IRDA published its annual report on 9th January 2019. Let us see the IRDA Claim Settlement Ratio 2017-18 and also which is the Best Life Insurance Company in 2019.

What is the meaning of Claim Settlement Ratio?

Claim Settlement Ratio is the indicator how much death claims Life Insurance Company settled in any financial year. It is calculated as the total number of claims received against the total number of claims settled. Let us say, Life Insurance Company received 100 claims and among that it settled 98, then claim settlement ratio is said to be 98%. Remaining 2% claims the Life Insurance Company rejected.

Based on this, we can easily assume how much customer friendly they are in dealing with death claims. However, I warn you that this claim settlement ratio is raw data.

It will not give you a clear picture of what types of products they settled. They may be Endowment plans, ULIPs or Term Insurance Plans. Hence, this is not a sole criterion in judging the performance of a life insurance company.

IRDA Claim Settlement Ratio 2017-18

Below is the IRDA Claim Settlement Ratio 2017-18 or up to 31st

You notice that among total 24 Life Insurance Companies, around 11companies are in GREEN (Claim Settlement Ratio above 95%). Rest of them are below 95%.

As usual, LIC tops the list. But don’t feel happy. Let us see the claim amount settled by individual companies to arrive at best companies.

Average Claim Settlement Amount of Life Insurance Companies in 2017-18

As I said above, the claim settlement ratio will not give you

Here come the results !! LIC stands in lowest with red in

It shows that, even though LIC settled the highest number of claims, the majority of such claims are less than Rs.2,00,000 Sum Assured. Hence, it is indicating indirectly that LIC’s claim settlement is mainly in the category of Endowment Plans but not Term Insurance.

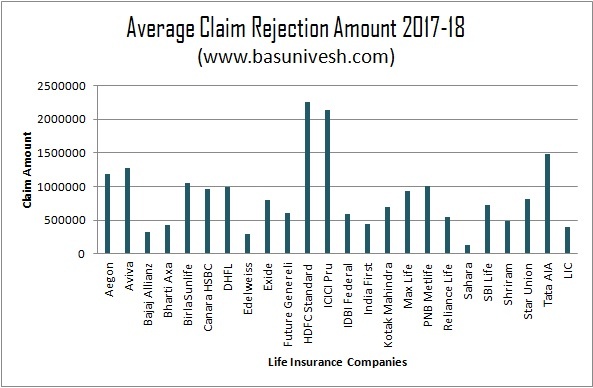

Average Claim Rejection Amount of Life Insurers in 2017-18

Now let us go deeper into IRDA Claim Settlement Ratio 2017-18 and try to analyze the how much amount of claims they rejected. Here, I calculated average amount as I don’t have data to check the maximum and minimum amount.

The results are as below.

You notice that Sahara’s claim rejection amount is less and then comes the LIC. LIC’s claim rejection is less because the quantum of claims it handles is HIGH but value is less. So no need to say that LIC done a great job here.

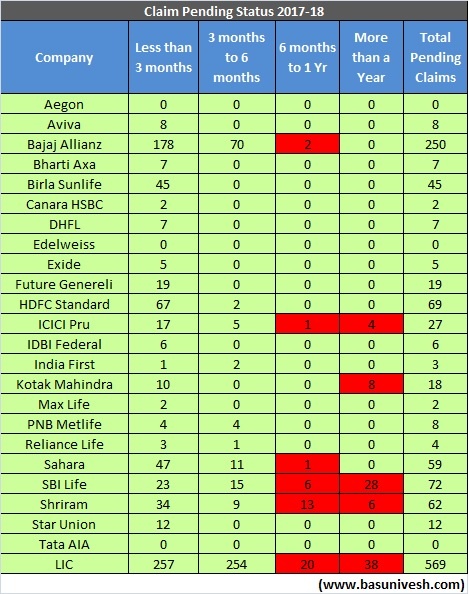

Claim Pending Status of Life Insurance Companies in 2017-18

The greatest fear for all of us is how fastly the Life Insurance Companies settle the claims. Let us now analyze the data of claims pending with Life Insurance Companies in 2017-18 and how old they are.

