Many of us buy LIC policies without knowing features and benefits. However, after few days we feel such LIC policies are irrelevant. Hence, we want to get rid of such policies. The solution is to surrender such LIC policies. How to Surrender LIC Policy after 3 years or before maturity?

What is the meaning of Surrender of Life Insurance Policy?

It is the option to exit from life insurance product before maturity wherein policyholder will get the amount which is called as Surrender Value. A regular premium policy will be eligible for surrendering after the policyholder has paid the premiums continuously for 3 years.

As I said, to be eligible for surrender the policy must complete 3 years. By surrendering LIC policy, you may not be in profit as they pay you some part of the total accumulated bonus and the premium you paid.

Implications after the Surrender LIC Policy

# You will loose the Life Insurance Protection available from the policy. As surrender of LIC policy is considered as the closure of the contract between you and insurance company.

# Tax Benefits availed under Sec.80C of IT Act will be reversed if the policy is terminated/cease to be in force within 2 years for traditional products and 5 years for ULIP products after the date of commencement of policy.

Refer the taxation of Life Insurance Policies at “Tax Benefits of Life Insurance“.

Types in the Surrender LIC Policy

There are two types of Surrenders. Let us discuss both the types.

1) Guaranteed Surrender Value

If your policy is eligible for this surrender value then it to be mentioned in the policy bond and is payable after the completion of 3 years. It is usually 30% of the premiums paid, excluding premium for the first year. It also excludes any additional premium paid for riders, taxes and any bonus that you may have received from the LIC.

However, the percentage of this Guaranteed Surrender Value will depend on the Policy Term and policy year in which the policy is surrendered.

Let us say your yearly premium is Rs.1 Lakh and you paid it for 4 years.

Total Premium Paid=Rs.4 lakh.

Premium excluding 1st year=Rs.3 lakh.

Then the Guaranteed Surrender Value will be 30% of the Premiums Paid (excluding 1st Year Premium). Hence, 30% of Rs.3,00,000 will be Rs.90,000 is what you get.

Remember, this Guaranteed Surrender Value will not add the already accrued bonus.

2) Special surrender value

It is calculated as below. But before that, you must understand one more term called Paid Up Value.

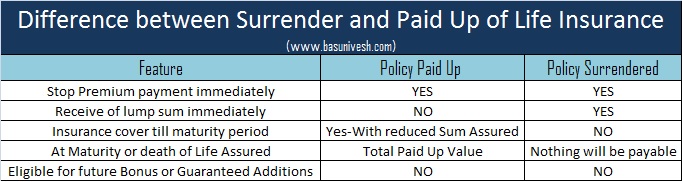

What is the meaning of Paid Up Value and Total Paid Up Value?

If premiums have been paid for at least three consecutive years and any subsequent premium has not been paid within the grace period, then such lapsed policies are called paid up policies. The sum assured is reduced to a proportionate sum assured which was available during the policy buying.

For example, if Sum Assured is Rs.5 lakh and the total number of premiums payable is 20 years and premium payable is yearly and let us say premiums are paid for 10 years. After that, you discontinue the policy.

Such discontinued policy is called paid up policy. This is calculated as below.

Paid Up Value=(No. of Premiums Paid/No. of Premiums Payable) * Sum Assured.

Paid Up Value=(10/20) * Rs.5 lakh=Rs.2,50,000.

So from the 11th year, the policy will continue with sum assured of Rs.2,50,000 only instead of original Rs.5,00,000. Along with this paid up sum assured the bonus already accrued up to the 10th year will be added. This is called Total Paid Up Value. Therefore Total Paid Up Value=Paid Up Value+Accrued Bonus.

If LIC declares any future bonus or guaranteed additions to the product, then your policy is not eligible for such future bonus or GA. You will receive only the Total Paid Up amount at maturity or death of policyholder.

Total Paid Up Value will be payable to you at maturity or your nominee (if your death occurs during the policy period).

What is the meaning of Special Surrender Value?

In simple terms, Special Surrender Value is the % of Total Paid-up Value and it is calculated as below.

Special Surrender Value=(Sum Assured * (No. of premiums paid/No. of premiums payable) + total bonus received)* surrender value factor.

In simple, Special Surrender Value=Total Paid Up Value*Surrender Value Factor.

This Surrender Value Factor changes based on the term of the policy and many other things. Usually, this value is zero for the first 3 years. Hence, for the particular year and for your policy, you have to check with LIC for this data.

What is the difference between Paid Up Value and Surrender Value?

I created below table for your understanding of the difference between the meanings of Paid Up Value and Surrender Value.

Hope you now understood the concept of Paid Up Value, Total Paid Up Value and Surrender Value.

How to Surrender LIC Policy?

First keep in mind that as of now Surrendering LIC policy is not possible ONLINE. Also, you have to surrender the LIC policy at your servicing LIC branch ONLY. Servicing branch may be the branch where you purchased the policy. Otherwise, if you changed the branch, then that particular LIC branch represent the servicing branch for you. The reason for this is, your all policy documents like proposal forms, loan details and all other details will be available at servicing branch only.

Also, keep in mind that you have to personally visit the branch and request for surrender of LIC policy.

Documents Required for Surrender LIC Policy

- Original Policy Bond

- Download LIC Policy Surrender Form No.5074. Take the printout and go with this form.

- Bank cancelled cheque leaf (your name should be printed on cheque) or bank passbook photocopy. Because now LIC issue the payment directly to beneficiary bank account. LIC stopped issuing cheques.

- Fill LIC’s NEFT Form, if you are not using the above said Surrender Form and submit the same.

- Go with original ID Proof like Aadhaar, Driving License or PAN Card. They verify and take the photocopy of the same and return the original one.

Once you submit the necessary documents, then within 5-10 days they transfer the fund to your bank account.

Dear sir,

I want to surrender my policy.i am paid every year premium Rs.75000 for 4 years.if close the policy how much I will get back.

Dear Raguram,

Contact the nearest LIC branch.

Hi Sir I ve taken 814 endowment plan 3 yrs back I didn’t know much about this policy and my policy maturity after 35 yrs and I will get 1cr but now its very difficult to continue premium of 60k p.a .What should I do now plz suggest best way to quit

Dear Wasef,

You don’t have any other option but to surrender or paid up. Visit the branch and ask for the values.

Sir, I took LIC Money Plus T No. 180 policy in 2007. Maturity date was March 2017. I paid annual 15000/- premium for subsequent 3 years till 2010. In 2010 the surrender value was calculated around 55000/- I did not opt for surrender then. Now I contacted LIC customer care, they told me this policy got “Foreclosed” so they can’t provide any SV details and I should contact the issuing branch. Kindly tell me how would the SV get calculated now ? How much money could I hope to get ? Where can I find details of such foreclosure ?

Dear Vivek,

As suggested by the contacted branch, better to visit the branch where you have purchased the policy.

Sir,

For surrender of policy, bank cancelled cheque/account should be the same from which premiums have been paid or another bank account of policy holder can be given for credit of surrender amount?

Dear Mansur,

Can you elaborate clearly?

Hi Sir,

I took jeevan labh for 4 lakhs for 16yrs. So far I paid 60k premium for 3 yrs. Now I would like to surrender my policy. Kindly advise the best way and how much I would get it

Dear Sandeep,

Better to opt for paid-up than surrender.

Dear Sir,

I had 15 years of LIC policy but I surrendered it after 10 years and I also got the lumsum amout of it. Now is this whole amount Taxable ? Do I need to declare the whole amount into ITR fill ?

Dear Vicky,

Refer my post “Tax Benefits of Life Insurance“.

Hi Sir , I have taken new Jeevan Anand policy in the year 2019 for the Sum assured of 10 L for 22 yrs.. Now I’ve paid 3 Yrs premium & want to discontinue this policy with paid up option.

Should I notify this to LIC or they will automatically convert into Paid up ?

Dear Babu,

You no need to intimate to LIC.

Sir, I have 7 policies of New Jeevan Anand and want to surrender it.

Premium period paid :- 5.5 years.

The surrender value is 22k to 17k of 7 policies with 25,26,27th year maturity and so on..

Premium per year paid is 36k

Accrued bonus is 24k in each policy.

Total surrender value of 7 policies will be more than 1 lakhs.

So, do I have to fill form 15g to avoid tax deduction and will I get part of accrued bonus ( call center says I won’t get any bonus)

Please help

Dear Poonam,

You will not get a full bonus as it is a surrender value.

I have a policy done for my kid and the premium each month was 2973 which I paid for 8 years, commencement of policy was from 11/2013 till 11/2028. I want to surrender the policy as of now and wanted to know how much will I get.

