Many of us investing in NPS (National Pension Scheme). But have you ever checked NPS Returns for 2018? Whether you analyzed who is the best NPS Fund Manager for 2018 or which is the best NPS Scheme for 2018?

NPS now slowly turning to be one of the major investment choices for many of us. It may be due to default option provided to Government employees, tax benefits at the time of investment or to create a retirement corpus.

What is Scheme Preference in NPS Account

In NPS, there are two types of options available to create your portfolio. They are as below. Remember this scheme preference is not available for Government Employees Tier 1 Account Type. However, they have a freedom to choose scheme preference in their Tier 2 account. For rest of all investors, you have an option to choose scheme preference.

# Active choice – You will decide on the asset classes in which the contributed funds are to be invested and their percentages (Asset class E-Maximum of 50%, Asset Class C, and Asset Class G ).

# Auto choice – Lifecycle Fund– This is the default option under NPS and wherein the management of investment of funds is done automatically based on the age profile of the subscriber. At the age of 18 years, the auto choice will invest 50% of pension wealth in E Class, 30% in C Class and 20% in G-Class. These ratios of investment will remain fixed for all contributions until the participant reaches the age of 36 yrs. From age 36 yrs onwards, the weight in E and C asset class will decrease annually and the weight in G class will increase annually till it reaches 10% in E, 10% in C and 80% in G class at age 55 yrs.

At the age of 18 years, the auto choice will invest 50% of pension wealth in E Class, 30% in C Class and 20% in G-Class. These ratios of investment will remain fixed for all contributions until the participant reaches the age of 36 yrs. From age 36 yrs onwards, the weight in E and C asset class will decrease annually and the weight in G class will increase annually till it reaches 10% in E, 10% in C and 80% in G class at age 55 yrs.

Such changes will be done on the birth date of the subscriber. Such changes can be done once in a financial year.

What are the types of funds available in NPS?

There are three types of NPS funds available. They are as below.

- Asset Class E : Invest in equity market instruments. This is the riskier asset class among all three.

- Asset Class G : Invest in fixed income instruments. The best example of this is central government bond. This is the secured among all three.

- Asset Class C : Invest in fixed income instruments. Examples of these are bonds issued by firms or companies. this neither risky like Asset Class E nor safe like Asset Class G.

Recently a new fund category by name Alternate investment has been introduced.

List of NPS Fund Managers

Currently, there are 8 Fund Managers who are managing our NPS corpus and they are as below.

- Birla Sun Life Pension Scheme

- HDFC Pension Fund

- ICICI Prudential Pension Fund

- Kotak Pension Fund

- LIC Pension Fund

- Reliance Capital Pension Fund

- SBI Pension Fund

- UTI Retirement Solutions

The Government employees NPS accounts and contributions are managed by LIC Pension Fund, SBI Pension Fund and UTI.

Under this category, up to 15% of the corpus can only be invested in Equity Fund. The remaining corpus is allocated to Corporate Bonds and Govt securities.

The private sector employees and other individuals can also invest in NPS. The Equity fund threshold limit is 75% in this case. These individuals can select any of the two investment options to select scheme preferences.

NPS Returns for 2018 – Who is best NPS Fund Manager?

Now let us concentrate on NPS Returns for 2018 and try to find who is the best NPS Fund Manager for 2018 or which is the best NPS fund for 2018.

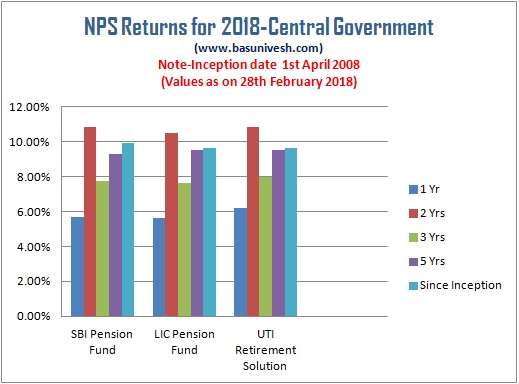

NPS Returns for 2018- Best NPS Fund under Central Government Scheme

As I said above, this scheme is meant for Central Government Employees only. Here, we can find only three fund managers and the returns are as below.

