Many of us have employer-provided health insurance. But have you never thought of who will pay the claim amount in case it is more than the sum insured? In such situation, the cheapest options are buying Top Up Health Insurance Plan & Super Top Health Insurance Plan. Let us see how they will be handy in such situations.

Considering the current health cost in India, especially in big cities, it is hard to believe that health insurance coverage of around Rs.3 lakh to Rs.5 lakh is sufficient. Also, many of salaried completely depend on employer-provided health insurance.

#Let us first discuss Top Up Health Insurance Plan.

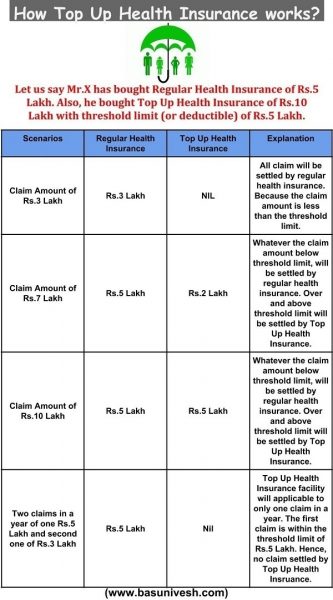

Top Up Health Insurance plan is a regular health insurance plan. But with certain threshold limit (deductible) to it. For example, if Top Up Health Insurance Plan offering you sum insurance of Rs.10 Lakh with threshold (deductible) limit of Rs.5 lakh. Then any health insurance claim arising more than Rs.5 lakh will be payable by this top up health insurance. Below Rs.5 lakh claim must be settled either by regular health insurance or we have to pay from our own pocket.

Let us say Mr.X has a regular health insurance of sum insured Rs.5 Lakh and a top up health insurance of Rs.10 lakh with a threshold limit of Rs.5 lakh. Suddenly one day due to health issues he got admitted to the hospital. The claim bill amount was Rs.6 lakh. His regular health insurance will pay Rs.5 lakh (as the maximum sum insured is Rs.5 lakh only). Who will pay the remaining Rs.1 lakh? As the claim amount is more than the threshold limit set by top-up health insurance, remaining Rs.1 lakh will be payable by this top up health insurance.

In the absence of any such top up health insurance, Mr.X might be forced to pay the remaining Rs.1 lakh claim amount from his own pocket. I explained the different scenarios of how the regular health insurance and top up health insurance will work in below image.

Now you got an idea of where the Top Up Health Insurance will be handy, apart from regular health insurance plans. If there is more than one claim in a single year, then such top up plan will not be useful, as these top up plans only applicable to one claim per year. If that particular single claim is above threshold limit, then you get the claim amount from top up plans. Otherwise, such top up plans will not be useful.

Here in such a situation, super top up health insurance plan will come in handy.

#Let us discuss Super Top Up Health Insurance Plan.

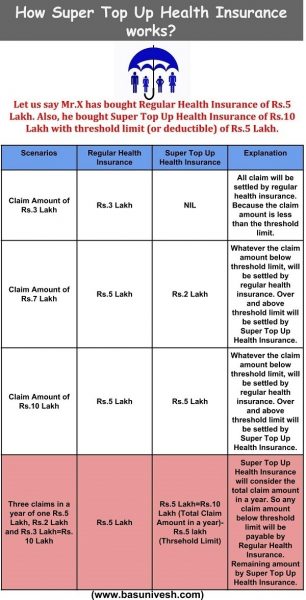

Super Top Up Health Insurance Plan works exactly like Top Up Health Insurance but with only one difference. In Top Up Health Insurance Plan, there is a limit for a claim in a year i.e. single claim in a year. However, in case of Super Top Up Health Insurance Plan, there is no such limit.

For example, in the last scenario of the above table, if Mr.X has Super Top Up Health Insurance, then the remaining Rs.3 lakh might be settled by this super top up health insurance but not from his own pocket.

Super Top Up Plans will consider the total claim amount in a year. Whatever the amount below threshold limit must be payable either by regular health insurance or from our own pocket. The remaining amount will be payable by super top up health insurance plans. I tried to explain the same in below image.

