IRDA recently published the Annual Report for FY 2016-17. Let us find out the IRDA Incurred Claim Ratio 2016-17 and which is Best Health Insurance Company in 2018 in India.

What is the meaning of Incurred Claim Ratio or ICR?

Incurred Claim Ratio or ICR is a ratio of the total value of claims paid or settled to the total premium collected in any given year. This can be calculated as Incurred Claim Ratio or ICR=(Total Value of Claims Paid/Total Premiums collected)*100.

For example, let us say Company ABC settled the total claim amount of Rs.90 Cr in the year 2015-16. In the same year, it collected Rs.100 Cr as a total premium. In this situation, the incurred ratio stands to be 90%.

This Incurred Claim Ratio is applicable only to non-life insurance companies. For life insurance companies, IRDA publishes Claim Settlement Ratio. I have already written a post on the same. You can refer it at “IRDA Claim Settlement Ratio 2016-17 | Best Life Insurance Company in 2018“.

What to judge from the Incurred Claim Ratio or ICR?

This is the one of identifying the financial health of non-life insurance companies.

# Incurred Claim Ratio or ICR more than 100%

It indicates that for every Rs.100 they collecting as premium, they are paying more than Rs.100 as a claim for a year. In simple terms, your income is Rs.100 but your expenses are Rs.100 or more. So instead of profit, they are into loss.

# Incurred Claim Ratio or ICR less than 100%

It indicates that for every Rs.100 they collecting as premium, they are paying less than Rs.100 as a claim for a year. Such companies are making a profit as your income is Rs.100 but expenses are less than Rs.100.

What it indicates that less ICR means the company is in profit or eyeing on profit. So either they may insure the less risky individuals or groups (customers rarely come forward for a claim) or rejecting the claims just to profit.

However, rejecting claims only on grounds to profit will not work out for any company. They have to look for reputation, future growth, and regular guidelines. Hence, simply for the sake of profit-making, they can’t deny claims.

In my view, going with companies of high ICR or low ICR is risky. Hence, always choose a company which is in between both these points.

Remember once again, ICR is not main criteria in selecting health insurance. However, it is one among many criteria.

IRDA Incurred Claim Ratio 2016-17

Now let us concentrate on IRDA’s Annual Report for 2016-17. We will check the IRDA Incurred Claim Ratio 2016-17 and identify which is the Best Health Insurance Company in 2018 in India.

Here, I will divide the health insurance companies into 3 categories. One as public sector companies, second as private companies and the third one as standalone health insurance companies.

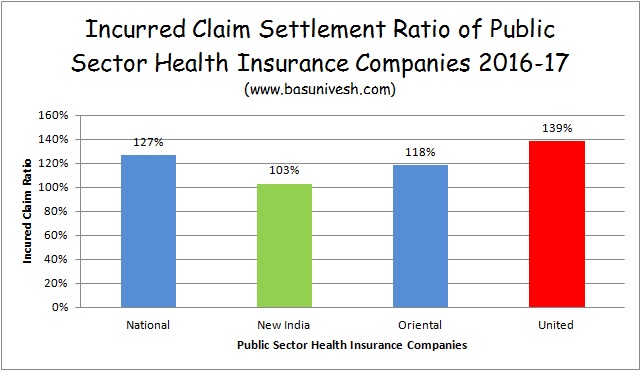

IRDA Incurred Claim Ratio 2016-17 for Public Sector Health Insurance Companies

Below is the data for the public sector companies.

New India managing the healthy 103% of ICR whereas United India’s ICR is just concerning. Last year for National it was 110%, New India 115%, Oriental 114%, and United was 122%.

IRDA Incurred Claim Ratio 2016-17 for Private Sector Health Insurance Companies

In below chart, I will show you the ICR of private sector health insurance companies.

I marked with red for those companies whose ICR is below 50% and above 100%. I marked with blue for those companies whose ICR ranges from less than 100% to 80%. I marked with green for those companies whose ICR ranges from above 50% to less than 80%.

IRDA Incurred Claim Ratio 2016-17 for Standalone Health Insurance Companies

In below image, I will share you the IRDA Incurred Claim Ratio 2016-17 for Standalone Health Insurance Companies.

Here, I marked with red whose ICR is below 50% and above 100%. However, Aditya Birla is the new entrant. Hence, we can’t judge or assume that this is worst data.

Best Health Insurance in India in 2018 -Checklist to shortlist the product

Now we understood the financial health of insurance companies. Let us move forward and identify the points before selecting the health insurance.