Dear Vijay,

Contact the branch.

Dear sir,

I have LIC New Jeevan Anand 815 Policy and details :

Sum Assured: 1000000

Monthly Premium : 6392 + GST (143.82) = 6,536

Paid until this month : 65 Months

Policy Start Date : Jan-2016

Policy End Date : Dec-2031

Maturity Date : Jan-2032

Total years : 16

Paid amount upto this month : Rs.415,480

If I surrender only I get 50% of the paid amount. What to do now? can I surrender or paid-up the policy? .Really confusing please guide me.

Thanks

Dear Raja,

Better to opt paid up.

Thank you sir

Dear sir,

I want to surrender my policy but my branch is too far .

Is there any option to surrender without visiting physically in branch.

Please Answer

Dear Shaifali,

Sadly NO.

Hi, I have LIC Jeevan Anand with a yearly premium of around Rs. 26000. When I started investing in Mutual Funds I realized that LIC was a mistake and now after 6 years of paying premiums I want to stop. What you suggest should I go Surrender or Paid Up?

Please advice.

Dear Harish,

Better to opt for paid up.

Hello sir, My jeevan saral 15 years LIC policy is not paid in last 4 years. I want to withdraw this policy. Please let me know how to proceed and what’s the amount I will be getting. The amount paid yearly was Rs 6,005.00 from 2011.

Thanks

Dear Smith,

Approach the branch.

Sir, I took an LIC Jeevan Anand policy (Plan 149) in Nov 2008. Sum assured is 5 Lakh /-. The year of last Premium payment is Nov 2026 and the policy Maturity Year is Nov 2077, till I get to 69 years. I have paid 12 premium instalments already and I need to pay the premium till 2026 (19 instalments). I haven’t taken any loan on the policy and I have made all prompt payments yearly. However, I see not much of a benefit in the policy other than the accident claim, what would be a more beneficial option for me – continue to pay the premiums till 2026 and then discontinue or surrender the policy or discontinue the policy forthwith after paying 12 premiums so far?? Also, should I go in for a Surrender value or Paid in value? Can you please let me know the appx amount I will get in both scenarios if the yearly Premium value was 29,500/-.

Dear CS,

Better to go for paid up.

Sir I want to break my policy.. What can 8 do

Dear Anuradha,

Approach the home branch.

Hello Sir – I have an accrued bonus of 1,00,000 rupees for my Jeevan Anand 149 policy that is currently in paid up status and not in force. If I surrender now, will I get part of the bonus amount or should I revive the policy and then surrender it.

Thank you

Dear Puneeth,

You will get part of the bonus. Whether to continue or surrender depends on YOU.

Hi , I took LIC Jeevan labh policy for sum assured as Rs 25 lakhs for 25 years. I wanted to stop the insurance after paying premium for 3 years and keep the money there for next 25 years. If I will withdraw money after 25 years, how much money I will get back.

Dear Vikram,

Without knowing the premium and other details, how can I know how much you get it? Also, it is hard for me to calculate for each individual.

Hello,

i want to know is it possible to close down the account .the plan is 333and policy status is In-Force.

but i have taken the loan

so what will be the procedure .

i creat account on 26-12-2018

and my instalment premium is (Rs32,950)

i took loan on January 2021.

it was Rs 70,000 .

i want to close down my account

so will i get refund or do i need to pay penalty .. how much will i get ??

thank you.

Dear Dipak,

You can close the policy. Be in touch with the home branch.

FOR PAST 3YEARS I PAID THE LIC (JEEVAN LABH PLAN). NOW I WANT TO SURRENDER MY POLICY. TILL DATE I PAID NEARLY 80000. HOW MUCH AMT WILL RETURN TO ME. ITS LIC GIVES ANY BONUS FOR THIS PAID AMT.

Dear Arimanikandan,

Approach the concerned branch of LIC.

Sir

I have payed the premium for 5 years

How much amount can I get now if I surrunder the policy

Half Yearly Premium is 4000 rs

Dear Nitin,

Approach the branch for the same.

Sir

I have payed the premium for 10 years

How much amount can I get now if I surrunder the policy

Monthly premium is 1021

Dear Mohammed,

Take the pain of reading the above post properly or visit the concerned branch.

Sir my HDFC Ergo term policy amount 80k every year for till 15 years. Just my 3 years policy completed (80k×3÷240k). So please tell me if today I’m withdraw my policy amount. How much amount will receive??

Dear Rohit,

Please verify what type of policy you are having. HDFC ERGO will not offer you Life Insurance products and secondly in case of Term Life Insurance, usually there is no survival benefits.

I wish to surrender my LIC term policy Amulya Jeevan 190 that had commenced in 2012. Will I get any returns on the premium paid till date on this policy.

Dear Seema,

It is term life insurance of LIC. Hence, to discontinue the policy, you just have to stop the premium payment. There is no maturity or surrender values in this product. Hence, you will not get any returns.

Dear Sir

Hats off to ur patients for answering the same Questions of lazy readers. Big Fan. !!

Dear Sami,

My pleasure 🙂

I have a LIC jeevan anand policy. I have paid premium from 2011 to 2020. If I surrender now, how much percentage will I get back the amount.

Dear Abu,

Approach the branch.

Dear Basavraj,

For all questions if you answer as “Contact the nearest branch” what is the use of this portal ???

Dear Anonymous,

I am not a branch where I have an access to your data and resolve your questions. If one not use such commonsense, then what can you expect from me?

Sir I want to withdraw my policy. Just I paid half year premium Stil it’s not completed year tell me tat shal I quit I don’t like to continue this policy

Dear Ramya,

If you close the policy now, then you will not get the money as I said above, you have to pay for at least 3 years.

Hi, Anybody can help me out with information that I have premium tenure for 10 years with Aditya Birla .. I have completed the 5 years of premium.. now will it be paid up or surrender value? And if I want to withdraw.. will there be any deductions or penalty from Aditya Birla.. will I get the whole amount (the amount showing as current value) at the time of withdraw ? Thanks

Dear Jitender,

Take the pain to read the above post again.

I am paying LIC premium from SEP 2017 to SEP 2020 for LIC money back plan . Now I want to preclude the policy. How much amount will I get if I surrender my policy?

Dear Suguna,

Please approach the nearest branch.

Hi Sir,

I am not happy with the LIC and hence wanted to surrender all the policies. Is it necessary to perform the procedure at the servicing branch only? Can’t we do this at any LIC branch?

Also, what is the procedure to change the servicing branch then? Since in the current situation, I can’t visit the servicing branch. Requesting you to please suggest the alternative for this.

Dear Chinmay,

You have to visit the home branch.

Hi There,

I’ve bought a LIC policy in Gorakhpur but for 9 years I’ve shifted to Delhi and now I need to surrender my LIC Policy. So it can be done from any LIC center or I’ve to approach the center from where policy is made.

Dear Karan,

You have to approach the home branch (Gorakhpur) or first transfer the policy dockets to Delhi, then can surrender from Delhi.

So, this can be done online or should I visit the nearest branch and ask them to transfer the policy to the Delhi branch and the last thing do I need to get the confirmation from the Gorakhpur branch regarding the same.

Dear Karan,

Transfer can be done by sending a letter to the home branch.

Hi Sir, thank you for this detailed explanation. However, I have a question:

I have a LIC Jeevan Anand Policy and have been paying all premiums (53,000 *2) from April 2014 to Oct 2020. This was a Half Yearly setup.

I am now planning to buy a house now and was considering using this as a Downpayment after withdrawing it.

Will the surrender value, in this case, make more sense, or taking a loan from LIC against it?

Somehow taking a loan from them for my own money doesn’t make clear sense, but I am open to your advice.

Dear Baptist,

If you surrender now, then I think you will get less than what you paid. Hence, if it is ok for you, then go ahead.

I have an policy, due every December. Can I pay my third year’s premium earlier, say in August of that year and surrender my policy after third installment?

Dear Eshwar,

You can do so but if surrender is the decision, then check at first what may be the surrender value if you pay the last year premium. Based on that you can take a call.

Hello sir I have LIC Jeevan Anand policy I had taken a loan on it but due to some financial problems I’m able to pay nor premium neither interest & both are getting accumulated. Now My policy is showing reduced paid up . If I wait till policy completion is my interest will also get increased. And I have to give a lot for interest or is it better to surrender it

Dear Samta,

Yes, obviously interest will accumulate.

Hi sir.

My husband has surrendered my ,his and my sons policy.

My bank account is not there.can we get the surrendered amount in my husbands bank account

Dear Gagan,

I don’t think so. Better you update your bank details with the LIC.

