Last year I published the list of Top 10 Best SIP Mutual Funds to invest in India in 2016. Now few started to force me to publish the post for Top 10 Best SIP Mutual Funds to invest in India in 2017. But before proceeding further, let us review the funds which I recommended last year.

Note:-My recommendations for the year 2018 are available in below posts. Please refer the same.

Below is the performance report of the funds which I recommended last year.

Before jumping into the selection of mutual funds, this time I thought to guide you why you MUST invest in equity mutual funds. The points are listed as below.

You must have a proper Financial Goal

I noticed that many of investors simply invest in mutual funds just they have some surplus money. The second reason may be someone guided that mutual funds are best in long run compared to Bank FDs, PPF, RDs, or even LIC endowment product.

If you have clarity like why you are investing, when you need money and how much you need money at that time, then you will get the better clarity in selecting the product. Hence, first identify your financial goals.

You must know the current cost of that particular goal. Along with that, you must also know the inflation rate associated with that particular goal. Remember that each financial goal to have it’s own inflation rate. For example, education or marriage cost of your kid’s is different inflation that the inflation rate of household expenses.

By identifying the current cost, time horizon and inflation rate of that particular goal, you can easily find out the future cost of that goal. This future cost of the goal is your target amount.

Asset Allocation is MUST

Next step is to identify the asset allocation. Whether it is short term goal or long term goal, the proper asset allocation between debt and equity is a must. I personally prefer the below asset allocation. Remember that it may differ from individual to individual. However, the basic idea of asset allocation is to protect your money and smoothly sail to reach the financial goals.

If the goal is below 5 years-Don’t touch equity product. Use the debt products of your choice like FDs, RDs or Debt Funds.

If the goal is 5 years to 10 years-Allocate debt:equity in the ratio of 40:60.

If the goal is more than 10 years-Allocate debt:equity in the ratio of 30:70.

While choosing debt product, make sure that the maturity period of the product must match your financial goals. For example, PPF is best debt product. However, it must match your financial goals. If the PPF maturity period is 13 years and your goal is 10 years, then you will fall short of meeting your financial goals.

Return Expectation

Next and the biggest step is the return expectation from each asset class. For equity, you can expect around 10% to 12% return. For debt, you can expect around 7% return expectation.

When your expectations are defined, then there is less probability of deviating or taking knee-jerk reactions to the volatility.

Portfolio Return Expectation

Once you understand how much is your return expectation from each asset class, then the next step is to identify the return expectation from the portfolio.

Let us say you defined the asset allocation of debt:equity as 30:70. Return expectation from debt is 7% and equity is 10%, then the overall portfolio return expectation is as below.

(70% x 10%) + (30% x 7%)=9.1%.

How much to invest?

Once the goals are defined with target amount, asset allocations is done, return expectation from each asset class is defined, then the final step is to identify the amount to invest each month.

There are two ways to do. One is constant monthly SIP throughout the goal period. Second is increasing some fixed % each year up to the goal period. Decide which suits best to you.

Hope the above information will give you clarity before jumping into equity mutual fund products.

How many mutual funds are enough?

How many mutual funds do we have? Is it 1, 3, 5 or more than 5? The answer is simple…you don’t need more than 3-4 funds for investing in mutual funds. Whether your investment is Rs.1,000 a month or Rs.1 lakh a month. With the maximum of 3-4 funds, you can easily create a diversified equity portfolio.

Having more fund does not give you enough diversification. Instead, in many cases, it may create you portfolio overlapping and leads to underperformance.

Now let us move to the selection of mutual funds.

How I selected Top 10 Best SIP Mutual Funds to invest in India in 2017?

I will first screen the top 15 funds in each category based on their returns to benchmark since inception. The funds who consistently beaten the benchmark are listed in that 15. Once I have the list in my hand, then I select the funds based on Risk-Return Analyzer.

Many simply select the funds based on eye-catching returns. However, at what cost the fund is giving you a better return? To what extent it protects my investment during a downturn is what differentiate from good fund to bad fund.

Again, I am not saying that these 1o funds alone be considered as “Top 10 Best SIP Mutual Funds to invest in India in 2017”. There may be fewer other funds, which are good to compete with these funds. However, I may be biased towards few Mutual Fund Companies (purely on their size and how long they are in MF business in India). Below are the metrics I used to arrive at finally selecting the funds.

If the fund cleared all these tests and given me around a minimum of 80% score since inception, will be added to my list.

- Beta-Volatility measure and tell how much the fund changes for a given change in the Index. Lower the beta, lower the volatility. Hence, your fund must have lower beta.

- Standard deviation-It tells us how for a given set of returns, how much do fund returns deviate from the average. Lower the standard deviation, lower the volatility. Hence, your fund must have lower beta.

- Alpha-It is the risk-adjusted measure. By taking risks, how much the fund manager generated the return over the benchmark. Higher the alpha, higher the outperformance of the fund.

- Sharpe Ratio-It is the risk-adjusted measure. Higher the Sharpe ratio, better is the performance.

- Sortino Ratio-It is the risk-adjusted measure. Higher the Sortino ratio, better is the performance.

- Treynor Ratio-It is also be known as reward ratio. Higher the Treynor ratio, better is the performance.

- Information Ratio-This is calculated by average excess return obtained compared to a benchmark and divides it by the standard deviation of excess returns. Higher the information ratio, higher the consistency in beating the benchmark.

- Omega Ratio- It is a risk-return performance measure of an investment asset.

- Downside deviation-This is also be called as BAD RISK.

- Upside potential-This is exactly the opposite of Downside deviation.

- R-squared- It is a measure of how correlated the fund’s NAV movement is with its index.

- SIP Returns-For how many times the fund’s returns are above the index when we invest in SIP.

- Lump Sum Returns-For how many times the fund’s returns are above the index when we invest in a lump sum.

Below are my selection in each category of funds.

Best SIP Mutual Funds to invest in India in 2017 -Large Cap

In this category, I found that funds like SBI Bluechip and Birla Sunlife Frontline Equity Fund are also best. However, I am going with below choices.

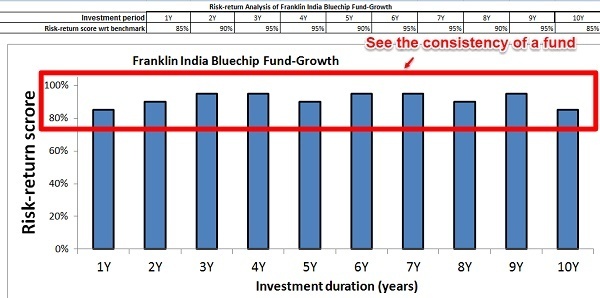

Check the consistency of Franklin India Bluechip Fund from this below image.

Check the consistency ratio of ICICI Pru Focussed Bluechip Fund in the below image.

As I said above, there are other funds also which scores equal or more than these two funds. But I stick to these two funds. There is no reason of negating these two funds.

Best SIP Mutual Funds to invest in India in 2017 -Multi Cap

Again in this category of funds, I found few funds like SBI Magnum Multiplier Fund and Franklin India High Growth Companies Fund. However, I stick to below two funds and which are my favorite too.

Check the consistency ratio of Franklin India Prima Plus Fund in below image.

You may notice that for a 1-year return the score is dropped below 80 and currently showing as 70. However, due to it’s long best track record, I suggest to invest and continue in the same fund (if few already invested in this fund).

Check the consistency ratio of ICICI Pru Value Discovery Fund in below image.

Same is the case with ICICI Fund also. However, considering the consistency and just a drop in that for a year does not mean that we must neglect this fund. Hence, I will stick to this fund.

Best SIP Mutual Funds to invest in India in 2017 -Mid Cap

Last year I selected HDFC Midcap Opp Fund and also Franklin India Prima Fund. I am continuing with same funds.

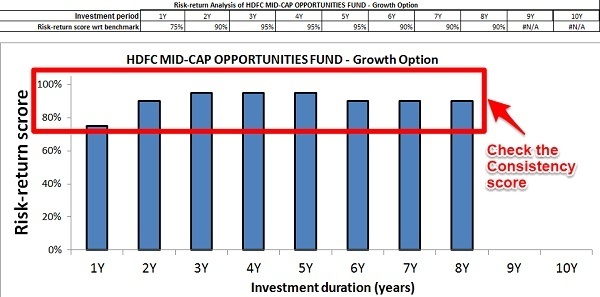

Check the consistency performance of HDFC Mid Cap Opp Fund in below image.

Check the consistency performance of Franklin India Prima Fund in below image.

A drop in a year from both funds does not mean they are BAD. Hence, considering the consistency of fund since long, I am suggesting these two as best funds.

Best SIP Mutual Funds to invest in India in 2017 -Small Cap

In small cap category, the funds in my mind are Canara Robeco Emerging Equities Fund, DSPBR Micro Cap Fund, and Franklin India Smaller Companies Fund. In these three, I go with DSPBR and Franklin.

I am unable to generate the consistency score for both the funds. I will update the image once I am able to do so. However, these two funds are my favorite among small cap.

