On 2nd June, 2016, CBDT notified the Cost of Inflation Index for FY 2016-17. Let us try to identify the changes and how it affects your tax calculation for long-term capital gains.

What is the meaning of short-term capital asset and long-term capital asset?

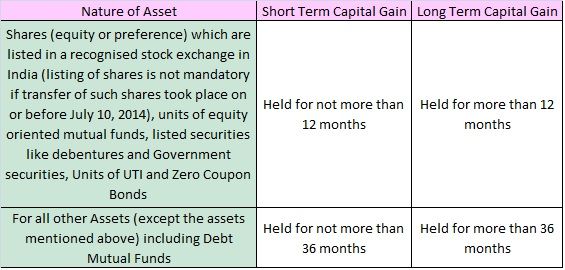

Based on holding period of an asset, the capital gain tax is defined. It is explained in below image.

What is Cost of Inflation Index?

It is a measure of inflation for computing cost of acquisition of an asset for the long term capital gain tax. It is declared every year by CBDT. It is based on financial year. So assessment year will not come into the picture.

Let us say you bought the property for Rs.10 lakh in the financial year of 2000-01 and you sold it for Rs.40 lakh in the financial year of 2015-16. The long-term capital gain is not Rs.20 lakh, but it is something different. Because here the cost of acquisition of property is inflated based on the Cost of Inflation Index of 2000. So it is computed as below.

(Cost of acquisition/Cost of Inflation Index for the year in which asset is acquired)*Cost of inflation index for the year in which the asset is transferred.

This is how it is calculated.

Note-Capital gain arising from property sell will always be with indexation at 20% tax. However, for benefit illustration, I showed the tax at 10%. Assets which are eligible for both 20% tax with indexation and 10% tax without indexation are as below.

(a) Any security which is listed in a recognised stock exchange in India;

(b) Any unit of UTI or mutual fund (whether listed or not);

(c) Zero coupon bonds

Now I will explain in detail. So the cost of acquisition will be (Rs.20 lakh/406)*1081=Rs.26,62,561 (Cost of inflation index for FY 2000-01 is 406 and for FY 2015-16 is 1081). Now the capital gain from this sale will be based on INDEXED COST OF ACQUICISATION but not based on the actual cost of acquisition. So the capital gain will be not Rs.40 lakh-Rs.26,62,561=Rs.13,37,439.

You can refer few examples from IT Department Tutorials.

Which assets will be eligible for indexation benefit?

Properties or securities (stocks, mutual funds or bonds). But bank FDs or RDs will not form part of such tax.

Hope the indexation benefit is clear now.

What is the Cost of Inflation Index for FY 2016-17 ?

The Cost of Inflation Index for FY 2016-17 is declared as 1125. Let us try to see the historical chart of Cost of Inflation Index from FY 1981-82 t0 FY 2016-17.

How the Cost of Inflation Index for FY 2016-17 is calculated?

There is a method to calculate the cost of inflation index on every year. It is 75% of an average rise in the consumer price index (CPI) for urban non-manual employees for the immediately preceding previous year will be added to the CII of the previous year.

The average CPI (Consumer Price Index) for FY 2015-16 was 5.43%. Now we have to make it 75% of 5.43%, this will be 4.07%. The CII (Cost of Inflation Index) for FY 2015-16 was 1081. We have to now multiply 4.07% with 1081 to arrive at the increasing value of Cost of Inflation Index for FY 2016-17. This value is 44. Now we have to add this number to previous year’s cost of an inflation index. By doing so we can easily arrive the current year cost of an inflation index. as 1125

Therefore, the Cost of Inflation Index for FY 2016-17 is 1081+44=1125.

Very detailed post sir, thank you !

I am a regular visitor to your blog and find you r posts useful. 🙂

I have a query, a farmer bought a agricultural land in the year 1962 for Rs.500. He used the land for farming (only source of income). As he has no source of income now, He sold the land in 2017 for 10 lakhs after conversion to non-agriculture land to increase sale value.

1)whether he’s liable to pay capital gains tax (LTCG)?

2) if yes, As per the above post I’ve tried calculating his tax

Cost of acquisition =500×272(CII for 2017) /100(CII for 1962,base year 2001) =1360/-

Sale value =10,00,000/-

Gain after Indexation= 10,00,000-1360 =9,98,640/-

20% LTCG tax =1,99,728/-

Budding-As per me YES as the property is now no more an agriculture land.

Thanks sir for fast reply! Really appreciate it 🙂

Sir, whats your view on NFO – birla sunlife dual advantage fund

Ketan-Avoid any kind of NFO. NFOs are meant for Mutual Fund Companies survival and advisers earning opportunity.

Thank you. which SIP you suggest considering 10 to 15 years horizon…

Ketan-Refer my earlier post “Top 10 Best SIP Mutual Funds to invest in India in 2016“.

Thanks Dear !!

Can you pls simplify the F&O, Derivatives (Call/Put), Commodity Market

What/Why/How ?

Neeraj-I am not an expert in that.

ARE THE DIVIDENDS DECLARED BY ARBITAGE FUNDS IN LESS THEN ONE YEAR ARE iNCOME TAX FREE OR NOT.

SECOND QUERY:IF THERE IS GAIN IN VALUE OF ARBITRAGE FUND IN LESS THEN ONE YEAR. THIS GAIN IS SHORT TERM GAIN OR LONG TERM GAIN?

Indra-Dividend income always tax free in the hands of an investor. Any gain within a year from Arbitrage fund is short-term capital gain.

Very informative. Thank you for your time.

Dear Basavraj, thanks for the information on the capital gain. You have been doing a great job for many needy persons like me. True guide.

Arun-Pleasure 🙂

VERY INFORMATIVE AND USEFUL FOR INSTANT REFERENCE.

Thanks for Sharing Information.

Nice information buddy. That is why equity is the best investment option. Its acts as a hedge against inflation.

Thanks

Sowmay-Pleasure. Yes, indeed.