Why we invest in Liquid Funds? We consider Liquid Fund safe and as an alternative to the savings account or to keep our emergency funds right? But what if suddenly Liquid Mutual Fund give 7% negative returns in a single day?

Let us say you invested in a liquid fund as an alternative to keeping your emergency cash of Rs.10 lakh. Suddenly next day it turned to be Rs.9,30,000 means? Shocking right? This incident recently happened with one such liquid fund.

Many of us never bother about the risk involved in our investment. Many of us simply follow the returns or so-called Star Ratings of the portals like Valueresearch, Morningstar or Moneycontrol.

Also, we strongly believe (or may be forced to believe by Mutual Fund Companies, Advisers or so-called IFAs) that Debt Funds are really safe instruments.

However, the reality is something different. We claim that there are strict regulation in mutual fund industry with a big watchdog always on mutual fund companies head.

However, Mutual Fund Companies need fresh cash to run their show. They have to attract investors with fancy returns and fancy fund names. In such madness, sometimes they float the rules in the air and take the risk at a ride.

Advisers, IFAs or Bankers now EYEING on Debt Funds to increase their AUM. So they MAY sell you debt funds as if an alternative to savings account. But hold a caution…

What is Liquid Fund?

Liquid Fund is a type of Debt Mutual Funds, which mainly invest in money market instruments like treasury bills (TB), certificates of deposit (CD), commercial paper (CP) and inter-bank call money, government securities, etc having a maturity of less than 91 days.

As the maximum maturity of all such underlying instruments is 91 days, the average maturity of Liquid Funds will always be less than 91 days.

Therefore such accumulated corpus from Liquid Funds will be invested in such short and secure money market instruments.

Is Liquid Fund Safe and alternative to Savings Account?

Liquid Fund is also the type of mutual funds. Hence, before you judge the safety, you must understand few risk measuring tools or how to identify the risk of debt mutual funds.

I already wrote a detailed post about who can invest and what is the taxation of Liquid Funds in my earlier post “Top 5 Best Liquid Mutual Funds in India in 2017“.

Now let us understand few new definitions to know more about liquid funds. For any debt fund selection, I suggest you must give utmost importance to the below-shared information.

Credit Risk-

Debt Mutual Funds invest in treasury bills, government securities, Certificate of Deposits (CDs), Commercial Papers (CPs), bonds, money market instruments and many more. The credit quality of these underlying instruments are measured in terms of ratings.

Usually higher the ratings leads to lower the return or risk. It is a misconception among many that credit risk refers to risk of default by the bond issuing entity. However, the truth is something different.

There is a possibility that the credit rating of a bond or instrument the fund is holding may change at any point of time. Let us say ABC Debt Fund holding the bond of XYZ which is rated as AAA by credit rating agencies (highest rating).

It does not mean that this rating is permanent. It may change at any point of time if the company XYZ’s finance changes.

Hence, never be in a misconception that credit rating refers to default risk and also credit rating of bond will NEVER CHANGE.

Modified Duration-

It is a measurement of a bond’s sensitivity to movements in interest rates. It is usually measured in years. For example, if debt mutual fund with the modified duration of 3.1% means if there is a 1% interest rate movement then the fund will undergo the movement of 3.1%.

Hence, higher the modified duration means higher the interest rate risk.

Average Maturity-

A debt fund portfolio usually consists of a number of bonds where each could have a different maturity date. Maturity is the time period remaining before which a bond comes up for repayment by the issuer. Average maturity is simply the weighted average time left up to the maturity of the various bonds in a portfolio.

Higher the average maturity greater the interest rate risk of the debt fund.

Now you understood few main terminologies which measure the risk of debt funds. Let us now concentrate on a risk which I am sharing with you in relation to Liquid Fund which fell to 7% in a single day.

Taurus Liquid Fund crashed to 7% in a single day!

See the below images of Valueresearch data for Taurus Liquid Fund.