# Fund Managers managing the scheme since 1st April 2008.

# SBI Manages the highest AUM (29254.83 Cr) followed by UTI (27490.44 Cr) and LIC (25532.34 Cr).

# When you compare 10 years returns, SBI tops with almost 10% returns (9.94%) and then LIC and UTI almost generated around 9.6% returns.

#All Fund Managers debt portfolio hold Govt Bonds which maturing from 2030 to around 2045. Hence, any interest rate fluctuation will impact the return badly. Because of longer the maturity period higher the interest rate impact on bond.

# Top 3 holdings of SBI Fund Manager is G-Sec, Banking and Financial Institutions. LIC Fund Manager holding is Govt. Sec, Finance, Banks. However, with UTI, it is Banks, Other credit granting, Housing credit Institutions.

# Benchmark return for 5 years is 9.03%, 3 years is 7.3%, 2 years is 9.48% and for 1 year it is 4.53%. Hence, all three fund managers have beaten the benchmark consistently since 5 years.

NPS Returns for 2018- Best NPS Fund under State Government Scheme

Now let us go with NPS Returns for 2018 under State Government Scheme. Here also you will find 3 fund managers like central government NPS. Let us see the performance.

# Fund Managers managing the scheme since 25th June 2009.

# SBI Manages the highest AUM (37751.06 Cr) followed by UTI (36790.49 Cr) and LIC (36476.09 Cr).

# When you compare 9 years returns, LIC tops with 9.66% returns and then UTI (9.6%) and SBI (9.49%).

#All Fund Managers debt portfolio hold Govt Bonds which maturing from 2030 (UTI holding bond maturing in the year of 2029) to around 2045. Hence, any interest rate fluctuation will impact the return badly. Because of longer the maturity period higher the interest rate impact on bond.

# Top 3 holdings of SBI Fund Manager is G-Sec, Banking, and Financial Institutions. LIC Fund Manager holding is Govt. Sec, Finance, and Banks. However, with UTI, it is Banks, Other credit granting, Housing credit Institutions.

# Benchmark return for 5 years is 9.03%, 3 years is 7.3%, 2 years is 9.48% and for 1 year it is 4.53%. Hence, all three fund managers have beaten the benchmark consistently since 5 years.

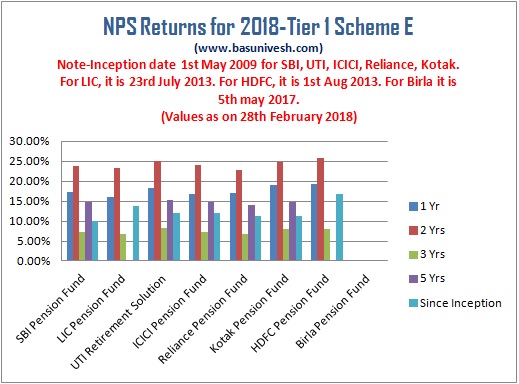

NPS Returns for 2018 – Best Performing NPS Tier 1 – Scheme E Fund Returns

Now let us concentrate on NPS Returns for 2018 in Tier 1 Scheme E. The returns are as below.

# The best performing NPS Pension Fund manager under NPS Tier-1 Scheme E is UTI Retirement Solutions. This scheme has generated returns of around 15.15% in the last 5 years. Also, since inception, it is 12.11%.

# The benchmark used for Equity plans is Nifty 50 Index.

# Also, weightage of top 5 holdings is less in case of UTI. It constitutes 24.81% of the overall portfolio. Kotak Fund holding even the Mutual Funds also like Birla Sunlife Top 100, Birla Sunlife Frontline Equity and SBI Magnum Multiplier. Seems strange to me as how they managing the expenses. Because there will be double expenses like Kotak expenses and also the Mutual Fund Expenses.

# The clear winner in this category is UTI followed by SBI.

NPS Returns for 2018 – Best Performing NPS Tier 1 – Scheme C (Corporate) Fund Returns

Now let us concentrate on NPS Returns for 2018 in Tier 1 Scheme C. The returns are as below.

