We all know there are term plans available in the market for individuals. But when both husband and wife are earning then why to buy separate term insurance and why not buy a Joint Life Term Insurance? Currently, few insurance companies started to offer such plans. Let us see the details of such plans.

In this plan, both husband and wife will be proposer. Hence, a spouse must undergo the medical test and produce the income proof. Along with these mandatory requirements, both husband and wife must submit all other necessary documents.

Currently in the market, there are so many variants of joint life term insurance policies. However, the two main types are as below.

- Insurance companies pay the death claim amount in the event of any one’s death (husband or wife). The policy stops there itself (Also called Single Payout policies). Usually such types of joint life term insurance are cheap.

- Insurance companies pay the death claim amount in the event of any one’s death (husband or wife). The surviving spouse will be covered for the sum assured as usual (few may offer premium waiver benefits).

Now let us consider the situations, where spouse bought Rs.1 Cr Joint Life Term Insurance. How the claim be settled in different situations. I considered the basic feature of Joint Life Term Insurance.

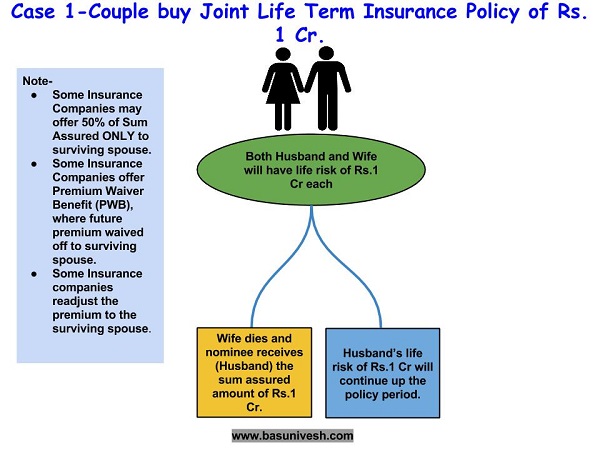

Case 1-

In this case, either a wife or husband dies and the sum insured will be payable to the nominee (husband). The future premium will be waived off. Surviving spouse’s life risk will continue as usual up to the remaining policy period. However, as I mentioned in the above note, few companies may offer 50% of the sum assured to the surviving spouse. Another point to note is, few companies have the inbuilt premium waiver benefit, but some may offer it as an additional rider (for which you have to pay the extra premium). Finally, few companies either continue the same premium rate for a surviving spouse or reduce it as the number of insured will come down.

What I explained above is a simple example of the joint life term insurance. However, check with individual insurance companies before going for such joint life term insurance products.

Case 2-

In the above case, death of a spouse occurs together. In such situation, nominee will receive the sum assured amount. Policy terminates there itself.

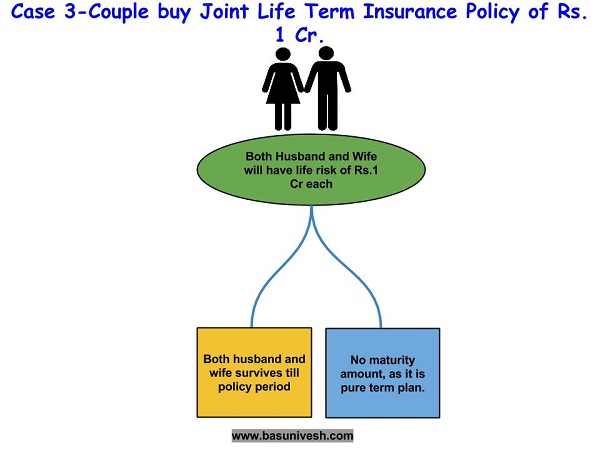

Case 3-

In this case, both husband and wife survive until policy period. As this is pure term plan, both will not get any maturity benefit and policy closes at the maturity date.

Advantages of Joint Life Term Insurance-

- Ease of manage-By holding a single policy, it is easy for a couple to manage their life insurance need.

- Premium Benefit-Instead of buying an individual policy, if you go with a joint life term insurance policy, then the premium will get reduced.

- Some joint life term insurance policies consider the average age of spouse, which may be beneficial in terms of premium rate consideration. However, do remember that some insurance companies may consider the age of the spouse who is older (like family floater health insurance policies).

Disadvantages of Joint Life Term Insurance–

- In the name of joint Life Insurance, your agent may sell you joint life ENDOWMENT PLAN. Hence, be cautious while buying.

