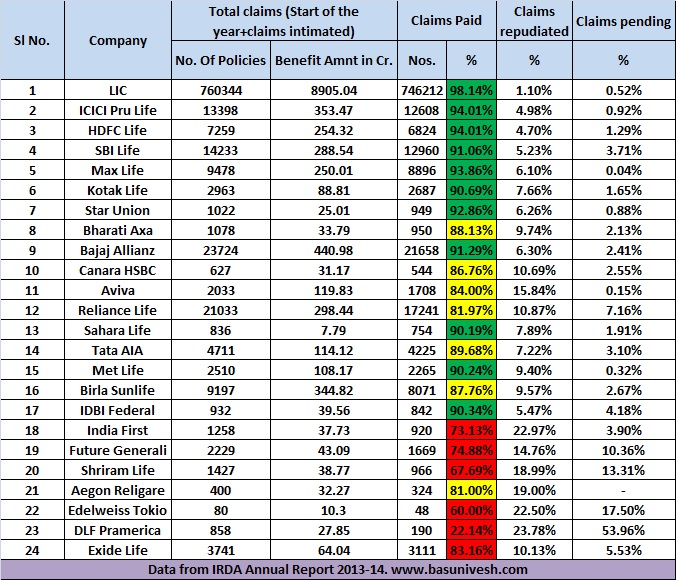

Today (8th January 2015) IRDA declared Annual Report 2013-14. This report gives you an insight into the Indian Insurance Industry and also let you know which company is top and how the rest of companies are performing.

Note-

IRDA Claim Settlement Ratio 2014-15-Which is best Life Insurance Company?

Top 5 Best Online Term Insurance Plans in India-2016

Term Insurance-Claim Settlement Ratio no more a big criteria

Below is the latest data of claim settlement ratio for the year 2013-14.

Note-I coloured with green, whose claim settlement is above 90%. I coloured with yellow, whose claim settlement ratio is more than 80% but less than 90%. I coloured with red, whose claim settlement ratio is less than 80%.

You notice that top five companies when it comes to claim settlement ratio, are LIC, ICICI, HDFC, Max Life, and Star Union. You need to concentrate on claim repudiation percentage also. Because, this clearly states the company’s acceptance of the claim it receives. Along with that, pending percentage indicates the slowness due to one reason or another.

What are the limitations of this report?

- It will not differentiate the type of products, which each company settled like endowment, term insurance or ULIPs.

- Reasons for rejection are not available.

- Usually settlement ratio increases as the company getting older into this industry. So older the insurance company higher chances of growing it’s settlement ratio.

- To add my reasoning to above point, usually early claims means the claims which are within 2-3 years of buy. Including LIC, all insurers do a strict scrutiny of such early claims. So there is high probability of rejection. If the insurance company started it’s business just 3-5 years back then it may receive all claims under early claims. So rejection may be higher. Ending this as a lower claim settlement ratio.

- No guarantee that a company which has the highest percentage of claim settlement ratio not rejects your claim.

- This data is for a year. So insurance companies either settled claims within a few days or might have taken less than a year.

Visit my earlier post “IRDA Claim Settlement Ratio 2012-2013-What it indicates?” to compare the report of previous year.

Hope this report will shed some light for you before selecting your insurance company.

I was buy a ageon life policy money back but not satisfy the poly duet o advisor worryingly advice so how can i refund my policy we have already pay 2 and half years

Mkhan-Either you have to forget the amount or continue up to 3 years and then get some part of what you paid by surrendering.

Please Provide Latest claim Settlement Ratio of FY 2015-16.

Karan-It is not yet published by IRDA.

Hi,

Thank you for notes and its very helpful guide to plan our finances. I have question regarding Term insurance, say if i am smoker and consume alcohol on weekends and by mentioning it i am going to pay extra 4-5k premium which i understand. My query is, even after mentioning that i am smoker and alcohol consumer and paying extra premium, do the insurance company has the right to reject my claim after few years or many years if incase the death is caused due to any of these reasons?

please help me to understand this clause.

Vel-They can’t reject the claim if death occurred due to smoking habit (which is already known to insurer).

Hi Basavaraj,

I am 31 year old, Non smoker and looking for best Term Insurance for 20-25 year & some investment plan for short term say 10 year for good return. I am quite confused as one of the my close relative LIC agent said that other companies might not pay/Reject the desired claim saying any other reason and you/your relative will end up saying that “would have been better if we had gone for LIC plan” Is that true? Also have one question- are these LIC policy’s customer focused or Agent focused, Whatever i have seen so far don’t think it gives greater return on investment and very little death claim. I see agents are growing in terms of wealth but not the actual customer!! strange!

Please advise me the best plan for Term Insurance & Investment with any specific company details.

Appreciate your help on it.

Thank you

Deepak-Your doubts are genuine. Your so called relative LIC agent, misguiding you. When it comes to claim rejection, private companies or LIC no one can reject blindly. All agents defend their insurance company. It is natural. Think on your own and decide. Regarding best term plan, refer my latest post “Top 5 Best Online Term Insurance Plans in India-2016“. Regarding investment, I can’t recommend anything. Because I am not sure about past financial life, present investments and future financial goals.

Hi Basa,

I am 35 years age and my annual income take home is around 5 lacs. I have 35 lacs trem plan of ICICI & 20 Lacs from Aegon Religare. Now, based on claim ratio I am confused in aegon credibility because his % is very low. Some LIC agents also told me that private insurance companies always try to hold the claim for one or the other reasons. Is it correct? Should I drop aegon religare term plan and opt for some other? then which company term plan? what should be my life cover? plz plz reply urgently.

Rohit-Don’t heed to agent’s advice. How can an LIC agent can say that competitive company is BEST? Your insurance cover must be around 15-20 times of your yearly income.

SHOULD I CONTINUE WITH AEGON RELIGARE IN SPITE ITS CLAIM RATIO % IS VERY LOW AS COMPARE TO OTHERS LIKE ICICI. CAN I STOP AEGON AND TAKE AROUND 50 LACS TERM PLAN FROM HDFC OR MAX LIFE OR ICICI ?

Rohit-If you are still comfortable with plan features and company, then continue.

try for sbi life

Hi Basavaraj,

your blog is very useful to get information about insurance policies. thank you so much.

After reading your all articles. I have decided to get one Term insurance for 30yrs & My age is 28years,.

But how to decide the cover amount 50L or 75L or 1Cr. please I need a logic for this like how you have given for policy term.

I am a IT professional with 8lakh PA income.

Vishwa-But around 15-20 times of your yearly income. To this amount, add the outstanding loan if you have any.

I am planning for sukanya samrudhi yojana for my daughter . she is 2 years old .

I have plans to settle abroad after may be 5 years . what will happen to the money that I pay for this 5 years and can I continue to pay even after I go abroad .

for example I become a NRI after I pay 10 years of amount what will be fate of that 10 years money.

RAvi-Forget about your NRI status change. First think whether this is a great product to beat the education and marriage inflation? It is a typical debt product handed in political parties. When government changes, then we don’t know the faith of such schemes. Stay away.

Hi,

My name is Gautam Shahi, age 22 years. I wanted to buy a Term insurance plan for maximum tenure i.e, 40 years but confused among ICICI Prudential and HDFC life. As i am seeing that premium cost of ICICI is more than ICICI. Apart form them all benefits are same except claim settlement ratio. So can you guide me which one would be better?

Gautam-Read my latest post on this “Top 5 Best Online Term Insurance Plans in India-2016“.

Hello Basu,

It’s nice reading your blog. Currently i am in search of Term plan for my elder brother fro around 50lakh – 1 crore. His age is 25yrs with yearly income of around 5-6 lakh and non-smoker. I have tried searching many Term plans and came down with two of them. HDFC Life & Edelwise Tokio . But I am being confused on the basis of benefits (Riders) and claim settlement ratio.

On the basis of riders :- common rider attached is Accidental Disability benefit available in both HDFC & Edelwise.

Wheres edelwise gets ahead in two cases:- Premium waiver rider and the Term plan premium amount which is comparatively less.

So, Now looking as per above scenario should i consider HDFC :- Being Trusted, High in claim settlement ratio, although it doen’t have premium waiver rider. OR

Edelwise :- Being Just new company,Low claim settlement ratio,Having fantastic riders and with Less Term plan premium amount?

