Which are the online Top 5 Best Term Insurance Plans in India 2018? What is the claim settlement ratio of these best term insurance plans? Let us choose the best term insurance plans in India by comparison with charts.

We have around 24 Life Insurance Companies and as of now, all insurance companies offer online term insurance plans. Hence, it is hard to shortlist the BEST among them. This post will help you in shortlisting the Top 5 Best Term Insurance Plans in India 2018.

What is Term Life Insurance?

Term Insurance is the type of Life Insurance. If death occurs of the policyholder during the policy period, then his/her nominee will receive the Sum Assured selected. If policyholder survives till the end of the policy period, then he/she will not receive any maturity amount.

This is the reason, these policies cost you very less and cover a large amount of life risk. This is the PURE LIFE INSURANCE. Hence, anyone who has financial dependents must buy this product immediately.

However, nowadays there are so many variants in Term Life Insurance. For example, the return of premium, Term Life Insurance up to 100 years of age, a variety of riders and variety of claim payable option.

But instead of complicating your dependents, buy a simple plain term life insurance. Why you complicate your dependents when you are buying this is that this product’s benefit will come into picture when you are not here.

What are the advantages of online Term Insurance Plans?

Nowadays all Life Insurance companies offer you online term insurance plans. The advantages of online term plans are as below.

# It is convenient to buy as with the click of a button you can buy it.

# As there will not be any middlemen involved, the price is cheap than offline term insurance plans.

# You fill the proposal form on your own. Hence, an error of margin is LESS.

# Undue influence by agents is not there.

# Along with the discount of DIRECT purchase, if you buy through online then now life insurance companies will give you 8% on your FIRST YEAR PREMIUM. This is to promote cashless online transactions.

Top 5 Best Term Insurance Plans in India 2018

Now let us shortlist the Top 5 Best Term Insurance Plans in India 2018. How I selected the Top 5 Best Term Insurance Plans in India 2018?

# How old are the companies

# Claim Settlement Ratio

# Premium Cost

# Plan Features.

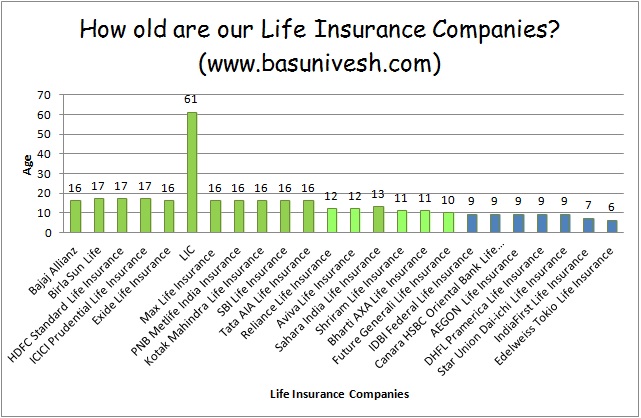

How old are our Life Insurance Companies?

Below is the chart which explains the age of all life insurance companies. I am comfortable with the company which is at least 10 years old.

You notice that among 24 Life Insurance Companies, only 17 companies completed 10 years or more. Therefore, my target is among these 17 companies only.

The reason behind this criteria is that Life Insurance is a long-term contract between you and insurance company. Hence, the older the company the more comfortable I feel.

IRDA Claim Settlement Ratio for 2016-17

I have already written a detailed post on this at “IRDA Claim Settlement Ratio 2016-17 | Best Life Insurance Company in 2018“.

However, for the better understanding purpose, I am putting the data again in this post.

You notice that among total 24 Life Insurance Companies, around 8 companies are in GREEN (Claim Settlement Ratio above 95%). Total 11 companies are in YELLOW (Claim Settlement ratio between 90% to 95%). Total 5 companies are in RED (Claim Settlement Ratio below 90%).

As usual, LIC tops the list. But don’t feel happy. Let us see the claim amount settled by individual companies to arrive at best companies.

Average Claim Settlement Amount of Life Insurance Companies in 2016-17

As I said above, the claim settlement ratio will not give you the clear picture about which type of products the insurance companies settled. However, we can assume the types of products they settled by looking at the average claim settlement amount of Life Insurance Companies in 2016-17.

Here come the results !! LIC stands in lowest with red in colour along with Life Insurance Companies like Sahara, Reliance Life, Exide and Future Generali. What is it indicating?

It shows that, even though LIC settled the highest number of claims, the majority of such claims are less than Rs.2,00,000 Sum Assured. Hence, it is indicating indirectly that LIC’s claim settlement is mainly in the category of Endowment Plans but not Term Insurance.

Hence, the moral of the story is that DON”T RELY TOO MUCH ON CLAIM SETTLEMENT RATIO ALONE!!

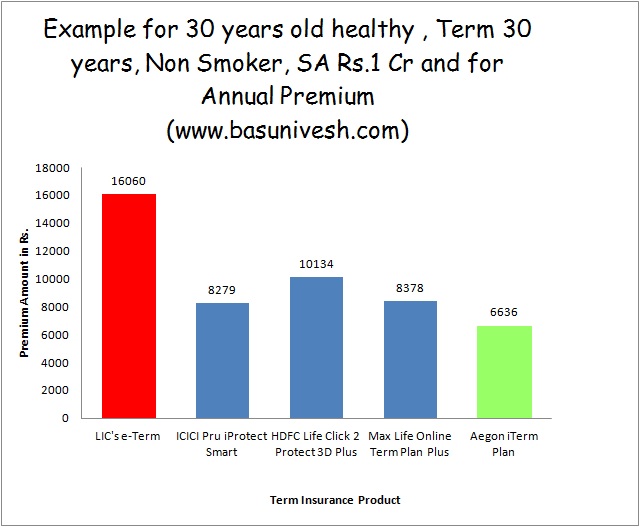

Premium Cost of Term Insurance Plans

Now I will consider these 5 Life Insurance Companies premium only to arrive at best. The Insurance Companies which I shortlisted are as below

- LIC (Why? Because the oldest and Government backed mammoth)

- ICICI

- HDFC

- Max Life

- Aegon Life (Why even though it is less than 10 years-Because of its claim settlement ratio and average claim amount it settled).

Last year I recommended SBI Life’s Term Life Insurance. However, this time I excluded that by including Aegon Life.

Now I will consider an example of a person whose age is 30 years, Term of Plan as 30 years, Non-Smoker and healthy, Sum Assured Rs.1 Cr and yearly premium payment. I selected plain vanilla product without any riders or add-on features.

Now let us look at the plan features and decide which are the Top 5 Best Term Insurance Plans in India 2018.

Few points to consider while buying term insurance

# Never rely on Claim Settlement Ratio

Claim Settlement Ratio is raw data. This data will not give you enough picture of what type of products the insurance companies settled. Hence, relying too much on this single data and selecting a product is not a good idea.

# Quantum of Life Cover

Ideally one must have at least 15-20 times of your yearly income. This is the basic calculation.

# Fill the data properly

Sharing data especially materialistic information must be accurate. If you are unable to understand anything, then immediately contact Life Insurer for the help. Understand the questions and fill only when you know what you are filling.

# Never allow someone to take over your decision

Never budge on the decision which is against your wish. If you are fully comfortable, then only go ahead and buy.

# Term of the policy

Ideally, it should be up to your retirement age. Because you retire when you are financially free. Hence, Life Insurance is not required during your retirement age.

# Splitting of Term Insurance

There are few who are apprehensive of relying on a single insurer. Hence, they try to split among few. But in reality, there is no logic in splitting. What is the guarantee that the all insurer will accept or reject the claim?

# Stay away from riders

Never combine Life Insurance with General Insurance requirement. You will get better-featured covers from general insurers regarding accidental and critical illness covers. Hence, simply avoid riders.

# Never heed the aggregators choice

Nowadays there are so many online aggregators. You may not know that they act exactly like insurance agents. Hence, never rely on their claim. Do your own research. If you are satisfied, then only go ahead and buy. Refer my post about the same “Beware of Insurance Comparison portals in India“.

# Know about Sec.45 of Insurance Act

After the recent clarification about Sec.45 of Insurance Act, the customer became king. It states “No policy of life insurance shall be called in question on any ground whatsoever after the expiry of three years from the date of the policy, i.e. from the date of issuance of the policy or the date of commencement of risk or the date of revival of the policy or the date of the rider to the policy, whichever is later.”

Refer the complete post at “Term Insurance-Claim Settlement Ratio no more a big criteria“.

# Review your life insurance cover

Buying Life Insurance of Rs.1 Cr or Rs.3 Cr is not a one-time affair. You must review your life insurance requirement at least once in the 5 years. If required, then you must increase the sum assured.

