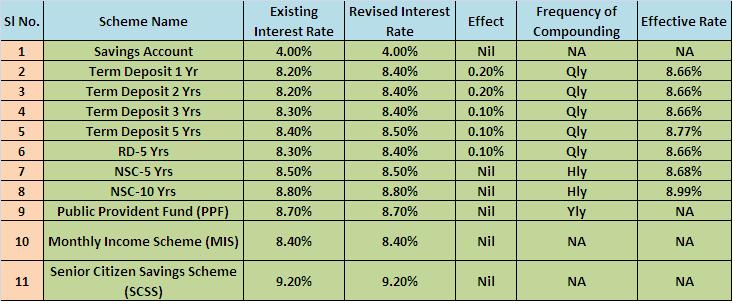

Today Government announced interest rates of various Post Office Saving Schemes for 2014-15. These changes will come into effect from 1st April 2014 to 31st March 2015.

Below I listed the revised interest rates with previous year rates for your easy understanding.

You notice that only Term Deposit and Postal Recurring Deposit interest rates are hiked. But no changes were done to NSC, PPF, MIS and for SCSS.

Government revises these rates on yearly base as per recommendation of Shyamala Gopinath Committee. Usually these rates were arrived to align G-Sec rates. Even though interest rates looks attractive but still you need to think post tax returns from each scheme before proceeding for investment.

56 Responses

What is the rate of interest for 2021 April to jun 2021?

Dear Panda,

Wait for the announcement.

Is there any lock in period for POIMS investment in the post office saving scheme.

Sachin-You refer my earlier post “Post Office Savings Schemes (RD, NSC, MIS, SCSS)-Premature closure rules“.

sir,

maine august 2014 ko post office mai RD khulwaai thi jo mai pure 5 year chalana chahta tha lekin mujhe paise ki jarurat thi to maine 3 year 1 mahina yaani 37 kist 3000 rs. par month ke hisaab se 111000 rs. jama kiya ab mujhe 37 month mai kitna interest milega. pls. help

Reply

Pushpendra-Check with Post Office.

Hello,

In the Mahila Pradhan Kshetriya bachat yojana of Post Office, the agent commission is 4% while for other schemes it is around 1%. Why is there so much difference? Kindly explain

Deepak-I am not the right person to answer. Because it is purely Post Office decision regarding setting the commission to agents. I think RD also provides higher commission to lady agents.

Dear Sir,

I want to invest 43000.00 Per Month for 5 years,Which is the best option for me.It must be secure of nature, So that the Minimum Return must be 30 to 40 Lac.

Sanjeev-May I know the definition of YOUR secure in nature? Do you know how much % of return is called secure in today’s interest rate cycle? Also, do you know how much % of return you are expecting?

Is there any one year rd scheme in post office?

Nithya-NO.

Dear Mr Basavaraj

i am 63 years old , my annual income is 7,20,000 / Annam

what are the saving scheme I should adopt to save Income tax

with regards

Chandrashekhar-There are many tax saving instruments available in the market. However, which suites to you will depend on YOU.

Sir, Iam 40 yrs old and looking for online Term insurance. Which term insurance should i select? pl guide.

Arunkumar-Please read my earlier post “Best online Term Insurance Plans in India for 2015-A comparative list“.

Hi,I am 28 years unmarried and want to take investment Plan for less than 5 years,kindly suggest me best plan, I can spand 6k to 8K per months .

Sudhir-Either opt for RDs or Debt Funds.

I want Postal Fixid Deposoit

whats is Mahila Pradhan Kshetriya Bachat Yojana (MPKBY). whats would be the interest rate and period .. could u guide me please..

Sneha-I need to check it out. Please provide me sometime.

Hlo Sir,

I am 27 yrs old unmarried person.My income is 3 lac per yr.

I havnt any saving scheme or policy.

I want to have one.

So pls tell me which one is best in respect of high returns and in what time: NSC,LIC,PPF,FD or any other.?

Malkeet-Products you mentioned are all low yielding. So if your time horizon is long term, like more than 5-7 years then why can’t opt for mutual funds? At the same time don’t forget to buy term insurance on your life.

Thanx for reply sir…????

Pls recommend me that which mutual fund is best and approx what returns are.

Also which term insurance should I buy.?

Again thanx sir g….

Malkeet-Please read my earlier posts “Best 10 Mutual Funds to Invest in India for 2014” and “Best Term Insurance plans in India (After 1st Jan 2014)” which helps you in shortlisting the funds and term insurance.

Hi

I am 37 yrs old. I have two kids both 2yrs 5 mths old…

My goals-2 crore each for them after 15 yrs for education and 3 crore more after another 08 yrs for daughter’ marriage

I have life insurance of 50 lakh.

Me and my family are medically covered. I am a govt employee so post retirement pension will be there

I have 4.5 lakh cash which I want to invest ……also I have 55000/- after my monthly expenditure…….pls suggest me how to divide this in various options….. To achieve my goals

Megha-First let me know how you arrived at Rs.2 Crore and Rs.3 Crore? Also do you feel your insurance coverage is enough? Ideal coverage should be around 15-20 times of income. Please reply so that we discuss further.

As on today the expenditure on one person’s higher education may vary from 40-50 lacs so after 15 yrs it would be May be four times …..a rough idea so around 2 crore

You are right about the insurance but I am the mother….my husband is also there and if something happens to me my husband is there……

Megha-May I know the course you are referring which costs currently Rs.40-50 lakhs? If no one financially dependent on you then insurance is truly not required. But whether your husband have sufficient insurance coverage?

i want to fix money in post office near about 100000 for 5 year which is best plan for me?

Rohit-You already have amount, time frame set and product also. Then what is your doubt?

