Which are the Top 5 Best Health Insurance Plans in India 2019? How to shortlist and what the cares you have to take care before buying the plans? Let us do the review and comparison.

Along with Life Insurance (Term Life Insurance), Health Insurance is also a must product one must have. While in case of Life Insurance, you have to buy it only if you have financial dependents. , However, this is not the case with health insurance. All of us have to buy as we don’t know when we get hospitalized due to illness.

An exception to this is, if you created enough corpus for your hospitalization need, then you may not need to buy health insurance. But many of us simply ignore the hospitalization cost in our life. Even salaried not worry about buying separate health insurance (even though company providing).

Cost of hospitalization as per my understanding inching up at the rate of 10%. Hence, in many cases, it is impossible to fund the hospitalization expenses from our own savings. A week hospitalization in expensive cities like Bangalore may ruin your few years of savings. Hence, one must take it as a serious need and buy it.

Top 5 Best Health Insurance Plans in India 2019 – Checklist

Before jumping into shortlist your Top 5 Best Health Insurance Plans in India 2019, you must understand what are the points you have to consider.

# Sum Insured: When you look at the rate of inflation of hospitalization, you find that it is nearly around 8% to 10%. Hence, always try to go for a sufficient sum insured health insurance base plan. Consider the members you are including in the policy. Based on that you have to take a call on the sum insured you are opting.

# Incurred Claim Ratio: You have to check the incurred claim ratio of Health Insurance Companies. Incurred Claim Ratio or ICR is a ratio of the total value of claims paid or settled to the total premium collected in any given year. This can be calculated as Incurred Claim Ratio or ICR=(Total Value of Claims Paid/Total Premiums collected)*100.

For example, let us say Company ABC settled the total claim amount of Rs.90 Cr in the year 2015-16. In the same year, it collected Rs.100 Cr as a total premium. In this situation, the incurred ratio stands to be 90%.

This Incurred Claim Ratio is applicable only to non-life insurance companies. For life insurance companies, IRDA publishes Claim Settlement Ratio. But sadly many (even experts) complicate it.

If the incurred claim ratio of a company is more than 100%, then it indicates that for every Rs.100 they collecting as premium, they are paying more than Rs.100 as a claim for a year. In simple terms, your income is Rs.100 but your expenses are Rs.100 or more. So instead of profit, they are into loss.

If the incurred claim ratio of a company is less than 100%, then it indicates that for every Rs.100 they collecting as premium, they are paying less than Rs.100 as a claim for a year. Such companies are making a profit as your income is Rs.100 but expenses are less than Rs.100.

However, rejecting claims only on grounds to profit will not work out for any company. They have to look for reputation, future growth, and regular guidelines. Hence, simply for the sake of profit-making, they can’t deny claims.

In my view, going with companies of high ICR or low ICR is risky. Hence, always choose a company which is in between both these points.

Do remember that Claim Settlement Ratio or CSR applies to Life Insurance products and Incurred Claim Settlement Ratio applies to Health Insurance Products.

Let us now look at the latest Incurred Ratio of all Health Insurance Companies.

You noticed that I have marked in green wherever the companies incurred ratio is good and near to category averages.

# Buy early: Buying at earlier age is the best than postponing it. We don’t know the health issues. Hence, the insurer may reject your proposal. Hence, always buy immediately and never postpone.

# Understand the cover: Identify the features you want to cover. Covering all NOT POSSIBLE. Hence, try to identify the product which covers many illnesses.

#Individual or Family Floater: Decide whether you want to go for individual or family floater. It is always best to go for an individual if the age of any one member of the family is so high than the others. For example, in a family of 4 the oldest person’s age is 65 years and rest of other 3 members age is less than 50 years, then better to buy an individual plan for that 65 years old individual and rest 3 members can buy a family floater.

Because the premium is fixed based on the age of the oldest person also.

# Entry Age and renewable clause: Check the entry age and for how long one can renew it.

# Waiting period: Identify the company which covers existing diseases at early. Usually, all insurance companies have a waiting period of 3-4 years for existing diseases. However, if your concern is to cover the existing diseases, then give first priority to this point.

# Room Rent Capping: Check for room rent capping.

# Co-payment clause: Higher the co-payment means lower the premium for you. Co-payment means how much you also have to pay in a total bill. If the co-payment clause states 20% co-payment, then for all bills claimed, you have to 20% and the rest 80% will be payable by a health insurance company.