You notice that ICICI Pru, Kotak Life, SBI Life, Shriram

Top 10 Best Life Insurance companies in India for 2019

Based on the IRDA Claim Settlement Ratio 2017-18, which are the Top and Best Life Insurance Company in 2019? I select only ten based on the above data. You may differ in my view and come up with a different set of ideas. But these are my choices.

- LIC

- Birla Sunlife

- Aegon

- Bharti Axa

- Exide

- HDFC Standard Life

- ICICI Pru Life

- Max Life

- SBI Life

- Tata AIA Life

Few important points before jumping into selecting of Life Insurance Companies

# Claim Settlement Ratio is raw data

As I pointed above, claim settlement ratio is just a raw data. It will not give us the specific data. Hence, never rely on this single data alone while shortlisting the insurance company.

# Concentrate on Product rather than company

Choose the product which suits your requirement and premium affordability. Declare the facts properly. Never hide any material facts. If all these you do, then an insurance company will have to accept your claim. Never give a room of suspicious on you to reject the claim.

# Section 45 of Insurance Act will guard YOU

According to Section 45 of Insurance Act “No policy of life insurance shall be called in question on any ground whatsoever after the expiry of three years from the date of the policy, i.e. from the date of issuance of the policy or the date of commencement of risk or the date of revival of the policy or the date of the rider to the policy, whichever is later”.

It says a lot. Even if you shared wrong information or hid some material facts, then also it is purely life insurance Company’s responsibility to dig deep and find out faults WITHIN 3 YEARS ONLY. After 3 years, they cannot question. Note the period of 3 years, it is from the date of issuance of the policy, or the date of commencement of risk or the date of revival of the policy or the date of a rider to the policy, WHICHEVER IS LATER. So let us say if you took the policy today and after a few years, the policy lapsed due to non-payment of premium. However, you thought to renew it again and paid all dues. In such situation, this 3-year period starts from such revival date, but not from the original policy issued date

# Disclose the facts Properly

While buying Life Insurance products, you must fill the proposal form on your own. Never allow any agent or Life Insurance Company representative to fill it. Disclose the facts properly without hiding anything. This will really help you in a big way. Also, it will not give any room for insurers to reject your claim.

Do the things properly which are in your hand. Rest HOPE for the best.

Can a nominee pay (via netbanking) the first premium of the Term plan? Will there be any problem?

Dear Raj,

Why nominee?

Can I buy a term policy from edelweiss tokio? How is this policy, please suggest me…

Dear Arunava,

I suggest a plan from well-setled companies.

Which is the best term insurance to buy in india

Dear Jacobjohn,

Refer my post “Top 5 Best Term Insurance Plans in India 2019“.

Dear Basavaraj,

Thanks for a nice blog with much useful info.

I recently , 20 days back purchased a term insurance with HDFC – 1Cr – 85yrs with approx 2.5k premium through Coverfox. Mainly because it had few features like add on rider Waiver of premium in case of Permanent Disability and Critical Illness. Also there was no Medical Checks performed eventhough they mentioned it will happen within a week. Recently I got a call from policybazar stating the claws for these features are very stringent and certification of IMA approved Doctors is must and suggested to switich to Tata AIA as premium for this is approx 1.2k less than HDFC without the features. How can we judge here ? Which company is best for Term Insurance in your view ? What are the other hidden factors that we need check from the company or else where? Where can we get the details of Term insurance data of these companies? Kindly could you help in this regard.

Thank You in Advance.

Dear Manohar,

I can say one thing, both HDFC and Policybazaar playing with you.

Hi,

The claim settlement % as said dont tell amount how much amount. In case of term plan say I took a plan for 50lacs and while settling they settled the amount for 10-15lacs still its considered settled? From where to get info How much claim amount is filed and how much comapny has settled?

Dear Rajanikant,

CSR data is raw data. It will not classify what type of products the companies settled. For example, LIC is topper in claim settlement. However, the average claim amount settled by LIC is like less than Rs.5 lakh. This shows LIC settled mainly traditional plans. Hence, never rely on CSR alone to buy term plan.

I want take policy from PNB met life is it okay please suggest

Dear Vinay,

If you already selected, then what is the issue here?

If Nominee has no surname as per documents for example SITA..And the proposal form shows nominee name as SITA NA. Here NA being told as Not Applicable by insurer. Can it be a cause of dispute or rejection in future.

Dear Sandeep,

NO.