See from above table where I highlighted the last row with a different colour. Here Super Top Up Health Insurance Plan will come into handy than regular plans or Top Up Health Insurance Plan.

Features of Top Up Health Insurance Plan & Super Top Health Insurance Plan

- No restriction to have Regular Health Insurance-There is no such restriction that you must have regular health insurance to buy either of these two. If you have regular health insurance, then below the threshold amount will be settled by the regular plans and above threshold claim amount by either of these two.

- Can buy from different insurers-You can buy regular health insurance from one company and top up plans from a different company.

- Cheaper than Regular Health Insurance Plans-Due to threshold limit or deductible clause, these plans are cheaper than regular health insurance plans.

- Both Individual and Family Floater Plans Available-Exactly like typical regular health insurance products, such top up plans will offer you to an individual or to a whole family.

- Come with regular exclusions-Regular exclusions also applicable to top up plans like existing diseases or dental care. Hence, check out for exclusions in detail.

- Tax Benefit-Exactly like regular health insurance products, you can claim the tax deduction under Sec.80D of IT Act.

- Works on reimbursement base-Before settling the claims under top up plans, insurers first check whether the below threshold limit amount of total claim bills paid from a policyholder or not. They will not bother whether below threshold amount is from the policyholder’s own pocket or from his regular health insurance. Then only any dues of above threshold limit settled by top up plans. Hence, you may say that getting cashless benefit from the top up plans is difficult.

- No NCB (No Claim Bonus)-These plans usually not offer any NCB benefits.

Who can go for Top Up Health Insurance Plan & Super Top Health Insurance Plan?

If your health insurance is negligible and budget is your problem, then definitely you can this of buying Top Up Health Insurance Plan & Super Top Health Insurance Plan. Because they are cheap. But do remember that claim settlement may be cumbersome with Top Up Health Insurance Plan & Super Top Health Insurance Plan. Hence, it is better to increase your cover from the existing health insurance itself.

If you plan to increase your health insurance cover, then first try to compare the premium of top up plans with regular plans. Go for top up plans only in case you feel cheaper than going for regular plans.

Usually, minor claims are more frequent than the huge claims. Hence, you may end up in forgetting the features of such top plans. Hence, make sure that you know the details regularly and it’s applicability.

Few Top Up Health Insurance Plan & Super Top Health Insurance Plan available in market

- United India Super Top Up plan

- Apollo Munich Optima Super Top Up

- Max Bupa Super Top Up plan

- HDFC Ergo Health Suraksha Top Up Plus

- Cigna TTK Super Top Plan

- Bajaj Allianz Extra Care

- Religare enhance

- ICICI Lombard Health Care Plus

- Star Super Surplus

You may also refer our earlier posts on Health Insurance.

- IRDA Incurred Claim Ratio-How to choose the best health Insurance?

- Jeevan Arogya-Do you know this LIC’s Health or Medical Insurance Policy?

- Best Senior Citizen Health Insurance in India-Product Comparison

- Facts about Third Party Administrator (TPA) of Health Insurance

- Senior citizen health insurance-Apollo Munich’s “Optima Senior

Dear Basuji,

Can you write an article on various super top plans available as on 2020. This article is old.

Regards,

A Bandyopadhyay

Dear Bandyopadhyay,

Sure..I will write on this.

Dear Sir,

I have finalised hdfc ergo optima restore for base plan after reading your article on health insurance.

I was going through super top article and finalised on Apollo munich optima super top up (now hdfc ergo) and Hdfc ergo health surkasha super top up( medicare) .

I saw that for apollo they are charging around 5300 for 4 lakh deductible and 10 lakhs Sum insured. ( 30 years age bracket floater)

But in Hdfc ergo health surkasha they are charging 2860 for 4 lakh deductible and 16 lakhs Sum insured.

This difference is huge if you select age bracket of 60 plus.

where is catch ?.. i tried to find some but was not successful … can you please tell atleast one major difference for such huge premium difference which is surprising because now they are under same parent company (HDFC Ergo).

Is it just like they (HDFC Ergo) have just done acquisition and have not revised their underwriting policies for apollo product …

are the offering by Apollo and hdfc ergo super top plan same or there is any difference.