# Be cautious with premium payment

In case of term insurance, you have to be very cautious when it comes to premium payment. It is always better to opt for yearly premium payment and also if possible make it automated by the way of ECS. If policy lapses due to your negligence, then you have to undergo medical tests and all kinds of stuff once again. If there are any health issues, then the insurer may reject to renew the policy.

# Never go for Telemedical Examination

Recently one of my blog readers pointed that few Life Insurance companies insisting just Telemedical Examination by questioning about your health details in the phone (Refer-Can I buy Term Life Insurance with Telemedical Verification?).

It may be the easiest process for you and for life insurance companies. However, I feel suspicious of such kind of medical examination. Because in future insurance companies may find 100000 reasons to reject the claim on health ground.

Instead, I suggest you to go for medical examination. This will really clear the dust or doubt in your mind about future claim settlement.

Final Note:-The list of “Top 5 Best Term Insurance Plans in India 2018” is my personal choice and comfort with insurance companies and by verifying features. However, it does not mean that my selection will be the UNIVERSAL selection.

Hence, if you have a different opinion from my selection, then it does not mean you are buying a wrong product. My only concern here is not to shortlist “Top 5 Best Term Insurance Plans in India 2018”, but to give the gyaan which you must take into consideration before you shortlist your term life insurance.

HDFC standard life wale Mera claim settled nahin kar rahe hain

Dear Deepak,

Knock IRDA.

Hi Basvaraj,

My insurance advisor says to invest in because it pays 10% interest: https://www.iciciprulife.com/money-back-endowment-plans/assured-savings-plan.html

Few years back, my parents purchased a similar plan, but it only pays 3.3% because it is pegged to 50% of G-sec. Do you think this is a similar scam? Or is it legit?

Dear Niranjan,

After your parent’s experience, if you still believe your adviser, then only god can protect your money.

I have chosen ICICI Term plan, even before issuing the policy they are pushing other medical products. Now I have requested for the cancellation of my policy. Can I choose Max life or HDFC? Confused with my desicion please help

Dear Joe,

Both HDFC and Max are good. You can go ahead.

Sir a Query :

Lic tech term or Hdfc 3d protect

Lic : pros it’s Govt backed

: cons : it’s Govt and you know how govt offices work.

Hdfc : Pros : Private player so good services

: cons : Not Govt backed . Risk

So in your view what to do ??

Dear Rajit,

For me both are equally good and bad 🙂

Dear sir plz suggest Between hdfc click 2 protect and icici i smart term plan for 1 CR sum assured.Hdfc is covering upto 82 yrs nad icici upto 85 yrs. I prefer maximum term . Plz guide on the plan on the basis of services, financial strongness of company and customer relationship .i m very confused which plan i have to choose. Premium of icici is little higher than hdfc. Now i m 32 yrs opd. According to your post both plan are good still as per your knowledge and research help me to choose best one for me.

Dear Sashi,

Do you need life insurance up to the age of 80+?

Yes sir i want cover upto 80 + as i calculate my family will be depend on me upto 70 yrs on me

Dear Sashi,

So you will not retire up to your age of 70 years as they are depending on your income? If your family depends on 70 years of age, then why life insurance beyond 70 years of age?

Sir as i think if my death occurrs after 80 and if i have taken plan upto 70 to 75 age then only for 5 yrs my all premium will be waste of money. So benefit will be given to NOMINEE .so i thought i should go maximum term cover .plz guide

Dear Sashi,

Great idea 🙂 But what will be the value of the sum assured you are opting today to when you turn 70 years of age?

Ok sir i m clear about your thought so plz suggest me which company i should select for plan icici or hdfc and upto which age i should take plan

Dear Sahi,

If the age up to which you cover matters, then go ahead with the one which offers you at maximum age.

Dear Sir ,

I have two question plz advise i want to purchase HDFC LIFE CLICK 2 PLAN FOR 1 CR THEY HAVE OPTION FOR PREMIUM PAYMENT IF I PAY SOME MORE PREMIUM TO NEXT 28 YRS (UPTO 60YRS OF MY AGE)THEN AFTER IT REMAINING 22 YRS(From age60 to Aage 82) OF MY COVER I WILL NOT HAVE TO PAY ANY PREMIUM AND MY COVER WILL WE CONTINUE. SO PLZ SUGGEST THIS OPTION OF PRIMIUM PMT IA GOOD FOR POLIC

Regular prem is – 16807 of i pay upto 82 yes

Limited premium is – 22925 if i pay upto 28 YRS

Plz suggest according to time value of money.

Dear Vaibhav,

Do you need the LIFE INSURANCE up to your 82 years of age? Also, what benefit they are giving you? Go for simple yearly premium payment.

Sir My age is 32 yrs and hdfc providing coverage upto next 50 yrs that is upto 82 yrs of my age. Benefit is if i pay premium upto 82 yrs of my age then i have to pay regularly Rs 16807 yearly

But if i pay upto 60 yrs of age then i have to pay Rs 20925 yearly and REMAINING 22 YRS upto 82 yrs of my age no premium i will have to pay. So PLZ suggest which option is suitable accordingly to time value of money

Dear Vaibhav,

Whether the premium for both the options are SAME? NO right? Then it is up to you which one to choose. But for me, I choose the regular yearly premium rather than limited premium payment. Again asking you, do you need Life Insurance up to the age of 82?

Yes sir i want to cover upto 82 yrs. Because i think after age of 60-70yrs chances of death is more. So i want to cover myself upto maximum age. Please suggest me am i right for this decision.

Next is i show you premium calculation

Regular prm- 16807*50=840305

20925*28=585900

So difference is840305-585900=254405 so i m saving this amount and after age 60 i will have not to pay any premium upto age 82 .

Please suggest

Dear Vaibhav,

When you retire from work, then no one will be financially dependent on you, then what is the use of Life Insurance? Also, the sum assured you have opted may be peanut when you reached 70 yrs or 80 yrs of age. Now regarding the so-called DISCOUNT, there is a concept called TIME VALUE OF MONEY. Hence, don’t feel it as a BIG DISCOUNT for you.

Thanks sir for your speedy reply and guidance . Plz suggest HDFC LIFE is good for me or i should explore more companies like SBI, ICICI ,MAX LIFE etc in the point of view that there is no issue of claim arise in future.

Dear Vaibhav,

Go ahead with your choice and disclose all facts properly.

Sir at present i have term plan of lic of 50 lakh, but i have to switch to hdfc life so i should intimate lic to close the term plan or simply if i dont pay premium of lic automatically this plan will lapse. About closer of this plan should also mention in new policy or simply buy new policy.second i have also lic endowment plan this will also mention in new policy document. Please guide

Dear Vaibhav,

In case of term life insurance, you no need to inform to existing life insurer about the closure. Also, while buying the new life insurance, if you are sure that you are closing the existing life insurance, then you no need to mention it while proposing.

I have 1cr Term plan from Eidelweiss Tokio for last 3 yrs, at a premium of Rs 15340/- per year. Now I am 34 yrs old. Is it ok, if I shift to low premium Term plan like Aegon? And discontinue from Eidelweiss?

Please suggest.

Thanks. regards,

Somnath

Dear Somnath,

If the difference is huge, then you can shift and cancel the existing once you receive the new policy in your hand.

Dear Sir, Thanks for the useful post. I wants to know is their any rule from Irda that if someone pay 3 consistently premium to any company then company has no right to cancel his claim.

Dear Ashit,

I already mentioned about the same in above post (Sec.45).

Dear,

Could please explain about accident rider benift? Does all term insurance cover any kind of death I meab natural/accident if so why there is additional accidental rider benift?.

Dear Makesh,

In the case of normal Term Life Insurance, assume you opted for Rs.1 Cr Term Life Insurance and death happened due to normal or death, the nominee will receive Rs.1 Cr ONLY. However, along with this normal cover, you have opted for an accidental rider of Rs.50 lakh and if death happened due to accident, then nominee will receive Rs.1.5 Cr (Rs.1 Cr normal life coverage, and Rs.50 Lakh Accidental Death Coverage). Hope you got the clarity.

Thanks for the response. So you suggest rider benift is not required due it will increase premium right?

And can you suggest me the best term policy which has low premium for 1Cr with good company.

Dear Makesh,

I am not suggesting to include not because of premium will increase. But you can buy such riders separately which will be exhaustive in features than these rider benefits. Regarding suggestion on term policy, I have already mentioned my choices in above post.

sir, i compleated 50yrs, my annual income is around 7 lac .i have paying nearly 2lac for insure [different company most of them investment basis all purchased through agents .without any knowledge and by obligation.

now i want to buy pure term insurense which can protect my family .i am a healthy man how i buy really good policy? aditya birla,max ,or you suggest good policy for me.

