Term Life Insurance is a NEED for all those who have their financial dependents. However, now such simple product is turning to be a complex one. The latest entry is Aegon Life iTerm Forever Whole Life Term Insurance. Whether it is really required?

What is Term Life Insurance?

A Term Life Insurance is a Life Insurance product which provides coverage for a certain period of years. If the insured dies during the policy tenure a death benefit (or sum assured) will be payable to the nominee. If the insured survives up to the tenure of the policy, then there is no maturity amount.

The main purpose of this product is to cover your life risk due to uncertain death of earning member of the family.

Insurance companies only charge you to the tune of life risk they cover. There is no maturity amount in such plans. Hence, they are cheaper than Endowment or Money Back Plans.

Aegon Life iTerm Forever Whole Life Term Insurance

Nowadays there is a huge competition among insurers to lure the term insurance buyers. Hence, a simple term life insurance now turning to be a complex and confusing product for buyers.

The latest one to this list is Aegon Life iTerm Forever Whole Life Term Insurance.

Let me illustrate the difference between a typical term life insurance to Aegon Life iTerm Forever Whole Life Term Insurance.

# Normal Term Life Insurance

Let us assume Mr.X who is 30 years old purchased Rs.5 Cr term life insurance with the premium paying term and policy term is 30 years. If he dies within 30 years of the policy period, then his nominee will receive the sum assured amount of Rs.5 Cr. However, if survive till the policy period, then he will not receive anything.

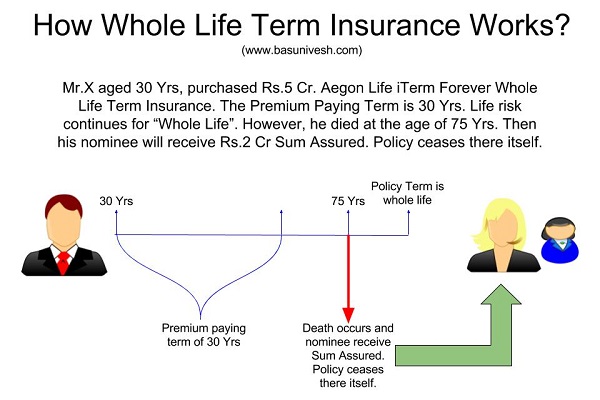

# Whole Life Term Insurance

Let us assume Mr.X who is 30 years old purchased Rs.5 Cr term life insurance with a premium paying term of 30 years. The term of the policy is WHOLE LIFE. Hence, the risk continues up to his last breath even if his premium paying term ends.

Assume he paid a premium for 30 years. But his life risk continues forever. Hence, whenever he dies then his nominee will receive the sum assured available in the plan. I explained the same with below illustration.

Now with above definition, only the difference is, in case of normal term life insurance the life risk ceases after certain policy period. However, in case of whole life term insurance, the life risk continues as long as the insured survive.

Hence, you may say that in normal term life insurance there is a change that your nominee may never receive the claim amount if you survive. However, in case of whole life term insurance, as death is sure to come one day. You are just arranging that much money as a fixed asset to them. When it will be available in their hands depends on your death!!

But hold on……Let us check the premium of this. Nothing is free and no need to rejoice.

Premium difference between regular Term Life Insurance Vs Whole Life Term Life Insurance

As you saw from above illustration, the product looks attractive. In no way, you are losing the money. Your nominee will receive the sum assured whether your death occurs today or after 100 years of age. But at what cost? Let us check the premium comparison.

If you compare the premium of Aegion iTerm Plan with Aegon iTerm Forever whole life term insurance, then the difference is huge.

For example, the premium for a 30 years old with Rs.1 Cr term insurance and premium paying term is 30 and term of the policy in iTerm is 30 years, then the premium for iTerm is Rs.7,497 but the premium for iTerm Forever, it is whopping Rs.39,570. This leads to a difference of around Rs.32,073.

Now the catch here is that even though in case of iTerm, policy features ends at the age of 60 years and the insured stop paying the premium. However, in case of iTerm Forever, you have to pay the premium up to your death.

Assume that one stayed up to 30 years. Also, he invested this difference of Rs.32,000 in an equity mutual fund which gives you 12% return, then the accumulated corpus will be Rs.86.49 lakh.

Therefore if you survive until the 60 years of age by buying the simple iTerm than iTerm Forever, you still be in a way losing money.

Insurance company wisely calculated this premium and returning the same to your nominee whenever you die.

Do life insurance required after retirement?

Many people by hook or crook want to get the benefits from term life insurance. They don’t want a single rupee to be lost for their term life insurance. Hence, without understanding the financial repercussion, they simply buy such products and end up in losing the money.

Also, you retire from your working life when you achieve your financial freedom. Once you achieve your financial freedom, then why one must need a life insurance?