Please suggest

Dear Vinay,

We can’t question the premium rate. However, both Apollo and HDFC now a same company, you can choose the one.

Dear Basavaraj,

I have basic sum assured 4 lakh from Star Health. Now, I want to top-up for 10 lakh from Star Health, have only 3 option of min. deductible amount of 3 or 5 or 10 Lakhs.

Now, should I opt for a min. deductible for 3 lakhs or it is better to increase my basic sum assured to 5 lakhs and opt for a min. deductible for 5 itself? Kindly suggest your views. Thanks

Dear Prakash,

Go with minimum deductable.

Hi,

Kindly clarify my doubt? I have Star Family Health Optima plan for 2A +1C. In that,

Basic Sum Insured: 4.0 lac

NCB: 1.35 lac

Limit of Coverage: 5.35 Lac

Recharge Benefit: 1.0 Lac

In this senario should I opt for a super top-up plan with the deductible amount 5.35 Lac or 6.35 Lac?

Dear Nitin,

Better to buy with co-payment of Rs.4 lakh.

Hello Basavaraj,

Will the Super top-up plan continue to exist even if the base group insurance plan expires for whatever reason? I have a group health insurance of a 3 lac family floater cover. I am now in a dilemma weather to pick up a fresh new individual policy of around 7 to 10 lacs or should I just go and get a super top plan for the same amount. Any guidance on the same would be greatly appreciated. Thanks in advance.

Dear Kevin,

The co-payment clause in Super Top Up plans in no way related to how you afford your part of co-payment. You can compensate from the base plan or from your own pocket. Better to have one base plan and then a super top up.

There is something strange about SUPRA SUPER TOPUP from Liberty Videocon Insurance where their premiums are very low like 60% less on comparing plans (comparing the quote is from policybazaar.com) ? Is there any catch ?

Dear Raja,

They may be reduced the premium just to garner more business. Check for exclusions cautiously.

Can I stack up Super Top-Up Plan to reduce the premium ? For (eg) I have my office primary group health plan for 5lakhs and I stack up with first Super Top Up Plan for 10 Lakh sum Insured with 5 Lakh deductible for Rs.7000 and another Super Top Up Plan ( Liberty Videocon Supra Super) for 1Cr with 10 lakh deductible for Rs.1600 which gives a saving of 35% (Rs.5000) premium if I had to take just one 30 lakh sum insured plan with 5 lakh deductible Super Top-Up Plan ?

Dear Raja,

Yes, you can do so. But in case of higher claim amount, then you have to knock different insurers to get the claim settled.

Adding to the post below I have also seen in many super top up policies about the deduction amount (which we have to pay from our pocket before the policy comes into effect).

Example if I am hospitalized and the expenses are 5L.

My base health insurance would cover me for 3L.

Apollo super top up says 2L deductible for 5L cover so does that mean I end up not utilizing the super top up policy benefits?

please help me understand..

Dear Shiva,

Co-Payment is nothing but the amount you pay from the claim bill (either from health insurance or from your own pocket). Hence, in your case buy super top up with co-payment of Rs.3 lakh.

Simple yet very effective post.. Thanks..

I have couple of Questions Sir..

-Me and my wife are covered under employee health insurance (5L each in individual companies plus spouse cover is also there within the same sum assured)

-I have take Apollo Optima restore Family floater-3L

I really feel that this health insurance is not enough and I am thinking about taking a super top up from Apollo again for around 5L(me,spouse and kid).

First Question-My kid is not covered in the base Apollo Optima restore Family floater,would she be covered under the super top up? (I am thinking negative).

Second Question-Would it make more sense if I invest to create wealth good enough to negate health insurance super top up or top up?

Dear Shiva,

Base plan is in no way connected to super top-up plan. Hence, you can include your kid in super top up plan. Is it not wise to transfer the risk to someone else (Insurance company) than taking that risk on our head? However, it does not mean that you must not consider to keep aside some amount for emergency corpus (even though you have Health Insurance). Because you will not get 100% of the claim get reimbursed.