Dear Hamsaraj,

Wait for my new post regarding the same.

That’s good news. I hope your fresh post soon. I want to buy a policy (age 42, income 6 lac) in this month. I will wait for your post to help me to take write decision. If possible send alert to my email ID.

Dear Paresh,

Thanks. You can subscribe to my posts (Widget is available at right-hand side of the post for a desktop view).

sir,can i buy two term insurense from two different company?

Dear Hamsaraj,

Why not?

Nice post Basunivesh !

People like you are very much needed, who provides Fact based Financial advice with a holistic Financial Planning orientation.

Dear Krishnamohan,

Pleasure 🙂

Hello Mr. Basavaraj,

I just wanted to know which of these two good to proceed with I.e. LIC E-term or ICICI Prudential iProtect Smart?

Because i heard ICICI cheating when it is coming at the time of claim settlement and make the people to suffer with respect documentation.

in other part, LIC premium is costly so pls advise based on your previous or others experiences.

Dear Anand,

We can’t judge the company just because one or two cases have issues. Also, we don’t know the reasons behind rejecting the claim. Hence, it is unfair to brand any company BLINDLY. Choose the one which is comfortable to you. For me both are equally good and bad.

Dear Sir,

Very nice and informative piece of work by you..thanks!

Kindly advise on two –

1) Purchasing term plan through online insurance comparison portal is ok?

2) Which is better mode of premium payment – month / yearly if both to be selected through ECS?

Regards

Dear George,

1) NO. They may push the products where they have more earning.

2) YEARLY.

Hello Sir,

I wanted to know when a claim gets rejected? From other blogs that I have read, if I don’t provide correct information in my proposal form then during the claim settlement time it causes an issue. For. e.g. If I am an occasional smoker and in my medical test I was found as a smoker(so I paid the premium of a smoker), then during the claim settlement time, Would that create an issue during the claim settlement as in my proposal form I had mentioned myself as a non-smoker?

Dear Raj,

If the policy was issued under Smoker category, then no need to worry.

Hi Basavaraj sir,

Which one would you prefer between Aegon, max and ICICI for term insurance and considering base plan without any add-on in all 3. I know by premuim wise Aegon is less expenesive, but I would like to know which company among above mentioned is most reliable or hassle free while settling the claims?

Dear Manoj,

All are equally good and bad.

I am going with max sir

Thank you

Hi Friend. it is a very nice article and informative. I took Aviva iTerm Plan for 50L cover when I was 35 years old and the term was 35 so the cover was till my 70Yrs. So now I understand the fact. Now I am 42 yrs old, and I feel I should have taken for 1Cr cover, so can I go ahead and take another 50L cover till my 60 Age? Please advise.

Dear Prabhat,

Why not?

sir one person take different comm-penis terms policy’s by or not my yearly income is 900000/- like icici and tata aia 7500000+7500000 by a two different policy’s plz answer me sir

Dear Parashuram,

Can you elaborate more?

I purchased the Sbi smart plan

3lac for 5 years the agent says you will get annual payment on year 6

Expected returns 8-10%

Is this a risky policy

Also it says

This is a Unit Linked Pension Plan which comes with a minimum Guaranteed Maturity Benefit of 101% of all premiums paid in case the funds do not give desired returns.

Do agents earn more commission on selling deferred plans

Is it better to buy guaranteed plan

Dear Ramesh,

NO RETURNS are guaranteed on such plans. Also, if your time horizon is less than or equal to 5 years, then NEVER touch equity products (whether it is ULIP or Equity MF).

It is Sbi retire smart plan

3 lac each year for 5 years

Then take annruity from 6

Is it better for me to change to guaranteed plan

Dear Ramesh,

I can say one thing, NEVER COMBINE INSURANCE WITH INVESTMENT.

Is the amount of money you invest say in a single premium plan guaranteed if the company

Collapse

Dear Ramesh,

They can’t shut their door and run away. It is highly regulated.

Say this happens is the money guaranteed by

Goverment

very informative views, sir, thanks, i was abt to buy lic plan but will give , aegon also a chance , thanks again

sir, i want term plan for myself, my annual income is 1.80 lacs approx, which company should i apply , since many private company wants 3 lacs as minumum annual income, n what should i prefer online or ofline policy ,

plz guide,

Dear Vishal,

You can buy the one as per your choice from the above-listed companies. Better to go for ONLINE.

Hello Mr. Basu,

I am 29 and I have got Max Life insurance just 6 months back. Now have got to know about TATA AIA Sampoorna Raksha plan with limited 5 years of premium payment and coverage of 40 years.

The TATA AIA premium for 5 years is nearly 2.3 times more that Max Life’s premium which have to continue to pay till my age 60.

I just wanted to know, if it is wise to switch to TATA AIA considering all the above factors OR stay with Max Life.

Thanks.

Dear Mahesh,

Whether you can afford such 2.3 times more premium? If YES, then go ahead.

Hi Mr. Basu, thanks for this very detailed info to choose the term plan by individual. I have got a point of thinking in riders element where i would differ from your blog. Why to choose standalone critical illness rather rider to term plan, when you get your premium fixed & less than from standalone? For example Maxlife Term plan CI Rider for 20 lakhs cost to 6k & standalone optima vital would cost you 9k & the same will keep on increasing. Pls correct me if my pov wrong & advise.

Dear Ritesh,

What about the other features? When you choose riders, they come with certain restrictions. Please cross check once again.

Siri am a state govt employee in Raj . Me ek term insurance plan Lena h me isme bare me kuch bi nai Janta mere poche meri family h mujhe ap suggest kare ki mujhe ye Lena chiye ya nai or konsa plan best rahega or kitna amount ka meri age 33 h thanks

Dear Lavkush,

I already shared my views in the above post.

Sir would like to know how is Edelweiss Term Insurrance Zindagi Plus Plan… I’m 49 years now…Pls help

Dear Lalit,

I usually not recommend the new entrant.

Hello Basavaraj,

Thanks for this detailed comparison of the best term insurance companies.

I am looking to buy one and had narrowed own on Aegon and then i also looked at Max Life.

As of today, i see that MAX life premium is the least.. Both have good settlement ratio, however it is not the most important factor as per you and i am inclined to think the same too..

The advantage of Max life from what i see is that, it comes with an option of paying the premium for only upto a retirement age of 60 years though the coverage term remains the same as we choose.. (Max upto 80 years)..

So we do not have to pay the premium for the next 20 years.. if all goes well 😉 ..

No doubt, yes the annual premium for this option would be higher..

Almost like 1.4times the normal one..

But overall you would still save quite some amount as you are paying for 20 less years.. (Assumign i opted for 80 years and paid for only for upto 60 years).

My question to you is… Should i go ahead with this option? Seems very lucrative.. However wanted your opinion on this..

Don;t know whats in store in the next 20-25 years.. I am a little skeptical and don;t if some of these condition’s change later and they do not honour it etc..

Do you see any dis-advantages in going with this option? or Do you see any catch here?

Really appreciate your reply on this.

Best Regards,

Munna

Dear Munna,

Do you need Life Insurance during your retirement?

Sorry i quite didn’t get that..

I do not have any life insurance and not plan to have one..

I was looking only for pure “Term Insurance Plan””..

I would like to invest on health insurance though..

Dear Munna,

Insurance is not investment 🙂

No doubt 🙂 … I didn’t mean to say invest.. (wrong word used) .. 😉

I would rather spend money on buying good health insurance policy than going for life insurance.. is what i meant..

Term insurance is definitely not an investment for myself.. but for sure it will help and support my family in the case of an unfortunate event..

So coming back to my original question…

Do you suggest going for Max life and pay the premium only till the age of 60?

Appreciate your response and the amount of time you spend in patiently answering even the silliest questions.. and guide people here.. and more so at no cost.. Rarely do we find such people.. Keep up the great work..

Dear Munna,

I am asking you same question. Do you need the Life Cover during your retirement age?

Hmm…. well it depends on various conditions is what i feel..

– Are You in Debt ?

– Are Your Children and Spouse Self-Sufficient?

– If i retire and no longer work to make ends meet, you probably don’t need it

So honestly am not sure if its really required..

But yeah maybe assuming these things are not bothering too much then yes don’t need a Life cover on retirement..

Your opinion would definetly help me weigh this.

Regards,

Munna

Dear Munna,

Financially you RETIRE only when you achieved FINANCIAL FREEDOM. When you have FINANCIAL FREEDOM, then LIFE INSURANCE is not at all required (whether it is today or tomorrow).

