Whenever you thought to invest then first thing you notice is, insurance agents luring you to invest in some insurance plans. One of reason from that may be his high paid commission structure. So it is best you understand it fully before proceeding further.

Note-The commission structure will change from 1st April, 2017. I have written a post on this. Refer this new updated post at “Life, Health and Vehicle Insurance Agents Commission in India”

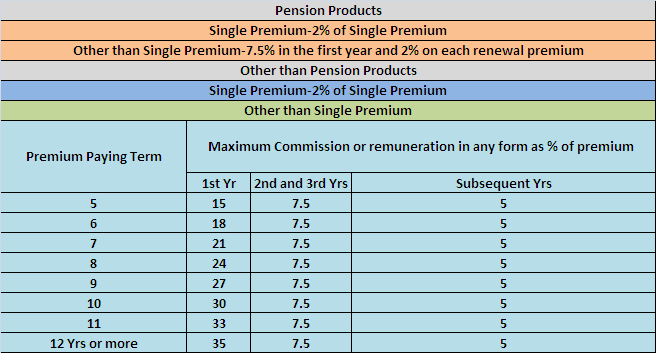

First let us see the commission structure of agents. This I am updating after the recent IRDA’s (Non-Linked Insurance Products) Regulations 2013. Below is the chart which will explain you the maximum commission structure in detail.

By looking at above table you noticed that if term is more then your agents commission is also more. So now ask yourself why your agent lure you to opt for longer period insurance product rather than shorter. I too believe that insurance is the long term product. But main motive is different than what you think. Even term plan which you take from offline mode also give the same commission structure to your agent. Their may be some minor changes based on product. For example in money back plans agents will receive less commission than normal endowment plans. But overall this is the structure you find for most of the traditional plans.

Here by publishing these rates I am neither against the commission structure nor I am supporting this. But it is your right to know the commission what your agent earn from your investment. I am expecting some agents comment who justifies this commission structure putting reason as the expenses they need to bear. Also I am expecting some comments who are totally against to such a high commission structure.

But I strongly believe that, hiding our main motive to sell (commission) and sharing the commission with clients are two major wrong things. When online term plans started by few insurance companies then few so called IFAs talked too much about the cost advantage of buying directly instead of offline. But I saw the same IFAs not opening their mouth regarding the direct plans of mutual funds. Each product has it’s own positive and negative points. So neglecting them outright from our point is not true. For example, Bank FD may be must not product for the young who is ready to take risk. But same FD may be the major investment product of the same age group guy who is totally risk averse.

Let us now take one example to understand how much an agent can earn.

Term of the plan-20 yrs, Product-Endowment Plan and Yearly Premium-Rs.1,00,000.

Looking at earning you may feel it a lucrative profession. But it is not that much easy as it looks. As I told above, few are also of opinion that commission need to be barred as is with mutual funds. Let me see what will unfold in future 🙂

My brother purchased LIC Endowment plan of 25 lakhs for 20+ years. Sir, is it better than other endowment policy of banks and private insurers. Please suggest how much would he get upon maturity with S.A+bonus+final addl bonus=?

Dear Samarth,

If your brother is comfortable with 4% to 6% returns, then let him continue. Regarding maturity amount, contact your insurer.

Sir, I read all of your posts. All are interesting with apt advice. Please advice me, …can I switchover to POSTAL LIFE INSURANCE for longer period, our agents are not recommending me…. rather asking me to go for other LIC policies. My age is 59 years and I am an Exserviceman. Being survived on pension. Solicit your advice please.

Dear Ramakumar,

You can’t switch from one insurer to another insurer.

Sir my monthly policy is 2274 but lic is taking from my bank is 2800 I didn’t get that.

Dear Yanki,

Check with LIC in this regard.

Hello, sir my mom paid 30000 lic plan for 15 years scheme and after maturity it wil be 50000 so how much commission does agent get from in it.please reply me…sir

Dear Ruchitha,

Please calculate as above and why NOW you need this calculation?

i have 4 SBI life policies foe which i pay yearly premiums. my agent will be getting a huge commission out of it, Is it possible for me to pay the premiums now without agent commission?

Dear Babu,

Sadly No. But do you think by avoiding the agent commission, still feel such products are best suitable for you?

i sell a policy for child money back plan for 19 years and premium is 18000 so what will be the commission?

Dear Deepak,

Refer above post or contact your Life Insurance Company.

How much commission does Sbi agent earn on investing

5lakh per year for 5 years

Dear Ramesh,

It is same as I mentioned in above chart.

Can agent’s license be transferred to other ?

Dear Sourav,

Sadly NO.

Sir, iam joing as adviser in sbi life insurance… what is the target I have reach within 6 months..? Or how many policy I have to give..?

Aru-Discuss the same with SBI LIfe.

Now I see why LIC agents mis-sell policies and showcase 8% Rate of return. Is there a way we can have such crooks penalized. Is there any formal process to bring this to open

Sachin-The rule of IRDA clearly defined to show INDICATIVE RETURNS only but not the expected returns. If few agents breaking this rule, then you can immediately complain against such agents with a concerned insurance company or IRDA Ombudsman.

Sir I want to take one policy without consulting agent. Please told me one security policy to my family’. Recently got govt job. But my economic position worst. So please tell best policy in LIC or any other Best policy

Srinivas-Security policy means?

Hello. I recently have a policy with yearly 25000 primium in 20 years term. I want to know can i have some commission from the agents commission?? Please let me know.

Manab-Asking commission sharing by you and the same sharing by an agent is ILLEGAL ACTIVITY.

It is Very Pathetic, it is Like Asking a piece of Bread what we are eating,

Now all insurance agents are sharing up to full extent of their commission to survive their agency, Or to Retain the club membership from some of the top Insurance agents, They just want policy count no matter how it come.

Investors also greedy, for a small first year commission they fall in a Trap of paying a policy for 15 to 20 years,

If Investor pays from 2nd Year it is ok otherwise, agent will be under big loss.

I have some policies in lici and other private companies.. is there any possibility of losing my money which i have invested in private INSURANCE companies?

2. My age is 23 and i want to know that if i save Rs. 5000 per montb in mutual fund then wbat will be my return amount when I will be aged 60years?

Raj-Loosing money in the sense what if they close the doors?? Expect around 7% from debt and 12% from equity. Do asset allocation in the ratio of 30:70 in debt and equity. Then you can expect around 10.5% from your portfolio. Calculate the same for your age of 60 years.

What is the minimum years of agency business to get lifetime renewal commission to insurance agents in life insurance?

Ajeet-As per my knowledge it is 5 years.

Sir when will agent get his bonus commission. I am only getting 25 percent of my commissions but they told me 35. Now they are saying 10 percent is bonus commission. Now its a puzzle for me

Deepak-Contact your insurance company.

Sir will I get accured bonus with while surrendering my new janaraksha plan

Bala-YES but not fully but based on surrender value formula.

i have an policy ,its been a year i am depositing money through an agent.

how to remove agent now from my policy?

Radhe-Sadly YOU CAN’T.

Sir , 35% of which year ?

From joining year of agent orr 1st year of policy of insured ,of agent gets 35% of premium.

Dear Pradeep,

It is first year commission.

Hai sir i am Santhosh have decide to join in a SBI life insurance as a agent.i need to clarify something about it, if i only earn commission or any monthly basic salary is available in this job. Pls tell me sir

Santhosh-This is a commission based business.

My Employers surrendered following policies of Bajaj Alliance Life Insurance Co Ltd . All polices are linked with life cover . Therefore can I assume that no TDS has been deducted while receiving the surrender amount:

1) Bajaj Allianz Group Asset Allocation Fund ( Premiums paid from 2010 to 2016 – 7 annual premiums paid) and surrendered on 02/08/2017

2) Bajaj Allianz Equity Index Pension Fund(Premiums paid from 2010 to 2017 – 8 annual premiums paid) and surrendered on 02/08/2017

3)Bajaj Allianz Equity Index Fund(Premiums paid from 2010 to 2017 – 8 annual premiums paid) and surrendered on 02/08/2017

4)Bajaj Allianz Max Gain Fund 1(Premiums paid from 2010 to 2016 – 7 annual premiums paid) and surrendered on 02/08/2017

Kindly reply.

