Recently LIC declared the bonus rates for the year 2017-18. Let us see the complete details about LIC Bonus Rates for 2017-18 and how they affect your life insurance returns.

What is the meaning of bonus for LIC policies?

When you buy a traditional with profit product from LIC, then your returns from such policy mainly depends on what will be the rate of bonus. LIC declares bonus on the yearly basis. Usually, you will not find any such drastic change. But it is always better to track the bonus rates.

Let us say you bought LIC’s Jeevan Anand for the term of 20 years and sum assured as Rs.5,00,000. If LIC declared bonus as Rs.45 for this product, then the calculation will be as below.

The bonus rates will be based on three criteria.

# Term of policy-Higher the tenure means higher the rate.

# Sum Assured-LIC bonus depends on per Rs.1,000 of Sum Assured. Hence, if you bought higher sum assured policy, then your bonus accumulation will be at the higher end.

So from above example, if LIC declared you Rs.45 as bonus per Rs.1,000 sum assured for 20 years policy, then the bonus accumulation for that year will be as below.

Rs.22,500=(Rs.45 x Rs.5,00,000)/Rs.1,000.

Remember this Rs.22,500 will not be payable to you. But it will be with LIC and you receive this amount during the time of death claim or maturity. The most important point to note that they will not add any amount on this Rs.22,500. It will remain same till the period of death claim or maturity date.

How to calculate returns for your LIC policy?

In simple, I explained how to calculate bonus for a year. But LIC offers different products like the endowment, limited endowment or money back plans. In such a situation, you may find it difficult to calculate returns on your LIC plan. Hence, I created a video about this.

This below video will explain you about how to calculate returns on your LIC plans using excel sheet. It is too simple and convenient for you to calculate.

LIC Bonus Rates for 2017-18 for closed plans

Hope you got the clarity about the importance of bonus rates for your traditional plans. Now let us concentrate on recently declared LIC Bonus Rates for 2017-18.

The below reversionary bonus rates are applicable for policy year entered upon during the inter valuation period i.e. 01/04/2016 to 31/03/2017 and in force for full sum assured as on 31/03/2017. It would apply to policies resulting into claims by death or maturity (including those discounted within one year of maturity) or surrendered on or after 01/01/2018.

The above interim bonus rates are applicable to policies in respect of each policy year entered upon after 31/03/2017 and result into claims by death or maturity (including those discounted within one year of maturity) or are surrendered during the period commencing from 01/01/2018 and ending 9 months from the date of next valuation.

No cash bonus has been declared in respect of New Jeevan Akshay – I (Plan 146).

This time, I separated the plans in two ways. One for the old policies which are closed and another list for the new policies which are currently available for purchase.

Note-The Bonus rates which are marked in red are changed from earlier rates. For example, earlier for Jeevan Surabhi (Plans 106, 107 and 108), the bonus rate for 11 to 15, 16-20 and above 20 years plans was Rs.38, Rs.42, and Rs.44 respectively. Not it changed to Rs.34, Rs.41, and Rs.50 respectively.

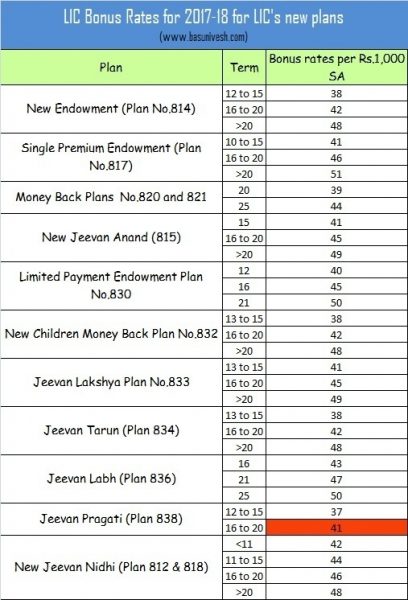

LIC Bonus Rates for 2017-18 for new plans

Let us now look at the bonus rates of the new plans which are currently offered by LIC.

Note-For Jeevan Pragati (Plan 838), earlier for policies whose term is between 16 years to 20 years was Rs.40. But now it increased to Rs.41.

LIC’s Jeevan Saral (Plan 165) Loyalty Addition for 2017-18

For LIC’s Jeevan Saral, Bonus will not apply. But it is LA based on the MSA (Refer my post “LIC’s Jeevan Saral-Why so much confusion?). This was the LIC’s special plan. Let us see the LA rates for this plan.

Along with Simple Reversionary Bonus, LIC also declares other types of bonuses like;

- Final Additional Bonus (FAB): It is paid to those policies which are of a longer duration and has run for say more than 15 years. This is the one-time payment payable either at the death of policy holder or at maturity.

- Loyalty Additions: LA is exactly like FAB. Few features offers such LA than Bonus (For example Jeevan Saral)

- They are paid as per the policy features and conditions. No LA will be payable if you surrender the policy in between (except Jeevan Saral).

Note-It is hard for me to share all plans FAB and LA rates. Hence, if you have a specific query related to FAB or LA rates, then you can comment it here and I will try to share the same.

Sir

Thank you for sharing the information. It is very helpful.

Can you please suggest if the bima gold plan 174 is applicable for any loyalty bonus ?

Dear Subinoy,

Yes.

Sir I am holding Jeevan chhaya plan

(103) SA-10000 .

20 years plan

Maturity date 25/10/2021

Pl tell me loyalty amount& maturity total amount

Dear Padma,

Please visit the branch to know the exact values.

Hello Sir,

I took Jeevan Saral plan on 05/01/2011 with Sum assured of 1390700/- and I am paying premium of Rs.5104 in monthly. I shall be surrender my policy as on 06/01/20210 (10 years completed). how much amount get me.

Dear Lovkesh,

Please approach the concerned branch.

Sir I am holding Jeevan saral plan. SA-500000 I have paid for 9 years out of 20 years. What will be expected maturity amount?

Dear Prasanna,

The returns may be around 4% to 5%.

For 179 the loyalty addition as you have mentioned is 100 per LA which is very less. Is the fig. correct?

Dear Guru,

Yes.

I have purchased a Jeevan Shree in 2001 with a yly premium of 30704/- for 16 yrs and paid all the premium the maturity date is 2026 but I need money now how much will get ?

Dear Ashish,

Approach the nearest LIC Branch.

Hi, how certain is LIC bonus and how much variation is possible? I mean is it risky may be like stock market? My main agenda is investment but I need to take one life insurance policy. Can you please tell me the non-market linked endowment LIC life insurance plan giving best returns or xirr.

Dear Gupta,

Do you in need of LIFE INSURANCE or an INVESTMENT PRODUCT?

I need life insurance giving good returns with good certainity

Is it possible to get LIC endowment policies bonus rate prior to 2003? If you have please share.

Dear Gaurav,

Yes, find the same in LIC website.

Dear Sir,

What I could read from the internet is that one time FAB is applicable for all the policies which are more than a tenure of 15 years at the time of Maturity/Death. I have a Jeevan Saral 165 policy for 35 years. Am I eligible for both LA and FAB at the end of maturity ?

Dear Praveen,

Forget about what you read for a moment. Do you feel such FAB really a great game changer in terms of returns??

Hi Sir,

Thanks for your quick response. Let me use the latest FAB rate(2018-2019) as reference to calculate in my case(Rs.18,375 /- Quarterly for 35 years). Since my Sum assured is more than 2 Lakhs and the policy term is for 35 years, the FAB rate is Rs. 2300 for 1000 sum assured

scenario 1- Assuming FAB rate is calculated on the basis of Death Sum Assured (which is 15 Lakhs in my case), it will be (2300*1500000)/1000 = Rs. 34,50,000/-

Scenario 2 – Assuming FAB rate is calculated on the basis of Final Maturity Sum assured( In my case, as per the online maturity calculator, approx . Maturity sum assured will be Rs.31,44,300/- ). So the Final FAB calculation will be (2300*3144300)/1000 = Rs.72,31,890/-

Considering the above scenarios, if the FAB is given at the time of maturity along with LA + maturity sum assured, then it could yield a better amount for the rates during that period?

Please let me know your comments.

Dear Praveen,

May I know what will be the value of today’s your calculated Rs.34,50,000 and Rs.72,31,890 after 35 years? Don’t judge the numbers rather calcualte the IRR and let me know how much it makes a difference. This is where many do the mistake.

Sir, Kindly publish the Rates for LA and FAB of current LIC Policies how to calculate them.

Thank you.

Dear Sitesh,

I do once I get the information on the same.

I have a Jeevan Anand plan 149 of sum assured 3 lacs. Premium paying term is 25 years. Done on 2009. Why the maturity date is 2089. And how much I could get after 25 years.

Dear Biswarup,

In case of Jeevan Anand, the first time maturity date will be one year after your last premium year of payment. The 2089 is the second maturity (only sum assured is covered). Please refer the policy feature in detail.