Hello Basavaraj,

Can you please let me know your opinion on this..

Should i consider the option of paying the premium till the age of only 60 ?

Also, another thing i noticed with Max Life is they are only asking for Telemedical Verification..

Can we insist them on a full medical verification instead? I will be calling them to check on this..

However if you have the information please do let me know..

Thanks,

Munna

Dear Munna,

I think you are unable to understand the question I am asking you. Life Insurance during retirement is WASTE. I am not sure why you want it up to 80 years of your age. Better to insist full medical examination.

Thanks a lot Basavaraj …

Yes i get your point and agree you don;t need a life insurance during retirement.. The concept behind that is by retirement age we should ideally be free of any liabilities, financial burdens, children’s are all grown up and on their own and things like that..

But life is full of uncertainties and hence we always see whats the backup plan if in-case something doesn’t work as planned..

While i was evaluating these different polices between Max life and Aegon i just found this option and then the thought/greed kicked in i guess 🙂 ..

Pay only till 60 years, but then coverage till 80 or more than 60 years… and looking at the premium i would have paid for opting only for 60 years Vs paying slightly more (ranging between 7-11k per year based on age) premium for the same period and getting an extended cover for another 20 years was tempting..

But for sure i was not looking for 80 years of coverage..

And that’s where my question was to you.. to help me understand..

I just feel these are some marketing tactics used by companies to play around/lure people in paying more premium…

Again thanks for your help..

I will insist on full medical checkup to be sure nothing is hidden and everything is in records..

Regards,

Munna

Dear Munna,

Also the point you have to consider the value of today’s sum assured you are opting to the value when you are 60 years of age.

Yep.. that’s not going to match or be enough with the kind of inflation etc …

I am planning to go ahead and but one for the period of 65 years.. (just pushing my retirement to that age :))

I had narrowed down on Max life.. Do you think i should again check between Max Life and Aegon?

Thanks,

Munna

Dear Munna,

Now you are on right track 🙂

Daer Basu sir , I want to take TP and my age is 35 smoker , I have not any major illness except one time nose bleeding due to high BP . Should I mention the same in application form for TP… Thanks

Dear Manjit,

Yes, you have to mention it without failure.

Hi,

Thanks for this elaborated comparison, I want to know as you said to stay away from riders, does it also mean to stay away from waiver of premium rider on disability and critical illness ? I am confused between HDFC, ICICI, Max & AEGON.

HDFC – Highest Premium because of WOP rider for CI & Disability

ICICI – Less than HDFC because there are no WOP riders

MAX – WOP CI rider available but for 35 Years term or 70 Yrs of age – premium almost same as ICICI

AEGON – Least premium in vanilla product but not sure about company’s reputation

Should I go for vanilla product or with WOP rider.

Thanks

Dear M,

You can opt for a premium waiver but not critical illness rider. You can buy accidental or critical illness policies separately. Regarding choices in the companies you mentioned, it is completely up to you to decide.

Sir plz help

Dear Suman,

Regarding?

Dear Sir,

My husband is 32yrs and non smoker.

We don’t have any kind of insurance rather than a star health insurance.

We are planning that we will only do a single insurance plan which is a term plan.

But unable to find the goodone.

I am confused on Max and Aegon.

Plz suggest,

as Aegon having maximum maturity age which is I think is good for term plan

but Max having good vintage and name in the market.

Sir, plz short out my confusion.

Dear Suman,

For me both are fine. But do you need life coverage during retirement age? As per me, NO. Hence, go for Max Life.

Thanku so much sir, it will really helpful

Sir Which is best Term insurance plan for better Advantage benefits.

plz suggest company plan

age 30

Term 40 year.

Dear Arun,

They are already listed in above post.

Sir, excellent article.You have simplified my plan to go for a term insurance for my daughter. My mind is clear now. Thanks.

Dear Rajam,

Pleasure 🙂

Sir,Thank you for your explicit and detailed coverage of term insurance in your article.I was in great dilemma whether to go for Aegon iTerm insurance for the past three months.In fact I directly received a quote from Aegon Life Insurance.Now I have decided after reading your article. I seek term insurance for my daughter aged 32,drawing Rs7-8 lakh annually.Suppose my daughter takes iTerm plan policy for 1 cr and she pays annual premium for 33 years(upto 65 of her age) ,will there be coverage for another 35 years till she becomes a centenarian if she is healthy and everything goes well? In other words,how to get cover for 100 years for the given data of my daughter under Aegon iTerm plan?

Dear Rajam,

Do you need coverage post retirement age?

Yes,upto 100 years, sir.

Dear Rajam,

May I know the logic behind having life insurance cover up to 100 years?

Sir, suppose she takes policy term upto her age 80 years, the policy matures ,no maturity amount will be given under term insurance, if she survives beyond 80 years. Suppose she lives beyond 80 and and goes to God in 90 years of her age,I want that she must leave behind the cover amount to her nominee. That is why I want life option under Aegon iTerm policy.

Dear Rajah,

What will be the value of the sum assured when she be 80 Yrs or 90 Yrs?

Hello sir, I got term insurance policy from Max life for lumpsum amount of 50 lakhs with critical illness rider of 15 lakhs. I have a past medical history of brain stroke. After medical tests, Max life rejected my application citing medical history as the reason. What options do I have of getting term insurance from other companies. Also I bought critical illness rider as I thought that the rider cost would be the same till end of policy term. Is this the correct way to go about critical illness rider or do you recommend stand alone critical illness policy. Please give your valuable thoughts on above two issues. Thanks sir.

Dear Navin,

“What options do I have of getting term insurance from other companies?”-Hard to say because it mainly depends on underwriter decision. Hence, you try your luck with a different insurer. It is best to choose a standalone critical illness.

Hello sir, my special thanks to u, i have been through ur article it is so informative about insurance plans and i was able to select one ( ICICI i smart). I am 30yrs old earning 15l per ann, also want to invest some amount like savings for future gains. Please enlighten as to what is d better way to safely invest. Thank you

Dear Hari,

Thanks for your kind words. Regarding guiding you for investment, it is a hard part from my end to guide you without knowing much about your financial life.

Hi,

I’m planning to take term insurance. i see huge difference for smokers and non-smokers. i’m smoker and planning to take term insurance as non-smoker to minimize the premium since as per IRDA SECTION 45 if the policy completed for 3 years there are no issues in claim settlement process even though if i hide material facts.

2) Kotak mahindra is offering term insurance for 1 crore without medicals so i’m planning to take that since i’m aware of sec 45.

3) As per sec 45 insurance companies have a right to do medical tests within 3 years but not sure how kotak is offering term plan without medicals.

plz let me know u r thoughts

Hi Sir,

I am planning to buy term insurance from my mother(Age 48), she has ITR’s for last two years earns upto 3 Lacs.

My questions are

1)Last two years ITR’s are enough to get the term plan?

2)Planning to buy till the age of 85(I will be 60 at that time),is it wise decision?

Dear Janakiram,

They need usually around 3 years ITR. But cross check yourself whether someone financially dependent on her? Is answer is YES, then go ahead and buy term life insurance.

great sir, very quick response and suggestions.

i will check with insurers.

Hi i hav purchased term insurance from maxlife with life age 80 years of mine nd payment term till 60 of mine age. I mistakenly decleared that i hav not taken leave for continuous 10 days in past one year i informed them through mail still they issued the policy without correction nd mentioned that they hav not done any medical …they told that medical at age of 32 not required. After 25 days they hav not changed my declearation.. today on friday when i called again for correction they told the concern person is onleave will call me back on monday but when in evening at 7 o clock i asked then about the procedure to close the policy immediately with in 5 min the sent mail that correction has been done.

The are not doing physical medical. Pl. Suggest me weather i should go for it or change the insurer.

Der Swamit,

If your concerns are resolved, then better to continue.

Dear Basavaraj Tonagatti, Your article really helped me to decide something. I am choosing a Term plan from ICICI only till 60 years (Retirement age). Only the life cover without any add ons.

Pay term is 10 years, as i feel i do not want to pay higher premiums / till my retirement age. Believe i can increase my policy term & life cover in future (Yet to get this confirmed from the insurer).

Is my decision wise ?

Question 2 – I shortlisted 2 insurer (HDFC,ICICI) only because of their pay term is reduced. Ex (5,7,10 years)

Whereas Max life can have pay term only as low as 30 years & Aegon cannot reduce the pay term at all. This was the only reason to avoid both the insurers.What would you suggest ?