Since, Term plan premium will be ultimately cost for me till the uncertain event, I was also looking from coverage part keeping to minimum premium amount. Please advise

Krunal-Don’t buy riders. Instead buy accidental insurance separately from general insurance companies. Read my latest post on my choices of term insurance plans “Top 5 Best Online Term Insurance Plans in India-2016“.

Hi Basavaraj,

First of all, I appreciate your effort in providing us with the information. I am new to this stuff. However, I decided to buy a term insurance for 1 cr. After some online research, I would like to go with Max life (50L) and PNB met life (50L). Is this a good idea? Could you suggest something better? I’m 27, m.

Many thanks in advance.

Sanjeev

I am sorry. It was actually PNB met life and HDFC. If I buy from 2 different companies, for 40 yrs term, I have to pay 11,362 rupees annually. Whereas, If I buy it only from PNB metlife, I will be paying only 8418 rupees p.a. Is it worth buying from two companies or just from PNB?

Thank you.

Sanjeev-No, stick to ONE.

Sanjeev-Read my latest post “Top 5 Best Online Term Insurance Plans in India-2016“.

Thank you Basa.

Hi Basu,

I have some queries regarding Home loan.

I have home loan with HDFC Bank and out standing amount 19lacs , and no og emi’s 144 and current interest rate 9.70%.

I want to move current interest rate 9.55% for this i have to pay conversion charges 5322.If i pay this charges no of EMI’s decreased to 141. Here nest reset date is showing 01-feb-2015.

1.Is that good idea to move current interest rate?

2.Is that right time to move current interest rate?

3.Once i move to current interest rate is always applicable to current interest rates(i mean it will always follow the RBI announced interest rate) or i have to pay once again charges?

Please advice me in detail.

Thanks,

chennaiah

Chennaiah-First let me know whether the 9.55% is floating rate loan or fixed?

Loan type is RESIDENT HOME LOAN-VARIABLE RATE-MONTHLY REST

I think it mean floting.

Is that correct?

Chennaiah-By moving to this lower home loan, you can save around Rs.23,000 on interest part for the whole tenure of period. But the cost of change itself is around Rs.5,000. I don’t think it creates much difference to you. Banks usually offer such things to lure the new customers or build their new book of loan. Don’t heed. Stick to your current floating rate loan. If the difference is more than 1% to 1.5% and the cost is same as that of Rs.5,000, then think of switching.

Thanks for your advise.

Hi Basava,

I want to purchase term plan here i concluded MAX Life, Reliance and Bharati AXA.

Among these MAX and Bharati are 35 years term where as reliance is 39 years

Let me know which is best and why.

Indra-Restrict your term insurance period equal to your working age. Term Insurance not required during retirement.

Is Term Insurance or Medi-claim worth ?? I heard that Insurance companies do not settle any of these claims easily.

They harass and comes with lots of terms and condition when claimed. They cover only natural death in term plan and only specific illness’ in medi- claim. No critical illness’ covered.

Why should than

Chittaranjan-There are many reasons for claim rejection. It may be due to hiding facts from buyer too. Many of us will think of insurance when emergency knocks our door. So we hide material facts to get the insurance at any cost. This results into claim rejection. Second point is we don’t know the exclusions or we never try to understand it. If according to you all claims start to get a reject, then I don’t think even insurance companies will survive in future.

At the other side, critical illness is a complicated product. It comes with so many restrictions and excludes, which many of us not understand and blame on insurance companies. If one has any such grievance, then there is always a way to go ahead like complaining with ombudsman or regulator. Ignorance is the main cause.

LIC has a good repo of settling claims. Rest all private players do not have the attitude to pay. They find reasons to reject your claim. They are only concerned with new premium.

Hence it is a request from all that take policy from a company who really pays your claim. Rather than private companies who puts conditions & rejects claims.

Please share claim experience with private companies, if you have.

Anil-May I know the value of each claim amount LIC settles? I think you noticed it or not. But all of them are endowment plans. So defending LIC is not worth based on claim settlement ratio.

Hi Basu,

I am planning to purchase LIC online term policy for 1 Crore. I am 28 yrs old non smoker. But compared to other private insurance companies, LIC premium is almost double. Please suggest which company I have to choose in terms of smooth claim settlement with reasonable premium.

Praveen-You can chose LIC (if you can afford), otherwise go for companies like HDFC, ICICI, Max, Bajaj, SBI or Kotak.

Basavaraj, are you a fee only financial planner? I am looking for a fee only financial planner based in Bangalore.

Venky-Sorry, I am not a Fee-ONLY Planner. You may find few from SEBI portal.

Hello Mr. Tonagatti,

This is a very resourceful web for the beginners like me. Plz help me out. I am a Govt. employee (Age 26) and want to invest 3000/month or sum total annually for 3 years targeted period, then which will be the best economical options for return? Can I get tax savings facility from that? plz suggest.

Shubhadip

Shubhadip-Use RDs or Bank FDs for your short term need. No, you will not get any tax benefits from this short period investment.

Hi Basavaraj,

I am purchasing term insurance with Max life, worth 50 lacs, age limit of 70 yrs and per yr premium of 6927.

Believe MAX is not a indian company and might have some agreement with indian counterparts?

what if there might be any issues between MAX and indian counterpart and if nominee has to get compensation, who would pay ?

I am sure IRDA has systems in place.

Could you kindly explain?

In what circumstances insurance companies will not pay nominee. Please explain this also…

Regards Sachin

Sachin-Please read my earlier post on the same “What if your Insurance Company goes bankrupt?“.

Can you tell me are these ulip plans are really good for our investement.?

Rohit-To me NONE.

Very Nice blog !. I wish i would have read your blog earlier ! Stuck in ULIP from last 4 years. Although premium is only 15k which is not much but i could have done something else with those 15k and still could have earned tax benefit.

Saumil-Pleasure and thanks for sharing your concerns.

Dear Sir,

I am 41years old with wife and two kids. I read your blog regarding the “Claim Settlement Ratio’ and I would like to seek a clarification. I am an NRI and my yearly average income is Rs:15 Lakhs.

I would like to join 2 Term insurance plans, ie 50 Lakhs sum assured in one company and 75 Lakhs some assured with another company. Now my concern is if I join two tern plans together, whether my nominees can get settlement from both companies or only from one company? At a time whether its permissible to get settlement from both term plans for same person’s nominees? How many term plans one person can join? If I join two term plans, should I declare to both the companies that I joined two term plans?.

Kindly advise,

Regards,

Loyit Mathew.

Loyit-You can have as many number of term plans as you wish. But there is no logic in splitting your term insurance. However, if you decided to split, then you have to buy the first term plan. From second plan onward, you have to mention the existing insurance without fail. If you do that, then I don’t think your nominees will face any issue.

Hi Basavaraj,

All insurance companies have different premium for smoker & non smoker. Suppose I buy a policy for 35 year and declare non smoking. My question is currently I am non smoker/non tobacco user. After say 10 or 15 year I start smoking or tobacco or start consuming alcohol. If i die during policy term will there be any issue in claim settlement?

Mayank-No issues as they ask only during issuing the policy.

Are you sure?

Vignesh-YES.

Very nice information. I am adding following clarification just for the benefit of the readers.

As per my information, you have to inform insurance company if you develop a smoking habit later. This may have some effect in your premium but this will ensure that your claim is not rejected later.

See PNB MetLife FAQ’s : https://online.pnbmetlife.com/meratermplan/LandingPage.aspx?UTM_Source=Landingpage&ID=3

It reads :

What if I develop a smoking habit after buying the insurance plan?

We have a term policy of 40 years and since it’s a long time, a person may develop smoking or drinking habits during that time. We urge you to disclose this fact to us as this will reduce your chance of a claim being rejected at the time of maturity

Abhay-Thanks for your inputs.

Hi,

Very good useful info provided. I have one question please let me know while choosing term insurance i should see claim settlement ration or the premium for example

kotak term insurance claim ration 90% where its premium is around 10k for 1 cr

hdfc term insuance claim ration 94% where its premium is around 13k for 1 cr

90% and 95% is really that much matter in future years it may change both companies are good i was thinking kotak is better to take as premium is less. pls let me know what other factors shd i consider?