Best SIP Mutual Funds to invest in India in 2017 -Equity Oriented Balanced Funds

Among this category, I have in mind the funds like HDFC Balanced Fund, ICICI Pru Balanced Fund, Tata balanced Fund and Franklin India Balanced Fund. But I go with HDFC and ICICI.

These are my choices of Best SIP Mutual Funds to invest in India in 2017. It does not mean that they are universal choices. There are certain other funds too. However, I stick to these funds as my best choices.

NOTE:-I have disabled commenting to this post. If you have a doubts or questions, then refer my latest post “Top 10 Best SIP Mutual Funds to invest in India in 2018” OR raise the doubts in BasuNivesh Forum.

Refer our other posts related to Mutual Fund Investment in 2017-

- Top 5 Best ELSS Tax Saving Mutual Funds to invest in 2017

- Top 5 Best Liquid Mutual Funds in India in 2017

- Top and Best Debt Mutual Funds in India for 2017

- Mutual Fund Taxation FY 2017-18 and Capital Gain Tax Rates

Dear Basavaraj,

Can you advise best Ultra Short term/ Short term debit funds for Debit investment use after 8 Years. How about one of these ?

SBI Magnum Gilt Fund – Short Term – Regular Plan – Growth

SBI Magnum Gilt Fund – Long Term – Regular Plan – Growth

Kumar-Refer my post “Top and Best Debt Mutual Funds in India for 2017“.

Sir,

I’m 31 years old with 8L salary p.a. I have been already investing in PPF for last 2 years of Rs. 75,00 per annum. I have Term & Health insurance. My next goal is Child’s education, wait time is 13 – 15 years and planning to invest in MFs with SIP Rs. 5,000 per month, however still at analysis stage. I’m a moderate risk take and have below clarifications.

1. How should i diversify my funds b/w Large, Mid & Small Cap funds. What should be the ratio?

2. Can i skip Large cap and focus only on Mid and Small cap funds alone?

3. Can you suggest funds for my case, advise from experts like you is really beneficial. I will surely analyze them before investing.

I would like to sincerely appreciate you on the excellent service/suggestions you do on Financial planning.

Correction in the above, my PPF investment is Rs. 75,000 per year.

Pradeep-1) There is no such defined rule. But I usually follow 50:30:20.

2) Large-cap also necessary.

3) My funds are already listed in above post.

Sir,

Thanks for your suggestion.

Hello Basavaraj,

I am Govt Employee 35 Year Old. I like to invest with following Portfolio for marriage of my daughter in next 18 years. I am moderate risk taker. My asset allocation in Equity:Debt is 45:55.

My FD having 500000 will get matured in January 2018. I am planning to invest this amount using STP again for 10 years. Please advice which fund is suitable to do this or please advice other plan to utilize this money with time horizon of 10 Years.

Kotal Select Focus(D) 3200

HDFC MidCAP Opprtunities(D) 3200

Motilal Oswal MOSt Focused Multicap(D) 35 Fund 3200

ICICI Pru Balance Fund(D) 3200

L&T Emerging Businesses Fund(D) 3200

Aditya Birla Sun Life Tax Relief 96 (G)(D) 4000

Total 20K per month

Besides this, I have

PPF 100000 Annual

NPS 9000 Monthly

FD 500000 (January 2018 maturity)

My query is, should I go for any new funds or increase investments in existing funds? I would just like you to review my mutual funds selection and would like to know your thoughts on it. If any changes you think is needed then please suggest.

Shreeja-Try to follow the asset allocation of around 30:70 between debt and equity. Regarding the fresh investment, use the same existing funds with proper asset allocation. You just need 2-3 funds from equity.

Hello Sir,

I am 35 Year Old and take Home salary is 3.50Lakhs per month.

Started Investing 3 months back, having SIP profile below with clear 15 Years Investment Horizon. Please advise me on my Current Portfolio. Does it require any change by adding or removing fund? My plan is to Stay Invested for a longer period & the motive is Wealth creation over a period of time.

My Risk appetite is Moderate to high. Asset Allocation (Equity:Debt) 70:30

LUMPSUM (3years Horizon)

Kotak Corporate Bond Direct 25Lakh

SBI Magnum Gilt Fund Direct 25Lakh

Franklin India Low Duration Fund Direct 25Lakh

SBI Magnum Income Direct Plan Direct 25Lakh

S I P(Monthly)

LARGE CAP

SBI Bluechip Fund Direct 13000/-

Aditya Birla Sun Life Frontline Equity Fund Direct 13000/-

Kotak Select Focus Fund Direct 13000/-

MID CAP

Mirae Emerging Bluechip Direct 10000/-

L&T Midcap Fund Direct 10000/-

SMALL CAP

DSP BlackRock Micro Cap Fund Direct 10000/-

BALANCED FUND

HDFC Balanced Fund Direct 10000/-

MULTICAP

L&T India Value fund Direct 10000/-

ELSS

Tata India Tax Savings Fund Direct 11000/-

Total Monthly SIP 100000/-

Suknya S.Yojna 1.5L Per Annum (since last 3 years)

PPF 1.5L Per Annum (since last 6 years)

NPS 120000 Per Annum (since last 6 years)

Mediclaim Annual Premium 15000/-

NFO ETF value worth Rs 100000

Contingency amount 500000 in Liquid Fund

I am in position to invest another surplus monthly amount worth 200000 with 3 Year horizon keeping in mind. Please guide me for how to utilize this portion as well.

I currently do not have any debt upon me. Hence looking for an opinion whether I should increase my SIP / exit or invest in any others that would probably be more preferable then any of the above.

Anil-For short-term goal, use Ultra Short Term or Short Term Gilt Funds. For long term goals, refer my above post of how to adhere to allocation and funds. You no need to have multiple funds within same cateogry.

Sir, Thank you for your reply. I value your suggestion. I also see it crowded and remove unnecessary fund and will keep it straight and result oriented. I will modify and follow funds below:

2 In large Cap

1 each in Small, Mid, Multi, ELSS and Balanced Fund.

I hope this will make the portfolio balanced and yield good returns, I expect not more than 10-12%

For monthly 2,00000/ will certainly opt short term.

Dear Basavaraj,

To have a good retirement corpus, planning to invest in balanced funds as they follow Debit:Equity in 30:70 ratio. Also, thinking to keep 20% of my invest in ultra short term debit funds. I don’t want to touch this fund in next 5 years.

planning to invest in lump-sum method and considering HDFC balanced fund. Is this OK or should I consider any other options. Is lump-sum better or should I invest in SIP in 6 months with weekly investment?

Let me know your feedback on balanced fund and lump-sum approach

Regards,

S. Kumar

Kumar-Whether your retirement is 5 years away from today? What allocation you are following between equity and debt? If the goal is long term (5+ years) and you did proper asset allocation, then spread your equity investment manually into not more than 5-6 months of investment than a lump sum.

Thanks Basavaraj Ji.

I will follow your advise and span it across 5-6 months instead one shot lump-sum. My allocation was 40% Debit in Short Term/Ultra Short Term and 60% equity and I am going to touch the corpus only after 8 years.

On 40% Debit allocation, part of balanced fund, assuming that 30% of investment will be in debit and 60% will be in equity. For remaining 10% debit (for total 40%), I would like to invest in Short Term/Ultra Short Term.

Is this OK?

Read in the first line that 40% debit (30% through Balanced fund and 10% in Short Term/Ultra Short Term

Kumar-Go ahead.

Many Thanks for your time, kind review and advise

BasavaRaj,

Another query on alternate to balanced Fund and go with below allocation.

Ultra Short term/Short Term : 40%

Large cap: 30%

Mid cap: 20%

Small cap: 10%

Span the lump sum investment in 4-5 months manually (preferably buying Daily)

Is the above allocation is OK or better to go with Balanced as per my above post on 21-Nov.

Can I Split Debit 40% between Ultra Short term 20% and Short Term 20%

Kumar-You can do so.

Dear Basavaraj,

For Debit portion, Can I consider NPS Tier1 account Government Bond Pland (Class G) ?

In Debit MFs & NPS- Class G investments, which one is safe among each other?

Kumar-They are risk as they hold long term gilt and other debt bonds.

Many Thanks Basavaraj.

Can you advise best Ultra Short term/ Short term debit funds for Debit investment use after 8 Years. How about one of these two?

SBI Magnum Gilt Fund – Short Term – Regular Plan – Growth

SBI Magnum Gilt Fund – Long Term – Regular Plan – Growth

Kumar-Refer my post “Top and Best Debt Mutual Funds in India for 2017“.

Dear Sir,

I am from Belgaum.

Can you please suggest Financial advisers in Belgaum?

Thanks

SRM

Shrinivas-No idea. Sorry.

Dear Vasu Sir,

I am 37 years and have a kid of 5 years. Have following investments. Want your opinion on my investments for any changes considering the long term returns, 10 years or above (wealth generation for my kids’ education). I am also planning to open “Sukanya Samriddhi Account” for here in new year with 2000 investment each month. Do I need to change my investments , especially MFs (or add more) . If so please guide.

Note : I started investing in MFs from this month only and your blogs guided me a lot.

Eagerly waiting for your advice.

