HDFC Life Pension Guaranteed Plan is claimed to be unique immediate and deferred annuity plan which many feel offers around 11% to 12% GUARANTEED pension during your retirement. Is it true to get such high pension from this product? Let us check the reality.

What is the difference between an immediate annuity and deferred annuity plans?

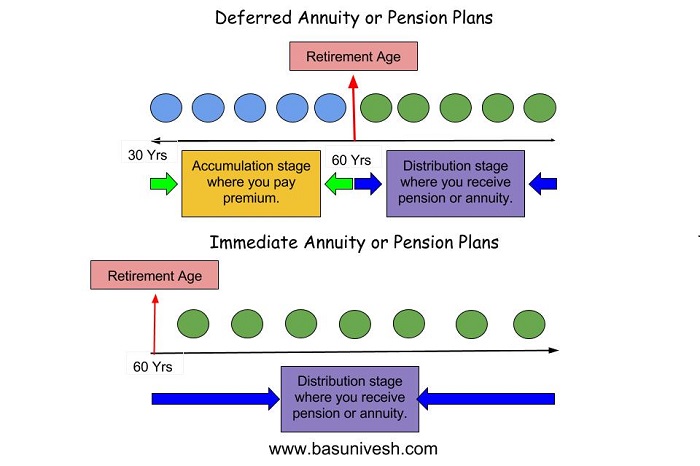

Before proceeding further, first, let us understand the meaning of immediate annuity and deferred annuity plans.

# Deferred Annuity Plan-

Let us assume you are 30 years of age and planning to retire at the age of 50 years. Now you start investing in such deferred annuity plan. Because your retirement is not immediate. Once you reach your retirement age of 50 years, then the annuity or pension will start. Hence, you are deferring annuity to match with your retirement age.

# Immediate Annuity Plan-

Let us assume you are 50 years of age and retiring today itself. Also, you have accumulated the retirement corpus to generate the pension or annuity. In such situation, you have to look for immediate annuity plan. Because your annuity is about to start.

HDFC Life Pension Guaranteed Plan Eligibility

Now let us concentrate on HDFC Life Pension Guaranteed Plan eligibility.

You noticed that for immediate annuity plans the minimum age is 30 years and for deferred annuity plan the eligibility is 45 years and above.

HDFC Life Pension Guaranteed Plan -Types of Annuity available

HDFC Life Pension Guaranteed Plan offers you three types of annuity features.

a) Immediate Life Annuity Option

This option is available on both single life and joint life basis.

# Single Life

• The annuity will be payable in arrears as per payment frequency is chosen by you, for as long as the annuitant is alive.

• On the death of the annuitant, the annuity payments will cease and no further benefits will be payable.

# Joint Life

• The annuity will be payable in arrears as per payment frequency is chosen by you, for as long as either of the primary or the secondary annuitant is alive.

• On the death of both annuitants, the annuity payments will cease and no further benefits will be payable

b) Immediate Life Annuity with Return of Purchase Price Option

This option is available on both single life and joint life basis.

# Single Life

• The annuity will be payable in arrears as per payment frequency is chosen by you, for as long as the annuitant is alive.

• On the death of the annuitant, Death benefit4 is payable as a lump sum to the nominee and no further amount will be

payable. Upon payment of the death benefit, the policy shall terminate and all other benefits shall cease.

# Joint Life

• The annuity will be payable in arrears as per payment frequency is chosen by you, for as long as either of the primary or the secondary annuitant is alive.

• DThe death benefit is payable as a lump sum to the nominee, on later of the deaths of the two annuitants. Upon payment of the death benefit, the policy shall terminate and all other benefits shall cease.

c) Deferred Life Annuity with Return of Purchase Price Option

This option is available on both single life and joint life basis. Deferment Period may be between 1 to 10 years, as chosen by you at inception. The annuity rate shall be as guaranteed at the inception of the Policy.

# Single Life

• The annuity will be payable in arrears post deferment period as per payment frequency is chosen by you, for as long

as the annuitant is alive.

• On the death of the annuitant, the death benefit is payable as a lump sum to the nominee and no further amount will be payable. Upon payment of the death benefit, the policy shall terminate and all other benefits shall cease.