- In case spouse death occurs together, then nominee receive on the sum assured. However, if spouse buys separate term insurance, then death claim amount will be based on individual policies sum assured.

- In case of single payout policies, the surviving spouse has to continue without any life insurance.

- If wife stayed away from the job due to managing kids, then no insurance required for her. However, buying such joint life insurance may hard to discontinue, in such situation or separate insured.

- In case of divorce, it is hard to delete any one insured and continue the policy. Either you have to continue the policy in joint name or discontinue.

Which companies currently offer such joint life term insurance products?

Currently, few companies offer such policies with a variety of features. Some of them are as below.

- PNB MetLife’s Mera Term Plan

- Aegon Religare’s iSpouse

- Bajaj Allianz iSecure

Note-As I said above, there is no uniformity of features among all joint life term insurance policies. Hence, check for features carefully before jumping into it.

You may also like our earliest posts-

- 5 ways to save your Term Insurance premium

- 5 Things to do after buying online term insurance

- Best online Term Insurance Plans in India for 2015-A comparative list

- Online Term Insurance in India-Beware before buying !!!

- Why your Insurance Agent not sold you Term Insurance?

Dear Basavaraj ji,

Me and my wife both are working. My wife is a govt employee,

I am having term insurance of kotak life insurance with Rs 75 Lakh risk cover.

Now i am looking to purchase term insurance for my wife also.

Please suggest where individual term plan is better or we should go with joint term plan.

Vaibhav-In my view, go for separate plans.

Should i add any rider in term plan?

Wife’s income is 6.00 lakh per anum. I am planning to buy max term plan with risk cover 75 lakh for the age of 62 years as retirement age is same.

Please suggest.

Vaibhav-No need to add any riders. Buy them separately. Ideal Life Insurance cover must be around 15-20 times of your yearly income+Liability.

Hi Sir,

After reading few comments about term insurance for spouse have following queries.

– Any specific reason why insurance companies do not offer insurance for housewife except for fact no dependency on them financially ?

– Is it possible for someone self employed and earns and files Income tax every year to apply for Term insurance ?

– What documents are required as proof of income to apply for term insurance, ITR documents will suffice ?

Thanks

Raj

Raj-1) One need an insurance NOT TO PROFIT but to protect the LOSS.

2) YES.

3) ITR documents.

Hello Sir,

Thank you for your answer.

Recently after I posted comment here was just thinking if this may hold valid or not.

– Even though lady may be housewife but there is still dependency on her w.r.t managing household responsibilities.

– Taking care of kids and other activities, while in case of working women its outsourced to other family members or day cares.

Agree we do not realize the real value add in terms of financial support but taking example of Miss world winner’s statement mother is the one who deserve high paycheck so if there is dependency on her the insurance companies should not deny insurance I feel.

Thanks

Raj-1) Financial dependency is different than household dependency.

2) It may be, but is there any financial loss involved?

Sir,

In real terms no financial loss, but it will lead to financial expenses for sure 🙂

my 2 cents : As an financial expert you can better asess the financial implications of hiring someone for each of chores & responsibilities and having someone take care of it.

I understand your point & insurance companies point of view.

Thanks

Raj-Then if you are worried about 2 cents of financial implication, cover the life risk to that extent only. But in reality, if the person has no earning, then how comes the financial loss to his or her dependents?

i have been jobless for more than a year and hence i have not earned any income in this period. Can I buy term insurance?

Dear Neeraj,

Sadly NO.

Dear Basavaraj Sir,

Is there any perticular reason why Housewife (Non earning) females are NOT offered Term Insurance? otherwise they are as vulnerable as working women for diseases and all other things, then why insurance companies do NOT offer the term insurance to Non earning females?

regards

RAJESH PAI B

Rajesh-Forget about Term Insurance, even normal insurance also not available for non-working individuals. You have to buy life insurance when someone is financially dependent on him or her.

Hello Sir

My self Dheeraj ag 33 Years, Married and Father of a 3 years kId. I am holding a Maxnewyork wholelife participation Policy, which is a traditional plan.

I am looking to surrender this policy, as it is having a very less sum assured. But it is increasing like a tortoise speed as company buy additional sun assured with the annual bonus declared by them. I am not finding it suitable enough. So thinking yo surrender it.