Thanks,

R.Ravichandran

Ravichandran-Refer the applicable TDS rules for Life Insurance as below. Based on that you can assume the TDS applicability.

TDS U/s 194DA is applicable to:

The policies where the sum assured is less than 5 times of the premium paid for policies issued on or before 31st March 2012 or where the sum assured is less than 10 times of the premium paid for policies issued on or after 1st April 2012.

All policy related payouts such as Partial Withdrawal, Surrender, Maturity, etc, if the payout is above Rs.100,000 within the same financial year.

Hello Basuji,

I have HDFC LIFE policy since last 2 years directly from HDFC bank and not agent. Yesterday I got call from a person pretending to be HDFC relationship manager ( in legal department). He told that the commission of 15k per year is directly going to agent and he reported the matter to senior official. He suggested that he will generate agent code so that all commissions gone to agent will be recovered. I would like to know could it be a trap and are there really agents in bank? I appreciate your reply.

Thanks

Rakesh-You guessed rightly. Report this to HDFC Life immediately that how they got your contact details and policy details.

Hi,

Even I have received the call today from 011-6615-1900 and the person who spoke with me told me that he is calling from LIC Head Office, Delhi. He further told me that my LIC policies have earned a profit of Rs.184000 and my agent would be getting 40% of this amount as commission since his agent code is tagged to my policies.

He suggested me to remove the agent code from the policies and add my customer ID so that I can start receiving the profits.

I realized the trap when he told me that I will have to buy a policy in the range of 40k- 50k from any of the 3 companies where LIC invested my funds in order to generate customer ID

I reported this to my LIC agent and hopefully LIC would take some stringent action against such people.

Chetan-Thanks for sharing this incident.

mjhe apnay aap se sharam aata hai sir ki is internet k zamanay mein insurance company se chuna kha gaya

now i want to state that i have a new jeevan anand policy of SA 20 lac with death benifit rider and term 33 years my current age is 27. I have paid 40k for premium, now i want to shif to ur style of Term insurance + PPF+ELSS.

What is guidance in this regard sir.

Maksi-You are in right direction.

Hi, My age is now 30 years. I have a baby of just 1 month.

Please advise which Insurance policy would be better for my baby’s future and also my future necessity.

Anirban

Anirban-Your requirement is insurance or investment?

Tell me insurance information

Sandeep-What information you need?

Have u taken a policy or not if not then I will help u out i’m an insurance agent .pls tell if u want a policy

Neha-Let her decide. Don’t try to sell your business. But sell your knowledge.

SIR I HAVE JUST BECOME AN LIC AGENT

SO PLZ U COULD TELL ME HOW WOULD I HAVE TO WORK AND ABOUT THE COMMISSION TOO

ANKIT

Ankit-Sadly I too don’t know.

Which payment of LIC agent ?

please answer sir .

Veer-I am unable to understand your doubt.

What is a an agency year? when will i get my bonus commission? will i get d bonus commission all together or in month wise. plz do rply

Vishal-Agency year is the date on which your agency became active to next 12 months. I am not sure when insurance companies pay bonus commission. Check with your branch.

Thank u so mch fr ur fast reply. as i m an agent n i have my date of joining as 18-9-15 so is my agency year is from 18-9-15 to 17-9-16?

Vishal-It starts from 18th Sept 2015 and ends on 17th Sept 2016.

Dear Sir,

I had worked as a LIC agent for around 3 years & 4 month and than after not able to continue my works due to delivery case and poor health condition. (Arthritis )

Sir, please suggest me how to claim for renewal commission as i am very need of money.

Regards

Aparna-If you not completed 5 agency years and not done minimum business then they not pay you the commission. I hope they might already told this reason to you.

Very nice

Dear Mr. Basavaraj

Excellent forum and Thanks for providing this platform..

I am 53 years old and would like to invest in Jeevan akshaya immediate annuity plan VI.. Sir is it advisable to apply online or offline ? I checked with an agent for sharing the commission.He says I will have trust him and He will pay when he gets it from LIC..

Or is it better to become an agent and get the commission on self policy..

My second question is on becoming agent and to continue to receive commission from LIC, is it necessary to sell 12 policies of total 1L Premium or one or less than 12 policies with premium of total 1L for five years.

Thanks in advance

Mohan-The plan is available ONLINE. Better to go with online option. Turning agent for this purpose will not serve any benefit for you. Because LIC pays around 2% commission on this plan and that too only once. Yes, minimum business requirement will apply if you take the LIC agency. Instead of all these, I suggest to buy it online.

Sir, I jave just taken max life advantage plan monthly income through yes bank for 12 years. Was this the good decision to take insurance plan from bank as I have not got and discount in premium? Although agent was offering some commission in first premium paid but this agent contacted through my friend is not local.

Rajesh-It is purely WRONG of buying a product without knowing for which purpose you are buying. Banks never remain as banks, they are the biggest SELLERS. Stay away.

Hello Sir,

good for revealing the hidden facts, but at the same time does this information indicate us not to buy policy at all? or should be bought online and not from agent? If from agent then should the bargaining be done while purchasing a policy?

Thanks

Rakesh-My point here is how dangerous are traditional plans and with such costs how can one expect return of around at least 8% also. Buying through online or offline is purely your comfort. I can’t say anything on that.

Hi Rakesh, Any policy is costly if you buy it through online, however if you buy it with an agent, then it will cheaper than online. for any other query you can contact me.

Fozail-ONLINE costlier than offline? Can you elaborate that?

yes sir. in terms of money security offline mod is correct. and your illustration about commission of agent is also not correct because you are not deducting the service tax applied on commission. that is 14.5% of commission. and still you claim that you are qualified. if you deduct this SERVICE TAX than an agent will get 115425 ;; not 135000 as shown. and even this commission he/she will get in long 15 years not i 1st year. if still someone want to buy online policy he/should see claim settlement ratio of online mod that is hardly 40%. rest it is your money your decision. FOR MORE INFORMATION CONTACT ON—– 8104518333

Deepak-Money Security-OFFLINE BEST? Can you elaborate more? Oh k…I not took into tax…let me deduct tax, your expenses in acquiring the client (by sharing commission), then sadly agent not left out anything right? May I know the data which makes you assume that online policies claim settlement ratio is 40%? I dig deep into IRDA annual report yearly and not found such separate data. Come on…don’t shoot at air 🙂

FOR MORE INFORMATION CONTACT ON—– 8104518333

I am not shooting in air call me & i will explain your every doubt. do not publish wrong facts

Deepak-Why to call? Why not explain here on this platform??

Sir, Am 31 years old. I have baby boy of 4 Months old. Kindly suggest me best LIC policy

Shrishail-Stay away from a product which combines insurance with investment.

Dear Basu……

When I was reading one of your blogs, saw something about TV anchors and their advice about investment and then couldn’t read.Plz. provide the link

Thanks

Ravinder-Hope you may be reading this post “Read this-Before you follow Financial Experts who appear in TV and Press“.

Thanks Basu…. as Always!!!!

I have purchase a policy from Aegon Religare Term Plan with Accidental rider.

my age is 31 and policy value is 87 lacs and 46 lacs respectively.

now i have heard by many of my friends and office colleagues that i have taken Term Plan from

Non- Brand Company so please i request you to suggest me should i continue with aegon or i moved it to other company.

personally i have faith in Aegon but his settlement ratio is Low.

pls advice me best.

one more question

i am taking very little amount of Wine/Beer in some party function and i have mention this in my policy.

in future if i will die at any reason or by alcoholic reason my claim will be reject due to this

Ajit-The brand of your friend may not be brand for me. So is same for you. Don’t believe on rumours or the so-called BRANDED INSURANCE COMPANIES. Continue with your plan. If you started any new habit, which you feel may affect your health badly, then better to inform the same to your insurance company (even though there is no such restrictions).

Ajit kumar do not worry as every insurance company has to take licence from IRDA. For which they have to deposit 200 corers rupees as security to IRDA. so no insuranc company can run with your hard earned money

Can I take a policy for myself being an agent from LIC and what benefit do I get out of it? Will it also be counted as one among the 12 in a year?