I want to take a health insurance of Rs.20 lakh. Is it better to take 5 lakh of health insurance or 10 lakh of health insurance with remaining amount in top up? Any better option than this is also welcome.

Dear Giriraj,

You can choose so like Rs.10 lakh base plan and then another Rs.10 lakh super top up with co-payment of Rs.10 lakh.

I am 65 years old having Rs 5 lakh individual policy from National india Assurance. I want to opt for super top up plan for a sum of Rs 10 to 15 lakhs. In view of multiple claims in a year is covered I am opting for super top up. National India has only top up and not super top up and eligibility age is 65 years. I approached United they did not accepted my proposal because no approval if more then 60 years. I approached hdfc ergo by online they rejected my proposal because my weight 90 kgs,167 cms height and bmi is more then 25. I am having bp which is in control by medicine (120/80). I take blood thinner acitrom 4 mg to control DVT with right INR. Under this situation I want to have any additional health cover for my basic coverage in the form of super top up and which company may consider my proposal. Please advice.

thanks

Subramanya-Hard to say considering the health and age issues. Try your luck with other insurers.

Dear Basavaraj

It was an excellent blog, thanks for your efforts…

Can you please give your comments about ICICI Pru iProtect Smart plan,which also covers 34 critical illness..

thanks

Santhosh-Instead of buying critical illness as rider, I suggest you to go for standalone plans of health insurance and critical illness plans.

If I have a base health plan from day New India and a super top up from a different company say icici lombard, during claim all the originals will be submitted to base policy cover provider. In that case would the claim process be difficult for the super top up from different company?

In that case I it advisable to have both base and super top up from the same company even if it is slightly pricier?

Or would the claim process be hassle free with both the companies sharing documents?

Thanks in anticipation

Saurabh-It is always best to have the base plan and super top up plan within the same insurer. In that case, you need to run behind two insurer when you are already mentally disturbed due to hospitalization.

Sir,

I have a question in my mind please let me clear.As i have my mediclaim policy with star health for 5LACSfrom last seven years and having TOPUP policy with ICICI LOMBARD for Rs.10 LACS with deductable of Rs.3 LACS.Please let me know that If I admidited a hospital for some serious issues and hospital told that expenses is near about Rs.10 LACS then can I claim Rs.5 Lcacs from STAR and rest Rs.5 LACS from ICICI LOMBARD.iS it possible?Please Clear

Vinit-YES. ICICI will be beneficiary here. So they accept the claim with SMILE.

Sir,

Thanks for your early,Please clear how ICICI will be benefited with my claim.As my base policy with STAR and topup with ICICI LOMBARD.And as they may be refuse my claim as I have not taken base policy with them.Secondly I would like to inform that STAR premium is quite low for base policy and ICICI has very low premium for TOPUP.Thats why I have taken these two policies from two different companies.

Hello,

I have a family floater health policy for myself 33 yrs wife 28 yrs and daughter 2 yrs through HDFC ergo for 3 lakhs at a premium of Rs 7900/- recently I got a call from them for a super top up plan of additional 7 lakhs for all 3 at a premium of Rs 2650/- when I checked their link it shows a plan of L&T insurance company my:health super top-up which is now a part of HDFC ergo, but others like ICICI and Apollo are offering the same plan at double the premium so my question is why are they giving it for so cheap what’s the difference and what’s not covered, kindly help.

Regards,

Prashant

Prashant-Check the exclusion and co-payment clause at first.

Hello I’ve noticed that organ donor is not included and also specific conditions have a 2 year exclusion period after which they will be covered too. Also I would like to add that my existing policy has regain benefit as well as enhanced cumulative bonus of 10% for every claim free year upto 100% of sum assured so my 3 lakh policy will double upto 6 lakhs if I don’t claim so is it still worth buying a 7 lakh super topup with a deductible of 3 lakhs, kindly help also if you find any loopholes in this policy please share. Regards Prashant.

Prashant-Exclusion clause is normal and also the waiting period. Hence, you may go ahead.

Great post as always ! Thanks for explaining in simple language what top up& super top means. Looking forward to see such enriching posts in future.

