Post Office SCSS, MIS, Term Deposits, PPF, Sukanya Samriddhi, NSC, KVP Interest Rates Oct-Dec 2016 were declared. This interest will be applicable from 1st October 2016 to 31st December 2016.

First, recap the changes done to all Post Office Savings schemes for the year 2016. Earlier the interest rates used to be announced on yearly once. However, now from 2016-17 the rate of interest will be fixed on a quarterly basis. I already wrote a detailed post on this. I am providing the links of those earlier posts below.

- Post Office Savings Schemes -Changes effective from 1st, April 2016

- Premature closure of PPF account – New Rules 2016

Based on these new changes, now onward interest rate will be declared on a quarterly basis. The earlier quarters (FY 2016-17) interest rate can be viewed in my earlier posts “Interest of PPF KVP NSC SCSS and Sukanya Samriddhi for April-June 2016“ and “PPF and Sukanya Samriddhi Scheme interest rate July-Sept 2016“.

Below is the timetable for change in interest rates for all Post Office Savings Schemes.

As per this timetable, Government recently announced PPF, Sukanya Samriddhi, NSC, KVP Interest Rates Oct-Dec 2016 and also for all Post Office Savings Schemes.

The Government this time not changed the interest rates of savings account. However, there is a small change in rest of all products. The Government reduced the interest of all schemes by 10 basis points (100 basis points=1%) for the third quarter of 2016-17 (Oct-Dec 2017).

PPF, Sukanya Samriddhi, NSC, KVP Interest Rates Oct-Dec 2016

Let us see the Post Office SCSS, MIS, Term Deposits, PPF, Sukanya Samriddhi, NSC, KVP Interest Oct-Dec 2016.

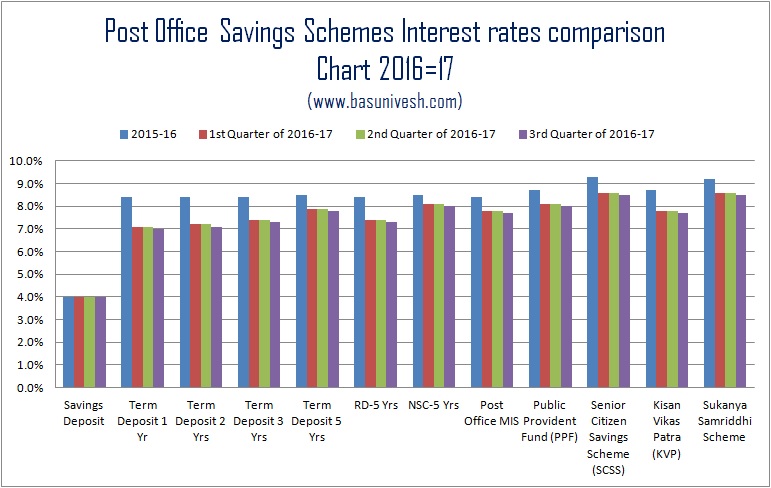

I highlighted the changes in different colour. You notice that except Savings Deposit, interest rates for Post Office SCSS, MIS, Term Deposits, PPF, Sukanya Samriddhi, NSC, KVP Interest Oct-Dec 2016 are changed slightly.

Kisan Vikas Patra (KVP) now doubles in 112 months instead of earlier 110 months. This is due to the reduction of interest rate from the earlier 7.8% to 7.7%.

In Below chart, I will try to show you the interest rate movement from FY 2015-16 up to the third quarter of 2016-17.

You notice the changes of all schemes from FY 2016-17 first quarter. They reduced drastically and now maintained the status quo of the same first quarter for the second quarter. For the third quarter, interest rates reduced slightly.

Hope this much information is enough to understand how the changes done to all Post Office SCSS, MIS, Term Deposits, PPF, Sukanya Samriddhi, NSC, KVP Interest Oct-Dec 2016.

Refer our earlier posts related to post office Savings Schemes-

- All about Public Provident Fund (PPF)

- How to encash or withdraw NSC bought from different Post Office?