# Joint Life

• The annuity will be payable in arrears post deferment period as per payment frequency is chosen by you, for as long

as either of the primary or the secondary annuitant is alive.

• The death benefit is payable as a lump sum to the nominee, on later of the deaths of the two annuitants. Upon payment of the death benefit, the policy shall terminate and all other benefits shall cease.

Death Benefits in HDFC Life Pension Guaranteed Plan

# In Immediate Annuity Plan-No death Benefits.

# Immediate Life Annuity with Return of Purchase Price Option-100% of the Purchase Price of the annuity.

# Deferred Life Annuity with Return of Purchase Price Option-The death benefits are as below.

Higher of

• Purchase Price + Guaranteed Additions(GA) – Total Annuity Payouts till date of death

• 110 % of Purchase Price where, GA = Purchase Price * Annuity Rate/12 And are accrued at the end of every policy month during the deferment period. GA stops accruing at the end of the deferment period.

Surrender Benefits in HDFC Life Pension Guaranteed Plan

This plan offers surrender benefits and are as below with respect to annuity option you choose.

a) Immediate Life Annuity Option (Single and Joint life option): Surrender not allowed.

b) Immediate and Deferred Life Annuity with Return of Purchase Price (Single and Joint life option):

Surrender Value shall be equal to the Present Value (PV) of expected future benefits discounted at the then

prevailing interest + 2%.

Other Features of HDFC Life Pension Guaranteed Plan

- This plan offers nomination facility.

- There are no maturity benefits under this plan.

- The policy loan is available on in case of Deferred Life Annuity option.

HDFC Life Pension Guaranteed Plan – Should you invest?

# Let us take an example of a person who is aged 50 years and looking for first annuity option (immediate life annuity) and investing Rs.1,00,000. The annuity rate is 7.05% and 7.32% for Rate A and Rate B (I am not sure what the difference as they have not explained in detail). However, if you compare the same with LIC’s Jeevan Akshay VI, I found that the annuity rate is 7.47%. Hence, I still feel in case of immediate annuity plan, LIC’s Jeevan Akshay VI is the winner with plenty of options.

# Let us take an example of a person who is aged 45 years and looking for third annuity option (Deferred Life Annuity with Return of Purchase Price Option) and with a deferment period of 10 years. This means he will invest today and wait for next 10 years. Once he reaches the 55 years of age, then he will start getting this pension. In such situation, the rate of annuity is mentioned as 11.54% and 12.17% (for Rate A and Rate B). EYE CATCHING RIGHT? 11% t0 12% GUARANTEED PENSION for life is everyone’s dream. But hold on.

The biggest catch in this plan is that you are investing today in case of deferred life annuity pension, but you will receive the returns only after 10 years.

Hence, let us assume that you are currently 45 years of age (this is what the minimum age to enter this feature of annuity) and investing this Rs.1,00,000 in a 10 years bank FD. I am considering the FD rate of around 6% (excluding the taxation).

Therefore after 10 years, the Rs.1,00,000 will be Rs.1,79,084. At maturity of FD, your age will be 55 years. Hence, let us consider now the same annuity option with considering your age as 55 years but DEFERREMENT PERIOD as 1 years only, then the return % is 6.7% and 6.97% (for Rate A and Rate B).

Hence, what I am trying to say is that 11% or 12% of GUARANTEED PENSION for life is eye-catching. However, the money you invest today will be with them for the next 10 years without giving you a single rupee back.

If you believe that your pension is GUARANTEED for 11% to 12% returns, then for that you have to invest today and forget up to your retirement. Hence, in reality, this is not the REAL 11% or 12% return. It is less than that and to be frank not cross the LIC’s Jeevan Akshay VI annuity rate.

# As per current income tax benefits, the annuity you will receive will be taxable income as per your tax slab. Hence, it will further reduce your income.

Conclusion:-This plan launched with the word GUARANTEED pension with around 11% to 12% in case of deferred annuity plans. But silent on mentioning that your money will be with them up to the deferred period closure. Hence, the actual return from this annuity will be around 6% to less than 8% for the various age group.

When you compare the annuity rate of this product with LIC’s Jeevan Akshay VI, then I found the LIC’s rates are most better than this product.