I & my family are already covered under my organizations group health insurance. In addition, I had taken an independent standalone health insurance policy from a private company,the renewal for which is approaching soon. Now, after reading through your post, I am thinking of converting my health insurance policy to Supertop up. I have selected United India,because of (a) high claim incurred settlement ratio( your post “best health insurance…..”,dtd sept 21st), and

(b) my group health insurance is being handled by united india, so according to you, its less hassle for primary &top up to be same company .

My query , Is my decision correct? I am unable to get premium online from united india, s0 no idea regarding premium. Also,is there any benefit like no claim bonus (eg higher sum assured)from united india if I purchase the policy before the expiry of my stand alone health policy.

Sreekumar-Even though your employer providing the cover, you MUST own your separate family floater. Hence, instead of cancelling the floater plan, if you feel of coverage not enough, then go for super top up.

Hi basu, i completly agree with you. And my query was exactly regarding that….. I would like to convert my family floater to super top. For my super top up, i have selected( not applied yet,waiting for your valuable opinion) united india supertop up, due to two specific reasons mentioned in my previous mail. Based on those TWO REASONS, am I correct in opting for united india or should i go with supertop up from my current health provider. Also, is there any specific benefits if I port to supertop up before the expiry of my current health coverage.( the renewal of my private health insurance is within next two days). One more request, is there any link to know united india premium online( deductible 5 lakhs)

Sreekumar-What I am suggesting is not to convert family floater. Retain that and if you still need cover, then go for super top up.

Ok. Thanks

Dear Basavaraj Sir,

Can anybody buy two super top up plans together? for ex if some body has 1 lakh mediclaim coverage and he buys 4 lakh super top up plan with 1 lakh deductible, and then he buys another company super top up plan for 5 lakhs with 5 lakh deductible? is it possible? is it wrong? any problems with such things sir? main reason is extended coverage at little less price.

regards

Dr Rajesh Pai B

Rajesh-Nothing wrong and one can buy so. Problem may be service related if insurers are different. Otherwise, legally not an issue.

THANK YOU SIR

sir ur articles r valuable,useful .sir just clear my doubts regarding lic jeevan arogya policy.whether to buy or not

Sudhir-Refer my post “Jeevan Arogya-Do you know this LIC’s Health or Medical Insurance Policy?“.

I’m a regular follower of your blog and wish to congratulate you on educating and empowering people on financial aspects.

My question is – After thoroughly researching on which Health Insurance to buy, I have zeroed in on Apollo Munich. I am 40 years, My wife is 35 and I have two kids aged 10 and 6 years. Between an Individual Optima Restore (10 lakhs each for me and my wife & 5 lakhs each for both the kids) and Optima Restore Family Floater Plan of 15 Lakhs, which one do you suggest? I already have a Health Insurance from New India Assurance for me and my wife for 1 lakh which I am planning to discontinue once i complete the 3 year PEI waiting period on the new one. I am ruling out combining Top-Up plans from two different sectors as it will be very tough to manage in case of claims.

Please advice weighing the Pros and Cons, as going forward we wish to be prepared for any eventuality and changing the plan then would mean going through the Waiting Period for PEI again.

Thanking you in anticipation.

Nag-Individual Optima Restore (10 lakhs each for me and my wife & 5 lakhs each for both the kids).

Thanks a lot Basu ji.

halo sir am new to your blog, could you please help me with a health insurance plan. Am 26 . I would like to have a cover for me and my Parents 56 and 51 . father is diabetic. i earn 30k a month and father has 4 years of service left.

Deepak-Separate your need with your parents need. Refer few companies of public sector for your parents. For you I suggest Apollo, MaxBupa or Religare.

Hello,

My question is if one has a regular family floater plan of 5 lk and top up or supertop up of 10lk. Then what he has access is additional 5 lk and not additional 10 lk? For example if the medical expense is 12 lakh how will it be paid by the insurance company?

Shrinidhi-In that case first Rs.5 lakh will be from base plan. Rest Rs.7 lakh will be from super top up.

I am having reliance family floater health insurance of Rs 5 lakh. As I am 55 yrs old now, can you please suggest it it is advisable to take top up, super top or both. Also what is the minimum coverage amount to take and from which insurer? Many thanks.