Thanks,

Dinesh kumar N

Dear Dinesh,

You are not allowed to increase policy term and cover in the same plan. You have to buy the new one either from the same insurer or different. You can go ahead with your choices.

Dear Basavaraj Tonagatti, Thanks for your response.

But i want to re-evaluate on these 2 points.

1. My age is 30, i think to choose a term plan only till 60. In case of uncertainity before turning 60 years, this will help my family. I do not want to have the term till 80 / 85 of age as i do not think this as a wealth which i can leave it to my familty considering a natural risk might occur before 80 / 85 of age.

On the other side, i also think like if everything goes as normal and this policy becomes void at my 60. if i tend to opt for a new risk policy considering to create a wealth out of it. The premium would be higher / unaffordable. Finally when comparing

Life cover – 2 Cr

Policy term = 50 years, Pay only for 10 years = Annually 50696

Policy term = 30 years, Pay only for 10 years = Annually 27810

If i choose the term as 30 years, after some 10/20 years considering the factors at that time and if i intend to go for a new term plan. Will that be correct / i have to regret why didnt i decide my term properly? this is really burdening me

2. I have short listed the insurer based on CSR, further filtered based on reduced Premium pay term (5,7,10 years only) and finally choosing the lowest premium insurer.

Just by looking at the cummulative value of paying premium for 30 yrs and 10 yrs i find paying premium for 10 years is low and adviseable. Do you have different thought on this ? Like pay lower annual premium for 30 years as this is comparitively better.

I am really sorry for writing such a detailed question and a heartfelt thanks for your upcoming and previous responses.

Thank,

Dinesh Kumar N

Dear Dinesh,

1) Whether you go for 30 years or 50 years, after 10 or 20 years, in both the cases, if your Life Insurance needs to be increased, then you have to buy one more plan. Then in what sense it makes difference?

2) Paying for 10 years is cheaper for you and better option for the insurer. Because they receive the advance payment from you which will not be the case with regular premium paying policies. Hence, cheaper for you. If you feel best, then go ahead and no harm in that.

Thanks a lot for your responses.. Your article and responses really helped me to decide something which fits me.

Thanks a lot.

Dinesh

Dear Dinesh,

Pleasure 🙂

Very nice article youbhave written. I have a confusion if you help me out. Icici Pru Iprotect smart offers payout for 34 critical illnesses. Should this option be taken? If not how otherwise can i seperatly cover such a risk. I was also looking at Tata AIA sampoorna suraksha plus as they have a short premium paying term with premium return option. Would this be wise?

Dear Tejas,

Buy separately rather than clubbing with Life Insurance.

Hello sir,

I want to know difference between term insurance and health insurance. Is taking health insurance recommended. I am planning to buy max online term plan. And which health insurance is best. Please recommend any.

Dear Ashish,

Term Insurance covers your life risk (death). Health Insurance covers your hospitalization expenses.

Dear sir, very nice article. I am 42. I want to buy a term insurance for 1 crore. My monthly salary is 60000. Which plan will be best for me? Please suggest.

Dear Vaibhav,

My choices are already mentioned in above post.

I have been researching term insurance for a week. Yours is by far the most helpful site I could find online. Thanks

Dear Rohit,

Pleasure 🙂

hi, very nice explanation and guidance

Dear Abhijit,

Pleasure 🙂

Hi Sir, Thanks for sharing this information……very Helpful…….

Dear Jagadeesh,

Pleasure 🙂

Sir thank you for sharing your thoughts with us.

Dr.Varun,

Pleasure 🙂

Hello,

As an NRI, do I need to cover the cost of the medical test if done locally for term plan?

Thank you

Dear Ravi,

It depends on company policy.

Hello Basu sir,

Recently got a change to visit the Edelweiss website for Term policy, and noticed that the premium is similar to the top 5 suggested by you. Additionally I saw an rider which I haven’t see in any other companies. Details below on the rider for which the Premium was just 250 rupees additional per year :

“Better Half – Better Zindagi – A Never-Seen-Before feature. The Edelweiss Tokio Life – Better Half Benefit gives an extra cover to your wife in case of your unfortunate demise. Hence, your children and parents can have enhanced protection.Whether she is a housewife or employed, she deserves the utmost care.

Upon your demise your nominee will get the sum assured you have selected.

50% of your life cover (max up to 1 cr.) will start in your wife’s name and she won’t have to pay any premium.”

PS : I am 33 now and already have a 60 year term with MAX for 1 Cr started last year.

My questions are :

1) Please shed your thoughts on this rider benefit ?

2) Do this rider seems genuine ?

3) How credible is this Edelweiss company?

4) Can I surrender the above policy and start a new one Edelweiss with the mentioned rider.

Kindly provide your suggestions like every time you do 🙂

Thanks for you patience in reading the bit long question.

Dear Balaji,

If she is not earning, then after your demise or now also WHETHER TERM LIFE INSURANCE IS REQUIRED FOR HER? These are fancy games played by insurers. Just ignore it.

Hi Basavraj

I have a difference of opinion here. Even if wife is a non earning member, there would be COSTS, in case something unfortunate happens to the wife. Such costs could be like employing a full time domestic help etc.

So I feel that a small cover for wife is also required.

Dear Sameer,

So as per you, you can’t afford the maid if something happens to your wife? God BLESS YOU. Go ahead as per your wish. You can afford your wife’s current expenses. But you can’t afford full-time maid cost if your wife not here. What a logic??

Dear Sir,

Thank you for the great article. My question is – if I need income protection in case I am unable to work due to disability/critical illness, which rider should I select ? I am not worried about the waiver of premium, it is mainly receiving monthly income if I cannot work.

Also one doubt – you mentioned general insurers can cover accident/critical insurance. But wouldn’t it be easier to combine everything with one provider ?

Dear Hemant,

There are no such income replacement insurance as of now to cover your job loss. However, if the income loss is due to disability or critical illness, then your accidental and critical illness covers such income loss.

Dear Sir,

My Age 56 Male and i am diabetic patient and i want to buy 50 Lac Max Life term plan & company charges total 3200 pm for 50 Lac so its good or not for me .

Or should i go with another insurer?

Dear Karan,

It is you to decide whether it is good or bad. But in my view, it is a better deal.

suggest best term insurance policy for NRI’s

Dear Raju,

You can approach the same insurers (mentioned above) with your status of NRI.

Hii Basu Namaskara..

Thanks for the valuable blog, i was just looking after the term insurance on line and visited the some policy sites to compare the premium , they are behind day and night calling on phone contentiously and convening me to buy policy of their best.

this blog has helped to decide to select the insurer from the top list of companies.

Thank,

Arvind Akki

Dear Aravind,

Pleasure 🙂 Take your own decision but not bend to their terms.

Hi Basavaraj,

First of all I would like to say Big Thanks for providing very good information and also for your patience to answer all our queries.

My query is : I am about to purchase ICICI Pru Term plan for tenure of 15 years. Can I renew it for 10 more years once 15yrs completed ?

Thanks

Sashi

Dear Sashi,

Once the term of 15 years is over, then if you approach for buy, then it is a fresh buy for you. You have to undergo once again all scrutiny like medical examination and income and existing coverage. Then only based on that day’s situation, they issue the fresh policy but they not RENEW it.

Dear sir, for a quote of 2Cr cover for 25 yrs for a 36 year old male, I was quoted 21500/- by ICICI (Pure Term Life, no other riders – iProtect Smart). However, after the medical tests, they are claiming Hba1C is slightly higher and so is the BMI (on the higher side) hence they want to increase the premium to 35700/-. On arguing with them, they asked me to redo the HBa1C alone and if the value was lower, they were willing to reduce the premium marginally ( havent told me how much). This steep escalation in premium in my view is unjust. What would be your advice – should i ask them to cancel (the policy is yet to be issued) or will this be the same with any other insurer? Thanks.

Dear Nav,

If you have the said health issues, then the result will be same even if you go with other insurers (except there may some differences in hike).

Thank you sir! Ironical that they wont reduce the premium if the policy holder’s BMI reduces after an year 😀

Dear NAV,

True and sad part also 🙂

Hi Basu,

Your articles are creating Social Awareness. Upon seeing this article, i chose ICICI. I went to their Branch to enquire the plans and details as i got confused online. There seems Life, Life Plus, Life & Health, All in One are the plans they mentioned and i saw in their website as well. Here the Base Plan is Life that provides Death Benefit + Terminal Illness + Waiver of Premium on permanent disability.As you said in this article, i could see they advertising for Riders. The things is i could not find plain Death Benefit Plan. The Starting Plan is “Life” only. Could you please comment on this ? Also i could see they are not interested in Medical tests. When i insisted, they said like two Tests Blood and Urine test will be conducted at Home. As i am not aware of what are the Tests that need to be conducted, i just skipped and thought of getting your thought on this before proceeding. Could you please say what Tests should/will be conducted for the Term Insurance ? And Will they do before or after Paying the first Premium ? Because i felt like they will come home to Test only after First Premium Paid. I know its little bit lengthy, sorry about that my friend.