Hello Basavraj

Your blogs are always helpful for taking any investment decisions.

You have given nice example comparing HDFC immediate annuity returns vs Jeevan Akshay.

Similarly please give sample comparison with HDFC differed annuity vs Jeevan shanti. I know its hard for you to compare all possibilities but as a sample joint life differed annuity for 5 years can be taken . (I tried to do it on HDFC calculator but its not giving me expected results, dont know why. )

Thnaks

HDFC life pension converted to yearly Annuity, is that payment considered as Income or interest for India income tax?

Dear Naresh,

Any pension or annuity income is considered as taxable income under the head of salary.

Is there any “guarantee” to the guaranteed pension plan. For eg. If the FD rates at that time reduces to 4% or so, will we get the pension mentioned in the policy

Dear Shaji,

GUARANTEED is the word used to fool the buyers.

I Want comparison between HDFC Life Pension Guaranteed Plan with LIC’s Jeevan Shanti.

Dear Debaprasad,

It is hard for me to compare each and every individual plan available in the market. However, I can help you in clearing your doubts.

Please advise if I invest 10,00,000 in Jeevan Akshay VI. My age is 51 and now jobless, requiring guaranteed monthly income lifelong. Any other suggestions is also appreciated. Thank you Basu,

Dear Rajeev,

Regarding annuity, you check the same on LIC portal (using online calculators). Regarding other options, for your age there are no such guaranteed products like SCSS or Pradhan Mantri Vaya Vandana Yojana. Hence, you have to rely on Postal MIS kind of products.

Immediate Annuity rate 6.5 to 6.8% if deferred by 10 yrs then rate will be 12.54% Guaranteed

Sailen-What about the returns of the deferred period? They retain with them and give you 12.54% then is it really 12.54% for you??

I want to invest rs 1500000/-at one time for 5-10yrs ,what will be the interest rate n monthly pension I will get?

Nakibur-Check with calculator available with HDFC Life portal.

HI Basu g, I m aged 40 yrs. Pls suggest me that, to accumulate 1Crore in 18 years, which is the best way.

SIP in Mutual funds Or

FDs and LIC

If SIP pls suggest which Mutual fund schemes Or

Which Lic plan.

Thanks g

Dalijit-It is hard for me to guide anything BLINDLY (without knowing your financial life).

Sir

Has HDFC given any numbers about the G. A. in the differed plan. How much will be added every year ?

Will the annuity be calculated (11 to 12 % ) on the premium amt OR on the premium + accumulate G A ?

ANAND

Anand-There is no GA during this deferred period. It will be on the invested amount (as per them).

Hello Sir whether is it true that if a women invested 1500 per month for 16 years of time, she would get around 1022400 Rs as maturity after 25 years ?

Vinay-In this plan, there is nothing such mentioned that for women a special benefit is provided. It is all sales trick. Stay away from all these.

Many propositions say pension plan should be Tax Free. Unlike Other countries.. What is the possibility of Earning out of Pension Plan to get Tax Exemptions..

Parul-That is the biggest drawback for senior citizens not only from pension products but from all products like SCSS or Pradhan Mantri Vaya Vandana Yojana.

Your view is a like businessmen.Alright.But who saves are they can do Business if so then why all savers and investors looking for savings and investments in all financial companies.They leave the whole matter entirely upon companies and become busy in their works or in daily routine.They sleep a peaceful night by securing their hard earned money not to compromise their individual goals they set for rest of life.Companies like LIC HDFC …..do the business of profit making as well as securing customers’ money in their business.They only takes RISKS not customers.They are not any NGO or charitable trust that they offer full profits out of money invested in their business.To run their business costs also come out of profits.Let them make profits and let the customers of theirs sleep well.They are distributing their profits but not leaving any headache to customers.Its their risk and their headache how they will repay to clients.Why are we worried

It would have been easier on my eyes, if you would have added some spaces

in your comment. (Not to mention grammar issues).

Yes, your description entirely matches mine.

“But who saves are they can do Business if so then why all savers and investors looking for savings and investments in all financial companies.They leave the whole matter entirely upon companies and become busy in their works or in daily routine.They sleep a peaceful night by securing their hard earned money not to compromise their individual goals they set for rest of life”

Whatever you feel comfortable with, go ahead and do.