Sharan-It does not matter and considering the recent amendment, claim settlement ratio not that a big criteria to chose the plan.

is there any problem to purchase on line HDFC LIFE insurance . Once policy is purchased , whether co. can make any objections in claiming? if yes what type of objections.

Deepak-There is no problem with HDFC as long as you declared all facts properly. Problems in claiming depends on case to case. Hard to say any such generic issues.

hello sir,

i am 43 years old and i want to buy term policy but i am confused between PNB Metlife and Maxlife since in pnb metlife cover is till 70 years and maxlife cover is till 75 years whereas the premium is same for both. kindly suggest

Hi Sir,

this is a different question all together, I want to become an Life Insurance Agent (not health insurance). I want to choose from ICICpru,Max and SBIlife.

What should be my criteria for choosing the company ? i think one criteria is certainly the Familiarity of the Company in public.

Kindly suggest

Thanks

Anand S.

Anand-Yes, in that case LIC hold’s first and then ICICI.

hello sir im 31years and want to buy term plan.

im confused between hdfc and max life. premium difference is only 2000 for 1crore policy.

should i go ahead with maxlife or hdfc which one do you refer.

Suresh-For me, both are fine. Act immediately and buy anyone.

thanks expert for guiding me . i have bought max life.

now looking forward for some mutual fund purchase.

Hi Suresh,

How was your experience with MaxLife? I am also planning to buy term insurance plan with them. Please suggest.

Hi Anand, experience will always be great while buying any term plan from any company. Issues and problems occurs only at the time of claim. 🙂

I would suggest if you want to buy 1 crore plan then you can consider to split between to like for example : take 50lakhs from max or etc and another 50lakhs from hdfc or icici / etc . you can choose any reputed company. i would suggest full lump sum payout in one time only.

Thanks,Suresh

Suresh-Any logic in splitting, especially after recent modification to Sec.45 of insurance act?

Dear sir

I m 27 year old.

I have aviva I term plan of sa 5000000.last two premium had paid.this is my third year. but I got a call from policy bazar nd they told me abt the claim ratio of aviva.and he advised me to purchase max life insurance bcoz they willsattle claim in just 10 days and aftr 2014 dec yheris a rule jisse jo policy dec 2014 k baad purchas krengeor usko agr do saaltk run krenge to claim reject nhi ho skta…. skta…I thought max life insurance is better than aviva so I purchased it.on 25sep15…but nw I am confused. ..my decision is correct to buy max life insurance or not….plz help…should I continue the aviva life insurance and cancel max life insurance since I hv not received bond pappers yet.

Aashi-Cross question-What guarantee the policybazaar guy will give you that the concerned person or the portal itself will be there when the actual claim arise? They don’t have any such set up to help you by handholding. Their concern is to SELL and EARN commission by selling SPECIFIC few online term plans. It is all sales gimmick. If you are comfortable with Aviva, then continue.

thanks for the fast reply.

Sir now please advise should i cancel max life insurance bcoz i have already paid the premium but i have not rcvd the bond of max life insurance policy and plz let me know the procedure to cancel this and request for refund.i have made the payment to purchase max insurance on 25sep15. i feel like cheated by policy bazar. please help me..i really need your advise.

one more thing i want to share with you when i purchase aviva ilife they said medical is not required.

i hope there wont be any problem in case of claim.

Aashi-If your Aviva is still continue and you no longer need this MaxLife, then better to cancel. You can cancel it during free-look in period (within 15 days from the date of receipt of policy document).

First of all sorry for the so many questions.

my aviva premium is overdue by 10 days.should i pay the premium of aviva and wait to receive max life insurance policy pappers and only than i can cancel the policy or i can cancel it right now.

how much time it will take to refund my money.i am really tensed, my money got stuck bcoz of my foolish and hasty decision.:-(

Aashi-Don’t wait, pay the Aviva premium. If you get the MaxLife and dedicded to retain MaxLife over Aviva, then cancel Aviva. In my view, it takes around 5-10 days to get back the money (They deduct the medical examination cost and the tax paid).

Last question sir,

Since I have both option…pay aviva premium and continue it or retain max life insurance.

I want to stick with the good and reliable insurance company coz I bought it to secure my family future.

According to you, should I stick with aviva or max.

Aashi-To me both are equally GOOD and BAD. Hence, you already have Aviva, stick to it.

Hello

I plan to take a term insurance for myself and one in my wife’s name. Both of us are earning members. I am in merchant navy and my residential status is NRI. My wife is a resident Indian and we both reside in India.

My query is as follows

1. Can I get a term insurance . Will me being a mariner/NRI have any issues on getting a term insurance ?

2. Which are the companies providing term insurance for people like me.

Thanks

Ajay-1) Yes, you get term insurance and there are few insurance companies which offers term insurance to NRIs too. So no need to worry.

2) There are many and few of them are like HDFC, ICICI or Max Life (few to name).

Myself too a person from merchant navy – NRI. Kindly note that only 2 companies are providing term cover for merchant navy people – Maxlife and Aviva. — means they cover onboard ship also ,means if any mishap happens onboard while in international waters also. whereas other companies issue for NRI but have various limitaions like it wont cover for persons working in military,merchant navy etc.etc.

So comparing Aviva and Metlife, I took a term policy from maxlife.

SO before taking any term policy, kindly confirm with the company’s highermost official you can about claims if happened onboard at open sea.

Gowtham-Thanks for sharing your experience.

Dear Sir,

My friend’s mother got expired due to brain hemorrhage. She had various policy from bajaj alliance, kotak and LIC. Is this considered as Accidental death?

Bajaj alliance is saying we can pass claim only and only if you can provide P.M report. They have not gone for P.M report because they are informed that it can much time. And at that critical time, relative pressure to wind up procedure is too high.

They have certificate from local doctor giving death cause.

Kotak is also asking for P.M.

LIC they have not started process.

Kindly suggest what can be done?

I want to go for term insurance. I am confused to choose company. I think LIC can be better as they are not asking for P.M report after 3 yrs.

Other private players they ask for P.M report if death is from accident(they know by other document that person is dead then why they insist P.M report? they should give normal death benefit). and doing P.M is tedious and time taking task.

What should i choose? LIC or other private player? confused…

Mehul-Your mother’s death is not considered as accidental. Hence, it is normal death and claim can be settled with usual process. I don’t think PM report is required.

Hello Basavaraj,

I am 31yrs and married. I am planning to buy term plan of Rs 1 cr. Could you kindly suggest me between PNB Metlife and Max Life. I will be taking it for 29yrs.

I have one more doubt , should I go for annual premium payout or one time premium payout.

Thanks,

Ravi

Ravi-Both are good. You can chose according to your comfort. In my view premium payment of both like yearly or lump sum have their own advantages and disadvantages. Better you go for annual premium.

Thanks alot for your inputs. That’s pretty fast reply. Much appreciated. I was expecting your reply by Monday 🙂

I will go for annual premium. But I have one doubt about MaxLife. were they able to last for 3 or more decades. in India.

I think PNBmet life can also survive.

Other major like : HDFC, ICICI, SBI, Bajaj are sure shot lasting companies.

Ravi-Read my earlier post on this doubt “What if your Insurance Company goes bankrupt?“.

Thanks for your reply.

Just one more doubt about rider options in policies.

Ex. :

1 case : Mr. ABC took term plan of 1Cr. without rider option and he passes away in accident or critical illness

2 case : Mr. XYZ took term plan of 1Cr. with rider option (25lalk) and he passes away in accident or critical illness.

Ans. 1 case : Family of Mr. ABC got only SA of 1 Cr.

2 case : Family of Mr. XYZ will get SA of 1 Cr plus rider benefit amount 25 lakhs.

is my understanding is correct about it.

However I called up PNBmetlife and asked them about rider option. But they told me that this option is not available right now they are seeking IRDA approval.

But Maxlife have this option. There call is disconnecting with me. I will try tomorrow with them.

Ravi-Your understanding is correct.

thanks Basavaraj for your expert advise.

I am taking Term plan now. It’s great for risk coverage .

I will be getting 1 cr. cover for just 7500 / yr.

Now I am planning to exit from my LIC Jeevan anand 149 which I am paying from last 4 years. around 21000 / yr.

So remaining amount I will put in Mutual Fund large and diversified.

Ravi-Go ahead.

Sir i am 34 years old i take sri ram life insurance policy But i am not satisfied plz details this company is under irdai and i believe this company.

