Recently HDFC Life launched one more Non-Linked Savings Insurance Plan HDFC Life Sanchay Plus. The eye-catching part of this product is GUARANTEED.

Long back I wrote a post about one of the HDFC Life’s products “HDFC Life Sanchay – Reality check of 8% to 9% Guaranteed Addition“. After visiting this particular post, many people requested me on what will be my review about HDFC Life Sanchay Plus. Hence, thought to write a post on this.

This is the typical Endowment Plan with different features added to it. The biggest tagline that attracts many of us is GUARANTEED.

HDFC Life Sanchay Plus – Eligibility

Let me share the HDFC Life Sanchay Plus eligibility criteria.

Benefit options in HDFC Life Sanchay Plus

This plan offers four types of Benefit Options. They are as below.

I am taking the example of a person whose age is 30 years and the yearly premium of Rs.30,000 (which is minimum).

# HDFC Life Sanchay Plus – Guaranteed Maturity Benefit and Returns

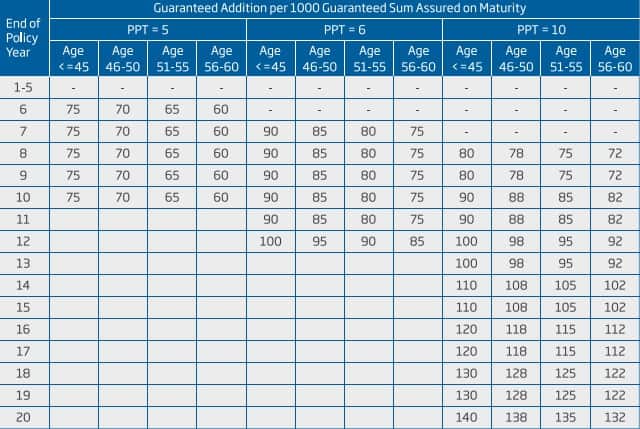

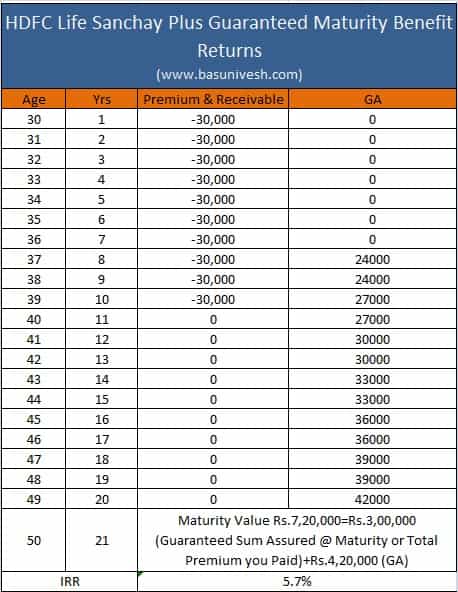

In this plan, the policy term is 20 years and the premium paying term is 10 years (this I have taken for my calculation purpose). At maturity, you will receive the Guaranteed Sum Assured on Maturity+Guaranteed Addition. Here, the guaranteed addition available is higher for younger age group and lower for older. The GA ranges from Rs.60 at the minimum to the maximum of Rs.140. Hence, to make sure how much the maximum benefits one can receive under this plan, I will take the 30 years young proposer example and the term also the long term. This makes us to consider the Rs.140 GA for our calculation.

One more catch here is that there is no GA for a certain period. See the below chart for the same.

After considering this maximum benefit, the results are as below.

You noticed that returns are around 5.7%. Hence, not a big game changer for your investment of around 20 years. Do remember that I have excluded the GST which you have to pay on the premium. If we consider this, then the returns will be less than 5.7%.

# HDFC Life Sanchay Plus – Guaranteed Income Benefit and Returns

Under this plan, the policy term is 11 years and the premium paying term is 10 years. From the 12th year onwards you will receive the GUARANTEED income for the next 10 years. As per the below illustration, one will receive the yearly benefit of Rs.61,800 for the 10 years.

Looks attractive right? You are paying Rs.30,000 for 10 years and from next year onwards yearly Rs.61,800 for the next 10 years. Each of your yearly premium paid will be doubled. Wait….Let us calculate the IRR of the investment. In principle, it is nothing but your each year money will be doubled for every 10 years. Hence, in plain, you can assume that the return on investment will be just 6%.

Look at the below calculation. I have not changed any numbers. Whatever it is shown in the benefit illustration, I have included for IRR calculation. The returns are just around 6%.

Do remember that I have excluded the GST which you have to pay on the premium. If we consider this, then the returns will be less than 6%.

# HDFC Life Sanchay Plus – Long Term Income Benefit and Returns

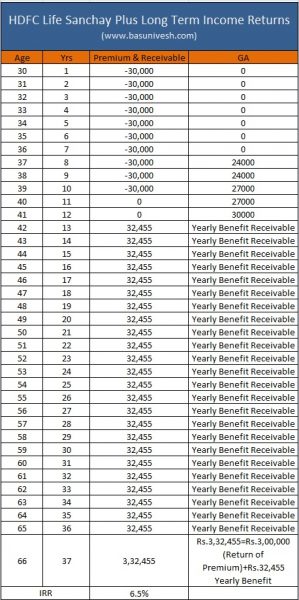

Under this plan, the policy term is 11 years and the premium paying term is 10 years. From the 12th year onwards you will receive the GUARANTEED income up to 36 years. As per the below illustration, one will receive the yearly benefit of Rs.32,455 for the 36 years. On 36th year, you will also receive the premium you paid along with 36th-year benefit.

Again an eye-catching of 36 years GUARANTEED income. But let us look into the IRR of this example.

You notice that IRR is again at 6.5%. No big differentiator. Do remember that I have excluded the GST which you have to pay on the premium. If we consider this, then the returns will be less than 6%.

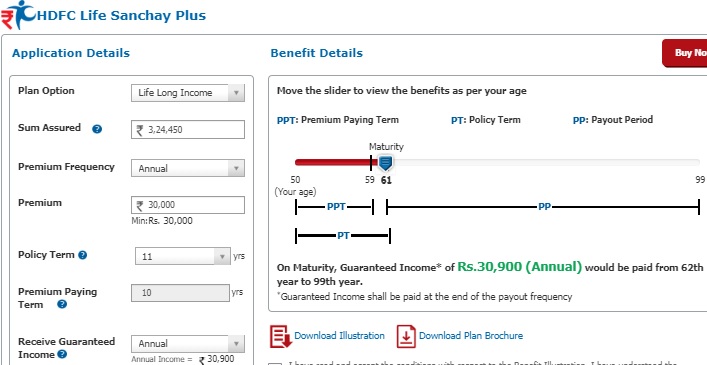

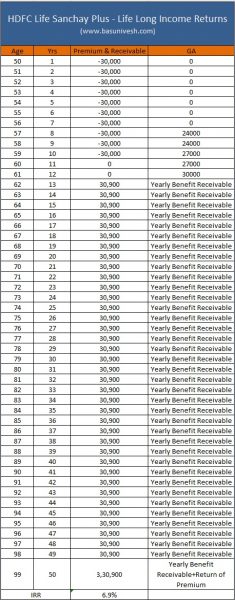

# HDFC Life Sanchay Plus – Life-Long Income Benefit and Returns

Here, one more surprise to us. This plan is only for those whose age is 50 years or above than that. Hence, it is nothing NEW but a LURING way of Life Long GUARANTEED income.

In this plan, you will pay the premium for 10 years. From 12th year to 99 years of your age, you will receive the Guaranteed Benefit.

Life Long GUARANTEED is an eye-catching term. But the reality is again something different when we check the IRR.

Image may look small. However, the end result is not more than 6.9%. When I wrote at first, I have not considered the return of premium which life assured will receive at 99 years of age. Few readers pointed out this error. But want to say one thing, if one assumes the 6% simple inflation and his age is 50 years, the amount of Rs.3,30,900 he receives at his 99 years of age in today’s value is Rs.19,041. It means almost half of what he is able to pay now. Do remember that I have considered 6% inflation. However, in reality, inflation is beyond 6%.

One more BIGGEST point which the DEFENDERS of this plan forgot that we have to pay GST on the premium (which I have excluded for illustration purpose). If we consider the GST, then the returns will be again at around 6%.

Do remember that I have excluded the GST which you have to pay on the premium. If we consider this, then the returns will be less than 6%.

HDFC Life Sanchay Plus – A Guaranteed TRAP!!

Yes, it is a TRAP in the name of GUARANTEED LONG TERM INCOME TRAP. You noticed that in all benefit options returns will not be more than 6%. Hence, should you buy it? My take

# This product is a typical endowment plan sold as if GUARANTEED income or GUARANTEED Addition. However, when you look at the returns, its just around 6%. Do remember that we have to pay GST on the premium also. Hence, if we consider this expense, then the returns from all the above options will be around 5%.