You notice the star rating provided by Valueresearch and also the sudden fall of 7% in a single day. Now let us consider the style box of the fund and other criteria which I discussed above.

You notice the Modified Duration, Average Maturity, and Fund Style Box. All indicates as safe product which holding mainly CRISIL A1 (Instruments with this rating are considered to have very strong degree of safety regarding timely payment of financial obligations. Such instruments carry lowest credit risk) rated underlying instruments.

Then what went wrong with Taurus Liquid Fund?

Credit Risk Rating agency India Ratings, downgraded the Short Term Bonds and CPs of the company called “Ballarpur Industries Limited (BILT)”. Earlier A1+ in 2013 and A1/RWE (Ratings Watch Evolving) in 2015 to A3/RWN (Rating Watch Negative) in December 2016 for the commercial paper (CP).

Now the rating agency downgraded the CP NCDs to Ind C as earlier it was IND A3/RWN.

This is the story of degrading the ratings of Commercial Papers of Ballarpur Industries Limited (BILT). As CPs are short-term instruments, I think this Liquid Fund also held such CPs of this company.

The holding as on 23rd February is around 4.33%. However, the fall is 7%. Why such a steep fall when the holding is just around 4%? Only the Fund Manager or Taurus AMC can answer this.

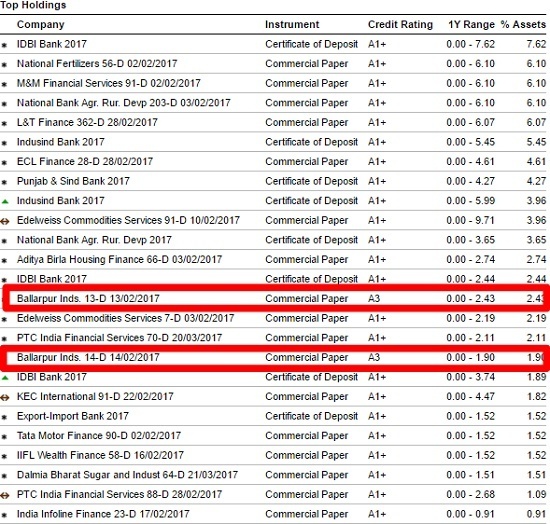

Now let us look at the Fund’s holding as on 31st January 2017.

You notice that the total holding of Ballarpur Industries Limited is 4.33% and rated as A3 (Instruments with this rating are considered to have moderate degree of safety regarding timely payment of financial obligations. Such instruments carry higher credit risk as compared to instruments rated A1 and A2).

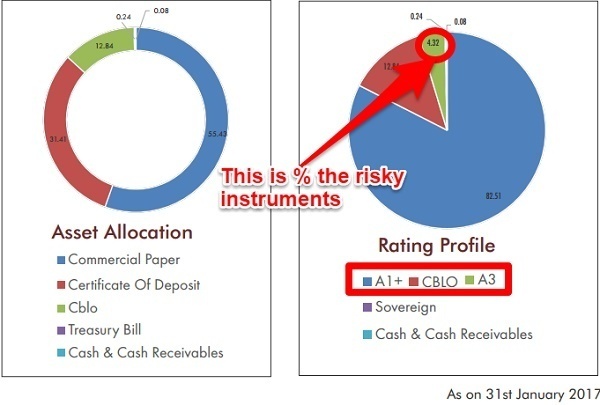

The same is explained in pie chart by Taurus AMC in the fund fact sheet of Taurus Liquid Fund.

The factsheet of 31st January 2017 shows that the fund is holding the low rated instruments. Also, if you look at financials of Ballarpur Industries, then you clearly notice that the company is not financially healthy (As per India Ratings-In 9MFY17, BILT reported consolidated revenue of INR16.9 billion (down 44.8%yoy) and consolidated EBITDA losses of INR744 million (INR5.6 billion) with net loss of INR9,037 million (negative INR781 million). BILT reported EBIT margin of negative 12.1% in 9MFY17 in the key paper segment (9MFY16: 16.1%).