Thanks,

Shanmugam

Dear Shanmugam,

The plain vanilla product is LIFE option (if I am correct). If they are not so eager about medical test, then simply skip this insurer and opt for someone else. Regarding the medical tests, it depends on sum assured you opted, age and other conditions seen by the insurer. Hence, it is hard to generalize the things.

Hi Basu,

Thanks so much for your kind and prompt reply. When i enquired about the insurance, they mentioned 2 things which i am not able to differentiate clearly even after Googling it – Death Benefit and Accidental Death Benefit. For Life Plan, only Death Benefit is there but for Life Plus, Accidental Death Benefit is the Rider is also included. Can you please give your thoughts on this Death Benefit and Accidental Death Benefit ? Thanks !

Regards,

Shanmugam

Dear Shanmugam,

Assume you opted for Rs.1 Cr term life insurance and also opted for Death Benefit. In that case, if death occurs due to any circumstances (inclusive of accidental death), your nominee will receive Rs.1 Cr ONLY. However, in case you opted for Accidental Death Benefit, in case of normal death, your nominee will receive Rs.1 Cr. However, death occurs due to the accident, then Rs.1 Cr (Basic Sum Assured)+Accidental Death Benefit Sum Assured is also payable to your nominee.

I am 34 yr old, annual income is 4 lakh, kindly suggest me one among five, Also kindly let me know the total SA.

Dear Santosh,

For me all are equally good and bad.

i have term insurance policy of rs 500000 upto age of 60 yrs in LICI.now i want to increase the 50lks to 1 cr. ..is it possible ? if yes hot to process?

Dear Sintu,

You are not allowed to increase the same. You have to buy the fresh one by following the rules applicable to new policy.

Hi,

I am looking for a term plan of 1 cr for cover upto age 75+ age

I want the payment should be in Single pay or Limited Pay(5-10 years).

If it include any additional options then better.

Would you suggest me any term plan name.

Dear Goldy,

Do you need life insurance up to your 75 years of age? May I know the reasons behind choosing single pay or limited pay?

I am working that in private company.As u know is no guarantee of jobs and currently i am ok with single pay or limited pay

Goldy,

But why you need life insurance up to 75+ years of age?

No any specific reason.I just compare the amount of 70 and 75 year payment term and there is not a big difference.According to you for how much age i should take term plan and suggestion for term plan

Dear Goldy,

Buy life insurance up to working age. During retirement, life insurance is not required.

Suggestion for term plan name.

Dear Goldy,

They are listed in above post.

What is the harm if someone gets insured for 80+ years & someone pays a few thousand more every year and the family after his death gets the full insured amount whatever may be its value that time . Instead of wasting the full premium paid till the age of 60 years when most of the human beings are alive. Isn’t it an investment for our family if we take the insurance for 80 + years ? As such if we die after 60 years we do not have to pay further premium.

Dear Sudip,

If your intention is to get the benefit at any cost, then the best idea is to buy it today and suicide ourselves after 1 year. Less premium paid, your family will receive the full sum assured right?

Very silly answer from a matured person. My intention was please do not misguide people by stopping them from buying for more years as the premium till 60 years will not go for a waste then. Its not my intention to get the benefit at any cost but everyone over here wants to benefit . At the end its the individual’s decision ofcourse.

Dear Sudip,

“At the end its the individual’s decision of course.”-GO AHEAD!!

I have very little knowledge about the insurance policies and claims, however I feel, during the retirement if any unfortunate happens, the nominee will get the sum assured, which is still a good deal for the dependent. Though the dependents are settled by our retirement age, the SA will certainly make a huge difference to their life. What you say?

Dear Chiranjeevi,

If you feel the sum assured you opted today will have some VALUE during your retirement, then go ahead.

With due respect i would like to ask you as i have seen many times you have asked others “do you need insurance till 70 or 75 years.” What i feel if we are paying yearly for 30 or 40 years why not instead keep it till 80 or 85 years by paying few thousands more every year and in that case either my wife or children someone will get the money once i die whatever the value maybe at that time. As such if i die before that age the premium will not have to be paid. In most of the cases till 60 years everywhere lives and all the premium paid goes for a waste. What do you say about this …i pay few thousand more yearly as an investment for my family.

Dear Sudip,

“WHATEVER VALUE MAY BE”-Then go ahead what doubt you have?

Whatever the value of 1 or 2 crore would be at that time i meant , but the value of premium one would be paying after 30 years would also seem like peanuts during that time, so i do not think there is any harm to get back those 2 crore even after 30 or 40 years where after inflation also that would be quite an amount. I do not have any doubt but was not satisfied as you are guiding people only to take insurance for more than 60 years. As an individual i feel the premium which i paid should not go waste and someone in my family needs to get it back.

Dear Sudip,

If you feel it is worth to have life insurance (when you have no financial dependents during retirement), then go ahead. The basic idea of life insurance to buy is when you have some financial dependents on you. Rest left with you.

Dear Sir,

Great post! I see that you are suggesting to stay away from riders. There is (a) premium waiver and (b) income replacement in case of disability due to accident and due to critical illness.

1. When you say stay away from riders, which one did you mean? Just b or both a & b.

2. Also, if we don’t take these riders, what kind of general insurance provide disability and critical illness cover? I assume it’s for the income replacement. Is there any long term plan available in such insurance? I see around Rs.20k premium for 3 years for 20 L coverage.

3. Slightly off the topic – Apart from Term insurance, Health insurance and General insurance (for income replacement?). What else should we plan for? Pension plan, Child education, etc. Could you please share your thoughts on these?

Thanks in advance.

Praveen

Dear Praveen,

1) a is optional to YOU and I am saying here about b.

2) You can buy separate accidental insurance from a general insurer or standalone insurance companies.

3) Three insurance are mandatory (Life, Health and Accidental), then don’t buy any product which is offered in the name of PENSION or CHILD plans.

Thank you sir for the quick reply. I am comparing the critical illness rider that comes with HDFC 3D Life with HDFC Ergo (randomly selected HDFC Ergo just for comparison purpose). For 10 Lakhs coverage, Ergo charges (15 diseases) Rs. 8260 annually. The rider that comes with HDFC 3D Life covers 10L (19 diseases) at Rs. 4464 per year. Premium is less and it’s guaranteed for the number of years we choose now. Where as the Ergo in this case has a risk of non-renewal or increase in premium for renewal.

Could you please help me clarify this confusion – why a separate policy is better than rider in this case? What’s the advantage of having a separate policy?

Thanks,

Praveen

Dear Praveen,

I will not go in deep. But apart from the coverage of diseases, you check it out the features. There are few other insurers also who provide more number of coverages than HDFC.

Hello Sir,

Its going to be detailed query, so bear with me.

I’m 36 yr old ( Non-Smoker) and planning to buy a pure term insurance. I noticed that only HDFC gives the option of choosing our own policy repayment term.(i.e., if my policy is for 24 yrs (till my 60), then i can either choose to pay yearly premium for 24 years or even pay them within 5 yrs or 6yrs etc. I can choose my premium payment term.

Obviously lets say if choose to payout my premium in 14 years (i.e.,by when i reach 50 yrs) my yearly premium tops at Rs.22k, which would be 22000×14 yrs = Rs 308000. But if i chose to pay my premium yearly for 24 years(i.e., till its maturity and my 60 yrs of age) my yearly premium would be Rs.15900, which would be 15900×24 yrs= Rs.381600.

So if i pay yearly for 24 yrs, i would be paying an extra Rs.73,600(i.e.,381600-30800).

I checked other providers and they dont provide the option of choosing our own lesser premium paying term. For eg. ICICI and Max both give an option called limited paying term and that term is fixed by them. In ICICI’s case for 24 yr term plan its fixed at 18 years. I can choosing anything lesser or more years to payout my premium.

My question is.

1.Is it good to choose 14 years as my paying term , Considering i’m saving Rs.73,600 in total money by paying out the premium in 14 years for a 24 year term plan? ( i.e., i know after paying out my premium in 14 years i cannot claim tax relief in Sec.80C, i can only claim it till i’ paying it). So considering both is it wise to pay out my premium in 14 years ?