I have initiated process of Max life term plan with return of premium of 75lac with 50 years terms including waiver of premium. Which covers me up to my age 80 and waiver of premium upto age of 65.

Before processing application I told them to take physical medical examination but they took tele-medical and issued policy. I denied the policy.

Now they are not answering or giving me any status of policy since last 10 days.

Should I cancel my policy or any other suggestion?

Dear Kashyap,

Better to cancel.

Dear Sir

I have planned became an agent with Adithya birla life insurance company.

Pls gave me suggestion about company

Dear Dhanjaya,

What suggestion you are looking at?

Hi Basavaraj,

This blog is really useful. Thank you. Can we please get the new updated charts for the year 2018-19?

Also, any tips for NRI’s to buy term plans in India? Is the claim settlement ratio different for NRI Term plans?

Please suggest.

Dear Suma,

This is the latest data available. Regarding Term Life Insurance for NRIs, think if you are planning to return before you retire. Otherwise, better to buy in the country where you staying. Claim settlement ratio is company-specific and will not change based on customers. Hence, it will remain same.

Thank you Basavaraj. I was looking at the MaxLife pure term plan of Rs. 2 crore. They mention that there is no medical checkup required if I provide all my financial proofs. But, I am planning to buy this policy only when I am in India for my vacation. So, is it better to get the medical checkup done before buying the policy?

Also, I had been issued a quote for “MaxLife Assured Wealth Plan” with (policy term of 10 years) sum insured of Rs. 57,00,000 for the annual premium of Rs.7.5 lakhs (premium payment term is 5 years). There is a death benefit for this policy.

– They claim that I need NOT pay any GST for the premium- Rs. 7.5 lakhs, if I pay in foreign currency. Is it true?

– Is 2 % TDS applied on my sum insured after maturity?

– The agent says that the amount is completely reptriable to foreign currency after 10 years. Is it true? or is there any trick in that?

– If I opt to convert INR to dollars after 10 years, do I have to pay any tax in foreign country for the profit I earned?

Please suggest. Your inputs are really valuable.

Dear Suma,

Many times these insurance are in a desperate mode to acquire the clients and hence go for non-medical policies. However, if you are declaring the facts properly, then no need to worry.

-I am not sure how they are going to compensate. It is one more lure to acquire the clients.

-Why for limited premium payment and why not regular yearly payment? No, there will not be any TDS.

-It is correct.

-It depends on the country where you reside.

But I logically saying, avoid any company which is eager to issue the policy without medical, by throwing the rules of GST and desperate to get the business. Also, if you are planning to stay forever in the country where you reside, then why you buying term life insurance from India?

Thank you Basavaraj for your prompt response.

I am currently residing in Australia and I have no idea if I will stay here forever or will go back to India 🙂 . I have bought a term insurance here in Australia which is linked to my Super account (an Australian govt declared pension scheme). Now, after 4-5 years if I decide to come back to India, I won’t be in a position to pay the premium in $$, as it is too expensive. Considering my age- 32, I want to make sure I buy a term plan in India as a backup option. So that, I can continue it when I’m back in India.

Now, I am actually looking for 2 different plans with MaxLife. One is ‘Assured Wealth Plan’ and another is ‘Pure Term Plan’. I opted the assured wealth plan because of its high returns and death benefit (also GST waive off). I am more concerned about savings for my kids education down the line after 10-12 years. When I looked at the child plans, the returns were very less compared to Assured plans. Also, in Australia the FD/ savings/ child plans interest rates are far less than that of in India.

When they confirm the GST waive off through an email communication, aren’t they bound to follow it? Please let me know if there are there any expected flaws/ issues with these kind of Assured plans that i need to be aware of.

About the Term plan, I will definitely avoid buying it without physical medical checkup. Any thoughts about the pure term plans of MaxLife with HDFCLife in-terms of claim settlement and trust.

Thanks again!

Dear Suma,

” I want to make sure I buy a term plan in India as a backup option. So that, I can continue it when I’m back in India.”-In that case you can.

Do you think these Insurance+Investment plans suitable for your kid’s future goals? You are considering the returns of the country where you stay to the returns in India. A normal NRE account FD is far far better to return generator than these bundled products. Regarding the GST, I still suggest you to reconfirm their claim. Both HDFC and Maxlife are good. You can go ahead (with the cautions I shared).