# The best performing NPS Pension Fund manager under NPS Tier-1 Scheme C is ICICI. This scheme has generated returns of around 9.79% in the last 5 years. Also, since inception, it is 10.52%.

# SBI’s AUM is highest here with around 1006.99 Cr followed by HDFC (572.52 Cr) and ICICI (540.47 Cr).

# The clear winner in this category is ICICI followed by SBI.

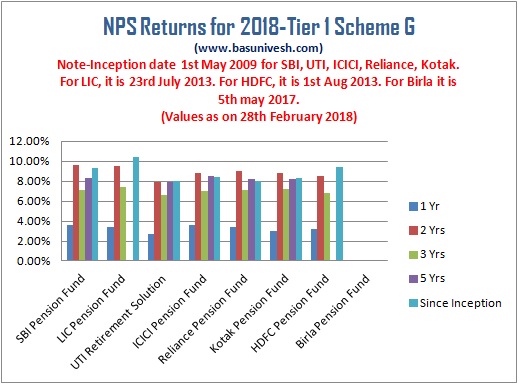

NPS Returns for 2018 – Best Performing NPS Tier 1 – Scheme G (Govt Securities) Fund Returns

Now let us look for NPS Returns for 2018 in NPS Tier 1 and Scheme G (Govt Securities).

# In this category, the higher and consistent performer is SBI Pension Fund.

# Have you noticed the less returns of all these funds since a year? The reason for underperformance by all these funds is that RBI paused the interest rate since few months due to higher inflation, higher crude price and for some other reasons. Due to this, the fund performance decreased drastically. Because these funds holding longer maturity Government bonds which are prone to interest rate movement.

NPS Returns for 2018 – Best Performing NPS Tier 2 – Scheme E Fund Returns

Let us now move to Tier 2 performance of NPS Returns 2018.

# The best performing NPS Pension Fund manager under NPS Tier-1 Scheme E is UTI Retirement Solutions. This scheme has generated returns of around 15.09% in the last 5 years. Also, since inception, it is 10.24%.

# The benchmark used for Equity plans is Nifty 50 Index.

# Also, weightage of top 5 holdings is less in case of UTI. It constitutes 27.47% of the overall portfolio. Kotak Fund holding even the Mutual Funds also like Birla Sunlife Top 100, Birla Sunlife Frontline Equity, ICICI Focused Equity and SBI Bluechip Fund. Seems strange to me as how they managing the expenses. Because there will be double expenses like Kotak expenses and also the Mutual Fund Expenses.

# The clear winner in this category is UTI followed by SBI.

NPS Returns for 2018 – Best Performing NPS Tier 2 – Scheme C (Corporate) Fund Returns

Now let us concentrate on NPS Returns for 2018 in Tier 2 Scheme C. The returns are as below.

# In this Scheme the winner is ICICI pension fund with 5 years return 9.69% and followed by Reliance Pension Fund.

# The highest AUM is managed by SBI Pension Fund and followed by ICICI Pension Fund.

NPS Returns for 2018 – Best Performing NPS Tier 2 – Scheme G (Govt Securities) Fund Returns

Let us not check the NPS Returns for 2018 for Tier 2-Scheme G (Government Securities).

# In this category the winner is SBI Pension Fund.

# Have you noticed the less returns of all these funds since a year? The reason for underperformance by all these funds is that RBI paused the interest rate since few months due to higher inflation, higher crude price and for some other reasons. Due to this, the fund performance decreased drastically. Because these funds holding longer maturity Government bonds which are prone to interest rate movement.

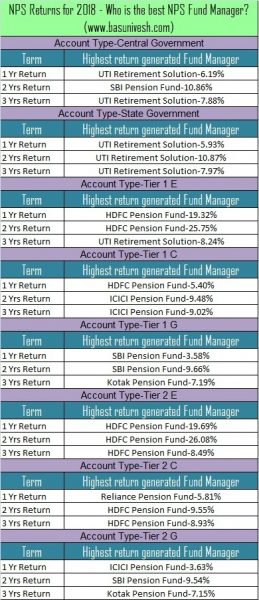

Who is the best NPS Fund Manager for 2018?