Nice article.. may i know one thing. The policy is in my wife’s name. If i want to surrender that can i go alone and get it done with her signature in the form? Or her physical presence is required at the concerned live office?

Dear Dinesh,

Better you go with your wife.

Sir I have a LIC jeevan Anand plan since 2012 now I want to surrender the same but I do not have the original bond it was misplaced while shifting my house so how can I surrender without bond.

Please help advice

Dear Nandini,

Yes, at first you have to apply for a duplicate bond and then you can surrender.

I took a policy in year 2000 and have paid all the premiums for 15 years. It shows a maturity date of 2025.

Since I have paid all premiums how much will I get it I close the policy now?

Dear VJ,

Contact the branch.

Hi Sir,

I have take Jeevan Anand 149 policy in 2012, December. If I surrender, shall I get at least what I paid till now? My agent is not giving any information. Please guide me on this. I have seen in internet that I dont even get what I paid till now if I surrender.

Thanks.

Dear Rana,

I hope so. Better you visit the branch for the exact values.

Dear sir,

First of all, I have not understood properly the guaranteed surrender type LIC surrender policy scheme as you explained above. By the way I have a Jeevan Labh Policy which have 12000 Monthly premium. and on March 2021 three years will complete. please tell if I surrender this policy on April 2021 How much amount will I get? Please say me in Rs. Value. No gape till now in premium payment.

Dear Bhagyesh,

Your policy is eligible once you complete 3 years, regarding the surrender value, better you approach the nearest branch.

Dear

I have taken one lic jivan saral policy on 2013 which annually amount was 36360.Last seven years I was regularly payment of policy amount but due carona i am job less and no money to continue this policy, so that want to stop and surrender the amount. Please suggest me after surrender the amount how much money will I get by lic

Dear Pravej,

Approach the nearest LIC branch.

Dear

I have paid till now on my policy 2.5 lac and after surrender can i get 2 lac or not

Dear Pravej,

It is hard for calculate for each individual. Take the pain and approach the nearest LIC Branch.

I HAVE 2 JIVAN SARAL POLICY POLICY TAKEN 11.01.2011 PREMIUM 12010 & 6005

10TH YEAR COMPLETE NOW I WANT TO SURRENDER POLICY

PLEASE SUGGEST WHAT IS AMOUNT RECEIVED ME

Dear Lokesh,

Approach the branch for the same.

Hi,

I have two lic policy from last 10 years which I want to surrender. My lic home branch is faraway from my current inlaws resisdence. Also I am pregnant and could not travel. So if ill send the documents along with my husband or sister then will the branch accept it? Or I have to go?

Hello sir,

In 2002 my mom taken a lic policy and she continued to pay the amount since 2006. After that, she didn’t perceive..my last my mom died. My father is a nominee and the maturity date is 2022. Shall we get any amount before maturity or else we have to wait until 2022?..if my father wants to get the money then what are the procedures? Can you explain sir

Dear Anitha,

You can adopt either of the approaches a) break the FD now or b) Let it be continued up to 2022.

This blog is useful. Regarding surrendering the LIC policy, the rules are framed in such a way that there is no way out once trapped . If one surrenders then huge loss. Better to either make it paid-up or pay till maturity to remind your own mistake committed for the loved ones. LIC should change with technology at least and be more empathetic towards investors.

Dear Biswas,

But they never change it 🙂

Hi Basavaraj,

I have taken a LIC policy in 2015 and have been continuously paying an annual premium of 27000 till date(2020). Now I don’t want to continue the LIC Policy any more and want to stop my LIC and surrender the same.

How much amount will I get if I surrender? Do the accumulated bonus during this 5 years will be provided to me by LIC.

Dear Bishwadeep,

Approach the branch for the value.

Hi

I had made 2 policies for 1 year in 2015 and did not continue the payment . Will I Be eligible to withdraw the money.

Dear Mohammed,

Take the pain to read the above post again.

Can I visit any lic branch or only my home branch to surrender lic policy please help

Dear Bharat,

You have to visit the home branch.

Hi, Thanks for your detail explanation about surrendering LIC. I a trying to surrender my LIC from last 5 years but my LIC agent is not supportive and make excuse every time. May I know how to surrender if your condition as followed:

1) You are not citizen of Indian from last 1 year.

2) You do not have any bank account in India now.

3) Your PAN, Aadhar, are invlaid and on;y driving lic is valid.

4) What is I want to gift my LIC to relatives.

Thanks if you read my msg and help me out as I lost my all hope on this LIC and regretted a lot.

Dear Pandya,

If you don’t have a bank account, PAN, Aadhaar or any KYC document, then how can they transfer the money to you? Please approach the concerned LIC branch directly.

Hi, thanks again for your reply. Well, I used to have my Pan, Aadhar, and bank account 1 year back and I tried a lot with my LIC agent to surrender my LIC but he always made excuses, I also tried contact LIC office and they also kept asking me to contact the agent. Well, now I am not citizen and my soul is still stuck on my LIC hard earn money. Anyways, I lost my hopes and want to advice all people here do not waste your money on this LIC as they are not worth trusting. for good example. 1990 RS was having good value you invested in LIC hoping to get 25 lakhs in 2030 but unfortunately when you reached in 2030 that 25 lakhs is nothing. So, use your money wisely and invest in something else but not in LIC> My hard earn knowledge.

Dear Pandya,

To surrender the Policy, AGENT is not required. If the branch is insisting for the same, then they are misguiding you. Regarding your views about products, NONE do this commonsense research before buying.

Hi Sir,

I have a LIC Policy of sum assured value 10lac and time period of 35 years and it has been started in Aug 2017 and it’s been more than 3 years I have paid the premiums regularly but I want to discontinue the LIC policy.

LIC New Jeevan Anand

What amount I’ll be getting after discontinuation and is it beneficial if I discontinue it.

Please help me as I’m not willing to go continue it

Dear Shashank,

Check with the branch.

Hi Sir,

I have 2 policies and paid for 2 years 20000 each policy. Can i transfer 1 policy paid premium amount into other policy without loosing any amount from the second policy before surrendering duration? So that i can pay from next year onwards for one policy 20000/-.

Dear Sekhar,

Sadly you can’t transfer that way.

Thank you sir for the reply.

I am holding a Bharti AXALife Elite Advantage Plan .(28 apr 2018) Maturity 30 apr 2030 .For sum reasons I want to discontnue this policy .What should I do and how much I will be paid.

Dear Vikas,

I think it is a traditional plan. So you are eligible for surrender once you complete 3 years of premium. For better understanding, be in touch with the concerned Insurance Company.

A 14-35 endowment policy was taken by me on the life of my daughter in 2000 for a sum assured of 6 lac. The policy is in force. My daughter now is a citizen of UK. Should she surrender the policy or can she continue. Kindly advise

Dear Moses,

It is hard for me to say so. If she feel the 4% to 5% returns are great, then continue. Else better to surrender.

sir,

Isn’t that possible to surrender the policies online as private companies are giving option to surrender the polices online via service mail id ?

Dear Gautam,

Sadly NO.

I purchased lic policy 2 months back, i want to cancel it now. Will i get my money back which I paid in the form of 2 premiums?

Dear Pallav,

Sadly NO.

Hi

I have a policy starting from 2016., due to mature in 2032.

But under very low financial conditions I am surrendering the Policy.

2 things I have found to Hate is

1. They are asking to submit, a Paper of tissue quality with delicately printed, called Policy Bond mailed to me in 2016., which got erased off by itself and almost rotten. I don’t know how this people are still living in medieval times. I think they do all this on purpose so that no one should be able to get there amount back.

2. They are giving me only about 70% not the full amount I’ve paid till now.

I believe I made a right decision to get out of this entity.

Kindly be careful and buy a locker first to keep your Policy safely first… Hahaha..

Regards

Dear Mohammed,

1) It is not like that. It is a standard procedure. If you have such a policy that is completely rotten, then you can apply for a new duplicate policy document and then can submit.

2) It is based on the surrender value.

Hi

I appreciate and thank you for your reply.

Also I will apologise for making fun of the system.

But, don’t you think that LIC is an entity that is a world in itself.

In the era where Tea, Banana and Vegetable vendor are going on Online payment., how come they are not going to Online banking or transactions?

Dear Mohammed,

I understand your anguish and especially during such situation, they have to develop a system to cater to their customers. But the sad part is that they are still living in the era of 1942.

Hello sir,,

I am having 2 lic policies, 1.jeevan anand and 2.jeevan saral… I paid 8 years premium for jeevan anand and 6 years premium for jeevan saral… Now I would like to surrender these both policies… Are they eligible for surrendering… What is the return expected?? Only paid premiums or with bonus also?? Please clarify

Dear Chiranjeevi,

Yes, they are eligible for surrender. Regarding the values, contact the branch.