Hello Sir,

I took Jeevan Saral plan on 11/11/2011 with Sum assured of 1500000/- (Fifteen lakhs), I am paying premium of quarterly of 18375/-, could you please help me by sharing the bonus I can get if I surrender the plan on 11/11/2021 when I completes my 10 years.

Dear Manav,

Please read the Jeevan Saral features once again. This plan does not offer Bonus but LA on MSA.

I took Jeevan Mitra 133 Triple Cover in 2010 with Sum Assured as 5,00,000,

Annual Premium = 21,120

Total Payment Period = 26 yrs,

Total Insured Period = 26 yrs,

And I calculated my Approximate returns after 26 yrs = 14,30,000

I feel that this Policy is good if I die within those 26 yrs but if I live, the maturity amount is around 3 lacs less when compared. I feel really cheated by the LIC agent after reading your blog and others too.

Sir, please tell me if I should stop paying premiums and invest those 20K in some other investment like TERM Insurance ?

Dear Paresh,

If you are CURRENTLY unsatisfied with the product it was sold to you, then why to continue?

Thanks for replying Sir.

Can you please confirm what will happen if stopping the premium payments but do not surrender the policy and keep it until complete tenure ?

I want to know

1) will I get bonus accured so far?

2) will I get FAB after policy term?

3) what will be maturity amt in above scenario?

Dear Paresh,

The policy will be turned as Paid Up and will not participate in the future policy benefits.

I am holding Jeevan Saral (165) and paid 10 premiums of 24020 . My age is 30 and sum assured is 500000 . What amount should i get if surrendering policy now ?

Dear Saurabh,

Better you be in touch with the home branch.

What is the Bonus and Loyalty Addition amount for LIC Bima Gold policy of 20 years for Sum Assured Rs 1000 Lacs, Period of Cover is from 28/03/2006 up to 28/03/2026

Dear Awasthi,

The accrued bonus data for your policy may be available online. Please check the bonus by login to LIC website.

I have New Jeevan Shree (Plan-151), premium schedule is completed and maturity in year 2028. How can I know about till date loyalty bonus

Dear Abhishek,

Check with concerned LIC Branch.

i will suggest my children never take LIC policies

Dear Sathisan,

It is wrong. Suggest them not to buy products which combine INSURANCE+INVESTMENT. But they must buy LIFE INSURANCE.

I have paid approx 7,20,000 in last 10 years under Jeevan Saral. With the above table, I should be getting 15,00,000/1000 * 425 = 6,37,500

Total payout excluding tax should be 7,20,000(premium paid for 10yrs)+6,37,500 = 13,57,500.

Is the above calculation correct ?

Dear Puneet,

You have to consider the MSA for 10 years but not the MSA mentioned on your policy bond.

my policy is Jeevan saral-165, sum assured is 1300000 and started in 2010 at the age of 30 yrs and policy term of 18 yrs. could you please let me know the approximate Loyalty additions will be added after maturity

Dear Venkat,

Refer above chart for the same.

Sir, I have two Jeevan Surabhi Plan of 1.5 lac and 2 lac for 15 years …which are going to mature in coming December 2018…please tell me how much I get at maturity of including of all benefits

Dear Sheikh,

It is hard for me to calculate each and everyone. However, you can expect around 5% returns.

Dear Mr. Basavaraj,

Which month/date LIC is declaring/added vested bonus in our policies & when we can see through our login the added vested bonus.

Dear Rupesh,

Once the policy completes three years, then you can see the vested bonus details. Regarding yearly update of the same, it is not disclosed by LIC.

Sir I have just joined Jeevan Labh (16yrs-25yrs) & New Jeevan Anand (31) What return rates i can expect after maturity ??

Hello Sir, When will LIC declare the latest Bonus rates for the year 2018?

Dear Bala,

They will declare it soon. I will update the same once they declare it.

Hi Mr. Basavaraj,

Thanks for your informative blog.

I have a Jeevan Saral policy (plan 165), with the first premium payment date in August 2011. I have paid 8 premiums so far. I am not particularly happy with the policy returns and would like to surrender. Given, I am so close to the loyalty addition cut-off (10 years), am I better off surrendering now or immediately after my 10th premium payment. Below are some details. Would be great if you could confirm that my calculations are not widely off

Yearly premium: 60,050

Sum assured: 12,50,000

Premium paying Term: 35 years

I estimate that I will suffer a loss of close to 2 lacs if i surrender now, and a loss of around 50,000 if i surrender after the 10th year. Am i right?

Thank you so much.

Dear Krishna,

Better to surrender once the policy completes 10 years.

I am holding LIC Jeewan Mitra Triple cover Plan : Table 133-20 SA : 50000 Policy date : 15.03.2000 Maturity date 15.03.2020. What will be maturity value. There is no gap in premium payment.

Dear Ajay,

It is hard for me to calculate for each individual. However, by referring to the above chart either calculate on your own or approach the nearest branch.

BONUS RATES FOR JEEVAN UMANG POLICY ? (DURING PPT)

BONUS RATES FOR JEEVAN UMANG POLICY ? (AFTER PPT ON DIFFERNTIAL SCALE WHICH IS DIFFERENT FROM SIMPLE REVISIONARY BONUS AS MENTIONED IN LIC DOCUMENT)

IF PPT TERM=15 YEARS,FAB @5 YEARS AFTER PPT AND FAB @10 YEARS AFTER PPT WILL DIFFER?

IF FULLY PAID UP AND I SURRENDER IN FUTURE,WILL I GET FAB?

I HAVE PAID FIRST PREMIUM ,SHOUD I SURRENDER IT OR NO?

PLEASE REPLY.

Dear Vishal,

Bonus rates not change based on your premium paying term. Please clear your confusion with concerned LIC branch or agent who sold you.

Mr. BT

I really appreciate your efforts for such a nice blog.

Dear Anil,

Pleasure 🙂

Bonus rate of policy newendowment for period 16years

Dear Arun,

Refer above post.

Hi Basavaraj,

Is this the latest Bonus list declared in March’2018

Dear Joyraj,

Please check the above post for the year of bonus rates.

March 2009 is the year of purchase of this Jeevan saral plan

Hello sir, this is regarding jeevan saral policy which i took in march 200. Two policies of Rs 1531 each monthly I m paying..What amount will i get if I surrender in 2019 march. Do I willlwill loyalty bonus also.

Dear Charu,

You can expect around 4% to 5% returns.

Hello Sir,

This is regarding Jeevan Shree (Plan-112). I paid Rs.24,590 for 16 yr term, maturity after 25 years. Sum assured is 5L. This was taken during 2001, I’ve paid the premium for 16 years without fail. Is FAB added to maturity amount for this policy? As this is an old policy, many don’t know the details.

Dear Lakshmi,

I think I replied to your earlier comment that this policy does not provide FAB facility. Also, FAB is not a big game changer.

Dear Sir,

I want to know about loyalty addition for “New Bima Gold (Plan-179)”. This is a money back policy. I have this policy for a term of 16 yrs. I didn’t get any information related loyalty addition rates. Could you please help me with this?

Dear Ashutosh,

For 12 years term, it is Rs.100 LA.

I have a Jeevan Mitra Triple Cover Policy Sum Assured of Rs 1 Lakh from 1993 and maturing during Sept 2018. What would be maturity value along with the Diamond Jubilee special Bonus.

Dear Myalai,

Refer above bonus rate and calculate on your own by referring my earliest post “Video tutor-How to calculate LIC policies maturity amount and returns?“.

Hello – I would like to know how interim bonus is calculated for Jeevan Anand – 149. Bonuses are declared in September and would be applied in March of the following year. Is my understanding right? My case is the Sum Assured has died on 15th March 2018. I see the formula as Sum assured per thousand * declared bonus rate. Will the bonus be applied for the whole years event though my sum assured is short of 15 days?

Dear Adex,

Yes, it will be applicable for whole year.

Hi all, I was going through many comments in this blog and Mr Basavaraj Tonagatti does a wonderful job through prompt replies. I found it very funny that some one saying that LIC is an excellent investment which gives guranteed returns till 100 years etc, but my understanding is, LIC is not investment, investment in LIC doesn’t involve any risk, It is a savings only. It gives capital guarantee to the policy holder and LIC returns are low to moderate. Lic has to be viewed as a debt instrument only, in my opinion Savings with LIC works as world’s best debt fund, since it has capital guarantee. Unlike PPF it doesn’t have any upper limit on amount saved every year, but also there is a possibility that proceeds from PPF may be taxed in future, however currently LIC policy holders are protected in this regard under section 10/10D. Policies taken under MWP act cannot be attached by any Financial institutions or courts also.

So I suggest everybody to stop viewing LIC as an investment but consider it as a savings tool.

When the returns are guaranteed and protected the returns will be obviously low.

If one has to be financially successful, he has to develop financial assets and Financial assets doesn’t just mean, LIC, MF Alone.

Thank you.

Dear Ravi,

Thanks for sharing your views.

Dear Basavaraj,

I wanted to surrender my policy and payback the amount received towards my house loan. Is it beneficial or not for me?