# Exclusions: Check for exclusions. If you feel the exclusions listed may be uncomfortable to you, then skip that product.

#Hospital Network: Check for hospital network availability in your city or town. The cashless hospital benefit is better than producing the bills and waiting for claim settlement.

# Policy Wordings: Read carefully the wordings of policy brochure. If you have doubts on any feature, then try to clarify it NOW itself.

# Common Features: Avoid all common features, which companies try to highlight.

# No Claim Bonus Offers: Check for No Claim Bonus company offers.

# Treatment wise limit: Check treatment wise limit if any.

# Premium: Check the premium rates. Especially check the rates for older age rates as few insurers jump the rate drastically for older age coverage.

# Super Top Up: Never rely on a base plan. Down the line, if your coverage is not sufficient, then go for Super Top Up Plans. They are cheap in nature compared base plans.

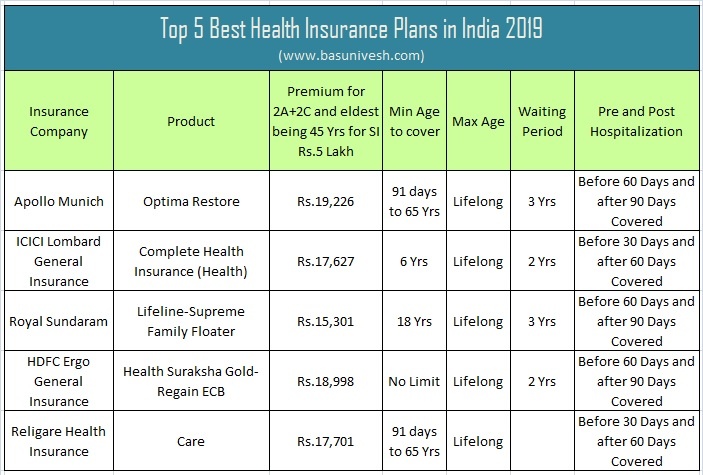

Top 5 Best Health Insurance Plans in India 2019

Now let us jump into selecting the Top 5 Best Health Insurance Plans in India 2019 among those so many Health Insurance providers.

Here, my concentration is mainly on Premium, Pre-Existing disease exclusion, the limit on room rent, wellness programme, restore benefits, claims settled and claim complaints.

Note:-Do remember that they are not on the order.

Disclaimer:- Health Insurance actually depends on your age, family size, your health status and the particular feature you are looking for. Hence, my choice is based on certain generic consideration. It is always best to cross-check the product brochure before you jump into buying.

Also, I am not claiming that these are the ONLY BEST in India. If certain features not suitable to you, then you can look for other products available in the market (but considering the above points which I have discussed).

Hope this article will help you in choosing the right health insurance for you or shortlisting the Top 5 Best Health Insurance Plans in India 2019.

Found your blog useful to decide on the health plan. After a year now, did you find any change in the list of top 5 health insurance plans . If so, please elaborate on it.

Dear Vishvak,

I hardly change. You can go ahead.

Hello Sir,

I want to buy health insurance. Please suggest me good health insurance. What is your about Manipal Cigna Pro Health Plus???

Dear Nikhil,

Refer above post.

Hi

I already have a Parivar Mediclaim family floater of 2 Lakhs, for me, wife and 2 children. I would like to increase the coverage, say by 3-5 Lakhs. Is it advisable to by the second policy from a private insurance? if Yes, which one would you recommend?

The thought behind adding a private insurer is the advantage of cashless facility whereas Parivar doesn’t have it in most of the hospitals in Kerala

Thanks

Ganesh

Dear Ganesh,

If cashless is your concern, then better to go with private sector companies. Refer above post.

Hello Sir,

Aditya Birla is offering 1Cr health insurance plan through policy bazaar for a premium of less than fifteen 15000/year for self and spouse ? should we go for it ?

Dear DP,

Don’t trust Policybazaar. If the features and premium is as per your requirement, then go ahead.

Policy bazaar also recommended me same policy Aditya Birla Capital – 1 Cr. Can someone please specify the list of check points while selecting the health insurance policy?

Dear Nikhil,

It is already listed above.

Hello Sir,

I am looking for a health insurance for my parents. My mother suffers from these aliments

1. diabetes (0ral medication)

2. Hypetension(No medication)

3. COPD(oral medication and inhaler)

My dad is perfectly fit.