2.Or would you advice me to pay it out yearly for 24 years, so even though i’m paying more premium on the whole, i can claim tax relief under Sec.80C for 24 years(i.e.,till my 60 yrs) ?

Please confirm

Thanks once again.

Dear Venkat,

1) Do you feel you are saving? They are giving you a discount because you are paying in ADVANCE. Hence, don’t be in the wrong belief that they are giving you some discount. However, if you feel this comforts you, then go ahead.

2) It is up to your comfort and affordability option.

Hello Sir,

I have become a big fan of yours for giving neutral and excellent articles on all areas of finance.

I am 39 years old and sole working member of my family with a wife and a 5 year old kid.

I am finding that for a 1 Cr. coverage till 65 Years the Bajaj Allianz Shield plus plan is giving me additional benefit of 1 Cr on Accidental disability and Premium Waiver . I could not find any other product with this benefit and I find their accidental disability rates very competitive compared to general insurance coverage as well. Firstly I did not find anyone giving a 1 Cr accidental benefit and the lower covers of 5 lac or 20 lac are as or more costlier than the 4k or 5k I may be paying compared to the cheaper plans.

Will be great to hear your opinion on this

Can you tell me any other equivalent products?

What could be the drawback/loopholes in going for this product or Bajaj Allianz group in general?

Dear Anshuman,

I am of the opinion that to not of clubbing Life Insurance with Accidental Insurance. However, if you feel the premium is cheaper and features are good, then go ahead. But also look for the features of Accidental rider details properly and then take a call.

Thanks Sir

Any general feedback on Bajaj Allianz?

Dear Anshuman,

For me all are equally good and bad.

Hi Basavraj Sir

I have taken ICIC Pru. Term plolicy last month without Medical from agent…. can i ask my agent to do medical now?

Dear Amol,

Now why they do the medical when the policy is already issued?

Hello Sir,

Should we buy incremental Term Plan or normal Term Plan.

If we take incremental term plan, then does our premium also keeps on increasing.

Please explain.

Thanks

Saurabh

Dear Saurabh,

Incremental plans are best rather than normal. Because it takes care of inflation and also you no need to buy different plans in future to enhance your life cover. Yes, the premium will be definitely high in incremental term plans.

Sir,

Please suggest on LIC on my lic policies, i want to invest in mututal fund and want to take a term plan now.

Commencement Date -January 2010

Sum Assured – 500000

Plan – Jeevan Anand

Policy Term -21 years

Premium -25028

Premium Payable -Yearly

Commencement Date -May 2011

Sum Assured – 700000

Plan – Jeevan Saathi

Policy Term -30 years

Premium -26820

Premium Payable -Yearly

Should i surrender the policy or make it paid up,

please suggest

Dear Mohit,

What prompted you to buy these two products and now why you felt MF and Term Plans are better?

Sir above products are suggested by old family friend,

And now following your blog/articles so i feel i should do some proper financial planning with your guidance.

Dear Mohit,

Please drop an email to [email protected].

Hello Sir,

I have already Term Plan of 50Lk with Term is 30 year, tile my 57 age.

I want to by one more term plan, but i just want cover of 1CR.

Could you help me can by new 1 CR term plan or go for 50Lk only.

Dear Abhijeet,

How can I say your life insurance requirement? If you feel Rs.50 lakh is the sufficient insurance, then continue the same and otherwise enhance it.

Sorry, i need 1cr cover , out of i a have already have 50lk.

just want to confirm that do i go for new 1 cr for 40 year or continue with only 50lk and by new with 50lk.

as old one cover up to the age 57 only and new one is cover tile 70.

so if i by new for 1cr so that was tile the age of 70.

Dear Abhijeet,

Do you need Life Insurance up to the age of 70 years? If so, then go ahead with Rs.1 Cr plan.

so can i close the old one and start new one with 1.Cr plan as premium almost same..

Dear Abhijeet,

If you feel it is required and the existing one not adding value, then go ahead and buy it.

Dear Basavaraj

Good Day! I have been offered a Term Plan for Tata AIA through my bank advisor for a term cover of 2Cr for 80 years. The premium i have to pay in 5 years and it will cost me about 1.8 Lakhs. I am currently 44. What you suggest?

Regards

Roy

Dear Roy,

Do you need Life Insurance up to the age of 80 years?

Sir I am 40 years old and want to opt 1.5 cr term plan for 25 years from hdfc life. Online quote is showing rs 21816. But the advisor says that there is no quote for a person aged 40 years wishing to take cover of 1.5 cr for 25 years. Also he warned me that during online purchase it may be difficult to complete the process , as this combination is not allowed by default.

What should I do please guide.

Dear Vineet,

HE IS COMPLETELY MISGUIDING YOU. If there is no such quote, then how HDFC Life generating that quote ONLINE?

Hi

I have an existing policy with Aegon since 2013. I feel that the coverage is now not adequate as there has been an addition in my family last year. Should I take another policy with Aegon or go with another vendor? Are there any issues having 2 policies from the same company?

Dear Victor,

If you have no issues with Aegon Life, then why to worry? Go ahead with the same insurer. There is no harm in having more than one insurance policy with the same insurer.

Hi ,

Actually i have TATA AIA term insurance

I drink alcohol once in two week , but the agent of TATA AIA didn’t not recorded it , i asked him to update but he is saying nothing will happen ,what should i do.

Dear Sachin,

Don’t let happen so. Write an email to the insurance company that agent hid this and you are disclosing the facts.

sir

I am 36 years old and my wife is of 33 years our annual income is 7L for myself and 3.5l For my wife is there any combine term insurance available for both of us? or we have to take it seperately?

Dear Bhagyesh,

Best to buy separately even though there are joint term life insurances available.

Basavaraj is aegon the only player giving term insurance to housewife?

Dear Devesh,

As per my knowledge YES. But not sure. You have to inquire with the respective insurer for the same.

hi Basu

Thanks for the wonderful information here!

I am 38, planning to buy only term insurance of 1.5 cr ( 15 lpa inocme) without any riders (AI & CI) with aegon with coverage upto 80 years.

Pls advise on the same

Dear Shekhar,

Go ahead but do you need Life Insurance up to the age of 80 years?

Thank you Basu!

Dear Basavaraj,

Thanks for the above in depth information.

one of my friend sells term insurance policies since i am looking for one I approached him and also told him that I am looking forward to buy either Aegon iterm plan or Max life but instead he is persuading me to by Birla sun life saying there is a birla sun life office in our locality hence when time comes for claim settlement it will be easy for my family …so i am confused now dose it really help?

I personally feel like to go for Aegon as it has the lowest premium and settlement ratio is above 97%

Since you are an expert i seek your suggestion which term policy should i buy out of Aegon ,MAx life or Birla sun life??

Dear Avinash,

Never go with adviser’s choice. They suggest the one where they have some higher commission payout. Try to think what is required for you and based on that buy it.

Dear Basavaraj,

How good is ICICI iprotect smart plan? I am seeing that you are advising this plan from 2015 consecutively. I also see that you are suggesting HDFC life click 2 protect, but each year are changing every variant in it. This year you have given that HDFC life click 2 protect 3d plus is better. Of these variants, which HDFC plan is better? Also, in both (ICICI and HDFC) which is better?

I really liked your blog and your replies to every query we ask.

Thank you for helping us out.

Dear KSSR,

The plan is same but they are going to addon new features just to lure buyers and to be stay in market.

So, as per your experience, which is better ICICI or HDFC?

Dear KSSR,

For me both are equally good and bad.

Please suggest me,, I have taken term insurance,, it is sufficient for my family now. I m having one lic endowment policy of RS.2.50 lakhs,taken 10yrs back. Will mature in2038. Plz suggest is it better to surrender policy? As return in lic is very less, and life cover also less.

Dear Prasanna,

You know that returns are less and cover also, then why to continue?

Sir,

Its always a great pleasure to send you a message and thanks a lot for your responses.

I already have a HDFC Life Click to Protect Plus – Extra Life plan.

Age when policy was taken: 25

Current Age: 29

Coverage: 50 lakhs on normal death and double the amount upon accidental.

Coverage for 35 years i.e., until I reach 60 years.

Premium Amount: 8962/-

I have just seen that Max Life Insurance is offering coverage term for 50 years from today for my age @ 1,049/- per month for 1 crore coverage. This covers me until I turn 79 years.

1) It makes complete sense to me to stop paying premium at HDFC Life and go with Max Life. Would you suggest me on this?

2) If I stop paying premium at HDFC Life, should I visit them or drop an email about handing over my existing policy to them?

Thank you.

Best regards,

Nithin.

Dear Nitin,

Do you need Life Insurance up to your 79 years of age?