I opened a policy for 30 year. now I closed my policy but lic not give me a payment … I have 12 year payment slip and all documents was surrender for closing the policy., lic not gave me a payment … I don’t believe on lic

Dear Sagar,

It is impossible to happen. May I know the policy name?

Hi Sir,

I have a policy for INR 500000 under Jeevan Anand 149 75 scheme. Out of the 20 yearly premiums of INR 26701 each, I have paid 10 of them. I would like to withdraw the the policy now. Could you please tell me how much can I expect from the same?

Dear Sam,

Hard to say. Please visit the branch for the same.

Hi sir, i have jeevan surabhi 107 sum assured 6 lac. Paid premium for 8 yrs got 02 money back of 1.5lac each. I want to surrender the policy. Will the 3 lac given to me recovered or that is not considered. 30% of premium – 1st year comes to be 1 lac only. Please clarify.

Dear Ramprabu,

It will not be considered.

Sir,

Myself Imtiaz Ahmed, I have New Jeevan Anand (with profits) policy… premium paid 4 years…. policy duration 21 years…. premium 5542 monthly… I want to surrender the policy and investing some SIP or PPF or Stock Market…. Is it beneficial or fully mature the policy ?

Dear Imtiaz,

Hard to say BLINDLY without knowing much of your financial life.

I have Bought jeevan anand 815 with monthly premium of 18660.now i am unavle to pay my policy.mis its possible to close this policy and can i get any money return back??please suggest

Dear Subramanian,

Yes possible if you completed 3 years of premium payment.

Hi I have 2 Jeevan labh policies for myself and spouse. Both policies term completed 3 years and I want to surrender the same. Can I alone go with all documents and submit it. Wife cannot travel due to small baby and not safe to travel.

Dear Hemant,

Yes, you can do so.

Sir my lic policy premium not paid by me last 5years how can I surrender my policy

Dear Pravin,

Check at first whether your policy is eligible for surrender or not.

Is Neft form mandatory even if I’m providing cancelled cheque?

Dear Rohit,

Yes.

I have 2 policies opened in 2007 and I paid premium till 2015 but after that due to some family issues I couldn’t pay premiums further. I just want to ask that can I surrender the both policies.

Dear Yogesh,

Yes, you can surrender.

Hi Sir,

I have started Jeevan Labh Policy on 30th july 2020 can I surrender it immediately.?

Will I het the 2 premium what ever I paid.

Dear Shri,

You can’t surrender now.

Hello sir i have 5 policies 3 is mine and 2 of them are my son .

All the poclicy start 2011 and paid till 2020 .

If i surrender all policy ,will i get my invest money . ?

Dear Sunil,

As per me, yes.

Hello Sir,

I have LIC Jeevan Anand Policy which I purchased in Jan 2012. It has a premium paying term of 21 and maturity of 67. The premium per month is 13,140 and sum assured of 25Lakhs. I checked the site and it says accursed bonus as something around 9Lakhs. Including July’s premium, till date I have paid 13.5Lakhs. My question is what will I get if I surrender it today? is it advisable to surrender?

Best Regards,

Mohammed

Dear Mohammed,

Approach the LIC branch to know the exact values of surrender.

Sir I have Jeevan Anand 149 started at 2012, sum assured is 5 lakhs. CAn I surrender this now

Dear Deepak,

Yes.

Hello Sir,

I just got to know that my dad opted for a lic market plus 1 plan 10 years back as he started receiving messages to choose annuity option . The investment has now matured. I searched online and I found that I can withdraw a maximum of 1/3rd of the fund amount and the rest has to be received as annuity. Is there an option to surrender the policy now to get back the entire amount? My dad doesn’t really need an annuity payment as such.

Dear Ragnu,

You can opt for surrender.

have Bought jeevan anand_ 2322 with monthly premium. now premium paid 9 months .but i am unavle to pay my policy.possible to close this policy.how to do get money back waiting for your positive response

Dear Ankit,

Sadly you can’t.

hi ,

i have lic policy of 4 lakh name jeevan aanand .which is going to mature on 2026 . what if i ll pay next 5 years amount at present and can recive matureity amont now. is dis possible

Dear Rohan,

Sadly you can’t do so.

Hello Sir,

I have few insurance policies and dont know the details regarding the same.

It was started by my father and he sadly passed away.

How can i get information on these policies. I dont know how it works for LIC in Mumbai as i live in canada.

Help will be greatly appreciated

Dear Arbaaz,

Better you be in touch with an agent or branch and try to find through your name. It is hard but you have to start.

Hi Sir… Thank you for the detailed information, especially the part explaining that we get the sum of accrued bonus (of course, new accruals will not happen once premium payment stops) and paid up value at maturity if we decide to stop paying premiums after 3 years.

We have a policy in the LIC Endowment Plan 814 . Sum Assured is Rs. 2 Lakhs, Start date Mar 2014, term is 16 years, current age is 31. Premium is Rs. 3262 quarterly.

We want to stop this policy and go for mutual fund investments (preferably Multicap funds as have ongoing SIPs in them). We also have dedicated health insurance and Term insurance policies. So we feel this policy is not adding any value to us.

We recently inquired the LIC agent on this and he gave us this info. Surrender Value Rs. 55,262, Paidup Value Rs. 75,000, Accrued Bonus Rs. 43,000.

We are unable to decide if we should go for surrender option (we get 55.2K now and we can invest this in MFs) or paid up option (we get 75K+43K in 2030). Kindly suggest us which option is better.

Dear Jaya,

If you leave the policy for 10 years, then it will fetch around 3% returns (From Rs.55,262 to Rs.75,000 at maturity). Hence, better to surrender now and invest. Even if you put the money in 10 years Bank FDs, it will generate more return after 10 years than Rs.75,000.

Hi, I have recently taken a limited endowment policy for yearly premium of 60,191 for a period of 9 years, with sum assured 600,000 in 12th year. I recently got to know that if the premium paid annually is more than 10% of sum assured, then the whole proceeds are taxable. Is this the case?If it so, will the tax slab be 30%, as per my current income tax slab? Also, is it possible to change the policy so that it falls within the 10% bucket, it is marginally higher? Would you suggest surrendering the scheme, now that my investment view on this product changed? Appreciate if you could respond soon, as the decision is time sensitive

Dear Naveena,

Yes, it is true. You can’t alter the policy now.

Hello,

I hold a jeevan anand policy with sum assured 2500000 with policy purchased at 2013 and yearly premium of 50,612.

The last premium is in year 2052.

I want to surrender/pre-mature my policy due to some financial crisis.

Can you please help me how can i do it. and also how much will be the surrender value i will recieve (approximate will do)

Dear Yadnesh,

Approach the branch for the same.

Dear sir

I have a jeevan saral plan 165 policy paying 15300 quarterly . I completed 7 years and planning to surrender the policy .How much money will I get. Will I get atleast the money paid in 7 years ? Can you please help.

Dear Sippy,

Better to complete 10 years and then surrender.

Hi Sir,

I had purchased two LIC policy(1. Jeevan Anand & 2. Jeevan Saral) on 2012 and i have paid 8 yearly premium of 4,00,000(25K * 2 Policy * 8 years).

I already owning Term Insurance for 50 Lakhs. I feeling now that these policy giving lower return (like 4 to 5 %).

I am having housing loan for 15 Lakhs.

Could you please help me resolve below two queries.

1. Is it right decision to surrender these policy and do partial payment in Housing Loan?

2. I had taken these two policy in Vellore distinct in TamilNadu whereas i am staying in Chennai now. Is it possible i can surrender these policy in Chennai itself.

Kindly help me on this

Dear Kannan,

1) Hard to say without knowing your financial details.

2) Sadly NO.

Dear Sir,

I have a Jeevan Anand policy and have been paying premium for the last 15 years and the next year is the last premium payment. However the maturity of the policy is in 2082. If I withdraw the policy after the full premium payment, would I be getting the full amount I paid? I don’t want to wait till end of the maturity period. Could you please advice me on what would be the best thing to do at this point?

Dear Divya,

Your policy is maturing in 2022 (if we consider your last premium is in 2021). After that LIC will pay you the sum assured and accrued bonus. However, the risk sum assured will continue throughout your life (2082).

Sir I have purchase lic policy in 9/2013 and now I want to surrender my policy ,can I surrender my policy online and what is the process of surrender policy

Dear Kashi,

Sadly NO. You have to visit the home branch for surrender.

After reading all the previous users Comments I got to know one thing that if someone wants to know as to how much money we will be getting after surrendering the policy then we will definitely get no reply other than “Please visit the LIC branch” advice. So i request people not to ask this question again.