Krishna-If you beleive this company then go ahead and continue.

Sir,

I’ve purchased 1crore term policy from max life on 23.9.15. PNB metlife premium is Rs.8972 & max life is Rs.9006. Did I do mistake by taking from max life. I’ve seen claim settlement ration 95.5% from max life. pls suggest as I need a correct insurer. Is PNB metlife better option than max life.

Madhusudhan-Will you change your policy if after sometimes X company offers it at Rs.500? No, it is not like that. You bought it and if declared all facts properlty means no need to worry.

Mr. Madhusudhan can you elaborate about the medical tests conducted by Max Life? Was the cost borne by you?

Hi Basavaraj,

Thank you so much for providing relevant information regarding various insurance providers. I just wanted to check if there’s a reason Apollo Munich is not mentioned in IRDA data, I hold Apollo Munich health insurance policy and I would like to change in time before its too late.

Thanks again for all your help.

– Shweta

Shweta-The above list if only for LIFE INSURANCE COMPANIES. You can check for health insurance companies at my earlier post at “IRDA Incurred Claim Ratio-How to choose the best health Insurance?“.

Hi Mr. Basavraj,

We are planning to take a home loan. Which would be the better option to cover the same i.e Pure term insurance or loan insurance?

My husband left smoking 3 years back. Where we should put him i.e smoking and nonsmoking category?

Kindly , suggest a good term insurance plan with permanent disability and critical illness option.

Regards,

Rupali

Rupali-The advantage of loan insurance is that the premium start to reduce (in pure term insurance it will be constant). Hence, I suggest a loan insurance, but not strictly with bank. You can check with other insurers and go ahead. I know banks may insist you to buy the product with them ONLY. But it is not mandatory to buy with them. Hence, buy separately. At the same time, disadvantage of loan insurance is, if in future you want to buy an insurance for your own then premium will be high. Considering both views, decide on your own. If he left the habit 3 years back and in future no plan to continue, then mention as non-smoker.

Hello..

First of all, Kudos for a nice article.

I have one query. I am 26 years old and soon will be 27th by Sept end. I am planning to purchase a Term Life Insurance before I turn one year older.

I am looking among LIC, HDFC and ICICI as they have good claims Paid Ratio. I request you to please let me know if there are any other factors as well apart from premium and claim ratio, while checking for Term Insurance.

LIC’s premium is too high when compared with HDFC or ICICI but its Claim Paid Ratio is high too. I don’t want to invest blindly and then live falsely thinking that I am insured. What are are the factors for claim rejection? And is it wise enough to prefer private companies over LIC ?

Also, is there any category of death too for claim rejection? And one more thing, can I get option for some disability (For Precautionary cause) along with the Term Insurance Plan ?

Please guide me.

Very Very Thanks in advance.

Ankit-You can go ahead with the selected insurers. There are million reasons for death and the million reasons for rejections. Thre is no difference between LIC and private insurers. So no need to worry and just go ahead declaring all facts properly. Disability options not available with pure term insurance.

Hi Basavraj,

I am looking for a life insurance with montly returns also it should come under 80 C.

Some of the agents suggested that Bharti AXA insuarane,details are below

1.Premium-1,00,000/year*180 months(15 years)=18,00,000

2.SA-18,00,000 i.e(10,000 per month for 180 months) after 15 year till 30th year

3.total 30 year [email protected]%on SA=24,30,000(81000*30)-received at 30th year

4.terminal bonus @20%on SA=3,60,000-received at 30th year

Toatal benifits=45,90,000

Shall I go for this plan and do you see any loopholes in this?

Also i see that the Claim settlement ratio for AXA is 88.13%

Can please suggest about this or any other company which has same plan

Regards,

Bishwa

Bishwa-First make up your mind like whether you need INSURANCE or INVESTMENT? I am not the fan of mixing both these. Whatever the plan you shared, will provide you a return of around 4% to 5%. If you can then go ahead.

Sir I am 30 year old and purchased a term plan of Max New York Life of SA of Rs. 50 lacs today itself. In case of mishappening they will give Rs. 20000 for 10 years for Rs. 6783. Sir, Is claim settlement ratio, Average Claim Settlement Time, Financial Background like Solvency ratio, Trust factor of Max Life Insurance is good or not? we all feel that our family should have less hassles and claim process should be simple. It does not have any riders also. Can I return the policy of Max New York life and purchase another one. Plz suggest me if my decision of purchasing max life if right or wrong..

Rajeev-Whether it is Max New York Life or LIC, all are equally good and bad. Because they are all into business.

Sir, as per claim settlement ratio, Average Claim Settlement Time, Financial Background like Solvency ratio, Trust factor of Max Life Insurance is a good option or not? Or some better option can be there?

Rajeev-Go ahead.

DEAR SIR,

I have one term policy with 80 lakh sum assured with Aviva last two premium given.

Now I want to know that Aviva is how much reliable for term policy. And what is govt. guideline for it.

Thanks

Vineet-It is equally reliable like LIC or any private big companies.

Non-Disclosure: Section 45 of the Insurance Act, 1938: No policy of life insurance

effected before the commencement of this Act shall after the expiry of two years from the

date of commencement of this Act and no policy of life insurance effected after the coming

into force of this Act shall, after the expiry of two years from the date on which it was

effected be called inquestion by an insurer on the ground that a statement made in the

proposal for insurance or in any report of a medical officer, or referee, or friend of the

insured, or in any other document leading to issue of the policy, was inaccurate or false,

unless the insurer shows that such statement was on a material matter or suppressed

facts which it was material to disclose and that it was fraudulently made by the

policyholder and that the policyholder knew at the time of making it that the statement

was false or that it suppressed facts which it was material to disclose.

Sir what it means, i taken from hdfc website

Rakesh-This states that insurance company can’t question the statements or information you DISCLOSED during policy buying after two years. But they have the authority to question any such information which they feel “material matter or suppressed facts which it was material to disclose and that it was fraudulently made by the policyholder and that the policyholder knew at the time of making it that the statement was false or that it suppressed facts which it was material to disclose”. Hence, disclosing all facts properly is the solution.

Thank u very much sir,

but if policy holder do not know that, in inner part of body, what type of disease he or she suffer, because he do not know the diseases that in his body and insurance company also go for the policy holder medical test and medical test also give report of no disease after taken of 2-3 years he his suffering from any disease and got death then sir ji what happen.

Rakesh-Any disease which they come to know that it was not there during policy buying, is considered as true disclosure. But some people try to avoid headache of rejection or loading premium.

thanku u very much , your suggestion is very useful for any buyer, such kind of help is priceless, god help u sir

sir is there is any guideline of IRDA, for the completed 3 years term policy for the claim settlement ratio.

sir i want to purchase click to protect from HDFC, is there is coverage of suicide, earthquake, floods , or rights

which insurance company provide maximum maturity year in term policy.

sir, i am self employed person, in 2015-16 Assessment i filled ITR of 9 lac but if my business get declined, if my income get low then, is there is possibility that insurance company deduct my SA. for not change.

how much i am eligible for term insurance, how they calculate eligibility for term plan

Rakesh-What guidelines you are looking at of 3 years term policy? maturity amount in term policy?? They look for your income only during buying. Hence, if your income decrease in coming years, then the policy will continue and they not reduce the SA. Eligibility of term insurance depends on company to company and your data. I can’t say that.

Thanks Sir for your suggestions,

Sir i want to know, one of LIC agent told me that, if term policy is enforce three years, then the claim rejection chances is very low, they consider claim.

Rakesh-It depends on case to case. You can’t generalize all cases.

hello sir , i m planning to buy a term insurance policy but bit confused between aegon religare i Term insurance plan and pnb metlife Mera term plan, which is good for me ? my annual salary package is 5 lakhs and i want sum assured 50 lakhs and policy term 25 yrs

I m 33 yrs old and i have one kid of 2 yrs old .

please suggest

Bhushan-How you arrived at these two plans?

I have a ULIP policy and an accident policy. Now since I have fathered a child I wish to secure his future by taking a term policy. The issue is that I have had a history of seizures . Is it essential that I disclose the same? My fear is the insurance company might reject my application and that might impact any subsequent application for a term insurance policy. What is your suggestion on this?

Das-But hiding may terribly impact your dependent if they reject the claim.