No loans on policy taken, no delay in premium payments till date. Please help me in understanding how much amount do I receive if I surrender this policy as on date.

Plan Name: Jeevan Anand (Plan-149)

Start Date: 23/11/2009

Premium Paying Term: 18 years

Policy Term: 74 years

Policy benefits: INR 400,000

Premium Mode: Half-yearly

Than you in advance.

Dear Narasimha,

Please contact the branch for the same.

Hi,

It is not advisable to surrender your policy as it is an endowment plan & you get less than what you had paid.

Dear Dhiraj,

So you are suggesting him to continue and satisfy with 4% to 5% returns?

I have taken Jeevan Saral policy (plan 165- 26-26) in 2008. Paying premium of Rs 24000 per annum . SI is Rs 5,00,000.

According to you , how much approximate amount I will receive at the time of maturity ?

Dear Sandeep,

Refer my post “LIC’s Jeevan Saral-Why so much confusion?“.

Hi

I have taken a jeevan ankur policy on may 2012 for sum assured 500000/- and paying 22500/ yr as premium, what will be the net sum i will be receiving at 2030

Thanks

Syam

Dear Syam,

Refer my post “Video tutor-How to calculate LIC policies maturity amount and returns?“.

Hello,

My Self Sanjay Vaishnav and i have purchased Jeevan Saral(165) in 2009.Pre -5104/- Per Month term-35 yrs.and i am confused to continue this policy or Not. Can I get the same returns shown in LIC Chart by Agent.

Or i will close it and invest in MF.

Dear Sanjay,

Never rely on agent’s claims. You can expect around 5% to 6% returns. If this is fine for you then continue.

Hi ,

I had purchases LIC Jeevan Anand (Plan 149) in Nov 2011. with sum assured 10 lac at maturity at age of 28. Policy premium paying is for 30 years. My premium is half yearly around 16.3k (32.5k yearly). I had already paid 6 years premiums (around 2lacs till date) and next 7th year 1st premium is due on May 2018. My age is 34 yrs and will be 35 yrs in June 2018. I am already investing in PPF & Mutual funds.

Please help what to do with this LIC policy. Should I stop paying premiums for it? Also if I stop paying premium and if it will be come paid up, then, can I change nominee in paid up policy?

One problem is that Policy has been issued by some remote branch very far from my place and LIC agent who opened it from that branch also left LIC Agent job. So, I am paying premium online and had never gone to that remote branch

Please help urgently as my next LIC premium is due in May 2018

Dear Deepak, In my view, it is better to surrender now rather than turning it to be paid up. Regarding branch, you write a letter to the concerned branch requesting them to transfer the same to your nearest branch. This will help you to get the services at best.

Hello sir, latest news says that lic has increased the bonus rates by 40% but still now lic officially not declared anything about this. Is this a false news or may happen in near future? Can you please tell when will lic declare new bonus rates for the financial year 2018/19???

Bala-Reality is in above post.

i have a policy of jeevan saral yearly amount is 25221… policy and paying term is 35 years. can you tell me the maturity amount after 35 years??? i cant understand your example

Pranoy-I can’t do calculations for each individual. However, if you can’t understand then I can make sure to clear your doubt. It is a simple 4th or 5th Std Mathematics you need to calculate.

Dear Basu- What is the FAB for New Money Back-Plan 93 maturing in March 2018 (term 25 yrs)?

Rabi-Check with LIC.

How much lump sum will I get at the end of premium payment term in LIC,s jeevan tarang (table no 178) with a sum assured of RS. 300000.

Krishna-Refer THIS post.

Does Jeevan Astha policy of LIC have any loyalty bonus?

Ashok-Yes.

What is th name of lic whole life insurance plan? Which gives bonus h70per 1000

Sandeep-It is the earlier Whole Life Plan, which is not available now.

could you please name one whole life insurance plan from either privat or public company?

Sandeep-Check with respective Life Insurance companies.

Hi Sandeep i can help you out selecting best insurance plan which gives highest return.

Please do call me at 9886917124

Dear JO,

Looking for INSURANCE or INVESTMENT?

Sir my father had old jeevan shree table 112 term 16/25. He take this policy on 2002.All primium have been paid within time. And last primium was on feb 2017. On 6/2/2018 my father leave this world(die). Now i wanted to know that how much amount finally will receive.

Sum assured = 500000

Premium instalment = 30704

Jay-Contact the branch for the quantum of money you will receive.

Sir tell me approx amount please.

5,00,000 (SUM Assured) + 16*37500 = 600,000 + LA Approx. 75,000/-

11,75,000 (approx)

Then what are you here for??

Dear Manjeet,

Valid POINT 🙂 But sadly I am not here to HANDHOLD each individual who BUY BLINDLY without knowing the basics of whom to approach for the values. The exactly Surrender and Paid Up value depends on individual policy details, which I don’t have. Hence, they have to contact the branch for the same. If you still not understand this basic requirement, then it is YOUR fault but not MINE 🙂

I have a question related to jeevan tarang and jeevan saral policy. What amount ahould i get after maturity of 200000 for 15 yr for each.

Pradhan-Hard to say BLINDLY. However, you can expect around 5% to 6% returns.

I have purchased jeevan saral 165-20 in 2009. I am paying prmium per month Rs.6125/-.

how much I ll get maturity amount with benefits on my maturity date?

Sandesh-Refer my post “LIC’s Jeevan Saral-Why so much confusion?“.

Till 16 th premium it shows LA 640 . So what you expect till 20th premium ?

Is it possible to reach at 800 ?

Rahul-Let us assume Rs.800, then may I know the return on investment??

Then it means provide 8 percent on an investment .I think it’s near equivalent to PPF

Rahul-Check IRR (If you don’t know, then search in Google) and let me know whether it crosses 7% or not?

i am thinking 800 on Rs 1000 sum assured . It seems 8 percent . Am i right? can you explain me how calculate in LIC policy terms ?

Rahul-8% one time benefit but not yearly benefit. If you don’t know the basics, then refer my post to calculate return on investment “Video tutor-How to calculate LIC policies maturity amount and returns?“.

Is FAB provide for Jeevan Saral ? If we paid premium till 15 years ?

Rahul-Jeevan Saral offers only MSA+LA but not FAB.

Hi Basavaraj Tonagatti,

I have two Jeevan Saral(165 ) policies with the following premium since January 2011.

3573 – Monthly – 15 years.

2552 – Monthly – 20years

Can you please help me guide if it is a good idea to continue in these policies and what would be final amount i would get at the end of 15 years and 20 years respectively.

Thanks,

Mithun

Mithun-Refer my post “LIC’s Jeevan Saral-Why so much confusion?“.

I have taken bima gold

for 12years. Maturety is on 28th March 2018. Insured amount ? 500000. What is loyalty bonus I will get.

Nilesh-It is Rs.100 per Rs.1,000 Sum Assured.

DEAR BASAVRAJ. T.

I have TAKEN JEEVAN CHAYA (plan 103) policy from LIC for my child. The policy commenced from 28/08/2002. I have been paying annaul premium of Rs. 25,538 without any discontinuation. Total sum assured is Rs. 400000. Can you please inform me whats the maturity return of this plan.

Thanks in advance.

Harishkumar-Please contact the concerned LIC Branch.

Dear Sir,

I bought Jeevan Saral (Table 165) plan in 2013 for 35 Years with Annual premium of Rs 18100. I had already paid 5 annual premium. Now If I will surrender my policy then what would be my surrender value and payable to me. Please guide me on this.

Hanif-Contact the home branch.

Thanks for reply

What is the loyality additon bonus i will receive for Jeevan varsha plan (12 Years) sum assured is Rs 100000/-

Rajiv-As of now, LIC declared 9 years LA rates for Jeevan Varsha and it is Rs.110 per Rs.1,000 SA.

I have taken jeevan varsha

for 9years. Maturety is on 28th March 2018. Insured amount ? 100000. What is loyalty bonus I will get.

Padma-Loyalty Addition for 9 years Jeevan Varsha is Rs.110 per Rs.1,000 Sum Assured.

January 21, 2018 at 9:36 PM

Padma-Loyalty Addition for 9 years Jeevan Varsha is Rs.110 per Rs.1,000 Sum Assured.thanku, please send sum assured rs100000 total maturity amount

Padma-Please calculate on your own or contact the branch.

I already went to Branch. They said Final Amount will be as mentioned below.

1. 60% of the Sum Assured – Rs. 60,000/-

2. GA Rs. 65/1000/year – Rs. 58,500/-

3. LA Rs. 110/1000 – Rs. 11,000/-

Total amount of Rs. 1,29,500/- will be credited to our account on the maturity date, if we submit the neft mandate form at LIC Branch.

I have taken Bima gold for 12 years. Maturety is on 28th March 2018. Insured amount ? 500000. What is loyalty bonus I will get.

Subba-Loyalty Addition for Bima Gold plan for 12 years plan is Rs.100 per Rs.1,000 Sum Assured.