# Coverage Amount-Concentrate on Sum Insured and think beyond the current hospitalization expenses. If premium costing you more, then fill the gap with the super top-up plans.

# Buy early-Buying at the earlier age is best than postponing it. We don’t know the health issues. Hence, the insurer may reject your proposal. Hence, always buy immediately and never postpone.

# Understand the cover-Identify the features you want to cover. Covering all NOT POSSIBLE. Hence, try to identify the product which covers many illnesses.

#Individual or Family Floater-Decide whether you want to go for individual or family floater. It is always best to go for an individual if the age of any one member of the family is so high than the others. For example, in a family of 4 the oldest person’s age is 65 years and rest of other 3 members age is less than 50 years, then better to buy an individual plan for that 65 years old individual and rest 3 members can buy a family floater.

Because the premium is fixed based on the age of oldest person also.

# Entry Age and renewable clause-Check the entry age and for how long one can renew it.

# Identify the company which covers existing diseases at early. Usually, all insurance companies have a waiting period 3-4 years for existing diseases. However, if your concern is to cover the existing diseases, then give first priority to this point.

# Check for room rent capping.

# Check for the co-payment clause. Higher the co-payment means lower the premium for you. Co-payment means how much you also have to pay in a total bill. If the co-payment clause states 20% co-payment, then for all bills claimed, you have to 20% and the rest 80% will be payable by health insurance company.

# Check for exclusions. If you feel the exclusions listed may be uncomfortable to you, then skip that product.

# Check for hospital network availability in your city or town. The cashless hospital benefit is better than producing the bills and waiting for claim settlement.

# Read carefully the wordings of policy brochure. If you have doubts on any feature, then try to clarify it NOW itself.

# Avoid all common features, which companies try to highlight.

# Check for No Claim Bonus company offers.

# Check treatment wise limit if any.

# Check the premium rates. Especially check the rates for older age rates as few insurers jump the rate drastically for older age coverage.

# Finally, if you feel the sum insured you opting is not within your budget, then go for sum insured according to your affordability and opt for a super top up plans.

Hope this much information is enough for you in shortlisting the health insurance product.

Refer other posts related to Health Insurance:-

- Health Insurance by Banks – Should you buy?

- GST Rates on Life Insurance, Health Insurance and Car Insurance Premium

- Life, Health and Vehicle Insurance Agents Commission in India

- Health Insurance Portability in India – Features and Process

- Health Insurance Regulations 2016 – 5 changes you must know

- Multiple health insurance policies -How to claim from all?

- Top Up Health Insurance Plan & Super Top Health Insurance Plan-What are they?

- Best Senior Citizen Health Insurance in India-Product Comparison

Dear sir , Iam having a Star Health insurance mediclaim policy, and want to switch over to Religare Health Insurance, please advise, it’s good for future or? Thanks OP sharma

Dear OP,

Check with Apollo or Max Bupa too.

hi basavraj,

need your help in selecting policy , as am existing policy member of Apollo Munich ( 3year old) for 10 lakh , which I bought in 2016 , but not used any claim so far and now my policy is , I am looking for policy portability in max bupa or ICICI Lombard policy but feature wise Max Is better and premium wise ICICI , am already insure through company policy for 6 lakh for my company and 7 lakh through my wife company which means 13 lakhs

need suggestion for below

1. How much amount I should go for slection for SUm insured – 5 lakh or 10 lakh as per current Hospital expenses ?

2. to go for ICICI or max bupa ?

3. which one is better in claim settlement as per IRDA ?

4. Should I go for Portability from Apollo munich or no need ?

5. should I go for any government policy or private ?

6. what kind of loss I am going to make if I switch from Apollo to another policy , as I have not claimed any claim for last 3 years apart from no claim bonus ?

7. is there any other private company policy better like TATA AIG ?– pls suggest as per company performance and reputation in claim settlement

Amit Bathla

9871005094

Dear Amit,

1) 5 lakh base plan and then go for super top up for 10 or 15 lakh.

2) Both are same to me in terms of claim settlement and business module.

3) Replied already.

4) But why?

5) First look for your need, then the question of which company.

6) If port, then no loss but the features changes as per new policy.

7) Why such in-depth research?

dear basavraj,

1. as I have already policy of 10 lakh of Apollo so I cannot port less than 10 Lakh , so 5 ;lakh base plan I can only buy as new policy not through portability – can you clarify more about this

2. what is claim settlement ratio of Max bupa

3. which plan Is better in max bupa for portability for 10 lakh and with better features

4. pls suggest if any other better policy with good feature like Max bupa but premium low and also good claim settlement

Dear Amit,

1) If idea is to port, then go for 25 lakh super top up with 10 lakh co-payment.