Best regards,

Sanjeev

PPF @12000 PM

EPF-EPS with my company contribution @13424PM

National Pension System-NPS @5000 (Started in Dec 2016)

Cooperative Society @2000 PM

HDFC- RD @2000 PM (ending in Jul 2019)

ICICI- RD @2000 PM (ending in Sep 2018)

MFs :

Equity- Large Cap @1000-SBI Blue Chip Growth

Equity- Large Cap @1000-ICICI Pru Focussed Bluechip Fund -Growth

Equity-Mid & Small Cap @1000-Franklin India Smaller Companies fund- growth

Equity-Mid Small Cap @1000-Reliance small cap fund- High risk high return

Equity-Diversified @1000-Franklin India High Growth Company Fund

Debt-Short Term @1000-Birla Sun Life Short Term – Growth

Sanjeev-What prompted you to go ahead with this plan and why you started to doubt yourself within a MONTH of investment?

Hi Basu Sir- Thanks for your comments

What prompted me ?

For conventional plan like PPF, NPS , CS and RDs : I just wanted to make saving. Frankly speaking, I was not much aware about other ways of savings. I just went with what my guardians and peers were doing to save money and taxes. I will love to continue with PPF, NPS, CS, and Sukanya Samriddhi

For MFs : I recently went to one meeting where they discussed about MFs, Shares, Gold, and other modes for high interest rate compared to other mode (they also discussed risks). I selected and invested (before I experienced your blog) these funds based on my own research online and discussion with few seniors investing in MFs.

Doubt :

The more I read or try to explore, more doubts come in my mind about my investments whether it is a right start or not ? I also want to increase (about double) my SIP amount in early 2018.

I just want to have your guidance on my current investments if it needs any changes considering my goal of wealth generation for my kid.

As usual , thanks for your advice.

Best regards,

Sanjeev

Sanjeev-Refer my above post fully (not the funds I listed). Wait for a year or so, then check the fund performance.

Will do so. Thanks a lot.

Best regards,

Sanjeev

Hi Basu,

I have one doubt. These days many foreign companies are working in India in Mutual funds industry. We are investing them in for say 10 years or more. Is it completely safe like what if they wind up their business in India after few years, so is it completely safe?

Thank you.

Pradeep-Nothing is safe on this earth including the money you are keeping money in your savings account. However, there are strict regulations by SEBI. They can’t wind up their business so easily.

Basavaraj Sir,

In your view which is better safe/ preference :

1) NPS

2) Mutual fund Co.

Saptarshi-Safety in what sense?

Hello Basu, Hope you are doing well. Just curious to know about the commission on MFs which we invest. When I was going through the NSDL report . I could see commission paid to the distributor comes around 2 to 3 % in total. When I had checked with my financial adviser, he told me that, if I invest for at least three years, there won’t be any deduction for the withdrawal and I have got few funds in ICICI securities , it’s same for them also. Apart from that , I have received email from ICICI securities , If our mutual fund holdings are less than 8 Lacs on the date of transaction, you will be charged the transaction charges as additional one.So I would wanted to check if we can transfer the mutual funds directly to originator or is there any better option to transfer the funds. Please advise.

Thank you,

Karthik Gangadharan

_

Karthik-Check the exit load and taxability of each fund you are holding before moving from regular to direct. ICICI Securities provides ONLY regular funds but not direct funds.

ok, thank you Basavaraj !

Hello Basu,

I am 30 yr old unmarried.i have invested in below.

Ppf- 2k/month

Axis long tem equity -2k/month.

Wants to start sip of 2k or 3k for next 5 years.can you plz suggest funds for my portfolio.

Abhi-As per me, if your time horizon is just 5 years, then stay away from equity investment.

Hi Basu ,

Many thanks for answering my previous queries! This time a new query for which my portfolio details are below

My goal : Retirement corpus

Investment Tenure: 20 years

Risk ability: Moderate

Investing last 1.5 years in the Debt: Equity ratio 65:35. Debt is EPF & VPF

Equity proposition : 50% Large cap, 30% mid , 10% – small and 10 % – multi (ELSS for tax saving) – 4 funds

Now I want to top up amounts my portfolio:

Recent announcement of FM Arun Jatley(2.11 lakh crore investment towards PSU development) had made me to think in investing Banking sector fund with 10% and my choice would be “ICICI Prudential Banking and Financial Services Fund ” in this space.

Would you advise go with this fund or would you suggest to increase/top up in existing fund? please advise.

As a golden rule, I will maintain the asset allocation according to the new top up. 🙂

Hari-Never chase them or a particular sector. I simply give a miss to such news based ups and downs.

Thanks Basu for your suggestion!

Hello Basu,

I had few SIP’s under a broker since Jan2015. I now understand importance of Direct and Regular fund. I want to invest in mutual funds myself henceforth. So i stopped those SIP. My query is –

1. Whether to redeem that money and pay Capital Gain? Then invest lumpsum in a fund and then start new SIP direct mode.

2. Or Keep the money until i require them and for now, just start new SIP direct mode.

3. Or Wait for 1 year, take LTCG benefit and then invest lumpsum in a fund and then go for a new SIP direct mode.

Sumit-Better to wait for 1 year completion (if they are equity funds). Then move all such one year completed units to direct. In the meantime start a SIP freshly in direct fund.

Hi,

Thanks for the reply.

Since i’m planning to invest in direct mutual funds through Zerodha’s Coin platform, I can’t transfer/move the amount (after 1 year) directly, so you suggest to redeem the amount and buy directly, right?

Sumit-Zerodha offers direct and makes you to hold it in demat account, which is not required. Yes, redeem and buy in direct is the way.

Hi Basu,

Interested to purchase a Direct Balanced MF through CAMS. Already, few MF’s running under CAMS through AMC.

Plan:

Investing Rs 1Lakh /year for 5years and excess amount is deposited after 5years also.

Withdrawal amount: Rs 2500/month and extra like Rs 1000/- withdraw after 5years only.

Please suggest me, which Fund suits me.

Thanks & Regards,

Praveen

Praveen-Refer above post properly.

Hai Mr. Basu,

I Am Anvesh. Age 25. I want to invest 10-15k in a month

I have shotlist the follwing funds:

1. Aditya Birla Sun Life Front Line Quity Fund – Growth

2. Mirae Asset Emerging Fund – Regular Growth

3. Principal Emerging Bluechip Fund – Growth

4. Canara Robeco Emerging Equities – Regular Plan – Growth

5. Kotak Select Focus Fund – Growth

6. L&T India Value Fund – Regular Plan – Growth

Can you please suggest whether the portifolio is too risky. Also, if you feel so, please suggest other funds

Thanks in Advance

Anvesh

Anvesh-How you arrived at these funds? What is the time horizon? What asset allocation you are following?

Dear sir, This is Rama Bhadra Rao, 32 years old. I am working in Taiwan and will be back to India after 5 years. I plan to invest 5L (Lump sum) in mutual funds. I do not want to use this amount for another 15 years (or above). Could you please let me know what are the best funds. I am very grateful to you if you can help to update the plan given below. Thanks a lot for your kind help.

As per my knowledge (1 L in each, total 5 ):

1. Large Cap Equity (Kotak Select Fund direct Growth )

2. Mid and small Cap Equity (L&T emerging businesses fund Direct Growth)

3. Diversified Equity fund (Principal Emerging Bluechip Fund – Direct Plan (G) )

4. Balanced Equity based fund (HDFC Balanced Fund )

5. Infrastructure Equity fund (DSP BR Natural Resources & New Energy – Direct (G))

I am expecting 15% average returns per year.

Thank you very much for your kind help.

Adari-How you arrived at these funds?

Hi, Thank You very much for your kind reply. I grab the list of funds from ,oney control based on last 5 years performance (reruns). Let me know your suggestion to meet my goal.

Adari-Sure..Go ahead.

Thank You very much for your kind reply and suggestion.

I will invest 2.5 L now (50000 in each). I will wait for a couple o months to put the remaining 2.5L for the same funds (market may come down in a couple of moths). Let me know if I am wrong.

Thanks a lot for your great help.

Adari-How you assume that market will come down?

Just fear… because market is at peak now.

Adari-If you have long term view and did proper asset allocation, then you no need to worry.

suppose if we invest almost 8-10 year compare in Large cap & mid cap cap which fund should continue in this both for risk & return wise i expect better return and low risk can i go with only mid cap fund because i seen large cap return good in long term

Jai-Contradictory statement “can i go with only mid cap fund because i seen large cap return good in long term”.

sorry my question is “can i go with only mid cap fund for up to 10 year because i seen large cap return is not good in long term as expected mid cap because i expect 18-20% return ”.

Jai-Mid caps may be eye catching during such bull run. But large caps gives you consistency. Same way small caps are more catchy than mid and large cap. But with risk. Decide what you do.

thank you for your clarifications

and

multicap risk factors also low as compare midcap??

Jai-Multicap funds have the mandate to move any market cap. Hence, it is hard to say whether less or riskier.

Hello Basuji,

I have MF investments in following funds. All are DIRECT-Growth using SIP. Started in Oct 2015.

My age is 32 and investments are for 18 years.