- NSC-Accrued Interest taxation and way to reduce it

- Post Office Monthly Income Scheme or MIS – A complete guide

- Premature closure of PPF account – New Rules 2016

- PPF withdrawal rules & options after 15 years maturity

- Public Provident Fund -20 unknown facts

- 15 Rules of availing Loan against PPF (Public Provident Fund)

- How to transfer PPF Account from Post Office or Bank to another Post Office or Bank?

- Excel PPF Calculator-Calculate goal, loan or withdrawal amounts

- PPF-Loan and Withdrawal

- PPF-When to contribute to get higher returns?

- All about Kisan Vikas Patra (KVP)-2014

- Sukanya Samriddhi Account -When to invest to earn more returns?

- Sukanya Samriddhi Account-An investment scheme for your girl child

- Post Office Senior Citizen Scheme (SCSS)-Benefits and Interest Rate

- NSC and KVP in e-mode and Passbook mode from 1st July 2016

- How to transfer NSC from one person to another?

- India Post Help Centre and a Toll-Free Number 1924 features

Hi Sir,

How is taxation applicability on KVP. as i heard 1st 3 years there is no tax on accrual interest.

How to calculate interest on KVP.

Girish-Who said that there is no taxation for first 3 years?

Hi Basu,

I have opened a PPF account in Nov 2016 and have also made in investment in the account.

As per my understanding if the PPF account is opened post 1st April 2016 the account will get active only in 1st April 2017 for the calculation of 15 years periods.

In that case can i invest in 2017 or the investment which i made during the time of opening will be considered for 2017.

Thanks in advance

Aroon-Who said that your account will get active after 1st April, 2017? Refer how the PPF years are counted at “PPF withdrawal rules & options after 15 years maturity“.

Hi Basu – In PPF April 1st – March 31st, financial year is considered to be a deposit year E.g. for an account opened in November 2010 – 2011, Year 1 will be April 1st 2011 – March 31st 2012 is it correct ?

In that case i have already invested 1.5 lacs while starting my PPF account so can i invest again in the 2011 – 2012 or my previous investment will be taken as the First year investment.

Please clarify

Aroon-I am not sure of what is your doubt. But the maximum limit applicable is for each Financial Year. Let us say you opened the account in November 2010. Then you can deposit maximum Rs.1,50,000 from November 2010 to 31st March 2012 (Earlier the limit was not Rs.1,50,000 and it was less. But giving you an example).

Hi Basu – I want to understand when is the first year if i open an account in Nov 2016. Some people say the First financial year after opening the account is considered as the First year of PPF so that i can avoid excess payment during the financial year.

Aroon-Let us say you opened the account in 15th Nov 2016. Then it completes 15 years after 15th Nov 2031. However, it matures on 1st April 2032 (the immediate next financial year after completion of 15th year). Hence, the first year for you is FY 2016-17.

Thanks for the clarification Mr.Basu

Hi Basu,

My Mom opened a ppf account when the rate of interest was 8.7 % and now it has been revised to 8%, so will this 8% will be effect from the time of opening the account or it will be effect only from Nov 2016.

Thanks

Aroon-It will affect from Nov 2016.

hi,

I have one question. if i invest in NSC, after maturity do i need to pay tax on interest earned?

is it totally tax free or there is any kind of tax?

also, can you please suggest post office schemes which are tax free? thank you.

Rajendra-Interest earned from NSC is fully taxable as per your tax slab.

Hi Basavaraj,

A valuable follow-up on the change in interest rates on these investment products.

Given that these products are attracting lower interest rates (and possibly may go south further in future), what is your view on considering such instruments (e.g. PPF) as a debt portion, while building your portfolio? Is it still worth considering? Or one should look out for better alternatives like debt funds, instead?

Mahesh-Considering the EEE feature of PPF, I still suggest PPF as best debt if time horizon matches the maturity of PPF.

Hi Basavaraj,

Thank you for the reply. Sorry, but EEE stands for?