Dear Jai,

Yes, because I don’t have your database like how LIC Branch will have 🙂

Hi sir,

My name is Sunita Negi. I purchased jeevan saral 165 policy in 2010, after paying premium for 7 years, I stopped paying the premiums. Policy details are as follows:

Policy term – 15 years

Total premium payable- 30

Total premium paid – 14

Premium amount – Rs. 29112/-

Policy years completed- 10 years

Now I want to surrender the policy. Please tell me approximately what amount will I get as a surrender value.

Regards,

Sunita Negi

Dear Sunita,

It is hard for me to guide like this. Better to approach the home branch for the same.

sir kuch issues hai kya jeevan saral policy me ise revival karna chaiye ki nahi please suggest.

Dear Anju,

Complete 10 years and surrender.

Hello Sir, I have purchased LIC child future plan on my daughter name in 2007 from there I am paying premiums regulalry yesterday I saw my policy bond throughly in that bond premium amount is Rs 15703 and PWB amount is Rs 94.25, but while making payiment LIC taking only Rs 15703 not taking PWB amount Rs 94.25, from 2007 this is happening, kindly explaim me what will happens with my policy

Dear Santosh,

Not sure what is an issue. Better to approach the nearest LIC Branch for the same.

Sir I have purchased 3 policies of single premium money back policy in 2016 Sept 1 lakh pr policy for 20 yrs time. I want to break this. How is this possible pls tell

Dear Ronny,

Approach the home branch for surrender.

Hello sir

I obtained lic by 2011 and now we leave this address and also I lost my bond . How can i get money back. Indemnity bond help me

Hi sir

My both policy 6 yrs old I paid premium regularly

My policy table no is 165 Jevan Saral my policy premium per month 2042/-

Now I want to be a surrender this policy

How much I get money back after surrendering this policy

Dear Vijay,

Approach LIC Branch.

Dear Akbar,

I have a policy which i started on 2002 April. My last premium is coming april 2020. The premium amount should be 1900/per year. after my last premium how can i withdraw my money and what is the amount i can get approx. Thanks.

1. what is procedures of withdraw money from LIC?

2. Howmuch the apprpx amount can i get?

Dear Sakthi,

1) Approach the branch.

2) Approach the nearest branch.

Dear sir,

I have 2 polycies under my niece & nephew names, the policy if for 21 years premium to be paid every 6 months each, I have paid 2.5 years premium for each policy and now I found that the policy is not what I was looking for.. can I surrender the policy..? And will I get returns what I had paid ..? Please reply.

Dear Akbar,

Please read the above post properly.

Thanks for the reaponse sir, I understood that premium to be paid for 3 years In order to surrender the policy.. I am already to pay the dues but when I visit to the branch office they said after I paid all the dues which will be 3.5 years of premium I can surrender the policy but in return I will get nothing, my 3.5 years paid amount will more then 2 lakh and i willnothing in return after surrendering the policy..? Please help..

Thank you.

Dear Akbar,

Sad part is that even after paying 3 years, if you try to surrender, then the return will be less than what you paid. It is a trap.

Dear sir thanks once again,

Less means how many percent I can get in return.? And what you suggest me in this my situation..? I wanna contact you directly can you send me your contact details to my email ID [email protected]

Thanks

Dear Akbar,

Regarding values, you contact the branch directly.

Hello,

If I surrender policy, can I get already accured bonus

Dear Karthi,

Not fully.

Hello sir if i am not paying 2 months perimum of lic now i dont to continue for personnel reason so it is necessary to pay that 2 months perimum for can i surrender the policy please help me

Dear Saiprasad,

Please read the above post to understand the policies which are eligible for surrender.

Dear Sir

I have submitted my document for surrender of lic .It has been passed 8 days but no any message on my mobile for the process or to be credit of amount.bHow long it will take time to get my mone please let me know!!

Dear Mohammad,

Approach the home branch.

Can I transfer my LIC policies to my home town .can I visit to nereast LIC office to transfer home town

Dear Saikhom,

Yes, you can transfer so but request should be given to the home branch ONLY.

can i Surrender the LICs After 6 years COMPLITE

Dear Mohit,

Yes.

I want to surrender policy bima gold 179

I have completed 12 years

My plan is of 20 years

My premium is 16547 rupee

I am confused to continue this policy

What if I surrender did I get loyalty and amount?

Dear Mohsin,

Yes but partly.

Dear sir I have a pic policy of952 rupees for month.i have given 6 year now I want tosurrender my policy ,can I get my total primium that I have given

Dear Mantu,

Hard to say and hence better to visit the home branch for the same.

Hi

I’m 35 years old and hold LIC’s Jeevan Anand (149) Policy taken in 2010 by my father for me. It’s for 21 years’ premium paying term. Policy term is 74 years. I pay an annual premium of ?123669. I’m really confused as what I’m going to get on maturity of this policy. I get different answers from different people. Also, I get a feeling that this is not a good policy from the perspective of investment. Will it be wise to surrender it now. Request your expert opinion.

Thanks

Dear Sarvesh,

Your returns will not be more than 6%.

Thanks for the reply.

I have already paid 9 years. Now I think it’s time to stop doing mistakes further. Do they give the bonus accrued so far, if I surrender now?

Regards

Dear Sarvesh,

Yes, but partly.

Dear sir it’s me lohith

I had taken a loan in lic using my bond if 18000

Now I need to surrender that is that possible

Weather it’s possible my lic bond premium paid is 3.6 years

Dear Lohith,

Yes, you can.

Hello Sir,

Very informative article and very nicely explained in detail.

I’ve questions regarding cancelling / surrender of my policies.

I’ve 12 Jeevan Saral policies, I’ve been paying against it since 2011. So far I’ve paid around Rs. 5,40,000/- till last year.

While opening these policies, I had specifically asked my agent to open 1 or 2 policies with the specific yearly amount. It was for income tax and investment perspective, I thought that time.

But the LIC agent broke that yearly amount in multiple premiums for him to get the benefit of it. I ignored that part and have been blindly paying the premium since then without fail. Recently I was reviewing the policies in detail. I created my login on LIC portal to review all. I realized that he has setup different maturity dates for all 12 policies with a difference of an year or 2 in between. Starting from 2032 onward.

Considering all this mess created by the agent and my ignorance I do not want to continue with these policies anymore. My question as below –

– Can I withdraw all the amount I’ve paid against these policies by cancelling or surrendering it ? Is there any way for that.

– If I do not pay going further will that lapse the policy and would there be any penalty against it?

– Is there any way I can complain about the agent in LIC to cancel his agent code? Because I recently I got know, few more people have been victimized by this agent’s approach of breaking the lump sum amount in small premiums to achieve his policy targets.

– How come the sum assured is less than the amount of premium for some of the policies? Is that compensated by the bonus ? Is the bonus / guaranteed addition for any policy declared at the beginning of it or later?

Dear Kedar,

It is better to surrender now. Sadly you can’t complain against LIC for your IGNORANCE.

Thanks for the reply sir. But my questions are :

– by surrendering those policies, would I get all the amount I’ve invested or will there be any deductions ? If any deductions then do you know the deductions percentage / calculations ?

– in case LIC does not allow me to surrender the policies and if I do not pay any more premiums, will there be any penalty levied against non-payment ? And would I be still eligible for all the default benefits in case I do not make any more premium payments ?

– How come the sum assured is less than the amount of premium for some of the policies? Is that compensated by the bonus ? Is the bonus / guaranteed addition for any policy declared at the beginning of it or later?

Dear Kedar,

-It depends on your policy details. Hence, better to approach the branch.

-They have no rights to stop you from surrendering.

-Many are under such myth. Sum Assured the amount you get in case of death or at maturity. It varies based on many factors.

Hello sir. Thanks for the article. I have few LIC policies running from last 20 years. I changed my name last year (added a middle name), but this has not been updated in the policies yet. Will it be a problem at the time of maturity? If yes, what should I do? Please suggest. Thanks.

Dear Gautham,

Better you visit the branch and update it.

Dear Sir. Last year in April 2019 i have taken Jeevan Tharun policy , I want to change to Jeevan Labh. I am ready to pay extra premium . His it possible

Dear Thippeswamy,

Sadly you can’t change the policies like this. You have to cancel the existing one and you can buy new one.

can i Surrender the LICs jeevan labh before 3 years

thanks

Dear Ketan,

NO.

hi i have Jeevan saral and jeevan ankur premium paying since 2012 and jeevan anand premium paying from 2006 , if i surrender this policies what we will get .

Dear Satish,

Contact the concerned home branch.