Michael-Opt for super top up if you feel the basic cover is sufficient.

How is relaince health policy and L& T super top up plan

Yashpal-Both are good if they match your requirement.

Dear Basava,

Suppose we have pre existing disease like BP/Diabetes, there will be 3-4 yrs waiting period, it means we cant claim anything during this 4 yrs.? What if we pay premiums in time, will the bonus added to Sum assured yearly? I mean no claim bonus. Kindly clarify.

Saleem-Yes, there is a waiting period for existing diseases in health insurance plans. Yes, if the policy offers NCB for claim free years, then definitely it is added.

Thanks Basu

I already have a family floater from National Insurance for 5L.

Now i am planning to buy additional for more coverage.

However , looking at he features for the two shortlisted Health Insurance ie Apollo and Religare.

I am confused should i go ahead and buy fresh Health Insurance or just go ahead with a top up to add extra to my existing health insurance .

Also could you suggest which is the best among Apollo and Religare with respect to features and other factors.

Thank you

Sachin-If you already have base plan, then I suggest to buy top up plan with National Insurance itself. Among Apollo and Religare, both are good when it comes to offering feature.

Dear Sir,

How is ICICI Lombard iHealth Family Floater Plan ? (2 adults + 2 children)

Also it has OPD option ? Is it advisable to go for that option (premium increases by 7K i.e. around 28%) or better to take a health card ?

Thanks very much

Chinmaya-Can you provide the link where they mentioned such OPD option?

suppose i take a family floater top up plan from a company, say for 10l with deductible of 2l. now after 5 yrs, i decide to take a individual health policy for myself(coming out of FF plan). will i get the cumulative benefit of waiting period for preexisting diseases in such case?

To give an eg: I am in the FF top up plan, no illness before, but during the course of time, i get just BP. now after 5 yrs i take an individual full policy instead of FF top up. after some months of taking the new policy i get a heart attack, then will the insurance co reject my claim telling that it is a preexisting disease and there should be waiting for 2ys/3yrs etc.

Suresh-Family floater and invidiual policies are two different categories. You can’t transfer the benefits.

how is reliance health gain policy?

Satish-It is good and if the features matches you then go ahead.

Hi Sir, I’m a keen follower of your blog. After going through your blog posts, i have decided to choose between Religare Care Health Insurance and United India Health Insurance (apart from my company provided family group floater; SI: 2 lakhs).

Cover includes: myself (age:29), my wife(27), my father(59) & mother(51). I cannot afford for individual health insurance and hence planning for 2 floater plans each for (myself&my wife) and for my parents. I’m also planning for a super top up plan above this.

Please help me in choosing between these 2 insurance plans?

Thanks in advance.

Guru Prasad Pandurengan,

Bangalore.

Guru-In my view both are good. But when it comes to features, I feel Religare holds good. You can go ahead with United (Public Sector and may be generous in claims) for your parents and for you Religare. For super top-up, you stick to Religare itself as the claim process for super-top-up may be easy if both basic and top plans are within same insurer.

I m 34 year old with wife and daughter, looking for a healthy insurance plan of 5 lacs for my family.

Please suggest me ASAP

Thanks

Vinay-check with Apollo, MaxBupa, National, New India or Religare.

sir,

i am about 40 yrs with no health issues for me and my family and have no health insurance till now. my family consists of 4 members, myself, wife and 2 minor children. Considering the health cost inflation scenario over next 20-30 years which will be relevant for me, i am planning to take health insurance in the following way.

1. one family floater plan of about 3 lakhs to cover the whole family.

2. a plan for higher amount say 15-20 lakhs( something like religare care), : i wish to take 2 policies, one each covering 1 adult+1 child.

what is your opinion on that

Satish-Go for around Rs.5 lakh regular family floater. Then buy a super top up plan.

thanks for the reply. The advantage of a fresh plan instead of a super top up is the no-claim bonus which can help me accumulate and enhance my insurance cover.Do you suggest to go for a individual super top up or family floater top up?

Satish-Family floater top up.

thanks but i have a few concerns.