2) It is there in the above post.

3) MaxBupa Heartbeat.

4) Hard to say with the limited sharing of your requirement.

Hello Basavaraj!

Can you please share your thoughts on Cigna TTK Prohealth plus policy?

I’m 30 and about to get married, looking for a good beneficial family floater. Thanks in advance.

Dear Paresh,

If the features are looking good for you, then what is the doubt?

Hello Basavaraj !

I am looking for 2 health insurance policies

1) For myself & my wife – Age 33 & 31

2) For my Mom – Age 54

1) For myself & my wife : No Pre-existing disease till date.

2) For my Mom PED is Diabetes.

What i am primarily looking for is :

i) Insurance companies who settle the claims without creating any issues, with good claim settlement ratio & At a later stage, increase the premium only as per age slab & not as per the past medical / claim history or as per their wish.

ii) Maternity cover (Only for policy covering myself & wife).

iii) No capping on room rent & ICU / ICCU.

iv) Covers OPD.

v) Restore / refill benefit in a policy year after exhaustion of sum insured + Acquired bonus coverage.

vi) Covers almost all day care treatments.(Waiting Period applicable)

vii) Less waiting period for PED.(In most of the cases it is 4 years)

I have shortlisted 4 health insurance companies getting close (but not all in one) to my above listed criteria:

1) New India Assurance – New India Mediclaim Policy

Fulfills : i), ii), v) & vi), Doesn’t fulfill : iii), iv), vii)

2) National Insurance – National Parivar Mediclaim Policy

Fulfills : i), ii), iv), vi) & iii) * Only in case of network hospitals,

vii)* Covered from Day 1 if opted for optional PED cover of Diabetes and/or Hypertension with additional premium of 13 to 30% depending on which one needs to be covered. Doesn’t fulfill : v) * Major drawback

3) Star Health & Allied Insurance : Star Comprehensive

Fulfills all the above except criteria iv) & vii)

4) Apollo Munich : Optima Restore

Fulfills all except ii), iv) & vii).

Major advantage is with criteria v). Optima Restore covers for same person, same illness in the policy year.

For myself & wife policy, i think i should go ahead with 10 lakh coverage from Public Sector with New India assurance – New India Mediclaim Policy & Super Top up from either Star or Apollo.

What do you say ?

For my mom : Already has Star Comprehensive policy of 7.5 lakhs coverage with 1 year completed & no claims made yet. 3 years more to go to cover Diabetes as PED.

Thinking of having a Super top up for her as well from may be New India assurance or National Insurance.

Is this the right time to go for Super top up ?

Your views / suggestions on the same will be helpful.

Looking forward to hear from you.

Thanks in advance

Regards

Amit

Dear Amit,

Your WISH list is LONG and you will not find all the features in a single product. Regarding your health insurance and your mother’s health insurance, you go ahead with the companies you are comfortable with. However, try to buy super top up also from the same insurance company where you have the base plan.

Thanks Basavaraj for your inputs.

You mentioned in your comment to “try a super top up from the same insurance company”

My Questions : 1) Does it gives any specific benefit ?

Also can you throw some light on important aspects to be looked for when selecting a super top up ?

2) Is it recommended to have 2 health insurances from 2 different companies ? If yes, 1 from public & another one from either private or standalone sector is Ok ?

Thanks & Regards

Amit

Dear Amit,

If your base plan and super top up plan is under same health insurance company, then the claim process will be easy.

Thanks a ton Basavaraj !!

Hi. Will i be able to avail tax benifits if i buy a 2 or 3 year health insurance policy at a stretch? (with a max of 25k pa)

Dear Sanjay,

Yes.

Basu Ji,

I am planning to take health insurance for my father. He is 70 years old and has hypertension, so I dont have much options. I find that Aditya Birla is offering me the policy closest to my requirement and within my budget. I was preferring Religare but it’s expensive and for Cigna TTK, I have received some bad reviews.

How is your assessment for Aditya Birla health insurance? For ABHI the premium is around 34,000 whereas for Religare it is 42,000 for similar (not same) terms and conditions.

Dear Praveen,

If it is matching your requirement, then go ahead.

Hi.