Hence, always go with plain simple term life insurance than these gimmicks. One more point to note that this plan is not available for direct purchase. You have to buy it from online web aggregators. Not sure why such facility and not sure why such restriction. But better to stay away from such fancy products.

Conclusion:-

First of all, understand the basics of Life Insurance. You need Life Insurance if someone is financially dependent on you. Hence, you retire from your working life once you achieve your financial independence. Therefore, you may not need the Life Insurance during your retirement period.

Term Life Insurance is the simplest product. However, Life Insurance Companies have to play such gimmicks to lure customers. Hence, they go on adding such new features. But do remember that they are into business not for social cause. Hence, each such gimmicks cost you the more.

Again this policy is can be purchased only from online aggregators like policybazaar. Online aggregators act like agents of Life Insurance Companies. Hence, even though they claim that this is an ONLINE plan, but you are forced to buy middlemen cost. Hence, may the difference is at a higher level between normal term life insurance to this product.

Considering all these aspects, I suggest you to stay away from such fancy product and stick to plain term life insurance (even without riders).

Refer our earlier posts related to Term Insurance:-

- Joint Life Term Insurance Policies-Who can buy?

- 5 ways to save your Term Insurance premium

- 5 Things to do after buying online term insurance

- Term Insurance-Claim Settlement Ratio no more a big criteria

- Beware of Insurance Comparison portals in India

Hi, Recently ICICI have launched 10 yr,33 yr limited pay option in 99 yr term plan. Considering I am into IT and can earn good for the first 15-20 years, would it make sense to pay 535477( after 5% discount as per today on yearly preimum) as the cumulative premium for 10 years for 75 lakh cover and also be assured that return will be there on any event of death(natural death in old age, accidental, etc) till 99 years? Or is there something fishy in this? This sounds like a traditional life insurance plan after the modification in 99year term plan but sounds too good to be true as per the returns offered?

Dear Ankur,

Do you need the life cover up to 99 years?

I have taken 2 separate term policies of same type – Aegon Life iTerm Insurance Plan.

One is upto my 65 years age with monthly premium of 1122

Second is upto 99 years of age with premium of 1931. I am 39 years of age now and

I want to continue only one of above.

Looking at overall calculations the 2nd option seems better.

Please advice..

Dear Prabhakar,

Do you need Life Insurance up to ht age of 99 years?

Hi basu sir,

Another plan Aegon offer is that they give tem life insurance up to 100 years of age. Should i buy it for my father as he is gov. officer and will receive pension after retirement. Premium is 29000 for 53 years old person.

Ankit-Do he need life insurance up to 100 years of age?

Sir, my annual income is 4lak 60 thousands. Last year I purchased maxlife term plan for 32lak. This year i applied another term plan from aegon term plan for 50lak. Is it correct decession? . One quary is in aegon term plan on-line application (3lak from pli (active) , one lak from lic(surrender)) . This Information is not given . Is any future problem at the time of claim?. Sir please give me advice sir

Gorusu-If you already applied, then why DOUBT NOW? Better to share all existing Life Insurance products.

Sir, I am Sridharan. 31 years & govt salaried job (ARMY).

I plan to invest RS. 2000/- PM.

1. Life Insurance. Aegon life iTerm 50 Lakh cover upto 50 years. Monthly ?.330/-

2. I need to invest RS. 1500/- in three mutual fund (RS.500 each) through SIP for 20 years.

3. Please suggest me best mutual funds to invest.

with regards sridharan

Sridharan-I replied to your email.

Hello sir,

I am a 25 yr old female.recently I have inquired about the iterm forever plan from aegon life insurance.and they told me the premium amount is around Rs.11000 yearly for me if I pay till death which will cover upto 100 yrs of age. If I count the premium it will cost me around Rs.8,25000/ for 75 yrs and for 1cr coverage.i find this plan lucrative.should I invest in this plan or still there would be some hidden clause like increase of premium in later years.or I should go with some normal term plan which cover upto age 60 or 65 yrs ? Plz reply

Ankita-Do you need insurance during your retirement?

One should not need insurance after retirement as there will be very less liabilities.but as I was thinking if the chances of getting the death benefit is very high in case of 75 yrs term plan with such low premium like 11000,why shouldn’t we go for it ?but it must not be as simple as it seems.

Correct me if I m wrong as it will be my first insurance policy.

Thanks

Ankita-But what is the value of this insurance sum assured at your age of 75 years of age?

The sum assured is 1 Cr and the policy term is 75 yrs.means it will cover me till the age of 100 yrs.

So should I go with normal term insurance or return of premium plans upto 60 yrs of age ?

Or I should go for whole life plan ?