Hi, Thanks for the column

I have taken LIC Health Plus in 2009 for yearly premium of Rs 6,000/- for insured amount of Rs 2,00,000/- This is upto age 65 years

I don’t want to continue LIC Health Plus, since i have taken better private ones.

I want to ‘Surrender This’ policy. Will i get any amount in return.

Thanks

Dear Karthik,

Yes.

sir please inform to me have any way of cancellation of lic policy through online

Dear Anjesh,

You can download the receipt by creating a login to LIC website.

sir, please send the link

They were said to continue but i am not interested because per monthly 6,686 rupees.

Dear Anjesh,

Please google it.

how much i will get if i pay only the first 3 year premium and let the policy mature for 20 years?

Dear Kirip,

It depends on the product.

it is jeevan labh

Basu Sir,

I need your help in evaluating whether to surrender or paid up my endowment whole life policy.

Insurer: SBI Life

Product: Shubh Nivesh whole life

Age : 31 yrs (now)

Sum Insured: Rs 57 Lakhs

Annual Premium: Rs. 3.27 Lakhs

Premium frequency: half yearly

Policy term: 20 yrs

Maturity benefit: Sum insured + simple revisionary bonus+terminal bonus

Other benefit: sum insured covered till 100 yrs after the maturity pay out

Premium paid so far: Rs 18.15 Lakhs (in 5.5 years or paid 11 half yearly)

Bonus accrued so far: Rs 9.975 Lakhs (6 annual bonus participated as policy start date is 25May2014)

My queries are below,

a) what would be the approx Surrender value if I need to surrender now?

b) what would be the ‘total paid up value’ if I need to stop paying premium further?

c) which option (a) or (b) is more sense considering the tax implications of 10(10D)- TDS?

d) Does it worth to continue for next 4.5 yrs and then let the policy paid up to save tax implications on 10(10D) TDS- in any annual premium it should not be higher than 10 times annual premium as sum insured. Is it a good strategy to continue the policy till 10 yrs and leave the policy paid up?

I ve enlightened not to get mixed up with insurance and investment, especially with something like endowment plans. Rather I would divert this into MF investment to generate my retirement corpus (goal).

Dear Bhavesh,

a) Contact the SBI Life for the values.

b) Contact the SBI Life for the values.

c) Surrender.

d) If you are OK to commit the same mistake again and again, then better to continue.

These are a dangerous product. Closing, investing the same in PPF may give you better returns than committing the same mistake.

I HAVE TAKEN LIC 820 POLICY,SUM ASSURED 30000/-IF NOW I WILL SURRENDER HOW MUCH I WILL GET IT?

Dear Kaston,

Contact the concerned LIC branch.

Why everyone is giving example of 4 years when we are planning to surrender after 3 years

Dear Skiran,

No idea. But yes, we can surrender after 3 years.

Hlw Sir…mene ek policy li thi or usme 50000 rs diye h 2 baar me…….2016 me.to vo wapis ho skte h kya

Dear Sheetal,

Hard to say without knowing the policy details.

So niw my question is about my 5 lic policies ,

1 is complete 27 years

2 is complete 35 years

3 is complete 20 years

4 is of my son is complete 18 years

5 also of my son is complete 20 years …and all policies i paid 10 years . So also i can rocver my invest money.?

Dear Sunil,

If you completed 10 years, then the best option is to convert those into Paid Up.

Dear Basvaraj,

I have a Jeevan Anand (Plan-149) that I had bought in Jan 2012 for a sum assured of 5 Lakhs for a period of 21 years (2012 – 32) with an annual premium of 25,764.

I want to surrender the policy now – my premium paid so far is 1,89,000 and vested bonus is 1,72,000. When I checked on the surrender value through customer care, I am told that it will be 1,39,000 and no bonus amount will be given, whereas clause 7 on the bond for Guaranteed Surrender Value reads, “The cash value of any existing vested bonus will also be allowed.”

I feel I am looted, even after 7 years, there is no single rupee benefit, instead still getting amount that is less than what I have been paying.

Please advise, if there is any possibility of getting anything above what is being told.

Indeed a worst investment ever…

Dear Hassan,

This is the reality and you have no option but to accept.

Raise grievance online on LIC portal, they are making us fool but you can raise your voice by raising grievance.

Hope it will help. you can contact me@[email protected] if more info required.

Sir, I am LIC’s Jeevan Saral policy holder. Date Of Commencement of Policy is Jun 2009 @ Rs. 3675 quarterly for 20 yrs term. My age was 24 yrs when i purchased the policy. Now i am planning to surrender it on Jul 2019 i.e, just immediately after completing 10 yrs. So how much do i expect to get back…???

Dear Rupesh,

Please contact the home branch for the same.

Hello Basavaraj Sir,

I have a New Jeevan Anand (With profits) policy. Now I want to surrender it.

Basic sum assured is 5 Lakhs & accidental benefit sum assured is 5 lakhs.

I have paid the premiums for 3 years without fail. Policy duration is from 2016 to 2036.

I request you to advise on below queries:

1. Can I surrender my policy.

2. How much will I get if I surrender it at this point of time.

Thanks in advance. Looking forward to hearing from you.

Regards,

Mudassir

Dear Mudassir,

1) If you are OK with around 5% returns for around 10 to 15 years of tenure, then go ahead and continue the policy. If NOT, then better to surrender.

2) Please be in touch the nearest LIC Branch.

Dear Basavaraj,

I am using Jeevan Saral LIC policy for almost 8 years. But I want to surrender it with below condition:-

1). I bought policy in Delhi, but currently relocated to Bangalore.

2). The address mentioned in the bond paper is no longer exist.

Now, please suggest what should i do, if i do not want to visit the Delhi-branch to close this policy?

Also, my friend told me to transfer the branch here locally at Bangalore, then surrender.

Please suggest your opinion.

Dear Prashant,

The best option for you is to first let it be transferred to Bangalore (Send a letter to Delhi branch to transfer the policy documents to Bangalore Branch). Once it is done, then go for surrender.

Hi Sir,

I have sent 2-3 email with attached adhar card to LIC office for transferring account from delhi to Mohali (Punjab).But still my account is not being transferred . I sent mail 2 months Back.

What should i do next?

One more question for closing account do we need to visit delhi branch?

Dear Abhishek,

Try to call them and check the status. Yes, the physical visit is a must to close the policy.

i want to surrendrer my policy but i lost my original bond. brach told me to filled form and that needs franklin and notary. i want to know how much amount of franklin and notary in required for that

Dear Shagufta,

I am not sure about how much amount required. Better you get that information from the branch itself.

i want to surreder the lic policy but i have not present on originator place where i have take policy. How can i surrender the LIC policy any other place or any other branch?

Dear Umesh,

Sadly you have no option but to visit the branch and surrender.

Hello Mr. Basavaraj,

For getting the surrender quote or to understand what will be the paid-up value, can I visit any LIC branch or do I have to visit the same LIC branch from where the policy was initiated? I was in Kolkata when the LIC policies were started and now I am in Mumbai so can I visit Mumbai LIC office or I need to go back to the Kolkata LIC office? Kindly advise. Many Thanks, Best Regards.

Dear Bhaskar,

You can visit the nearest LIC branch.

many thanks for the quick reply

Hi, I have 2 LiC policies

Jeevan saral & Jeevan anand since Jan 2010

Now after knowing the disadvantages I want to close it

What will be the sum assured ?

It seems I have payed more than 5 years, so will it be 100% ?

Dear Siddhesh,

Contact the LIC Branch for the same.

Dear Basavaraj

I have a policy (term plan) that charges around 38,000/- per quarter for a term cover and some maturity benefit. I’ve been paying this regularly for the past 5 years. I decided I don’t want to continue with this and have not paid the last two payments of my premium. Also, I received an intimation that the surrender value is now 5,11,000/-. I want to surrender but I have two questions:

How do I surrender if I have lost the original bond?

And, if I have not paid the last two premiums and want to surrender now, what will happen? Do I have to pay first or can I just simply surrender?

Dear Abhishek,

How can a term plan is eligible for surrender value? Please cross check your policy details.

It’s not a term plan. My mistake. Its a plan where I pay for 8 years and I get a maturity benefit after20 years and then death benefit. I don’t want to continue this. Now? I have a surrender value of 5,11,000/- and also I haven’t paid last two premiums.. also I have lost the document. Please advise.

Dear Abhishek,

Approach the home branch to know the values and surrender.

It isn’t a Term Plan. It’s LIC Jeevan Tarang with a 30 L maturity benefit. My premium is 1.57L per annum quarterly. I lost the document and missed the last two payments. I want to surrender and I have a surrender value of 5,11,000/- . What can I do and what will the non-payment impact?