Dear sir,

I am a serving army officer presently posted in West Bengal. I may be posted in disturbed or border areas or go to war if/when declared.

Is death during military operations, war or counter insurgency operations, aid to civil authorities during natural calamities covered in term insurance policies being offered by various insurance companies. Are there any specific exclusions pertaining to death while on military duties.

Satish-They will inform you about this during buying of a policy (considering your profession). It depends on company to company.

Hi,

Can please brief your views on NPS I got mail like this

Life’s best journey start after retirement. But only when you’ve secured a wealthier future for yourself.

Invest in National Pension System (NPS) – A Government of India Initiative

What’s more you get additional tax benefit of up to Rs.50,000 a year under Section 80CCD 1(b) which is over the limit of Rs. 1.5 Lakh under Section 80C of Income Tax Act.

Highlights:

Regulated by pension fund Regulatory and Development Authority (PFRDA),Statutory body by an Act of Parliament

Minimum annual contribution of Rs. 6000 a year

Choose out of 7 Fund Managers

Choose your allocation between Equities, Govt. Bonds & Govt. Securities

Start getting pension after age 60

To know more Click Here

Bajaj Capital has been granted Certificate of Registration to act as Point of Presence by PFRDA.

Regards,

Bajaj Capital

Chennaiah-What about the taxation of withdrawal? It is taxed in future according to your tax slab. They wisely neglected that part and this how the products sold 🙂

Thanks for your replay.

I have small query. I have home loan(with interest of 9.95%) some times i am paying prepayment of principle amount also.

1.I have planning to put some fund to Mutual funds instead of paying prepayment of principle amount

Is that Good idea?

Please Advise me.

Chennaiah-What if you get return less than 9.95%?

Dear,

my Age is 31 yrs. And i have a term plan of Rs 50 lac. can i buy one more term plan of rs 25 lac. what is eligible criteria as per IRDA & what is required income for that.pls tell me.

Jain-You can buy and the eligibility and all other income criteria are same as was during your first buy.

I need help my husband had purchased HDFC Life policy 7 yrs back we have paid all the premiums regularly. My husband expired in june we put in a death claim. HDFC Life gave me my premium paid so far with 4% interest but the bonus which was declared has not been given . They are not even giving me a break up had mailed them repeatedly but they are not responding pls help me to know how i can get my money.

S Modi-Can you provide the product name please?

Hi Basavaraj

I am currently 29 yrs old and planning to purchase one term plan also want one term plan for my wife. she is housewife. should i go with which company please suggest. i have checked 2 company Maxlife and PNB metlife.

PNB metlife recently launch term insurance as my knowledge so should i go with them or you suggest any other company or policy name. term plan should be 35 or 40 years?

Vijay-If your wife is not an earning member then no need to buy term insurance in her name. Because no one is financially dependent on her. If plan features are suitable to you and premium is within your budget then go ahead with PNB. Term of plan should be up to your earning age.

Thanks,

Can i go 1cr with max life and 1cr with Metlife or 2cr with same company.

Dear Basavaraj ji ,

Namankara ,

Sir , I am a 53 yr old working in pvt.sector & getting gross amount rs. 7 lacs per annum (3.5 lacs salary & 3.5 lacs as travelling expenses ). Can you suggest me which company’s basic term plan I must purchase which must be most reliable & @ lowest price tag..

Paramjeet-Reliable and lowest are one and opposite 🙂 You can chose from the big players like LIC, HDFC, LIC, SBI, Bajaj or Max.

Kudos to your effort guys:) I need some help.

I bought a term plan from HDFC(Sum assured 1 cr), first they did not contact me for any medical and all when i started telling them to return my money, they are saying we will see medical is needed or not in my case.

Question is

1) if the company is saying we do not need medical how should I force them to do it?

2) still if they are not doing it how should i get a proof from them that they asked me its not needed.

3) I have declared my habits (Smoking and drinking) also my family history very well, do you think is there any thing else i should tell them?(This question comes because they are not doing the medical)

4) I missed to inform them one detail of my family history while filling the online form, will they consider it now if I send them the same in a mail?

Hi Basavaraj,

I am 28years old , married & have a 1 year old kid , To secure his future I have opted IMaximize child plan by aegon religare . I am not aware that much & as the agent suggested me it better then any other plan I have chosen this . yesterday I have seen the claim settlement ratio for last two year . Please suggest as just one month back I have bought the policy , should I continue or withdraw the same . Please suggest about the company future & plan performance also.

Thanks

Rakesh-Forget about claim settlement, the product which bought by you is combination of Insurance+Investment (which are not good for investment). Hence, you can cancel the policy within free look in period (within 15 days of receiving the policy document). Go ahead and cancel and at the same time, buy term insurance to cover your life risk immediately.

Thanks Basavara for the suggestion , I have proceeded with the same , can you please suggest which term insurance plan will be good .

Rakesh-I already wrote a post “Best online Term Insurance Plans in India for 2015-A comparative list“.

Sir ji

i want to buy a health insurance. only think i need is claim settlement if somethng happens (apart from death) in any hospital in india. i have a lic plan and a term plan also. so i have life insurance but now searching for a health plan.

Hi Basavaraj,

Myself Umesh, I am planning to take family health policy from Star health insurance. The guy explained me about policy i.e. 7,200 for 2 Adult and one child coverage 6 Lac and one more he told 9200 i.e for 10 lac.

Can i go with first one or 2nd one. Star health insurance is good one?

Let me know ASAP.

Thanks,

Umesh

Umesh-Without knowing the product names how can I suggest you?

Hi Basu,

I have a query about eligibility for buying life insurance product. At the outset, I would like to highlight that I have extensively studied websites of various insurance providers and IRDA before writing this post as I could not find answer to my doubt on online resources of any insurance company or IRDA. I have also approached life insurance companies for clarification, but they come up with a standard answer which is not applicable to my resident/citizenship status.

I am a foreign national and OCI. I am currently living in India thus I am a resident individual. Eligibility conditions for Life Insurance policies cover only 3 conditions: Indian Citizens, NRIs and OCIs living overseas. For example LIC website says” “Welcome to NRI Centre. We have made an attempt here to furnish important features applicable to Non-Resident Indians (NRI) and People of Indian Origin having foreign nationality and residing in foreign countries. (PIO)”.

However I fall in the fourth category: I am an OCI living in India. Could you please share your knowledge on eligibility of OCIs living in India as far as getting a life insurance policy is concerned?

VB-In my view yes. Because your status is OCI but you are staying in India. However, give me some time and let me check with few more experts. You can mail me at [email protected]. I will reply within a day or two.

VB-I got a confirmation from experts. As you being OCI and staying in India, you can buy insurance products considering as Indian Citizens. So go ahead.

Dear Basavaraj,

I am an OCI. When i’ve approached HDFC Life for a term policy, the online agent said they don’t offer term policies to OCIs. My suspicion is, the agent did not know the rules and simply shunned me.

I have all the documents like PAN, Aadhaar, etc. Should i just apply with those and not specifically mention my OCI status? One concern is that, though i am able to get the policy now, if at a future date my family were to raise a claim, the claim may be rejected because of my OCI status.

Appreciate your guidance.

Regards!

Satya

Satya-Instead of calling, write a mail to HDFC mentioning your OCI status. Let them confirm. Then you can move with OCI status ONLY.

Hello

Please advise a reliable health care insurer for coverage of me, wife and 2 kids . Age 46,W-44,Son-16,Daughter-12

I have a policy from New India but premium is now 20000 approx for coverage of self,spouse 4.75L, children-4 .

I am finding this premium (20000) to high. and my policy is from 2004 with no claim anytime before.

Pl also advise if family Floater will be cheaper and if it is possible to migrate the policy to another co (if a better option exists) . The policy renewal is due on 27-Aug-2015. I am ready to reduce the sum Assured to 2 L .

Thanks

Daniel Mascarenhas

Daniel-I feel it is costlier one of what you already have. You can use the option of portability and move to some other insurers like Star, Apollo, Max or Religare. Don’t reduce sum insured.

Dear Basu,

I am a Govt. Servant in Delhi and I am 53 years of age and I want to buy Term Plan. The following queries may please be clarify:-

1. Is it right time to buy Term Plan for me for a period of 17 years at this stage?

2. Pre Medical Facility are available in any Term Plan for consider sun assured.

3.I will avail retirement benefits from the Govt. then Term Plan can be benefited to me at this stage.

