Section 80C is one of the great tax saving tools for all of us. In my last post, I explained all options available for tax saving. But in this post, I will concentrate only on the deduction under Section 80C.

History of Section 80C

Section 80C replaced the old Sec.88 and came into effect from 1st April, 2006. The current maximum limit of Deduction under Section 80C is Rs.1,50,000 in a financial year. The earlier limit of Section 80C was Rs.1,00,000 up to FY 2014-15. Later on, it was increased to Rs.1,50,000 and same is continued.

Section 80C constitutes many investment options for tax savers. Hence, it is the top most choice to many. But many believe that only investments can be claimed for Deduction under Section 80C but the reality is some expenses like tuition fee or home loan are also part of such Deduction under Section 80C.

This section is available only for individuals and HUF only.

Deduction under Section 80C options for Individual and HUF- # Life Insurance Premium

# Life Insurance Premium

Long back, I wrote a complete post on this. You can refer the post “Tax Benefits of Life Insurance“. Just I am copy pasting the same content here as below.

- Any premium paid towards a life insurance policy on self, spouse or kids and if the policy was issued on or before 31st March 2012 then the eligible deduction under Sec 80C will be only 20% of the sum assured. Let us say Mr.X took life insurance plan before 31st March 2012 with Sum Assured as Rs.3,00,000 term being 10 years and yearly premium Rs.65,000. But according to above rule, only 20% of Sum Assured (in this case 20% of Rs.3,00,000 which is Rs.60,000) is eligible for tax deduction under Sec 80C. So Mr.X can avail benefit only up to Rs.60, 000 but not Rs.65, 000.

- Any premium paid towards a life insurance policy on self, spouse or kids and if the policy was issued on or after 1st April 2012, then eligible deduction under Sec 80C will be only 10% of the sum assured. Let us say Mr.X took life insurance plan after 1st April 2012 with Sum Assured as Rs.3,00,000 term being 10 years and yearly premium Rs.65,000. But according to above rule only 10% of Sum Assured (in this case 10%

- Kids may be minor, major, married, unmarried, dependent or independent. It does not matter at all.

- You can’t claim Deduction under Section 80C towards the life insurance premium paid towards parents or in-laws.

- You can claim Deduction under Section 80C if you paid the premium to any of the insurance company. So there is no such condition that your policy must be from LIC. Life insurance premium paid towards private sector insurance policies are also form part of tax benefit.

- In case of HUF, the deduction can be claim towards the premium paid on the life of the member of HUF.

Sec 80C Reversal-Benefit you availed under Sec80C will be reversed if your policy closed or terminated within 2 years for traditional policies and 5 years for ULIP products after the date of commencement of policy.

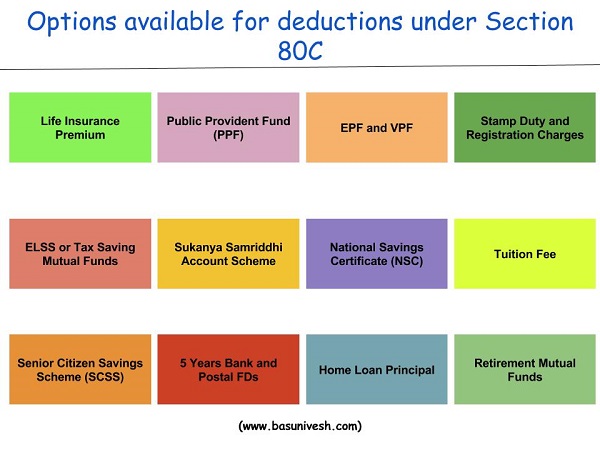

# Public Provident Fund

- Any amount you invested towards Pubic Provident Fund (PPF) in the name of self, spouse or child.

- Please remember that child may be minor, major, married, unmarried, dependent or independent. It does not matter at all.

- Let us say you have PPF account and if your wife deposited the amount from her source of income, then she can claim the deduction under section 80c, but you can’t claim the deduction. Because source of investment is from your wife. So only the person depositing into PPF will be eligible for tax benefit but the person who is holding it.