Axis long term ELSS – 4k/m

Aditya birla sunlife Top 100 – 3.5k/m

HDFC balanced – 2.5k/m

Mirae asset emerging bluechip – 3k/m

I am handling my debt investments using PPF and FD. (equity:debt = 70:30)

Questions:

1. Is my portfolio on track. Do I need to perform any changes to my investments.

2. Is it advisable to add one multi cap fund or should i increase my SIP amount instead.

3. Is it true to understand Axis long term MF as a multicap fund in addition to its 80C benefits. (Reason being it as 25~30% investments in mid cap companies)

Mukul-Yes fine but review once in a year must. Regarding axis, it is more inclined to large cap with around 50% and rest spread in between small and mid cap.

i have separate portfolio with 5 different fund house for direct plan is that good or i need to move at signal place (like- zerodha) for all invest means is that secure to invest with MF fund house directly because i am not able to track my all fund at one place .

Lokesh-Refer my post “Best Direct Mutual Funds Platforms in India to invest online“.

Your explanation on every point is wonderful

Lokesh-Pleasure.

I would like to extend my thank to you . You did wonderful blog ! Appreciate your efforts .. Long way to go bro 🙂

Karthik-Pleasure 🙂

Dear Basu

I need additional amount about 50 lakhs in next 3 years for buying a bigger home . For this goal alone what should be the monthly SIP and which segment large cap/mid cap and which fund house you recommend. Please guide

Seema-For such short-term goal, stay away from equity-related products. Stick to Ultra Short Term Debt Funds.

Hi basu,

Your work is highly appreciated.Thanks a lot for your valuable service.

I have already investing in SIP and have identified goals and accordingly invested in SIP ,PPF with 70% in equity and 30% debt with time horizon of more than 10 years.

However,I still have around 30 lakh in my saving account which i dont need in near future atleast 7-8 years.What is the best way to invest this money?

Sravan-Same process. Do the asset allocation and if you feel fear to invest lump sum in one go, then spread that for parts of not more than a year.

Thanks basu..but i do not have any financial goal to invest remaining money.Is is wise to invest lumsump in ultrashort term or gilt fund as safer option? Thanks in advance.

Sravan-You use Short Term Gilt Funds.

Dear Mr.Basu Ji,

This blog is very informative and knowledgeable and Many Many Thanks for this. I ‘ve below queries for your valuable feedback.

Q1).

I am 44 year old and planning for retirement investment some 50 lacs. Out of this I want to put 25lacs(from property sale) as lumpsum now and remaining 25 lacs to accumulate to a good amount in 10 years of time and then take the returns through SWP. Here are the funds I am planning to consider the below funds. Please advise.

a). HDFC Balanced Fund (20%) = 5 lacs Lumpsum + 5 lacs SIP

b). L&T India Value fund (20%) = 5 lacs Lumpsum + 5 lacs SIP

c). Franklin Build India high grown companies fund(20%) = 5 lacs Lumpsum + 5 lacs SIP

d). Mirae asset emerging blue chip fund (40%) = 10 lacs Lumpsum + 10 lacs SIP

Q2). I would like to invest 25 lacs through SIP for my children’s education in next two years. would like to accumulate returns to take the returns after 8 years from now. For this I am considering the below funds. Please advise these are OK or any better funds you suggest..

a). L& T Prudence Fund – 8 lacs

b). SBI Magnum Mid cap fund – 8 lacs

c). Mirae asset emerging blue chip fund – 9 lacs.

Kumar-1) How much asset allocation you did between debt and equity?

2) Again you missed the asset allocation.

Thanks Basu for the feedback.

Considering your valuable feedback and following the principle 30:70, I planning to make the allocations as below.

Retirement: Would like to invest 60lacs as almost lump-sum and Expecting returns to take after 7 Years. (25 lacs lump-sum and another 25 lacs SIP in 4 months]. Here is my plan and allotments

a). HDFC Balanced Fund (50%) = 15 lacs Lump-sum + 15 lacs SIP

b). Reliance Monthly Income Plan-Growth Plan (10%) = 3 lacs lump-sum + 3 lacs SIP

c).DSP BlackRock Micro Cap Fund – Regular – Growth (15%) = 4.5 lacs lumpsum + 4.5 lacs SIP

d). ICICI Prudential Value discovery fund (10%) = 3 lacs lump-sum + 3 lacs SIP

e). Mirae Asset Emerging Bluechip Fund -Regular- Growth Option(10%)=3 lacs lump-sum + 3 lacs SIP

Child Education: [25 lacs SIP in tw0 years and expecting to take only after 8 years from now for my children education]

i). HDFC Children Gift Fund-Investment – 8 lacs SIP in 2 years

j). Aditya Birla Sun Life Balanced 95 Fund – Regular Plan-Growth – 7 lacs – SIP in 2 years

k). Mirae Asset India Opportunities Fund – Growth Plan – 5 lacs SIP in 2 years

l). Aditya Birla Sun Life Tax Relief ’96 – Growth Option – 5 lacs SIP in 2 years

Is the above allotment for the said purposes is OK or any other expert suggestion to change allotments or other funds for consideration.

Thanks in Advance for your time and feedback.

Kumar-For your 7 and 8 years goals, 30:70 is bit risky. I suggest around 50:50 or 40:60. Also, for all such goals, in equity one large cap (60%), one mid cap (30%) and one small cap (10%) enough. For debt, use ultra short term debt funds or short term gilt funds.

Dear Basu,

Thanks for yourfeedback.

I can take moderate risk and per your feedback, changed the allotmnets to as below.

Balanced Equity: HDFC Balanced fund (10 lacs), L&T Prudence Fund (10 lacs)

Large Cap: Kotak Select Focus fund (5 lacs)

Diversified: Mirae Asset India Opportunities Fund(7.5 lacs)

Mid & Small cap: DSP BlackRock Micro Cap Fund(7.5 lacs) & Mirae Asset Emerging Bluechip Fund (5 lacs)

Balanced Debt to reduce risk : Reliance Monthly Income Plan (5lacs)

Can you review and provide your valuable advise on the above fund combination. If anything to be changed, please let me know.

Thanks in advance

Kumar-Whether you checked the balanced funds portfolio of equity and debt? Why MIP in debt? Why two funds within same categories?

Dear Basu,

Thanks. I missed a point that fund selection should not only be on category and should also the fund portfolio whether it is matching our purpose.

In HDFC balanced fund, 31.25% is under debit and L&T Prudance 24% is under Debit.

It was mistake that I mentioned MIP in debit. In Debit, my choice is Aditya Birla Sun Life Dynamic Bond Fund – Growth

Under Mid & Small, I will stick to Mirae Asset Emerging Bluechip Fund due to its low standard deviation, low beta and high alpha compared to DSP BR Micro cap fund.

Here is modified fund selection further to your feedback.

Balanced Equity: HDFC Balanced fund (10 lacs), L&T Prudence Fund (10 lacs)

Large Cap: Kotak Select Focus fund (5 lacs)

Diversified: Mirae Asset India Opportunities Fund(7.5 lacs)

Mid & Small cap: Mirae Asset Emerging Bluechip Fund (12.5 lacs)

Debt Fund : Aditya Birla Sun Life Dynamic Bond Fund – Growth (5lacs)

Is the above OK or still you suggest to increase Debit %?

Please let me know your expert inputs on the above MF Portfolio composition as lump-sum investment. Next 8 years I do not want to touch this as the purpose is for retirement corpus building.

Kumar-In debt, I will not go beyond short term or ultra short term debt funds. Because you have already enough volatility in equity. For 8 years plan stay away from small cap. One large cap and one mid cap enough with separate debt fund.

Thanks again for the feedback.

I’ve chosen Mirae Asset Emerging Bluechip Fund and thought it is mid cap. Please confirm is this Mid cap or small cap fund. Under Short Term debit Debit, Aditya Birla Sun Life Treasury Optimizer Fund. Here is the MF portfolio list after suggested modifications

Balanced Equity: HDFC Balanced fund (10 lacs), L&T Prudence Fund (10 lacs)

Large Cap: Kotak Select Focus fund (5 lacs)

Diversified: Mirae Asset India Opportunities Fund(7.5 lacs)

Mid cap: Mirae Asset Emerging Bluechip Fund (12.5 lacs)

Short Term Debt :Aditya Birla Sun Life Treasury Optimizer Fund. (5lacs)

Is the above list is OK or any other changes to be made? Please suggest funds still I need to consider to make the MF Portfolio stronger for 8 years Retirement fund

Thanks in Advance

Kumar-It is large cap with around 70% in large cap and another 30% spread in mid and small cap. I don’t think any reason to go for two balanced funds in fact with balanced funds when you specifically allocating between debt and equity.

I PUT 200000/- IN franklin ultra short bond fund super institutional plan IS THAT OK FOR ONE YEAR?

AND MY sip IS

1- Sbi MEGNUM MID CAP -2000/-

2- Franklin Smaller cap fund 2500/-

3- Mirae Asset Emerging Bluechip Fund 1500/-

For 5 Year Horizon please suggest me sir if any change need in portfolio

Lokesh-You can go ahead. If your time horizon is 5 years, don’t touch equity.

dear sir

i want invest

5 lac lumsum as per your suggestion which fund is better expected return 10 time fram maximum 2 year

Lokesh-Invest either in liquid funds or ultra short term debt funds.