Srinath-Yes, you can buy the policy on your own. For commission purpose, it is considered as regular policy. But you can’t fill the moral hazard report for your own report. It must be from your development officer or someone from LIC officials.

Means, I will be getting commission for my own policy? right?

Srinath-YES.

Sir

I take LIC agency under a D.O. but now I want to work as a C.L.I agent under a CMS club member agent. What is the procedure to change the agency.

Kuntal-Ask your Branch Manager.

Sir,

I am Policy holder of LIC Jeevan Anand from last 5 years and pay 50k premium yearly. Two days ago, i received a call from Delhi LIC office from finance department that it is our company policy that we invest 40% of premium paid by customers to share market and whatever the profit company makes it is distributed to agents because they manage the policy on behalf of the customers but if the profit amount is huge in monetary terms then it is the moral responsibility of the agents to inform and apprise the customers about the profit and give them share of it & if he does’t inform you then provide me another agent code of the person of your acquaintance and we will transfer the money to his/her account but without the agent code we fail to do so. He also said the i am pleased to inform you that your profit is exact Rs 189345 and your agent has already moved the file to get it & we call only to those customers whose profit is huge so that they can’t get cheated by their agents .

Sir, tell me what to do .How can i get the profit or share of it as my agent denies that it was a fake call.

But he told me the file no also and date on which agent moved the file along with the agent code which i found true when i match the code with the premium statement mentioned as Agency code no.

help me out from this sir, i will be grateful to you.

Singh-It is purely a SPAM. If you receive one more such call, then inform him that you will complain with local policy and also with LIC.

Hi – I am an LIC agent.. basically I work in an MNC and LIC is on my free time. I want to sell motor insurance. I live in Chennai. Please guide how to become motor insurance agent on part time basis just like LIC.

Srinath-Contact general insurance companies of your choice.

Thanks. I have 2 questions please.

1. in LIC, When will the bonus on the commission paid to the agent. I have completed two policies and got the commission. the commission bill says as bonus on commission as 10%.. when am I expected to receive this money?

2. In LIC, What is the requirement for staying as active agents? is it 1 lakh premium for the 1st year and likewise for the consecutive two years? if so, from 4th year, will i receive my commision though I don’t source policies?

Srinath-1) In initial years of agency, I think they pay it yearly once. But later on it will be regular one with commission.

2) You must continue the business for at least 5 years with minimum business requirement. Then only you are eligible for renewal commission (even if you stay away from agency).

Thanks.

What is the minimum business requirement? If I ask my DO he says life time… I know that isn’t fact…. Pls let me know…if I source 1 lakh premium in the first yr we’d the suffice?

Srinath-It is Rs.1 lakh of premium from first year policies and 12 number of policies.

What is your thoughts on LIC’s new Jeevan Labh policy?

Srinath-Read my latest post “LIC’s Jeevan Labh (Table No.836)-Features and Review“.

Sir i want to ask you that a lic agent also works as a hdfc bank agents .

Kapil-Yes but not as an life insurance agent of HDFC Life.

Sirji,

I am now 58 years old and doing work as LIC Agent since last 12 years and Now Zonal Manager’s Club Member at Nagpur. In 12 years I have experienced that people wants LIC policies as per their needs such as 5 years policy, 7 years policy, 9 years policy, 15 years policy, 20 years policy, 35 years policy, whole life policy, child plan, plan for youth, pension policy, policies for ladies, policies for couple (both husband and wife) and so on and I have sold all the abovesaid policies as per the policy holder’s needs never think that I am getting less commission because it is short term policy.

Some times the Branch Manager himself convince Agents to sell long term policy or surrender one policy and draw new policy. In this fact it is contraversial.

I reality An Agent (As per dictionary meaning Ä Gentleman) think others needs and then convince and then sell the policy whatever the commission he don’t think for commission he think for people’s welfare. In every field there is Dukhi Atma and they doing the wrong business such as Chartered Accounts guiding the people for black money manipulation.

LIC polices are guaranteed by Central Government of India. We see our currency note it is guaranteed by Central Government, like that LIC policies are guaranteed by Central Government. In case of Private Insurer it is registered with IRDA it donesn’t mean that it is guaranteed by Central Government.

Dilip Krishnarao Thugaonkar

Dilip-What is and how much is guaranteed? Also, when it comes to considering these products as investment, then how much according to you the returns will be? When it comes to considering these products as insurance, then for long the dependent survive with the death claim amount?

sir I am qualified in Lic ado exam.one of my friend says it is a tension job,termination will there,Lic ado is a target oriented job.so I am not able to take the decision to go with Lic ado job or not,so please guide me

what is the salary,during training after training,how much target they give initially,is there any growth in future it is suitable for me or not,my qualification is b.tech

Sathish-I am not sure about salary, perks or targets they give to you. But it is a pure sales related job. Hence, be ready for all types of tamasha. Also, huge earning potential.

sir,I want to know which is the best option Lic ado or SBI clerk,why is best.

Satish-Both are GOOD.

Very Informative!

Need small clarification even which I failed to ask to Agent and He too didn’t informed me the same.

I am planning to take Money Back Policy for 20 Years with 90K/Year (Or 1 L Premium/Year)

So as per Table he showed after paying Premium for 5 Years I will receiving BONUS of 2.25L (which means I invested 4,50,000 and I will get 2.25L as Bonus)..

Now He says 3 Years in Minimum if paid I will get return or else I loose money in form of Tax etc etc.

My Question is After paying Premium for 5 Years and if I stop from there will I still entitled to get back 4,50,000 (My Invested Money)+2,25,000(Bonus)?

Jayakumar-First understand whether you need INSURANCE or INVESTMENT. Second thing, they will not pay you the BONUS after 5 years, but the part of sum assured. They give you BONUS only at death claim or end of policy term. Third, if you want to close after 5 years, then it is called surrender or paid up according to decision you take. In both the options, you will not get the full amount of what you paid+bonus. This is a trap which NO ONE will share 🙂

Thanks for your reply!

I am looking for INVESTMENT for my Daughter’s with fair returns on timely fashion (so that same can be utilize for educations or purchasing of Gold or plot as an investments for their future) and premium payable not spreading over a period that by the time Policy ends and same invested money must be used for their higher educations.

I am 37 and 1st Daughter is of 2 Years and 2nd is of 8 Months Old.

In my earlier Post I was mentioning about Policy Premium was to be paid for 20 Years and Policy was for 25 Years (PLAN ID: – 821, Money Back Policy 25 Years).

Cant even use this money for my 1st Daughter’s marriage (2 Years+25 Years=27 Years)!

So my wife and I feel it is too long period of WAIT..

ALL Agents are more interested in selling Policy not less than 25 Years OR 20 Years.

Can you please help me by suggesting some of the best Policies?

Thanks & Regards,

Jaykumar

Jayakumar-If your main purpose is INVESTMENt, then seriously stay away from all LIC policies.

Thanks A Lot!

Sure.

I will look out for some other options.

It was timely Help!

Dear Mr. jayakumar

Insurance should not be confused with investments.

Insurance comes into action only in our absence. Otherwise overall it will fetch you an average of 6 to 8 % interest.

For eg.,

scenario 1: If I am paying a premium of 10k/ mth. and if I die in an accident after paying 3 premium, my family will get rs.40lac, where as investing in mutual will fetch you not more than 35k.

Scenario 2: I am well and I pay completing full term of 2oyrs are so. Your money will be given back with an interest of not more than 6 to 8% interest. So you money is safe.

Its you who need to decide on which one to go.

If you ve decided to go for an insurance, ask your agent for Plan 833(Jeevan Lakshya) of 10 policies of equal premium, term ranging from 10 to 19 yrs.

This will help you for your Daughters Studies as well as for her marriage ( Even in your absence).

Mani-Scenerio 1-I buy a term insurance of Rs.1 Cr with the premium of Rs.15,000 a year. Rest I invest in mutual funds. I death occurs after three years (as you explained), then my nominee will receive Rs.1 Cr insurance claim and Rs.15,000 from mutual fund. Which holds good??

