Whether we can use NPS Tier 2 account as an alternative to savings account, FDs or debt mutual funds? This is the question recently asked by a blog reader. His reasons are very much valid. Let us see whether it is suitable or not.

The reason for his question is valid. Hence, thought to discuss more on this in a separate post.

What is NPS Tier 2 Account?

NPS is the retirement product also called as Defined Contributory product. There is no defined benefit. You contribute to this product (in the case of Govt. employees, your employer too). Your retirement corpus depends on the amount you contribute and the income generated from this contribution.

Such accumulated retirement corpus can be withdrawn once you retire and can be utilized to buy an annuity (pension product). You are allowed to withdraw part of it before you can buy an annuity. We can explain the same as below.

This is regulated by Government body called as Pension Fund Regulatory Development Authority (PFRDA). PFRDA appointed fund managers, who manage your fund. There are various options of investment to choose based on your risk appetite.

An individual with the age limit of minimum 18 years and maximum 60 years of age can join NPS. Now, NRIs are also allowed to open NPS account.

Once you open NPS account, then you will be allowed a PRAN (Permanent Retirement Account Number), a 12 digit unique number. A minimum of Rs.6,000 can be invested and there is no maximum limit. But minimum single contribution is Rs.500 for Tier 1 and for Tier 2 it is Rs.1,000.

As of now, there are 7 fund managers, who managing the overall NPS amount. They are as below.

- HDFC Pension Management Company

- LIC Pension Fund

- ICICI Prudential Pension Fund

- Kotak Mahindra Pension Fund

- Reliance Pension Fund

- SBI Pension Fund

- UTI Retirement Solutions

The subscriber has been given the flexibility to choose any one out of the available Fund Managers and also the percentage in which the selected PFM will invest the funds.

The three asset classes are

- E = Equity

- C = Corporate bonds (invest in investments in fixed income instruments other than Government securities.)

- G = Government Securities (investments in Government securities)

As of now, there are 7 insurance companies, who provides you pension products for NPS. They are as below.

- Life Insurance Corporation of India (LIC)

- SBI Life Insurance

- ICICI Prudential Life Insurance

- Bajaj Allianz Life Insurance

- Star-Daichi Life Insurance

- Reliance Life Insurance

- HDFC Standard Life Insurance

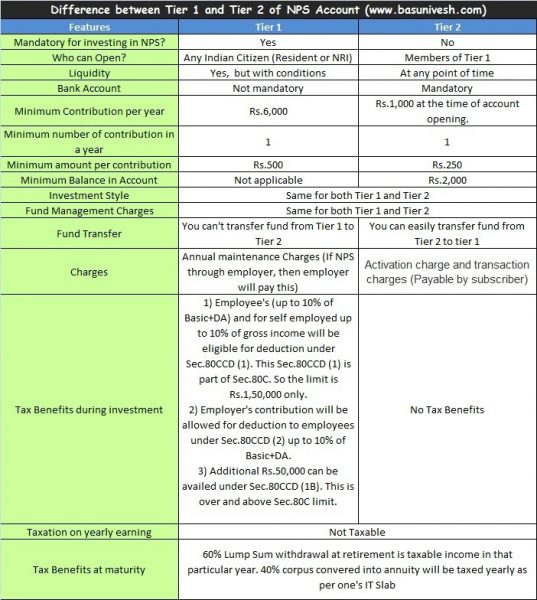

There are two types of accounts in NPS. One is Tier 1 and the second one is Tier 2. I tried to explain the both the account features in below image.

Note-

-As per recent PFRDA circular dated 8th August, 2016, the minimum contribution in Tier 1 Account is now reduced to Rs.1,000 a year. There will be no minimum investment limit for Tier 2 account (Earlier, it was Rs.250). Also you no need to maintain the minimum balance in Tier 2 account (Earlier, it was Rs.2,ooo).

-From Budget 2016, the 40% withdrawal at the time of your retirement from NPS will be tax-free. Rest 60% of the corpus will be treated taxable income as per old rules. Hope this above table cleared your doubts.

Additional features of NPS Tier 2 account

- No additional CRA (Central Record Keeping) charges will be levied for account opening and annual maintenance in respect of Tier II.

- However, CRA will charge separately for each transaction in Tier II, the charges being identical to the transaction charge structure in Tier I.

- There will be a facility for separate nomination and scheme preference in Tier II.

- The subscriber would have the same choice of PFMs and schemes as in the case of Tier I account in the unorganized sector.

- Contributions can be made through any POP/POP-SP.

- Bank details will be mandatory for opening a Tier II account.