Both are senior citizens. Could you please guide me in choosing correct health insurance for them and the insurance amount limit.

Dear Anuj,

I suggest you to go for public sector companies. Especially buy separately for both fo them.

Universal Sompo calculate premium for health insurance on the basis of age of proposer , not on the age of eldest person. This is benefit as the parents can be covered on very low premium.

Dear User,

RISKY ALSO 🙂

Hello Basavaraj,

I have got Family floater health insurance with Religare of SI 10L since 4 years. Looking at the premium costs, I would like to port it to Royal Sundaram(Supreme). They say that the waiting period would be 3 years as I have detected with Thyroid three year back. Do you think it will be a wise decision to switch over to Royal Sundaram? Alternatively, which other option do you suggest?

Dear Shyam,

Whether you checked with Apollo or MaxBupa? Yes, new insurer will definitely put certain waiting period in your case.

Hi Basavara, since the claim ratio of all the public sector companies is very good, shouldn’t some of them be listed in the Best 5 health Insurance policies in 2019?

Dear Ankit,

Claim Incurred ratio is HIGH means they are less profitable. Currently, they may be stable as Govt backed. But for how many years?

Dear sir,

I am planning to take family flooter health insurance plan and critical health insurance

Separately for me(35 years) n my wife (34 years). Is my idea is good? Can you suggest me some good plan.

Dear Ra,

Yes, it is always better to separate. Regarding the products, refer above post.

Hi Mr. Basu, These days we move around cities quite a bit, or even move out of the country. Is it good idea then to buy a health plan?

Dear Sowmya,

Yes, it is best to have your own health insurance as you no need to worry about travel. Because they have network hospitals.

Hi sir,

I want to take health policy for myself Age 26yrs, and my mother age 40 yrs. After my marriage i’ll add my wife in the policy. Which is better thing?

1. Taking separate individual policies for my me and mother and after marriage me and my wife will take family floater plan,

2. Taking combined policy for me and mother and adding my wife in the plan.

Sum assured 7 lakhs

my options are

1. HDFC ERGO

2. Cigna TTK

Which one do you suggest

Dear Ramchander,

1st Option is best.

Hello basu sir, I am 34 years old. My wife is 33 years old. I have Diabetes and My wife has high blood pressure. I have daughter of 6 years old.

Which medical policy i should buy and how much should be amount?

Thank you..

Dear Chirag,

You can check the above products and choose one among them. But make sure that you disclose all facts properly.

Hello Sir,

Please suggest a Good Health insurance for My father AGE : 69.

Does Public insurance provide same for more than 65 yrs age. ?? i checked new india and found limit of 65. Please correct me if i am wrong.

incase i have to go for private please suggest 1-2 options with priority as

1. good settlement ratio

2. cashless feature

3. convinence / good room availability

i was thinking of max bupa, HDFC ergo but is not sure of claim settlement ration.

Thnx!!!

Dear Abhi,

It is hard to get health insurance for his age. Because in many cases the entry age is 65 years. However, you can check with other public sector companies or go with Apollo, MaxBupa.

Dear Basu,

I am 43 years old and had Colon Cancer surgery in June 2018 and am looking for a Health policy for around 10 lakhs. Which one do you suggest?

Further do you advice taking a floater for my wife and kid as well Or is individual policy for all 3 is preferable?

Thanks in advance,

Vijay Kamath

Dear Vijay,

Try to buy the from above listed. Better you separate your need from family need.

I am 63 year old and my wife is 57 years old which health insurance cover and co. you will suggest?

Dear Pradip,

Go with Public Sector Companies.

Hi basu

thanks for the info . I hold a manipal cigna policy . going by the article i feel i should surrender it now and buy a new one . what would you suggest on the same . thanks

Dear Dees,

If there are no issues with the existing ones, then why to surrender?

Hi there!

Very informative article especially when policy Bazaar calls so much without any concrete on product . I recently.lost my job and was covered with HDFC ergo by my office in group policy from last 5 years. I recently was asked to quit due to downsizing and now in a complete fix as I have no other mediclaim and my father has to now undergo frequent dialysis. I tried converting my current group policy into individual plan but the insurance people are not being entirely supportive and they want to read the underwriting . Can you suggest

A plan that covers dialysis

Any suggestion on above

Dear Payal,

This is the biggest mistake many do. How an insurance company will now cover your father when they know that you are buying a policy now to cover your CURRENT expenses?

