Today LIC launched two new money back plans. One is New Moneyback Plan of 20 Yrs (No.820) and another is New Moneyback Plan of 25 Yrs (No.821). These two are the new versions of old plans Moneyback Plan 20 Yrs (No. 75) and Moneyback Plan 25 Yrs (No.93). Below are the features of the same.

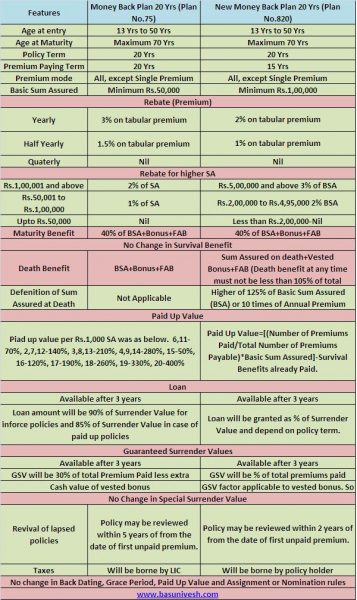

1) New Money Back Plan 20 Yrs (No.820)

2) New Money Back Plan 20 Yrs (No.821)

What are the changes?

- Death Benefit

- Paid Up Value

- Premium Paying Term

- Minimum Basic Sum Assured

- Rebate on premium paying mode

- Rebate on higher Sum Assured

- Loan availability

- Guaranteed Surrender Value definition

- Revival concession on lapsed policies

- Taxes

But the major changes all looking at will be, whether these are costlier to older plans or what? The answer is, as of now we are unable to judge. We will come to know within a few days about this.

DEAR SIR,

PLS HELP ME TO GET BEETER MONEY BACK PLANS FOR 20 YEARS ,

AS MY NEED TO GET MONEY IN INTERWALS…IN FUTURE,

PLS ADVICE.

THANKS

PRASHANT

Prashant-Are you satisfied with the return of around 5% to 6%?

Hi Sir,

I have got 2 LIC plans-

1. Jeevan Saral – 1000/- per month from 2011 for a term of 25 yrs and

2. Money Back – 1000/- per month from 2012 for a term of 20 yrs

Have already enrolled for a Term plan of 75 lacs to cover the insurance part and I’m planning to exit from the above 2 LIC plans.

Considering the fact that it would not give returns more than 6-8%, can you please advise me inorder to surrender Jeevan Saral Should I wait for 5 yrs i.e. till 2016 and what is the best time to surrender money back plan, after 3yrs or 5yrs ?

Lastly, once the policy is surrendered where can I invest this amount ? I’m thinking of 1000/- pm in PPF and 1000/-pm in mutual funds via SIP.

Can you please advise me on this one

Vimal-Jeevan Saral after 5 years and Money Back after 3 years. Again you are doing the same mistake of what you committed earlier. Why to run behind products? First understand your need and goals. Based on goals try to select the product. Product selection must be at end but not at beginning of investment.

Thanks for your quick response.

If I understood this correctly, I can submit Jeeval Saral after 5 yrs and Money back Policy after 3 yrs. By any chance would you be able to help me how much can I expect on surrendering these policies after 5 and 3 yrs respectively.

You are correct in saying that, first I need to have clear goals. So I would also need your help to choose the correct products to achieve my 2 goals.

1. Child’s Education – 30 lacs after 18 yrs and

2. Retirement Planning – 3 crores.

Goals Monthly Investment Rate Of Interest Tenure Maturity Amount

Child Education 5000 12% 18yrs 35,25,193

Retirement plan 10000 12% 30yrs 3,05,20,132

Please advise.

Vimal-Regarding valuation of surrender, please contact LIC branch they will guide you in better way. Regarding the goals you mentioned, may I know how you arrived at Rs.30 lakh and Rs.3 Cr?

Hi Sir,

iam shairif and my age is 24 and iam working as a office admin. I was joined in job after completion of my course. I want to invest money that i will get a bulk amount in futute though it can help me at that time. I searched many policies b i was confused. can u please refer me a good policy though i can save money for my future use from now.

Meera-Can you define the meaning of bulk amount and within how many years you want to have it?

Hi Basavaraj…Could u tell me pros n cons of ths policies (Endowment & Money back plan) in details so that we cn cm to know about that fact why r u saying Stay Away from these coz I ws also interested in Money back Plan…Could u suggesst Any good Term Plan. .. i am looking for a policy which cover mu life as well as give me good investment. Could u suggesst me anyone?

Thanks in Anticipation

Satnam-Why you buy insurance? To cover your life sufficiently thinking that if death occurs then your nominees will live a life as they are today. Why you invest in any product (especially for long term)? To get good return (again definition of good return varies as 8% to 25%). But the ideal investment for long term should be to beat inflation (also called real return). So in case of endowment and money back plans both these requirements not get fulfilled. Because you can’t buy insurance cover for yourself to the tune of around 15-20 times of your yearly income (set as 15-20 times because at least for next 15-20 years your dependent may survive with current income flow). Return from such policies will be around 6% where as inflation rate itself now 6% to 8%. So how you sustain in long run??

The ideal solution is NEVER MIX YOUR INSURANCE NEED WITH INVESTMENT NEED. Now choice is your’s.

Dear Sir,

Glad to see your site,there are very people who feels Need Based Approach is very significant in sales process.I called it Process,as actually it is not far different than treatment given by a doctor to patient after diagnosis of disease.

I’ll be in touch with you to exchange knowledge.

Makrand-Pleasure 🙂

ok thanks lets wait and watch

dear sir,

finally what is your conclusion shall we proceed with this policy as per your last post of endowment policy you hav recomend to stay away,

and another querry of or still we wait & watch for new products.at what period we hav to wait for reviews.

Raj-STAY AWAY. Because Moneyback plans are worse than endowment plans. So concentrate only on term insurance. Let us wait when LIC will come up with competitive term plan 🙂

sir, i want to buy an insurance plan plz suggest me which better between lic new jeevan anand and new money back plan. for the term 25 year. and sum assured money is 2 lakhs or endowment plan. my age 25 year.

Ranvijay-Both are not good. Better to opt for term plan.