- No separate KYC for opening Tier II account will be required; the only requirement is a pre-existing Tier I account.

Hope you now got a clarity on what is NPS Tier 2 account.

Let us consider whether NPS Tier 2 can be considered as an alternative for Savings Account, Bank FDs or Debt Mutual Funds.

# Liquidity of NPS Tier 2-

You can withdraw the money from NPS Tier 2 account as and when you need. Hence, liquidity is not an issue. Therefore, we may say as its liquid product like Bank FDs or Debt Mutual Funds. However, we may not say as liquid as your savings account. Because redemption may take some time in NPS Tier 2 (not sure of how many days it takes).

# Returns of NPS Tier 2

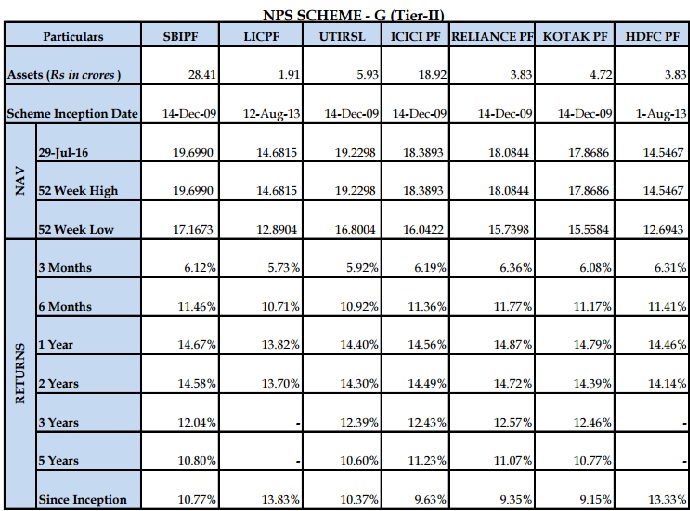

As this post is meant to find out the answer of whether NPS Tier 2 can be an alternative solution to the savings account, Bank FDs or Debt Funds, I will concentrate on Asset Class C (investments in fixed income instruments other than Government securities) and G (investments in Government securities). Below is the returns from these asset classes of NPS Tier 2.

First look at the returns of Asset class C (investments in fixed income instruments other than Government securities).

You notice that the returns are much higher than what you get from a typical savings account, Bank FDs, and Debt Funds. Returns are as on 29th July, 2016.

Similarly, let us look at the returns of Asset Class G (investments in Government securities).

Here also you notice that returns are best when you compare to Savings Account, Bank FDs or Debt Mutual Funds. Returns are as on 29th July, 2016.

# Volatility of NPS Tier 2 Returns

This is the major point which many of us forget to consider. NPS is a product meant for long term goal called retirement. However, with fancy returns and liquidity as an alternative plus point, we are comparing NPS Tier 2 with Savings Account, Bank FDs or Debt Mutual Funds (Debt Mutual Funds means my assumption is only for Liquid Funds, Ultra Short Term Funds, and Short Term Funds).

NPS Asset Class C and Asset Class G holding long term maturity bonds and papers. Therefore, the interest risk is always there. Check the maturity date of the underlying bonds of Asset Class C and Asset Class G.

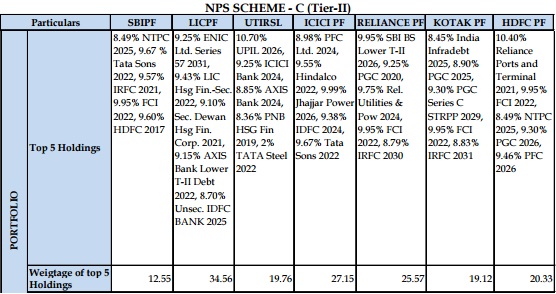

First, let us check the underlying bonds of Asset Class C.

Here, I concentrated only on Top 5 holdings. You notice that maturity periods of corporate bonds are of long-term in nature.

Now, let us understand the holdings of Asset Class G.

Notice the maturity periods of G-Sec bonds and the weightage in the holding.

In the bond market, higher the maturity period greater would be the interest rate risk. Hence, never try to compare the interest rate risk of savings account, Bank FDs or Debt Mutual Funds ((Debt Mutual Funds means my assumption is only for Liquid Funds, Ultra Short Term Funds, and Short Term Funds) with NPS Tier 2.

# Taxation of NPS Tier 2-

For your surprise, there is no clarity on NPS Tier 2 withdrawal taxation. We all know that if you invest in NPS Tier 2, then you will not enjoy any tax benefits. However, there is no clarity on withdrawal taxation. Because withdrawal rules under Sec.10 give you correct indications that tax benefits during withdrawals are only for NPS Tier 1.