But keep an eye on returns generated in other instruments.

After you make a big commitment (10L), from which you can never

turn back, without taking a big loss, and if you are happy with this – go ahead.

Don’t read these blogs and comments. They will only make you even more uncertain.

I did exactly that, I had worked from 1982 to 2010, and then retired peacefully at 50.

I am 58 now, with 3 pensions worth 27k pm plus a very big FD pool that matures every month,

yes every month till 2021 Jan. Then from all the monthly returns (I do spend only 1/5th of

my monthly earnings), I invest back in various instruments, So the 2021 Jan date is pushed back

further and further — way deep into the future. I have 50% more of value of my FDs, in LIC

and MFs and stocks.

I think even my son can depend on all this without ever having to work.

(I did not tell him all that of course).

And I started all the savings, way back in 1994-95 when I just had 5k to spare every month.

But check out CRISIL’s ratings on MFs in moneycontrol(dot)com. And follow their

returns, while HDFC hatches your eggs.

I too had my share of losses, but the gains from fiscal discipline, has wiped the losses out.

Subha-Well said and thanks for sharing your experience 🙂

Sailen-CONFIRMED!!! You belong to agent fraternity. So it is obvious that you must defend 🙂

Yes time value is PEACE OF MIND….now all fixed secured rate is 6%-6.5% ..HDFC giving after deferred period 8%-12.39% why????why they r giving DOUBLE of present rate ????Time value is added here with GUARANTEED secured No risk but GAIN

Sailen-Great LOGIC!! Go ahead and invest and Best Of Luck 🙂 However, if you are representative of HDFC Life, then it is my caution to the people who read this blog and taking your suggestion to think twice before investing!!

Basavaraj,

Most of the educated folks are stupid and greedy. They are ready to throw money without doing calculations and understanding risks. No wonder the founders run away with public money. Guys of 25 yrs age happily starts to invest 80k per year for 30 yrs to get a 25k per month pension @ age 60?

Just throw words like fixed rate guaranteed 12% and people will queue up to throw money.

Make your own corpus and purchase a laddered immediate annuity from a part of it @age 60.

Anant-They lack FINANCIAL EDUCATION and COMMON SENSE (which sadly they not learned in their school).

Truth. Well Said sir.

Do this to minimize risk – Buy immediate annuity with no more than 30% of your portfolio after 60 years of age. Buy with 2 different providers. Ladder every 5 years to counter inflation.

Do not fall for pension plan,defered annuity etc. Buy only from provider who will be in business for your lifetime.

Anant-Well said.

Mr.Basavaraj Tonagatti after reading your chat with Subha who gave surprisingly different picture of this plan which u tried best to criticise…

I feel your are now diplomatically trying to save yourself from misleading interpretation you did about this plan..

You would gain more respect if accept the fact of this plan n try not to sell LIC indrectly.

would wait to see how bold u r to accept the fact that this seem to be the best retirement option

Parul-I am neither DIPLOMATIC nor AGGRESSIVE 🙂 My point is if you feel NEGATIVE REAL RETURN is best return for you, then it is your own choice not mine. Because at the end it is your money. However, keep one thing mind, I am neither LIC agent nor represent any LIfe Insurance Company. Hence, it matters to me by neither defending LIC nor others.

There are many ways to manage your retirement corpus (like simple using debt products or using bucket strategy and mix with debt and equity). The problem is you are just looking for GUARANTEED. But not ready to accept AT WHAT COST?

At age of 75 when medically,physically n mentality person is at his most vunerable stage n you stupid strategy will make me run from pillar to post to manage funds in debt n equity buckets…

so the real cost basis your advice is one should keep risking there cost of mental peace .

Parul-But do you think there is only one way to it? What I am saying is there are many ways to manage money. If you are satisfied with 4% to 6% returns for the sake of your comfort (thinking you are unable to move due to medically, physically and mentally ill person), then it is up to you to manage your money. That is the reason I said, if you are comfortable with the kind of return, then who is STOPPING you on this earth?

Parul, your reaction has befuddled me ! Not to mention your happiness with 6%.