2) I am well and survie the 20 years. Then I simply forget the yearly premium paid towards term insurance and get a decent return from mutual funds at 12%.

Which holds good?

Show me a LIC traditional product which fetches 8% returns please…

Mutual fund is totally depended on market, what if the market fails OS goes down, LIC is better and safe option 🙂

Arun-Do you feel LIC returns not depend on market? Do you have an idea of where LIC invest? Do you know which LIC product gives you GUARANTEED return?

This is surely not a trap when we agents giving a policy we will be telling every small detail of the policy , yes there is no bonus after 5 years only the surrendered value or the premium what u have paid in that 5 years will be given back there is no spam that things are all open don’t just misguide people please

Punith-Do all agents make sure that their clients aware of what they are buying??

DEAR SIR

I have invested Birla Sun life frontline equity -regular-growth plan from 15-09-14..now I wish to switch to direct plan of same fund. will it be attracted Exit load? when enquired in BSL customer care they said that every SIP instalment should complete 1 year… I have given request for SIP CANCELLATION for Regular plan and starting SIP for Direct plan through online..

let me know whether should I wait for anothe1 year to switch or now itself? .. can you please help me? I ve given below SIP details of plan.

15-09-2014 Purchase 1000 147.43

14-10-2014 Purchase 1000 143.97

14-11-2014 Purchase 1000 155.6

15-12-2014 Purchase 1000 154.44

14-01-2015 Purchase 1000 157.73

16-02-2015 Purchase 1000 167.92

16-03-2015 Purchase 1000 165.41

15-04-2015 Purchase 1000 168.32

14-05-2015 Purchase 1000 159.62

15-06-2015 Purchase 1000 156.68

14-07-2015 Purchase 1000 166.17

14-08-2015 Purchase 1000 168.9

Ramesh-Yes, you have to wait to avoid exit load as well as tax.

Sir, i want to join as a LIC agent

Life insurance corporation of India can you please give the correct guide lines , because i don’t know what is the procedure , and other thing how i can believe other agents because they not give any information ,

After reading your article, i think you can help to me for correct information

Please sir, because i and my father and mother previous getting more loss from invest in lic because of wrong guide lines from selfish agent, so I want to join as a LIC agent and give the correct information to customers for help to them and getting help me also

Thank you

Sir, can you please reply

Jitendra-Contact LIC Development Officers available in nearest branch of LIC.

i am starting with lic agent and one of my relative is buying policy for 10 lakhs

so what will be my commission on it. this will be my 1st policy sell

Rohit-Contact your Development Officer (DO).

Hello sir,

I am going to start LIC . One of the LIC agent is given me the following plan which is in budget for me . Please check and suggest me if i can go to start it or not.

Premium for Plan 833/16/13

S.A.: 400000

D.A.B. 400000

TR SA. 400000

YLY: 31578

HLY: 15952

QLY: 8057

MLY: 2686

Daily: 87

Total Maturity: 691600

Plan Special Feature:

If death occures within policy period then

1) 10 % of SA shall be payable from next year of date of death till the date of maturity. i.e 40000

2) 110% of Basic Sum Assured + Bonus and FAB, are payable on due date of maturity. i.e. 731600

Thanks,

RAfiq-First understand for how long your nominee will survive with Rs.4,00,000 (if death occurs during policy period). Whether they can manage at least for 15-20 years with this Rs.4,00,000 when you are not there? Also, if we go by your agent’s claim that maturity value will be Rs.6,91,000 for the term of 16 years, then return on this investment will be 4% (Term 16 years, yearly premium Rs.31,578 and maturity value as Rs.6,91,000). Your savings account itself providing the safest return of 4% then why to take pain of investing in this product? A simple way like buying an online term plan (from LIC itself) and investing in PPF (which fetches you around 8.7% return) will be a great combination than this worst product. Think and decide.

i want to be insurance agent.

I am replying to above article. Not all LIC agents lure customers to take policies with longer termes. There are many agents who try to sell the best product the customer needs! And regarding the commission… People should understand how much knowledge is needed to explain every product and their features and also suggest the best with customer needs!! What is the agents time and knowledge then if he can’t make his income out of it?? Luring is really an offending term insulting a persons profession. You should not convey your msg in such a wrong manner. There should be much better ways I guess to communicate the knowledge. FYI this is my thought and I have personally seen many hard working LIC agents!! no offense meant to the author but this is my view on your article!

Anusha-The picture you are creating about agents who only “sell best product the customer needs” or “knowledge is needed to explain” are the imaginary picture than the reality. If they are selling the BEST then why can’t sell pure insurance called Term Insurance?? Anyhow, it is your job to make your client to understand about the importance of insurance. Once it is done then why can’t only pure insurance than a combo product??

Hello,

My best wishes to all who are hsaring your views here!

Insurance policies coupled with investment options are really interesting from a global perspective.

Probably India is one big market in Asia which sells this product targeting mainly the middle income group!

Commission structure vs Cost base has to be looked into very carefully, we all understand that not all insurance agents are unethical or misselling the products with commissions in mind, but at the same time there is no other business which pays as high as 35% commission on some of the longer term policies and additionally 5% standard commission every year till the end of the policy term!

This is INSANE way of doing business, despite LIC is saving on salaries!

For example: on a 20 year endowment policy an agent is going to earn 35% in the 1st year, 7.5% for next 2 years and then 5% for the remaining 17 years which is equivalent to 135% of yearly premium!

Ofcourse, we need to consider time value of money here, but more than 1/3rd of the commission money comes in the 1st 3 years itself which is more than enough to motivate the agents!

LIC is so aggressive in promoting the policies through out the country by very attractive commission structure.

If LIC is so confident about their products, then hey can substantially reduce these commissions and invest them properly for customers and give more returns rather a meagre 6%-7% !

So when people say these commissions are very high, they clearly have a point and LIC is still able to honour them because the returns they are promising are compartively less and they are massive in size, as they have built a safe heaven kind of an image for a common man!

But, they can do a much better job in creating value to customers by cutting dwon heavily on commissions!

We all agree to the fact that incentives are essential, but it has to be fair and sustainable focusing on value creation to customers!

We are in a transition phase now, genrations have changed and people are more educated and informed. So, it’s a matter of time for LIC to restructure it’s business by considering the Indian macro economic scenario and global insurance industry becnmarks to be more profitable and sustainable!

Thanks.

Prasanna-Thanks for your views and endorsing my points 🙂

.Mr.Prasanna .

Your points are true and I am happy to see so many valid points. I have thought the same way about these high commission, but I guess there are some main reason behind this, 1) Very less percentage of ppl take initiation to go through the detailed information of the LIC policy they are going to take 2) psychologically i guess they want a physical agent to relay on in case of any doubt or any problem rather than going to a office or reading the terms and condition. 3) You get a trust or some belief when you feel that your money is in LIC and it is being guaranteed that the money is safe through a know agent who will be your relative or some known person 4) As you rightly said there is no transparent(As far I have seen) option for a customer to invest in LIC without agent help. It there is pls tell a way 5)Even if he invest without a agents help does his premium gets less or does he have added advantage in his money invested( Which I am not sure of) .

Thanks.

Balaji Srinivasan

sir,

i am planing to take lic policy for 20 years,

the plan is: i need to pay 50,000 every year for 20 years.

and at the end of 20 th year,i will get 35 lakh amount.

what do you think…this is good plan??

can i invest in this plan?

and how to know the LIC agent i am taking policy is the genuine person,

because i am paying 50,000 for him in the beginning itself,before he giving me LIC policy

Pls give guidance

Jsavita-First let me know which LIC plan that offering you such high return? I think your agent misleading you. Check how he arrived at this maturity amount. Also, you are not giving the premium to an agent but to LIC. If you feel so unsecured then pay him by cheque but not through cash.

i m lic adviser my agency coad is 1855 880 6207 foart branch , laxmi building , p.m. shah marg, i m complited my 3 agency year i want see my every month commission up dates, plese help me .

thanking you,

yours fathfully,

vikas c sawant

adviser from l.i.c.

agency coad 1855 880 6207

Vikas-Usually your branch provide the earning reports. Check with them.