Hi Sir,

My age is 36, and my wife age is 29, and daughter age is 2 years, which health insurance plan is good for me, please suggest.

Dear Ravi,

Refer above list.

Hi Basu, I have already ICICI Health Saver plan since 2010 and paying premium of 22000/- for 2A+2C. This is market linked plan. Should I purchase any pure health insurance? If yes, which one you suggest!

Thanks.

Dear Rajneesh,

Better to stay away from such junks and buy pure health insurance plans.

Hi Sir,

Any plan for senior citizen, Who’s age is 60.

Dear Anandkumar,

There are specific plans offered by all health insurance companies for senior citizens. You want me to write a separate post? If yes, then please wait.

Yes

Hi Basavaraj,

What about Max Bupa Health first plan. Planning to take for me and my wife. It has very less waiting period. Bit confused, Can you suggest. Eldest age is 27.

Dear Anandkumar,

You can go ahead.

Wont the premium be same every year, Is there any plan like which will have same premium every year?

Dear Anandkumar,

Sadly NO. Because in case of health insurance, the premium will increase based on the age group.

Dear Mr. Basavaraj, I am planning to take a family floater plan of 5 lakhs from Star Health but I have come across many comments online regarding low claims, What is your opinion on this insurance company?

Dear Leela,

Better to choose the one from the above list.

Hello Basu, I am from delhi and hold a medical policy from appolo, the only concern i have is they do nover one of the hospital “Ganga Ram” as cashless. This is one of the good hospitals in delhi. Whats your view of star health

Dear Amit,

Do find if there are any other best hospitals listed (especially within the nearby area of your stay). If the answer is NO, then opt for other insurers.

Dear Basu,

What is your opinion on Tata AIA Health Wallet comparing to Apollo Munich Optima restore?

Dear Ram,

May I know the reason for you to compare that particular product?

Dear Sir,

Please suggest if one should opt for Public Health Insurance or Private? What is the single most differentiator? Would claims for insurance from public companies get approved easily vs pvt? thank you again

Regards,

Isha

Dear Isha,

No such difference. However, look for the features and premium affordability you are looking at.

thank you Sir. Should I go with a floater or individual policies for the husband and spouse (30 and 41 years respectively) as the premium for individual policy seems better for a 10 lac/per person cover compared to a floater policy of 10 lac for two people. Why is it so? What could be the reason for such a difference in premium between individual/floater?

Dear Isha,

Better to go with floater. Whether you compared TWO INDIVIDUAL PLANS with FAMILY FLOATER?

Sir, Not sure what I should compare as both are restore policies so should be the same? 🙁

Dear Isha,

Just read above post properly and understand what you have to look for.

Sir, I understood everything you have said above. The benefits for both floater/individual insurance is same in Apollo or Religare (shortlisted ones). Here is what I see:

2 Individual policies for a couple with 10 lac each cover premium is 10k+12k and floater policy with 10 lac cover premium is 18k…

Regards

Isha

Dear Isha,

In that case which is cheaper? Rs.22,000 or Rs.18,000?

individual plans 🙂

Sorry, I meant buying a 20lac cover as individual plans makes more sense than paying 18k for a 10lac floater

Dear Isha,

How about buying Rs.10 lakh base plan and then opt for super top up plan?

Hi,

IM 36, my wife is 31, Daughters are 6 and 1. I right now have a corporate health insurance from national insurance. IM planning to take another health insurance sepately for my family as IM planning to resign from current company and will open a new company of my own. Which is better ? public sector insurance or private? If so whats the reason?

Dear Uday,

My choices are already listed in the above post.

i have icici pru health saver, family floater of 3 lakh sum assured bought 12 years back .

how can i use fund of it ??

should i take another health insurance or opt for top -up health insurance plan.

please suggest some companies

Dear Gayatri,

If your intention is to enhance the sum insured, then you can enhance the same in the existing health insurance.

Is it safe to buy online term plan.and

How can we claim for a plan purchased online?

Dear Divya,

It is equally safe and your nominee has to approach the life insurance company for the claim.

Why is star health policies not here as it’s the largest health care insurance provider…

Dear AI,

Largest does not mean the BEST 🙂

Hi Basu,

Apollo Optima restore Post hospitalization is 180 days. Please have a look.