Hi Basavaraj,

Kindly let me know if we break RD,MIS & NSC after 3 year before its maturity then how much intrest will be give on on all these products.

Is there premature withdrawal allowed in MIS,NSC & RD ?

What is maturity time frame for MIS & NSC..Is it 5 years or 6 years..?

Thanks

Vishal Garg

Vishal-Premature withdrawal permissible in RD only after 3 years (interest will be current applicable savings account), MIS after 1 year (discount of 2% interest). But if premature after 3 years then discount on interest will be 1%. NSC can’t pre-closed (except death of investor or Govt orders).

MIS is for a period of 5 years. NSC for period of 5 years or 10 years.

Hello Basu,

I want to buy a traditional life insurance of about Rs 1000 a month first before I start investing in mutual funds. Please advise the best product in the market. Thanks!!

Surendra-May I know the reason behind going for Rs.1,000 per month investment in traditional plans?

Hello Basavaraj,

i am Rathanvel. I would to start a New LIC Policy ( New Jeevan Anand -815). i have one doubt,plz clarify me.

if i start the LIC policy through LIC Direct marketing is better OR start the policy through the LIC Agent is better?

Instead of start with LIC Agent, i will start my policy through LID Direct marketing, Can I get any more benefits ( @maturity values). plz calarify it.

because, i hear about that, if we start the policy Directly, the Agent Commission is Saves for LIC, so the LIC provides some percentage of amount to the Customer at the time of maturity. is it true ?

plz clarify it. i am expecting your reply.

Thank you.

Rathnavel-As of now there is no such set up in LIC that to buy plans directly without the involvement of agents or direct marketing executes. Even if you visit LIC branch directly and buy the product then there will be no such benefit. So I don’t think any difference.

What you heard about direct buying and such saved commission payout to you at the time of maturity as additional benefit is all false.

Sir, this is to have my life covered first and get some returns, cause I don’t have much idea I am just playing it safe….and I am open to change the idea though.

Surendra-Well said 🙂 You need to buy insurance to cover your life right?? So I have a question for you, suppose after buying this plan, you die then for how many years your wife and kid will survive with the insurance claim amount and death claim proceeds of this policy? One year…two year or maximum 3 years. Afterwards??

Also I am not promoting you only tax free bonds. I just gave you an example by stating that without risk you can earn GUARANTEED return from other products too. Also in such tax free bonds you know how much you get in advance. But in such traditional plans returns depends on bonus which fluctuate yearly.

So let me know your decision.

Looking upon your feedback/suggestions, I have decided to go for Large Cap Mutual Funds (SIP)….Please advise.

Surendra-You can go with Franklin India Bluechip Fund (G). At the same time don’t forget to buy the term insurance to the tune of at least 15 times of your yearly income immediately.

Hi Basu, thank you very much for your valuable suggestions/feeback.

Surendra-Pleasure 🙂

Hello Basavaraj,

i am Ramkuar. I would to start a New LIC Policy ( New Jeevan Anand -815). plz clarify my doubt.

if i start the LIC policy through LIC Direct marketing OR take the policy through the LIC Agent is better?

Instead of LIC Agent, i start my policy through LIC Direct marketing, Can I get any more benefits ( @maturity values). plz clarify it.

.

Thank you.

Hi Basavaraj,

i like to take new LIC new jeevan anand policy. i can able to pay Rs 8000 to 10,000 per year.

so, can i take @ 2lac and 21 years is better OR 1.5 lac – 16 years is better.

@ which one we will get more FAB and Bonus, which is better for maturity value ? plz reply

Thanks

Geetha

i like to take new LIC new jeevan anand policy. i can able to pay Rs 8000 to 10,000 per year.

so, can i take @ 2lac and 21 years is better OR 1.5 lac – 16 years is better.

@ which one we will get more FAB and Bonus, which is better for maturity value ? plz reply

and also Compare to Bank OR post office FD’s , How LIC is best ? OR compare to LIC, Bank OR postoffice FD’s are better ? .. please suggest me.

Thanks

Geetha

Geetha-To me the first concept of mixing your insurance need with investment is a big mistake. Second thing, yes if you look at long run these LIC policies will fetch you lesser returns than FDs or PPF.

Geetha-First let me know whether you are buying this policy for the sake of insurance of investment?

Thanks for your reply. i like to do the investment only. so which is better ?

Kanagavel-Then no need to buy any LIC plans. Buy term plan to the tune of 10-15 times of yearly income, rest based on your financial goal and your risk appetite start investing in products.

Hi Basavaraj,

i have a samruthi plus ( unit linked deposit ) from last 3.5 years. i would like to close this is better ? OR can i wait some more years ( 1 to 2 years) ?

how it is benefit for my maturity value ?

suggest me.

plz reply

Thanks

kanagavel.

Kanagavel-It is a worst product.But you already entered then you have only option is to let it complete 5 years then come out of this plan. Because there will be no charges if you come out of this plan after 5 years.

Hi Basavaraj,

thank you so much, and 1 doubt on this, in this samruthi plus they are informed “Highest NAV value ” during the period ( example : maximum NAV value @ 5 years)only will be the maturity return points like that.

so, we will get the maturity returns of the Maximum NAV valve OR the current NAV value is the maturity value ? plz clarify it.

thank you.

Kanagavel-Even if you stay for long, return from this plan will not cross more than 8%. This product simply fooled all investors (sorry to use investor for insurance product). That is the reason IRDA curtailed in launching new such plans. It is a typical debt product but sold as if you will get GUARANTEED return from equity investment.

I need full details about the LIC plans Jeevan saral and Jeevan anand. Mainly how jeevan saral bonuses will be given.

Sakthi-I think my previous posts about Old Jeevan Anand, New Jeevan Anand and Jeevan Saral will help you in understanding better.