer nahi aayga or call krtey raho aapko galat banatey rahengay yeh log

Dear Suraj,

Thanks for sharing your experience.

Dear Sir,

HDFC Life Sanchay plus- long term income says on paying 1 lac per annum till 10 policy year they will pay Guaranteed 1,08,150 every year for 25 years after policy term of 11 year.

You pay 10 lacs and they paying around 37 lac ( from year 12 to 24 every year 1,08,150 and in the 25th year 1138150.

I appreciate if you can guide whats is catch in it? As it seems good plan, as it all Guaranteed.

Dear Kapil,

Wait for my next post 🙂

So over 10 yrs one will pay 10 lacs as full premium. Every year one can earn 80 thousands as interest over 10 lacs@8%.Here after 11 years one will earn little more than 1 lacs every year which can be just interest payout every year on 10 lacs. Customer will have no freedom to withdraw his own money(10 lacs at one time). So only only benefit is tax saving and big financial loss.

Dear Entaz,

Along with that many of those who defend are completely forgetting how this product protects us from INFLATION.

In depth article, you had teared HDFC Life Sanchay.

Great eye opener!!!

Dear Tobias,

Pleasure 🙂

Please let me know about sanchay plus and not sanchay.. if you can share the link where you have done the analysis. Thank you for doing a great job.. God bless

Dear Ravi,

Let me write a post on this.

Real eye opener. Request your analysis of HDFCLIFE CLICK TO WEALTH ULIP . I am keenly awaiting your views .

Dear Karnik,

Sure.

informative and helpful

How was the premium of 114,877 calculated? What is the GST rate assumed here?

Dear Haldar,

It is based on their own product brochure.

your research is commendable. Kindly help me HDFC commit ed 6.55 IRR for Sanchay Plus . Please suggest

Dear Aparna,

COMMITTED in the sense anything in writing? If so, then let me know. If they just claiming it, then DON’T BUY THEIR CLAIM.

Thank you Sir ….you have calculated 5.1 as IRR for sanchay can I get what would be IRR for Sanchay Plus from HDFC Life . Is this better option than FD of 8.5 % from IndusInd bank

Dear Aparna,

It may be around same 5% but not more than 7%.

Sir . One of representative from hdfc life says if i invest 1 lakh each for 5 years. I will get back 17 lakh after 15 years under sanchay plan. 11 lakh maturity of policy + 6 lakh as interrst. He says it will be written in policy. Kindly tell is it true

Dear Upendra,

These are selling tactics and let him show one policy bond issued by HDFC where it is mentioned. Above that, first calculate the IRR.

Hello from Scotland. I have a young family and was looking at some safe investment options with assured returns and for a call from hdfc about this. I was quite sold until I came across your blog and the simple maths of it. Disappointed that I didn’t pick this up. Relieved that you did. Thank you.

I may be exploring your blog further now to find something that may meet my requirements..

Dear Arjun,

Great to know this 🙂

I am 51 now and wife 45. Want to get 6-7 lakh per year from my age 60 till life and after me my wife should get the same till her life and the deposit amount should be returned to nominee with some interest. I prefer to avoid IT after age of 60

Dear Sanjib,

Sadly your wish list can’t be feasible 🙂

Hello Basavaraj,

What is a decent investment now? I want to invest 1 lakh yearly…

Dear VB,

It depends on many criteria. Merely by few lines of your sharing, I can’t suggest a product BLINDLY.

Sir, i want to invest 50k yearly in HDFC Life Sanchay Plus for investment purpose. Sir please guide

Deepak,

Calculate the returns based on the past performance of the product. If you feel 4% to 6% is the BEST return for your long term investment, then GO AHEAD!!

Dear Basavaraj, could you please share your review for “HDFC Life Sanchay Plus” which was launched 15days back?

Dear Kavi,

I strictly say NEVER COMBINE BOTH INVESTMENT AND INSURANCE.

why sir?

Deepak,

Calculate the returns based on the past performance of the product. If you feel 4% to 6% is the BEST return for your long term investment, then GO AHEAD!!

Dear sir I purchase HDFC life sanchay policy in 2017 .as a yearly mode for 15 years , I pay 48058 Rs. Annual . So after 15 years how much I get total amount please rply .

Thank you

Dear Mohammad,

Please refer above post once again.

Dear sir I purchase HDFC life sanchay policy in 2017 .as a yearly mode for 15 years , I pay 48058 Rs. Annual . So after 15 years how much I get total amount please rply .

Thank you

Dear Mohammad,

Refer the above post properly.

Thanks a lot sir for clarifying on the returns at maturity. HDFC folks blalanty lie about the return stating that maturity amount is 220% of SA + Guaranteed Additions (GA) and hence their CAGR is in excess of 9%.

After reading your blog and then going back to the plan brochure, I realized that the fact is maturity amount is only 220% of SA (inclusive of GA).

Dear Mukesh,

Pleasure 🙂

thanks for the Blog. I was informed that HDFC life Sanchay gives a return of 8.75 % which is more than PPF.. after reading this, when i calculated the maturity amount vs investment in HDFC Life Sanchay – it comes out to be @ 5.7 % compounded interest rate.

1 L invested in HDFC life Sanchat for 5 years would fetch @ 10-10.5 L at maturity in 15 years.

Same amount in PPF would be 14 L+.

Please do not believe the sales executives and do the calculations yourself before investing.

Dear AB,

Pleasure 🙂

Dear sir,

Can you please suggest me which investment is best either Lic endowment policy or SIP mutual fund. I am 52 years old & am planning to invest RS 5000/ pm. So kindly advise me which investment is best sir.

Thank you

Ramamurthy

Ramamurthy-Hard to say anything BLINDLY without knowing much of your financial details.

Hi Basu sir, thanks a lot great detailed analysis and understandable to common people like us thanks a lot

Sat-Pleasure.

Thank you Basu very detailed analysis for the product

Rahul-Pleasure 🙂

Hi

Can you please tell the value of Guess in the IRR formula you have used.I left the guess blank and am getting 6.49 %

Gautham-Why to put the value of guess? Without that, you can calculate.

HOW U CALCULATE IRR. SHARE THE FORMULA

Dear Praveen,

You can calculate the same using excel.

Great article on Sanchay ! Thx Basu . You are doing such a great service to all of us

Rajini-Pleasure 🙂

Thanks for the great post as i was about to buy this policy..how can i contact you to get your proper advise/service in helping me to invest right.

Dear Sayeed,

You can mail me at [email protected]