- You can’t claim any deduction under section 80c by investing in parents, siblings or in-laws PPF account.

Few posts related to the public provident fund are as below.

- All about Public Provident Fund (PPF)

- PPF-Loan and Withdrawal

- PPF-When to contribute to get higher returns?

- Excel PPF Calculator-Calculate goal, loan or withdrawal amounts

- How to transfer PPF Account from Post Office or Bank to another Post Office or Bank?

- 15 Rules of availing Loan against PPF (Public Provident Fund)

- Public Provident Fund -20 unknown facts

- PPF withdrawal rules & options after 15 years maturity

- Premature closure of PPF account – New Rules 2016

# Employees’ Provident Fund (EPF) and Voluntary Provident Fund (VPF)

Any contribution you made (employees) made towards EPF and VPF will qualify for deduction under Section 80C. This is the automatic option of investment, which salaried will enjoy. Hence, you can claim this investment without any hassle.

# Equity Linked Savings Scheme or Tax Saving Mutual Funds (ELSS)

These are actually equity oriented mutual funds. Such Mutual Funds will offer you 3-years lock-in. After three years you are free to withdraw the amount. But keep in mind that If you start SIP in the month of July, 2016, then you are eligible to withdraw this invested amount (units) only after July, 2019. Next month SIP will be after August, 2019. So if you start the SIP of a year, then you will not be eligible to withdraw all amount exactly after the 3 years from first SIP investment. But after 4th-year completion, you can withdraw the whole amount.

One more thing to keep in mind that ELSS mutual funds are equity-oriented products. Hence, do keep in mind that equity investment is meant for long term. Therefore, never enter into ELSS with a belief that after 3 years you can withdraw it. Market may give you negative returns too.

I wrote a post on top-rated equity-linked tax saving schemes. Refer below link for the same.

# Sukanya Samriddhi Account Scheme

Any amount you invested under Sukanya Samriddhi Account Scheme will be eligible for deduction under Section 80C. Note that this the girl child scheme launched by Government. I wrote about this product long back. Please click on below post to read about the same.

- Sukanya Samriddhi Account-An investment scheme for your girl child

- Sukanya Samriddhi Account -When to invest to earn more returns?

Do remember that this is debt product. Hence, you can’t achieve your financial goals by investing ONLY in this scheme. Treat this product as debt product and include the equity funds to achieve the kid’s long-term education and marriage goals.

# National Savings Certificate

This is the post office savings scheme. Minimum you can invest Rs.100 and there is no maximum limit. It is a 5-year product. This is the most famous product among all tax savers. But do remember that it is an illiquid product. I wrote about NSC long back. Please refer below posts for the same.

- NSC-Accrued Interest taxation and way to reduce it

- Post Office Savings Schemes (RD, NSC, MIS, SCSS)-Premature closure rules

- How to encash or withdraw NSC bought from different Post Office?

# Senior Citizen Savings Scheme

This product is mainly meant for senior citizens. You have to invest in a lump sum and you start to get the interest rate on a quarterly basis. The minimum amount is Rs.1,000 and maximum is Rs.15 lakh for an individual. Maturity period is 5 years. Any individual whose age is above 60 years can open this account. The complete detail about this product can be read from below link of my blog post.

# 5 Yrs Bank and Post FDs

These are fixed deposit meant for tax saving purpose and lock-in will be 5 years. Any amount you invested under such FDs will qualify for deduction under Section 80C. Please note that there are many variants of FDs like a year, 2 yrs, 3 years or 5 years (in both bank and Post Office). But 5 years FDs will only qualify for tax saving purpose.

# Home Loan Principal

In your home loan EMI, the total part of principal repayment will qualify for deduction under section 80C. Few points to remember.

- Tax Benefit will be on payment basis but not on due basis. Let us your repayment towards principal was due on March, 2016. But you paid it in April, 2016 means such principal repayment will be considered for deduction under section 80c for FY 2016-17 but not for FY 2015-16.

- Principal repayment during construction period will not qualify for tax deduction. You can claim the deduction only after the construction is over.