# This product even though claim to be LIFE LONG GUARANTEED income for you. But fail to give the solution to inflation. You will receive the same income throughout your life (In Life Long Option). How this is going to benefit ONLY GOD KNOWS.

# Wisely they increased the minimum age for Life Long Income Option to 50 years and make sure that their liability of paying you the GUARANTEED income should be to the maximum of 49 years (90 Yrs-50 Yrs). Hence, it is completely an eyewash to present you in a different AVATAR of the benefit option LONG TERM INCOME.

# Many of your Bank RMs may be behind you to buy this product. However, look at the pathetic returns of around 6%, which even can’t beat the inflation. Hence, it is better to say NO.

# One must not buy just because there is a tagline GUARANTEED. We have to think about how much is GUARANTEED and what will be the final returns.

# In the Guaranteed Maturity Benefit, their Guaranteed Addition looks attractive. However, the GA will not be added to you immediately you start the policy. They will add it after a certain period. Hence, this again lowers the returns to around 5.7% (in the above example).

# It is better to buy a term life insurance and by investing monthly in PPF kind of product, you have the possibility to earn more than this plan.

FINAL THOUGHT…STAY AWAY FROM SUCH PRODUCTS!!

Well said. Also one more thing if we take inflation into account then the client is not going to get any.

Dear Arun,

Thanks for airing your views.

Sir this year on 14 mar i have purchased this policy 100000 p.a PPT 8 Years and after reading it i am so much confused what about to do now?

Dear Avijit,

If you are fine with above-mentioned returns from this policy, then can continue. Else, you have to think twice.

in how many years, policy can surrendered? or can policy discontinued after a year

Dear Snehanshu,

After 3 years in case of traditional policies.

Many thanks for the detailed explanation Sir.

I already paid one year premium for HDFC sanchay plus plan which is 71,000 last year and now I have to pay the second year premium. Now, after reading all these I am very much confused whether to continue the plan or just let go off the premium paid. Request you please advice me whether to continue or let go of 71k?

Dear Srikanth,

It is painful to say that you forgo the first-year premium. However, it seems to be sensible.

Hi Sir,

Thank you for writing about this and awaring us.

But, If someone like me has already purchased this then what we could do to have the least loss, Should we surrender it or what we should do,

Please explain in detail

Thanks

Dear Chandan,

It is painful to suggest. But better to convert into paid up.

I red this article completely. I am happy that we also did this much deeper analysis.

1) we also calculated around 6-6.5% IRR only.

2) we considered FD rates are similar or slightly lower at that point of time.

3) we considered it as a fixed income allocation

4) we considered some amount coming till the age of 99 including for spouse is big saviour in any adverse financial situations.

5) we also considered tax exemption is a benefit relative to any FD.

6) we also thought after 10-20 years possibility of intrest rates going down sub 7% is high than going beyond 7%.

While I appreciate the author’s view point of enlightening the community, this all depends upon the contextual background and relativity. If he says for all the money I have yes, he is right. But when I do 2% of my money for longtime safety I am right.

Coming to the marketing gimmick… yes. Marketing means that only without cheating. And I also feel the same with HDFC balance advantage fund. When you have SWP with every product, now a days monthly fixed income is just a marketing gimmick and no relevance.

Dear Raj,

2% of your net worth or cash flow?

Hi Basu,

I regret purchasing the ‘HDFC LIFE SANCHAY PLUS PLAN’. I got lured by the banker to purchase the long term income plan. I have to pay a premium of 1lpa anually for six years(3 premiums paid until now) after which from 8th year I shall be paid 40k annually until the 37th year when i also get back the principal amount.

I understand the damage is done thus request you to please guide what best can be done after it matures.

There is a clause in the policy about maturity which goes as :

(On the maturity date, you shall have an option to receive the Guaranteed Sum Assured on Maturity(4.56lpa printed on my policy), which under this

option, shall be the present value of future payouts, discounted at a rate of 9%p.a. This interest rate is not guaranteed.

However, any change in the interest rate will be subject to prior approval of the Authority and will be applicable only to

the policies sold after the date of change.

At any point of time during the Payout Period, you shall have an option to receive the future income as a lump sum,

which shall be the present value of future payouts, discounted at a rate which is computed using the prevailing interest rates.)

1) Could you please help me in understanding this clause.

2) Is receiving the amount in lumpsum or continuing it more practical?

Highly appreciate if you could provide some guidance

Dear Suyash,

I am unsure of when you purchased the policy. Hence, hard for me to guide anything. Regarding the clause, it is the current value discounted at 9% and will be payable to you.

Thanks, after reading your post had just checked today for hdfc sanchay plus long term income 10yr premium payment 2 yr deferment and income from 13th yr for 25yrs and return of premium on 25th year in policy bazar website.

The xirr shown was 7.22% without considering the the gst implications for 1lakh premium

Dear Kaushal,

Calculate on YOUR OWN rather than depending on someone else claim.

Currently these plan for 25yrs income or 30yrs income plus return of premium is offering 7.1% tax free return after consideration of the gst on premium. Which other fixed return instrument shall offer more as rbi bonds have floating interest rate and 5yrs or 8yrs down the line it shall not offer more return after considering the tax implications on it. PPf has a limit of 1.5Lakh so cant go more than that. Please highlight anyother scheme which can offer better return for a longer period.

Dear Kaushal,

For 25 years to 30 years, if as per your calculation the returns are 7.1%, then go ahead. But calculate on your own before you believe of 7.1%.

I guess you must understand the plan first then write nonsense and illogical post, your post is misleading.

From 6.9% IRR just by adding GST of 2.25% how will the IRR drop below 6% ??

Also getting tax free returns of 6% is not a very bad idea for long term.

Dear Varun,

Thanks for your kind words. Please come up with your own calculation then compare mine. If I am wrong, then I will accept it.

Hi

Your analysis seems to be half baked.

Could you please suggest any other debt oriented guaranteed investment option which can give a yield of 7% tax free?

If yes, plz suggest. Otherwise plz don’t downgrade such big conglomerate for sadistic pleasure.

Dear Hidayat,

Thanks. PPF is one such instrument. Another one is VPF.

Hi, thanks for your analysis…

My bank representative is saying that in the long term income plan, after 12 years of payment, from 14th year onwards , if we want, we can take the lump sum amount, which will be given for next 25 years… So 25x amount we will get at 14 th year (-9% service deduction)… This seems attractive to me… What’s your take on that?

Dear Vmano,

The first rule of financial planning is staying away from BANKERS. They are the most dangerous species for your money nowadays. If you feel 5% to 6% returns are attractive by holding for the such long term, then please go ahead. As per me, its a worst decision.

Dear Sir,

Under this product itself I have come across a prospect of 5 premium term and 15 payout/policy term by a broker, where in document he provided if I provide 5L premium for years then return at the end of 15 yrs will be 54,44,240 which is astonishingly 50% of the invested value at the end of 5th yr (5L for 5 yrs will be 25L). Kindly suggest.

Dear Harshit,

Do you think it is ASTONISHING 50%? This is where we all do mistakes. If you use the simple calculation of the IRR function in excel (which is how the return on any investment should be calculated), it is just 6.1% but not 50% returns like how you are assuming. Remember, there is a gap of 10 years to double your money for them. They are doing any great work here. Don’t be obsessed with their numbers. Do your own research and calculation like how I told you. You will come to know the realities.

Could you please tell me the advantages and disadvantages of HDFC life sanchay plus, please

Dear S,

Refer the above post.

I agree with some positive remarks about this product covered by some respondents.

It is a good product for those who are in the age group of 50 to 60 years. As explained earlier ppf and other schemes have an upper limit. Also we can not put all eggs in one basket.

So in order to diversify your portfolio this is a good product. When we add the tax and insurance cost in our calculations, the returns are more than 8.5 % which is a good return for this long duration in my opinion.

Dear Jay,

If you feel this is the BEST product to diversify, then go ahead!!

Sir I feel bad that I have subscribed to a policy which I did not research enough. I recently saw an article on these endowment plans and I am seeing the truth of the HDFC Life Sanchay Plus plan. I had this gut feeling when I visited the bank and the bank employee recommended and almost lead me to investing into this trap that this plan may be a bait and I shoud re think about it but at the moment I was not thinking straight. Luckily, I did not agree on a large amount or long term.. I agreed on 50k for 5yr but maturity is 16yr. Also, I did not find it beneficial to drop it as it will deduct most of the invested amount as policy cancellation fee. Hopefully I will be careful in researching and investing in the future. I have a lot of respect for doing the putting in the time to research and telling the truth about the marketing traps that the banks use to trap people in these plans.

Dear Imran,

Happy to know that you learned and decided to be cautious in the future.

I believe this is a completely flawed analysis. People in the age group of 45-55 who are beginning to plan for the retirement are looking for tax-free guaranteed benefits especially when the global economy is a bit turbulent.