As the age advances we do tend to acquire conditions like BP, diabetes etc and the real need for insurance comes then. It would be difficult to go for higher cover at that age and also once we are “diagnosed” of a condition.

There is also a waiting period of upto 3/4 years for preexisting illness.

So a 5lakh FF plan with super top up to say 20L might look good and cheaper now, but suppose i get BP/sugar by 45/50 and i want to sufficiently cover myself for serious illness like heart attack/stroke etc, then porting/enhancing cover at that age might be probably difficult.

I wish to state that iam a man of clean habbits and a medical professional. I am asking this both for myself and also for public in general.

There are many articles on health insurance for the young and senior citizens, but very less info for those starting at 40+. Do think and guide

Satish-It is misconception among us that buying health or life insurance is one-time process. It is not like that. As and when we feel the more liability, then we must increase our insurance. I understand your concerns. But why I suggested the top up is, because it is available for you at cheap and also any claim more than the basic floater will be compensated by this. In my view, insurance must be reviewed once in a five years at least.

what about L & T Super Top -Up plan , I have apply to that

Yes, you can apply.

Thank you for the information sir. I am a govt employee. We have a company provided medical insurance for 2 lakhs + 3 lakhs. First 2 lakhs is for total life time. i.e., any claim sanctioned will be deducted from this 2 lakhs, once claims totalling 2 lakhs completed, balance 3 lakh will come into force. Claims thereafter will be settled from 3 lakhs. This 3 Lakh is for one year, that is every year we get 3 lakhs coverage, after exhausting first 2 lakhs.

My query is i am 38 year old, wish to have 3 to 5 lakh more health insurance.

Plz suggest me how to select policy for my particular case.

Thank you sir.

Srinivas-Both of your existing health insurance covers are with you until you be an employee. But what about at your retirement age? Hence, instead of going for top up health plans, I suggest you to have family floater health insurance.

Sir, both the above policies cover after my retirement also as i will be a pensioner until i deceased.Plz me the nature of policies to take considering the pecular method of policies provided by my employer and I will be pleasured if you suggest 1 or 2 insurers also.

Thank you sir.

Srinivas-Whether there is facility to increase it to higher sum insured from your Rs.2 lakh health insruance?

No sir, it is fixed and onlyafter utilising this 2 lakh, we get additional 3 lakh insurance which refreshes every year since employee contributes a fixed monthly sum towards addl 3 lakh insurance.

Srinivas-My question is whether you can increase the sum insured on your own or there is an option from your employer?

No. We cant enhance the sum insured, neither any options.

Srinivas-In that case use super top up plans. Because initially the claims covered under base plan and later it will be from Rs.3 lakh. Take the cover with thrsehold limit of Rs.5 lakh. If you do that then more than Rs.5 lakh claim be settled by this super top-up plan.

Thank you Mr. Basu. I am a regular follower of ur fb posts and blog. You give us very useful information. Thanks Basu.

I have a general query. I am an employee and covered for both Life Insurance and Health insurance by the Company. Should I parallely get myself insured personally for both. I heard, in case you are insured from multiple insurance companies, all of them can deny the claim. Can you please chalk out a best suitable way to get insured for working people like me in our mid thirties (corporate insurances + personal insurances)

Vineet-Relying on employer-provided health and life insurance will not a great idea. Because you don’t know when you leave the company or new company may offer or not. At the same time, there is no such thing that if one insurer reject the claim then ALL MUST reject it. It is purely dependent on individual insurance companies. Hence, don’t be in such false beleif. Buy your own health and life insurance immediately.

Thank you for this article.

My company has provided us a family health insurance plan and having another personal family floater regular health insurance plan. Both policies are taken from the Oriental Insurance Company.

I shall appreciate, if you can advise, how should we claim, if we have two REGULAR policies and both are from the SAME Insurance company.

Shubh-First use your company insurance to get the claim. If the claim amount is more than that of sum insured in company insurance, then go for your personal health insurance. In that case the claim will be settled through a process of contribution clause (% of sum insured).

Sir nanage 3lac health insurance madabeku yavudu olleyadu heli. Sir

Jagadish-You can check with public sector companies like New India, National or United. From private sectors Star, Apollo, Max or Religare.