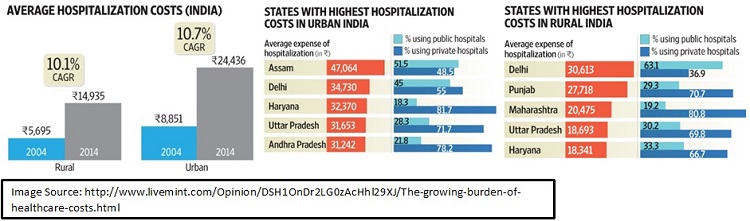

“He who has health, has hope; and he who has hope, has everything.” –Thomas Carlyle Good Health seems hard to achieve and even harder to maintain. No matter how clichéd it sounds, health is wealth, and there’s no denying this fact. The cost of healthcare treatments in Indian have been rising tremendously with approximately 10% annual growth from 2004 to 2014. With a scenario where an average expense of hospitalization is far from what an average citizen can afford in most of the states, health insurance becomes all the more imperative.

Most Indians who are covered by an insurance plan from their employer commit the mistake of perceiving their plan as an adequate one. However, these plans might be useful but not adequate. Such a mistake might cost you your entire life’s savings at the time of crisis leaving you with nothing but bitterness and an empty pocket. Therefore, evaluating your needs and buying adequate cover is important to keep you and your family covered. Before you really get into it and choose a plan, there are certain things that you will need to consider. Needless to say, you don’t want to fall into the trap of buying a plan that you do not need or cannot even use. Here are some pointers put together to help you find the perfect plan ultimately giving you the advantage you need when you’re taking that fated trip to the doctor’s office or even the emergency room (heaven forbid, though).

What’s Your Health Telling You?

Buying health insurance that does not cover a health treatment you are most likely to need is useless, isn’t it? So, if you are buying a plan, look for the day care procedures covered by your insurance provider. Interestingly, relying on a longer list of day care procedures can be misleading. Curious to know how? Suppose ‘Provider A’ enlists 20 day care procedures and ‘Provider B’ enlists 100. The list of 20 day care procedures mentions ‘Dental Procedures’ while the list of 100 mentions 10 specific dental procedures. Dental procedures is a broad term and might involve much more than those 10 specific procedures listed on the list of Provider B. That’s how a short list of procedures might actually be wider instead of a longer list. Going through the entire list might help you decide which plan suits you better as there are plans that do not cover eye and dental treatments at all and you might want them in your plan.

Consider your Healthcare Provider

One of the biggest mistakes that people tend to make when trying to start a healthcare plan is not considering their health care provider. You may have a certain provider in mind, even if you have not started seeing them yet, and perhaps you are actually limited by your area. Whatever the case may be, you should always speak to your potential care provider first and make sure that they actually accept the insurance that you plan to obtain. Health Insurance Plans obtained from ICICI Lombard or other trusted insurance providers ensure that your insurance is acceptable in almost all the major hospitals. Double-check before you jump in. After all, is there any point buying an insurance plan that no one in your area accepts?

The Cost Sharing Issue

Over 80% of health insurance in India is private financing that includes a major fraction of out-of-pocket payments and ignoring the pre-payment schemes. If you have a surgery, for example, will the insurance company cover the entire thing, or will you be left standing with a portion of the bill? Even 10% of a bill can be rather costly, and it is not something that you want to be stuck with. Always speak with the insurance company to find out what kind of plan you need – if any from them. Even if you feel awkward doing so, always ask questions! It can save you untold amounts of trouble – more than you realize.

Are Your Dependents Covered?

Factor in the coverage you need for your kids, spouse or dependent parents and whether you have them covered in the insurance policy you looking to buy. The benefits of getting your family covered does not end at the level of security rather it offers great tax benefits as anyone paying premiums for parents, apart from themselves, spouse and children, they can claim deductions up to INR 55,000, according to Section 80D. While getting your family covered, evaluate predisposition towards ailments and your family’s health history.

