LIC is launching a new money-back and Guaranteed Addition plan of LIC Dhan Rekha 863. It is a Non-Linked, Non – Participating, Individual, Savings, Money Back Life Insurance Plan.

Let us look at the plan features, eligibility, and whether one should buy this product or not.

Features and eligibility of LIC Dhan Rekha 863

All modes of premium payment are available like single premium, yearly, half-yearly, quarterly or monthly. The attraction of this policy is the GUARANTEED ADDITION and the rates of the same are as below.

Term 6-20 Yrs – Rs.50 per Rs.1,000 Sum Assured

Term 21-30 Yrs – Rs.55 per Rs.1,000 Sum Assured

Term 31-40 Yrs – Rs.60 per Rs.1,000 Sum Assured.

It means suppose if you opted for 30 years policy, then there is no GA from the 1st year to 5th year. From 6th year onwards to 20 years period, the GA is added at Rs.50 and then from 21 to 30 years, the GA is considered as Rs.55. Like this, the GA will increase based on the above table and terms of the policy.

LIC Dhan Rekha 863 Benefits

Let us now look into the LIC Dhan Rekha 863 benefits. Usually, in the case of such money-back plans, there are two types of benefits. One is survival benefit (if the policyholder survives till the maturity date) or death benefit.

# Surival Benefits of LIC Dhan Rekha

Survival Benefits under this policy is payable as below based on the term of the policy.

20 Years Policy – 10% of Sum Assured at the end of 10th and 15th Year. On 20th year, the Sum Assured + Guaranteed Addition @ Rs.50 per Rs.1,000 Sum Assured from the 6th year to the 20th year is payable. For the 1st to 5th year, there is no GA.

30 Years Policy – 15% of Sum Assured at the end of 15th, 20th, and 25th Year. On the 30th year, the Sum Assured + Guaranteed Addition @ Rs.50 per Rs.1,000 Sum Assured from 6th to 20 year is payable. From 21st to 30th year, the GA @ Rs.55 per Rs.1,000 Sum Assured is payable.

40 Years Policy – 20% of Sum Assured at the end of 20th, 25th, 30th, and 35th Year. On the 40th year, the Sum Assured + Guaranteed Addition @ Rs.50 per Rs.1,000 Sum Assured from 6th to 20 years is payable. From 21st to 30th year, the GA @ Rs.55 per Rs.1,000 Sum Assured is payable. For the final 31st to 40 years period, the GA is calculated @ Rs.60 per Rs.1,000 Sum Assured is payable.

# Death Benefits of LIC Dhan Rekha

If a policyholder’s death happens during the policy term, then 125% of Sum Assured + Accrued Guaranteed Addition.

LIC Dhan Rekha 863 – Should you invest?

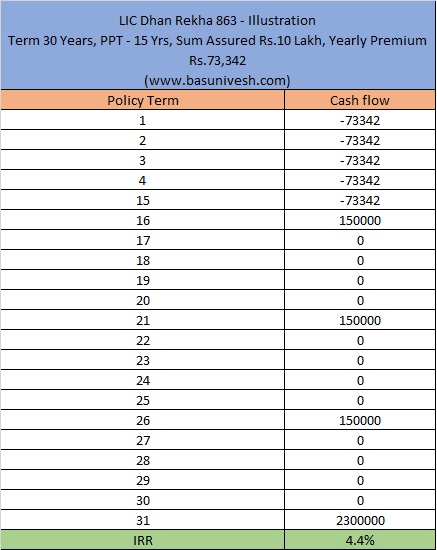

It is a typical traditional plan where the returns are less than or around 5%. The only thing that you can see here is again LIC is bringing its old concept of selling the products as GUARANTEED. As I told you many times if you really wish to sell something in India BLINDLY, then three things matter – Tax Saving, Guaranteed, and Tax-Free returns. This is one such product. However, generating around 5% returns for your long-term investments like 20, 30, or 40 years is not worthy. Let me give you an example of this plan and show you how it works.

In the above example, you start paying the premium from the 1st year to the 15th year. On completion of 15th year (beginning of 16th), 20th and 25th year, LIC will give you 15% of Sum Assured. After the completion of 30th year (beginning of the 31st year), LIC will pay you the full sum assured i.e Rs.10 lakh and GA as Rs.50 from 6th to 20 year (Rs.7,50,000=Rs.50,000*15) and Rs.55 from 21st to 30th year (Rs.5,50,000=Rs.55,000*10). So in total, you will receive Rs.23,00,000 after the completion of 30 years.