“(12A) any payment from the National Pension System Trust to an employee on closure of his account or on his opting out of the pension scheme referred to in section 80CCD, to the extent it does not exceed forty per cent of the total amount payable to him at the time of such closure or his opting out of the scheme”.

Few argue that it will be taxed like debt and equity mutual funds. It means, if your holding period is less than 3 years then it will be taxed as per your tax slab. If your holding period is more than 3 years, then at 20% with indexation benefit. However, there is no clarity either from PFRDA or CBDT.

In such a situation, it is hard to believe the taxation part and blindly invest by comparing with Savings Account, Bank FDs or Debt Mutual Funds.

As of now, it is the purely subjective matter which different people have different views.

# Expenses NPS of Tier 2-

NPS is considered as one of the lowest charging product. But it does not mean that it is free. If you invest through POPs, then you have to bear the cost of 0.25% of the contribution (Min. Rs 20 Max. Rs 25000). However, if you invest through eNPS (which is online direct mode), the charges are 0.05% of the transaction, subject to the minimum of Rs.5 and maximum of Rs.5,000 per transaction.

Considering all these costs of the transaction, it is not worth for investing in a small amount. If your investable amount is high, then it may be worth to consider.

Wher we consider NPS Tier 2 as an alternative to Savings Account, Bank FDs or Debt Mutual Funds?

In my view NO. Considering liquidity and the returns, if one decided to invest in NPS Tier 2 account, then it is considered as a blind investment. Conclusions are as below.

- NPS Tier 2 may be the liquid product but not as liquid as your savings bank account or liquid funds.

- Returns may be eye-catching. But you can’t deny risks.

- NPS is meant for the long-term financial goal of retirement. Hence, NPS holds long-term maturity debt papers in Asset C and Asset G. Hence, the risk of interest rate volatility is high. Therefore, it is not worth to consider as an alternative for Savings Account, Liquid Funds, Ultra Short Term Debt Fund, Short Term Debt Fund or short term FDs.

- There is ambiguity regarding taxation of NPS Tier 2 withdrawal. Hence, the sword of confusion always be on your head.

- You need to consider the transaction cost also before jumping into NPS Tier 2 to park your emergency fund or any short term goal fund.

hi, how much would be the tax on withdrawals from Tier II account? Is the entire amount taxed or only the profit?

Dear Rahul,

Regarding the taxation of Tier 2 withdrawal is not yet clear. It is always only the profit is taxable in all assets but not the principal.

Dear Sir

Very useful information. One doubt, as per the Table you Tier I funds cannot be transferred this means those will be locked in Tier I & for Tier II we need to transfer funds in fresh

Dear Amit,

Transfer means from Tier 1 to Tier 2 is not possible. You can invest in both Tier 1 or Tier 2.

What would you say about this

How are withdrawals from NPS Tier II account taxed?

1.

Gains on the Tier II account are taxed when any withdrawals are made from it. The gain is added to your income and taxed according to your tax slab. Indexation is not applicable

By Valueresearch

https://www.valueresearchonline.com/story/h2_storyview.asp?str=32056

2.

withdrawals within a year of investment attract short-term capital tax while those after a year of depositing earn long-term capital tax. For debt funds it is 10% while for equity funds the tax applicable is nil.

By bankbazaar.com

All about Tier 2 National Pension Scheme Account

https://www.bankbazaar.com/saving-schemes/all-about-tier-2-national-pension-scheme-account.html

Raghavendra-There is no clarity either from PFRDA or CBDT. Hence, I can’t authenticate the claims.

Hi guys, Just an update for those who opened their NPS accounts via PoPs, typically banks. You had to either shell out 0.25% of contribution amount each time if you invest via PoP or 0.05% if you use eNPS. So banks are freeloading on the subscriber, as this was before eNPS.

Now you have an option to shift to eNPS by selecting ‘”Shift to eNPS” under “Transaction” menu. Click and after an OTP confirmation, you are free from your POP forever. If you use netbanking you just pay 0.60 paise + GST per contribution. Pretty cool.

Ram-Thanks for sharing this update.

Sir I m already contributing t-1.if i m going to t-2,,government will pay like t-1???if not why i should invest in that….. Why not in mutual fund…. And post off rd…. Or diversified. It is mere a simple investment… Nothing else… Sir is it any additional benefit…

Sudhanshu-I am against NPS.

Why you are against NPS?