Dear Hari,

But when I checked it is same as what I mentioned above.

Sir, I have already purchased sbi health insurance. Should I change health insurance company in the next renewal or should I continue with the same? Please suggest.

Dear Nibedita,

If there are no issues and you are comfortable with the features, then why to change?

Sir, I need a best policy which covers 5 lakhs rupees for my 3 members family. Should I buy family floater scheme? My age is 50 years, wife 44, daughter 14. Please suggest.

Dear Sanjib,

Please go ahead with family floater health insurance. You can choose the product from above list.

Hi Sir,

I plan to buy a Medical insurance for my parents & In-laws all of them aged between 55 yrs to 60 yrs, does this list hold true for this as well?

Dear Nish,

In case of senior citizens, I suggest to check with public sector companies.

Sir, why would public sector companies be a better option for senior citizens? I am planning to purchase one for my mother who is 56 now..and I plan to purchase one for myself although I have corporate insurance that covers my parents and I at this point.

Dear Isha,

They are bit lenient in claim settlement than the private sector.

Okay Sir. I already bought Religare just before my Dad turned 60 and he’s now a heart patient so I cannot switch. Will look for a public sector company insurance for my mom.

Dear Sir,

2 health insurance plan required, 1. My parents – Father-55 , mohter -53 (NON-Smokers, Non-Alcoholic), No medical histroy.

2. My family, Myself-30, wife – 30 , son- 3 years (NON-Smokers, Non-Alcoholic), Only Child having medical history.

Note – Life Style- Normal, less Risky. Employers health insurance for my family and Parents.

Please suggest best companies & plans considering below keeping in mind below aspects

1. Less waiting period

2. Critical illness riders that we can take

3. In house and high claim to settlement ration.

Dear Raj,

Your all wishes can’t be fulfilled.

Please suggest best plan atleast. Thank you Sir

Dear Raj,

I have already listed them in above post.

Sir

Are critical illness’s covered under Health Care insurance plans? Not expecting them to provide a lumpsum like it happens in a pure critical illness plan but are hospitalization costs for a critical illness covered under health insurance?

Regards,

Rajesh

Dear Rajesh,

Hospitalization is covered.

Sir,

I am looking for a health Insurance for a family.Can you suggest me which one I should go. My age: 36, Wife age: 27, daughter age: 8. It’s better to go for individual/ family flotter.

Also how much the insured value I need to take. Need to take super top up also?

Kindly suggest sir

Dear Srinivas,

My choices are listed above. Go for family floater plans. Regarding the coverage, better to go with how much premium you can afford (minimum of Rs.5 lakh) and then super top up.

DEAR SIR

I HAVE MEDICLAIM FOR ME AND MY FAMILY FROM MY JOB, BUT NOW MY CHILDREN ARE NEAR TO 25 AGE AND MY RETIREMENT IS AFTER 5 YRS SO I AM PLANNING TO BUY MEDICLAIM FOR MY SON AGE 24 AND DAUGHTER AGE 26 , IS IT RIGHT DICISION ? WHICH POLICY WILL BE BETTER ? PLS GUIDE ME

Dear Chintan,

Yes, it is the best decision. You can go ahead with the products mentioned above.

Thank you sir for such a great write up ! This is super useful in deciding which health insurance plan to opt for when there are so many of them.

I wanted to know if, for example, I opt for Apollo Munich – Optima Restore, should I include any add on for cancer. This is the option which I am getting in Policy Bazaar when I was comparing plans based on the knowledge that I gained reading your blog. Also, if there are any such plan you would like to suggest along with the ones that you have mentioned.

Regards,

Milan

Dear Milan,

I think your question is about adding the riders like cancer critical illness care. Better you buy such add-ons separately.

Dear sir, Please mention the drawbacks in max bupa Health companion why it is not included in the list as previously I have set my mind for this policy now I am little bit confused.

Dear Sanjeev,

It is in my list and I also recommend to my fee-only clients. Hence, don’t worry you can go ahead. Here, I have to show only the top 5. Hence, I have not listed that.

Dear Sir, What is your opinion on Future Generali Health Total Vital Plan?

Dear Swapnil,

Whether features are OK for you along with premium? If the answer is YES< then go ahead.

Sir, what is the difference between stand alone companies and other. What is the difference.

Dear Rajesh,

Standalone companies involved in the health insurance business. However, other non-life insurance companies involved in other products of general insurance business.