Dear sir, i have 3 policies from Reliance life ins. Company.

I am recuevung many call saying that on my policy there is an agent gide and all my comission is being taken by him self.

If i want to gwt that benwfit i will have to take a diiferent policy without any agent cide after that my all benefit will be rransfered on that account

Pl guide me is it true.

Vivek-It is illegal to expect agent’s commission.

Dear Mr.Tonagatti

Why it is illegal.I m a customer,I want to cancel my agent code so that i can get the benefits.Kindly advice.If you can share your contact no. also will be helpful for me.Treat its an urgent query.

Thx

Balvinder Singh

Hello Mr.Basu

thanks for enlightening new comers like me to this world of Commissions & LIC Investments. I have a 7-year old Jeevan Saral policy. (and another 2 years old same Jeevan Saral).

My question is how will i come to know the exact Corpus i should recieve at the time of withdrawal.

The premium paying term mentioned in my policy document is 35 years. Does this mean that policy maturity is at 35 years from the date of 1st premium?

Will i be able to withdraw the money at say, 15 years… how will i know the exact amount i should get at that time?

Unfortunately my LIC agent is extremely rude and unhelping nature. He clearly refuses to help me at times of need… (like when i wanted to apply for a loan against my policy). but i need this information so that i can plan somethinge for my future.

Jayashree-You will not get the exact maturity amount because it depends on a yearly declaration of LA (in your case). Yes, maturity will be after 35 years. Regarding this Jeevan Saral, you can read my earlier post “LIC’s Jeevan Saral-Why so much confusion?“.

Hi Basu,

Please clarify my following queries,

1] For an LIC agent, Minimum number of policies per year 12 and the policy amount should be more than or equal to 1lakh rupees. here, if any one condition met is enough or we should satisfy both the conditions every year?

2] If I am an LIC agent and I am opening the new policies only from my family members (My Children, Spouse ) every year to satisfy the above conditions, does it matter for LIC?

Thanks and Regards,

Hariharan

Hariharan-1) You have to satisfy both the conditions. 2) It does not matter to LIC. They just need new business, that’s it 🙂

Dear sir, I have gone through your chart of how much comission does your agent get from procurring various policy under different term range.I found misleading statement given in this chart that, 12 year term policy fetches 35% 1st year comission. This data is absolutely wrong, misleading data to your folloers.As far as I am convinced since the LIC’s plans launched since 1956, there is no such plans of 12yr policy which generate 35% 1st yr comission. If you have any circular/notification then post it to correct your previous post.I think there is no such plans or policy yet.Pl.don’t misguide to people by wrong information.

Omprakash-It includes the first year bonus commission also (usually 40% of first year premium). Please read the post fully.

DEAR SIR. THE ANSWER IS 100% WRONG.SINCE MY AGENCY IN LIC FROM LAST 17 YEARS I AM ASTONISHED TO HEAR 40% 1ST YEAR COMISSION INCLUDING 1ST YR COMISSION WHICH IS ABSOLUTELY MISGUIDING YOUR FOLLOWERS AND GEN. PUBLIC .SINCE 1956 TO 2015 NO PLANS OF LIC FETCHES SUCH % OF COMISSION.IF YOU HAVE ANY PLAN IN YOUR KNOWLEDGE PLEASE MENTION ITS NAME AND TA LE No. LAUNCHED EVER BY LIC. THANKS.

Omprakash-Sorry to say if not known the commission structure very well. In first year, for policies more than 12 yrs or so, the commission will be 25%+40% of the 25%. This means 35% first-year commission. Please check with your branch if I am wrong 🙂

Dear sir, No policy of 12 yr premium term of lic fetches 35% overall comission. Pl. Share any plan name or table no. Of lic plans that gives 40% total comission As you posted earlier. It is absolutely baseless and unauthenticated data you posted ealier.Only 15 yrs or more premium paying term fetches overall 35% comission including bonus comission that is also on selected endowmend plans not all. Pl. Check before posting any data..Thanks for reply.

Omprakash-Can you point a line where I said agents get 40% commission? This table is not my own creation, but based on recent changes of IRDA rules.

Let’s take an example of a 20 year policy for Rs. 2,00,000 Sum Assurance and the Maximum Commissions Payable there under:

For ease of calculations and understanding the premiums are rounded off which is about the average premium for insurable Ages

Annual premium – rs.10,000 First Year commission @ 35% =rs.3,500 2nd & 3rd Yr @7.5% ==Rs.1,500 4th 20th Yr @5%== 8,500 Total rs.13,500

On final analysis, the following findings emerge out

Sum assured – Rs.2,00,000 Maturity Value Rs.4,00,000 Policy Commission over 20 years Rs.13,500

Commission as a percentage of sum assured over 20 yrs 13500 / 200000 =6.75%

Commission as a percentage of maturity value over 20 yrs 13500 / 40000 = 3.375 %

Annual fee as a percentage of sum assured 6.75/20=0.33%

Annual fee as a percentage of maturity value 3.375/20=0.17%

Thus no greater than 0.17 % (which is the highest) is paid per annum to the Agent as a percentage of the amount he is responsible for. The Agent is paid higher commission in the first year in view of the fact that unless he chases a number of people, one policy can’t be sold. All of us should remember that “Insurance is a subject matter of solicitation”.

The above calculations are based on the Highest Commissions payable.

millions of pension policies are sold by agents with 2% commission (one time ) for which agents are serving the policy for life time of the customer

Yet another glaring example of Agents selfless contribution to this country is the success of Varista Pension Bima Yojna introduced by LIC of India for a limited period of 3 to 4 months in which the Senior Citizens were given a life long 9 % p.a. pension. Millions of Policies issued under this plan are still in force. The Life Insurance Agents have brought in more than Rs. 3000 Cr. Premium under plan . the commission payable under this plan was 0.1%(one time). Agents are serving their policy holders even today to the senior citizens .

Harsha-Great Findings…let me sell LIC Endowment Products agressively 🙂 But wrongly presented !!! When I invest (forget as Insurance, because here you are calculating returns and expenses) Rs.2,00,000 over 20 years then am I a fool to give around 6.75% as agents commission alone? Do you feel apart from that LIC not charge anything? In that case, even if we consider the LIC expenses at around 2% to 3% then what it assumes to be? Staggering 8% expenses on my invstments. Pension policies are sold at 2%, because it is one time investment. Hence, no social service attached to this selling.

For your information, Varishta Pension Bima Yojana was not launched by LIC, but Govt of India. Don’t attach the social service tag to your profession, when agents looking for commission structured selling. If they are so caring about society then let them sell term isnruance and cover the families at first.

Your assumptions are so wrong. Because you not calcuating the expenses on what you are investing and how much return you get back. Also, if LIC is so aggressively investing in equity and getting profit (again a scapegoat to Govt) then why not the return from endowment policies not even at 8%??

Hello,

I have completed 5 years as LIC Agent. my question is still i need to do the minimum 12 policy for my agencies continues.

pls suggest.

regards,

Sanket

Sanket-Yes..in my view it is mandatory. But for more clarity approach your branch manager or development officer.

how to become agent of more than one insurance company?

sir can you tell the eaxm pattern for preparation of lic agent how to become lic agent and what the topics to prepare what is the pass percentage to be get qualified lic agent license any spl coaching required and training institutions when will be the eaxm mode of eaxm if any links regrading the eaxm please share thank you for the time and consideration.

Ramesh-Please contact nearest LIC office. They guide you.

I recently received a call from some people from Mumbai stating that they are from insurance claim department of ICICI Prudential from a mobile number. They have taken my policy details and stated the amounts that agent is getting in terms of commission and bonus. They claimed that by following below two steps, commission and bonus of the policy will be returned to me:

1: Deactivate the agent code from the policy

2. Create a new customer id for myself and link it to the policy

and then claim the commission and bonus.

And also they mentioned only HDFC insurance and Bharati Axa has the right to create customer id in private sector insurance companies and to get customer id created I need to open one more policy in any one of these insurance companies.

Seeing all this I am thinking that this is a fraud call from some guys to make me open a new policy.