1. No mention that these are tax-free returns.

2. No mention that you also get Life cover from the day 1 (I know all these Fin advisors will jump on Term insurance but if a policy is giving that why not highlight that.) We know insurance and investment are separate.

3. PF limit is only 1.5 Lakhs. How do you get regular income out of it.

4. RBI (7.15) bonds are taxable at the income slab.

5. All other bond incomes are taxable as well with exception of some “Tax-free bonds”.

6. While Mr. Basu keeps saying Mutual funds and other stuff, he should understand the risk-appetite of a person nearing his retirement is different. He/She would rather be focussed on monthly income credited to his account than looking for secondary market and bonds.

7. I agree that lock in period is there for 10 years but at least the output is planned and regular which is the need for the old age.

8. I would have loved if he would have suggested NPS as a very good suggestion. NO mention of that.

9. These are guaranteed because these are Non-participating and Non-linking policy. Hence , that assurance of guaranteed income.

Dear Ritesh,

Based on current higher interest rate regime, do you feel generating 5% tax-free return is very difficult? Check the Gilt Bonds and SDL, they are offering beyond what you mentioned (7.15). Even if we one assume the person is under highest tax bracket, one can easily earn more than what this plan offers in the name of TAX FREE. I am not pointing at equity or risky debt funds when I said mutual funds. Rather there are various ways through which one can easily generate more than what this plan offers. NPS best product? I feel you are unaware of the underlying portfolio. Please go through the holdings 🙂

WHAT WILL HAPPEN IF I GOT TRAPPED AND PAID FIRST PREMIUM AND DONT WANT TO CONTINUE

WHAT PAYMENT WILL I GET BACK AND WHEN

OR

IS IT FULL PAYMENT WILL BE FORFEITED BY HDFC LIFE JEEVAN SANCHAY PLUS GAUARNTEED REGULAR INCOM PLAN FOR 33 YEARS TERM TAKEN 6 PAY YEARS AND 33 BENEFIT YEARS

Dear Vatsal,

If you paid the premium and policy is already issued, then you have two options.

1) If it is within 14 days, then you can request for closure within this 14 days free-look in period.

2) If the 14 days period already lapsed, then either you have to continue the premium payment or forget the amount what you paid.

You have written “It is better to buy a term life insurance and by investing monthly in PPF kind of product, you have the possibility to earn more than this plan”. But PPF limit is 1.5 lakhs per year. Where else can we invest after retirement for protection of principal, safety and highest possible return?

Dear Jayanta,

If you are exhausting PPF, then there are many options available like Govt Bonds too.

I have HDFC Life insurance policy booked in June 2020 . The policy document do not have my signatures anywhere. I was told that HDFC Life insurance policies do not contain signatures. But what I know is that before wet signatures were disposed off, signatures were mandatory especially on Benefit Illustration.

Dear Megha,

Policy bonds usually do not have your insured signature.

Hi Sir,

my account manager is pushing me to invest in “HDFC Life Sanchay Fixed Maturity Plan” plan but i dont have agood feeling about this for below reason?

1. I have to invest 1 Lakh for 5 years

2. Policy will mature after 10 years

3. if i surrender i have to will only get about 60% back, i will lose about 30%-40% depending when i decide to surrender if i do

5. I have to pay GST 4.5%, for 1st year & 2.25% for next 4 years

6. at this point payment i may get after 10 years is will be around 6.8 Lakh which seems low as to me

7. I am not sure how must tax i have to pay when my policy mature? will it be 10% or more?

if i add all GST + Tax then returns seems to be far less

Most of the above information i have got from internet as Account Manager has not shared much details about policy. I would appreciate your advice on this to me returns to me seems low after 10 years if i opt for lumsum amount?

Dear Majid,

Better to stay away.

Today I don’t see any fresh TAX FREE bonds available . All TAX FREE bonds in the market are available at a very significant premium of 20 to 30%.

So, while I understand what you are trying to imply, I am not seeing a practical way of making an investment that generates some regular income. AT the end of the day, one has to keep dabbling dynamically with debt funds etc. and manage them to generate constant income of 5.5% or more . There is a practical limit to the age till which one can be engaged in making investments dynamically even if it is debt-based.

This does seem like an alternative to some steady passive income. If there are other such instruments, please specify .

Dear Vikas,

Sadly you are unable to understand the concept of YIELD in bonds rather than just concentrating on price 🙂

Sir I already purchased HDFC Life Sanchay Plus in oct 2019 and paying premium regularly. How to close it. Will they give atleast paid premium…? Pl advice.. Thanks

Dear Udayakumar,

Sadly you can close it after 3 years but the surrender value is obviously less than what you paid. This is the real trap of such products.

Mr Expert….. Can u tell me, the PF interest is guaranteed for life long or for these many years???? No, na??? If u are a good financial planning expert, then you should say the good and bad both things, about the product…… Dont try to impose your foolish thoughts to the customers mind…… Either you doesnt know the abcd of financial planning or you have some other vested interest as you may be working as some plan agent….. Very bad dear….

Dear Mr.Harikumar,

It is the universal truth that PF interest changes. I am not hiding this 🙂 Now, regarding the long-term goals, why one should only rely on PPF or Debt Instruments? Regarding my knowledge of ABCD of Financial Planning, I never said I am an EXPERT. It is you who branded me on your own thought process. Then whose fault it is??

I can understand your anguish when such things are exposed. You are not the new one to me. I have experience of such guys since the start of this blog in 2011. Regarding my vested interest, if you prove, then I be your servant forever. Do you have DARING to prove? An open challenge to you 🙂

You are assuming on your own that I am an EXPERT, you are assuming on your own that I have some FOOLISH THOUGHTS, you are assuming on your own that I have some vested interest and you are assuming on your own that I am working as some plan agent. PROVE…COME FORWARD…I CHALLENGE 🙂

Tax free 6% means taxable 9% still if you think it’s not good can you suggest me any other options where my money is safe and I may get 9%

Dear Kalpesh,

TAX-FREE is the tool they use to fool us. There are many tax-free instruments one can play like EPF and PPF. If you don’t know the options, then it is your fault. If you feel this is the only product on this earth that is giving 6% returns, then please go ahead. They are waiting for you.

Actually — what will people do after PPF and other limits are exhausted.

If you really think it’s a TRAP — kindly suggest other viable means that help generate better returns with as low risk.

The basic problem is that just by EPF, PPF one cannot survive. Why is this a bad policy to help ensure some basic returns for the longterm ? Interest rates have been falling and something that ensure 5.5–6.0 % for next 30 yrs does not sound too unreasonable ?

I recall, when I just started to work FD interest rates were around 10% and today 6 % .

So, while conservative, this scheme seems lime a reasonable alterative. ?

Please help understand.

Dear Vikas,

There are many tax-free bonds which are offering you a better yield and kind of RBI Floating Rate Bonds which are a boon to many of those who are looking for a constant stream of income. However, in debt space to accumulate, various categories of funds are available where you can easily avoid default or downgrade risk easily. It is an art of managing than sticking to one product and saying other than this product there is no other. If someone say so, then he or she may be a representative of that company and trying to sell this product.

does this plan make sense now considering PF above 2.5 L is taxed. mainly for investors failing in 30% tax bracket.

Dear Naveen,

Post-tax returns from EPF are far better than this plan.

Dear Sir,

I have already taken HDFC Sanchay 3 years back. Can I surrender it or is there any way out to stop this policy?

Dear Pooja,

The only option now for you is to stop the premium payment and let the policy be converted into paid up.

Hi

I am 30 yr old and was looking for the investment. And confused in between Hdfc Sanchay and lic Jeevan UMANG.

Also I am confused whether I should go for a term insurance and mutual fund investments.

But don’t have enough knowledge of mutual fund and it’s not a safe instrument.

And this insurance policy attract by saying guaranteed.

Lic Jeevan UMANG says to pay 1 Lac till 15 yr and ll get 1lac till life long and surrender value also they are offering in the age of 70 is 80 Lac. Is this true.

I have checked on leader app.

Plz suggest.

Dear Basu,

42 years old and looking for a safe guaranteed investment plan to get a lumpsum end of 5yrs or 10yrs premium term for child’s education and marriage plans . Please advice if Sanchay plus is a safe bet. ?

Dear Balaji,

Are you comfortable with 5% returns?

Dear sir

Plz suggest if I should go for hdfc sanchay plus or lic umang.

My age is 32 years and can pay yearly premium of 60k for 12-15 years.

I am looking for a guaranteed long term income plan.

Assuming that I am surrendering the policy after 70 years, which plan would give better returns.

Thankyou

Dear Arul,

At what cost you are looking for GUARANTEED returns? As you are young, do you think these two policies are the great products for you?

Dear Basu

Thanks for the detailed analysis.

Considering that the returns are 6% and there’s no tax, the pre tax IRR amounts to 9% (for those falling in 30% tax bracket) guaranteed for decades in the falling interest rate regime.

Do you still disapprove this product for those who want to have this as one component of their retirement plan?