- You will not get any tax benefits for those periods of construction during which you paid principal.

- If you transfer (sold) the property before the expiration period of 5 years from the end of the Financial Year in which he obtains the possession, then aggregate amount of tax deduction already claimed in respect of previous years shall be deemed to be the Income of the Assessee of such year in which the property has been sold and the Assessee shall be liable to pay tax on such income.

# Stamp Duty and Registration Charges of home buying

Any amount you pay towards stamp duty and registration charges while buying a home will be eligible for deduction under Section 80C for the year in which you buy the house.

#NABARD Bonds-

Anything you invest in notified special NABARD Bonds for agriculture and rural development will qualify for tax deduction under section 80C.

# Tuition Fee-

Any amount you paid towards tuition fee of your kids (maximum 2 kids per individual) will eligible for deduction under section 80C. Few points to remember-

- An individual can claim up to the maximum of 2 kids.

- Deduction is available only towards tuition fee.

- Full-time courses are only eligible for deduction.

- Development fees or donations will not be eligible for deduction.

- Education institute must be situated in India.

- The school, college or university in which child studies should have necessary affiliations.

- You can claim the tax benefits for your adopted kid also (but within a limit of 2 kids).

# Retirement Mutual Funds

Thre are few special equity mutual funds which are meant for retirement. Such schemes qualify for deduction under Sec.80C. I wrote about such plans long back. Please refer below posts for the same. Currently, there may be few more in the market. But these two below posts will give you an idea of how such mutual funds will work.

- Reliance Retirement Fund-Is it a best pension plan with 80C benefit?

- Two Mutual Funds-Tax Efficient (Sec. 80C) and Pension Plans in India !!!

Other options to claim deduction under Section 80C of IT Act-

I discussed the major options available for an individual or HUF to avail the deduction under section 80C. Below are few other options which are also be part of this Section 80C.

- Payment in respect of non-commutable deferred annuity. It should be taken in the name of the individual, his wife or any child. In case of HUF, it is on the life of any member.

- Contribution towards approved superannuation fund.

- Sum paid towards notified annuity plan of LIC (LIC’s New Jeevan Nidhi).

- Subscription to notified deposit scheme or notified pension fund set up by National Housing Bank [Home Loan Account Scheme/National Housing Banks (Tax Saving) Term Deposit Scheme, 2008].

Along with all these default list, I want to add one more point here regarding NSC investment. The yearly interest accrued can be shown as income under the head of “Income from Other Sources” and claim the deduction under section 80c for the same amount as re-invested. I explained this concept in my earlier post. Please go through the below link for the same.

Conclusion-I am not saying that tax saving is BAD idea. But make sure that each of your investment should be linked to your financial goals. Many invest only to save tax. First, analyze your financial goals. Once they are identified, then while investing choose the product which suits to your risk appetite and goal tenure.

The second major mistake almost all does is to start investing after January month of every year. This is the bad idea. In a hurry, you may not plan well. This leads to investing in a wrong product.

I tried to cover all relevant options available for tax saving under section 80C. If anything is missing then you are free to comment.

invested in PNB Mera wealth plan it is a non participated unit link plan premium of 10000 per month term of 10 years . will it be beneficiary. should i get income tax benefit on it or not?

Mukesh-What prompted you to select this plan?

for wealth creation and life insurance

Mukesh-Never combine INSURANCE with your WEALTH CREATION.

Sir,I have invested in kotak assured savings plan with annual premium of RS. 75000 in my name which I have shown for tax exemption last year now can I show it for my husband tax exemption this year

Gane-Yes, he can show in his tax exemption stating he paid the premium towards your life insurance.

We ( myself & my wife) are planning to go for SBI MAX GAIN home loan for an amount of rs. 27 lakhs . how much ttax saving can i avail from this loan . rate of interest as per bank is around 8.50% .

Kiran-Please check the amortization table based on that principal of what you pay can be claimed under Sec.80C (as explained above) and interest part will be claimed under deduction of Sec.24 for up to Rs.2 lakh.