I want a mediclaim for myself(45), spouse(49), son(18),daughter (15).In 2017,we opted for MaxBupa with a premium around 18000.But next year they increased it to around 24000(they said due to some change in govt. slabs). But I discontinued it as they couldn’t stand on their words of premium increase. Their representative told me that it would only increase around 600-1000 rupees. So, now i want to go for another health insurance for 4 of us. Please suggest which would be better-MaxBupa, Religare, Apollo Munich, HDFC Ergo. Or some Public insurer.

Dear Ritu,

Check with Apollo or Maxbupa (even though you have earlier with them).

I have a family of 3 in need of medical policy. Adults 2 (55 & 46) and one son 8. Cover Rs5 lakhs and premium not more/around Rs24000.I have been studying policies/companies for the past one month(!) and the conclusion does not seem to be in sight.Health insurance laws rules seem to be more complicated than income tax!

I am desperate (age 83!). Would like to end the search soon. You sound very thorough and knowledgeable.

Can you suggest some companies in order of preference

P. Ranganathan IRS (RETIRED)

9449038493/7349310550

Dear Ranganathan,

You will not get everything in a single policy and that also within your budget. Check with Apollo Munich or MaxLife.

Thank you very much.

Hello Basu,

Again thanks for this post..

Just wanted a little help…

Based on your research on this post, i was planning to take a health insurance floater policy for a family of 3.. (Myself, my wife and my daughter). I was planning to for a 10 Lakh base policy and also opt for a super top.

I had shortlisted

1. New India Assurance

2. Max Bupa

If its just the base policy then New India was working out cheaper… However with TOP ups from the respective companies, the total premium (Base + Top up) .. Max bupa was working out better..

And as we understand all these Health insurance companies nearly have the same type of exlcusions etc..

Advantage of Bupa Vs New India what i could see

1. Room Rent Capping :

Bupa no capping (Except for suite and baove category )

New India it was max 1% of the Cover.. SO basically 10000 in this case

2. NCB :

Bupa has this NCB of 20% every year.. to max of 100% accumulation

New India doesn’t have any.

3. Health Checkup: BUPA provides Annual Health Check up for all members) .. New india doesn’t..

Healt check up for 2 members would atleast cost 5k min.. so in a way its benefit..

4. Refill Benefit : Possible in BUpa.. (If we have exhausted our Base Sum Insured, you are entitled for an additional sum insured equal to the base sum insured for a subsequent claim in the same year, provided it is for an unrelated illness) ..

5. One Advantage of NEW INDIA :

The age bucket of new India was quite large.. and for that bucket the premium would be same or very nominal change.. The have age brackets of 36-45, 46-50, 51-55,56-60, 61-65..

When we compare this with Bupa.. they will give a policy for 2 years at a strecth, however the premium after 2 years would be prevalent at that time.. and this difference looked large to me.. if i consider even a agre bracket for 5 years..

I currently fall in 36-45 bucket and i would still have another 5 years before my premium drastically changes..

These were some major differences i could see..

Just wanted to get a quick opinion of yours.. and see if i am in the right path..

Please let me know, what would you have looked at based on your experience..

Regards,

Munna

Dear Munna,

Well researched 🙂 Go with MaxBupa.

Hello sir…I am 34years old having wife and a baby of 9months, I am working in a private company. My job is not constant in one particular location.

Q.1) Through my company I have my medical policy with IFFCO TOKIO.

Is it possible that after changing the company will this policy be continued?

Q.2) I need health policy which having easy claim settlement method. Policy bazzar suggested to take RELIGER, but after reading various reviews now I am totally confused/afraid to take it. What should I do kindly suggest me the trustee policy.

Deepak

7069184885

Dear Deepak,

1) Sadly NO. That is the reason it is always best to buy on your own one also.

2) Those who can claim EASY may not be EASY at the time of claim. Hence, it is hard to say so which is EASY settlement company. Look at features at first and then decide.

Have one policy of your own, atleast of 3 lakhs , Family floater , this will keep you safe , dueing transition from one company to other , and other part is , it will also go on acruing No CLaim bonus , my 2006 policy of 3 lakhs has now become over 5 lakhs , due to No Claim Bonus .

Hi Basunivesh,

My age is 32.i am state government employee. Annual salary 6lakhs

I want to take life insurance for one Crore without any rider. Premium should be low

I want separate health insurance for my son(age 3)and husband (age 36. Annual income 13 lakhs) with accidental cover, disability cover and critical illness cover

Please suggest

Dear Priya,

Regarding Life Insurance, you can check with Aegon, MaxLife or Kotak (for lower premium). Regarding health insurance, why a separate plan rather than family floater?