But still, the fund manager took the risk of holding around 4.33% of such unhealthy company.

Who noticed this risk?

NONE…Including Fund Manager, AMC, Investors, Middlemen or so-called IFAs and even SEBI. However, many of us (advisers, IFAs, Banks and investors) concentrated on star ratings mainly and invested. This turned to be the classic example of how star ratings really misguide us.

So we have to avoid Liquid Funds?

Now comes the tricky question after reading all the above information. Whether we have to avoid liquid funds as an alternative to the savings account or keeping an emergency money?

In my view, partly YES. Reasons are as below.

# Liquid Funds are not so LIQUID-

Many of us invest in Liquid Funds as if we have the access to cash like savings account. But the reality is, if you requested for the redemption of the fund (before 2 PM), then it usually takes around T+1 days to get the cash.

In such a situation, how can we meet our emergencies?

# Returns not GUARANTEED

When we invest in Liquid Funds, our (many of us) actual intention is to beat the savings account interest rate or short term FD rates. But the reality is that when we are investing our emergency fund, then our first MOTTO should be how much liquid is the product.

In case if you are investing for a very short period (other than emergency fund), then the utmost important should be safe keeping of principal but not expecting higher returns.

After all HIGHER RISK does not mean GUARANTEED HIGHER RETURN.

# Risk involved in Liquid Fund

You noticed from above example that the small portion of around 4.33% of risky exposure resulted into 7% fall in a single day. It is all due to not understanding or not monitoring the fund portfolio.

We not go so deep and verify the underlying debt papers. We simply believe that Liquid Funds are safe. So if you really eager to invest in Liquid Fund, then go deep and understand the underlying papers the fund is investing.

If you are uncomfortable with the quality of paper or the fund manager’s risk-taking ability, then simply dump the fund. Study the key information document (KIM) or Scheme information document (SID) to understand risk. Check past factsheets as mentioned above.

After all the art of investment is how to manage the risk than how to avoid the risk.

# Invest only in high rated AAA Liquid Funds

Instead of taking the risk, try to invest in high rated liquid funds. (I already wrote a post on this “Top 5 Best Liquid Mutual Funds in India in 2017“). Such funds or cash management funds may not be high rated by rating portals. However, stick to your basics and safety at first and invest wisely.

# If still confused, then completely avoid Liquid Funds

If you still confused with all these GYAAN, then either take the help of reliable and knowledgeable (the biggest task to identify in the crowd of advisers, IFAs and Banks) adviser and invest.

Otherwise, simply avoid the Liquid Fund and invest in traditional instruments like Bank FDs or RDs. After all your circus of looking for Liquid Funds is to earn a bit better return than these safe instruments.

Hi sir,

If someone want to invest lumpsum amount it is advisable to invest in liquid fund and and do STP to equity fund. Is it correct process.

Nikhil-You can do so.

Why can’t the amount be kept in savings bank with auto sweep facility and move to equity funds through STP? This is more advantageous, I think.

Dear Madhu,

To do the STP, the money should be invested in liquid fund of a same AMC and from there you can opt for STP.

EARLIER ALSO I HAVE MENTIONED ADVISOR ARE IMPORTANT IN EVERY THING . LIKE IF U FALL ILL YOU MUST GO TO DOCTOR FOR YOUR TREATMENT , IF U WANT TO FILE YOUR RETURN U NEED CA FOR THAT . IN EVERY FILED SOMETHING IS WRONG OR SOME PEOPLE ARE BAD