Hello Basavaraj Sir,

Really good article ! Came to know more factors other settlement ratio.

(1) Nowadays there are so many companies providing Term Insurance. So can we get data: from last how many years any company is Selling Term Insurance.

(2) And I just have 1 doubt – If we buy Term Insurance for next 35-40 years, and If unfortunately that company get closed in Future. So who will settle the claim ?

Dear Raghunandan,

1) How it helps you?

2) Refer my post “What if your Insurance Company goes bankrupt?“.

Hi Sir,

They have issue me 2 Crore policy without medical examination. All documents are taken directly from ICICI bank I mobile application as i have salary account there directly and it is issued in 30 Hours ( All digital verification carried out ) . Will it affect change of claim rejection as medical is not carried out.

Age : 27 Years.

Dear Test,

If the disclosure done by you are PROPER, then no need to worry.

Hi Sir,

I have purchase policy from Imobile application of ICICI.

They have made a lot of chnges in data i have shared. like

1) Nominee spelling mistake

2) Medical condition of parents i said they had medical issue even i told same during telemedical. however it is not considered in application form. though i have mentioned same there.

Dear Test,

It is a RED FLAG if they changing the disclosure on their own to issue the policy. Better to discontinue immediately.

Hi Sir,

Planning to take term plan. They have asked me to fill proposal form, and also called me for my medical details.

They anyways have done my medical checkup. So if there is any mismatch between Proposal form, Tele Medical and Actual Medical, if they still accept the contract, would they able to reject claim on this ground in future?

So if there is any mismatch between these three, would they be in position to reject claim? Or as they have done my medical checkup, previous 2 does not hold any meaning now?

Dear Nikas,

“They anyways have done my medical checkup. So if there is any mismatch between Proposal form, Tele Medical and Actual Medical, if they still accept the contract, would they able to reject claim on this ground in future?”-THEY ACCEPT PROPOSAL BASED ON YOUR MEDICAL TESTS.

Thanks Basavaraj,

So tele medical, proposal form wont hold any meaning in future now right? Or should i inform them if there is anyting (like dates, for my mothers previous hospitalization i gave 1999 my mistake in proposal form where it was 2009 as in tele medical) wrong in proposal form?

Dear Nikas,

A medical examination did means telemedical will not hold. At the same time, if they found any other information wrongly shared by you, then there is a possibility to reject the claim.

Is SBI life reliable for term insurance?

Dear Mahendra,

Yes. Why you are doubting?

As per the data Max life performed very well compared to top 10, but it has been kept at 8th position. Any specific reasons?

Dear Gaurav,

As I said above, its based on my comfort. If you are comfortable with Max Life, then no harm.

Hi Sir,

I took term plan of 1 Cr from Edelweiss [ Plan name : Edelweiss Tokio Zindagi + ]

Is it good ?? or should I opt for other company ?

, since i got the additional option of better half benefit which suit all my requirement.

Please guide.

Dear Rahul,

If is it suitable for your requirements, then why to worry?

BECAUSE AFTER THE DEATH OF PRIMARY POLICYHOLDER SPOUSE COVERAGE GET STARTED, THATS WHY HE NEEDS TO WORRY BASAVRAJ SIR

Dear Prateek,

What I mean to say that if features are suitable for your requirements, then go ahead. But I usually avoid new entrants.

Hello Basu Sir,

Referred your few articles. I am 35 years old. I want to take term insurance of 2 CR for next 35 yrs.

I want to split it in 2 companies. I have filtered 3 choices:

• HDFC Standard Life

• ICICI Pru Life

• Birla Sunlife

Can you please guide which are the best 2 companies in long run from reliability point of view?

Secondly, what should be my % of sum assured between two companies from reliability point of view?

Regards,

Onkar

Dear Onkar,

Why two and why not ONE?

Sir, I have want to choose BEST 2 companies in order to mitigate the risk and dependency factor. Please suggest.

Dear Onkar,

How it diversify your risk?

Sir,

If in case, one company does not approve my claim then I can depend on another company.

Dear Onkar,

What is the guarantee that another will accept? What if the rejected company share this with another company?

Ok Valid point. So please suggest me the best term policy plan for 2 cr. as I need to apply before 31st July.

Dear Onkar,

Refer my post related to best term life insurance.