So can you please tell me, whether what these guys have stated is true or false??

Manohar-Looks like a spam call to me. Please avoid.

Yesterday I got the same kind of call from Mumbai.

Nice article sir. s there a method to pay policy premium without agent getting commission as he has not bothered to interact after the initial premium?

regards

Mohan-There is no such way as of now, where you can pay to direct and stop agent’s income. That is why it is a lucrative for few. That is the reason your agent not bothering about you. Because he know that whatever way you pay, the income will be in his pocket.

Dear Sir

Really it was a awesome piece from you, I have a doubt for long time

# if I took a policy from agent and start paying my second premium onwards through online mode do my agent get commission for that…

Muthukumar-Yes he will get it.

sir i received my first commision from lic but when next premium become due it is not paid by the policyholder and that’s y my commission is taken back. what should i do now ?

Chandni-Simple…force your policy holder to pay dues with penalty and from next time let him pay within due date. If possible track the dates and remind him.

sir i am new one to LIC agent since last 8 months, i done 6 policies only somebody told me minimum 12 policies must,and 1 lakh premium to collect in 1 year, and i am trying sale policies if it fails what happens.

and one more doubt can i become ‘appollo munich’ health insurance agent from IRDA same licence

Sriivas-Yes you need to complete the yearly minimum balance. If not completed and your agency not completed 5 years then in case of your agency lapse, you will not get any commission from whatever business you done. So you need to run the show to earn the existing policies income.

sir i am new one to LIC agent since last 8 months, i done 6 policies only somebody told me minimum 12 policies must,and 1 lakh premium to collect in 1 year, and i am trying sale policies if it fails what happens

Basu, Thanks very much for the article with so much insight. Also I admire your patient in responding to the critics with so much politeness. Please keep up the good work of spreading knowledge.

Arun-Thanks for your kind words Arun 🙂 Those who comment with so much anger also have some good qualities. So instead of concentrating on negative, better to concentrate on positive.

Can I work for more than one insurance company? if yes how?

Bhimashankar-No you can’t.

I, on behalf of Sjt.Jagannath Sharma, father of LIC’s authorised agent Bubul Sarmah who unfortunately expired on 06/09/2013 beg to inform you that agent Bubul Sarmah had made his business till his death since joining and enjoyed his regular commission against his business. But paying of the commission is stopped since expiry of Bubul Sarmah despite of the renewal premiums are being made by the policyholders regularly against their policies. On the otherhand, LIC authorities were kind enough to pay the GIS money.

Would you please let me know that whether late Sarmah’s father is entitled to get the benefit of the commission against the renewal premiums and other benefits as per rule.

With regards.

L.N.Bhattacharyya-Sir, first of all sorry about your son’s sudden demise. Let his soul rest in peace. Second thing, I am not aware about the rules. But why can’t you contact Branch Manager? They will definitely help you.

I want become a insurance agent, so can you suggest which insurance company pays a high commission and offers good facilities to their agents for short and long time…

Pushpa-In insurance industry there is nothing called high or low pay. Depending on the product you sell there is equal earning, irrespective of company. So you can opt company based on your comfort. But LIC have more faith among Indians, so you may feel more comfort in selling LIC products than private insurers.

Dear Sir

I have worked for three years as LIC agent. Presentaly I am not working. My License is valid up to May 2015. Will I be able to get commission for worked last three years?

Pawan-If you not do minimum business then in your case you loose commission. Because minimum 5 years of working as an agent will fetch your commission in future irrespective of whether you continue business or not.

Dear Sir,

please tell me a insurance agent receives commission only at the beginning or throughout the policy. if the policy is of 10 years. then life insurance agent receives commision only in 1 year or all the 10 years. please reply as soon as possible.

Shyam-At beginning it will be high like range from 35% to 10% and afterwards whenever policy holder pays the premium he receives commission till the policy maturity or death claim.

Basu your articles are very informative and help make right decisions, I was immediately able to calculate return on investment when an LIC agent came up with retirement plan, I invested in MF + PPF combination rather than LIC. agents for their livelihood resort to all kinds of lies they mention false returns which is worst part.( i am not trying to generalize but sharing my specific experience). I Strongly believe in today’s online age its not worth paying 35% commission just for filling up your forms and providing information

Raghunandan-Thanks for sharing your knowledge and experience.

In IT industry and many other organisation people are paid in lacs……do you think they are worth for it or does they do such unique jobs

for being paid heavily.

Lic has schemes and they have this commission structure. If you are convinced with the plan go for it.

Uma=It is headache of those who offer them such high salary and in return charge to their clients. Why I nee to bother? I am neither investor of that company nor buying any company from them. But while investing our money then we have right to do research what is EXPENSE involved. Your comparison is too rude.

dear all

while it is appreciated that we should know how much money/ or so called commission an agent is earning but at the same time , do we really understand what is meant by this .It is also very sad that some people here on this forum are trying to misguide about agent commssion . Let me try to explain .

each product and service has its cost and it includes basic cost + profit + commission etc .

each company or selller has its own way to sell or distribute products or services .

is it wrong to do this by agents . every one do that . just look around you.

your nearest shopkeeper . what is he . is he not a agent selling to grocery and taking some commssion .

you can take many example . It very funny to see commnents by some people that its thier money from which aggent commssion is paid . Of course it your money and commssion ia paid from it only.just think from where you want commission to be paid . tomorrow you would say , its our money from where LIC is getting profit and paying Bonus.

Tomorrow you would say its our money from where LIC is paying claims to some one . Yes its your money. No doubt about that . But than thats they way system works . ISt it.

let see how

1. when you buy a bottle of coke – do you ask shopkeeper how much commission he get by selling that poison bottle. even he tells you than what you would do . ask the shopkeeper its too much . than say its my money you are getting commission . or you would say i would buy this bottle directly from coke or pepsi.

you would take a taxi , and ask how much commsssion / profit taxi driver earns . its your money so what do you do . drive yourself or ask driver to sit on back seat and tell him take only petrol charges as i have driven . . ok if you can do that , do it . if you can not than simply pay the fare .

2. Its just ridiclous . what ever you call it , commssion or profit or incentive or whatever name you wish to give. all comes from your money only . wherether you like it or not but thats the way everything works .

3. as some one here righly says , why you worried about agents commssion . you are free to take policy from anyehere . check all the features and benefit and than buy .

4. yes there may be bad people / agent like you have many bad people in every indutsry .

5. but than so what .

6. you have a process to lodge compalaint and take action against bad people as in other trades .

7. but that does not mean you start potraying as if agent commsssion is something which is not known to person who is buy policy.

come on freidns , lets be mature enough and talk sensibly.

simply by saying i am neither against and nor in favour , does not solve the issue .

in today world, even a child knows that nothing comes for free.

For god sake even the news on TV is paid . so what do you do . do u really think , its not your money .

just be practical please.

however i really appreciate the good work of spreading finacial freedom /knowledge . keep it up .

but for god sake , kindly do not misguide people about agent commsison.

regards

arun aggarwal

Arun-Thanks for wonderful narration 🙂

1) Do you not do your homework while buying a TV or Fridge to your home by asking the cheapest shop? When I am investing Rs.100 then why not ask? Also if there is so much genuine in agency fraternity then why to shy away from declaring it? Being an investor I have every right to know where my Rs.100 invested will go.

2) That is a way things work and few agents do share. Why they share if they are so confident of their business ethics?

Do you know how much it is difficult to lodge compliant with any insurance company or with IRDA? Do you know how many companies treat you in same manner as they treat while buying?? Paid media? Do you know the quality of it? Also the faith once people understand about the paid media?

I am doing this only on investor point of view. Each individual have right to know about everything about expenses to investment. Because nothing is free in this world brother 🙂

Hi Basu…I have already paid 3 years full premiums (Quarterly 6125) + 1 extra premium (Thus a total of 79625 Rs) against my Jeevan Saral TP 165 Policy.

On 17-12-15 , I will be completing 5 Years though Policy Term I opted was 25 years.