. I MENTIONED IN PAST ALSO YOU NEED AN ADVISOR FOR MANAGING YOUR HARD MONEY EARNED . BEFORE GIVING ANY INVESTMENT ADVISE I PERSONALLY SEE PORTFOLIO OF THAT FUND . WHETHER ITS HOLDING AAA+ , AA+ , A+ OR THEY HAVE G SEC OR NOT AND THERE ARE MANY THINGS WE HAVE TO SEE WHICH I CAN NOT EXPLAIN ALL IN FEW LINES . I M DOING ALL SINCE LAST 8 YEARS AND MANAGING GOOD AMOUNT OF CORPUS AND MAKING MONEY EVERY DAY FOR MY CLIENTS . LOOK THOSE INVEST VERY SMALL AMOUNT AND IN 10 PERCENT INCOME TAX BRACKET ITS FINE THEY GO FOR FD . BUT FOR BIGGER AMOUNT WE NEED INDEXATION BENEFIT FOR OUR TAXATION PAYMENT . YES MUTUAL FUND HAVE A RISK BUT IF U HAVE A GOOD ADVIOSR HE CAN MANAGE YOUR PORTFOLIO VERY SMARTLY CAN MAKE MONEY FOR YOU WHETHER ITS DEBTS FUND , EQUITY FUNDS OR ANY MUTUAL FUNDS . JUST TAKIN ONE OR TWO REFERENCE AND BLAMING ENTIRE MUTUAL FUND INDUSTRY IS NIT GOOD AT ALL . MUTUAL FUNDS ARE DOING VERY GOOD ONLY PROBLEM IS THAT IF U DONT HAVE A PROPER KNOWLEDGE THAN GO WITH THE ADVIOSRS WHO CAN HELP YOU AND GUIDE YOU . THANKS

Anand-So as per you those invested in above fund are all DIRECT investors? Don’t say that middlemen are MUST. If one has time and capability to manage his own portfolio, then why not DIRECT? Also, let me know the quality of good adviser, I am still searching!!

With people like Anand managing 600 crore AUM fund, god help the people of India. I am having serious doubts on the ability and knowledge of all fund managers in India now. If people like Anand are not clear on simple concepts like CAGR, NAV and XIRR, how is he even calling himself a financial expert?

Anjan-True 🙂

Nice joke …if someone in the entire industry do something unethical and because of that reason you doubt entire industry than kindly put your money in bank account and earn 4 to 6 % int and be happy..big corporates and hni clients are not fool .they deals with good advisors and take expert advice before investing.they don’t invest and redeem there money because of petty issues .taurus AMC is a very small company and they were managing only 80 crores in that liquid fund .I never invested and neither advised my clients to invest in small AMC like taurus .my all clients are so happy with Me .since last 8 years m involved in financial advisory. I saved my clients many times ..I know how to manage my client money .my firm name is anand financial services and yes if u are client of my company than plese redeem your money as early as possible because I dont manage small amount..minimum size 1 crores ..and u were one of them than u were known about liquid funds risk ..stay invested in savings account and missed the benefit of capital indexation as well .If one investor invested 10 lakhs in Fd nd another one in liquid funds ..if they hold money for 3 years than he can claim indexation benefit to .near about he can save 10 % .SBI ,Birla ,Icici ,Hdfc ,reliance ,Uti ,Franklin any one AMC liquid funds u can invest there is no risk .I know the quality of papers they have in the portfolio .

Anand-Now why you are defending your Rs.600 Cr AUM here?? Also, all know the indexation benefits and taxation. Say something new which you shared in earlier comments like CAGR, IRR and ABSOLUTE RETURN. For your information, just check the data and find out that the AMCs which have big name in equity are BAD in managing debt. The best example is Franklin. Rest I left the case with you to decide 🙂

War of wards help us to understand many things any how thankful to basavaraj sir

Janakiraman-Thanks 🙂

I think you don’t have proper knowledge of liquid funds .you quoted 7 % minus in one day .you must clear that point that it is cagr returns not absolute returns .example – 1 lakhs if someone invest in liquid funds and if 7% falls in one day it mean that u will incur a loss of rs 19.17 only .100000×7% =7000 /365mean loss of only 19.17 rs .In case any investor do FD and premature his Fd than he will charged 1% .liquids funds are fully safe and anyone can invest money without hesitation .Even few people’s says investment in lic safe but everyone must know that if u premature your policy u will incur 30 % loss on your capital investment value .liquid fund gives us a one working day liquidity .sometimes liquid funds comes down that only because of rbi monetary policy changes .In liquid funds they invest and diversify there portfolios in such a manner that capital is safe, only interest part may vary due to changes in monetary policies of rbi .