Hello Sir,

I am Arun, My age is 37.

I want take term plan of 1cr cover.

My income is variable yearly, any year it is above 5 lac and other year may be 1 lac, as i work independently,

If I get term cover on current income base, and at the time claim its not the same, as if it is less, would it be matter at time of settlement of claim?

– Arun

Dear Aru,

Don’t worry, for Life Insurance company your current income is necessary to issue the policy but not the future.

Hello Sir , Iam 31 years old and Iam planning to buy a term plan .

Iam really confused weather to go for LIC company or Tata Aia company (which is giving me 99 year cover) ??

Thanks.

Dear Viraj,

What is your confusion?

is it better to take Critical illness in term plan rather in health plan

Dear ABC,

Better buy it separately.

Hello, Sir

I took ICICI’s term insurance on 26.06.2019.

And my 12th is + Duploma. But if the form has been graduated at the time of filling, then there will be some problem whether Sir

thanks

Dear Kishor,

NO.

Hello sir,

Two years ago I tried for LIC e term plan of 75 lakhs but in health report some sugar factor was increased slightly so LIC increased the premium. I did not opt. Now after two years again I applied. This time my all reports are perfect. But still LIC is charging higher premium.When I asked they replied that all reports were considered (previous also) so the premium is high. Please suggest what to do. Are they telling lie?

Dear Harshit,

Whether they are telling lie or truth, whatever they say, the final thing is you have to accept it. Otherwise, opt for another insurer.

Hi Basavaraj,

Can we get the list of reasons why an insurance company reject a claim? Is it available anywhere in IRDA or any other common known facts ?

Dear Mohan,

It is hard to collect the data and arrive at the general conclusion. Because there are MILLIONS of reasons for death and same way MILLIONS of reasons to reject the claim.

sir, do you have any suggestion for curving down claim ratio in group mediclaim.?

Dear Anumisha,

Sadly NO.

Dear Basu sir,

Out of your selection, ICICI Pru and HDFC have highest claim rejection amount. Do we need to worry about that… And is there any problem to deal, if term insurance is issued by issuer without any medical checks, is it have any high probability of rejection?

Dear Adarsh,

Regarding claim rejection, you no need to worry. They are not so big. Yes, if the policy is issued without medical examination, then it is a bit risky.

Thank you for the swift reply and kind advice. Currently My BMI is 26.1 , I think it will increase the bare premium, Better to have a diet and gym session before medical examination… Is it better? …

Dear Adarsh,

Being healthy is not only important while buying insurance but for you and your family also.

Hi sir in term plane if the person dies due to alcoholic and smoking habbiet and the declaration is given at the time of form submission that person is smoker and drinker so is there any possibility policy company can reject the claim

Dear Sunny,

If the death occurs within 3 days, then it is hard to say that claim get accepted or not. Also, by disclosing the wrong facts, you are risking your financial dependents.

Sir, My age is 23 and i want to buy a term insurance of 1 crore, suggest me which company i choose? Please specify a single company.

Dear Shaunit,

Refer my post “Top 5 Best Term Insurance Plans in India 2019“.

Hi Basu Sir,

I am 31 year old, I am getting confused between ICICI, HDFC & Aegon for term plan. Which 1 would u suggest to go with. or at least can you please tell me the order in which you rate them.

Dear Piyush,

Refer my latest post “Top 5 Best Term Insurance Plans in India 2019“.

Sir, in your opinion, which is the best health insurance plan I should go for. Which one would you choose?

Dear Dennis,

Refer my post “Top 5 Best Health Insurance Plans in India 2019“.

I want to insure my life for 1 crore, is it good idea to cover myself with LIC and Max life 50% each? As LIC is good in terms of claim rate and Max is good in terms of premium to be paid. – Does it make sense ?

Dear Harish,

There is no logic in spreading your cover in different insurers.

For 1 crore coverage LIC chargers more premium (nearly 30k) where as Max charges 16k. Hence I wanted to split the coverage between these two. This saves nearly 10k premium amount and as LIC’s gives better settlement claim, some part of settlement risk is also covered. Do you agree with this sir? Need your view to take wise decision in terms of this risk coverage? Many thanks 🙂

If one company rejects a claim than the other have a reference to reject with no more explanations. Typically LIC claim settlement takes long time. If your claim is rejected by Max, LIC will probably do the same. Important is that you provide all the details correctly when buying the policy. Splitting the policy is not of much help. You should rather focus on your investments. Just buy a plain term policy.