You noticed that the returns are so minimal that hard to say how LIC designed it. If you are happy to get 4.4% returns by investing for 30 years, then go ahead and enjoy this policy.

The catch here is that from the 1st year to 5th year, LIC is not giving you any GA. It is a kind of ZERO return on investment.

Considering all these horrific features like long-term abysmal returns, I strongly suggest you stay away from such products. I know that agents may try to pitch you the product with the claim of GUARANTEED, TAX SAVING, or TAX-FREE MATURED amount. But at what cost? If the inflation is at around 6% and such products offer you 5% returns, then obviously by each passing year, you are under the negative return of -1%.

THINK TWICE BEFORE BUYING SUCH PRODUCTS. By selling this product to you, LIC agents DHAN REKHA will increase but not your’s.

Your comments are freely available on Internet, still people are asking for information about traditional insurance plans, why it is so?

Dear Gaurav,

Sadly people want READYMADE and INSTANT answers 🙂

Dear Basu….Thank you for all your efforts and informative articles. My daughter is 3 year 11 months old and we want to make a suitable investment where I can pay premium of 75k – 1 lakh per year for the next 10 years and want to get the money from this policy when she turns 18 or 19 years old for her higher education. Please suggest suitable suggestions with maximum returns. Thank you in advance.

Dear Raghav,

Why Life Insurance for INVESTMENT?

CAN YOU EXPLAIN HOW YOU CALCULATED IRR ??

IRR(values, [guess])

Is this the formula used in excel ??

Dear Manu,

Values matters than guess (you can ignore it). Refer my Youtube video also on how to calculate LIC policies returns. Otherwise, you can refer various videos on how to calculate IRR and XIRR.

Hi.. I guess Jeevan Umang is a better one in recent launches. Guaranteed is 8% and also covers life risk

Dear Salam,

GUARANTEED 8%?? Cross-check your fact properly, please.

In fact, LIC agents earn anywhere between 15% to 25% on first year’s premium and then a flat 5% commission for the rest of the Policy term. All LIC policies are designed to make their agents richer and that’s why the RoI is abysmal low at around 5 to 6% p.a. IRR.

Dear Kamal,

Rightly pointed 🙂

What is the commission rate of dhan laxmi plans

Dear Basant,

Are you asking as an investor or agent? For 10 years premium paying policies, the commission is 20% in the first year and then onwards 7.5% and 5%. For 15-20 years premium paying policies, the first-year commission is 25%.

Sir my take is LIC is offering 4.38%for 30 yrs… In many countries there is no concept like Interest. Here Insurance 10,00,000 for 30 yrs + Guaranteed returns @ 4.38% without Deducting Survival Amt…. I feel it is a uno product from LIC.

Dear Sankaranarayan,

Why for 30 years of investment, do we have to run behind the concept of interest? If an investment product giving you 4.38% returns for 30 years investment seems to be like 8th wonder of the world, then please go ahead and buy.

The above policy or for the reason of any life Insurance policy rarely gives a good return. We need not look to any life insurance plan for return as an investment.

Dear Narendra,

Why to look for any other life insurance for investment? Why not look at investment products for investment?

Is this good policy to invest money sir

Dear Wajeed,

As I told you, if you feel around 4% returns are best for your long term investment, then go ahead. Otherwise a complete NO.

Which product we should buy?

Dear Vishal,

Hard to say BLINDLY without knowing your financial life.

Sir can you please suggest any other plan which can give me better guaranteed return than this plan.

Regards

Bhanu

Dear Bhanu,

If you feel GUARANTEED 4.4% is the BEST investment for you, then please go ahead. However, just imagine the value of whatever they give at maturity be for how many months expenses for you? If you are ignoring the cause of INFLATION, then you are at the wrong end. It is up to you to decide.

Dear Basu Sir,

Nicely explained and written.

Last sentence is just too good ” LIC agents DHAN REKHA will increase but not your’s”

regards

Dear Rajesh,

I really appreciate your each comment and thanks a lot.