4.Kindly suggest any other Insurance Plan at this stage.

R.S.Bisht

Bisht-1) It always right time if you want to cover your risk. But restrict your insurance need up to your retirement start age.

2) Term Insurance is Life Insurance but not Medical Insurance. Hence, no such facility available.

3) Retirement benefit is different and term insurance is different. Why you are linking both?

4) I suggest you a plan up to the age of 60 yrs only. Check the insurers who can offer you at this age.

Hi All,

I’m planing to buy a term plan from HDFC I have few questions about that.

1) What kind of death will be covered? will they cove (Natural\Terrorist Attack\Accident\Illness)

2) If death happens in 1st year your policy you will not get any claim.

3) What if insured wants to go for organ donation and something happens in future because of that will the nominee get anything.

4) Is it there responsibility to figure out what all the disease I have (Of course I will declare if I smoke or drink) there might be some hidden problem which i’m not aware of as of now but that may cause something in future.

5) Why its important to tell them the history of our parents ? if its important to tell them should I mention every single detail about them?

6) What if anything happened to my grandparent brother do i have to mention that also.?

Kiran-1) Usually all term plans cover deaths like natural, accident or illness. Regarding some specific deaths, you have to check with particular company. 2) Forget in a first year, if death occurs the next day of proposal acceptance, then insurance company must settle the claim (provided the claim must be genuine).

3) Yes.

4) There are million reasons for death and each can be examined by the insurance company. It will be run on faith. Hence, you must disclose the facts properly.

5) History of parents required to judge your health.

6) What happen to mean?

First for all big thanks to your patience 🙂

Means I should consider my immediate blood relatives like my Father Mother Grand Parents siblings..

What about if some illness was there for some of your Grand parents siblings do we need to mention that as well?

Even some times your parents had some illness long back(Before your birth) and now its cured should we mention that as well?

Sounds strange but insurance companies have lot of reason to reject your claim 🙂

Kiran-Grand parents not at all required. No need to mention the diseases which are not in repetitive or will be with them for life (like diabetic, BP or heart issues). Yes, they have millions of reasons to reject. Hence, you have to be cautious.

Please provide suggestions actually i have taken the LIC jeevan anand policy (lack of awarness)with my name(sum assured 15 lacks with half yearly premium 288841) my spouse name (8 lacks sum assured with premium of around 23k) And i have taken home loan recently also with interest rates(9.95%) .But i came to know that lic providing on that final maturity with 5.5 % interest . Because of that i want paid off those policies .and i want to take one term policy instead of those .Other than those policies insurance coverage 22 lacks is there. My annual package is 9 lacks and I want invest where i will get more than my home loan interest

Chennaiah-You are asking me about your insurance doubts and at the same time asking me the investment idea which can give you the more return than home loan. Please clarify your doubt once again.

Thanks for your replay. Yes your correct.If paid off those policies is benefit able(old jeevan anad) for me or not.Please give on suggestions Good investment and more than home loan interest.I am planning to take hdfc pure term insurance policy 1cr.Is it GOOD?

Chennaiah-You can go ahead with HDFC. But suggesting you best investment based on many data from your end. I can’t blindly suggest any investment.

Thanks for your reply,

Please let me know old jeevan anad paid off T&C value if you know.

I am planning to invest on mutual funds i have done some analysis on this i observed the earned rate is around 24%.Is it true ?.While exiting mutual funds how much tax they will charge .Finally how much we will get final . I am not looking for tax saving purpose .I have planning to invest some amount short term and some amount on long term.Funds india suggested following equity plans Mirae Asset India Opportunities Fund-Reg(G)

Franklin India High Growth Cos Fund(G)

UTI Opportunities Fund(G)

SBI Magnum MidCap Fund-Reg(G)

.As per my knowledge equity are very risk.Shall i go for some amount on equity and some amount on mutual funds .Please suggest me Good mutual funds plan and equity plans

Chennaiah-paid off terms and conditions means? Which analysis showed you 24% returns? Can you share the same? When you invest in equity funds then it is tax-free after a year of holding. Equity is risk when you not understand what you are doing and invest for short term goals. What do you mean by some amount on equity and some on mutual funds? I think you totally misunderstood the basics. First read what are mutual funds and their types. Then we discuss further.

Thanks for your replay. I will read .I will let you know my understands.

Hi Basavaraj,

I am 29 years. My wife is 28 years. We both want to go for a term insurance of 75 Lakhs for 35 years. I researched a bit and narrowed down to MaxLife and Kotak Life insurance plans, as they have good CSR, Solvency ratio and low premiums. Could you please suggest which one of these two will be the best? And also let me know if both of us should go for same insurer or different ones?

Thanks

Das-To me both are good and you can go ahead. Also, there is no harm in having insurance from same insurer from both of you.

I am planing to buy HDFC CTP I have one doubt..what if i’m planing to stay abroad for 10-15 years than come back…meanwhile if anything happens there in such circumstances will my family will get claim?

Amit-Yes, but you have to inform insurance company for your abroad travel and stay.

What channel i have to use to inform them? is it through email or in writing? will i get any acknowledgement for that?

Amit-Better through e-mail.

I have a policies if lic jeevan anand and money back policies from the same now for a sum assured fir 25laks and 15laks now I want a term policy for sum assured 1 crore which policy is good is hdfc sampoorna samvurdhi plus is good or there isany other policy… let me know

Muni-For your information, HDFC Sampoorna Samridhi plus” is not a term plan but a typical endowment plan like Jeevan Anand. They are misguiding you.

sir

please help me about term plans

i m 23 years old and want to take max life cover

i want to go with aegon religare 75 lac. insurance @6048 per annum.

is this ok or i will try to another company due to csr,

also is term plan covers me to 75 yrs but i will retire at 60 .what will happen then to the premiums.

is it necessary to be salaried after retirement ,im confused plz help.

Saumendra-You can go ahead and disclose all facts properly. If you are planning to retire at 60 years then term insurance cover must be sufficient up to that age.

SIR

IS IRDA HELPING ON CLAIMS IF NOT MADE WITHOUT ANY VALID REASON AND SHALL I GO AHEAD WITH AEGON RELIGARE.

Saumendra-IRDA is not claim settlement body. But it act as a regulator exactly like RBI to Banks.

i m going with aegon religare .they r saying there latest claim settlement ratio is 97% is this correct.

Saumendra-Check the latest claim settlement ratio from above post and this is the reality. If you have doubt then you can cross check with IRDA.

I am planning to take HDFC Click 2 protect plus extra life option term plan. Sum Assured 50 lakh. term 30 years. including accidental death and permanent disability rider,total preminum is Rs 9513/- annually. My DOB is 15th Aug 1987. Is it a good plan and decision ?

Do i need to take any other accidental insurance ? Please suggest.

If necessary then please suggest few plan ?

Kumar-Never run behind fancy options available in term plans. Buy a pure term plan and separate your accidental insurance needs.

Thanks Basavaraj.

Out of HDFC,ICICI,Kotak and Max, which one should be preferred for pure online term plan?

Kumar-I prefer ICICI, then HDFC and finally either Max or Kotak.

I have purchased ageon religare iterm plan with critical illness rider in december 2014 under non-smoker or non drinker category.

As of now I am non smoker and non drinker. but nobady knows about future, if my good habits turns into bad habits means I starts drinking or smoking . what would be effect of this in my term plan?

Ashwani-You get the claim. But being good on your own is good for your FAMILY too.

My apology for writing your name wrong (Bhavesh) Mr. Basavraj

Dear Bhavesh,

Pls suggest that i should take my health policy through on line portal like policybazar or coverfox or directly through company. Which way is better and why ?

Does on line portal are actually do after sale service and really helpful in claim settlements , documentation and all.

Gaurav-In my view better to go through an advice. Because, in health insurance it is the agent’s presence during the emergencies required most than online. Hence, avoid the online portals.

What if the Agent is no more ? , like in a matter of 20 + years how we are sure that the agent will be still there in service ?

hi, pls suggest ur view on tata aia life insurance maha raksha supreme term insurance, i like to go off line this term insurance bcoz

1. they cover upto 80 years and premium is very less comparing to others

2. 50% sum assured they are giving if diagnosed critical illness

3. tata group 75% share

ur suggestion wl very helpful for me. thanks in advance

Govind-1) Term insurance up to 80 years not required. 2) It is a rider and it charged in your premium. Hence, don’t think it is free. 3) So what?