Deo-Liquidity, taxation during retirement and sticking to the selected few fund managers ONLY.

True. But any retirement instrument which turns into annuity have all these features. How would you compare it against any other retirement instrument ?

Deo-I am against the RETIREMENT PRODUCT itself 🙂 Why can’t invest on our own in equity and debt funds and create corpus on our own? In that case withdrawal from equity is tax-free and debt part may be taxed but still tax efficient.

Please relook the whole issue on these aspects:

NPS as alternative to a FD/MF with only liquidity and returns as point of interest.

Here let us keep the taxation part apart, assuming that the individual has already taken care of 80 C by some other means.(else bank FD wont come into picture).

IF i want to build up a fund for a 3yr short term goa(like an RD)l/park my funds for short term (like in MF/FD) then why not tier 2 ?.

Here , since i am almost clear as to when and how i am depositing the money and also when i want the money back, i think procedural delays are taken care of.

Satish-But within Tier 2, which asset class you choose? Equity or Debt? If debt, then do you feel it is safer than FD or RD? Do you think Debt funds not volatile in nature (especially if the underlying bonds are of long-term maturity)?

Hi Basu,

Informative article. Thanks so much for your blog.

A suggestion – Would it be possible to provide a printable format button on your blog ? This will help us to print the articles in a doc-friendly way. Currently, all the ads appear when we take a printout .

Prashanth-Thanks for your advice. I will make sure this option available. Thanks once again.

As amazing and helpful as always.

Sandip-Pleasure.

Hi, very informative article.

I am 28 years old and I am searching for good investment options. I just came to know about peer to peer lending as an emerging platform in India and wanted your views on that.

Rajat-I am not an expert on that. Sorry.

Hiii basu sir,

I m ajai age 27 govt employee earnings approx 42k..I want short term gain where I should invest? Will opting tier 2 suit my profile?

Actually I don’t have any idea abt investment so plz suggest me.

Thanks

Ajai-If you don’t have any idea, then try to first learn it. Blind investment is the most DANGEROUS investment.

I am group four railway employee and my age is 35. I want make investment.but I am confused which plan to choose means in ppf,EPF,pli,sip or in fd . please suggest me and guide me.

Anil-Without knowing your financial life and goals, it is hard for me to guide you.

Thanks for the great article. I never considered the fact that the portfolio has long term holdings.Better to stick to short term debt mutual funds as an alternative to bank fixed deposit.Can you suggest any? How do you see dynamic bond funds?

Sreekumar-In my view, if your concern is debt mutual funds investment, then don’t go beyond short-term debt fund. It is misconception that debt funds are SAFE. Dynamic bonds are such funds which comes with volatility and other risks.

Dear sir I have pran no . And nps monthly 1000 rs debited my ac. Regularly.but. I can’t detail check online. It show invalid pran. At online registration or login.

Harshad-Contact PFRDA immediately.

DearBasu,

I have a doubt regarding employer contribution and its deduction….When an employer contributes to his employees a 10% of his basic +DA ,it is directly invested in NPS using PRAN and hence it is not shown as an income in tax calculation ..so how can i claim this deduction for contributon from the employer?

Kindly clarify sir

Anesh-You can show it by calculating the employer contribution in total for that FY. You will not show the proof to IT Dept right? But you must have proof of your claims (which in your case salary slips or even a letter from employer is enough) when AO ask for the same.

Sir,

Is the amount invested in Pension funds directly by the employer to be shown as current fiscal years income??

Kindly clarify

Anesh-It is not your income.

Dear sir,

I read that uder sec 80ccd ,we can avail deduction for employers contribution in NPS ac….Is it over and above 1.50 lakh limit of 80 c or within the limit of 1.50 lakh for all ppf,lic ,elss and so on ????kindly guide

Anesh-Sec.80CCD (1B) of additional investment Rs.50,000 is only above the overall limit of Sec.80C.

yes it is over and above 1.5 lac

so ttoal tax benefit is 1.5 + ).5 = 2.0 lac

Hi Basavaraj

I had asked about NPS Tier 2 vs RD investment

Thanks for the details explination given below

Deepak-Yes, I know. But final conclusion is same for RD too 🙂

Thanks

Article needs to be updated.

1. NPS Tier-1 minimum contribution is now Rs. 1000/-

2. No more minimum contribution for NPS Tier-2.

http://www.pfrda.org.in/WriteReadData/Links/CIRCULARskj12361107d67-baf8-4640-90fa-6d9f1875a0f3.pdf

Sreekanth-Thanks for the updates. I searched this circular, but not found. Finally, you shared it. Thanks once again 🙂