Arvind

Dear Arvind,

GUARANTEED and TAX FREE are the two major motives to invest in such products. But we ignore the impact of inflation, which such products fail to deliver.

The returns that you get, what is the taxation implication? Would those get taxed as income?

In that case for an FD only the interest gets taxed right?

Or would the payments coming in be tax free?

Dear Rahul,

It is tax-free.

Dear Basavaraj sir,

I am 40yrs age and getting sanchay plus as the following:

Premum pay for first 10 years is 10 lacs (each year pay 1 lac). 11th year is cooling period. From 12th year I get 188000 every year for next 10 yrs upto 21st year. So its like 10 yrs pay 10 lacs total and get 1880000 totally at end of 20 years.

My crude calculation says this gives better returns that bank FD. I somehow dont understand IRR, what would it be and do u recommend this plan ?

Dear Ankur,

By investing for 10 years or so, if you feel FD returns are the BEST returns for you, then go ahead.

Hello Basu

Given the current low returns, are there any other products that provide 7% or more IRR.

My investment time frame is about 5 years as I have about 4 years of working life.

Thanks

Dear Subbu,

For such short term, it is always better to prefer safe options than chasing the returns.

Dear sir

Plz suggest. Should I go for sanchay plus or capital guarantee plan( combo of sanchay plus and clik to wealth) by hdfc. Policy ppt 12 years and annual premium of 60000.

Dear Arul,

May I know the reason for choosing these two products?

Company is giving gurantee IRR of 6% (R).

Please add mortality cost (M), remember there’s insurance involved.

Please add operations expenses (OE). You’ll agree that there’ll be expenses to run a company.

If it’s sold through bancassurance (annual incentives to the employee) plus benefits to the bank whose employee is sellin it. If it’s through an agent the commission paid to the agent. In any scenario there’s an expense involved (C).

All the money collected in these policies will be invested in G Sec or other asset class.

Now please add 6 (R)+(M)+(OE)+(C) the returns from the investing in G Sec or in any other similar asset class has to be atleast 9 to 9.50%.

Hope you’ll agree that it’s such a product that billionaires, millionaires and entrepreneurs should ALL the wealth and income in these kind of products.

Dear Raju,

First time I learned that this way too one can calculate 🙂 Great…go ahead with 9.5% returns generating product. Just because all billionaires, millionaires and entrepreneurs are investing does not mean that one must invest BLINDLY. Their portion of investment in such products may be minuscule. How can you compare their net worth and their investment style with yours??

Dear Basu,

I read all your reviews and noticed the bottom line that all plans are offering return (IRR) aprox 6%.

Currently hdfc life is offering a plan to pay 1lac per year for 10 years and with pay annually 95000 from 12th year to 36th year (25 years) including premium paid (10lacs) on last payout. IRR comes 6.20%.

I am already investing in PPF. So, can u advise where to invest if plans like Sanchay plus are traps.

Thanks in advance

Hi Basu,

I was looking to opt sanchay par advantage guaranteed income plan and then read your article.

They had given an example: if 1L is paid every year for a term of 12 years. I get 40K every year as guaranteed income right from the second year till the age of 100.

If I decide to opt out / surrender after 12 years as per maturity date, I get 13L at the end 13th year.

(Plus the profit I had got every year until 12th year of 40K * 12 = 4.8L)

Could you please advise if this is profitable compared to lic money back policies?

Also could you please if this is profitable generally?

Looking for your genuine advise.

Thanks.

Dear Karthik,

Whether you checked the IRR?

Dear sir, I am 42 yrs old, a salaried employee, and seek your inputs on the safest investment plan with high returns for 1) short term say 5 years..2) retirement plan

Please suggest thanks

Dear Ginny,

Financial Planning can’t be done over such a platform.

How is this compared with Jeevan Umag from.LIC? returns are better in jeevan umang whats your view on this?

Dear Girish,

Both are of same to me.

I took this policy and paid one premium of 2Lakhs.but now am afraid I have made a mistake.heard the bank is in trouble.will I lose money after paying for 5yrs or should I back out now

Dear Chindu,

HDFC Bank is different from HDFC Life.

Why do u so called self proclaimed financial advisors stick to Rs.30,000 investment..

Why can’t u ask people to think big and invest 1lakh for 11 years and get double for next 10 years.

U Also don’t explain the death benefit.

All u want is people to invest in mutual funds and other fluctuating financial products.

In the name of GST u instill fear amongst people…I have also seen financial scammers not planners criticising Jeevan umang plan of Lic

Dear Kapil,

I can understand your anguish 🙂 Regarding Rs.30,000 investment, I just took an example. You are FREE BIRD to assume either Rs.3 crore or Rs.3,000 also. Coming back to Mutual Funds, am I said that one MUST invest in mutual funds? It is your own views that you created if I highlighted negatives.

Dear sir

PL tell us which annuity plan or pension plan is good for retirement as I am working in private company age 46 years

And PL tell where to invest money for short term for 3years max

Dear Shivanandi,

Don’t run behind pension or annuity plans. Try to invest as much as possible and accumulate at first. Regarding investing for 3 years, use Bank FDs.

I was investing in VPF. With the announcement of new taxation rules on PF contributions about 2.5 lac pa, I am looking to invest in an alternate fund which is “safe”. I was suggested HFDC Sanchay Plus by someone, I am also considering Debt funds. Do you have a suggestion for a investment avenue which is low-risk and with an investment horizon of around 5 years (with a view to build retirement corpus)? I am 46 years.

Dear Srivatsa,

Post tax returns on EPF is far better than these SANCHAY kinds of products.

Can you elaborate on this? with the EPF rate of around 8.5% and tax being applied on the contribution above 2.5L, the net post tax IRR will be less than 6 % for highest tax bracket in EPF. Isn’t this the same?

Dear Anil,

It is far better than this product??

Dear Basavaraj, How is HDFC Sanchay Par advantage? Both are part of the same well? 🙂 I started looking for its reviews after RMs are offering it as an alternative to low interest FDs.

Dear Srikanth,

Old wine in a new bottle.

Hi..

I have taken policy from pnb met life premium payment of Rs. 1 lakh per year for 10 yrs and guaranteed income returns of 1.71 lakh per year..as I m conservative in investing my money.. and want security.. if I will do normal fd for 10 yrs then I will just getting 5.2% I didn’t it as my money is safe and I will also getting interest more than bank and 10 times risk cover also.. is there risk in investing in this plan of pnb met life..? Will I get my returns surely?

Dear A,

What is the use of analyzing the RISK and aftereffects when you already into the well?

Hi Sir,

On Maturity Date, policyholder shall have an option to receive the future regular income as a lump sum, which shall be the present value of future payouts, discounted at a rate of 9% p.a

So, if I pay a premium of 3,60,000 for 10 years and they assure me 3,35,700 will be paid for the next 24 years, does that mean I will get 335700*91%*24, if I opt for Lump Sum payment on the 12th year?

Sorry if this is repeated.

Dear Ananthram,

It is not your premium what they pay but the maturity proceeds. Also, it is DISCOUNTED value of those future cash flows by 9%.

Thank you very much for taking time to reply, Sir.

Regarding the maturity proceeds, they are specifying a guaranteed payout of 335700 per year. My concern here is, how are they able to give all of the future payouts ((335700-9%)*24) as a lump sum, if I opt out in the 12th year? That comes to around 73 lakhs against the total premium paid of 36L+GST.

I am trying to understand this. If possible, please throw some light on it.

Dear Ananthram,

Assume that you are about to get Rs.100 as yearly payout. They will give you Rs.91 today at 9% discounted value of that year.

Hi Basavaraj,

I have one query about this premium and maturity proceeds. I’ve paid two premiums on a 5 yeah plan. Due to covid situation and job uncertainties I’m thinking about breaking this. I’ve enough money ready to pay one more premium. If I break this after paying three premiums, would I get the premium amount back? Or only maturity proceeds will be paid out?

Thanks in advance

Dear Meera,

If you paid for three years, then the surrender value is less than what you paid.

Hi Basavaraj,

Thanks for the reply. Tbh I’m not very knowledgeable about the technical terms in finance area. Could you please explain when you say surrender value is less than what I paid, does that mean I’ll not get even close to my paid premium amounts back? Say I’ve paid 3 Lacs annually for 3 years and after 6 years am I eligible to get any amount back?

Thanks again for your time

if the rate is 6% I feel this is awesome because after 10years I don’t see any product which will be offering tax free even 6% that too with for 25years and with return of premium. I always see there is huge craze when Govt. Of India issues tax free bonds for 10 or 15years and to the HNI & UHNI segment huge demand for that bonds.

As it’s traditional in nature, it’s shows the return which is easy to calculate the IRR , it also ensures that the rate or IRR for the time when into that particular segment such instruments will be available. The best way to consider this as locking the rate for longer tenure with certain portion of my investments.