Dear Basavaraj,

I’m 34 year old non-smoker and planning to take a term insurance for myself and wife(she is working).I have got an option as ‘iSpouse’ policy from Aegon Religare which will cover both as a family.In such case,will both of us get tax benefits on premium paid(sharing basis) or only one can get?

Sagar-It is the source of premium payment that is matters.

Thanks for your response and sorry to bother you much on same…!

Since it is single premium for both’s cover,it would be on either name,right? In such case how can we split and submit the proof?

Sagar-You can’t split it. Anyone person can claim the benefit.

please advice

In term plans whether one should go for longest term available or upto a certain age.

Ranjeet-It is up to your retirement age.

Hi Sir

One question currently i’m 30(Retirement is 60) i’m planing to buy HDFC CTP for a term of 40 years now i have 2 questions.

1) Why it is not advisable to take a term plan after our retirement your family may need it after your retirement as well?

2) After 60 years what documents they need for the plan? A non-pensioner will not be having an form 16 or salary slip or any source of income will they count such situation as well they might say a person is was not working so why to settle the claim?

Amit-If you are not creating enough retirement corpus then you not retire. You are claiming that you retire at 60 years of age. In your own question of second, you mentioned that you will not have any source of income. Hence, insurance requirement stop when the person stops earning. Also, with retirmeent corpus in hand, why you need insurance? Also, what will be the value of current term insurance when you are at 60 years of age? When issue the policy then they only look for death happened or not. They not look for your income even after the next year of issuing a policy.

Dear Sir,

I want to take term plan and found edelweiss very interesting but its claim ratio is far too low. So should i go with edelweiss tokyo term plan or not?

Ankur-If the plan is perfectly suited your need then go ahead.

Hello Basavji, I have gone thru questions by diff people and your advise to them. Its very good initiative by you to spread knowledge. I have couple of questions. I am 36 yrs old male. 1) I have a term plan from Aegon Religare which I bought in June last year for 50 lacs. I want to buy additional term plan for Rs. 50 lacs. Kindly advise is it advisable to buy it from other insurer. 2) I had a health check up recently on 3rd July and found for the first time that I am hypertensive. I am on medication now. While buying new policy, I will definitely declare this; however, is it obligatory to inform the existing insurer. Kindly advise. Thank you so much in advance.

Navpritsingh-It is purely your comfort either to go with existing insurer or new one. If you feel no issues with Aegon then why to go for new? No need to inform about hypertension to the existing insurer. However, it is a must to inform while buying new insurance.

I am planning to buy a term plan. I have one doubt that whether I should go for 2 policies from 2 different companies (50 Lacs each) or 1 crore from a single company. This doubt comes into my mind because if at the time of claim if an insurence company has to settle an amount of 50 lac then then chances of settlement are more than settling 1 crore.

Is my doubt correct or should I go for directly 1 crore.

Go with one for the following reason.

1. For splitting you will end up paying a higher premium.

2. 1 extra bill/payment to remember

3. If you have not hidden any information and your proposal is accepted by the insurance company then they there is no reason they should reject your claim.

Having said that, always go for the “Most Trusted Brand ” insurance provider as the policy will benefit the nominees in your absence. Dont think about paying a little extra if it can give you peace of mind.

Hi,

My name is abhishek. Iam 30 year 4 month old ,non smoker . i want to buy term insurance for 35 years for amount 1cr. suggest me one good company for which i should go for with moderate premium.

I have checked and confused as for above insurance HDFC quotes 11900, ICICI 12500,agon 9000 etc.

Please suggest ASAP.

Thanks in advance

Abhishek-You can go with one between HDFC or ICICI.

Sir,

I am about to submit my term insurance policy through HDFC click to protect plan, But Before that I just want to know one thing, that why there is so much diffrences in premium value, between the various Insurance comapnies, for the same sum assured and same tenure , as No insurance company can reject the claim unless and untill the details which were provided in policy form are incorrect and faulse.

so why need pay more if you can purchase the policy of same sum assured value at cheapest premium value, does it only mean the company charging extra premium from u as brand name.

Hi Sir,

I am 29 year old, married and planning to take a term plan of 1 CR for 40 year (as it will cover my max age and not only till I am working). There are few questions

1) Is it feasible to split it into two HDFC and Kotak for 50L each (so that atleast one settlement is faster )

2) My decision to take term plan for 40 year is right or not?

3) I have not taken any retirement plan can you suggest some

4) I am only investing in 1L PPF and 2000 in SIP, I still have arround 10000 P.m to invest, can you suggest some plans which will help me

Siddhant-1) Not a best strategy. Go with one insurer. 2) No, because you need term insurance only up to the start of your retirement age. During retirement, you don’t need term insurance. 3) You have to build on your own. Because there is no such product in pension which we can say BEST. 4) Funds are listed in my earlier post at “Top 10 Best Mutual Funds to invest in India for 2015“.

Dear Sir,

Thanks for the information.

I am of 27 years a non smoker. I want to take a term plan of 1crore for 35 to 40 years.

Kindly suggest whether I should take it from “Aviva” or “Aegon”! Which one will be good? As the CSR is going down year by year I am confused on this. kindly suggest.

Or else suggest whether I should go for any of the top 5 Insurance companies as you mentioned in order.

Regards,

Pradeep.

Pradeep-How you arrived at Aviva or Aegon?

Hi, I am 37 years old. now i want to buy term insurance. i am occasionally smoker in month 2-5 cig. my question is that, do i need to show smoker there?

Thanks

Amit-Better you mention your habit. Because don’t know when the current level of your habit increases 🙂

Hi,

I am 33 year, married man with two kids. I have a 12 lakh LIC jeevan anand policy. Since its insufficient cover, i am planning to go for a term plan of 1 crore. I am thinking about HDFC click to protect.

I am a social drinker but don’t smoke. Do you have any further suggestion/ feedback.

Can you recommend/ suggest any good plans?

Regards,

Vilas

Vilas-You can go ahead with HDFC but don’t forget to mention about your social activity.

Hi Basavaraj,

I thank you much for running this post and providing wonderful suggestions on insurance to all with much clarity.

I have few queries, can you please help clarify?

I have taken a 1 Cr term insurance policy from Aviva in Sep 2011. As the claim settlement ratio is falling y-o-y for Aviva I now feel worried. Should I look out for a better insurer although the premium will be higher?

Over years as the the liabilities are increasing and maintaining life style is becoming costly, thinking to take another term policy. So is it ok to have multiple policies from multiple insurers?

In one of your posts, you talked “Stick to one. No logic in splitting. Who knows later on all insurers come up with an idea of sharing claims info to one another??”

Even if the insurers share the info will it be a problem if one has disclosed everything correct while applying for the policy?

Also as I am planning to buy one more policy do I need to inform Aviva about the new policy if it is issued?

Thanks in advance.

NC-If you personally don’t have any issues with Aviva, then I don’t think it is worrying part. Yes, you can opt multiple policies from multiple insurers. But do remember to mention the existing all policies while buying new one. If you are correct then I don’t think anyone can forcibly reject your claim. You no need to inform to Aviva about the new policy buying.

Nice to see u to help the people.Pl suggest i have applied the HDFC life click to protect for cover of Rs 1cr for premium amount Rs 12698 for 40 years.HDFC had taken my medical test. hdfc intimate me that there is Elevated Liver Enzymes diagoned during medical check up,Now they charge additional premium charge rs 6949 apart from Rs 12698.HDFC agent says that if i dont want to pay incremental in premium then they either reduce the term i.e 25 to 30 years or withdraw your proposal.

Please share your opinion regarding this matter.

Teji-Yes, if you are unable to pay the higher premium then they may reduce the sum assured. If you are comfortable and know that you are suffering from such disease then better you continue by paying a higher premium. Otherwise, you can check out with insurers.

Hi Basavraj,

I have taken a term insurance for Rs 1 crore from HDFC.Will it be ok to stick to it or should I switch to LIC

Avishek-Why you want to switch? If you disclosed all facts properly then I don’t think it is required.

Hi Basavaraj,

I am in a confusing regarding the tern insurance.