I would like to know whether I will get this whole 79625 on 17-12-15 as I am not willing to pay any more Premiums on this Policy

Even I m ready to pay a minimum Premium , if I get the whole money back ( without any loyalty addition or bonus) on 17-12-2015

Pls advise what will be the best option If I want to get my entire money back , at least whatever I paid to LIC

Thanks in advance

Sijesh

Sijish-I can’t say how much you get. Contact LIC branch for the same.

I want to work for farmers… how can I help them as lic agent?

Pravin-Cover their life by proper INSURANCE based on their income range. But don’t try to sell any endowment plans.

Nice article! I also heard that :

– For the first premium, we have an option to ask the agent have to pay some % as premium on behalf of us.

– Also the first commission the agent gets, would be shared with the customer too.

Is that true? If yes, it is true for ALL types of insurance? I am looking at LIC Retire and Benefit Policy.

Uma-What you heard about sharing premium is illegal for agents as well as to you. But agents use to do this to garner business.

Sir one particular LIC agent has duped my father by citing false information about Jeevan Saral.My father should not have gone for the policy at 60 yrs at all.He made my dad invest in 2 policies for 10 years.Is there anything we can do to make the agent pay for his act?He has made me and my sisters invest in too many policies,can I do something to stop him from getting his commission atleast?

Ronita-First approach the concerned branch to which he belong. If still not work then go IRDA.

LIC is better than any other Private insurance but more products of Lic have on 10 year investment return is 3 to 4 % so this not a good for a investment purpose.

please kindly suggest.

Dear,

Pls understand what exactly insurance is. Never mix Insurance and Investment. Insurance plan will never give good returns cause they are not suppose to. On the other side any investment plan will not provide Insurance (Security).

The main purpose for Insurance is Security and secondary purpose is Returns. If you are a beginner in your career or you don”t have enough money to secure your Dependents life and you are having too much responsibility then insurance will provide you Good Security at low cost.

If you really want good returns then I will prefer Mutual Fund but as SIP, Stock Market, Physically Gold, FD, PPF etc etc etc. They are too many investment plans.

Basically I am an Engineer and also working as LIC Agent from last 3 years. I was interested in learning all the things related to Insurance. I have studied too many things and my first conclusion is “Investment is Investment, Insurance is Insurance”.

Regards: Devendra Jain

respected sir,

i have changed my profession from Chef to a financial planner, i am joined as a office assistant in a consultancy which provides financial planning to the clients, mainly our work is to deal with LIC policy and other investment plans like, PPF, NSC, etc etc..

sir i read your blog about LIC agents and other financial plans.

Sir my Question is, how i become a agent and and how to approach to customers to give various investment plans and give financial solutions to them??

Virendra-First select insurance company of which you want to become agent. Once that is done, then visit your nearest branch and they will guide you. Giving financial solutions to client need a learning from you. So start learning yourself and give advise to clients.

thanks for ur good advice

Sunita-Pleasure 🙂

What is this article about? Is it encouraging or discouraging savings?

When you buy a plan look for the need and benefit.Not the earning of the person who is giving service for it.He is paid for it.

Every product has its own advantage.just check if it fits into your needs.

Transparency and genuinity is needed. But there is some limit.If you go and shop for something ..say a Tv, do you look for features or what the manufacturer is getting profit?

Then why you expect life insurance for free of cost at your door step? Think it over…

Rajesh-Thanks for your views 🙂 Yes you are right, when we buy products then we need to look for a need and benefit. But when from such traditional plans neither our insurance need nor our financial goals will not be met because of lower return then can I still go ahead to have such products? Also it is my right as an investor to analyze why products are yielding high returns or low return. If in my Rs.100 investment, Rs.35 to Rs.40 will be eaten up by middlemen then is it frightening or not?

Dear when you go on a shop and you ask for some thing at that time you will never ask shopkeeper that how much he is earning on the product. You will select the required product. You will check whether it is upto your requirement and it is having all the things which you need. Then you will just buy the same.

Similarly look LIC in that point of view. Its a product if you need the same then just buy it. Check all the features and benefits. Dont look into profit of your agent.

Second thing, dont think that you are paying agent unnecessarily. He/She is the one who is guiding you in right direction. It is his/her responsibility to take care of all the issues related to the policy. You are planning a insurance for security of your family. In case if by chance any thing wrong goes with you. Then agent will take care of all the claim procedure and will work for you till the payment is released. That means your family members will not have to take efforts for the same. At that time they will not be in case to think for all this things.

So dont worry about agents income. Just think about your need, requirements and what all benefits you are getting from the plan. If you think that you are getting good benefit than just go ahead else drop your idea for insurance plan and go for other investment plan

Mr. Basu NIvesh

Thanks a lot for the article. It has come to me or Google led me here on a timely need when I have been fighting back to a strong advice of ‘ Invest before 31st else we loose money ” .

Your article here and the one on changes to policies has given me excellent ground to support my intentions.

For me ‘Form filling’ is important, I work in a hazardous work area, I notice few agents don’t care to fill these things up as it might increase premium up or require medicals,they do not seem to care the problem my family would face if the company

refuses claim on hidden facts.

Let me ask you a simple question, what is your take on multiple life insurance products.

i.,e if I have five life insurance policies of different companies( 3 from LIC, 1 from ICICI , 1 from Bajaj) , upon my death would my family get the Sum assured from each product?

mkj011urali-Thanks for your appreciation. There is no cause of concern having insurance policies with different insurer until and unless you declared all materiel cases exactly (for example in your case it is your work condition). So no need to bother.

Thanks for the information. I hope that LIC provides good plans from January taking into account customer benefits.

You had mentioned in above comments about online plans.

I would like to know the advantages of online plans ..may be NAV linked without any middlemen.

Dattatraya-Online plans for term plan (which are pure insurance product) are out of any middlemen. So the cost you pay to your agent will indirectly reducing. Hence they are cheap. Let us hope that LIC will come out with customer friendly plans rather than agents friendly.

Hi Basavaraj,

I’m also from Bangalore. I want to understand one thing. When I took policy (Non-single premium), that time agent was there..now I’m paying premiums through on-line, why does the agent get the commission still? Ideally I should be given waiver in my premiums. Does my point is valid?

Sudhakar-Your point is 200% valid. But sad to say that still the 50 years old rules are followed by regulators. So you don’t have any other choice but to follow. Let us see how they make it competitive. Do you know if any agent does business for 5 years with LIC and left that profession then still he will receive the commission till all plans closes which were done by him. He change the profession but income stream will continue 🙂

Dear,

You look like a nosy fellow who is trying to garner sone accredition by declaring things which need not be declared. It will be very hard to find things like what is the cut of dealer in brittania biscuit or owner of McDonalds franchisee because they have very less moles in their ranks unlike in this insurance and investment advisory field, where we have you.

I think it is downright stupid if not completely unethical to discuss a certain section of the society’s earnings with the others and whining over them getting benefits. If you have got the guts , just leave your qualification at home and get into the market. See how tough it is to sell insurance today. Try making a cold call or knocking on someone’s door to sell insurance and if you are not treated as vermin do let me know because I will need to shift in your locality then. Working as an agent today is one of the toughest means of livelihood. And here we have people like you uselessly commenting that they should not get money if someone’s paying a premium online. As cisf, I have every knowledge of how much you earn and HOW you are earning. So please try to mind your own biz and spend time guiding your clients through investment options rather than these stupid attention grabbing tricks like disclosing commissions etc.

Rakesh-Thanks for your wonderful comment 🙂 I have only two lines in reply to your lengthy comment.

1) When you are buying biscuit or pizza then you are not investing, instead you are buying a commodity. But in India insurance is sold as investment. So investors have every right to ask 100 questions.

2) Take hold your breath !!! I am LIC agent since 11 years and doing good by disclosing above facts 🙂

What is the change after 1 Jan 2014 in life insurance in terms of cover. I was told by an agent that insurance cover in case of death will be equal to the sum-assured (traditional plans) only, unlike 3-4 times of sum-assured offered currently. Is it true?

Raj-Please read my post “IRDA Life Insurance Regulations 2013-Do you know these changes?“

Thank You For Your Reply…

Would add Some Term Insurance with LIC in 2014 as , people said they would be cheaper.