Also, my wife is working as a private teacher, I am thinking to buy a Joint Life Term insurance of around 75 Lacs to 1 Cr. Please suggest some good plan. and would the amount sufficient till the max age of 70?

Dheeraj-Better to go for individual plans than JOINT.

Thanks Basavaraj Sir,

You have suggested to go for Individual Plan, but how can i buy cover for my wife. No insurance company provide Term plan for Housewife/person with no legal income. As i told she has just started working as a private teacher and her Employer does not provide salary slip/Form 16. Please suggest, still should i go for individual Term plan.

Also, i am waiting for your response on Maxnewyork wholelife participation Policy, which is a traditional plan. Shall i continue with this policy or Surrender it ?

Dheeraj-I don’t think at this juncture she need cover. Hence, better now you buy on your own. Once she start to get enough income and also income proof, then buy term plan on her name.

Never ever try to buy the so called products which combine Insurance with investment (whether they are whole life, endowment or moneyback)

If we file a Income tax return for a lady to take term insurance.. is it mandatory to pay premium by lady or her husband can pay & claim rebate u/s 80c.

Is there any complication in insurance claim if it is done so & at any time claim is presented on casualty

Pradeep-Husband can also pay the premium and claim tax benefits.

Is there any complication in insurance claim if it is done so & at any time claim is presented on casualty

Pradeep-No, there will not be any problem in claim settlement.

Hi

basunivesh ji why not required house wife insurance ple

Ranjeet-Think about the requirement of insurance. When you have earning then your family feel the burden if sudden demise of you. However, for non-earning person, there will be no financial burden on his/her dependents. The concept of life insurance is to compensate the financial loss. Hence, no insurance companies offer life insurance to non-earning person. That is the reason, if wife is not earning, then life insurance is not required for her.

Basuji, I recently tried applying for LIC online e-term plan for my pregnant wife. But it shows that this plan is unavailable for pregnant ladies.. why s it so? What are the other alternatives?

Thanks

Abhishek

Abhishek-No company offers insurance to pregnant women. She can buy after giving birth to kid (again there will be some waiting period like after 6 months of pregnancy or so).

Sir, I am having online e term policy from maxlife insurance for Rs.25 lakshs taken two years back. My wife and me are Govt. employees. My wife is not having any term policy. Now I would like to enhance my term policy amount from 25 lakhs to 50 lakhs. What I have to do ? Whether I should take separate term policies (one is for me to enhance term policy amount and another one is new term policy for my wife) or joint term policy covering both of us. Which Insurance company can u suggest ? Taking term policy with riders is good or not ? if term policy with riders is good, which riders should I take ? with regards.

Kishore-You can’t enhance the existing term insurance. You have to buy the new policy. In my view, better to stick to individual plans without riders.

Sir, why are you not suggesting riders with term policy, can u pls explain in detail. Is it possible to take riders separately. If yes which insurance company is best.

Kishore-When you buy riders with life insurance, then they restrict the sum assured and also will not get full features of benefit which you get by buying direct accidental or critical illness insurance. Hence, it is of no use to combine. There are many general insurance companies which offers accidental and critical illness insurance.

Hi Basu,

I am regular reader of this blog. Also asked many questions on insurance.

I have 1.5 crore term insurance and 50 lakh corporate term plan. I have taken Jeevan Sathi policy from LIC

in 2007 with Sum assured RS/-220000 for 21 years where i have to pay around 250000.

I dont know how much i will get after full term. Till now I have already paid around 1 lakh. Do I need to continue or surrender. I am planning to surrender the policy and rest 1.5 lakh amount for 13 years will invest in PPF in my child account. Also invest these surrender amount in Fixed deposit or PPF. In that way I will get more than what I was told by LIC agent for mature amount(around 5 lakh) after 21 year.

My wife is housewife and this policy is a joint life policy.

Please advice???

Thanks,

Pradipta

Pradipta-You are on right track and go ahead. If your wife is housewife, then at first instance she don’t need any insurance. Second thing, this is a typical endowment plan. Hence, returns may be around 5% to 6%. Also, instead of using PPF you can go with equity oriented balanced funds to enhance your return expectation.

Hi Basu,

Does LIC offer Joint term insurance and is it worth taking it?

Ajith-Currently LIC not offers this facility. I listed both positive and negative side of this feature. Please go through above post and if it suites your requirement, then go ahead.