1. I am 31 years old & smokes 3 to 4 cigarates per day. I have a income around 8 lpa. I want to go for 75 lakhs Term insurance. Which one is more preferable LIC or ICICI or HDFC?

2. Before giving the Term insurance policy, whether all the companies will ask for medical test? If so do they share the details after the medical test? Becaue they should not alter the mediacl test reports after few years without my consent.

3. HDFC guys are calling me everyday & they are telling that compared to LIC & ICICI they have more features like income plus option & so on.

Please let me know which one is more suitable for me.

Sanj-1) All the said companies are good. 2) Yes, usually all companies suggest to go for medical test. Also, it depends on company to share the information with you. What they get from altering your reports? In fact they loose the business right? 3) Don’t go for additional features, instead buy a simple term plan.

Hi Basavaraj,

My monthly income is Rs30000/-………..I am 28 years old & married from kolkata. I have floating Rs7lakh medical insurance .I have a 50Lakh term plan from MAX LIFE for 30 years from the last moth as a nominee of my wife.I have Rs10,000 of SIP in few funds including Rs 4000 in ELSS fund for tax saving.And used to save Rs 50000/ year for in PPF.

So now my question is what extra I have to do with in my boundary to achieve financial strength.

Sourav-The main purpose I am missing in your life is identifying the goals. Also, non-target based investment. Simply investing surplus or for tax saving is not a right strategy.

Hi Basavaraj,

I am 32, I am planning to got for 1 Cr term plan by breaking them in 2 one 50L in LIC and other 50in Premium Back TERM Insurance plans for better control on insurance claim and keeping overall annual premium in mind. looking at the report I felt that LIC settles claims better than any other insurance provider. Of course the premium is high compared to other policy providers. Every insurance company would scrutinise to polices and claims to make money , but I felt there is no point in taking insurance from companies who do 10 out of 100 rejections compared with 1 out of 100 rejections. Id rather prefer to be in a member of 1 than 10. If my thought is wrong in it or the way plan please suggest me the best options

It would be grateful if you could suggestion on companies who provide premium back term plans.

cheers

Kishore-First myth-This claim ratio not ONLY for Term Insurance, but it also includes endowment and ULIPs. Hence, don’t rely too much on this data. Second myth-Splitting of insurance will not serve any purpose. Third myth-Unable to understand how you be in control by opting to separate insurance and one by premium back.

Hi Basavaraj,

I am planning FDs and ULPs/mutual funds as my additional savings with other companies. Term plan is purely for unexpected risk coverage and a reliable policy provider that can offer prompt claim in case of unexpected. purpose of splitting is balancing of funds with High premium term plan and mid price premium back term plan that offers a confidence in claims considering their past track records. for Ex: (HPTP)10000+(PBTP)15000 = 25000 rather than spending on all 20000(HPTP) on one insurance and relying on one. more over on maturity we can get the premiums of PBTP. I am working more on probability of gaining benefit by minimising risk a win win situation. so I am requesting your input on best premium back term plans.

Kishore-May I know the value (considering the inflation) of the total premium you receive back if you survive? Will this be a great benefit from this term plan? What if second company informs to first one about it’s rejection? Whether the first company accept it or not? Above all it is your turn to decide.

Basunivesh, Just to add some more points is one should consider customer support, consistent high claim settlement ratio and premiums as part of choosing best term insurance plans…

Suresh-Sadly we will come to know about customer support only when we not live. However, we can take the reviews of existing claim settled. But it is hard to get such reviews from anyone. Regarding claim settlement ratio, the data not provide you the clear picture of claims settled related to term insurance. Hence, that too a big drawback (If we believe on claim settlement ratio and try to buy term insurance).

Accident Death Claim and sum assured Claim is applicable in following case or not

1. Working in my company and any mishap happen and death occur.

2. In official tour and some mishap happen and death occur.

3. In holiday in hill station and accident occur while traveling like road or air accident and death occur.

4. Working in hilly area and earthquake or avalanche or flood occur and death occur.

5. Critical illness diagnosed after one year and death occur.

6. Normal road accident in my hometown outside office are and death occur.

Kindly tell me detail about both the claim is applicable or not

Sukesh-Except the point No.4, rest of the points are very much eligible to get the claim under Accidental as well as the Sum Assured available in a plan. You have to check plan features with an individual insurer regarding the coverage of natural calamity.

Thankyou Sir

Hi Sir

I want to take a term plan for 50L, I was 33 years old, non smoker, I would like to take Max life or Aegon refer best one from both of these

Can i take any riders?

Thanks

Seshu

Nagaseshu-Both are best to me.

Can i take any riders or plain term plan

Nagaseshu-Better plain term plan.

Sir, Wht is the best duration.

In Aegon it is coming as 27 default but in Max it is not there

Specify best duration

Thanks

Nagaseshu-The best duration will be up to your retirement age.

Sir

Can you please provide 2014-15 claim settlement ratio Table

Thanks

Nageseshu-It is not yet published by IRDA.

I want to buy a term plan for 30 or 35 yrs. But not that much idea which company i should buy. I am non smoker and please suggest me any particular company. And can i take two term plans of different company of 50 Laks.

Waiting your suggestion.

Regards

shiv

Shiv-Your queries are all answered at my earlier post of “Best online Term Insurance Plans in India for 2015-A comparative list“.

Dear Mr Basavaraj,

I am a defense officer. I was planning to buy HDFC term insurance, before making payment, i got a call from there service representative. I asked if the term insurance and Accidental Death benefit is applicable to those in defense services?

He said, the policy is not applicable if something happens to insured persons while on duty !!! however, it is applicable if you are not on duty!

They could not explain what that exactly meant.

Is it true?

regards

Dushyant-What a strange reply? If one dies during duty means no claim? I suggest to write a mail or visit nearest branch of HDFC Life and get confirmation from them.

Hello Sir,

I am looking for Good Term plan insurance. Currently i don’t have any term Insurance. I have LIC Jeevan Saral insurance.

I am 33yrs old and have 15lac p.a. package. I am occasional smoker. Looking for 75Lac plan.

Please guide me on below queries:

1. Which plan to take?

2. what will be Premium?

3. How plan is differ for Smoker and non-smoker.

Many thanks for above helpful article.

Tushar-1) Term Plan. 2) It depends on your age, term and health condition. Hence, I can’t say. 3) You notice the premium difference while mentioning both.

why not u should go for health insurance policy for your family financial budget

Dear Sir,

I have purchased Agone religare term plan for 1 Cr. around 3 years back with Accidental rider (40 lacs) and Critical illness rider. (Year of birth is 1987)

I Am non smoker and provided complete medical history.

as of now I am confused whether I shall buy another term plan from any of the reputed players like HDFC, ICICI or LIC as some of my friends suggested that don’t completely rely on Agon religare.

Please suggest whether I shall continue with Agone religare or I should buy second term plan?

is it allowed to take second term plan in India from different player?

Vinit-Continue Aegon plan. If you still feel uncomfortable, when your next time review of insurance requirement you can opt the companies which you mentioned.

I have recently taken Reliance online term plan of 1 Cr. I wanted to whether it is a correct decision or i should have gone with other company term insurance plan.

Please reply.

Alok-If you declared all facts properly, then no need to worry.

I am a single son having two sisters. I am married. I don’t have kid right now. Main purpose of taking Reliance 1 Cr term insurance plan is sister’s education, marriage and parent’s security. After education and marriage of sister’s purpose of this plan may be changed. Reliance 1 Cr term insurance plan will be changed afterwards.

Whether it is advisable for me to have one more 1 Cr plan of HDFC term insurance click to protect plus for my wife and kid future security. If yes, then for how many years i should take it. Kindly suggest as per my situation.

Alok-If you want to split your insurance requirement based on financial responsibilities you have, then it is great. Ideal insurance coverage will be 15-20 times of yearly income+Loan.

Dear Basavaraj

Thanks for keeping people informed on such important issue.!

I have been an occasional smoker (not more than 1 cigarette a day!). I intend to take a term cover of 1 crore. My questions are as follows:

1. Would I be treated as smoker or non-smoker?

2. If my insurance cover is taken as a non-smoker after blood tests. Can the insurance company reject claim in case of death because of smoking.

3. Is the claim accepted in case of suicide or death in case of drunk driving?

I know these questions sound insane, but future is very uncertain!. Hope to receive a positive reply from you.

Thanks.