Which are the best Debt Mutual Funds when interest rates are rising? Up to last year, we were in a different mode of the interest rate cycle. However, now due to inflation, global economic slowdown, and certain other external factors interest rates are rising. In such a situation obliviously people try to look for the options available in front of us.

Bond Price Vs Interest Rate Cycle

To understand the relationship between bond price movement and the interest rate cycle, let me give you an example. Assume that you are holding a 10-year bond of Rs.100 face value and the coupon on this bond is 6%. Let us assume that your friend is also holding a 10- year bond of the same face value of Rs.100 and the coupon on his bond is 8%. Let us assume that Bank FD rates are currently at 7%.

If you and your friend try to sell both of your bonds in the secondary market (for various reasons), then there will not be anyone to buy your bond as the FD rates and some other bonds (like your friend’s bond) are having a high coupon rate. Hence, you are forced to sell at a discounted price than what you have invested. Same way let us assume that your friend trying to sell his bond, then obviously as his bond is offering an attractive rate, people will try to buy a bond. Hence, considering the demand, his bond may be sold at a premium price than what he invested.

This way on a daily basis the price movement of the bond works in a secondary market. This movement of the bond is high for long-term maturity bonds than the short-term maturity bonds. Such interest rate sensitivity is called DURATION in the bond world. Higher the modified duration, the greater the sensitivity to interest rate movements.

Do remember that this interest rate sensitivity is applicable to all categories of bonds INCLUDING GOVT BONDS also. By avoiding corporate bonds, you can avoid default or downgrade risk. However, you can’t run away from interest rate volatility.

Now how this price is related to yield or Yield To Maturity?

If we take the above example of you and your friend, then if someone is trying to buy your bond where you are selling at a discounted price, then obviously for a new buyer this is the best opportunity. Because face value is the same, a coupon is the same, and tenure is fixed but the price is available at a discounted price than it’s face value. Hence, if someone is buying this bond, then the return on investment for him will be higher than you. This is represented by a YTM or Yield To Maturity concept. It simply means if someone is buying your bond at what discounted price you are selling, then if the buyer is ready to hold the bond till maturity, then what is the return on investment?

To simplify this, bond price and yield are in inverse proportion. If the bond prices started to fall, then the yield will increase and vice versa.

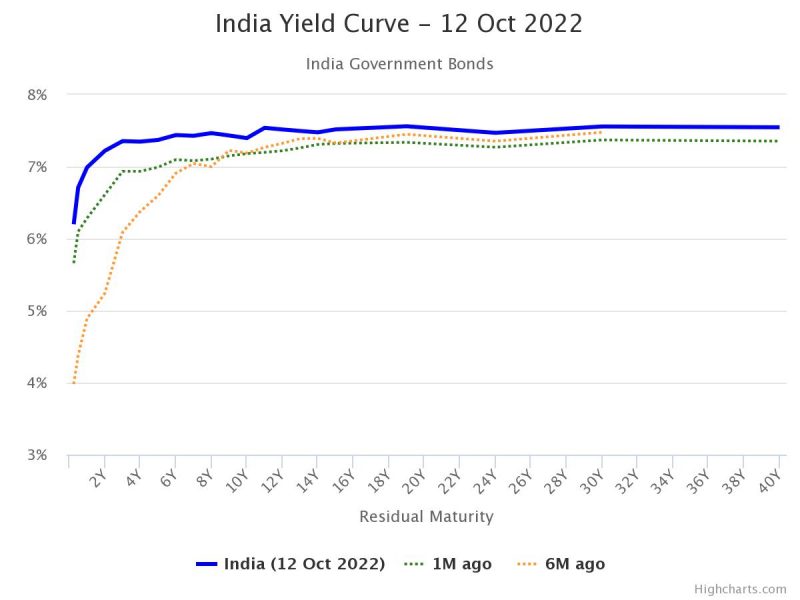

Let us now look into the last two years of yield movement and RBI repo rate movement.

Notice the yield movement. As the repo rate is increasing, bond prices are falling and hence the increase in yield.

As I mentioned above, this impact of interest rate movement will be more for long-term bonds than the short-term bonds. Hence, let us understand the yield impact for the various residual maturity bonds since 6 months.

Now you understood the concept of interest rate movement, bond price movement, and how the yield impacts the bondholder or fresh investors.

Best Debt Mutual Funds when Interest Rates Rising

Now let us come back to the main agenda of this post. When many choose the debt portfolio, they obliviously think that it is SAFE. For many Indian investors, the common belief is that equity is risky and debt is safe. However, the reality is entirely different. If you blindly chase the returns or what we call yield (in the bond market), without knowing why the yield is high, then you end up in big trouble.

In fact, there are instances where liquid funds showed a downfall of more than 5% in a single day (Refer to our 2017 article here “Is Liquid Fund Safe and alternative to Savings Account?“).

Hence, knowing the purpose of using debt in your portfolio must be clear to you. Use the debt portfolio to fund your short-term goals and diversify for your long-term goals. If you try to chase the yield from the debt portfolio, then the whole portfolio looks risky.

As I mentioned above, we can to a certain extent avoid default or downgrade risk by including the sovereign bond funds. However, we can’t run away from interest rate movements. Hence, first, follow these important aspects before just randomly picking the high-yielding funds.

# Stick to simple products which you can understand.

# Always make sure that your requirement should be more than the average maturity of the bond. Let us assume that you need the money after 5 years, then make sure to choose the funds whose average maturity is around 3 years or so. Never rely on the standard guidelines of the financial world “match your requirement with average maturity”. It is high risk.