In above charts we the NPS Returns for 2018. Now based on those performance returns, who is the best NPS Fund Manager? To identify the best NPS fund manager, I considered last 3 years returns of each scheme. I purposely avoided 5 years returns as two funds not yet completed 5 years.

In below chart, I show you the highest return generated fund manager for each asset class for a different time period of 1 year, 2 years and 3 years. The data looks like below.

Hope this much information is enough for you to judge how your NPS is performing. Do remember that NPS comes with lock-in, annuity you buy will be taxable and you have to stick to limited fund managers. Never invest in NPS with the sole intention of tax saving.

Refer our other posts related to NPS:-

- NPS Tax Benefits – Sec. 80CCD(1), 80CCD(2) and 80CCD(1B)

- NPS Tier 2 – Alternative to Savings Account, FDs or Debt Mutual Funds?

- eNPS – How open and invest in NPS account online?

- Difference between Tier 1 and Tier 2 Account in NPS

Sir

when we reached the age of 60, 40% of the accumulated corpus utilized for the purchase of the annuity is tax-exempt. Of the remaining 60% corpus withdrawn by the NPS subscriber at the time of retirement, 40% is tax-exempt and 20% is taxable.

1} Am I correct with the above points applicable to NRI too?

2} Now I heard that,the tax exemption is extended to the entire 60% (w.e.f April 2019).

Can u please clarify these?

BASWARAJ, I AM IN 30% INCOME TAX SLAB. I WISH TO OPEN NPS TIER 2. PLEASE TELL ME WHICH (ECG) IS BETTER FOR ME AS I WILL NOT MONITOR AND WISH TO INVEST FOR TAX SAVING AS WELL AS SOME INVESTMENT FOR OLD AGE, NOW I AM OF 43 YEARS. THANKS.

Dear Praveen,

If you are not Government Employee, then how your NPS Tier 2 account will gives you tax benefit?

But dear Basa, though NPS has all those disadvantages, is it a good idea to just put 50k in it every year to get that extra tax benefit over 80c?

Dear San,

Look which side is more ADVANTAGES or DISADVANTAGES? Based on that take a call.

Dear Basavraj,

The above article is indeed very useful, gives a lot of insight into the details of NPS.

With the recent changes in the taxation rules (i.e. 60% corpus being offered tax free) would you still suggest not to invest in NPS and rather build the corpus independently using Debt/Equity ?

FYI…i am 36 years as of now and fall under 30% tax slab.

Kindly share your opinion.

Dear Sumeet,

Even after recent changes, I strongly suggest you to stay away from NPS.

Hi Basav,

Restructuring life at 40 and starting to build corpus. Considering NPS for long term wealth & retirement pension. With 20yrs of horizon, should I invest 10% in NPS(@ECG : 30:40:30) and consider other options in market?

Dear Anisha,

Refer my latest post before you jump into “National Pension Scheme (NPS) – 5 Biggest Disadvantages“.

Hi,

Which is best for Retirement???(25 yrs-Horizon)

NPS or Equity MF

Dear Paras,

Your BEST depends on many things. Hence, hard to say that THIS IS BEST FOR RETIREMENT. But I am against NPS as a retirement product.

Hi Sir,

So as per you which is the best retirement product.

Dear Giridhar,

Accumulate on your own using equity and debt products in right proportion.

Hello Baasvaraj,

I have been researching on NPS for quite some time. For most of the forums are giving me a divided opinion on NPS since

1. It has a long lock-in period

2. Ultra frigid investment

3. Does not produce remarkable returns on the invested corpus.

I need your valuable opinion – should I invest in NPS for my OLD age living or any other better instrument available in markets( other than MF or direct Stocks)?

Requesting your help.

Regards,

Somenath Ghosh

Dear Somenath,

Yes, the points are valid and the current tax structure of NPS for retirees is horrible. Hence, better to stay away. Returns it may or may not produce. But liquidity, freedom and tax issues are the major concerns.

Thank You Basavaraj.

I have E=50%, C=5%, G=40, A=5% with UTI. HDFC is good in E and C.

is if ok to switch to HDFC and change in % like E=50%,C=40%,G=5%,A=5%

Dear Arul,

It is hard for me to guide asset allocation without knowing much about your financial life.