Dear Srimanta,

If you feel 6% is the GREAT return on your investment to sustain after 10 years, then please GO AHEAD!!

Hi Basu, first of all good review and thanks for your time. I purchased HDFC life Sanchay plus after carefully evaluating my portfolio and i am ok with 6% return. Already have investments in PPF, FD, Gold and shares. After this policy i can be little aggressive in buying small caps/midcap as point of this is to get balance in my portfolio in long term.

My question is that 1. after purchasing policy customer service is very bad. I am concerned that after policy is matured will i have to follow up for guaranteed income or they will credit directly in bank.

2. What this clause means – Guaranteed sum on maturity : “On Maturity Date, policyholder shall have an option to receive the future regular income as a lump sum, which shall be the present value of future payouts, discounted at a rate of 9% p.a”

Dear Harsangeet,

1) They can’t harass in getting the maturity. Don’t worry.

2) It is the total amount which you will get as lump sum as maturity amount rather than future payment at the discounted value of 9% per annum.

Thanks for quick reply, much appreciated.

for point 2, is it the option which i can opt after premium payment term is over? how is it calculated, e.g. i pay 1 lakh each year for 10 years (Total payout – 10 lakh) and have long term income plan (Payout of 25 years, each year payout of 90000 and 10 lakh return with last payout). How to calculate this.

Dear Harsangeet,

Less of 9% for each future contribution they pay you as lump sum in one go at maturity.

Hi Basu

I fell in this trap, one hdfc RM give me hdfclife sanchey policy in 2015, i payed 50,000/- lateron i invested in sbi and stop paying premium, after 5years now june 2020i visited hdfclife office so that i can get the premium refunded , assuming they will deduct some panaliy whatsoever .Now i came to knw that i will not get any penny because i have to pay 3 premium minimum. But policy does not say anything like that they use a term GIR grunteed invetmnt return ,policy will get GiR after 3premiums, but it does not say whatever you payed will become zero if you dont achieve GIR, i feel cheated now, pls advice what to do, where to aproach, is there any hope to get my money back

Dear Kuldeep,

Sadly their version is correct and the rule.

Dear Basavaraj

Thank you for a detailed analysis. I request your review on the following points:

Assumptions:

– I am actually considering Aditya Birla ABSLI Secure Plus Plan (same product as Sanchay Plus)

– 2L + GST Premium for 12 years (comes to 2.09L for 1st year, and 2.045L for 2nd through 12th year)

– Payout at 2x = 4L starts from 14th year to 25th year

– IRR comes to about 5.28% (using excel IRR formula)

– Comparing this product only to other debt products and not Equity MFs or ELSS etc. I have already maxed out PPF etc.

Results:

– Since the maturity amount is tax free, to compare with other taxable products I have multiplied the return by 1.45. (At 31.2% tax bracket including cess). Assuming a 5.28% IRR this comes to around 7.65%. (5.28 x 1.45)

– Since this is an insurance product, the premium can be paid by credit card, which earns you an extra 1% or more – tax free. Again this is worth 1.45%.

– There are some added minor benefits such as accidental insurance etc., which I am not putting a value on since I am looking at it is only a debt investment.

Simply adding the two yields around 9.1% taxable, which is a decent return. If a long term FD of 9.1% were to be offered today from a safe bank such as SBI, HDFC etc. I am sure most people would jump on it.

Thoughts? What am I missing.

Thanks in advance – and great work!

Another update to the above.

HDFC Sanchay Plus when bought from the website of HDFC Life gives a higher return vs. logging into your HDFC Netbanking or through your RM. Details below:

Premium (assumption of 2L – same as above):

– 2L + GST for 12 years (2.09L for 1st year and 2.045L for 2nd to 12th year)

– 12 years PPT (Premium Paying Term)

Payout (via RM)

– 2x = 4L from 14th to 25th year

– IRR = 5.28% (using excel IRR formula)

– Taxed return = 5.28*1.45 = 7.65%

Payout (via HDFCLife)

– 2.15x = Rs 430,540 to be precise from 14th to 25th year

– IRR = 5.87% (using excel IRR formula)

– Taxed return = 5.87*1.45 = 8.51%

Dear K,

So the returns from this plan is more than 7%? May I know how you calculated the IRR?

Dear K,

If your goal is long term, then why debt ONLY? Why not mix debt and equity and accumulate well?

Hello Basavaraj,

Thank you for your responses.

I am looking at the Sanchay Plus only from the debt part of my portfolio. Equity part is separate. With the recent fear around debt funds, RBI withdrawing the 7.75 bonds and FDs/Liquid Funds yielding no more than 6% I dont see a lot of choices. Yes Bank and some banks like IDFC First offer 7 to 7.5% but I am worried about the banks viability and NPAs once this pandemic is over.

For the IRR I got 5.87% (pre-tax) from IRR formula in excel (see below). Since I fall in 31.2% tax bracket, to compare with other taxable products I multiplied by 1.45. So if I make 8.51%, after tax deduction at the rate of 31.2%, the number would be 5.87%.

Here is how I got IRR – since I cannot attach it here.

Excel Row 1 = -209,000 (-ive 2.09L)

Excel Row 2 to 12 = -204,500 (-ive 2.04L)

Excel Row 13 = Blank

Excel Row 14 to 25 = 430,540 (+ive 4.3L)

Excel row 26 = IRR (1:25) = 5.87% [I also used XIRR formula with dates, same result]

Excel row 27 = Tax rate = 31.2%

Excel row 28 = 5.87% divided by (100%-31.2%) = 8.51%

So comparing with taxable products (e.g.: FD) the yield is 8.51%, which is not bad. Now since this is HDFC Life, I feel they are a fairly safe company and comparable to FD in HDFC or SBI.

Please let me know if I have missed something or a made an error. Since I am a novice, there is probably something obvious that I have missed :)!

Thank you again for the wonderful work you are doing!

Sir, in the income-plans, the money is taxable or non-taxable? I heard that it is either 80C or 10D. I don’t have hope of 80C. it will go away. But what about 10D?

All these plans come under 10D and no need to pay tax ?

and I saw that 10D is applicable only if the following condition is met.

“The insurance premium for any year during the policy tenure should not exceed 15% of the sum assured. Besides, it also should not have been purchased on or after 1st April 2013. Also, the insurance policy must be for the life of any individual who meets the following criteria:

Disabled or severely disability individual, as specified under Section 80U of the Income Tax Act, 1961

Suffering from a disease as specified under Section 80DDB of the Income Tax Act, 1961”

Does this mean, that actually the income is taxable for normal people. ?

Dear Raju,

Life Insurance companies are smart. They made it eligible by following those norms.

Dear Raju,

It is not like EITHER 80C or 10D. Please read the conditions properly.

Sir, I have one question.

Is that 5% or 6% fixed? I mean, is the return linked to RBI repo rate and keeps changing every year? or is it always 5-6% and nothing linked to market?

Dear Raju,

Refer the post properly.

Nice information, how is sbi life smart money back gold as per them, if we pay 1L premium per year for next 12/15 years we will get close to 27 Lakhs at the end of the term i.e 12/15 years, if not what are the other best options we have in similar products to invest?

Dear Raviprem,

It is not so different from this product.

The income received every year on this sheme, is it taxable under my tax slab?

Dear Samyuktha,

NO.

Can you suggest any investment opportunity for a 47 year old person who is conservative in investment, but can take a calculated risk

Dear Anand,

Let me know what is the meaning of CONVERVATIE and CALCULATED RISK as per YOU.

Dear Sir,

Very interesting article. What is your view on HDFC Life Guarnateed income plan and Aditya Birla Sun Life Insurance guarnateed income plan?

Dear Abhishek,

Stay away.

Hi Basu, very interesting info and very useful for people like myself who are not familiar with the finer details of such plans. Can u tell me if SBI saral pension plan is worth investing for retirement income? Or can u suggest some investments which will give guaranteed income after retirement. Kindly advise

Dear Savita,

Stay away from products that will combine insurance and investment. Better you create your own retirement corpus.

Sir more than insurance i take it as an investment product. I agree return is hardly 6%. But that alone is misleading. U hv to take other factors into consideration, like how fd rates hv been declining over the years n how they will continue to fall in coming years. Each of us does invest in fds although return is meagre compared to mfs. Moreover u r getting benefit of 80c and maturity is tax free as well which isnt the case in fds.. saving 30000 pa isnt a big deal for most of us. Although returns r not much but still it encourages u to save atleast something. Do reply

Dear Kunal,

If you feel 6% is the BEST RETURN FOR LONG TERM, TAX BENEFIT and if you feel it ENCOURAGES you to save, then PLESE go ahead and buy it TODAY. Bank RMs are eagerly awaiting for you.

If we are comparing plans like LIC Jeevan Umang and HDFC Life Sanchay then which one is more better. One may ready to take 6% IRR as life long tax free income. As india is developing country where future interest rate is to be going down by time gap. Today PPF interest rate may be near 8% which may get reduced to 5% in span of 15 year and more in coming years. If we get IRR of 6% with long life income then is it good to invest my debt portion?