# For short-term goals like less than 3 years or so, use simple products like Bank FDs or RDs. You can explore Liquid Funds also (when you are unsure of when you need the money).

# For medium-term goals, stick to Ultra Short Term Debt Funds or Money Market Funds.

# For long-term goals like more than 10 years or so, as NONE can predict the interest rate cycle, mix your portfolio with short-term and long-term bond funds.

# As we mentioned above, the longer the bond maturity higher the volatility, use long-term bond funds if you are ready to digest the volatility.

# Stay away from the so-called concept of CORE and SATELLITE portfolio concept. Whether it is a core portfolio or satellite portfolio, it is your hard-earned money that is at RISK. Those who propagate such theories are nothing but here to complicate your financial life or try to sell something to you.

If you are unsure of how to play with all these scenarios, then the simplest approach is using the Target Maturity Funds or Debt Index Funds. We have already written a detailed post on this. You can refer to the same at “List of Target Maturity or Debt Index Funds To Invest in India in 2022“.

Target Maturity Funds have a different flavor. Hence, don’t be fooled by the current yield. Refer to the above-shared link for a complete understanding of the TMFs.

Finally, our recommendation of Best Debt Mutual Funds when Interest Rates Rise is as below.

# Liquid Funds

Quantum Liquid Fund or Parag Parikh Liquid Fund

# Ultra Short-Term Debt Funds

ICICI Pru Ultra Short Term Debt Fund or SBI Ultra Short Term Debt Fund

# Money Market Funds

ICICI Pru Money Market Fund or SBI

# Gilt Funds

ICICI Pru Gilt Fund or SBI Gilt Fund

# Target Maturity Funds (refer our post link)

Avoid all forms of debt funds. Our advice may look silly or laughable. However, when you are choosing the debt portfolio, as we mentioned above, the idea is to diversify and safety but not to chase the yield. If you are really fond of generating higher returns, then increase your equity exposure if your stomach digest. But don’t take the undue risk of especially the default or downgrade risk in debt funds.

Many are blindly exploring the Government Bonds or State Government Bonds available in the RBI Retail Direct platform as the yields are currently at a mouthwatering yield and all of us feel that government bonds are safe. However, as we cautioned you above, you can avoid default or downgrade risk. But you can’t run away from interest rate risks. Refer to our posts “How to buy RBI Floating Rate Bonds online?” and “High-yielding SDL/Govt Bonds OR FDs/Debt Funds?“. Because they are meant for different purposes and not suitable for all.

The Mutual Fund industry is here to create stories and collect the money from us as their profile module is based on AUM. Hence, rather than exploring the other categories of debt funds, stick to these basic and simple products during such a higher interest rate regime.

Dear Sir,

I was going through the factsheets of Money Market Funds you recommended of ICICI Pru Money Market Fund. I found some scary Bonds in it and I don’t have the risk appetite of Borrowers in that factsheet. SBI’s Savings Fund is better but is that the only choice if I want to invest only in Funds which have a modified Duration of up to 1 year and have clean factsheets, invests in

1. TBills

2. CDs and

3. fairly known borrowers in CP

4. Not AT1or AT2 bonds

5. No Commercial papers whose borrowers are sketchy

For Liquid Fund as you have recommended I have money parked in Parag Parikh Liquid Fund however the average maturity is just 42 days now. (As liquid) Anything similar in larger tenure funds?

Dear KB,

I have already replied to your comment for other posts on this topic.

Sir, Now I feel it is the time to also write about Which Debt Mutual Funds to switch to when interest rate cycle pauses and subsequently falls.

Dear KB,

Surely I will write soon.

Can you name some 40 year Gilt Funds.

Dear KB,

You can get that information from RBI Retail Direct.

Dear Sir,

Can you recommend some more liquid funds which invests in G-Secs? I follow your index approach for the long term but for 25-30 days I can’t find a liquid fund which has 0 credit risk, less expense ratio, a Good Fund manager and a sizable AUM.

I was thinking of PP Liquid Fund as you said as but its AUM is very low . Can you help me out here, please if there are other options?

Dear KB,

If your requiremnet is just to park for 25-30 days, then either use Overnight Funds (of any AMC) or use the sweep-in account of your bank (or FD). There is no such a great advantage by parking your money in liquid funds for your required 25-30 days time horizon.

Sir I forgot to tell you 25 days each month. And every month after 25 days majority money will be redeemed. But some will stay.

Dear KB,

Can you elaborate more about your actual requirement?

Yes Sir. And deeply thankful to you for replying.

1. I get funds between the 5-10th of each month. And about 25% is expenditure. Thae last and major expense is on the 30th of each month.

2. I invest the remaining balance as per opportunity available. But in some months, there are few and unpredictable thus invest the remaining 75% with a lag.

So the 25% of money will be put for 20-25 days each month for full year as each month I will get salary and each month I have to pay bills that’s why I said 25 days in a month repeated for a full year.

The rest 75%(1 month salary) or 150%(2 month salary residual) for 1 maybe say 1.5 months , This will not be a repeated cycle.

I need a mutual fund which has a , Sizeable AUM, 90% plus investments in T-Bills and GSecs, Fund manager which has shown a good history in managing and less expense ratio

I have chosen PPLF as 90% investments (I check each fortnight) are with sovereign guarantee.

So I have invested this month’s excess balance in PPLF (direct-growth). Any more Liquid-Low duration options which you might suggest

Dear KB,

You can check Quantum Liquid Fund (not Quant) along with PPLF. One more option of risk-free parking is using Overnight Funds.

Thank you sir.

Enlightened. but after complete reading , all I can do is to just stick to your recomendations! thank you!

Dear Venkata,

Thanks 🙂