Dear Abhishek,

If you not paid the dues, then currently the policy is in lapsed mode. However, if you paid 3 years of premium, then you still go for surrender.

thank you for taking time to share the information, it really helped!

sir, I have a endorsement plan of lic bunch of 20 policies and I am paying 38300 yearly since 2012 but now I want to surrender my all policies so please tell how much of amount I will get

Dear Tarun,

Please visit the home branch.

Dear sir,

I have jeevan saral policy. paid premium for 6 yr . now i want to surrender this policy… i want to know that can i get my 100? of premium paid amont?.

Dear Nisha,

Sadly NO.

yes today i visited LIC branch…they told me i will get around 75 to 80% of total premium paid amount in 6yrs…

Dear Nisha,

In that case what is your call?

I will surrender it…bcz there is no reason for continue…

Dear Nisha,

Go ahead!

Thank you…..

Hi… i have also same issue. Can you please help me to surrender

my LIC policy ??

Hello sir, I have LIC Money Plus (paying only Rs.15000 .3 qtrly -2007) 20 years policy. Now can I surrender my Policy

Dear Sreenivasulu,

Yes.

Thankyou Sir

Want to surrender my two reliance nipon policy how much return money i will get want to know about that

Dear Jitinder,

Approach Reliance Nippon Life.

Dear Mr. Basavaraj,

I have Jeevan Tarang policy. My yearly premium is 83674 and I am paying from 2012. Also I have another policy whose premium is 1844. In all I am paying 85518 and I have to pay till 2032. I want to discontinue this policy. How much amount will I get.

Please reply.

Thanks

Dear Dhiraj,

Better to contact the nearest or home branch of LIC.

Hi sir, i’ m paying premium for lic Anmol Jeevan -I (plan- 164) from 2013 ; now I want to stop the premium wether i’ get any amount or not sir; as my agent told me this is a risk policy.

Dear Raghavendra,

As it is a pure term life insurance product, you will not get any amount if you close the policy (even at maturity also).

Hello sir,

I have opted for Lic jevaan laabh…..with yearly premium of 70,000/-, I have paid the first premium but now I wanted to quit………!!!!!!

Shall I quit right now or complete the 3 years………which will be better…….???

Plz do reply sir.

Thanks

Dear Sanjeev,

Hard but best is to close NOW.

Dear Basavraj,

I am also a victim of falling in the hands of LIC agents who sell policies to young and vulnerable clients and don’t actually explain the consequences of it. I bought JEEVAN ANAND (149). The date of maturity is 2085 answer the current status of the policy is “In Force” with premium paying terms of 30 years. What will happen if I want to terminate the policy? Will I get any money back ? I have paid premiums for last 10 years.

Dear Saket,

If you terminate, then you have two option to choose. One is surrender and another is paid up. Better to surrender.

Thanks for your reply, Basavaraj. Will I get any money back by surrendering my policy?

Dear Saket,

Yes if you paid 3 years premium. But the quantum of the money should be get it if you visit the home branch.

Sir, I am started LIC policy (31.03.2017) Now i am not interest to pay for this.

how to i Claim to paid amount ?

Dear Sanjeev,

You can cliam it if you paid the premium for at least 3 years. That also, you will not get the full amount of what you paid.

I took up the lic policy in 2005

I have been paying regularly and I have to pay till 2025.

But now I realised maturity is in 2077.

I don’t want to wait till maturity and so if I surrender,how much will I loose?

Dear Abhi,

Which policy it is? If Jeevan Anand, then your maturity may be in 2015. Cross check the same with LIC Branch also.

Hello,

I would like to know, what are the consequences if I stop my policy before 3 years?

Thanks

Dear Sandesh,

You have to forget of whatever you have paid.

Hi Sir

Mine Jeevan anand policy complete s 5 years from commencement on Dec 2018..

1. If I surrender policy or Jan or Feb 2019 is there any effect for 80 c claimed deduction for the current FY..

2. Which ITR is correct and where to show surrender amount in case no tax and no 80 c reversion..

Dear Keshav,

Refer my post “Tax Benefits of Life Insurance“.

1.Policy completed 5years..now we are in end of FY 18-19..premium paid till Jan is still claimed under 80 c dedction if I surrender before FY ..

2. Read few articles..for surrender if annual premium paid is less than 10%..surrender value is not taxable right..correct me if I’m wrong

1.Policy completed 5years..now we are in end of FY 18-19..premium paid till Jan is still claimed under 80 c dedction if I surrender before FY ..

2. Read few articles..for surrender if annual premium paid is less than 10%..surrender value is not taxable right..correct me if I’m wrong

Dear Keshavamurthy,

Refer my post “Tax Benefits of Life Insurance“.

Hello sir, 2 of my policies were purchased from KA state branch & nowadays I’ve been shifted to MH. While surrendering the same will i have to visit the serving branch?

Dear Shiva,

Sadly YES. However, the alternative is that you first transfer both the policies to your nearest branch (by sending the written request to the home branch). Once the transfer is done, then you can surrender the same from the new branch.

Hi Sir,

My policy Name : LIC Jeevan Labh

total premium amount : 15 Lacks for 12 years

yearly i have to pay 80000/-

Clarification : i want to surrender this amount this year 2019 ( will complete 3 years ), can i get complete paid amount.

Example : 80,000 * 3 = 2,40,000/- will get or not?

Dear Ravi,

Sadly NO.

Hello Sir,

I have paid premiums for Jeevan Anand 149 plan amounting to 30516 for 8 years now from 2010, there are 12 individual policies with maturity of 1Lakh each. Now I am thinking of closing the policy now. Need to know the amount that I will get if I close now.

Thanks.

Dear Mahesh,

Approach the concerned LIC office for the same.

Dear Basavaraj,

I have paid 6 quarterly premiums so far. I am quite young. I signed up for the policy by mistake. I don’t intend on continuing the payment. What will have to the 1.5 yrs of premiums I paid?

Dear AM,

Either you have to complete 3 years or forget of whatever you paid now.

I have taken Loan against 2 LIC policies…so further I wanted to stop these policies,So how much I should pay further or I will get return amt.from LIC?

please help

Dear Amit,

LIC will first arrive at surrender value If you are planning to close it. In that surrender value, they deduct the outstanding loan dues and pay you the rest of the amount.

Dear Sir,

I don’t want to surrender the policy, but won’t be able to pay future premium. To convert it to paid up policy, dose I need to contact servicing branch? Do I need to give letter in writing? Please clarify…

Dear Shrinivas,

Not required. Just stop paying premium.

Hi Basavaraj,

3 years completed, If we stop paying premium.Should we get money or not. If yes when shall we get. i paid almost 1.5L

Dear Behara,

If you completed three policy periods, then yes you can surrender but sadly you will receive less of what you paid actually.

Dear Basavaraj,

I don’t want to surrender and I don’t want to continue. i want to stop here in this case what will happen.

Thanks.

Dear Behara,

In that case, policy will turn to be Paid Up. You will receive this paid up value at maturity or at death.

Dear sir i had buy an one of the LIC plan recently and they committed me to medical insurance and credit card of LIC along with policy after a long time six months they still not given me the same. i had paid one installment and don’t want pay or continue the policy as i found cheated.. sir what to di pls advise. Thanks

Dear Jitendra,

You are get cheated horribly by those who sold you. You can complain against this with LIC at first immediately.

Hello sir, what is the procedure to surrender LIC policy which is in the name of minor

Dear Raj,

It is same as I have explained in above post (because the policyholder is minor). Hence, proposer has to go ahead and complete the surrendering process.

Hello sir, I have LIC Jeevan Saral (paying 12000 from Dec 2010, SA 2,50,000) and Jeevan Anand (paying 12000 from Jul 2011, SA 2,00,000) policies. Both are 20 years policy. I plan to close both due to financial situation. Is it good to proceed now for surrender. Whether I will get any partial policy bonus? Please advice.

Dear Sridaran,

GOOD or BAD depends on whether you feel these products suitable for you or not. Regarding partial bonus availability, YES, but better to contact the home branch for the same.

Thanks for your reply sir. I came to know that Jeeval Saral is not good and I won’t get complete paid amount.Don’t know about Jeevan Anand. I thought I can close one based on return profit and hold other to compensate loss if any in coming months.

Dear Sridaran,

If you are OK with around 5% to 6% returns, then continue. Otherwise, you have to come out.

helo sir mane lic policy li hai aur 5 year complit bhi hogya hai isme mujhe 2 baar mony back aya hai 10000 thaushand ka meri monthli lic 1040 ki debit hoti hai ab me ye lic close karna chata hu to bataye mujhe kya benefit hai…

Dear Pradeep,

You can close now and for that visit the concerned LIC Branch.

i have paid 3 installment of LIC jeevan anand 815, i want to close LIC thsi policy, how much i will get back money.