Basavraj is doing a good job here, though he may improve on his communication a bit, I feel.

Subha-Thanks for your suggestion. Yes, I know my English is too bad 🙂 But Parul trying to say that this is the BEST RETIREMENT solution!!

Finally u accept it is best retirement plan …

Parul-Who said??

Mr.Basavaraj Tonagatti

Can u suggest me a plan which can give me 6% return guranteed 10 years after… I will invest today my money in mutual fund but i need only 6 % guranteed on my corpous 10 year after with no if n but. I dnt want to tension during retirement..n risk on falling interest rates

Parul-You are happy with 6% returns, then why not keep the money in savings accounts (where few banks offer you 6% returns). If you are satisfied with 6% then go ahead. But sad to hear that you are unable to understand the concept of inflation and real return. At the end, it is your money. Therefore whether you need 6% return or NEGATIVE 1% REAL RETURN is left with you 🙂

what will be inflation rate after 10 years….

what is current inflation rate..

Parul-Google it with Govt data. Come up with results you found. Come up with your expected rate of return from your retirement corpus (inclusive of tax and inflation), then can we discuss?

Your questions are an indicator of your confusion. You wanted 6%. Well almost all basic investments give that return. But then you ask about inflation, which is a totally different vector that interacts with the returns vector.

And then again, FD rates are revised every so often.

And you also want GUARANTEE.

Any financial advisor, will be happy to guide you on these, given a fee, like a Doctor or a Lawyer. You may even hire Basavraj for this. It is the magnanimity on the part of Basavraj, to set up a free advice blog here, and what you give him in return are only insults.

Subha-But for few even 4% is the BEST return. We can’t change their mindset. Thanks for endorsing my views 🙂

Review of product is based on perceptions of person …

perceptions are generally based on risk appetite n experience of reviewer…

When Equity Market do well every pan wala talk like a Howard Pass out .

I have seen many review of basavaraj n had been following his blogs from many years…

Just in this his view are biased…

as it is based on his perceptions of taking risk…which he can but many other cant…

Parul-I never said I am an expert. Now regarding equity market and experts, how it relates to this product review? My only point here is to claim and spread the false propaganda by few that this product gives you 12% or more GUARANTEED pension.

The age and risk go adversely.The more you old the less risk one want to take.Thats true to your age Sir.In line with risk appetite you should do a plan of HDFC which will give you from year1 6.89%p.a for the years coming till your last day

Sailen-RISK must be aligned with age but with financial goals and tenure of goals.

I have 3 pension plans from LIC. I had bought them long ago.

1. Plan 189 – purchase price Rs. 381662 immediate annuity

2. Plan 147 – I paid 22L – over 11 yrs

3. Plan 147 – Deferred plan – Paid 4L – Value after 10 yrs Rs 8,55,172

No 3 is like the HDFC plan, but my nominee will get Rs 855172 after me.

And I get a pension of Rs 5088 pm which is about 15% of 4L. Well anybody can see that I got a better deal.

Subha-How you arrived at 15%? Can you calculate and let me know? You have to consider the time value of money also.

Looking at HDFC ‘s Guaranteed pension on a deferred (for 10y) plan of 12%. The 12 % pension is on the amount paid 10 yrs before the pension starts. The parallel math in my case is 5088×12 on 4L after 10 yrs.

Unless of course HDFC pays 12% on the value reached after 10 yrs.

Subha-But how many believe on this simple maths? For few, HDFC LIfe took a great leap with 12% GUARANTEED COMMITMENT 🙂

What happened Basavraj, where did I go wrong ?

You have drawn nice diagrams, but I find the terminologies a little short. Also I suggest, you write your posts with section numbers, so one can refer to them when posting commsnts.

What is my purchase price ? 4L or 8.55 L ? I guess the later is. Then what is the former called ?

Subha-But none believing that 10 years deferred time value of money. All comparing Rs.4 lakh to what HDFC Life will give you after 10 years!! I am not saying you are wrong 🙂

Kindly elaborate where did u find subha right…if you are saying that he is not wrong..

Parul-Read and reread.

Thanks a lot.

Currently i m investing 3000 SIP in elss fund AXIS, IDFC. Also 30K per year in PPF from last 3 years.