Inflation gap is always there but i just compared my debt investment part only which i can kept only in terms of FD, PPF or liquid fund. So inflation rate is to be ignored as per my understanding. Clarify me if i am wrong.

Dear Priyank,

If 6% is best for you, then please go ahead and BUY.

Hello Sir,

I’ve invested in the ULIP & paid 2 premiums (HDFC Click 2 Invest – 3000/month for 5 years and policy term as 15 years). Your suggestions regarding what should I do after 5 years (lock-in period ends here). Secondly, after reading your views on Guaranteed income plans, I’m confused whether to go ahead or not. Is it advisable from your end to rather invest in Postal Life Insurance’s Endowment Plan (SANTOSH) as I’m eligible to invest in it. It gives us bonus based returns and more importantly comes with a security that it is the product of Central Government. I’m planning to invest 3550/month for next 23 years and chosen 10 Lac as my Sum Assured in the SANTOSH Plan. If the bonus remains constant at Rs. 58000/10 Lac, then I might end up receiving Rs. 23,92000/- lumpsum when I turn 60 (after 23 years from now.

Dear Abhijit,

Simple answer-NEVER COMBINE INSURANCE WITH INVESTMENT.

Sir, If we take illustration of 10L per year in HDFC sanchay plus 25 years they pay 9.6L per year tax free that amounts to be 2.4cr in total after 25 years and 1cr initial investment is paid back so total of 3.4cr is earned in 25 years if stayed invested.

So looking at these figures what is your thought? All these will be confirmed returns.

Dear Sagar,

By taking higher or lower premium rates, does your return on investment change?

Sir, if you are suggesting PPF instead of HDFC sanchay how this can replace PPF if amount limit is 1.5L per year in PPF.

Say i have to Invest 5L per annum in this product then i cannot substitute to PPF.

Dear Sagar,

You mean debt part of your investment per year is Rs.5 lakh? Then how much will be your equity part per year?

Dear basa sir,

Happy to hear from advices..

I am investing 150K/Year in PPF, Beyond that could you help me to choose good product where i could invest 1lakh/ year and provides good returns after 20 Years as pension fund. It may be taxable also, that doesnt matters

Dear Chezhian,

It is hard to do the whole planning on such public platform without clear understanding of your financial life.

Dear Basavraj,

Thanks for your views, but I still feel that the primary aim of buying Life Insurance endowment policies,( be it LIC, HDFC,) is life cover & death benefits, and not returns. Any endowment policy doesn’t provide more than 6% IRR, but it is usually purchased for the life cover & death benefits, While PPF, mutual funds, etc provide better IRR, still none of them provide life cover, hence the purpose of buying a product should be clear in every investor’s mind.

Thanks,

Shantanu.

Dear Shantanu,

If your main purpose of BUYING LIFE INSURANCE is “life cover & death benefits, and not returns”, then why not buy HDFC Life’s Term Plan rather than this product?

“I never lose, either I gain or I learn”.

I have now bought shares in HDFC life and HDFC Bank & the returns are fantastic.

How did I learn – my HDFC RM palmed me off an HDFC savings assurance plan for which I continued paying premium for 10 years. The lump-sum I rec’d in the 11th year amounted to an IRR of 5.1%. I honestly felt cheated with this product and found so many like me crib about the product. But as HDFC BANK & HDFC LIFE continued to make handsome gains I realized, I need to move from the customer (victim you might say) to the owner side and enjoy the benefits.

Kindly keep morality out of investment as evidenced time & again by big corporations across the world.

Dear Financial Consultant,

Having HDFC Bank, HDFC AMC and HDFC Life stocks is far far better than investing in such dumb products.

Please advise if one fell in the trap and has taken this policy, what is the way out, as returns are certainly discouraging and like you mentioned if one is looking for life insurance better to go for term policies.

Dear Roopesh,

Below are the options:-

1) If the policy is in free-look in the period, then close it immediately.

2) If you paid 1-2 years policy premium, then either you have to FORGET what you paid or surrender after 3 years of completion.

3) If the policy is paid for more than three years, then better to surrender.

Hello Mr.Basavaraj. Thanks for the nice article and interesting comments too. I am unable to understand the IRR calculations clearly though.

But could you advise how this compares to GCAP from Edelweiss Tokio? Certainly the returns are higher, but from IRR perspective, does it tick better against the inflation in your view? Can they be looked as a diversification?

Also, are these guaranteed maturity (from any company) really guaranteed!?! Can IRDAI have a say when these guys refuse to pay out during maturity? Thanks.

Dear Prabhu,

Whether it is this HDFC Plan or Edelweiss, the returns will not be more than 7%. In such a situation, how you can fight the inflation? Stay away from such junk products.

Hello Sir..

Want to know about Hdfc 3 D protect plus term insurance plan.. i m 40 yrs non tobaco user

Dear Sandip,

What you want to know?

Hi I have opted for sanchay plus.but the benefits suggested by them are not as per the description mentioned and they also promised , free medical policy, but they haven’t provided one. Sow wanted to know, following two points.

How do I cancel the policy, as I am not interested in continuing the policy and block my money for years.

Also how to I complaint about their false promises, as I forwarded the complaint to HDFC as well , but they are not willing to listen and have a pre defined answer.

Dear Parth,

You can cancel the policy within 15 days of free-look in period. NONE can stop you from exercising the rights of cancelling the policy.

Hi Sir,

How about the TATA AIA Diamond plus plan. Is it really good to invest as they are guaranteeing for 20% for 8 year policy term?

Dear Kaushik,

God bless them that they are guaranteeing 20% returns. If you get it in written and share with IRDA, then Tata AIA will be closed immediately.

Hi,

The commitment on the 20% is available in their website detailing the plan details under the Disclaimer Section. Following is the link.

https://tataaia.com/life-insurance-plans/savings-plans/diamond-savings-plan.html

Dear Kaushik,

I have not seen the number 20%. Can you paste the exact sentence where they mentioned 20%?

Hello Sir,

Which are competitors plans for HDFC Life Sanchay?

Which one is best among all? (For the people happy to receive IRR 5.5% – 6.0%, guaranteed tax free returns)

Dear Chanpreet,

Why you are desperately searching for such DUMMY PRODUCTS?

Hello sir, superb artical. How do I connect with you?

Dear Manohar,

Regarding?

Hi, How do I connect with you? I have a few questions regarding HDFC Life Click to Wealth Plan and Bharti AXA elite .

7738145225

Dear Ravindra,

Drop an email to [email protected].

Hi Basavaraj,

I have been contacted with the same plan. I need one clarification. In HDFC Life Sanchay Plus – Life-Long Income Benefit and Returns , suppose I invest 1lakh every year for 10 yrs, the person is saying that if you want to take the maturity amount after the completion of 11 years (10 yrs premium + 1 year cooling period ) you can do so and that will be equal to maturity at the end on 30 yrs minus 9%pa i.e 25 lakh(25 years ~1lakh per year) minus 9%pa i.e nearly equal to 22 lakh by end on 11 th year . Is this correct . They also are showing the proof in the policy by referring to page 7 where its written as following –

“At the end of the Payout Period, the policy terminates by returning Total Premiums paid. On the maturity date, you shall have an option to receive the Guaranteed Sum Assured on Maturity, which under this option, shall be the present value of future payouts, discounted at a rate of 9% p.a. This interest rate is not guaranteed. However, any change in the interest rate will be subject to prior approval of the Authority and will be applicable only to the policies sold after the date of change. At any point of time during the Payout Period, you shall have an option to receive the future income as a lump sum, which shall be the present value of future payouts, discounted at a rate which is computed using the prevailing interest rates”

Can you pl enlighten me on this . Is it again a trap or they are saying correct thing

Awaiting for your response

Dear Vishal,

Let them add few more dozen of features, the returns will not go beyond 6% 🙂

Should I invest in PPF 15+5 years? Please suggest.

Dear Gourav,

Yes, as long as you wish for.

Thanks Basavraj, Saved from trap.

Dear Aniket,

Pleasure 🙂

Hello

Thanks for your efforts to log this all down in nice fashion.

Just got written reply from HDFC life on “Will nominee also get back all premiums paid at the end of payout period ?

Ans:Yes,”On death of the Life Assured during the Payout Period, the nominee shall continue receiving Guaranteed Income as per Income Payout Frequency & benefit option chosen till the end of Payout Period.At the end of payout period, nominee get back total premiums paid (excluding the underwriting extra premiums, taxes and other statutory levies, rider premium, if any)

There is provision “At any point of time during the Payout Period, you shall have an option to receive the future income as a lump sum, which shall be the present value of future payouts, discounted at a rate which is computed using the prevailing interest rates.” However I could not get any details on it how it will be calculated.