Last 3rd Premium paid date is – 25June 2018

Dear Amol,

Please visit the nearest LIC branch.

Hello Sir,

My relative had taken Jeevan Anand (Table No. 149)

Policy Purchase Year: 2011.

Sum Assured : 400000

Tenure: 16 years.

Premium: 27652 Rupees / Year

Premium payment Date: 28/Dec

He has paid first 2 installments and after 2012, he has not paid anything.

1) What happens to 2 paid installments ? will it remain as it is or will LIC charge any money on it.

2) Is there any Bonus Earned on those 2 installments ?

3) Life cover is still there?

4) When can invested money can be withdrawn or recovered ?

Dear Nikhil,

I have already replied to your FB message.

Hello Sir, I have taken Jeevan Saral profit plan in Oct-2010, with half yearly premium of Rs. 6065/- and paying payed all the premiums on time till Oct’2017. I want to surrender the policy now because of some financial conditions. Can you please tell what will be the amount I will get back if I surrender now.

Also I am in another city now, so can I send the required documents to my home branch by post and expect to get the work done?

Dear Abhinov,

Visit the nearest LIC Branch for the valuation purpose. Yes, they accept if you send the documents through the post. But be careful and follow up the same regularly.

he has to re-run it after submitting late fees…there is no benefit in surrendering lic as it gives maximum returns on maturity…jeewan anand is a very good plan….u will not get a single rupees if u havent paid money for three years continuously…run it till maturity if u have opted this plan and if u can manage to pay…hope this helps…even if u surrender it after three years itz a big big loss…thanks

Dear RJ,

“maximum returns on maturity”-HOW MUCH? Can you elaborate? Don’t act like typical LIC Agent. Think about the money of the people who invest for their future.

Jeevan saral with annual premium of 36k in 2012 Dec.

Now it has completed 7 years and i now when i search accross i get the return on such policy are around 6-8% and not more then that.

when i review my finacial stuff i dont think i need such policy and hence need advice if i should surrender.

but the surrender charges are 30 k (I invested 109k and i am getting back 87k ).

Not sure if i continue for 10 years and then see or how should i take it since loss is very high.

Dear Lalit,

Even if you continue also, the returns are not more than 6%. I am not sure who told you that your current returns are even 8%. Think that you committed the mistake and paying penalty for your ignorance.

no after maturity definitely u r going to get benefit….dont opt for market plus policy…..becos lic gives returns by investing in market and by people like you…who surrender it uselessly and accrue losses….

Sir, is there any way to take loan from lic policy through online? If yes how much amount can I take.

Dear Meren,

Sadly NO.

I have taken a Jeevan saral policy, tenure is 35yrs. Already finished 9yrs. Intend to stop the policy after completion of 10yrs. Kindly advise

Dear Dom,

Better to do that.

Dear Basu,

As Jeevan Saral include Special surrender value, 100% premium will be back after 5 yrs. My policy completed 8 yrs. Intend to surrender it ASAP OR after 10 yrs. Its matter of 2 yrs.

Can you plz confirm if policy will be surrender, then amount would include loyalty addition (after 10 yrs).?

Hello,

Is there any way in which we can lower the tenure of the policy. Eg one policy which i took has been issued to me for 35 years, which i feel now is a little too much. Can I reduce the tenure for this policy to close to 20 years somehow

Thanks

Dear Danny,

Yes, you can reduce the premium paying term. However, proportionally the premium will increase.

Good morning Basuraj,

Two things I would like to know from you sir :

1. I’m paying annual premium of 5 lacs towards LIC – mostly Jeevan Saral policies. All these policies have completed 3 years of continuous payment.

Is it worth stopping them and investing that amount in Mutual funds?

2. Since I have taken 2 lacs loan against two LIC policies, can I surrender or make it paid-up without repaying the loan amount?

Dear Anil,

1) Yes, it is worth but also if you go for surrender, then be ready to get less than what you paid.

2) You can either surrender or paid up. After deducting the outstanding loan, then paid you or convert to paid up.

I have Jeevan Anand Policy with 11000 yearly premium. I have already paid 12 installaments. (12 years). term – 21 years

Now I want to surrender the polciy.

Can you please let me know how much I will get back on this.

Dear Babu,

Please visit the branch for exact values.

I purchased a Policy from PNB Metlife. For 1st year I paid the premium in single shot. For 2nd year I opted for monthly ECS.. Which continued for 1 year and suddenly it stopped, offcourse not due to insufficient funds.. When approached, costumer service executive told me that it is due to some technical error at their end, which will be rectified soon.. However, it never renewed. Pls suggest, What should I do in this case?

Dear Faraz,

It is the biggest blunder they committed and let them correct it.

Dear Basav,

Thanks a lot for such a prompt revert. Would you advise for surrendering the policy and withdraw the money..? And go for a new policy may be..

Dear Faraz,

It is not your fault, then let them correct. However, if you are looking for a completely new product, then you can move on.

I was purchase policy 2008. I was paid premium only 2.5 year then stop paying premium any reason .now i want to surrender my policy ..the period was 10 year …can i eligible to my money back how i paid ..which process i do

Dear Dheeraj,

You are eligible for surrender if you paid 3 years premium.

Dear Sir ,

I have money back policy no 127787789 , 3 years completed . I am planing to policy surrender as not paynig farther premiums .

Request you to please let me know your suggestio how to proceed I have taken term insurance for my insurance needs.

Thanks

Dear Devraj,

Refer above post and visit the concerned branch for the same.

Hi Basavraj,

I have taken New Jeevan Anand (Plan-815) sum assured is 15,00,000 and installment Premium is 1,16,437 and Policy Term 15 years and Premium Paying Term is 15 years and policy benefit is 15,00,000.00 date of maturity in 15 years

Is above policy worth to take what ? After maturity with interest how much amount i will get? or

1)After paying 3 years Guaranteed Surrender Value Surrender will come around 1,20,000 is waste to go with it?

2)after paying 3 years Special surrender value i will be 4,00,000 for 7.5 Lakhs for what i paid?Special surrender value will get after date of maturity only na ?

Shall i quit this plan or continue with this plan?or Shall i go with any sip?

Please suggest?

Dear Vaibhav,

Continue this policy if you feel Rs.15,00,000 life insurance is sufficient for your family dependents to survive in your absence. Continue this policy if you feel 4% to 5% returns are best for the 15 years of investment.

Dear Sir,

After open policy i have paid 3 premium after that i stopped, so will this money refund?

Dear Atin,

Refer the above post properly.

Hello sir, I joined in a Bima gold policy in 2006 with 50000Rs 20years. I want to cancel the policy. Is this good decision?

Is this possible?

Dear Padmasri,

Yes, you can surrender now. But good or bad depends on why you decided now to close it?

Sir , I have lost my policy bond or either the agent wouldn’t provided me , can I surrender my policy with first premium receipt ?

Please let me know the process to retrieve duplicate policy bond.

Currently my location is Bangalore and I have done my policy from west Bengal.

Thanks in advance

Dear Jaidev,

You have to approach to the branch for duplicate bond at first. Then you can surrender it. Please be in touch with your agent or the concerned branch.

Dear Sir,

Thanks a lot for clearing the confusion 🙂

Sir I have a jivan saral policy (with profits) purchased in December 2013. And I have paid total 4042 per month*53month

…so sir please tell me how many surrender value amount or paid up value return to me from lic of india

Dear Jignesh,

Contact the LIC Branch for the same.

i have a jeevan anand policy for 25 years which i took in 2014, paid up to 4 premiums now. Is there an option to extend it to 35 years (policy term) as that seems to fetch me more returns ? If not possible pls advice me if i can cancel that and take a new jeevan anada with 35 years?

Dear Vignesh,

You can’t extend the policy period in between. However, you can buy a new one. But do you feel such products right for long-term investment?

Hi Sir, I have taken a New Jeevan Anand policy of Sum assured 500,000 in 2017 and have paid 1 annual premium so far. Understand that if I pay 2 more annual premiums i.e. complete 3 years and lapse thereafter then it would be considered as Paid-up value. There are 2 options to take the paid-up value; One is to take this paid-up value on maturity with bonus and other option is to take the paid-up value after 8 years without bonus. Is the second option true? Please advise

Dear Rajesh,

Even I am also hearing this second option with YOU itself. Cross check with LIC officials (not agents) directly.

Dear Sir,

Thanks for your response.