Anand-Great GYAAN 🙂 Let us assume you invested Rs.1,00,000 on the previous day of 7% fall. Next day your amount will be Rs.93,000. Then, how many days it will take to reach the level of Rs.1,00,000 (forget about the absolute return or CAGR return). You can’t spread that 7% fall and average it to 365 days. Hope you understand of what I am saying.

7 % FALLS MEANS ONLY RS 20 SIR in 1 lakhs its not 7000 plese dont spread rumors ..ITS A CAGR FALL NOT ABSOLUTE .SIR U CLAIMED THAT U ARE CERTIFIED FINANCIAL ADVISOR AND IF U DONT KNOW THE DIFference BETWEEN ABSOLUTE AND CAGR RETUNRS THAN I CANT MAKE U UNDERSTAND THE EXAMPLE .PLESE READ ABOUT CAGR RETURNS THAN ONLY U WILL BE ABLE TO UNDERSTAND .AT THIS MOMENT M MANAGING 600 CRORES IN MY AUM WHICH IS IN LIQUID FUNDS .FOR DETAILED CONCEPT OF LIQUID FUNDS U HAVE TO SPEND MONTHS, ITS NOT POSSIBLE TO UNDERSTAND WITHOUT HAVING SOUND KNOWLEDGE OF LIQUID FUNDS PORTFOLIO MANAGEMENT .AS I MENTIONED EARLIER ALSO THERE IS RISK IN INTEREST PART ONLY NOT IN YOUR CAPITAL .BEACAUSE 7% CAGR MEAN ONLY RS 20 WHICH CAN BE REVOERD BY 1 DAY NORMAL INTEREST .SUPPOSE U ARE GAINING 7 % RETURNS IN A YEAR .AND IF ITS FALLS BY 7% CAGR IT MEAN THAT U LOOSE ONLY 1 DAY INTEREST NOT MORE THAN ..WITHIN 2 TO 3 DAYS U WILL RECOVER THAT LOSS AND EVEN PROFIT WILL BE SHOW IN UR INVESTMENT AMOUNT ..RBI DOES NOT change monetary policy on a daily basis .so its happen once or twice in a year which hardly matters because sometimes its goes in favour of the nav also .u can track any liquid funds .in last 25 years never anyone incur a loss if stays for 2 to 3 days .yes i agree interest part may vary ..sometimes we get 8% returns sometimes 5 % .but avg now we are getting near 7 % ..if anyone hold money for 7 days only than he will be able to get minimum 7 % .ANYWAYS ITS NOT EASY TO UNDERSTAND IN A VERY SHORT SPAM OF TIME OR IN FEW LINES .KINDLY MEET ANY TRUE CERTIFIED FINANCIAL ADVISOR FOR MORE CLARIFICATION .THANKING YOU , OR IF U COME KOLKATA U CAN COME TO MEET ME IN MY OFFICE .

Anand-Let us say equity market fallen at 7%, and your fund also fallen in same value means it is 7% from the previous level or what?? Thanks for showing me the path of what is ABSOLUTE RETURN and CAGR 🙂 Can you show me that after a 7% fall of that fund, whether it regained within a single day or within 2-3 days? Just have this chart of the fund of VR. As per your claim, it must recover within 2-3 days, right? But it is almost 2+ months, but still, that fund not reached the earlier stage of NAV.

Now regarding the calculation of your’s the NAV of that fund before the fall was at Rs.17.47. Let us say you invested Rs.1,00,000 in this fund. Then you might have received 5724 units. The next day, NAV fell to Rs.16.21. Then as per units you holding to NAV, the invested value is Rs.92,787. Now, whose claim is correct? My claim of loss of around Rs.7,000 or your claim of around Rs.20?? Just over the NAV history of fund and calculate.