Think about Insurance Overcompensation

Some people tend to sign up for an insurance policy and take everything they can get ‘just in case’. Do you really need your insurance plan to cover 90 percent of your policy? If you are a relatively healthy person, then there is a good chance that you can back off on the percentage and go with a plan that is a bit more suited to you. Also, a big cover is not necessary for combating your health care needs because a lot of top ups and add-on covers do the same job while costing you less.

Can You Customize?

The last thing to address is the failure to customize your plan. There is this inherent belief that one size fits all when it comes to insurance, and it simply isn’t true. There are so many things to consider regarding your health, habits, age, area you live in etc. for example, if you are living in Delhi or Mumbai with a family of four young and healthy members, you can go for a cover of 5 lacs which has to be increased every 5 years considering inflation, health requirements and ageing. Figure out what type of coverage you need, and then make your purchase.

There are many more mistakes that can be made in the name of healthcare purchases, and these are merely a few of them. Figuring out most of them before you fall and commit them can save you loads of annoyance and stress. Start planning your future today. Talk to a healthcare provider, speak with an insurance expert, and live a happy, healthy life for the foreseeable future.

Note-This is a guest post by Neelam, a Personal Finance Freelancer.

Hi Basu,

Thanks for the article. I’ve two queries –

1. Does room-rent cap decide all other reimbursements ? Say I’ve a cap of 2000 Rs/day, and I’m admitted in a room having rent Rs 4000/ day. If I undergo a surgery of say 20000. Do I get full refund of 20000 (provided all other criterias are met) or they refund me just 10000 (2000 *2000/4000) ?

2. I was checking Star Comprehensive. I’m currently 40, and for 2A + 1C and SA Rs7,50,000 the premium is 18500 + tax. But for 71-75 it is 96000 + tax. Does that men when I reach 70 years, I’ve to pay annual premium of 1 lakh plus ?

Can you suggest any health insurance plan ?

Dear Amartya,

1) In your case the room rent is 50% of your actual cap. Hence, all your claims will be settled at 50% only (Rs.10,000) but not fully.

2) YES.

Hello Sir,

Would you recommend health plans that include dental procedures,OPD,pharmacy bills though the cost of the premiums would be almost double the amount compared to vanilla health policies..

These days the OPD costs,consultations,pharmacy bills are becoming more and more expensive hence this question..

Thanks

Dear Shiva,

Yes, premium will be higher as you go for more features. Each such features cost you. If you feel that such costs are not affordable for you and better to transfer to an insurance company, then go ahead.

And also life insurance for my mother of 63 with sum insured of 2 crore? Any good companies..

Hi Basuji,

I hv two Apollo health policies of 10 lakh sum assurance. One of family floater of my wife and two kids, my age 46. Another individual of my mother 63 with sum assurance of 10 lakhs. Now I want to port bcoz of Apollo claim issue with my uncle.

Which company is good and enhance sum assurance to 50 lakhs?

Or should I go for 20 lakhs considering no claim bonus is 20%?

Or should i opt for super top up?

Your advise please…thank you sir.

Dgouda-Check with public sector companies.

hi sir,

I want to take a medical policy for my in laws. their details are below:-

Father-in-law=aged about 65 yrs; have blood pressure issue;1 week back he slipped in the bathroom and suffered head injury and admitted to ICU but is recovering.

Mother-in-law=aged about 55 years;suffers from neuro problems and is taking medicine.

They stay in cuttack and me n my husband in delhi.so now i want to take a good policy for them but market is flooded with policies and i am confused please help me to get a good one.

i have already taken a medical policy of religare which covers me my husband and my 4 yrs old son.

what i should do now?should i take independent policy for in laws or should include them in our policy.

please suggest…

Sneha-First understand that no insurer will cover the existing diseases. There is always a waiting period. Second thing, based on the health of your laws, premium varies. Third, try to separate their need with your needs (buy separate health insurance to in-laws).

I suggest you to check with first public sector companies like United, National or New India. If you not succeed in getting, then go with Religare (I am recommending this, because you already owning your own family floater). Let me know the status at later stage to discuss more.