Your analysis is quite right that returns are not that great except for higher tax bracket customers who may get benefited from total tax free payouts/returns. You said right that investment in PPF / MIS etc are better than such type of investments but both has limitation of max investment amount allowed.

So customers who are looking for lump sum investment of considerable amount in safe instrument, don’t have much choices than to choose this plan (for tax free income) or Jeevan shanti.

Whats your views ?

Dear Janu,

Why these LIFE INSURANCE plans only? Why not Tax-Free bonds kind of products?

Dear Basavraj

Yes..Tax free bonds would be great option but when those are available in primary market..I dont see any bond would be available in near future for fresh purchase. Also I dont know if it would make any sense to buy them in secondary market or above insurance product would give more IRR than secondary market bond purchase.. Pl guide.

Dear Janu,

Currently, there are no such bonds in the primary market. However, you can easily buy them in the secondary market. Who told you that LIFE INSURANCE PRODUCTS GIVE YOU MORE IRR? Cross-check your IRR of Life Insurance with the Bond Yield of these tax-free bonds as of TODAY.

Hi .. loved the analysis – have one query – for long term income scheme – under the 5 years option, are the repayments eligible for exemption under sec 10 10 d? Hope you would throw light on this

Dear Narayanan,

Any survival benefit you receive from life insurance is subject to the rules of Sec.10(10D).

Superb Article recently getting more calls from HDFC stating guaranteed returns even Preferred customer care person also forcing to take these plans…..thanks for giving headsup.

Dear Prasanth,

Pleasure 🙂

Hi, thanks for a detailed analytical review. As I understand the returns are very low in HDFC guaranteed return life insurance product. I want to invest in guaranteed life insurance plan. I have heard LIC plans give 7%+ return. However I have not understood their “bonus” concept and how certain is that. Can you please tell me the best guaranteed return life insurance plan giving best XIRR. Thanks

Dear Gupta,

Why you need a GUARANTEED product and also why you need LIFE INSURANCE?

I have some unique requirement due to which I need to start a life insurance policy. I want to invest some money in fixed income products but those are taxable and tax free bonds are highly priced. Personally I feel tax free guaranteed returns of around 7% in a life insurance provides me a good combination of life insurance and investment. Thats why my query, can you please tell me a guaranteed return life insurance plan giving best XIRR.

Good that you have choose LIC as your trusted insurance and saving partner.

Dear Naresh,

Why defending LIC rather than the actual product?

I disagree,

These all points intact is the need of customer.

Also on Guaranteed Income, you, consciously, did not discussed about 12-1-12 option.

Sorry to say, bit shrewd of you.

Dear Amit,

12-112 OPTION?

To all those saying pre tax returns are high and the person wjo calculated 33% tax rate— why would someone like that need guaranteed income? The people looking for guaranteed income are people who are making under 10 lakh probably which means they are probably not going to have to pay tax anyway.

Dear Test,

But sadly those who are crying are too much caring for those who are in 33% tax bracket 🙂

Dear Basu Sir, thank you for the excellent analysis. Appreciate the time and effort from you to enlighten investors. Request your opinion on invits as an option to get passive income instead of such insurance plans. I heard irb and indigrid offer 17 % and 13% pre tax yields

Dear Daya,

Thanks for your suggestion. Sadly I do not follow such products which you referred.

Superb Article..I was about to take this plan and also my friend was thinking to buy that ,but fortunately I tried to find pros and cons of this plan and luckily,I got this article.I already have term plan of 1 crore..So,why should I waste my money in buying this plan just for cover ? instead it is very good if I can diversify that amount into PPF/MF/NPS/Stocks/FD..It can overall will make me earn some handsome return in total after I retire if my investment purpose is for long term..BUt sir,one thing I do not understand is TAX FREE.If I have invested my other money in PPF/MF/NPS/Stocks/FD (after saving in 80c),if I withdraw that amount then will I have to pay tax for all of them ? Please explain in detail sir.Thanks in advance.

Dear Raj,

Each product comes with it’s own positive and negative. It is you who has to decide. Regarding taxation, it is hard for me to explain about all product in comment section.

Basavaraj,

I don’t understand the reason why are you hell-bent to malign this product. With due respect to your knowledge I would like to make the following points:

1. I am not an Insurance agent but have little bit of understanding about financial products

2. Each & every financial product has its PROs & CONs

3. IRR, Inflation, taxation etc. these fancy words are good for discussion but the typical Indian mentality is that Insurance is for investment, tax saving or may be for layering black money. Till few years back nobody, nobody use to talk about Term insurance. Now atleast few people are talking and buying it, but may be not in its pure term.

4. Any one buying insurance asks the 1st question- what is the return?(Maybe I will also ask) So all Insurance companies design products as per the market demand to survive. And these products are approved by IRDA.

5. There are always better alternatives available against any product but that depends on the buyer’s risk appetite, knowledge & awareness, time he can invest etc.E.g. Why only PPF? If someone invests in a Bluechip Share and remains invested for say 15-20 years, maybe he will get 20%+ return.

As an advisor it is expected that one should tell the PROS & CONS and let the audience to judge on their own.

Sorry, but your review is giving a sense of bais.

Regards,

Rajiv

Dear Rajiv,

I am not here to malign any product and also whether you are an adviser or not that also does not matter to me. I am just putting the facts, rest is up to the readers to decide. However, if one investing without understanding the IRR, Inflation and taxation, then everything will be bad shape. I hope you being knowledgeable understand the importance of IRR, Inflation, and Taxation when one try to invest. As an adviser, it is my duty to highlight the things which matter the most. This is what I did by highlighting the INFLATION, IRR and TAXATION, which are utmost important before investing. If you feel they are not relevant, then god bless you 🙂 Please invest 🙂

Seems that you want to prove your point at any cost. You probably missed what I wished to highlight – “Each & every financial product has its PROs & CONs”. Just highlighting the CONs is partial sharing of fact.

Anyway its your blog….Can write anything you wish

Dear Rajiv,

What if there are more CONs rather than PROs? In what sense it protect the investors?

Great response

Namaskara Basu,

I have tried calculation for the Guaranteed Income Option and I see that You haven’t taken into consideration of the Compounding ..

Dear Shivaram,

Please understand the meaning of IRR, Compounding, XIRR, Absolute Return and Simple Interest, then we discuss. At least let me know how one has calculate the returns? What is IRR?

Thank You Basu , I think I need to do my Homework

Hi – One of my friend just retired; he is actively looking into this plan for a long term income option like pension for himself and his spouse (100% like him) after 5 years of deferment. He is in 30% Tax bracket and likely to be for many years. Please let me know what can be better low risk plan/invest option. Understand overall Tax Free return from this plan is around 6% which hardly beats inflation. You will appreciate PPF investment is limited (1.5 Lacs) and no VPF investment opportunity.

Dear Halder,

What is his age? How well he planned for emergencies? What about his family dependents? How long he need this income? By mere sharing few lines, I can’t guide you properly. It is dangerous to your friend than me.

Thanks. He is 60 now; his emergencies and family dependents are well covered; he wants this secured income lifelong for himself and his spouse. Please let me know if you need further details

Dear Halder,

Yes, with this mere sharing, I can’t judge. Better you drop an email to [email protected]. Just one thing I can say, if there are no financial dependents, then why he is looking for a LIFE INSURANCE+INVESTMENT product rather than the INVESTMENT PRODUCT?

I have read your whole thing above. Even the paytm bank FB is giving 7.60% interest on GB. You are correct this policy yeald low returns as compared to PPF. Thank-you for your reply. I will figure out myself on how to cancel this policy or to continue with it.

Dear Jatin,

Thanks for understanding the concerns I aired against this policy.

Purchased HDFC Life Sanchay Plus on 21st June 2019. Premium Rs 5225 per month.I want to know do I get the full amount invested + interest or I should quit this plan and invest in PPF. I have just paid one premium. My only concern is will I get the amount I have Invested back including interest. I want my money to be save. I should not feel that after few years this plan is bad debt for the HDFC bank and I loose whole my money.

Dear Jatin,

Refer the above post properly. If you still feel it is a good policy, then go ahead. If you close the policy now, then you will not get anything.

I HAVE GOT THIS POLICY DETAIL THAT I HAVE PAY 104500/- PA FOR 12 YRS AND FROM 13TH YEAR IWILL GET 231750/- FOR THE NEXT 12 YRS WHICH IS TOTATALLING TO RS.2781000/- PLZ EXPLAIN THE IRR WHICH IS COMING AROUND 7%

Dear Akash,

Don’t believe either on me or the person who claimed 7% returns. Calculate the IRR on your own the way I did it in the above post.

I am 44 years old. Does the Critical Illness cover option with Guaranteed Income (13 years) plan help? I do not have any health insurance or term insurance apart from the Corporate Health Insurance.

Secondly, I am having NPS (Tier II) and some MFs and PPF as investments. Is the plan help me for post retirement tenure ? I am more interested to get a fixed income on retirement and life insurance.