LIC bonus rate ranges from 35to 48 . But if you invest in Postal Life insurance then Bonus will be 58 for endowment and 85 for suraksha. This is best plan in terms of tax saving, insurance and investment. If you calculate in terms of rate of interest, then it exceeds 8.1 % for 15 years plan . which is higher than any savings schemes like PPF and RD.

I think the bonus rates what you said is for 2015-2016 fy. As per my knowledge 2017-2018 it is 50 rs for endowment and 65 for whole life assurance policies. Also, pli plans are only for govt or semi-govt employeees not for private working employee unless one of the spouse is govt and other pvt. Employee.

Thank you.

Ranjan-The above-published bonus rates are the latest one.

Where can I find officially, if it is current bonus rate then it’s awesome. Where can I purchase one online or in post office.

Ranjan-If you feel the returns of around 5% to 6% are BEST for your long term INVESTMENT, then go ahead and buy. However, my suggestion is that SEPARATE INSURANCE WITH INVESTMENT.

Do you mean even this PLI is also not good. He says around 8 + percentage returns guaranteed. I just want to earn at least 9 to 10 percentage returns. I don’t want much risk but can afford up to 10 %. I see hdfc and SBI mfs are good. If am wrong let me know one we’re I can invest online directly. I want to start from this month as my future savings only as investment purpose.

Ranjan-GUARANTEED? Cross check with that person who claims so.

Lalit-Whether all are ELIGIBLE?

Loyalty addition bonus in Jeevan saral will be payable only one time at the exit or will be payable for all the year after 10year till maturity.??

Arif-At the time of exit.

Dear Sir,

I have a Jeevan Shree 1 policy (Plan 162) which was commenced in 2011 with Sum Assured of 5 Lakhs. What should be an approx amount of vested bonus till the current date? The vested bonus figure that I see in my online LIC profile does not match to what I have read about in policy’s benefits.

Thanks

Sanjeevan-The accumulated bonus is what it is showing in LIC portal (may be missing of current year). If you still have doubts, then approach LIC branch for the same.

sir

please tell me the bonus mention in each plan of LIC is payable to us or not?? second also tell what bonus i will get..the bonus which is shown to me now or the bonus final at that time??? i am confused how the calculation will be at my maturity??? coz each year bonus is going dip not up…please clear me

Manoj-Here is the trick. The bonus will be payable to you during death claim or at maturity. However, they not add a single additional rupee on such accured bonus and they keep it as it with them. Refer my post “Video tutor-How to calculate LIC policies maturity amount and returns?“.

Sir,

I am having Old jeevan anand policy for 25 years & sum assured is 25 years. what will be my maturity amount including bonus ? If i want to surrender policy immediately after maturity, what extra amount i will get?

Abhinava-Please visit the nearest branch for exact values.

Dear Sir

I want your reply on my Query.

I had taken New Jeevan Suraksha Policy (Table No. -147) in January 2004. Policy period is 30 years and the last date for premium payment is Jnauary 2034. I am paying Rs. 10,000 as premium amount every year

The present surrender value of the Policy is around 1.9 lakhs

Please let me know if I can surrender this policy. I am confused. If I should surrender or not as people say that this is a very old policy with assured returns and that I will get a good pension amount. Some also say if I want to surrender, than I should surrender at the fag end of the policy tenure , as I will get a good surrender amount of approx. 8 to 9 lakhs. With the present going rates of bonus in this policy what can be pension amount expected after maturity ?

Please let me know what to do – to surrender or not to surrender

Awaiting your expert opinion

Vivek-It is a pension plan. People say many things, but all forget the IRR the policy generates. Hence, better to surrender NOW than heeding the people who throw their view in AIR.

Thanks a lot for the prompt reply sir..

I had 1 more query ..

With the present going rates of bonus in this policy what can be pension amount expected after maturity of New Jeevan Suraksha Policy (Table No. -147)

Vivek-It depends on your age and the sum assured you opted. Hard for me to say BLINDLY.

Sir, regarding Jeevan Shree calculation 500*75*25=937500+500000+Loyalty addition LIKELY PAYABLE for 25 year term policy it will be 65to 70% of SA AS LA THAT COMES AROUND 400000, SO IT WILL BE 18,37,500

Siddesh-Your LA depends on MSA but not on Sum assured.

Can you explain MSA and SA please ? I was thinking the same as above calculation till now .

Also whats the Loyalty addittion for Jeevan shree(112) ? Could you please post it

Naresh-MSA is only for Jeevan Saral for rest of all plans of LIC SA is applicable for calculation of LA or Bonus. LA For Jeevan Shree (112) is shared in blog comment and post also. Please refer the same.

Basavaraj sir… I want to surrender my jeevan anand policy(149) commenced on 24/06/2005.i have paid premiums upto 26/09/2017.(quarterly rs. 3893). My bonus accumulated till date is rs. 178,000.it is 21 yrs policy.

1)in which month Lic adds the bonus of the year 2017-18

2)shall i have to wait till march 2018 end to get bonus

3)shall i need to pay December and march premiums to get bonus benefit

4)how much i will get if i surrender in January or april 2018 (sum assured 3 lac)

Pl answer sir

Sai-Surrender NOW rather than waiting for their paltry BONUS (which you will not get fully as you are surrendering).

Sir ,I have Jeevan saral plan,I purchased on date 8 /1/2008.quaterly 1531.can I surrender now?How much amount will I get?

Aslam-Yes, you can surrender now. Regarding values, please contact the branch.

Sir

I have two running policies Jeevan saral 165,term 25 with SA 250000 and endowment plan table 14 for 35 years with SA of 50000. Both the policies started from 2008 and 2010 respectively. From last week I am receiving calls from lic, one from head office and one from accounts dept that some dividend on policies has been declared which I would only get through after changing agent code to self assessment code. For this they asked me to buy another life insurance policy other than lic to get the self assessment code. After taking the policy they again said me that some more is showing to us from tha date you had started lic policies and you have to buy another policy to pay the charges of add on forms. Please help me in giving advice is lic has actually distribute benefits to the policyholders? or I am receiving some fake calls or after giving those people self assessment code, can they use them anyhow to withdraw the dividend themselves?. Please suggest asap.

Thanks in advance

Pooja-It is a completely FAKE call or to DUPE you. If they call again, then immediately warn them and inform to nearest Police Station and also the LIC Branch.

Thank you for your advice.

One more thing, is there any need to change agent code to self-assessment code during the term of policy period? What if, I continue with the agent code? Or should I simply surrender these policies now?

Pooja-You no need to change or allowed to change agent code to existing Life Insurance.

Thank you for the responses.

LIC Term insurance Premium is very high when compared to other companies. Any idea behind that?

Sudhakar-NONE have an idea as it depends on company’s decision, profitability and actuaries design of the plan.

Hi

I have an LIC policy , details as per below, which I wish to surrender due to financial reasons.

Kindly let me know how much will I get if I surrender the policy now.

Details of my policy are:

Policy name : LIC Jeevan Tarang

SA : Rs. 900000

Tenure : 20 years

EMI : Rs. 11305

Total premium paid : 21 months.

Would appreciate your response

Prashant-Please contact the nearest branch or home branch.

Hi Basavaraj / Pradeep,

I have one Jeevan Anand (149) policy. Sum assured is 1000000. (10L), Policy Term is 21 years (This is a old policy which was discontinued). In the bonus rates for 2017-2018 it was mentioned as 49 Rupees / 1000 for this policy for term >20.

Mine is 21 years term. This rate of 49 is a fixed one for all 21 years are they will be revising this every year. If they are revising every year, the bonus for each year will be calculated based on the rate declared every year and summed up or at the end of 21 years, the rate in that year will be used to calculate for all 21 years? Also for this policy will there be any FAB?

Thanks in advance

Sudhakar-It will change yearly based on LIC’s business performance. Yes, your understanding about calculation is right. Yes, this plan also offers FAB.

ok thanks. Now I have a clarity on my policy.

Author: sudhakar

Comment:

Hi, I enrolled for The Endowment Assurance Policy Limited Payment (Plan-48) in 2002, Sum assured 500000, Policy term is 20 years and premium paying term is 15. It is now fully paid. The vested bonus shows only 3,30,000 till date. Also initially in 2002 when the LIC Agent marketed this product he told returns will be close to 16 lacs. Now when I contacted he is not telling how much I will get. I checked with LIC and no one is helping. Can you help what is the final amount I will receive by 2023?

Thanks

Sudhakar

Hello, I felt bad after reading yours. Before purchasing anything we enquire about that product or things deeply, how you trusted that fellow simply without any data. I when opted for insurance took all the data details and rough copy of bonus details, rates, maturity value. I think they will give you a software copy of insurance details which contains Maturity value. If you have one go and ask directly.

Few people who are not aware of insurance or funds are also marketing. Please be aware of those crooks. Don’t trust anyone untill you get proper answer or details; sometimes not even our own shadow.

One person here showed you calculated maturity value. Hope that helps you. Yes, returns are less but i think guaranteed. Because, I received said amount from old policies.