Dear sir

I want 1 crore after 20 years. My investment is following

1) SBI emerging business fund-1000

2) reliance tax saver-2500

3) Birla tax relief 96-1500

4) IDFC premium equity-2000

5) Birla frontline equity-2000

6) Birla India gennext -2000

7) Franklin smaller fund-3000

8) Kotak select focus-2000

9) reliance gold fund-1000

Kindly guide me if any chance regarding to achieve my goals.

Ritesh-Frist follow the asset allocation and choose the funds based on that. You no need to require so many funds.

Thanks for your reply,

I have made some changes in the list. Pl suggest is this OK.

S.No Fund Name Investment amount Tenure

1 Birla sunlife front line equity fund 3500 >10 years

2 ICICI Pru value discovery fund 2000 >10 years

3 HDFC Balanced fund 1500 >10 years

4 HDFC Mid cap opp fund 3500 5-10 years

5 SBI Magnum gilt fund 1500 5 years

Shiva-Please refer above post properly and the asset allocation you have to do. You included Midcap fund for 5-10 years. Not sure when the goal is. There is a huge gap of 5 years between 5th and 10th year.

Dear Mr. Basu,

I have planned to invest 10k monthly through SIP. Pl advice whether the below proposition is good for the tenure I choose.

S.No Fund Name Investment amount Tenure

1 Birla sunlife front line equity fund 3000 >10 years

2 ICICI Pru value discovery fund 2000 >10 years

3 HDFC Mid cap opp fund 2000 >10 years

4 HDFC Balanced fund 2000 5 years

5 SBI Magnum gilt fund 2000 5 years

Shiva-For each time horizon, you must have a proper asset allocation. Where is the debt allocation for your 10 years goal? Please refer above post properly.

Hi Basu,

I have read many blogs related to this topic but you were taken a place in my mind. It is really very different in comparison with other blogs. Yours was the most unique and attractive one. You actually really write something different and real.

Nisha-Thanks for your kind words 🙂

Hi Basu sir,

please review my portfolio:

Investment Time Horizon is 15 years.

I am investing 10000 per month in the below mutual funds.

1)Franklin india blue chip fund(G) -5000

2)HDFC midcap opportunities fund(G)-3000

3)Franklin india smaller companies fund(G)-2000

And PPF-5000

My overall Equity:Debt allocation is 70:30 (10000:5000).

i also invested Rs.200000/-lumpsum in ultra short term debt fund(Birla sunlife floating rate fund(G)-direct) for 10 years.

please let me know,is my portfolio balanced ?

Thanks in advance…

Sukumar-Why Rs.2,00,000 lump sum in short term debt fund? Why not you did the asset allocation for that also?

Hi Basu Sir,

Could you please review my portfolio below

I have been investing 30000 since last 2 years in the below mutual funds.

ICICI Pru Focused Bluechip fund- 6000

Reliance Small Cap fund- 9000

HDFC Mid Cap Opportunity Fund-9000

HDFC Balanced Fund-6000

PF- 6000

Investment Time Horizon-12 years

I am considering balanced fund and PF for my debit portion. Overall Equity and debit portfolio allocation is as below

Equity : Debit= 70:30 (24000:12000 – As i said that I am considering balanced fund and PF for my debit portion.)

Could you please let me know that if my portfolio is balanced.

Thanks in advance!!!

Jitendra-Check the overlap with HDFC Balanced to other funds. If they are not that much, then you can hold and continue. Also, instead of higher exposure to large cap, you have given more importance to mid and small cap. Increase exposure to large cap and then mid cap and in small portion towards small cap.

Thanks a lot sir for quick response. I will increase some more exposure to large cap.

I am thinking to alloate money in the below ratio.

Large cap- 30%

Mid cap – 30%

Small cap-20%

Balanced- 20%

Please let me know if equity allocation is fine for 12 years.

Thanks in advance!!!

Jitendra-You may go ahead.

What is your perspective of not keeping ABSL Advantage Fund in your selection?

Sudipta-What prompted you to select this fund?

Hello. My age is 37. I had sips running earlier for 3 years. Now i am planning following 4 sips.

1. Kotak select focus fund G Rs. 5000

2. A birla frontline equity G Rs. 5000

3. Hdfc midcap oppn fund G Rs. 5000

4. Mirrae asset emerging bluechip G Rs. 5000.

The objective is wealth creation over long term over 10-15 years. Can you please advice if this looks ok?

Andy-10 years or 15 years? Be specific at first. Second thing, what asset allocation you are following? What are the funds where you already investing?

Hello

It is 15 yrs to be specific. The asset allocation is 30 :70 where 70 is equity. I have current sip running in Franklin India bluechip growth, icicipru focused bluechip G and hdfc midcap opp fund all totalling to Rs.10000.

Andy-Then why can’t retain the same ONE LARGE CAP and the same mid cap?

Hi Basu,

Hope u r doing well!My present investments are as follows:

SIP

Franklin india prima plus growth direct-5000/pm

Franklin’s india smaller companies fund direct-4000/pm

Pf-15000/pm

Post office rd-5000/pm

Now I wish to invest further total 10000 per month in equity mf devided in 2 sip,duration- 10+ yrs and 3-5 yrs.My plan is as below:

HDFC balanced fund-4000 pm-3-5yrs

Icici Pru focussed blue chip /frankline ind blue chip fund or

Any other large cap fund- 6000/pm-10+yrs

Kindly give ur valuable advice about my overall portfolio and new investments.

Waiting for your feedback.

Shekhar-First thing, if your time horizon is around 3-5 years, then don’t enter into equity. Second thing, regarding the investing or rejig in current portfolio, hold one large cap, one mid cap and small portion of small cap fund enough in equity. Regarding debt, if PF or Post Office RD maturity in line with your financial goal, then you can continue. Otherwise, try to use debt funds.

Thanks for quick response.

Re my mf portfolio as per ur advice one small cap ( Franklin smaller companies fund) is there. One multi cap(Franklin prima plus) I am holding.Now I have 2 questions.

1. I wish to add one large cap I am confused between icici focussed blue chip fund and Franklin blue chip fund.

2.Further one mid cap fund should be there as u advised. Kindly clarify one multi cap (Franklin prima plus which i am holding) will solve the purpose of having exclusive mid cap fund.Your insight is requested to finalise my investment/ shuffling in portfolio.

With Regards,

Shekhar

Shekhar-1) Franklin.

2) The problem with the multi cap is that they have the mandate to move in any market cap segment. Hence, at any one point you may have higher exposure towards one single market cap without your notice. Hence, I suggest separate mid cap.

Hello Sir,

I am a 33 Years old salaried professional. Presently, I do not have any equity exposure and have around Rs.5 Lakh in my debt portfolio inclusive of FDs, NSCs and PPF A/c in the ratio 3:1:5. Additionally, I have investible surplus funds of around Rs. 1.5 lakh ,which I want to invest in Mutual Funds and have thought of the below mentioned plans.

Further, I also plan to invest in 2 SIP plans worth Rs.2500/- each per month which will come out o fmy monthly salary. As you can see below, I have included some debt funds also as I plan to increase the amount proportionately in the same funds in the years to come. Kindly advise whether or not I should go for it and what changes can be made in my portfolio:

Lumpsum Investments:

Large Cap Equity – Birla Sunlife Frontline Equity Fund (Growth, Direct Plan) – Rs.50000/-

Mid Cap Equity – HDFC Mid Cap Opportunities Fund (Growth, Direct Plan) – Rs.30000/-

Small Cap Equity – Franklin India Smaller Companies Fund (Growth, Direct Plan) – Rs.20000/-

Short Term Debt Fund – Franklin India Low Duration Fund – Rs.25000/-

Gilt Short Term Debt – SBI Magnum Gilt Fund – Rs.25000/-

TOTAL ——————-

Rs.150000/-

——————-

SIP:

Large Cap Equity – SBI Bluechip Fund (Growth, Direct Plan) – Rs.2500/-

Dynamic Bond – ICICI Prudential Long Term Fund – Rs.2500/-

——————-

Rs.5000/- p.m

——————-

Regards

PKA-You have not shared the time horizon. However, by referring my suggestion, you can follow the same.

I would not be needing the above mentioned lump sum amount for another 5 years

PKA-If time horizon is just 5 years, then DON”T ENTER INTO EQUITY PRODUCTS.

Hello Sir

I want to enter MF investments starting from this year, I am 30 yrs old married. No kids.

I currently hold 5 lakhs of savings in my FDs+RDs. I already have Medical insurance and Term insurance plan.

I am saving 1.5 lakhs each year in PPF and save 20k pm in RDs.

Can you please suggest if my picks are correct for entering into MF for getting most out of it after 5-7 years of time.

1. FranklinIndia Prima Plus Growth (Large CAP)- 5k pm

2. SBI Magnum Midcap Find Growth- 5k pm

Vikas-Refer my post properly and then think of what is the meaning of GETTING MOST OUT OF IT.

Ok, thanks Sir. Need your opinion if I should keep on investing in RDs or should I go for MFs.

Also, please let me know if you have personal finance planning solutions.

Vikas-It depends on many things like MF or RD. How can I say you without understanding?