Hi Basu, I have taken optima restore family floater from appolo munich two years ago through portability (before that I was in national insurance for two years). I found the insurance preium is higher in optima restore for age after 50s. now I am planning to move star health insurance. Could I move. Please advise

Narayan-You may feel premium higher compare to star. But check the co-payment clause of Apollo to Star. In star it is higher.

Hi Basu

I want to buy health insurance for my sister, age 40, unmarried with no current conditions (but family history of cardiac disease, cancer and BP) and my mother, age 65, a few current conditions (not of the critical type).

What providers would you recommend? How do I go about deciding?

Also, is there an additional benefit of cashless policies that I don’t have to worry about paying a hospital deposit if either of them are in an emergency and need to be hospitalised? I live in a different city.

Many thanks for your help.

Dinesh-You can check with standalone companies or public sector companies. Nowadays cashless facility is provided by all insurers. So you have to check in advance of which hospitals provides it in your area.

Hi Basu

I’m a police officer age 38 Iwant to take term insurance of 50 lacks but private companies like hdfc don’t give me term insurance

They says claim will not be settled when incident wiil happen when I will be on duty

Please suggest me which company should I prefer

Subhash-The problem may be due to your profession. I am not sure which company offers. But check with other companies.

Hi Basu,

Can you help me with best health insurance for me my detail is age 23, sum insured around 2-3 L, no pre existing disease and plan in which i can add my partner in future. can you please put some light on Universal Sompo’s Helth plan because price point of view they are looking good.

waiting your reply, Thanks in advanced.

Nikhil

Nikhil-Go ahead with Star, Apollo, MaxBupa or Religare.

and UNIVARSAL SOMPO?? can you pls give any suggestion on it and its plans?

Thanks.

Nikhil

Nikhil-It is new bee in market. Let us wait.

Hi Basavaraj,

I am 33 years old married . Currently i have default medical insurance of my office of 2 lakh. I need health insurance for me and my wife .

1)Should i take floater policy ? How much amount ? I earn 12lakh p a

1)Should i go for another independent health insurance or should i do super top up?

2)If so please let me know some companies which are good (whether public or private), please don’t give diplomatic answers .

Regards,

Siddharth

Siddharth-1) Go with family floater of around Rs.5 lakh.

2) At later stage, considering the inflation and insurance requirement, you can go ahead with top up. However, first have a basic family floater.

3) To me all are equally good and bad. Hence, first understand your requirement, comfort with company and premium affordability.

Hi ,

I have family health insurance from company from past 10 years. Would like to go for personal health insurance for Father of age 63 and Mother of age 59. could you pl help which Insurance company will agree (With best claim ratio) for coverage from Day 1 by considering previous insurance . My plan is to quite job in next couple of months.

Also, which is the best plan for my family ( MY age of 37 , Wife and 2 kids).

Subhash-If your parents are the member of your existing health insurance product, then you can opt for health insurance for your parents from the same insurer. However, considering their age, they may ask for medical report. If any existing diseases, then they put waiting period.

plz guide suitable life insurnce polic for housewives as they r non earning members no one can submit it returns?

if husb is govt employ can he take joint lif insurnce for her non earning wif? wat r prevailing high sum assured joint life insur plans , endowment plans and term plan for working male and no earning wife?

Thanks in advance for your suggestion.

Thanks,

anand

Anand-Life Insurance is not at all required for her. Stay away from any LIFE INSURANCE POLICY.

hi sir,

what is the difference between health insurance and life insurance???

Montu-Health insurance pays you the cost of hospitalization and life insurance means in case of sudden demise of policyholder, insurance company provides the claim amount (equal to sum assured in policy) to a nominee.

thanks sir,,,

which company family floter plan best for the me+wife+parents.

Montu-There is no SPECIFIC company, which we can say as BEST. First understand your requirement.

hi basu ,

which company plan will u recommend for my family (6) which should cover pregnancy too.

Praveen-Your concern is pregnancy cover?

Hi Sir.

I have a query about health insurance.

Why do most of the health insurance companies (almost all ) not cover pregnancy in their product? Is it something to do with high probability.