Guys, before taking insurance decide whether you want to take only insurance or both insurance+Investment or only good returns.

If you are going for insurance and Investment, then don’t expect high returns like in ppf/fds/mfs/stocks.

Ranjan-Well said.

Thanks Ranjan and Basavaraj,

I agree, this was 15 years before when Did not have much idea and was lured by the well known agents. Post the policies which I took after some years, I did a deep drive research and then opted. But It is a valid input to thoroughly do a research before investing in money. Thanks.

Sudhakar S

Sir i have jeevan shree table 112 term 16/25. All primium have been paid within time. Now i wanted to know that how much amount finally will receive on the time of maturity.

My SA is – Rs. 5,00,000

Gurateed Bonus – Rs. 9,37,500

Loyalty addition – Rs. 75,000

60 year Spl Bonus – Rs. 15,000

FAB ????? Advice – Rs.

Unable to calculate lum sum maturity amount

Awaiting your prompt reply

Regards

Kumar.

Kumar-You know all values (except FAB), then what is the problem here? Also, FAB will not a big game changer in % of returns.

Dear Kumar, Basavraj

I hold a similar policy and not to attain unnecessary heat clarify that I am not a LIC agent.

Further, Jeevan Shree (Table 112) 16/25 for 500000 . Maturity amount is SA+GA+LA = 500000 + 937500 + 650000 = 20,87,500. No FAB or Special Bonus in Jeevan Shree 112.

Hope this clarifies. Thanks

Vivek-Any valid clarification either from any reader or LIC agent is never going to be questioned 🙂

Hi,

Where did you get the loyalty addition for plan -112? Any link or reference will be helpful. Thanks in advance

Tanmay-It is from recent LICs declaration. You will get this notification in LIC branch (if you ask for).

Hi, I enrolled for The Endowment Assurance Policy Limited Payment (Plan-48) in 2002, Sum assured 500000, Policy term is 20 years and premium paying term is 20. It is now fully paid. The vested bonus shows only 3,30,000 till date. Also initially in 2002 when the LIC Agent marketed this product he told returns will be close to 16 lacs. Now when I contacted he is not telling how much I will get. I checked with LIC and no one is helping. Can you help what is the final amount I will receive by 2023?

Thanks

Sudhakar

Sudhakar-It is easy to calculate. Refer my post “Video tutor-How to calculate LIC policies maturity amount and returns?“.

Thanks Basavaraj, In my case my policy term is 20 and my premium paying term is 15. So this criteria is not covered in the tutor.

Thanks

Sudhakar

Hi,

The calculation is very simple. Your maturity amount is Sum Assured + Bonuses + FAB.

Sum assured is 5,00,000

Bonus has been 22,000 per year for past 15 years which comes to 3,30,000

For next 5 years you are going to receive similar amount every year, so that is another 1,10,000

FAB is currently 70 Rs per 1000 Rs Sum assured for 20 year tenure. For 5,00,000 sum assured, thats about 35,000.

Final calculation = 5,00,000 + 3,30,000 + 1,10,000 + 35,000 = 9,75,000.

No where close to 15-16 lacs promised by your agent.

Hope this helps.

Pradeep-That’s great patience 🙂 Thanks for replying to him.

Basu,

My pleasure.

I want all those pathetic LIC agents to come and talk about the returns in this case.

Do they have any courage?

Pradeep-They never 🙂

Thanks a Pradeep. This helped me to close my concern. Funny part on your question on LIC agents, I spoke to 4 people and none of them were able to clearly explain or give the breakup. They spoke jargons like government will be in loss if they give more bonus, so such decisions have been taken to reduce bonus. And they told we shall give LIC higher officials who can help with my query. This is the so called technical knowledge about the agents.

Thanks

Sudhakar

Sudhakar-Simply say them that MY HARD EARNED MONEY IS NOT FOR THE SAKE OF MAKING GOVT PROFIT.

Sir, Mine in Old Bima gold Policy, T.No 174 which is maturing on 2018 March. But for this policy no any cash bonus is indicated in this post. Is this policy eligible for bonus or not? and as it is completed 16 years, what about the FAB? Please clarify.. Thank You.

Dhana-This plan not offers any bonus or FAB but only LA. Check with LIC branch for the LA.

Thanks..

LA for Policy Table # 174 is 100 per 1000 for maturity in 2018. Thx

Why half information given? What is the loyalty addition declared for old jeevan shrree policy table 112? Please update complete information sir

Ram-It is impossible to update all information within the post. Whether you need that particular information?

Old Jeevan Shree Policy Table 112, latest lyalty addition rate is 1300 per thousand for 25 years maturity.

Vivek-Thanks for sharing.

Hi Vivek,

I read my policy document. I could not find anything regarding the loyalty addition rate. On last page of policy, it only mentions about GA.

I am talking about Jeevan Shree (without accident benefit) – 112.

Thanks

Rahul

Rahul-As per me, this plan offers GA+LA. If you are unable to find, then approach LIC for clarification.

Dear Basu

I had taken a Lic Jeevan Saral policy in dec 2010 for 16 year term

Pl suggest me should I surrrender the same or be invested

Surya-Better to surrender.

Sir

Is any surrender charges as I have paid 7 premiums

Thanx in advance

Basu Sir

Thanx for replying

As per your suggestion & jeevan saral LA chart my amount after completion of full policy term comes out to be 20lac+ .Incase i surrender this policy at this time i suffer a loss of 1.5 lac & at the same time if i invest this entire corpus and upcoming installments in some good Fund expecting a XIRR of 12% ,the expected corpus would be around 20lac but without life cover.

Now pl suggest wht should i do ???????

Surya-Cover can be easily purchased with cheapest online term plans. Whether you considered the amount to be re-invested which you receive as a surrender amount in your so-called 12% generating product?

Sir

Yes sir the 3.5 lac which i would be receiving as surrender amount pl

along with the future premiums for next 9 years

Surya-Now regarding the final value calculation, whether you did that on your own or through an agent? What IRR he showed you from Jeevan Saral?

Surya-Now regarding the final value calculation, whether you did that on your own or through an agent? What IRR he showed you from Jeevan Saral?

I’m 31 Years old, I have Old Jeevan Anand (149), PPT 40 Years, SA 1010000, Premium 1881 (monthly) since Sept, 2013. I’ll be really thankful to you if you kindly share the FAB details of my policy which I will get after 40 years?

And is that guaranteed once declared because my agent is saying that I will get around 65 to 70 Lacs minimum after 40 years! And if so then please share how the final figure is coming ie. the calculation details because I’m investing Rs. 10 Lacs only?

Thanks in advance..

Subhayan-The FAB at the time of 40 years maturity will apply to you not today’s FAB. Please keep it in mind that FAB stands for FINAL ADDITIONAL BONUS.In whatever way you or your agent calculate, the returns will not be more than 7% or 8%.

Hi, I got angry on my agent once I came to know that I am getting less than 6.5 percentage for Jeevan Labh as said by cfp. But, he explained me compounding the amount I am paying yearly. It’s getting 7.5 percentage. But these guys told to calculate in irr through system and some other cagr tool. One cfp is telling less than 6% and other tells 6.5% and I met one cfp he is telling 6.8%. They showing in table. But when calculated by hand spending half an hour I understood the actual scenario as am paying premium little yearly unlike FD not at once. I was not fooled. I am happy at least my agent spent time and explained to me clearly about Returns. By listening to cfp I thought to surrender in anger but later dropped off. At least am in safe hands and getting Assured returns. Don’t surrender and waste half the money unnecessarily. Instead invest little savings in ppf or post office schemes. Think twice before investing in mfs or stocks. They are not guaranteed as that say and they tell us obey all rules like if loss or profit occurs it’s our personal responsibility. My frnds uncle invested in stocks and lost everything. But, for one thing am annoyed is, commission process. It should be only for two or three years, not till ppt. Remaining commission should be added to customer only. CFP are also charging too heavily. Am too against agents. However, am happy for my safe returns. My frnd unnecessarily surrendered and lost 80000, he got jus 70000. If any one applying for new insurance. Better take term plan and only invest in secured post office or ppf. Good luck.

Thank You.

Ranjan-Compounding in BONUS???? The return calculation may be varied from 6.5% to 7%. But IRDA (the regulator) itself insist to calculate the returns as IRR, XIRR or CAGR. Hence, don’t blame the calculating method. I am not sure which way your adviser satisfied you and that also claiming BONUS will compound. I know that by surrendering you may be under loss. But you can easily compensate the loss and make more money by investing properly. However, if you feel that continuing the policy is BEST to you, then you can.

Coming back to charges of CFPs, if you can’t afford, then the BEST way is to DIY approach. This is the long lasting solution. The best financial planner for you is YOU.

Ok got. Thank you very much. I am happy for positive reply. I can afford the amount but said as I came to know when met. However, self analysing is good. I got some useful information from your site and thankful for that. Good day.

Thanks sir

V informative post .