Dear Basu,

Thanks again for your helpful article. I’m 40, I want to take a floater policy for me, my wife and kid. I’m unsure about which policy to go with. I know a star agent, he suggested Family Health Optima (10 lakh cover) or Star Comprehensive (7.5 lakh cover). The comprehensive plan seems to be expensive. I’m currently covered by my employer and don’t expect any claim from my personal health insurance in the next 5 -10 years. Does the higher premium of the comprehensive plan be worthwhile? As per my understanding for SA of 10 lakh of “Family Health Optima Plan”, the room rent is not an issue. But they have a co-payment after 60 years of age. I’m concerned about the high premium of “Star Comprehensive” for the old age, when it’ll be more than 1 lakh for two of us.

Dear Amartya,

Having your own health insurance is the BEST option. Hence, don’t think of the future premium (especially about your old age). But cover it at first.

Hi Basu,

Thanks for your suggestion. Any thought on Star Family Health Optima (SA- 10 lakhs) ?

Thanks

Dear Amartya,

It is hard to say anything about a particular product without understanding your need.

Dear Basu,

I took 1 umbrella Medicalim policy from National insurance for my Father, Mother, Myself and wife in 2011

1. They have increased my premium more than 140% in last 4 years eventhough i didn’t claim anything since 2011 till date.

2. My Father has completed age of 71 yr this year and NI company has increased premium by 43% and imposed a NEW condition during renewal of policy for paying only 75% for Sr. Citizen claim….I am shocked..!!!

currently, I have paid premium of Rs. 29000/- for Rs. 4 Lc SA.

Could you pl. suggest

1. If Insurance company can impose new condition any time during renewal of policy/product..?

2. Should i continue with NI or switch to other NI company.

3. Pl. suggest other good company for Umbrella Medicalim policy.

Best regards,

Ashutosh

Dear Ashutosh,

It is not wise to include in your health insurance. Because the premium will be fixed based on the age of the oldest family person. May be due to the risk involved in your parents health, they might increase the premium drastically (once they fall in next age group).

1) As per my knowledge NO.

2) Better to separate your parents insurance from your insurance (wife and you).

I hv national insurance 5 lac. But room cap is 5000 only. I want to port . So tell me which is best. I figure our these 4 below company which hv no cap on room rent..

Apolo munich optima restore

Icici complete i health

Hdfc gold ergo

Bupa max

Which is best company in ur thought…

Dear Pankaj,

You can go with Apollo.

Thanks…

sir GO to religare health insurance best and cheapest

Dear Sharafat,

How it is BEST? So anything that is CHEAP is eligible to buy?

Perhaps you have written wrong that “it is mandatory to link aadhar with MF”.

Dear Utpal,

Above post was written before the recent supreme court judgement.

Hi Basu,

I have taken Aditya Birla family floater health insurance 4 months ago and now I felt that I have missed some information about my wife’s health condition. Should I contact aditya Birla and informed them ?

I have read in some article that insurance company rejecting claim for these reason also.

Dear Kumar,

Better to approach and inform the details.

Thanks for the wonderful write up, it helped me understand this settlement claim ratio

Dear Marwyn,

Pleasure 🙂

Dear Basu,

Thanks a lot for your wonderful service.Appreciate a lot.

I am planning to buy health insurance however I am an NRI and planning to return in 2-3 years.

I did some research and I have few questions as below:

1.Can NRI take health insurance in india? I did not find answer online.

2.I like Appolo Munich family floater plan.What is your opinion on this insurer?

3.Most of the online resources suggest insurance companies which are private companies.What is your take on government companies?Are they equally good in terms of customer service and claim settlement speed?

Appreciate your response on above.

thanks

Dear Sravan,

1) Yes.

2) You can choose it.

3) Yes, both are equally good. However, data suggests that in fact, Public Sector Insurers claim settlement is high than private players. But I can’t guarantee you about their service and speedy settlement.

Dear, I have already travel insurance for New Zealand which was i buy it from Bharti Hexlife, Now i want to extend it for more days, i was writing to them but they have no any replay.Now you imagine the service of Bharti Hexalife?

Now suggest to me can i buy new travel insurance and which one is good.Currently i am in New Zealand.

Dear Harhajan,

If they are not responding properly, then go with other insurers. Regarding choosing the insurance, refer my post “Best Accidental Insurance Policy in India-How to choose them?“.

Dear, I am 59 year old retired, i need a mediclam (Hospitalization) policy for me and my spouse.Please suggest me good one for 5Lac cover.

Dear Harhajan,

Check with few Public Sector Companies.