Sir, you have not mentioned about how to buy Health insurance policy? i.e. Online Direct purchase after thoroughly research or go for an agent

Dear Arijit,

I feel better to buy offline if the agent is helpful in claim settlement.

Hello sir,

I have star health policy from last 5 months of 4 lac family floater for 2 member (17, 48,5) my dist network Hospitals totally 5 my near dist network Hospitals 9 . Sir this company. Good are not. Should I change the company to in this 5 top company?please suggest me please sir

Dear Kkapilreddyloka,

Please continue the same as you don’t have any issues as of now.

Hi Sir

I am a two member family with me & wife & baby expected by year end, Pls suggest for best plan. By God blessing having no desease except thyroid to wife. As I am so much confused & want to buy policy before 31st March 2019. Looking for your best & positive reply.

Dear Vinay,

You can choose anyone from the above listed.

Sir Recently I have purchased Aditya birla Health insurance.. Do it was a wrong decision?

Dear Piyush,

Please continue if there are no issues from insurer end.

Sir, I have corporate mediclaim (5lac-20k)with supertop up facility(10lac-30k) all family members covered(2 sr.citizen).wife also working and also has corporate mediclam(5lac-free).i have national insurace mediclaim(4lac-17.5k wife not covered).Should i buy another mediclaim as everyone suggested for me and my wife?

Dear Maunish,

If you dont have your own health insurance (family floater), then better to buy it.

Okay…thank you sir…

Sir i have my personal (and old national insurance) mediclaim with my parents(4lac at premium of 17.5k).Should i buy new mediclaim with my wife or should i include my wife in national insurance mediclaim?

Dear Maunish,

Better you separate you and your wife health insurance with your parent’s health insurance.

Sir

what is ur views on Personal Accident coverage attached to Health insurance.STAR COMPREHENSIVE INSURANCE POLICY offering this option [Personal accident cover against Death and Permanent total disablement (equal to the Health Insurance cover) at no additional cost].

I may choose Star insurance company bcoz it’s the only insurer has the network hospital near to my home.

So expecting ur valuable reply whether we(me and wife only, Am now in 30 the age) opt this policy or should go for floater basis family health optima plan and personal accident insurance plan separately?

Dear Albin,

Such small coverage of personal accidental not sufficient. Rather than that, better you choose separate accidental insurance from the same Star Health Insurance Company.

thank you for immediate reply.

Sir, presently i have floater mediclaim with bank of india -national insurance of 4lakh for 4years. The bank has snapped its tie from 31st october 2018.my renewal is on 21st may. Sir please suggest me where to port

Dear Santanu,

If you don’t have any issue with National Insurance, then why not port with the same company?

Hello Basu Sir..I m your’s Blogs Frequent Reader

I wanna take my First Health Insurance my requirment are below plz suggest me best Product

*Health insurance

?Claim settlement percentage above 90%

*Max ?cover primium low

*? cashless facilities

*Large network in New Mumbai

?*OPD counselting

? *alternative treatment except allopathic.. LIKE AYURVEDA

??*pre-existing diseases waiting period low

Dear Kapil,

You can choose the product from my above list.

Plus the issue is loss of one’s freedom of choice. There are few companies in your list, in which one can opt for any room without exception (eg- Apollo Munich Optima Restore) and others are with capping (eg – Royal Sundaram 1 % of sum insured).

Now, say I have a 10 Lakhs policy, I could easily avail the top most room available in hospital of most tier 2 and 3 cities and even few tier 1 cities with either no capping policies or with 1 % of sum insured which surmounts to 10,000 per day.

But in Religare, I cannot avail the top most room even if the room charges are 4-5k per day since the hospital might have a primitive room costing 1.5-2k per day and I am forced to opt for that. So don’t you think it goes against one’s freedom of choice?

P.S: I am not recommending or condemning any plans / company. Just to bring about the discussion on nuances of few plans.

Dear Sevan,

I am not saying that you are either for or against a particular product or company. But my point is that you might have asked for the definition mentioned in the policy.

Dear Mr. Sevan,

please let us know which one you have opted because i have few doubts about religare because i am also continuing from last 5 years.

thanks

Dear Indrajeet,

Sevan already cleared few of the issues Religare posing to HIM. You may refer his earlier comments or wait for his reply to your comment.

I have gone for Max Bupa Health Companion.