Thanks sir for all your suggestions.Only one more thing are u happy with the performance of icici long term equity fund or I should switch to some other ELSS fund.If I have to switch kindly suggest me some other ELSS FUND.

Aji-What prompted you to doubt that fund?

Sir it is not performing well from last one year looking at its peer in ELSS

Thanks sir for your prompt reply. All the fund mentioned above I have invested with the aim of more than 10 years. And birla sunlife fund which I mentioned above may be read as birla sunlife front line equity fund. All the other fund are clear.

Sir plz guide now.

Aji-Increase more towards large cap and then to mid cap and finally around Rs.1,000 into small cap. Restrict your exposure to small cap as your tenure is 10 years.

Basu Sir by your advice I have created following portfolio 3 years back.

1)icici long term equity fund 4000 sip

2)hdfc midcap 1000 sip

3)birla sun life 1000 sip

4) Franklin India smaller comp fund 2000.

I have debt ammmont of around 60000 in ppf lic pli etc per annum

Thanks sir for your kind advice at that time.I n fact it is because of u I become financial literate.

Do you think my portfolio is OK at present time or u recommend certain change.

Sir plz reply

Aji-What asset allocation you are following? Also, you have not specified the full names of funds. Hence, hard to guide.

I am following 60:40 asset allocation in equity:debt

Hello Sir,

I have MF investments in following funds. All are DIRECT-Growth using SIP. Started in oct 2015.

My age is 32 and investments are for 18 years.

Axis long term ELSS – 4k/m

ICICI pru val discovery – 2.5k/m

HDFC balanced – 2.5k/m

Mirae asset emerging bluechip – 3k/m

I am handling my debt investments using PPF – 30K yearly and 2oK in FD.

Questions:

1. Is my portfolio on track.

2. I am not planning to add any other fund.

Mukul-What % of asset allocation you are following between debt and equity?

Sir,

I am following 70:30 (equity:debt). In additiona to (PPF+FD) in debt part I have one Jeewan saral LIC policy, Premium 25K per year. Policy will be expiring in next 4 years. I have no plans to surrender this policy.

Mukul-Come out from multicap and include one large cap.

Sir,

Thanks for writing.

1. Any specific reason for leaving multicap (ICICI pru value discovery).

2. can you suggest one large cap fund..

Mukul-The only disadvantage is that you can’t track their moment and at the certain stage your portfolio may be tilted more towards one market cap. Hence, better to avoid. Large cap list is available in above post.

Hi Sir, Icici Pru value discovery fund seems not performing in the last 1 year. Pl advice whether to hold or shift the portfolio to other fund.

Shiva-HOLD.

Respected Sir,

Myself Saranya Ravi a pvt. school teacher, monthly income rs.20000 pm. I am new to Mutual fund, My friend who is working in ICICI Direct account. Through his guidance I opened an account and invest the amount in below Mutual Funds as Lump sum… to hold atleastfor atleast 3 to 4 yrs for 5yrs old daughter savings.

1. Reliance Small cap fund (R) – Rs.25000 Lumpsum

2. L&T Emerging Business fund(R) – Rs.25000 Lumpsum

3. Hdfc Prudence fund (R) – Rs, 25000 Lumpsum

4. Axis Dynamic Equity fund (R) – Rs.50000 lumpsum.

Respected Sir, Now I need your valuable opinion whether the above MF investment is Ok or I have to quit from any MF or Modify any MF. Please give me your valuable reply to correct my Portfolios… Since I am very new to this MF investing. Waiting for your kind and valuable reply sir. Thank you very much sir.

Saranya-I confused with your statement. You are planning for your kids future who is currently at 5 years of age. But claiming that you want to hold this just for 3-4 years. If your intention is to hold for 3-4 years, then DON”T ENTER INTO EQUITY.

Also, investing in Mutual Funds through ICICI Direct is the costliest way of investment. Demat account is not at all required for investing in mutual funds.

Respected Sir, Thanks for your immediate response and advise me to move out from ICICI Direct. However Now, I had already invested the above MF’s last month. Now kindly please suggest me whether the above MF’s is good to holding for long term gain or is there any MF’s should be avoided or to change the MF portfolio. Awaiting for your valuable guidance.

Regards,

Saranya.R

SaranyaRavi-Good or bad you will come to know if you read above post properly like what you have to do before you jump into investing.

Hi Basu,

I need your help in guiding for a specific financial goal in my life.

For my child’s higher education after 15 years, I want to save Rs 35 lakhs.

I have around 3 lakhs in NSC/PPF in my wife’s name currently which might grow up to 10 lakhs.

So I want to build a corpus of remaining 25 lakhs in equity/mutual funds. I can invest up to 7k/month.

In the above situation, on which mutual funds should I invest?

Please guide me.

Regards,

Gajapathi

Gajapathi-Refer above post. Especially the first part of the gyaan.

Hi Basu ,

Hope you are really doing well.

Can’t thank you enough for the financial knowledge you are sharing.

I am outlining my Investment MF Portfolio with you and need your valuable insight into it. I do have a investment time horizon of about 20/25 Years. I am planning to start investing 21K (Equity:Debt: 70:30) per month in

below Funds with a yearly increase of 10%.

1)ICICI Pru Focused Bluechip Equity Fund(G) – 8000 – Large Cap

2)Franklin India Prima Fund(G) – 3000 – Midcap

3)HDFC Balanced Fund(G) – 3000 – Equity Balance Fund

4)Franklin India Smaller Companies Fund(G) – 2000 – Small Cap

5)PPF – 5000 -Debt

Kindly advise if the above mentioned funds are good to go ahead with and do i need to add any more Fund to my Portfolio.

Thanks a Ton…

Regards

Amiya

Amiya-Go ahead and review once in a year.

Thanks a lot for your help….

Sir ,

I have a sip of 5000 per month in ICICI VALUE DISCOVERY FUND for the last 3 years.

The fund is not performing well for the last 1 year .

The AUM has also become enormous:17000cr.

Shall I stop my sip? And start in another multicap fund.

Is the gigantic AUM causing its downfall?

Please advise

Regards

Sameer

Sameer-How you felt that fund is under performing? What was your expectation while investing? How much is the fund generating? There is a misconception that AUM harm the performance. But do remember that such theories are copycat of the foreign market (which is much bigger than ours).

hi,

what is your advise with regard to starting new SIPs in funds which have stopped taking lumpsum investments and restricted monthly investment values? Probably the fund manager is already overburdened and is it wise to stay away for new investments?

There are some conflicting reviews about HDFC mid cap opp fund, FI prima funds. DO you suggest fresh SIPs in these funds?

Sreenivas-Do you think that particular ONE fund is the UNIVERSAL BEST? Don’t be so attached to fund, fund house or fund manager. You have to think what is required for YOU.

Hi Basu,

I am having 4000 monthly SIP of ICICI Prudential Focused Bluechip Equity Fund – Growth.

Last week I decided of adding 4000 more to this existing SIP but by mistake I created a SIP for ICICI Prudential Focused Bluechip Equity Fund – Direct Plan – Growth

Queries

1) Please let me know if returns are same for ICICI Prudential Focused Bluechip Equity Fund – Growth and ICICI

Prudential Focused Bluechip Equity Fund – Direct Plan – Growth.

2) Please suggest shall I stop the SIP for new Direct Plan – Growth and again create ICICI Prudential Focused

Bluechip Equity Fund – Growth.

Regards,

Rishi

Rishi-1) Direct scores more return over regular around 1% to 1.5%.

2) First understand the difference between DIRECT and REGULAR, then we discuss further.

Thanks Basu. Looks everything same in terms of portfolio. May be I wl continue with this Direct plan 🙂

Rishi-Better.

Hello Sir,

I kindly require your valuable advise on the below doubts with respect to MF investing only.

Let say I am 30 years now and i want to invest in mutual fund for 20 years,

Risk appetite – High,

Say i can start with 5k p/m & and increasing with certain % on yearly basis, with expected return of 10% to 12% at the end of 30 years (i.e, 20year investing & 10 year wait period =30years total, as I require the amount from my 61st year. )

So further going with allocation on the basis of 70 : 30 (Equity : Debt) –

1) Franklin India Bluechip Fund (G) – 2k p/m

2) ICICI Pru Value Discovery Fund (G) – 1.5k p/m

3) Birla Sun Life short term fund – 1.5k p/m

Now my question is :

1) Am I on the right direction towards investing in MF as per above details? If yes

2) Is the allocation ok or do I have to add or delete anything

3) Can I transact through AMC online or MFutility as I can monitor on my own.

If any other suggestions please advise

Kindly waiting for your kind reply.

Regards.

Madhu-Your investable amount is less. Hence, we can’t select each category of fund. However, better you include one large cap and one mid cap in equity. In debt, you can either use PPF, EPF or Ultra Short Term Debt Fund. Better to use MFU as it is one place for all your funds to review and monitor.