Hi Basavaraj

I am planning to take bank loan for open plot. Can I utilize this amount for tax deduction under 80C? Please confirm.

Santosh-For land or plot purchase, you will get any tax benefits under Sec.80C.

is amount paid for health insurance not covered under this?

Aniruddha-No, Health insurance premium deduction will be available under Sec.80D.

I am a salaried individual having minor daughter. With a purview of long term tax planning, can you suggest if I shall opt for “Specific beneficiary trust” (Private trust) or HUF?

Which option shall provide me and my daughter safety & security legally and financially in the long term?

Ankit-May I know in detail about your requirement of “safety & security legally and financially in the long term”?

I am earning 40K per month and i am investing currently in following manners:

2000 – Post RD( my name

2000 – Post RD(my wife Name)

2000 – PNB Rd(my name)

1500 – Axis ELSS

1000 – kotak select focus fund

1000 – ICICI Balanced Advantage Fund Growth

Now i want to invest more 1500 more per month for following goal:

Retirement planning and child education planning.

Please suggest me best way to invest 1500 per month.(NPS,PPF or any good SIP)

Vishal-Without knowing the goal time frame, how can I guide you?

I am 28 year old and want to invest for child education is 15 years and for retirement is 20 years.

Vishal-If your goals are more than 15+ years, why you opted RDs??

RD is not for that goal. RD is only for your information of my investment for better suggestion.

Vishal-That is OK, but if your goal is 15 years or 20 years, then RD not at all required.

yes, i know that, but now i want to put more 1500 monthly saving per month.

i want help from you about where to put this money .

every investment must have goal for this reason i have said my goal. you can suggest me better options after knowing my current investment.so i have mentioned these.

Please forget RD for long term goal.

and please suggest me one GOOD SIP for putting 1500 per month.

Vishal-First do asset allocation properly. For both goals debt and equity must be in ratio of 30:70. Check whether the products you are investing are matching this asset allocation. Also, whether they are liquid enough to use when you reach 15 years or 20 years. Can you answer me?

Yes, you are right, i need same kind of allocation and liquid.

so please suggest me these kind of good product name.

Vishal-For equity, you can refer my blog post “Top 10 Best SIP Mutual Funds to invest in India in 2016“. For debt, you can use PPF.

Dear Basu Ji, your website is awesome! Got to learn so many things from here. Can I ask one question-

I’ve salary income in private MNC have form 16, ad-sense income, FD interest income, and little savings a/c income. I’ve sold some old used items on ebay, and got some income from it reflected in my bank a/c. And did some online tuition, fees sent to my savings a/c online.

My question is which ITR file should I use to claim return? I’ve not submitted 15G/H form.

Deepak-Refer my latest post for the same “Income Tax Return filing forms for AY 2016-17 (FY 2015-16)-Which form to use?“.

When parents become dependent, can I claim their insurance premium amount to under my 80 c?

Siva-Premium paid towards self, spouse or kids (Kids may be minor, major, married, unmarried, dependent or independent) will be allowed for deduction under Sec.80C. You can’t claim on parent’s insurance premium.

thank you for your clarification on my doubt sir.

Hi Basunivesh,

I am an NRI citizen. I am holding resident savings account in India and not yet converted the account to NRO. The interest earned in this domestic fixed deposits are TDS at 10% . The total income earned in India is less than 1 lakh through bank fixed deposit interest. Also please note that this is the only income I earn in India.

Can I claim the refund while filing the tax returns? Please advise.

Prasanna-The first wrong you did is holding savings account. Second wrong you are planning to do is to claim the amount while your status is NRI.

Thanks Basu for your reply. Lets say If I hold NRO account then Am I eligible to apply refund the TDS?

Prasanna-Yes, if your tax liability is less than the TDS rate.

Sir, i am investing 10,000/- in LIC money plus ULIP since 2007. shall i continue this or discontinue. pls advice thanks

Ketan-For what purpose you invested and why you now felt to withdraw?

invested on my wifes name for life insurance. just started checking on net there is no good feedback, wanted to check with you for its performance

Ketan-Better to come out at the earliest.

Thank You