Pranav-First do asset allocation between equity and debt based on time horizon of the goal. Then finally select the funds.

100 rupees in 10 yrs become 170 with present rate of FDrate 6 -6.5%…and then u invest in pension you will what get as after 10 yrs (year 2028)rate is not now unknown

If we take declining rate 5%then 170 will give yearly 85 means 8.5 %ROP you will then get for rest of life …if we take 6%present rate continued for 10yrs from today till year 2028 then 170 will give yrly 102 means 10.2%…But here HDFC will give 13%…Wohaaa what an IDEA SIRJI

Sailen-Simple logic, check the immediate annuity rate for your Rs.170 investment, then claim whether the rates are BEST in the market or not 🙂 NONE especially HDFC Life not here for SOCIAL SERVICE. They are into business. If you still not understand these logics, then BEST OF LUCK and INVEST 🙂

FUTURE RATE IS ALWAYS UNCERTAIN AND NOT GUARANTEED BY LICI n Any other companies.Here HDFC has done a great Job by providing a GUARANTEED RATE OF ANNUITY in Future.One who is looking for Pension after 5 or 10 years need not be worried about what rate of return he is going to get.Here is WRITTEN from Day1 what he will get after 5 or 10yrs.What an IDEA sirji Hdfc launched.Thanks to HDFC’s dearest n darest approach and risk taking bold approach for PENSIONERS

Sailen-At what COST HDFC Life is GUARANTEEING YOU?? They take away deferment period returns and give it back to you. If you are unable to understand this simple GIMMICK, then I feel pity of your finance basics.

You are an ADVERTISER OF LICI I know thats why you dont understand….

Sailen-Ha ha….I am neither attached with HDFC nor with LIC. Because by pampering any company, I will not get anything. I can understand your frustration of you being associated with HDFC Life 🙂

Your logic in terms of return is not up to the knowledge of ANNUITY…u r comparing present view but you can not predict FUTURE RATE which HDFC has done.What a daring approach towards old persons and their secured avenues of having PENSION…Thats the great initiative they have taken and the great step they have taken.Its quite expect from a company like HDFC topping the chart always with a most trusted Brand

Sailen-Saying again, I am feeling pity of your basics of financial knowledge. If you are feeling HDFC DID DARING, then go ahead and invest 🙂

Yes I have been saving yearly 1.5 lakh IN HDFCLIFE

Sailen-Best of luck for your retirement life 🙂

Hi

HDFC LIFE is waste , if you want I will give proof

Venkat-But I not brand any particular company as WASTE. I analyze their product and share my views. It is left with readers to decide.

Agree with you Basu, that was just my experience with the kind of response

Hi Basu Sir,

Well explained and very well written blog. I fully agree to your conclusion.

Sir, i believe our countries financial rules are NOT strict, so that anybody or any company can cheat people and escape punishment, not only that they can run abroad and comfortably live there with our money (Nirav Modi, Mallya, Lalit modi are examples). HDFC life is born to cheat people.

I heartily appreciate your sincere efforts in providing financial education to common man.

regards

Rajesh-Thanks a lot for sharing your views 🙂

I am suprised to find every day comments from people who so innocently assume, and even believe that money grows on trees. The so called Kalpataru myth is still alive.

Even just for a moment they do not consider the fact that all these BIG and super BIG companies whose market caps are among the top 5 in the country, who spend trillions on advertising in media, while boys play bat ball, and women stars display their oh so attractive bodies, actually make all their money by luring you into their trap. Try making even 1 rupee with your blood and sweat, and you will immediately see that with honest effort how little is actually made in today’s time.

Subha-Well said 🙂

To continue ..

If a hungry man steals a piece of bread, you will have no compassion for him, and beat him to death, while the high fliers will show off useless pieces of stones, they call diamond, at yet other useless assemblage of starry shows of hollywood, while sucking out gazillions worth of your own hard earned money, and then flee the country. Yet other high fliers selling alcohol will live in sprawling high-end villas, race even more useless glittery 4 wheelers, living a high life, and continuously spew out excuses in defence. Politicians will don garbs embedded with diamonds and precious stones and then auction them off at lakhs, with absolutely no shame and haaya. In the process they try to garner more voter sympathy standing for false values.