Hi Basu

Hope you are doing well

I am a beginner and wants to invest in Mutual funds, already gone through with your post and suggestions however not sure how and where to start. Target is to have enough money for kid education by 2028 which is 10 years from now

Just to give you a background –

1. Already having a PPF account with nominal savings say 1K per month and thinking to increase

2. LIC Jeevan Anand with 7 Lac sum assured

3. Term insurance – don’t have & wanted to buy

4. Medical insurance – Only corporate, should I buy personal as well?

Jasvinder-What is your doubt after reading above post. Can you raise those specific questions?

Hi –

Need suggestion on following, my target is 10 years from now

1. Equity – which MF to start with, large/mid/small or balanced. I am targeting Franklin with 5K-10K per month, please suggest

2. Debt – Is 1ooK a year in PPF sensible or should I think something else as well

3. LIC – Should I keep it till maturity or surrender it now, I am having 2 Jeevan Anand (3ooK & 400K sum insured for 16 years and 21 years respectively initiated in 2009 & 2010)

Jasvinder-1) One large, one mid and small portion of small cap.

2) Your time horizon is 10 years, then how can a product which is 15 years (PPF) suitable for you?

3) In my view better to surrender.

Sorry, I forgot to mention that PPF account is 5 years old so I would be able to withdraw by 2028 hence asking for 100K-150K of deposit for remaining period. Also while going through internet, it seems depositing yearly amount between 1st to 5th April every year will yield maximum benefit in PPF.

Requesting your guidance

Jasvinder-Then you can use PPF as debt part. Yes, investing before 1st to 5th of every month or in April has some advantage.

HI Basu,

Recently only i came to know about your website. I found it very interesting and very helpful in improving our financial knowledge. I have following funds with me. Please let me know your inputs:

SBI Bluechip (1000 SIP)

DSP BR Focus 25 (1000 SIP)

ICICI Value discovery (1000 SIP)

HDFC Mid cap (1000 SIP)

DSP Micro cap (1000 SIP)

TATA Tax saving (1000 SIP) – Though i have selected this fund for tax savings. But since i invest in PPF, so i don’t need this fund.

ICICI Balanced fund (1000 SIP)

Birla sunline MIP Savings 5 – dividend payout (For lumpsum investment)

Problem is that i don’t have clear objectives for my investments. My only objective is to maximize my returns in the SAFEST manner. All my investments are long term.

Please let me know your inputs.

Saurabh-Can you define what is MAXIMIZE returns and SAFEST manner?

by maximize i want to point out interest rate scenario that we have today. Icici is offer 6.75 ROI and considering that i am in 30% tax bracket, i hardly make any money from FD’s.

That is why i am looking for other investment options (after exhausting my PPF limit) that can give me better returns. Since i am looking for long term investment, so equity exposure seems OK to me.

SAFEST – Here i believe that markets are very high these days. I want to be bit cautious while investing. Birla sunlife MIP i have chosen as a alternative of FD. Not sure if my decision is good.

Saurabh-Whether MIPs are safest? Above that which is SAFEST? The art of INVESTMENT is art of managing RISK. Don’t chase returns based on the market cycle. But go for equity and debt based on the time horizon of the goal. This is what I explained in above post.

Hi Basu I hope you are doing well thanks a lot for the valuable article I will be starting SIP as an example, I have 100 INR amount invest per month , time horizon 10 Years+ for all and Equity to Debt ratio 70:30

35 INR SIP PM in SBI Bluechip G

21 INR Mirae Asset Emerging Bluechip Fund (G)

14 INR SIP in DSPBR micro cap fund G

Debt:-

30 INR PM in PM time horizon again 10+years , if there is any Fund that can be better that it on second best please advise also

1. Please advise if you think there is some correction needed

2. Please advise if I have to top up the funds by parking some surplus money with similar time horizon objective, can i follow same pattern

3. Please advise if you have to change any funds in Debt and Equity

4. Please advise how to allocate balance fund like HDFC Balanced Fund (G) by exchanging any of above

Shahnawaz-It looks fine. But for DSPBR fund as of now you can’t invest. Regarding, debt, what product you selected? Whether it is for SIP or top up, you can use the same funds for the set time horizon with same asset allocation.

Thanks can you replace DSPBR with HDFC Balanced Fund (G) please advise or suggest anything else

In addition please advise any DEBt for 10+ years time horizon still not able to finalize although read your article

Shahnawaz-My list is already shared in above post. You already asked that doubt regarding debt funds in another post. Please refer my reply.

sir i 47yr, I am investing given below funds. Do you think my portfolio is ok or should i change?

Please Reply

Thanks in advance.

BSL Resurgent India Fund Series 1 Growth Regular

Sundaram Select Microcap SR 9-5 Year Regular Growth

HDFC Long Term Advantage Fund Regular Plan Divident

HDFC Mid-Cap Oppertunities Fund Regular Plan Growth (SIP) Rs.1000/m

HDFC Balanced Fund Regular Plan Growth-(SIP) Rs.3000/m

ICICI Prudential Value Disvovery Fund Growth (SIP) Rs.1000/m

IDFC Balanced Fund Regular Plan Growth (SIP) Rs.1000/m

IDFC Dynamic Equity Fund Regular Plan Growth (SIP) Rs.1000/m

IDFC Tax Advantage Fund (ELSS)Divident Regular Plan (SIP) Rs.1000/m

Kumar

Kumar-Without knowing time horizon of goal, asset allocation, and your personal finance life, it is hard for me to guide anything.

Dear basu.. lot of people asking for funds for goals.. many of Ppeople like us dnt know how to set goals which are more practical.. i request n suggest u give some time and write an article about setting goals n accordingly choosing funds. Some very generic goals with different aged people as example… so that most of us can get clear picture of Goals n funds for them… i thought after reading the new article people can ask u specific n clear questions….

Thanks

Prashant-Thanks for your inputs and definitely I will come up with an article on this.

Hi Basu first of all thanks a lot for this great article and advice, in your article as you advise the one should invest in maximum 3-4 funds based on goals , but I just need to know how we can choose between large cap, multi cap I mean can those 3-4 fund can be all all multi cap or large cap or mid cap or one fund from each category e.t.c

In addition talking of about debt:equity as 30:70 , debt here can be one of of debt mutual fund in your other posts or it should be only bank FD, RD or PPF or it should be mix of both, how to mange this

Appreciate your advice

Regards

Shahnawaz-One large, one mid and one small cap fund enough for equity. It can be any debt product like FD, RD, PPF, EPF or Debt Funds (based on your goal time horizon and comfort with the product).

Hi Basu,

Appreciate if you could write an article on the way to rebalance mutual fund portfolio year on year basis.

Ajith-Thanks for your inputs. Surely I will write a post soon on this.

Hi Basu,

Whats your opinion for ETF equity fund and index fund. They are good for investing for 20 years?

Naveen-It may be but the problem is liquidity.

What problem liquidity? I new to mf can you elaborate?

Hi I am 35, Started investing this year. Currently have the following SIP’s

HDFC Prudence Fund – 2000

Birla Sun lime Small & Mid Cap – 2000

ICICI Pru Value Discovery – 1000

Mirae India Opportunities fund -1000

I am planning to add a liquid fund and also Blue Chip fund to this portfolio. Planning Franklin BlueChip & Birla Sun life Cash plus.

Your advice?

Time Horizon 20 years

Subramani-What allocation % you are performing between debt and equity? If time horizon is 20 years, then why the liquid fund? Whether you checked the overlap of the portfolio in the existing investment?

Basu,

Thanks for your reply.

I am planning to shift a portion of my emergency funds to Liquid fund. The Liquid fund I am planning for a year to 18 month SIP of Rs 5000 and then let the investment continue.

I have not really checked the portfolio overlap. Will do so over the weekend. I have an MIP which focuses on debt funds at around Rs 4000 per month.

I am fine with a riskier portfolio in my first 10 years as I want to maximize the returns over the 10 year period, before rebalancing.

So I was thinking my Portfolio lacks a largecap/bluechip fund and obviously the liquid fund for the near-term.

Subramani-But do you feel HIGHER RISK ALWAYS LEADS TO HIGHER RETURN??

Well I do not mean a 20% return as a high return. I would be happy between 12%-15% return over the next 10 year period. Which I think is reasonable on these funds.

Subramani-Then go ahead if you are confident of.

Dear Basu,

I am 36 and planning to invest Rs.10K per month in the asset allocation between Debt(30%) and Equity(70%)

Time Horizon – 10 years for my Kid’s education and marriage

Planning to move all my matured fixed deposits close to 1.5L in MFs

So far, my MF SIP investments for the past year are split-up accordingly

With Motilal Oswal – 30 K

———————————-

SBI MAGNUM MULTICAP FUND (Exit load period not over yet)

RELIANCE SMALL CAP FUND – GROWTH PLAN ((Exit load period not over yet)

RELIANCE TOP 200 FUND – GROWTH PLAN (Exit load period not over yet)

With Motilal and Funds India

——————————–

SBI BLUE CHIP FUND- GROWTH

With Funds India – 1.25 L

————————————————

Birla SL Dynamic Bond-Fund-Reg

Birla SL Frontline Equity Fund (G)

Birla SL Treasury OPtimizer Plan (G)

Franklin India Prima Plus Fund (G)

HDFC Balanced Fund(G)

Mirae Asset Emerging Bluechip-Reg(G)

I have gone through your post which made me think to regulate my MFs.