Hi Sir,

Thanks for writing this article. I want to buy health insurance plan but according to your site data, some companies ICR is not good but on other websites like: bankbazaar.com, trucompare.in etc shows good ICR for those companies.

How can I check the real data from IRDA? and which health insurance plan is better with maternity cover?

My age is 34 and wife age is 29.

Thanks

Dear Arjun,

Do one thing. Don’t trust either my data or other data. Check IRDA annual report and you will find the same.

I want to need a insurance policy regards health

Universal sompoo is better or not?

Dear Pawan,

How you selected that company only?

Hello Sir

I am 47, female, diabetic, BP, thyroid. I have son 21 yrs old. No spouse. Do you suggest we buy individual plans or floater? Which companies are preferred based on your analysis above?

Dear Ana,

Go with family floater.

Dear sir,

I have taken SBI arogya top up policy(insured amount 50lakh from deduction of 1 lakh),for my father(age 57, diabetic ) mother(aged 49)..completing second year Coverage on August 2018.right now,I come to know about “no copay” and “super top up”.can you please suggest me any better policy ,I like to go for portable of existing SBI arogya top up.

Dear Chandra,

It is best to switch to super top up plans. Refer to my post “Top Up Health Insurance Plan & Super Top Health Insurance Plan-What are they?“.

Please send details claim ratio of stand alone health insurance companies in india 2017-18

Dear Neelam,

This is the latest data available with IRDA. Hence, you have to rely on this data to decide your purchase. I request you not to share your personal details on such public platforms (like your mobile number).

I was searching for Cancer coverage policy and was inclined for ABSL cancer coverage…. considering the different advantages…

Should I go by the above insurer ?

Bose-You can go ahead if your requirement are matching with said product.

Sir, i wanted to buy health policy for my son aged 31. Please advise should i go to private or govt.

Praveen-Refer above post.

Hi

Is hdfc ergo super top up of net 8 lakhs better for parents aged 54 and 60 ..

Thanks for the reply in advance

Nishita-If you are OK with 8 lakh and feel the features matching you, then go ahead.

Your Article is very informative. So, I want to ask that which is a better policy between New India Mediclaim Policy and Appolo Munich Optima Restore for Individual Only in terms of Claim Settlement (Premium not an issue)? There is a perception that private companies try to reject claims on one basis or another, so its better to opt for a PSU, is this argument correct?

Nitish- Your understanding regarding claim settlement is correct.

sir

i am planning for cigna ttk health insurance, pls confirm if it is good decision.

Rohit-If product features are suitable to you and the premium is affordable to you, then go ahead.

Dear Basavaraj,

I tried posting this question before, however it is not appearing in the forum.

Can you kindly tell me what are the rules and regulations governing health insurance for NRI in India? If nothing is mentioned in writing can it be assumed that NRI’s are eligible? I am asking this as in life insurance I have seen many companies telling in writing about NRI’s been not eligible eg:LIC; however in health insurance I am unable to seen anything in writing. Kindly Clarify

Arun-You have to directly contact respective health insurance company and ask the eligibility for NRIs.

Kindly let me know which medical policy is best among these.

1. ICICI Lombard i-Health

2. Max Bupa Heart Beat or Health companion

3. Appollo Easy Health or Optima restore

4. Religare Care

5. Bajaj Allianz Health Guard

I am 42 year old and want to cover my wife and daughter along with me.

Is it time to buy separate critical illness cover.

Vinod-To me all are equally good and bad. If you have a family history of critical illness, then better to buy separately.

In Max Bupa – Heartbeat is better than Health Companion because the latter has 48 months waiting period and former has only 24months waiting period.

Amma-If waiting period is your concern then go for Heartbeat.

Looking for health insurance for SA=5Lakh.

Sort listed Cigna TTK ProHealth Plus and Royal Sundaram lifeline supreme. Both premium is around 5500.

Factors I considered for my decision making:

1) Co-pay: Cigna has co-pay of 80:20 after 65 years (can be brought out by paying extra 18% premium). While RS does not have the same lifetime.

2) International checkup: Cigna covers till SA, RS does not provide the same.

3) Reimbursement settlement: Cigna says can be done online via soft copy, RS has to be couriered.

4) Cashless Tie-up: Cigna has around 5000 while RS around 4100.

5) AYUSH: Cigna-NO, RS- YES

5) OPD: Cigna provides 2000 (can incld AYUSH), RS-NO

The most imp factor I felt is co-pay option to distinguish the same.

Please advise whether Cigna or RS?