Agreed, but would it be fine to stick to PPF alone as your debt portion, or one should consider debt funds also for more balanced approach?

Mahesh-EEE-Tax Benefits while investing, no tax on interest earned yearly-maturity is fully tax-free. You look at debt fund to reduce the volatility in your portfolio and also during market fall in equity the debt will act as cushion. But it does not mean that all debt funds are safe and less volatile. Take the example of long term gilt, dynamic funds or income funds. Volatility in debt funds not known to many.

Thanks for explaining EEE.

I think you are right. Many people do not recognize the fact that debt funds too are prone to market volatility, albeit not to the extent of equity-oriented ones.

Thanks for the info.

Mahesh-Pleasure.

Hi Basu,

I heard about Co-operative bank like Indian railways etc. ,It is safe to deposits under this bank as the interest rates are higher like 9% to 9.25% in Indian railways for senior citizen & for general citizen its around 8.5%. Although there are not so much user friendly as other bank. Please provide your valuable input on this.

Thanks,

Shalabh

Shalabh-Higher returns always associated higher risk. I am not sure about their financials and hence I can’t comment to what extent they are reliable.

I have a doubt regarding interest rates and its revision,…If i had opened a ppf ac two years back,will i get that interest contracted till end or i get the reduced interest on revision?

Anesh-Interest will change on quarterly basis. Hence, you will not get the old PPF interest rate. But for current year it is based on current year interest rate. You are not locking your interest rate like Bank FDs.

Dear Basu ji

Thanks for your wonderful educational articles.

I am 31 years old, married with a son (new born) with an annual income of 4.2L pa

I have taken the following insurance plans : –

Jeevan Saral plan – premium paid is 25K per annum (coverage of 10L)

Term plan from ICICI Pru – (coverage 60L)

Health insurance (Family floater) for myself & wife – coverage of 3L

Apart from these I have a mediclaim coverage from my employers for Rs. 1 L.

Would you suggest me to go for any health insurance or personal accidental insurance?

Thanks

Abhi

Dear Abhi,

I’m regular reader of Basu articles/similar blogs and developed my knowledge. I would like to share my idea for your portfolio.

1. Increase your exposure to Mutual Funds. Invest 30% of money in Mutual funds.

2. Open PPF account and allocate 30%

3. Open NPS account and allocate 20% of your investment. It will be helpful once you draw more salary.

4. Allocate 20% amount on Term insurance and medical premium insurance.

Thanks

Abhi-Try to increase your personal health insurance coverage to another 1-2 lakh. Yes, you must buy personal accidental insurance also.

Hi Basu,

Thanks for sharing wonderful articles.

My brother sold my fathers house after my father died. I received my share of 30 lakhs INR in my account through this property sale. The property was in Bangalore.

Do I need to pay tax for this amount? If Yes how it will be calculated please?

Please provide your comments.

Prabhakar-There is no tax on inheritance property. However, whatever earning or sales from this property in future will be taxed under your income.

Understand that NSS has been discontinued. Was told to withdraw the balance in the account. Since 20% tax is deductible and also toold that there is limit on annual withdrawal how to go about it. When Pass Book was updated noticed that it earns interest still. Someone told me that the nominee/successor is not required to pay IT when withdrawing the balance. Thanks for your advice in advance

TRC

Chandrasekaran-Who told NSC was discontinued? Who told there is a limit of withdrawal? I am not getting of what you are saying. Can you elaborate whether you are saying about NSC or something else?

Not a good news for senior citizens and for rural people who pour in major portion of their investment in these products. The bad thing is interest rates are expected to fall further in the years to come and they have to brace for the same.

Even though, Government data shows inflation is falling, ground reality is different where one witnesses increase in prices of basic goods and services.

Ritesh-I understand your concerns.

Plz sugest me details of nsc

Chandra-I will write on it soon. But if you need information immediately, then you can visit the India Post portal.

Namaste,

Nice Information About Postal Investment.

Thanks for the same.

Anand-Pleasure 🙂