Sir if there really million reasons of rejecting claim.. Then we can say we should not be be optimistic… Rather choose some other way of protecting our family..

Dear Harinderjit,

May I know which way you can protect your family in case they are financially dependent on you? Eager to listen and learn.

What is the maximum amount insured in term policy, if I got 1 lakh per month.

Dear Ravi,

There is no such Maximum amount limit. However, life insurance companies issue the policies based on your income, age and health.

Hi Basu sir, Thankyou very much for speedy response for giving such good information and knowledge thanks for the same.

You have posted some amount on Y- axis but you haven’t clearified that amount is in lacs or crores or any other. Please mention that. Rest article is awesome and very useful thanks for this.

Dear Mubin,

Obviously, for both average claim acceptance and rejection, it is in LAKHS but not in CRORES.

Sir, will it be good idea to purchase 2 or 3 different companies plan of 40 lakh each rahter than one crore of a single company ?

..bcz. risk factor will be minimized there.. plz give suggestions

Dear Inder,

How can you GUARANTEE that by diversifying this way your all claims will be settled? Do you know the reasons for your death NOW?

Hi Basu sir, Thanks and appreciated, Every year your are giving such good information and knowledge thanks for the same

Dear Sat,

Pleasure 🙂

The way it is mentioned in life insurance that even if wrong facts are mentioned in the application , it cannot be the ground for rejection of claim after 3 yrs, is there a simailar clause for mediclaim? Pre existing disease is at times misused by insurance co. One can not possibly have all ailments details for last 10/15 yrs if one is taking mediclaim at age of 35/40. I understand that if symptoms have not appeared in last 4 yrs it is not treated as pre existing disease. is that correct?

Dear Dipak,

Sadly there is no such clause in Mediclaim.

Hi sir, is there any data available about claim settlement ratio of exclusive term policies? Because above data is showing that all companies settled the policies whose claims are near to 10 L. So what is the fate of term policies whose claims will be more than 50L as in recent years term insurance has gained popularity because of huge coverage with nominal premium.

Dear Sudheer,

I already mentioned in above post that neither IRDA nor Life Insurance Companies taking it seriously to share in a better way.

What are the reasons behind rejection ?

Dear Rattan,

It is hard to say the reasons as there are MILLIONS of reasons for an individual’s death.

I have a query regarding this Claim Settlement Ratio numbers for LIC. Does it include the closure done for ULIP and Endowment Policy also?

Dear Puneet,

This above data for all insurance companies is combined of Endowment, ULIP and Term Insurance Plans.

Thank you for your reply. Then it’s not necessary that LIC has good IRDA Claim Settlement Ratio, as most of the plans are Endowment and ULIP.

Dear Puneet,

Yes, I already mentioned the same.

Sir,

1) if we will pay premium regularly of term insurance all the time, then after 3 years any company has to settle the claim without asking any question.. this means that after 3 Years it will not matter that from which company you bought the term insurance.. So is it advisable that buy the cheapest online ? and pray that there will be no mishappening at lease for 3 Years.

2)Another point if you choose the company which has the cheapest premium and provide all the details correct and hide no details then also chance of claim settle is good if mishappening happen before 3 years.

So can you please suggest me 3 company which has the cheapest premium in term Insurance ??

Regards,

Ketan Patel.

Dear Ketan,

1) This is what I often say. Many people do such intensive research to buy such a simple product. There is no such guarantee that even Sec.45 may protect your death. Because cause of death is not KNOWN TO YOU NOW.

2) They simply can’t deny the claim just because their premium is CHEAP.

Good research on term insurance. Can u please share the types of rejections by insurance companies during settlement. Why there is no riders in LIC?

Dear Rao,

There are millions of reasons for an individual’s death. Same way there are millions of reasons for claim rejections also. Hence, it is hard to generalize and share. LIC offers riders. Please check the plan features.

hi,

Is there Star health insurance claim ratio included in this article…I saw Star union being mentioned, but both are different right..???

Dear Mohan,

This post is related to Life Insurance Companies but not for General Insurance companies. Hence, Star Health Insurance data is not included here.