I am planning to move all my existing MFs to Zerodha (or) MF Utility

Large cap

—————–

Franklin India BlueChip

Mid Cap

——————————-

HDFC Mid Cap Opp Fund (G)

Ultra short term or short term gilt debt funds

———————————————————

Franklin India Smaller Companies Fund (G)

Need your suggestion,

(1) If I had made right decision to move all MFs to mentioned diversification

(2) Your thoughts on Zerodha and MF Utility

(3) Should I invest some amount in PPF also ?

(4) Is it worth to move Reliance and SBI Magnum before exit period gets over ?

Dear Basu,

Could you please confirm if the distribution looks fine ?

Ramanathan-For 10 years goal, make sure to have proper asset allocation. Yes, your final fund selection is good for equity. But for debt choose ultra short term debt fund or short term gilt funds. In my view MFU is best than Zerodha as MFU is completely free. Your goal time horizon is 10 years but PPF is 15 years product. Hence, this product is not suitable to you. Stick to 2-3 funds in equity and one fund in debt. This much is enough.

Dear Basu, Thanks for your suggestion.

My Asset Allocation- Equity- 70%- Debt 30% Out of 70% in Equity, 40% in Large Cap and 30% in Mid-Cap and

Out of 30% in Debt-Ultra short term or short term gilt debt funds, I thought

Franklin India Smaller Companies Fund (G) is the one. Can you please confirm ?.

Also, For 15 years plan,

I am investing Rs.2000/- in Sukanya Samriddhi account for my daughters marriage.

If it’s for 15 years, Can I continue with Sukanya Samriddhi investment or I can opt for PPF

Ramanathan-In Equity-50% in large, 30% in mid and 20% in small cap. Your debt is OK. I am not fond of this Govt scheme. Because I feel now this Govt launched it and giving highest return. However, if Govt changes then they may not be so aggressive like this Govt. Instead, I prefer PPF.

Hi Basunivesh,

I would like to invest in below funds:

for large cap : ICICI Pru focussed blue chip Equity fund (OR) – SBI blue chip – Rs5000

Mid cap : HDFC Mid Cap Opp Fund – Rs5000

Small Cap : DSPBR Micro Cap Fund (G) – Rs 5000

Can you please suggest any better funds in the above categories. As i am new to the invest methods, could you please let us know at where i need to invest these funds or whom to contact for investing of SIP

Please let me know.

Phani-What is the time horizon? What asset allocation you are following?

Hi Basunivesh,

I am looking for 15 years and 18 years. I am following debt:equity as 20:80

Phani-Go ahead but DSPBR fund is temporarily stopped accepting fresh investment.

hello sir,

I am planning to invest 14000/- in mutual funds by monthly sip. time horizen– 18 to 20 years..I choose following funds in different categories

Large Cap:-

1.. Birla Sun Life Frontline Equity Fund

2. Mirae Asset India Opportunities Fund

Small Cap:-

1. Reliance Small Cap Fund

2. Franklin India Smaller Companies Fund

Mid cap:-

1. Mirae Emerging Blue Chip Fund

2. dsp small & midcap fund

3 HDFC Mid Cap Opp Fund

Kindly comment on these chosen funds.. if possible suggest some more good funds.

Arun-Why not single fund from each category also refer above post and do asset allocation between debt and equity.

Because of market risk and performance of every fund.. I think every fund performs in their own way..it may be possible if one fund is not performing ,choosing two funds in one category may minimize the loss. This is my opinion. I invest 1.5 lakhs every year in PPF also..

Arun-In my view, hold single fund which is best track record, give enough time for fund to judge before jumping or quitting. Doing re-balancing and reviewing once in a year are best. May be I am biased. But I love to simplify the investment from those experts who made it as if ROCKET Science 🙂

Sir, you are right. Investments should be kept as simple as possible. I am new to mutual funds. So don’t have much knowledge about judging the performance of a fund.. can you please tell me how to judge the performance of a fund..

Hi arun, I am also a newbie… i came to know about few ways to choose by my financial freinds spurce.. i.e. see the track record of 1yr and 5yr returns and ranking… and ur intution… but past performance cant ensure future ..but its one of the ways may be to choose… Basu might give better insights… thanks

Prashant

Prashant-I am of the opinion that holding single fund is better as holding multiple funds with same underlying stocks or with the same benchmark may hardly give any diversification. However, if your fund is continuously under performing the BENCHMARK (not it’s peers), then you can think of switching. Whether you invest in 1 fund or many funds, tracking and managing risk is more important.

I use rolling returns for 3yrs to choose the best fund from each category.

Jerry-Do you think 3 years return suffice to judge a fund?

hi. iam 42yrs now and am planning to invest in SIP MF. Goals are retirement/child education 18yrs (for both). I have allocated 30% for debt in form of PPF,NPS and debt funds. Planning to invest remainder in equity.I can spare about Rs 50000 monthly for the same . I am considering to invest in following funds; Large cap-Kotak select focus & BSlife frontline equity: Multi cap- motilal oswal most 35, Midcap–mirae asset emerging blue chip and HDFC opp. Small cap: REliance small cap. What is your opinion about fund selection? I am having some confusion between BSL Fe and SBI blue chip . also Between HDFC midcap opp, reliance small cap, FI small co, DSP BR small and midcap.

Suresh-One large cap is fine and I suggest either Birla or SBI. In mid cap I am inclined towards HDFC. In small cap DSPBR.

Hi–thanks for reply.

I have 2 doubts:

1. just like mutual fund returns are influenced by market performance, what is the effect/impact of the funds on the market performance?

2. considering even the worst crashes of market, how much would actually one loose by investing in mutual funds ?He might not get the expected returns, but will he really loose out all?

Suresh-1) It is exactly like few chasing many or many chasing few. But in the current scenario, I don’t think a single fund can turn the market. It is collective money across all AMCs, which may impact.

2) Anything can happen. Hence, the art of investing is the art of MANAGING RISK but not chasing returns.

You really write well. I have seen lot of blogs on this subject but yours was the most logical and articulate. I also read your Jeevan Umang review which my LIC agent has been asking me to buy and of all reviews on the net, yours was the best.

Harinee-Thanks for your kind words.

Hello Sir,

Nice Informative article with many queries and quick responses! Truly appreciate!

I have LIC policy with yearly premium of 16500/y, PPF of 470000 (because of decreasing interest rates, I add just 1K/y in it now onwards, maturing in 2022)

Started to invest in Mutual Funds from last 2 years only.

MF Lumpsum are as below:

DSP Micro Cap: 30000

DSP Small & Mid cap – 5000

Franklin India Opportunity – 20000

Franklin India Smaller Company – 20000

DSP Small & Mid cap: 2000 SIP from last 3 months

Franklin India Smaller Company – 2500 SIP from last 4 months

Goal: 10 years (Minimum)

Monthly desired investment – 10000

Please suggest me if I am doing right or which funds I should Switch/add new?

Kindly appreciate your help!

Thanks,

Tanvi

Tanvi-What asset allocation you are following? Refer above post properly and do start investing.

Hello Basuji,

Asset allocation is 30:70. For 30% Debt, I have PPF, LIC etc. I am looking forward to buy some equity based Mutual Fund. But confused about which one to select to get maximum wealth creation benefit. Can you please help me in selection?

Thanks in advance…

Tanvi

Tanvi-One large cap, one mid cap and one small cap in the ratio of 50:30:20 is enough.

Hi.. i am little worried/confused.. why do u suggest only 1 fund in each catagory? Many funds have not given verygood/good returns but few have given best consistanly… and future depends on market and mainly the thinking of fund manager…. if we choose one smll cal… arent we taking risk with on find manager?? If he fails to tackle right stocks… growth is not expected… but if we choose atleast 2 good funds in each catagory…doesnt that make better risk diversification??

Prashant-If both funds tracking the same index as their benchmark and if the particular fund is not beating it consistently, then you have to think of switching. However, PEER comparison is the biggest enemy in investing. Also, do remember that whether you choose SINGLE or 10 FUNDS within the same category, no fund will be BEST forever. The art of investing is the art of managing risk. Stop chasing funds returns. But concentrate on fund returns. If the fund is generating your expected return, then why to worry? Also, invest in equity MF does not mean you invest today and forget for next 10 years. You have to review and do rebalancing activity once in a year.

HI Basu,

I m planning to invest my monthly in different sectors i.e mutual funds, PPF and in other investment. Kindly guide me which are good for above 15 years.

Looking for the response.

Rahul-Combination of PPF and equity mutual funds based on above asset allocation.

SIR CAN U PLS LET ME KNOW HOW MUCH % I HAVE TO INVEST IN PPF, SIP , MUTUAL FUND AND OTHER

Rahul-The asset allocation is already explained in above post.

Dear Basu,

I am a 33 year old guy. I am getting Rs. 3 lakh after the maturity of my LIC policy. And I want to re-invest that amount for my family’s future. I don’t know much about mutual funds so please guide me.

My goal is to gain maximum returns.

Time horizon is 15 – 20 years.

Risk level is moderate.

So, please tell me that should I invest this amount in SIP or as Lump sum and in which funds so that I can get maximum returns??

Thank you in advance.