Satbir-For me both are equally good.

Do I need to consider co-pay or international checkup? That’s my last point to take discussion I think, it’s a very imp factor for health insurance I believe.

Satbir-Co-Payment clause you have to check. If you feel international check-up required, then check the same also.

really confused on co-pay or international.

Cigna TTK (International YES, Copay- 80:20 if age>65 yrs, OPD-YES 2000)

RS (International NO, Copay-NO, OPD-NO)

Please suggest which would be better

Satbir-What confused you about co-payment when they actually clarified clearly?

Clear with all features.

Just confused on taking decision, do I need to choose co-pay or International checkup factor?

Satbir-Concentrate on co-payment only.

Hello sir, my age is 29 and my wife 24 so I am going to buy health insurance but there is confusion for choosing between public sector or private sector company. Which is best company for all parameter by you. Public sector or private? Please suggest

Prashant-For me all are equally good and bad.

Hi sir,

I am planning to take health insurance. i have gone through your suggestions for takin Critical illness insurance, When i enquired Religare(CARE: Comprehensive Health Insurance), they were saying their insurance will cover all, including critical illness. No need to take separate critical illness. Is it true.. Kindly let me know whether to go ahead or not.

Thanks

Arun

Arun-I think they want sell CI as rider. Stay away from this and buy pure health insurance only.

Hi Sir,

But when i enquired, they did not mentioned any Rider for this CARE-Comprehensive Health Insurance. And they have NCB Super, which they will add 60% for the first two years. Means, if i take 10lac policy, they will add first year NCB has 6 lacs, total becomes 16lac, And second year same 60% applied for NCB, the total sum assured becomes 16+6=22 lacs, from third year onwards it is 10%, one lac added total becomes 23 lacs..

Arun-Check and take the decision as per your requirement.

Hi Basu, I have the same policy for my Dad who will turn 62 next month however I’m in a huge dilemma since his insurance is due for renewal by next week and the company has now increased the premium from Rs.22K last year to Rs.34k this year – reason given to me is that he’s in a higher age group, I agree the premium goes up in specific age groups but a jump of almost 50% is ridiculous for any insurance!! When I said this they were ready to reduce the premium by 15% which I find very strange. now, my problem is that I cannot port to say New India Assurance (since I was thinking of a PSU insurance) as the time is too little and it is the 3rd year with Religare in terms of waiting period… please advise what can I do in such a situation?

A little history on the health of my Dad – he underwent a bypass and two angioplasties in the last 4 months and my corporate insurance took care of most expenses fortunately…

Dear Isha,

There are two reasons to increase in premium may be-One is the age group and another is his last hospitalization. However, considering his health issue, I feel it is best to continue. Because if you opted for portability, they either may deny the proposal or put some exclusion clause.

Hence, please continue the same and use your corporate health insurance for any further claims.

Thanks Basu! I never used the private policy for Dad’s treatment. I went with m corporate plan as there is very little scope for rejection and it covers pre-existing illness. Religare claims that the new insurance premium is purely for the increased age group but a 50% increase every 4-5 years is not ethical/correct?

Dear Isha,

I completely agree that the quantum of the increment is totally unacceptable. Let them give in writing regarding the reasons to raise to this level. Based on that, you can easily knock the doors of the Insurance Ombudsman.

Thank you so much! i didn’t know how to approach this situation… I shall request your advice if it reaches a point where I need to approach the IO. I was also contacted by Star Health for portability for past few weeks and they said they can port the policy even if the renewal is due in next two weeks – I’m looking at their benefits vs religare.. is it good to make it a floater to inlcude my mom or would it turn out to be more expensive than individual policies? Thank you again for all your help 🙂

Dear Isha,

Separate your mother from your insurance.

Dear Basu, The company that was willing to port my fathers policy now thinks he’s a risky customer since he underwent heart procedure in the last few months. What I’m unable to understand is – will this mean my current insurance company (Religare) will charge me higher premium as loading charges or they cannot do so because this ailment was diagnosed almost after two years of holding the policy. They are already charging me loading fees for Diabetes. Now, I’m in a fix with the due date approaching. My understanding is that Religare cannot charge me higher premium as this health condition is diagnosed after two years of having policy – is that right?

Dear Isha,

You have valid point and rightly saying. Let them give in writing like email and write an email directly at higher level of the company (at first), if they not listen then you can knock IRDA.

I finally received a response from Religare saying they are not going to charge anything extra for the new health situation. So, I’m now paying them only for the increased premium and loading charges for Diabetes. Still they are charging me atleast 40% more than previous year 🙂

Dear Isha,

It is great to know. However, I still suggest you to go ahead with Religare (even they are charging you more).