But Plan like Jivan Anand and Jivan Saral Claiming 7% Return with Investment would be available in Jan 2014 or should invest some partial amount Now?

Thank You For Guidance.

Regards

Alap

Alap-No need to hurry. LIC will come up existing plans with new features. So better to wait.

Alap- I am an LIC insurance agent. New jeevan anand policy( Plan 815) is both a term insurance and endowment policy. It is also highest selling policy in LIC.

Sneha-Why to club both needs? Why can’t one opt them separately? What about returns? If this plan is LIC’s highest selling plan means one have to buy it blindly??

Hello Mr Basu..

Nice to Read your portal..Very Informative..

Mr Basu , I want to 50,000 Rs Annual Premium in LIC.

Is it right to invest Right Now or Should Wait for New Plan. I want to invest in Traditional Plans only for Return around 7%.

Please suggest plan I should invest if I should invest before 2014.

Regards

Alap Shah

Alap-Wait till Jan 2014. But think twice about your decision of satisfying yourself with 7% return and clubbing insurance with investment

JEEVAN ANAND – Instead of investing a lumpsum of 4lac for 18 yrs I am planning on investing 4 x 1lac for 16,17,18,19 yrs ..Is it advisable and any way beneficial??

Hemanth-It only beneficial in such a way that you receive the maturity on yearly base after 16,17,18 and 19 years onward. Apart from this I don’t think it is any beneficial for you.

Would there be any loss specifically if i do so in 1lac partitions sir??

Hemanth-No loss. But there is a slab for bonus declaration based on term of the policy. Like for example in case of Jeevan Anand, less than 11 years, 11 years to 15 years, 16 years to 20 years and more than 20 years. So as the term increases bonus increases accordingly. For better understanding of this feature you can refer “LIC’s Bonus rates for 2013-14 and Comparison“.

BasuNivesh Sir, Greetings

i just wanted to know if there will be any difference in the final bonuses which we receive along with the sum assured due to this commission thing for agents…bcoz agents quote the same premium amount as lic personnel do???

Hemanth-Bonus means what? It is the LIC profit from your investment amount which they distribute among policy holders. So ultimately when you invest Rs.100 then agent’s commission and other expenses will eat around Rs.40. Left out portion of Rs.60 will be invested and whatever they earn from this Rs.60 will be getting paid back to you as a bonus. Agents quote and LIC quote is same as both quotes include these expenses. Because LIC will pay to agent directly but not you.

Sir is the left out rs 60/- even if i directly walk into an LIC office and open it (no agent involved).

Hemanth-No you can’t do so. You have to buy insurance products from LIC through this mode only. No other options for you 🙂

Thank you so much sir!!!

But on LIC website we have option for opening it online..I tried it and a person from LIC contacted me and he says it is better to buy it from him than an LIC agent.. what exactly he means by that..

Hemanth-Whoever he may be, as of now except one and only online plan of LIC Jeevan Akshay VI (immediate pension plan), none of the plans are agent’s cost free. If you have doubt ask the same person what benefit of buying from him? Never ever be in trap of one time commission sharing by these agents. But look if any benefit throughout the period of plan like premium reduction if you buy from that guy.

Thank you so much for clarifying my queries sir!!! and most of all so promptly!!!

Hemanth-Pleasure 🙂

Hi Sir

Is there any idea whether premium rates will go up from 1st Jan 2014 for new Plans ? and at present (before 31/12/13) which plan can be taken for 15 year term with condition of high returns out of available LIC products ?

Thanks in Advance

Shivaraj

Shivaraj-All are expecting the decrease in premium as everyone is expecting that LIC will be adopting new mortality rate. High returns from LIC traditional plans? My simple answer is “STAY AWAY”.

What are Commissions for CHILD PLANS,PENSION PLAN,RETEIREMENT PLAN

Vyom-If child plans are endowment types then the commission will be equal to traditional plans. For retirement plans, it depends on the product to product.

Whenever you plan for life insurance, first thing you think is Financial Security to family, how particular policy cover the your family needs, Don’t think investment point of view or agent commission, agent’s will get commission (salary) for their service/work. If agent is getting more commission on particular policy, that means do you avoid those policy, it’s wrong perception.

Sridhar-Well said. But if agents commission and other expenses are bearing lot of weightage on one’s product then do you think it is worth to buy? When ULIPs were sold like hot cakes this what all neglected-cost of buying the product. You can’t ignore the cost involved in any product. Will you buy the same product which cost you for Rs.100 or for Rs.200 (wherein Rs.100 is middlemen’s expenses)? Obviously it is Rs.100. So we just can’t ignore and buy any product.

I have nothing to do with all this. I am neither an agent nor an investor. But, still couldn’t stop myself from commenting on this. What the hell are you doing here? You are just trying to become a hero. Nothing else. You said you have been an agent for long. If you think getting commission by selling insurance is not a good deed then why the hell are you doing the same thing? Do you work for free? Just because you have answer to every question asked doesn’t make you superior. You have no idea what kind of hard work those poor agents do in getting every single deal. At least, they are not committing any crime robbing others. Their commission is comparatively little higher because they don’t get salary. When you walk upto a private bank to open an account, the executive get commission too in the form salary+commission+promotion ( if his/her target is met).

Roy-I am neither fond of being HERO nor SUPERIOR. But when any investor invest in any product then he have right to know the expenses. That is what I said above. Nothing is free whether to those poor agents or you and me. So it is hard earned money of each individual who want to invest efficiently.

LIC Bakbash hai

Golu-LIC is not bad but some people made it like that. No product of this earth is bad until the buyer is understood it and buy if it actually suited to his/her need. What if someone is content with the kind of return of around 6-7% and always looking for security as his major concern? So no products are bad but choosing based on our need is the requirement.

I agree with you, Plans are based on need, requirement and financial conditions

Thirupathi-Thanks 🙂

I like and I want to become agent of lice

Akansha-Best of luck 🙂

Hi I need your feedback, we are investing in LIC for our kids education and we pay quarterly 15808/-as of now we have paid for 2 years and i think the returns what i get is less compare to the money i invest, can you suggest me some policies or funds which would give good returns at the time of their higher education . My kids are now in 8 and 5. I have taken this policy only out of force. My agent said i would get around 7.5Lakhs total…is it worth continuing this policy.

Vidya-When you are considering for your kid’s education in mind, you need to understand the inflation at which expenses of the current education system are rising. Suppose education inflation is around 7% and your return on investment is around 8% then the real return will be 1% only but not 8%. Hence considering the long term perspective of your kids education expenses (I consider as 18 years when you start to pay huge sum towards their education), I suggest you to first take a term insurance before going ahead for cancelling this LIC policy. Once it is issued then better to start investing in 25% Secured products and 75% equity investment. If you do so then you will be in a better position to beat the education inflation. If you still have doubt then let me know.

Very good.

Hello Mr basavaraj, basunivesh n Mr maxyork….

What’s wrong with u abt agents commission? And also customers, why so curiosity over ur agents commission?

Dear customers, wen u r planning to buy a product, know what premium u pay n what ll b ur sum assured and also c Wat ratio of amt u r earning at the time of maturity in ur policy plan so along with dis know to take bonuses in such policys so afterall every one knows abt death benefit also ——— now getting such a benefits ( 1 : 3 ratio of sum assured u r getting at da maturity time of ur plan ) den in which way u people r thinking dat he s cheating u ?

Cheating in da sense, when he s miss – selling d products

Dear customers, even i am also an agent in max life insurance company, but i like to share my commissions with my customers…… But also if i didn’t mention abt my commission means its not like I am cheating my customer ok!! but i know my job is a noble job cos i sell a correct product that which is suitable for their positions n conditions n also as per their requirements so 1 day it helps them in right conditions and in right time n dey remember me on dat day……

IRDA ( insurance regulatory and development authority ) made a commissions for a agents to cheat customers eh Mr. Basavaraj n ur supporters?

What I am telling s that the above debate discussions s not right as u people r talking with smiley’s….

So people tell me nw ——-))) who s agree with mee (1) or who is agree with basavaraj (2) once again? 1 or 2 ??