Then we discuss an ABSOLUTE RETURN, CAGR, IRR and XIRR.

Great to know that you are managing Rs.600 Cr AUM of the liquid fund. God bless your investors! Regarding your view that understanding of liquid fund takes so much time, it may be for YOU. But it does not mean that all MUST spend a month to understand this product. This is how the financial industry made complicated and made to rely on middlemen. Complicate investors and let them follow blindly.

tell me that liquid funds names which is fallen by 7 % .and i will send u the chart and excat impact on nav price ..for becoimg experts u take months of study and apart from normal person like u can be made in a single days ….tel me the aum are u managing in the industry ??????/its very easy to read books and comments ..but practical exp is something different and for that level of knowledge its takes time ..lets not go to the personal level and debate on that funds ///kindy provide me scheme name and after that it will be easier to clear you …waiting for the response

Anand-For your information, managing HUGE AUM does not mean the EXPERT TAG 😛 Yes, PRACTICAL approach is very much important. Now calculate as I pointed about the said fund (whose name is already available in above image) and let me know whether the fall is Rs.7,000 or as per you just Rs.20. Then we discuss further who is expert in LIQUID FUNDS. What you say brother??

kindly provide me the meaning of middlemen .for filling of tax u need ca?????so he or she is a miedlmen …for treatment u need doctor ..than heor she is middlemen ?????????..like that in finance sector also u need advisor …they are not middlemen they are experts ….its seem like u are middlemen and dont have a proper knoledge of liquids funds and spreading rumors in public ..tell me the funds name of that liquid funds and i will give u the exacts impacts on nav after falling by 7 % cagr in one day ..thanking you ,

Anand-Do you think middlemen really required for investing?? Why not one can practice Do It Yourself approach? According to you all middlemen or as per you the so-called experts are real EXPERTS? Coming back to the liquid fund we are discussing, I already provided the fund name in above image and also provided the link of performance chart of VR. Please have a look and calculate and let me know the 7% down is whether around Rs.7,000 fall or Rs.20 (as per you). I said that the fall of 7% is from previous day NAV. Also, I said that you invested previous day Rs.1,00,000 at that day’s prevailing NAV. Now calculate the value of your investment after the 7% NAV with the number of units you are holding. Let me know the downfall from that invested Rs.1,00,000. Whether it is around Rs.7,000 or as per your claim it is just Rs.20.

Also, check the chart and let me know whether the fund recovered the loss or not. You claimed that such 7% down can be regained within 2-3 days in case of LIQUID FUNDS. However, it is still unable to reach the level of that NAV rate of pre-fall even after the tenure of around 2-3 months.

Let me know your conclusion. Eager to listen about LIQUID FUNDS, CAGR, ABSOLUTE RETURN from an expert adviser who is handling an AUM of Rs.600 Cr.

that fund is suspended due to they have done something wrong related to regulations.nothing to be related towards liquid fund performance ..its a matter of investigation .i cant give my recommendations till not cleared by amc .thanking you ,

Anand-Then what I wrongly said?? 🙂 I am pointing about this fund and you are expressing something different! Whether the fund is suspended or whatever, investor have to bear the loss. I am not saying you that you have given this recommendation to all your Rs.600 AUM based customers. But trying to say from this post that even Liquid Funds are also not safe until and unless you understand the underlying risks. Also, for your information, to understand Liquid Funds, one must not require months of time or an EXPERT. One can do on his own if he is ready to understand some basics of investment.

Regarding CAGR and IRR or ABSOLUTE RETURN, it is in my blood since 6-7 years. But I never claim that I am an expert. I am also learning. But surprised the way an EXPERT who claim to be having Rs.600 Cr AUM failed to understand what I said in above post.

Anyhow nice discussion. Shared on social media. Let readers enjoy our discussion and understand in a better way.

Can you please name your AMC, and fund which you managing, so that I can withdrawmy money and alert others too and make you popular

Kolkata office – most likely Essel liquid fund.