Dear Sir..

It’s great article..

Nice work..

Sir, where i can get the last 5 years ICR of public and private health insurance firms ?

Vinayak-In IRDA website you have to search for annual reports.

Hello sir,

My age is 30 and I am looking forward for health insurance for me, wife & kid and another for my parents aged 63 & 59(no illness)

I have no idea regarding the health insurance.

I have read your article and is very helpful in understanding many thing.

Still I would like to request you to kindly suggest few good policies and companies.

Shagir-Hard to point any few. Better you first understand your need and based on that choose the product. If you found any difficulty in understanding, then we can discuss.

Hi Basu Sir,

I have purchased Apollo Munich health Optima Restore for myself (Individual plan – 15 lakh coverage) and Max Bupa for my wife and daughter (Wife is primary applicant, Family floater – 25 lakh coverage).

Now my question is,

1.) Is it ok to have 2 different health policies in the same family?

2) Is it ok to to have wife as primary applicant in Family Floater when husband is still alive?

3) Should I continue with 2 separate health policies or should I have continue with only one health policy including everyone.

Please advice.

Thanks

Sharath

Sharath-I have already replied to your email.

Thanks a lot Basu,

[ answer : better to buy a single family floater]

Is it because any problem during claim?

Sharath-Claim, simplicity and also the cost.

Thanks Basu

Dear Sir,

A very nice article you have written. Just one query. With reference to the chart for IRDA Incurred Claim Ratio 2016-17 (Private Sector Health Insurance Companies), please suggest if the blue coloured companies are more preferable or the green ones?

Rahul-Green one are more preferable as they are neck to neck when it comes to profitability.

Thanks for your prompt reply. I highly appreciate your help in helping me chose the best possible policy / company.

Sir my mother age is 52 years, currently staying in pune maharashtra, so can u guide me which insurance company I can go for and safeguard her interest. She doesn’t have any illness as of.

Nilesh-Check with Public Sector Companies.

u can go through with star health which is very gud as per claim settlement and other services

Harish-May I know what prompted you to refer that PARTICULAR company?

Hi.

Does it mean that we should go with company having highest ICR…thereby meaning easy settlement of claims and disbursal of claim amounts.

Please also suggest a good cancer protection insurance plan and company.

Anuj-Higher ICR means company under loss right? Refer my post “Best Critical illness policy in India – Comparison Table” or “LIC Cancer Care (Plan 905) – Features, Benefits and Review“.

Is it better to buy critical illness plan or a cancer protection plan

Anuj-Better is Critical Illness.

Hi,

Thanks for the analysis but did not find details of the claim settlement ratio for health insurance companies.

I am intrested to know how private sector is competing with the public sector health insurance plans

Ashirbad-The above article is related to the same only.

Hi,

I am talking about the claim settlement ratio. Could you help me that? Your article talks about ICR

Ashirbad-For Health Insurance it is ICR for Life Insurance it is CSR.

oh i see. I thought ICR meant how much you as a company gave back in comparison to the amount of premium your received from the market and therefore if it was more than 100%, it meant the financial health of the company is not so good.

So do you mean that higher the ICR- safer is it to buy policy from that company and vice-versa?

Ashirbad-ICR is the data which related to Health Insurance. Regarding the ICR, refer above post.

Very good article man. Keep up the good work of enlightening the general public so they dont fall into the trap of insurance agents. My father bought lots of unnecessary insurance covers throughout his life which was adviced by family, friends and agents and is regretting now. That generation considered insurance as an investment.

Ashwash-Pleasure 🙂

U r only stating paid claims in a year. I presume it is FY. What about outstanding claims?

U r stating premium collected during the year for ICR. Suppose claims for the FY are 10 crores, and on 31st march, there is a huge policy underwritten of 100 crores?

Suresh-Outstanding claims details for Health Insurance separately not available in Annual Report of IRDA. Hence, hard to judge. It may or may not be regarding your numbers.

MY FATHER AGE IS 67 now , HE IS CONTINUE WITH National Insurance Varishtha Mediclaim from last 2 years . As its only 1 lakh cover for normal claims & 2 lakhs for critical care . please tell me some suggestion which will increase the SA with minimum pocket pinch for him ( not more than 15K per year).

Subrata-Go for super top up plans.

Sir do the ICR of public sector insurance companies include all types of general insurance or only Heath

Anurag-It is only HEALTH.