I bought plan no 165 jeevan saral dtd 21 oct 2017 . And paying 10,208 rs monthly .

I have taken it for 16 yrs .

What approx Rate of interest can i expect from Lic.

Is it advisable to foreclose the policy.

Should i wait for 10 Yrs

Or for 16 yrs ?

I have as such no money req as of now .

But pl advise , what will be the best suited in my case.

Mohit-Refer my post “LIC’s Jeevan Saral-Why so much confusion?“.

I like when people share their views. Few information I found from Advisors is good and informative. I can’t afford to open blog but few blogs like this and others give opportunity to express our doubts. Sorry if am wrong about irda and sebi rules. Just mentioned as read somewhere. Be happy people.

Hi guys. Why you people are simply fighting with tounges chill. Each one of them are sharing their views. There are many insurance companies in market all most all are in same line. Insurance Agents give exam under irda and follow their rules. Financial Advisors give exam under sebi and follow their rules. Agents work under companies. Financial Advisors work under sebi or individually. Only difference is Agents work according to policy types and earn for hardwork. Financial Advisors do the same by giving suggestions on investment as said by sebi. If any one read sebi rules list for financial advisors, then everyone will understand. It is not Basu ji fault nor some others like few from one insurance company or other. It just says financial advisors to more focus on term plans and MF. Nothing wrong in that. Every plan is good, depends on individual person according to their needs. Moreover, if everyone earns more money then everyone would have been king. No one would have been under kings. Guys, jus relax and be free to express. Agents advised customer listened. Now financial advisors advise we listen. Don’t know tommorow. However, it’s our money we need to Invest in what ever we feel good and secured. Listen to heart before listening to me or basu or some other. He is jus guiding. If good follow or else leave it that’s it. I took Labh it is good. Want to take term too and not sure of mfs because of risks involved. Will see how it works.

Be Good Do Good.

Thanks

Be Good Do Good.

Ranjan-That is why, I used to say few things also. DOUBT ALL and NEVER BELIEVE ON ANYONE BLINDLY. The BEST FINANCIAL PLANNER IS YOU YOURSELF.

I think all this discussions are waste of time. Please put some best mutual funds to invest with guarantee. What types of mfs are there. Present guaranteed term plans. I am really looking to put some amount in mfs with no risk and good returns. Also term plans with less premium and more coverage of 1 cr guaranteed claim. If possible let us know about bit coin investment and forex.

Thanks.

Ranjan-First change your views in relation to MF and Term Insurance-GUARANTEE, NO RISK, GOOD RETURNS and GUARANTEED CLAIM.

Why? I want to invest in good MF with no risk/less where I can get good returns. Even I heard your views on term insurance. Your explanation on that was good. is it wrong to ask good term plans and best companies to take policy. I saw in your blogs information explained clearly. So, I am commenting here for some comparison. Even though it’s my end decision to chose best policy. But, knowing about better term insurance and MF plans is not wrong.

If you don’t like to tell. Then it’s ok. Delete my comments please. I thought this link best to express, but your are telling to change views. I have to compare my self now. Thanks anyway for your valuable time at least for replying. You are targeting those who are against. Support those who cope. I didn’t support both. However, I just came to know I don’t get answers. Ok anyway thanks.

Ranjan-Please do your study. Which MF does not have RISK and which provides you GUARANTEE? Please do some study on how MF and Term Life Insurance works. I am forcing you to read, understand and then act but not providing you readymade answers. This is for your own long-term benefit. Hope you understand.

Ya I got what you mean. I expected you might guide me. You are putting some good stuff. Expected same incase of mfs. I am often hearing about mfs and term plans much. So

I thought why don’t I ask a financial advisor. It’s ok I will check somewhere. Thank you.

Based on the information provided I will think about best plan to choose.

Hello Sir,

I have 2 LIC Policies with me and want to surrender both policies because I have already got term plan in place for life cover. So want to invest this amount somewhere else where I can get better returns.

Plz suggest shall I do it immediately or wait for some more years?

And what will be surrender value I will get for both?

Any better Investment option for the same?

Policy Details:

Jeevan Anand (149)- Premium -15429 Yrly, SA-300000, Policy Term – 21 Yrs, Policy Start Date – 25th Dec,2010, All Premium paid till date (total 7 premium)

Jeevan Mitra (133) – Premium -20668 Yrly, SA-400000, Policy Term – 21 Yrs, Policy Start Date – 25th Dec,2010, All Premium paid till date (total 7 premium)

Kind Regards,

Sanjeev Kumar

09712935971

Sanjeev-Better to surrender.

Hello Sir,

Thanks for quick response. Plz update regarding these queries also:

– And what will be surrender value I will get for both?

– Any better Investment option for the same?

Kind Regards,

Sanjeev Kumar

9712935971

Sanjeev-Contact LIC branch for exact surrender value. Better investment option depends on lot of your financial life sharing. Hence, it is hard for me to guide you BLINDLY.

What is FAB of Jeevan LABH and New Jeevan Anand policies?

Ayush-Both are new plans (New Jeevan Anand). As of now LIC not declared it.

Sir, I have a LIC policy i.e. jeevan anand of sum assured rs 10 lacs. I am paying 51,000/- annum since 2009. Time duration is 21 years.

Today I got a message from LIC for accrued bonus of rs 3,88,000/-.

Please inform about the actual amount will I received on maturity of this policy.

Elaborate each component, please.

Rajesh-This is the total accumulated bonus as of today for your policy. You will get it at maturity or your nominee in case of your untimely death.

Hello sir. Wat is loyalty addition rate for jeevan rakshak and jeevan sthamb both 20 years term….

Sandeep-Both are new plans. LIC was not yet disclosed the same.

Sir wat may be expected loyalty addition according to u

Sandeep-Hard to say exactly.

Sir I said roughly… how much u expect

Sandeep-Check the past LA rates of other plans.

Its really ironic that LIC is “Building” our nation and giving sub-par returns to its policyholders.

Ritesh-Don’t say so, otherwise, agents fraternity will harp on you 🙂

Hi Basavaraj Tonagatti,

I hold a LIC Jeevan Anand policy with premium due every year on 24 Aug. Since I want to surrender the policy so I have not paid the premium for Aug 2017. When checked with LIC office the surrender value as on date is 45112. So my doubt is if I do the pay the premium for 2017 and surrender this policy of mine in Jan or Feb 2018 will I get an increased surrender value when compared to 45112 as of today or it will remain the same? Pls clarify. Thanks in advance.

Amit-It increased but not that much. Hence, better to surrender now.

Actually sorry it was my mistake while typing. My doubt was if I DO NOT pay the premium for 2017 and surrender this policy of mine in Jan or Feb 2018 will I get an increased surrender value when compared to 45112 as of today or it will remain the same? Thanks again.

Amit-For each passing year and for each premium you pay, the surrender value will increase. But to the extent that it will overtake the premium, you will pay. Hence, I said better to surrender.

Makes sense, thanks!

I have taken an bima diamond plan with a sum assured 2 lakhs for 16 policy term…what would be the loyalty addition at the end? Plz help me out in this..thanks in advance!!

Phaniteja-It is the recently launched plan. Hence, as of now LIC not declared the LA for this plan.

Sir I heard that it is a closing plan? So when I expect LA for bima diamond? I can get 300 per each 1000 SA?

Phaniteja-As of now, we can predict LA but certainly say. But you can expect around 5% to 6% returns.

Sir , i am looking for a retirement plan oof monthly 50,000 pension.

My age now is 38 and would retire in 50 years. Please mention some plans and how much i should invest. Dont want much risk either.

Thank you.

Sunny-Stay away from any plans which are sold as PENSION or RETIREMENT plans. Accumulate on your using mutual funds and other debt products. If you are unable to do that, then take the help of a planner.

Dear sir,

Kindly suggest best investment plan for my 1 year babyboy. I can invest 2000 rs/month and tenure can be 15 years. Please also suggest investment plan for my 4 years niece. For her Tenure can be 15 years and amount can be 1000 rs/month

Gaurang-Refer my earlier post “Best child saving and investment plan in India -10 Steps to identify“.

I am not a financial expert but my sincere advice to people out here.. Never invest only in mf and term insurance…

Invest in lic plans like jeevan anand.. Secured ncds… Recurring deposits of postal departments..

Lakhs of policies… Crores of business yet people make fun of LIC …

How many out of hundred are ready for term insurance..?? How mNy are ready to loose premium?? Very few i think not morethan 20 out of 100..

I am not an agent or worker in lic..

Dheeraz-Term Insurance is NOT INVESTMENT 🙂 Also, for any service you purchase, there is a price to it. The premium of term life insurance such charge. If you do not understand the concept of this, then better understand the IMPORTANCE OF LIFE INSURANCE (not endowment or money back plans).