Ankita-But a simple term plan which covers up to your working life. Life Insurance is not at all required during your retirement. All these add-on features are just gimmicking.

Thanks a lot sir for your suggestions.

Hi,

I am investing in LIC Jeevan Anand(823) with risk cover of 5,00,000 for PPT of 21 yrs., Right now, premium is 28,000/year. Same policy protects till last breath for about 5,00,000…

Now, do i need to stop this policy and need to invest in EMF???, I am confused!!!!

Paras-It is up to you to decide. If you feel Rs.5,00,000 life insurance really protect your family in your absence then continue. Also, if you feel your 4% to 5% returns are best to you, then also continue. Otherwise, think seriously to discontinue.

Hi Basu,

I am planning to buy a term insurance. However i have some quires.

What should be the ideal term of policy.

Can you please suggest which one is better. Max Life vs PNBMetlife, which is having better claim settlement facility.

In Maxlife i am getting 1CR cover by paying premium of 16000/- for 75 year however in pnbmetlife i am getting cover of 1CR by paying 19706/- for 99 years. Suggest which one should i go.

Also is there any term insurance where they provide any benefit in case of partial disability.

Looking for your expert advice.

Amit-The ideal term should be up to your retirement age. To me all insurers are same. But choose the one with which you feel comfortable (I personally go with insurer who are old enough in the industry). You no need to have life insurance beyond your working age. Disability features will come into picture when you add accidental insurance as a rider. However, I suggest you to buy accidental insurance from general insurer rather than going by riders.

Thanks for your prompt response. I appreciate your time.

As you suggested that we should go with who are old in market. I don’t have any idea about that. Can you please suggest according which one is better.

Maxlife

Pnbmetlife

TataAIA

Or any other company

Is it fine if I go with 75 year or should it be less than that 70, 65…

Please suggest as I am planning to buy it before 10th.

Thanks once again.

Amit-Who are OLD-Data available in this post “Top 5 Best Online Term Insurance Plans in India in 2017“. Better to restrict the term to your retirement age.

Hi Sir,

I am 23 year old salaried employee. By 23rd of this month, I will be completing 24. Which term insurance is best one for me ?

Normal or Return of Premium or Whole life ?

Rathesh-NORMAL.

I am a central govt employee, My gross payment for a month is 52000/- out of which I deposit 20000/- in my PF.Kindly suggest me to better investment plan in mutual fund which can give me better returns than PF.

Ravi-Sorry…without knowing much about your financial life, it is hard for me to guide anything BLINDLY.

I am sridharan, 31 years old. Salaried employee.

Please suggest me..

Return of premium paid term insurance plan for 1 crore up to 60 years or 70 years

Sridharan-Do you think return of premium paid term insurance is the best option?

Yes sir.. please suggest me..

Sridharan-If you feel that is the right option for your money, then go ahead. What to suggest for? As per me, that option is a terrible mistake. To make you understand, just check the premium rates of with return or without the return of premium. You will notice the difference.

Hi Basu, This blog was quite helpful. I needed some suggestions on Term Insurance.

Is a combo of (Term Insurance + Accidental Benifit + Critical Illness Benifit) in one insurance better or buying them separately beneficial?

I am looking at ICICI’s iProtect Smart which gives 4 options:

1. Death Benifit [Cover can be increased in future]

2. Death Benifit + Accidental Benifit [Cover remains fixed]

3. Death Benifit + Critical Illness Benifit [Cover remains fixed]

4. All in one. [Cover remains fixed]

The first plan allows me to increase my cover in future, while the 3rd plan covers me against critical illness without option to increase cover in future. Which is better to be taken? Considering my age is 26, i will need to increase my cover at a later stage, and also i shall need protection against Critical Illness.

Also, is there a better Term Insurance plan that allows me to independently buy any Critical Illness or Accidental Benifit Rider with option to increase my cover and also buy any rider in future without opting for them in the beginning ?

Thanks.

Pratik-Go for option 1 and buy the accidental and critical covers from Non-Life Insurers.

Hi Basu, the stated facts are bit misleading. You mentioned in the article that insurance cover would be there for life term (beyond 30 yrs) even when we pay premium for 30 years. In the premium comparison, it is mentioned that premium need to be paid till the death of the insured. Higher premium till death for wholelife does not make sense.

Krish-It is not misleading. You have both options like a limited premium payment as well as lifelong premium payment option. Choice is your’s.

Hi basu, I have bought normal term plan from this company. Is it reliable or I should buy from a reputed company. Hope they will settle my claim in an unfortunate event!!

Niraj-Continue the same. If you declared facts properly, then no need to worry.

Dear Sir,

Well explained and Very well drawn conclusion. Overall, very nice article.

regards

RAJESH PAI

Rajesh-Pleasure 🙂