Indianns and common people from all countries will always remain gullible and fall prey to false and cheap talk.

You are saying that LIC’ s jeevan Akshay is a good plan though the deffered annuity from HDFC is giving more return than Lic’s!!!

Sivasree-MORE RETURN?? Who will eat your return during the deferred period? I know that Jeevan Akshay is the immediate annuity plan. But in what sense when you calculate, it gives you MORE RETURN? Can you explain?

*First of its kind in the Industry*

*??Pension Guaranteed Plan : Deferred Annuity??*

?Single Premium Plan

?Guaranteed Rates for life time

?Deferred Period of 0 – 10 Years

? Available in Joint Life Basis

*?Guarantee Rates upto 12.45% of the invested amount (minus GST)::: First time in Industry* :: Depends on age & deferred period.

?Unique option of top up

?Liquidity option

?it’s a traditional plan

?Future Rates available today

*Sample Rates*

*55 Years age* (Single Life)

3 Years Deferred : 8.03%

5 Years Deferred : 9.25%

8 Years Deferred : 11.35%

10 Years Deferred : 12.90%

*All This is guaranteed for life time today*

*60 Years age* (Single Life)

3 Years Deferred : 8.14%

5 Years Deferred : 9.47%

8 Years Deferred : 11.69%

10 Years Deferred : 13.26%

*All This is guaranteed for life time today*

Sailen-But what about the returns on investment during a deferred period? Will they give it to YOU or what? If you people still unable to understand the concept of time value of money, then sorry. Please go ahead and INVEST 🙂

Sailen,

I have been following your comments all along. I have also

given an example of my own pension plan from LIC bought at a time

when there were no other companies in the market.

The point here is that when you invest say 10L in a deferred plan for say 10y

and then you get an interest at a rate of say 12.5 % promised today, but which

you will be paid 10yrs later on 10L only.

Actually 10 yrs later the 10L will grow to 3105848.21 assuming HDFC

earns at a rate of 12% compounded yearly, with your money.

They will actually use your 10L to fund businesses for 10 years, and the figure

of 31L is not unusual for a bank. You can yourself pretend to be a business man

and ask HDFC for a loan of 10L for 10y, and they will ask you to pay back 31L if not more.

Calculate yourself here –

http://www.moneycontrol.com/fixed-income/calculator/canara-bank/fixed-deposit-calculator-CB06-BCB001.html

Then if they pay you 12.5% on 10L which is actually only 1/3 the value of your money.

This will no doubt make HDFC a very profitable bank.

This is what Basavraj had been trying to say.

Finally Mr. SAILEN MAITY got the answer. Frankly all companies are still focusing on common people who really lack of financial knowledge. Sadly the % is on higher side in our country.

I was one of them until i start comparing and reading myself.

Dear BASU, appreciate your help via blog helping us to understand complex policy and spreading general awareness of finance that is also for free.

Mayank- pleasure.

Excellent analysis I think finance companies create a lot of false claims or confusing claims which seems too good. The reality is understood only when someone like you sir dig deeper and unravel the truth.

Pramod-Pleasure 🙂

Very well written article Sir. You are my fav finance blogger.

Sir, my father had opened Birla Sun Life Insurance Bachat Endowment Plan of premium amounting Rs 19775 p.a on 2013 for 20yrs term. The sum assured is Rs 1 lakh on the policy. Yesterday I went thru the policy and found out to be a useless one. The thing is my father is critically ill and might not survive. God forbit it, if something bad happens then how much will my mother who is a nominee will get? We have been paying premium regularly without failure. Please reponse asap as we are in a dilema.

Ashwash-This is what is written in product brochure in case of death of the policyholder.

All Monthly Base Premiums paid (or Sum Assured if higher); plus

All Bachat Additions earned; plus

The Loyalty Addition

Thank you Sir

Hi ,

Thanks for info. I want to take pension or retirement plan. Currently my age is 30. And income is 40k per month. So which plan or investment can I choose??

Pranav-Better to create your own corpus by investing in equity (mutual funds) and debt (products like PPF, EPF or Debt Funds).