Please let me know if you come across any health insurance company providing pregnancy cover in their product.

Also, please through some light on reasons for high number of complaints against health insurance companies.

Thanks in advance.

Ritesh-It is not true that pregnancy not covered. But covered with waiting period. What people do is, when they plan kid, then suddenly they get the GYAAN about medical cost involved in pregnancy. So first they buy the health insurance by paying premium of around Rs.10,000 to Rs.15,000 and after 9 months or a year they claim it with hefty bills of around Rs.50,000 to Rs.1 lakh. Which business sustains with this logic from buyer? Hence, the waiting period.

Who to blame most for this situation? (rising complaints against health insurance companies)

Regulator (IRDA) or

Insurance Companies or

Insurance Agents or

Customer

Ritesh-First to US. Mis-selling or wrong information will be circulated to those who don’t know. Hence, we must first understand what we are buying and for what purpose we are investing. Insurance companies or regulators are just mere coincidence.

Hi Basu,

Planning to buy Religare Care Health insurance Policy for myself (34), wife (31) and my 2 heal old son for 25 lacs. I may consider Apollo Munich as well .

Need you suggestion on the same

Kind Regards,

Anuj Ajmani

Anuj-Both are great products. Go ahead and chose the anyone.

Hi Basu,

I would like to buy additional insurance cover for my parents although they are covered by my existing insurance cover (6 lacs for all members) from the employer. They are 53 and 60 yrs old and do you think I should buy a floater or individual policies for them with Top up or Super Top up? Could you suggest some good plans for them and also the amounts we should look at?

Also, my husbands employer does not provide good health insurance cover (just 2lacs) and I was thinking it would make sense for him to buy an individual policy as he’s 40 yrs old. I’m 32 and I was thinking taking additional individual policies would be more helpful in our case? what do you think and suggest?

Regards

Manisha

Manisha-Better to buy individual health insurance to them. Considering their age, I suggest to go first with public sector companies. If you not get then check with Star, Apollo or Maxbupa. Ideal cover to them must be anywhere around Rs.5 lakh to Rs.10 lakh. For your family, I suggest to go with family floater (even though members are covered by employers). You can check with Star, Apollo, Religare or MaxBupa.

Thank you Basu! How about a top up or super top up for my parents and the two of us? Should w consider that as well? Are there good options for this in the market?

Regards

manisha

Manisha-If your budget is tight, then definitely you can consider super top up plan (but not top up). Yes, currently all insurance companies offer super top up plans. Buy the one within the same company where you have base health insurance plan. This will make easy during claim.

Dear Anuj..

Religare and Apollo, both are good. Both r offering one feature of AUTO RECHARGE of sum insured in case of basic sum insured (BSI) is exhusated.

But one major difference in their mediclaim policy.

In Apollo optima restore plan- auto recharge comes in picture if ur exhusated yr entire BSI.

In Religare ‘Care plan’ they rechare it fully irrespective of claim amount.

So In my view, Religare CARE is better.

Google it, n copmare this yrself.

Dipak-I stayed away from recommending any SINGLE product 🙂

Hi Basu,

Nice article thank you very much for info, i would like to share my insurance request you please have your expert view let me know if anything needs to be change

we’re 3 family members (Me (32 years),wife (26 years) & our 2 years daughter)

Family floater for 5 lacs

Company provided insurance is of 5 lacs

Critical illness plan for me & my wife is of 7 lacs

Along with this we both have term plan of 50 lacs(mine) & 80 lacs(wife)

Sumedh-Any specific reason of having higher sum assured term insurance for wife? Include accidental insurance also.

HI Basu,

As usual and not to mention very very useful information in deed, on a personal note i have been covered with my employer around 2.5L and i have family of 5, can you please suggest how can i plan further, also do you mind suggesting some of best plans available in market present?

Thanks in advance for your suggestion.

Thanks,

Mahesh

Mahesh-Considering your family strength, I feel the insurance is low. Better to enhance around at least of another 3-4 lakhs. There is no such BEST. First understand your requirement, then we discuss.