Ok So tell me company name who gives me 7.5%ROI Gurentee for Life time…on my investment

Vaibhav-You are acting like a frog in small well and assuming it as a sea. If you don’t know how to generate 7.5% return on your own for LONG TERM, then it is your problem but not mine. Regarding the product, SIMPLE if you understand how GOI Bonds works out and how to buy them. The yield there is more than your paltry 7.5% and it is guaranteed by GOI. Along with this, there are other types of bonds which you might not aware like secured NCD (if you know the basics of ratings and how they work). Try these if you are non-senior and ready to sacrifice your working age and ready to work hard to make sure your money just be IDLE and give you NEGATIVE Real RETURN. Read about bond and bond market and how they work, what is ratings, what is modified duration and who giving you guarantee, then you will come to know where you are NOW. LIC is not fooling and that is why it recently modified Jeevan Akshay VI. If you don’t know why it was changed due to macro and micro economic, then again it is YOUR PROBLEM but not MINE.

Even your own lovable LIC’s sister concern’s LIC Housing Finance FDs available for you for more than your 7.5% returns 🙂 If you don’t know how to invest smartly, then don’t think all also DON”T KNOW.

I am saying from the beginning, there are many many ways nowadays where 7.5% generation of money for your so-called LONG TERM is not at all an issue. If you don’t know or not ready to learn smartly, then it is your problem but not MINE 🙂

I THINK YOU NOT UNDERSTAND ENGLISH LANGUAGE PROPERTY…..I NEED LIFE TIME GARUNTTED RETURN FOR NEXT 100 YRS….. What type of bond give me that….they give for only 5 yrs to 10 yrs…AND WHAT ABOUT MY COMPARISON OF JANAAND AND …PPF ACCOUNT….ANS ME …DONT CREAT STUPID DRAMA…..!!!!LIKE an hocker….in circus….

Vaibhav-Will you live for next 100 years is the first question you have to ask yourself. If you are guaranteed of that, then your LIC company closes today 🙂 There are something called perpetual bonds. I am stressing you once again, if you don’t know how the financial market works but only knows about LIC products, then it is your problem, but not mine!! Please give me an example of Term, Premium, and age of your customer’s Jeevan Anand Plan. We compare same with PPF. Again, you are UNIQUE PIECE, no decency of how to behave in public. Learn something from your beloved parents, seniors, or with LIC itself. Then we discuss 🙂

You are not answering my questions . And skipping ground…ok no … problem.. I Understand yours problem….bye Basu ji and Pradeep ji …you keep writing blogs against LIC …LIc doing business more and more…and building national more and more …with thrust of 30 cr people….good bye have a nice day……..Basu…………..!!!! !!!!!!!!?

What you are not diverting subject….please give me.Ans of my question…..??????If you have not and then stop the conversation…..I have not time for your teach on conversation manner…..

Vaibhav-Replied 🙂 Don’t frustrate!! I never ever told you to teach me. It is you, who is giving GYAN, which others feeling and tagged you as UNIQUE PIECE.

Again and again you not discussing on point…. Diverting subject….

Vaibhav-I answered, if you can’t understand, then I can’t go to your level right? 🙂

As a Adviser , I read one of the best reply on Term Insurance + MF investment concepts. Yes, 90% of people not understanding basic concept of Term + Investment combination and making loss.

Chetan-Pleasure 🙂

Hi Dheeraz,

One simple question to you.

LIC promised 40% more bonus this year. Why have they cheated by not paying the same. You can read the news below.

http://www.livemint.com/Money/H1lQrcBZVXFDYdm473hLNI/LIC-to-pay-40-more-dividend-bonus-in-201617.html

Answer this one question please. No deviation.

Pradeep-They never answer to direct questions like your’s or mine of whether 5% or 6% return a great return for such long term goals or not. They only create emotional situation saying LIC since many years, trust worthy and help in nation building, BUT AT WHOSE COST? If we are so fan of LIC for it’s social work, then let us DONATE rather than saying INVESTED 🙂

I think you got Ans Mr …Basu ji…..From Dheerajs coment …just stop nonsense saying against Largest Financial Institution…To whom 30 cr people Thrust…. and you dont have worthiness to say against.so please creat first ….People Like You Dont accept That…….CNBC channel owner Anil Tulsiyani Purchase J Anand Policy of 21 cr SA And many more personality Thrust LIC now whats your Ans….They Have not knowledge Of financial market only you have knowledge in 30 cr people….created blog and saying nonsense think and confuse people…….

Vaibhav-I am not against LIC but against few who sell for their own benefits and claim they are doing SOCIAL SERVICE 🙂 I am a hardcore fan of LIC’s Online Term Insurance and one more BEST but MOST neglected plan of LIC by agents and LIC officials. By the way, one important information for you, I am an LIC agent also (My agency is still alive), where I sold term insurance since the beginning. So don’t say that I am against LIC!!

Regarding few biggies whose name you shared as if they are the greatest financial wizards and hence we too follow, each individuals requirement is unique. It is foolishness to say that someone from CNBC purchased this product, hence I too. He may feel better to get 5% return than keeping money idle in savings account. But it does not same with others right?

There are many ways you turn to be CROREPATI, one risk-free way is keeping money in savings account by earning 4% return to another extreme of risking money in illegal activities. Hence, don’t defend that LIC’s products are the ONLY product on this earth, where we can generate return and BE PART OF NATION BUILDING 🙂

Sir I am not saying each Individual shuld purchase LIC traditional plane….but I am saying that the plans are Unique in market and they are perfect For whoom Whoz Requiredment matches with plane fetures ……and sir acording to many Financial specialist Ideal Investment Is that where Your Capital is Guaranted and then Intrest…and Thies is only in LIC traditional plane SA and acquired bonuses are Guaranteed by central government where In banks only Your Investment Upto 1 lack is Insured …and LIC plane are Unique then dosent have to compare with other Investment…. And as I know whre is Low risk …low ROI…and where Hi risk…Hiii ROI…. so please dont comment blindly against LIC traditional plane…..I purchases J akshay last year of 50 Lack SA who giving me 7.5% ROI for Life time Guaranteed ….Tell me single company that gives me Government guarantee..of 7.5% For Life time..Thirs is power of LIC thats why LIC is Unique …What LIC design no other company In Idia has ability to Designed that same product….I am not saying that each individual should purchase LIC traditional plane but whoz requiremnt matchs who need solid guarantee then LIC is Unique…So please stop against Blindly comment on LIC traditional plane…

Vaibhav-“There is only in LIC traditional plane SA and acquired bonuses are Guaranteed by central government”-What about PPF, SSY, Postal Schemes? PPF, SSY not generates more than more than these LIC plans? Who said you that LOW RISK MEANS LOW RETURN AND HIGH RISK MEANS HIGH RETURN? It may reverse also. I am not commenting BLINDLY on LIC PLANS, BUT AGGRESSIVE ON THOSE AGENTS WHO SAY LIC is in nation building activity. Hence, let we also contribute to it 🙂

Generating 7.5% return not a big if you know the art of investing. If don’t know, then you have to scarify your return expectation and satisfy with low return. Hence, IT IS YOUR PROBLEM, but not all of us right? You are rounding again and again in justifying LIC as if the BIGGEST WORLD’s UNIQUE company. If they are so efficient in managing people money, then why not transfer the same with LIC MF?

Sir please copare LIC j labh 16/25..Plane returns with PPF account by taking extension of 10 yrs without deposit…The returns are equal and in LIC insurance factot is additional…. and give me single company name who Manage my fund of 50 lakh and give 7.5% ROI life time gurantee wih Capital of 50 lakh Guranteed…and sir please check the retuns of LIC jeevan shree plane they are more than any postal or government schems…..I think your study on LIC is low..and about Low risk Low return statment …is of CA aman chaugh youngest CA of India and Advisor of most Fortu e companies Like icicI Prudential.. Reliance…and many more…and who is you that telling me stupid Imformation Abou such a large organization

Hey comedy piece,

Jeevan Labh has given 4.7% bonus. PPF nearly 8% and compounds annually.

PPF allows holder to withdraw 50% of his money after 5 years and any time in case of medical treatment.

Most importantly PPF provides higher return if interest rates go up.

You have issues and that can’t be treated here.

Go consult a shrimp.