Mudit-Now it is your turn to withdraw from that fund 🙂

Basav,

I think he removed his comment now. Previously he mentioned his AMC name and Fund Name. I think it’s Tauras AMC 🙂

Mudit-Ha ha….They come and they vanish exactly like their BUSINESS 🙂

Very nicely explained the risk involved while investing in a liquid fund with the help of an example. Thank you 🙂

I appreciate your transparency and honesty in guiding the investors. It helps me creation of better awareness drives of my followers

Om-Pleasure 🙂

Hats Off , Basu.

Awesome Article.

Thanks a lot. I got the clear vision about the liquid Funds.

Any idea, about the rental act or long term lease act.(For Renting home)

As i am having money but do not want to buy the home in Pune (For 5o Lacs)

I fill its foolish to buy the home for living for such Price.

Regards

Mahesh Deshmukh

Regards

Mahesh Deshmukh.

Mahesh-Wait for sometime when Real Estate Act is live.

Sir, Thanks for the article and caution that the liquid funds are not as safe as it is recommended. Then which fund is as safe as bank deposit with more returns that the F.D.

Sankarasubramanian-Without knowing the reasons for your investment, its hard for me to recommend anything blindly.

Sir, I am retired person. I am ready to invest in mutual funds upto 10 lakhs. I desire monthloy returns through my investment over and above the bank interest rate. Some balanced funds are declaringmonthly dividends which works out up tp 9 to 10 per centage. It will be suffcient for me. I request your suggestion in this regard.

Sankarasubramanian-But these balanced fund 9% or 10% is not guaranteed.

Sir, Yes. As you said the balanced fund returns are not guaranteed. The Bank F.D interest though it is guaranteed, the rate of interest is very low. Then what is the alternative investment opportunity before us which is safe like bank F.D , as well as returns are also good?

Sankarasubramanain-You have to sacrify one between SAFE and RETURN. Also, sacrificing SAFE may not guarantee you RETURN.

Sir sorry to say that this financial does not have a proper knowledge about liquid funds .I think you don’t have proper knowledge of liquid funds .you quoted 7 % minus in one day .you must clear that point that it is cagr returns not absolute returns .example – 1 lakhs if someone invest in liquid funds and if 7% falls in one day it mean that u will incur a loss of rs 19.17 only .100000×7% =7000 /365mean loss of only 19.17 rs .In case any investor do FD and premature his Fd than he will charged 1% .liquids funds are fully safe and anyone can invest money without hesitation .Even few people’s says investment in lic safe but everyone must know that if u premature your policy u will incur 30 % loss on your capital investment value .liquid fund gives us a one working day liquidity .sometimes liquid funds comes down that only because of rbi monetary policy changes .In liquid funds they invest and diversify there portfolios in such a manner that capital is safe, only interest part may vary due to changes in monetary policies of rbi .

Anand-Can you elaborate more about your GYAAN? Let us say you have invested Rs.1,00,000 and next day 7% fall means your invested amount will fall to level of Rs.99,980.83 (Rs.19.17 fall as per your averaging of that 7% fall) or Rs.97,000? Also, if you are claiming LIQUID FUNDS, especially the above-said fund is so SAFE, then how many days investor have to wait to regain from the 7% of the loss to reach back to Rs.1,00,000 (the original invested amount). This is where the game of modified duration and average maturity will play a role. Hope you understood of what I am pointing 🙂

Do remember that the fall I am discussing here is a single day fall from its previous level. Hence, averaging that to a year is the wrong thing.

Hi Basava Raj sir

what about Arbitrage fund as alternative to liquid fund, at least compared to relative safety? some portion of emergency fund( with more than one year horizon) may be parked in Arbitrage fund.

Suru-Nowadays it became trend to recommend arbitrage fund because of tax benefit the fund is eligible for. However, if there is no such arbitrage opportunity and many funds following a single opportunity, then the fund may end up with less return. Hard to track the quality and performance. Because it all depends on the skill of fund manager in identifying the opportunity in early than others.