Dear Abhijit,

GUARANTEED income at what cost? Whether you considered the INFLATION to arrive at judging about this product? Buy the insurance separately for INSURANCE sake. I am repeating again, you have to consider the INFLATION before judging which one to buy.

Thanks for the clarity. My banker was behind me and was proposing this on top of their voice. Thanks that I didnt fall for it

Dear Chandramohan,

Great to know.

Sanchay plus is offering the highest return amongst all guaranteed income products available in the market. The IRR is 6.4.to 6.9 which is tax free hence the pre tax returns are around 9-9.5%. It is a shame that the so called SEBI approved advisor is publishing highly biased and non factual malignant blogs.

Dear Amit,

Thanks for your kind words 🙂 Coming back to returns, as per you pre-tax returns are 9% to 9.5%. Can share how you arrived? Your plan adding 3% to the 6% is so funny. HIGHEST GUARANTEED RETURN at what cost?

Assuming a person is in 30% tax bracket with surcharge and eduction cess etc. pre tax return will be 6/(1-.33) roughly 9%. Assuming roughly 6% tax free return from this scheme and pension is available to spouse. Please let me know if this understanding is correct.

Dear S,

I am again stressing on INFLATION, but few are JUST concentrating on GUARANTEE and TAX FREE 🙂 Only God can protect.

Are you from HDFC??? He has rightly given his view and clearly illustrated that it’s foolish to buy this HDFC plan.

Dear Naresh,

Whether he is representative of HDFC or LIC, it does not matter to me 🙂

Hi Basu,

Thanks for explaining this plan.

I am married and considering family planning now. Few days ago, I was considering this plan for getting some fix amount every year which I will utilise for my child school fees after 10 years. My goal is to have good amount from some plan every year to pay school fees annually and then for higher education.Please suggest some plan. This type of plan will work for this purpose or not?

Thanks,

Kumar Divyaprakash

Dear Kumar,

Your kid’s school inflation is more than 8% and this plan generates around 6%. Then how can you beat inflation? Either you have to satisfy with lower returns and sacrifice your kid’s goal or be ready to invest more IF YOU LOVE THIS PRODUCT. The choice is in your hand.

Thanks Basu.

Which type of investment will be suitable for child education planning?

Thanks,

Kumar Divyaprakash

Dear Divyaprakash,

If your goal is more than 10 years or so, then definitely you have to include equity and debt in the right proportion to achieve the goal. For equity, you can use the Equity Funds and for debt, you can use PPF or Debt Funds.

I really appreciate Basveraju to give clarity on this. Specially keeping in mind inflation..

Dear Sakfrsh,

Pleasure 🙂

People who are still confused about investing in Sanchay Plus…..should once sit with any authorized person of HDFC Life (Fc) to get the true picture before going in to judgement.

Dear Amritendu,

Why confusion? Why not refer HDFC Life online content to decide? Is it necessary for one to meet HDFC LIFE? I definitely know that they brainwash buyers with certain FANCY numbers.

Life insurance products should not be compared with other fin instruments,

Dear Amritendu,

EXACTLY…We have to consider Life Insurance product as a pure life insurance products only not as an investment tool 🙂

Over all , in this product segment, People want to save their Money with Guranteed Words. And I think and Mostly observed all investor donot want to take Risk!!!

In this Plan also capturing the Life protection. Which will be not cover by term plan to all….bcs for term plan always need the U/w profile. We Can’t offer Term plan to any one. So, for Saving, it is not bad option.

Dear Shashi,

Why can’t we offer term plan to any ONE??

I think Term plan does not come under investment. It is for life secure your dependents. But, here we can get some guaranteed money.

Dear Abhijit,

Who said Term Insurance is an INVESTMENT? I always say that we have to separate Insurance with Investment. Here, you get GUARANTEE money, but at what cost??

Hi Basavaraj,

This is one great post. Thanks for sharing such useful info. I have a query, I want to invest for my kid(long term) and i ma getting a gurranted plan for Kotak where i have to pay 1lakh every yr for 10 yrs and after 5 yrs i will get approx 15.6 lakhs.

Can you please suggest whether its a good plan or i can invest somewhere else where i will get good returns.

Thanks

Dear Sagar,

Features look the same as the above plan. Refer to the above images, where I have calculated the IRR. The same way you can come up with IRR returns. But as per me, stay away from such dangerous products.

Besides you have wrongly or deliberately missed up factoring in Lump Sum returns that customer gets in the Long Term and Life Long Options. Best part is that he even acknowledges that Sanchay Plus is offering an IRR of 6.9% guaranteed ,plus tax benefits and Life Cover and besides saying that only PPF is slightly better than this *means that it is best in Insurance Space*.

HDFC Group Products are always The best in Financial Industry, be it in banking, AMC, GI or LI Space.

Net IRR of 6.23% to 6.80% and after adding Lump Sum returns this adds to 7.10% to 7.93% Tax Free means that this product offers 8.91% -9.23% Guaranteed Gross returns, *means this is a wonderful product*.

No current insurance product offers such good and gauranteed return that too with life cover.

It has deleibrately calculated it on 30K, when we know that higher the ticket size higher is the return in this plan.

Sanchay plus, super product, competition ko pagal kardiyaa eis product nay*.. !!

This is the first time I have ever seen a geek increasing the calculated returns of a product because its tax free.

The way I have always seen is the return once known can reduce if there is tax to be paid. And it remains the same when there is no tax paid.

Such is the literacy in this country.

Dear Pradeep,

For them TAX-FREE and GUARANTEE only matters. How much and what is the REAL RETURN? Neither they know nor they try to understand.

Dear Manik,

Please check the above post properly. I have included the premium return at the policy maturity. I am not sure what DELIBERATE action is pinching you. 6.9% tax-free guaranteed for the long term means the BEST for you, then let God protect you in your journey of wealth creation 🙂 PPF slightly better than this plan?? Come on…. 🙂

Ha ha, as Pradeep pointed, you the only rarest of rare who is increasing the returns by adding your taxation part to return. God bless the people like you and your financial literacy level.

You show me with an example that if the premium is Rs.30,000, then returns will be less and if the premium is Rs.3,00,000 or Rs.30,00,000, then the returns will be higher. Can you please share your validation with IRR calculations?? Just throwing in the air without valid reasons 🙂

Sir with the economy growth rate and with past experiences we can assume that interest rates will definitely comedown secondly what the future govts will do regarding the ppf rates. It may change no guarantee. This product definitely gives guaranteed returns for next 25/50 years why ppl should risk their money in other instruments. Why you calling it a trap? Because the invest ment period is 10 years with life cover and tax free returns and it is a contract which cannot be changed also you mentioned about 6.9% retun..

Dear Lakshmanan,

Definitely, PPF interest is not FIXED. Definitely with the economy (If inflation stays at low), then interest rates will fall. However, do we have only such products in long run to create wealth? You are explaining as if we don’t have any other option on this earth than this HDFC product. Come on..open your eyes. Getting around 7% with the proper asset allocation for long term like 10+ years is not a big thing. This product is a TRAP because it failed to address the basic concept of INFLATION in the name of so-called GUARANTEED. I can understand your frustration 🙂

HDFC Life is making 25% profit every quarter but the people who pay premiums to them are making 6% return.

The fact that they go with ‘Guaranteed returns’ to sell this plan indicates they will not pay a single penny more even if their profits increase to 30%. Surely if more people buy this plan, their profits will go to 30%.

Oh here is a question to you. Would you work for a company that will pay you the same salary for 25 years?

Is it okay if you dont get any hike at all? I am sure you will accept it if they pay 1 crore every month but not 25,000 Rs.

Dear Pradeep,

Well said and I hope these guys understand the concept of how HDFC Life making profit at the cost of these guys who are defending.

well said

Well i would like to ask a question… Which traditional plan in market gives the return of IRR that is higher than this plan? There is no other traditional. Plans in market as such… After analyising all the plans in market for traditional i am. 100 percent sure about this. So kindly get the celredentials cleat… I have invested in other traditional. Plans in market, ehich has not given me returns as higher as this one. Ehen u say negative about something please speak positive about something too.

Dear Niks,

Do we need TRADITIONAL plans for our long term goals? If YES, then WHY? It is your mindset that you need it. There is nothing to say positive about this as the basic principle of investing of beating the inflation itself failed here. Also, do remember one thing, I will not get anything by saying EITHER POSITIVE or NEGATIVE.

It seems you are an agent of Aditya Birla Capital Life Insurance , I can understand the level of frustration you are passing through now a days, there is no better insurance plan then sanchay plus among all the insurance companies accros the country, let you buy one for yourself, plz confirm the appointment date and time so that I can arrange a financial advisor for you, who will explain this plan to you and will provide you this policy, last I request to go with higher premium I mean more than 1 Lakh so that the IRR will be around 8-9%, don’t go with 30 thousand, advice is for you don’t make people fool from your rubbish blogs,

Dear so-called XXX 🙂