Pradeep-Don’t worry he will soon stop 🙂 Because no logic, no valid points but just airing emotional melodrama in the air. The problem is not in him. But he might have attended some SALES training or his DO and Manager might be filled some encouraging stories in his mind. Here, the change mind by giving biggies example and convince these agents mind that how to justify 5% or 6% return by giving an example like few big names or some CAs. They do the same with others 🙂

Vaibhav-May I know in what way you are claiming Jeevan Labh superior to PPF? Can you provide some proof on your claims? Regarding your 7.5% returns claim, I already replied. If you don’t know the art of investing and generating and how the compounding works, then it is YOUR PROBLEM, but neither mine or others. If you are satisfied with 7.5% negative real return, then it is you and your life but not MINE right? Again, may I know which Jeevan Shree plan you are quoting? The one which was closed in 2000 era or the current one? If the current one, then can you claim how it is superior to other products? If it is earlier Jeevan Shree, then keep in mind that interest rate cycle during that period was also high. Hence, LIC offered that. Later on it closed. Do you think CA means he is capable of handling INVESTMENT part also? CA is expert in tax part. But he may be dumb in investment. If you don’t want to share such stupid information, then better you stop than repeating same justification 🙂

Bsu ji and mr pradeep take 20 lakh SA j labh 16/25….prev year and Thies yrar bonus is 50 rs per thousand fab for 25 yrs is 450 rs per thousand maturity is 54,00,000…..premium for that policy is nearly 89,000 Yearly basis that means take 7400 / monthly now take any financial calculator from play store and take Ppf account of 7400/ monthly And take 10Yrs extension that means total 25 Yrs ….Thier is ROI as Gov declare is 7.9 % latest we assume this is same for whole term the maturity. Is 53,36,000 …but in We pay 89000 /more because 16 yrs pPT that means take maturity nearly equal…In both sides Here In LIC Insurance is more important Like Natural .. Double Accidental … Disability…….Now take 2nd example of J Anand policy of 25Yrs Age person Of SA 20Lakh premium is 56500 / Yearly for 35Yrs term .. according to todaybonus rate of 49 rs and FAB of 2300.rs maturity comes of 1,0030,000 And Life time risk cover of 20 Lakh.. That means Total return of 1,20,000,00…Now take Same PPF account of 4700 /Mly deposit that means 56500/ Yearly of regular 15 Years PPf account and give extension of 20. Yrs with same deposit of 4700 / Means total 35 Yrs deposit with 7.9% ROI … maturity is 99,11,666…only Now In LIc cover of 25 Lakh from 1st Day for natural and 45 LAkh for accidental 20Lakh for disability cover with premium waving Feature ….Third policy I purchase last year You need calculation I give it now stop your stupidest comments …ok….give me any company name or any national bank or post. ? not knowledge ….To Take my 50 Lakh fund on 7.5% Life time ROI …..Your stupidest man…..That have not ability to Accepting Real fact……

One very simple reason why I would choose PPF here is, if I am not able to deposit 90k for a year they don’t stop paying interest to me. And if I want to withdraw money after 5 years including the interest, PPF allows me to do that.

PPF pays me higher interest when rates rises in the system.

PPF money cannot be attached by any courts.

PPF allows me to deposit money as per my wish on any day and month and I can even put 1.5 lacs any given year.

Most importantly PPF does not pay even 1 rupee of my money to any agent.

All of PPF money I deposit is completely mine any day.

All of this said after your calculations show PPF and LIC returns are the same.

I have already assured my family will get 1 crore if I die through term insurance.

LIC’s 20 lac is not enough for me.

I don’t want involve in nation building using my money as I pay taxes already.

Pradeep-Do you think he listens ?? 🙂

Not sure, but don’t you pay taxes in PPF if you withdraw before retirement age?

Also, there’s no harm in taking longterm LIC policies like jeevan saral. Not as an investment, but for security and tax free payouts. Though, it should only be 20% to 30% of your net worth.

SaralRider-SECURITY of what? TAX-FREE payout only available in this plan?

What retirement age are you talking about? PPF is a 15 year fixed tenure product that can be extended for blocks of 5 years after that. If you open a PPF account at the age of 30, its tenure ends when you are 45. After 5 years of opening, it allows withdrawal of upto 50% without taxes.

Tell me one LIC policy that does not penalise you for premature withdrawal? I bet you dont even get back all you premiums if you withdraw which means you end up in negative returns.

And finally safety and security? LIC puts most of the premiums in stock markets. Last year they had blockbuster returns from their investments. Look at what bonus they have paid, same as previous year.

I bet if there is a 50% market fall, LIC with all the losses will probably not pay any bonus. Most of their bonus payouts are not guaranteed. Anything thats labelled as long term, no damn company will guarantee you anything.

If you understand this, its better for you or else its better for LIC because they get their hands on your money, pay you peanuts and fund agents retirement

Pradeep-Let us wait for his reply 🙂

Vaibhav-If don’t know the art of investing, then why you are forcing all of us to follow the same 7.5% plan where you invested? Do you think on this EARTH, that plan alone generate 7.5% return??? Just show some maturity and decency while interacting on the public platform. Your tone of talking and the language you used up to now, show the mentality and frustration.

This is how agents fraternity getting a bad name, but not LIC. You defend your views, discuss healthy, but using bad language against anyone shows your status of mind and what type of person you are. Since the beginning, you are using the language which is not good for your own future. Forget about this discussion, let readers decide who is right and who is wrong. But try to understand the basics of communication and how to behave with others.

I kept silent and not uttered any single bad word against you. But you are using bad words to Pradeep also. This shows your mentality and how you grown up.

When I Prove…my side How Lic is unique then you Divert from subject..Ya I know your problem…that their is no option for you…..I fell So said about you that..I prove you as you are personaly again LIC …so sorry Basu ji

…Do your Lie work and be happy in speaking against LIC (Hathi chale Bazar ………bhukane Lage Hazar). I am not agent …but I am policy Holder of LIC…good by and really sorry….

Vaibhav-Not deviating. I am still alive and energetic to discuss, BUT HEALTHY discussion ONLY. Not the discussion which you are using without knowing what is decency. You proved I am against LIC? I am still saying, I am LIC agent 🙂 I am fan of two plans of LICs!! Whether you are agent or whoever, it does not matter to me. But numbers and knowledge speaks louder than misbehave 🙂

About j Anand I discussed all parameters and calculation in my previous Discussion …And I need 100Yrs Garuntted for me and after me for my wife ….what about I live or not live for 100Yrs is not a point but point is 100Yrs guruntee…

Vaibhav-Hats OFF….UNIQUE PIECE!! Long live the LIC with such agents. Now let readers decide who is NONSENSE 🙂

Basu,

Can you please keep out mentally retarded people out of your blogs?

Clowns can be irritating sometimes.

Pradep-That’s why tagged him finally UNIQUE PIECE 🙂

Dear Basu Sir,

I think you should IGNORE guys like Dheeraj and Vaibhav. They are hidden LIC agents. They cant digest facts. Even new born kid of today knows that LIC returns are 4% and if you adjust that to mortality rates, the returns are 1.5% per annum. They are fools to pay for 25 yrs and then get returns of 4%. Even staying in SIP MF for 25 yrs will pay you 20% CAGR growth. You truly said they are the Frogs in the Well.

regards

RAJESH PAI

Rajesh-It is common for me whenever I write against LIC’s low yielding products. I can understand their frustration. They create noise and after that they silent. But for all readers, they give the actual image of LIC products 🙂

Hi Basavaraj Sir,

Your blog is really very informative.

I was sold a Jeevan Saral policy by my LIC agent in 2008 & i have been paying Rs. 19200 premium (half-yearly) since Jan-08. I have completed my 10 years when i paid my 20th premium this Jul-17.

I would want to surrender this policy & get a term policy.

I have not been able to find out what the surrender value would be since there is some confusion regarding Guaranteed surrender value, special surrender value etc.

Can you please let me know what would my final settlement value be if I surrender the policy tomorrow.

Would greatly appreciate your help.

Regards,

Rohit

Rohit-Based on the applicable MSA, you will get the LA (Rate for 10 years plans, which explained above). If you have a doubt regarding the same, then contact your branch, they tell you the MSA for 10 years for your policy. Based on that you can assume the value of maturity considering above Jeevan Saral LA rates.

The applicable MSA would be pro-rated right ?

As in, since my MSA = 17,04,352 for a term of 35 years, applicable MSA would be 1704352/35*10 = 486958 . Would that be correct ?

Special Surrender Value = Sum (100% MSA for the completed term + LA)

LA = 486958/1000 * 400 = 194783 (Acc. to latest LA LIC table of 2017-18 )

Hence Special Surrender Value = sum(486958 + 194783) = 681741.

Is that correct sir ?

Rohit-No, it will not work like this. You have to specifically ask the MSA for 10 years. It is not to be pro-rated.

I found this link :-

http://www.investobite.com/maturity-calculator/lic-jeevan-saral-plan-165.html

where I put in my Death Sum Assured = 800000

Age at purchase : 22

Policy Term : 10 years

Year at purchase : 2008

This gives me MSA = 3,56,704

Hope this is correct ?

Rohit-I can’t authenticate that portal. Better you check with branch rather than this. But you can randomly work out. Now consider MSA as Rs.3,56,704, then LA for 10 years term and premium band of your’s is Rs.400. So the total LA will be (Rs.3,56,704*400)/Rs.1,000=Rs.1,42,681. Hence, total you will receive inclusive of LA is Rs.4,99,385. If you do the return on investment (IRR), then it is meager 5%. This is the REALITY of such plans. Invest for 10 years and expect just 1% more than your savings account interest rate. But agents claim LIC helping in nation building. At what cost?? It is at the cost of your’s MONEY.

Completely agree Mr.Basu. I got fooled into buying this policy at a young age since the LIC agent was my father’s friend.

Would advise all to not buy such endowment plans, rather use LIC for only pure insurance policies.

Thanks again for your help !