Surprised not to find it listed in top 5 in this article.

Basu Sir, your views on this product please..

Dear Sevan,

There is no such intention. Max Bupa was in my 6th place. However, in this post, I am highlighting only 5. Hence, not listed. There is no such negativity about MaxBupa.

Dear Sir,

I have discussed this room availability issue with religare area state sales manager because my policy is given by him and then he told me

1- We can take the single private AC Room in 5lkh care policy.

2- If single private ac room is not available then after getting the not availability certificate of that category room from hospital, you can upgrade the room as per sales manager.

3- Generally they provide 1% of policy cover for room and 2% for the ICU conditions for 5lk policy.

Bashu Sir, could you know us some OPD add on treatment Ryder policies or some normal dental treatment facility available plans with medical insurance. Because without hospitalization we pay much amount for normal problems in the year and that is not reimbursed.

Second thing, could you verify with your sources what i have got information from my adviser and i shared here, that is correct?

Thanks.

Just ask the sales manager to send you a mail regarding these clarifications.

Then you will realise the truth for yourself.

Religare, although a great product, has a great disadvantage for customers. The Plan entitles one to opt for a “Single private room” during hospitalisation. The definition of “single private room” is that the room is the most basic one available in the hospital.

So consider 2 scenarios,

1. the hospital has a basic Non-ac room. In this case, one has to opt for it and not the AC room even though he might have a huge insurance cover !!!. Most of the hospitals have both AC and Non AC rooms.

2. In case, the most basic room is not available in the hospital, you cannot upgrade to the next category of room! You have to pay the proportionate bill for upgrade and the only option available would be to downgrade and go to semi-private rooms. It is not uncommon these days that the basic rooms will be occupied with availability of only premium rooms in the hospital.

So if you are under this plan, you have to pray for 2 things if you need hospitalisation – hospital does not have Non-AC room and that the most basic room is not occupied. So basically it limits one’s freedom of choice.

Dear Sevan,

How you arrived at the conclusion that “Single Private Room” means not the AC but the BASIC one?

I had Religare Care insurance for myself and family few years back. Had to hospitalise my mother for a surgery. I opted for a room and when I spoke to them, they told me the definition of “single private room”. And for the information, it is also very well defined in the policy wordings. Only for sum insured worth 15 Lacs and above, is the single private room upgradable to next level.

Dear Sevan,

I think you might have asked for the definition. Because it is nowhere mentioned that AC rooms are not allowed. Telling orally is different than showing the proof.

“Single Private Room means an air conditioned room in a Hospital where a

single patient is accommodated and which has an attached toilet (lavatory and

bath). Such room type shall be the most basic and the most economical of all

accommodations available as a Single room in that Hospital.”

This is the extract from their policy wordings.

I am sorry. Until about 2016, the word AC was not there in their policy wordings. That was the time I ported my policy to some other company.

But rest all inconveniences stay.

1. It should be the most basic AC room.

2. If that room is unavailable, one cannot upgrade to available cheapest room unless he pays the proportionate differential.

How often can we find a hospital which has cheapest room unoccupied?

Dear Sevan,

One thing I want to say you. If you are insured does not mean you get 100% claim on all your 100% expenses. Because they are into the business not for social cause.

Sir, I beg to disagree.

We pay timely premiums during healthy days hoping that in case we need hospitalisation, the burden does not fall on us. The company are in business and not for social cause- I very well agree. But the company cannot include unnecessary clauses taking away our freedom. When I need to get admitted to hospital due to ill health, the last thing I will be looking into is the fares of different rooms in a hospital and praying cheapest is available.

In fact, financial blogs like yours must condemn these caveats so that better products are designed and available to customers.

I am sure there are so many of us who visit your site on daily basis and take your advices as gospel.

Dear Sevan,

That is the reason my first suggestion to all is that READ each wordings of whatever the product you buy. Never trust on an individual (whoever he may be) when it comes to money matters. But many times people’s negligence or blind trust will kill them one day.

Hello sir I wants to take pure health insurance policy I saw list but can u sujjest me as per market survay, it’s good and hassale free.please sujjest me.

Dear Tukaram,

Where is the market survey available?

Hello sir,

I have star health policy from last 3 yrs of 3 lac family floater for 3 member (37, 28,5) bonus already added 1lac in this policy. Should I change the company to in this 5 top company?

Dear Moydul,

Please continue the same.