Dear Mr. Basavaraj

You have suggested to not go with insurance providers who do not go for medical checkup but insist on tele-medical checkup. Does it really matter? Once the policy is issued, can’t we rely on Section 45 of the new Insurance Bill which states that a policy cannot be called in question after three years of its issuance. Hence, the insurance provider cannot reject the claim based on health checkup not done. What do you think?

Dear Pawan,

Please check the details of Sec.45 of Insurance Act. It does not mean that you hide anything and get the insurance and finally claim.

Hi Sir,

I checked ICICI term plan. my age is 27

In a single payment for 1 cr, till 60 years the amount is 1,19,711/-…so, if I pay this amount once now.,.till 60 is it completely covered? and can I increase the value from 1cr to more in future?

Can you suggest if paying monthly / yearly / once is better, if affordable?

the monthly premium for the above is 732/-, which means till 60 if I continued I will pay around 4 lakhs..but if I pay at once, it is only 1 lakh 19 thousand…is this correct? and do you suggest going ahead with single payment of 1,19,711/-?

Dear Sharath,

“till 60 is it completely covered? and can I increase the value from 1cr to more in future?”-YES.

If you can afford the one time payment then can choose that also. What will be the value of today’s Rs.1.19 lakh when you are at the age of 60 years? They are smart and they are not giving anything at free.

We have checked the site of Aegon Insurance. The provide term plan with 80 years of life coverage whereas you have mentioned 100 yrs in your comparison chart above.

Dear Sanjay,

Maybe they have changed the features. Let me update and thanks for pointing.

Is, term insurance+mutual funds >>>> ULIPs?

Dear Abhishek,

Can you elaborate your comment, please?

as i am 25 years old would it be better for me to buy a term insurance plan till 60yrs and invest in mutual funds simultaneously rather than going for a good ULIP?

Dear Abhishek,

Yes it is the best option rather than choosing ULIP.

Thank you

Sir thanks for your valuable information,

Max life reject my application boz i received Salary by cash., Is it any special case for Salary by Cash

Dear Rajasekar,

Because they need the proof of income. That may be the reason.

How can I apply as a salary rec’d by cash

Dear Rajasekar,

If you are filing IT Return, then I don’t think other insurers will have any question about your cash salary payment.

Want to opt a term plan with cover of 1.25 cr.

Please help me choose between icici vs hdfc vs max life.

Hi Basavaraj ,

I have read your contain about Term policy, can you suggest me, should i go with the Aegon Term plain or HDFC 3D Please….

Dear Amul,

I never recommend any one product particularly.

Dear vineet,

All the three are equally good and worst. Choose the one which you are comfortable rather than wasting time in thinking so much.

Thanks. Still confused.

Finally I will go with icici Prudential.

Dear Sir, I am 35 yrs old now and have 10 lakh LIC policy and 50 lakh term insurance. I also have my company and personal health insurance. I have one new born kid. My wife and I have combined monthly income of rs. 1.5 lakh. Can you please suggest if I need some more insurance. thanks.

Dear Vishal,

The rough requirement of insurance is around 15-20 times of yearly income+any liability. However, the actual calculation of desired insurance may differ.

Dear Sir, I have Jeevan Anand for 5 Lakh and Jeevan Tarang for 5 Lakh. I have taken accident rider on my existing health insurance from Apollo and my company is giving separate accidental insurance. My liability is of 40 lakh home loan.

I have 50 lakh term insurance. My wife does not get any insurance from company. She has her personal health insurance and critical illness insurance.

What do you suggest? Thanks sir so much.

Dear Vishal,

I will not consider those LIC plans as Life Insurance Plans. Buy accidental insurance separately. Regarding term life insurance, the coverage should be around 15-20 times of your yearly income+liability.

I’am taking a home loan for Rupees 27 lakhs from IIFL Bank, Bangalore. The tenure is 15 years. I am planning to buy SBI eshield term life insurance however IIFL are saying that as per their policy, since loan is taken from them, I should go with the insurance that they’ve tied up with. They’re saying that they’ve tie up ICICI Lombard, TATA AIG and few more but I don’t want housing loan protection insurance. I want term life insurance for about 2.1 Crore for 18 years so that my family is protected.

My question to you is that, is there any rule that I’ve to go with what the bank has suggested or is there any law or act that prevents banks from doing monopoly so that I can choose my desired insurance. Please reply soon as banks are pushing their own insurance and with insurance the loan sanction will not happen. Thanks in advance.

Dear Fox,

There is no such rule that you have to buy as per their terms. They are misguiding you. Let them show such government notification.

Hi Basavaraj,

Thank you for your very quick response and guidance. Really appreciate your advice in this matter. Further to my first query, I checked the IIFL bank’s website (https://www.iifl.com/sites/default/files/pdf/home-loans-most-important-terms-and-conditions.pdf Page No. 2 and point number 8.) and they’ve the following conditions :

Insurance of the property / Borrowers:

(i) The Borrower/s shall keep the property under security insured with Comprehensive Insurance Policy equivalent to the loan

outstanding at any point of time during the pendency of the loan with IIFL HFC as the sole beneficiary under said policy /

policies.

(ii) The Borrower/s may keep his/their life insured equivalent to loan outstanding at any point of time during the pendency of the

loan with IIFL HFC as the sole beneficiary under said policy / policies.

These above two conditions are mandatory for Disbursement of the Loan so could you please let me know if I go only with a term life insurance policy for eg. 1.1 Crore for 20 years, will I be eligible for the disbursement or do I still require to buy a general insurance policy to insure the property.

Regards,

Fox Mulder

Dear Fox,

They are insisting you to protect your life against their loan dues. No harm in that. The harm is to insist to go for their CHOICE but not as per your wish.

I just wish to say thanks. Nice guidance on how to analyse the insurer before purchase of the policy.

Dear Mandar,

Pleasure 🙂

Sir,

Iam 34 years old female, govt job, 2 days back,

I bought a term plan sbilife shield for 1cr and accidental death cover of 50 lacs for rs. 18497. I have to pay for 30 years. Is this a good buy ?? I still have time to cancel it.

Dear Vasu,

Don’t waste your time in doing too much research and go ahead.

Hello Sir,

I will turn 25 this October and will be joining a Central Govt. service within August,2018. As such I will be eligible for CGHS. Do I need any insurance other than a term insurance till 60 yrs of age?

And my CTC would be 5.5 lpa and will change into 8 lpa before 2020. How much should be my sum assured?

Dear Rahul,

In my view, you need term life insurance and if possible accidental and critical illness insurance.

Hi, i am 47, Is it necessary to go for 12 years term plan of 1 cr. i am financially not sound. Can i go with 5 years plan, then after that again 5 years and so on. Pl guide.

Dear Rajesh,

If you are financially not sound, then first check whether you are eligible to buy Rs.1 Cr term life insurance. Usually, insurance companies provide the sum assured of around 15-20 times of your yearly income. Regarding splitting your insurance for each block of 5 years, what if you diagnosed with some health issues after 5th year? Insurance companies will deny the policy. Also, buying at a younger age will be cheaper for you than buying the same policy after 5 years.

Dear Sir,

I am 40 now, working with private and have a term insurance from Aviva for 1 Cr. since 2014.

My CTC was 6 lac in 2014 and Now it is 32 Lac.

Please help me to finding the following answers.

1- I feel to enhance the term insurance limit now. Please suggest me the Sum Assured I should go for.

2- Like mobile number portability, is it suggested to go with different insurer in different years. Because when I search best term plan, I don’t find Aviva in list.

3- Some where I read, you should go for two term insurance with different insurer, to reduce the claim settlement risk. Please suggest.

4- I am bit confuse to select the term insurance house. Please suggest – HDFC, MAX, Metlife, Exide, Ageon, ICICI

Dear Manas,

1) The random calculation is around 15-20 times of your yearly income+any liability.

2) Portability option is not available in Life Insurance.

3) The more you diversify your Life Insurance, the more work you give to your nominee. No login in spreading.

4) To me all are good and bad.

Hi Basu,

Thanks for sharing the knowledge, really appreciate it.

I am 28 yrs old, non smoker and planning for ICICI i protect term for 30 yrs.

Knowing your intention for Riders , I just want to confirm if I should go with riders or buying riders individually is also a good choice.

Regards,

Brijesh

Dear Brijesh,

Don’t go with riders. Buy such insurances separately from general insurance companies.

Dear Basavaraj,

My name is Nikunj, Age – 26, Non smoker.

First of all, I would like to thank you for this blog. I had no knowledge about term plans but now I gave some sense of selection thanks to the knowledge shared by you.

My queries are as follows.