A few days back SBI launched the new senior citizen deposit scheme branding it as an SBI WeCare Deposit. Between SBI Wecare Deposit Vs Senior Citizens Savings Scheme (SCSS), which is the best one you can choose?

What are the features of the SBI WeCare Deposit Scheme for Senior Citizens?

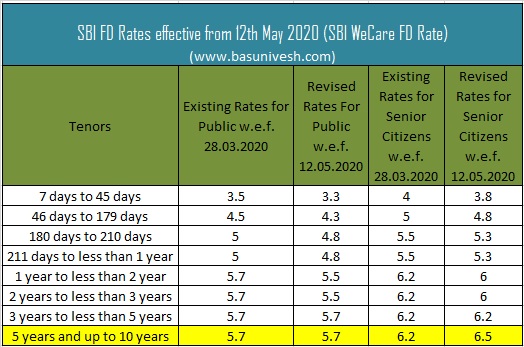

# This scheme is meant for Senior Citizens whose age is 60 years and above.

# Available for Resident Indians ONLY. This scheme is not meant for NRIs.

# You can open this deposit only for 5 years to 10 years term.

# It’s a special scheme launched to help seniors during the COVID-triggered interest rate reduction. Hence, this is a limited period scheme. The scheme is open between May 12, 2020, and September 30, 2020.

# The current interest rate for SBI WeCare is 0.80% higher than the normal FD rates. Usually, the interest rate difference between normal citizens to senior citizens is 0.50%. However, for this SBI WeCare Deposits (5 years and 10 years deposits), they are higher of 80 BPS. Hence, the current interest rate on SBI WeCare Deposit is 6.5%.

I have highligted in yellow with respect to the applicable interest rate on SBI WeCare Deposit.

# Premature withdrawal is allowed. However, the additional 0.30% benefit for 5 years and 10 years deposit will not be payable. Hence, if you tried to withdraw before maturity, then you will get the interest rate of 6.2%

# Interest payment is either monthly/quarterly or at maturity.

# There is no tax benefit under this scheme.

# TDS will be deducted on the interest payment if the total interest (from all FDs, RD, etc. but not savings account) paid in a financial year exceeds Rs 50,000.

# You can avail a loan on this Deposit.

SBI WeCare Deposit Vs Senior Citizens Savings Scheme (SCSS) – Which is the best?

Now let us understand the difference between SBI WeCare Deposit Vs Senior Citizens Savings Scheme (SCSS).

# The biggest difference is an interest payout. The current interest rate on the Senior Citizens Savings Scheme (SCSS) is at 7.4%. However, the SBI WeCare Deposit offers you at 6.5%. It is almost a 0.9% difference.

# SBI WeCare Deposit is available for up to Rs.2 Cr. However, the Senior Citizens Savings Scheme (SCSS) maximum limit is Rs.15 lakh ONLY.

# No Income Tax Benefit if you invest in SBI WeCare Deposit. However, the money you deposit in the Senior Citizens Savings Scheme (SCSS) is eligible for deduction under Sec.80C.

# Interest payment in SBI WeCare Deposit is on monthly/quarterly or at maturity. However, in the case of the Senior Citizens Savings Scheme (SCSS), it is on a quarterly basis.

# If you try to break the SBI WeCare Deposit before maturity, then you will end up earning the interest rate of 6.2%. However, in case of Senior Citizens Savings Scheme (SCSS), the account is closed after the expiry of 1 year but before the expiry of 2 years from the date of opening of the account, an amount 1.5% of the deposit shall be deducted and the balance paid to the depositor. In case the account is closed on or after the expiry of 2 years from the date of opening of the account, an amount equal to 1% of the deposit shall be deducted and balance paid to the depositor.

# Loan facility is available in the case of SBI WeCare. But you can’t avail the loan in case of Senior Citizens Savings Scheme (SCSS).

# In the case of SBI WeCare Deposit, the term available is 5 years to 10 years. However, in the case of SCSS, it is 5 years only. Also, in the case of SCSS, you are allowed to extend for one more time only once.

Refer the complete details about Senior Citizens Savings Scheme (SCSS) at our post “Post Office Senior Citizen Scheme (SCSS)-Benefits and Interest Rate“.

Conclusion:-Considering all the above features, I don’t think it is worth to invest in SBI WeCare FD. Instead, I feel the Senior Citizen Savings Scheme (SCSS) is far better.

Refer our latest posts:-

- EPF Scheme 2026: EPF, EPS and EDLI Rules Explained Fully

- Financial Freedom Without Health? You’ll Regret It Later

- The Peltzman Effect: Why Playing It Safe Can Make You Poor

- Your Retirement Success Depends on Luck, Not Skill

- Never Compare Nifty 50 Index Funds Vs Active Large Cap Funds!

- Nifty 500 Multicap 50:25:25 vs Nifty 500: Which Is Best?

My father had a SCSS in post office and he expired on 25-04-2021. I presented my death claim and got money on 19-06-2021. I ought to have got the money for this particular quarter at SCSS rate from 01-04-2021 to 19-06-2021. But when I calculated there was a shortfall of around Rs. 10K. My question is that the interest in SCSS will be calculated for senior citizen from 01-04-2021 to 25-04-2021 ( upto the date of death ) or upto 19-06-2021.

Further , my father and I had a joint fd deposit in SBI and my father ( senior citizen ) being the 1st holder. He expired on the above date and he was getting monthly interest and maturity was in 2025. I continued the fd just removing his name but actually new fd was of less amount. The principal amount got reduced . In other words, I have not closed but wanted to continue the same original terms. My question is that SBI is right for this blatant violation. Please reply at the earliest. What post office and RBI says about this.

Dear Vipin,

In case of SCSS, interest will be calculated up to the date of death of the holder. If you are a second holder of SBI FD, then you have all rights to continue.

In SCSS suppose claim was made after quarter then what will post office do.

As regards to SBI FD, I wanted to continue upto original maturity date ie 2025. But SBI issued new fd for one year tenure with rate of todays which is 5%. And that too after deducting interest on penalty. So my father original principal amount got reduced and created new fd. further, they have not given monthly interest which was due on 05-07-2021. I raised claim on 03-07-2021. I think I should file FIR for this day light legal robbery.

Dear Vipin,

They will deduct the extra paid interest and return you the principal. Creating new FD is fine but penalty is wrong with SBI FD.

Dear Sir,

Is it possible to open two accounts under the senior citizen savings scheme, for example, one in the post office 15 lac and one in the bank 15 lac?

Dear Manjunatha,

Sadly NO.

If total income from all sources including interest is less than 5 lacs, how can we get exemption from TDS?

Dear Ramachandra,

You have to submit Form 15G/H to avoid TDS.

What penalty will be charged if the Senior citizen expires before the tenure of SCSS ? Also, can the nominee continue the to stay invested in the scheme after the death of senior citizen ?

Dear Alok,

There is no penalty if death happens. The nominee will not be allowed to continue.

I agree

After investing in SCSS, what are the options for Sr Citizens for further investment. No to shares and MF

Dear Gupta,

You can explore the options like Tax Free Bonds or PMVVY (if Govt reopens the same).

SCSS ID CAPPED FOR 15 LAKH FOR MANY YEARS SND CENTRAL GOVT HAS NO INTENTION TO INCREASE IT WHENCE PRESENT SITUATION DEMANDS AN INCREASE OT TO 30 LAKH.

BUT, ALAS !!

SENIOR CITIZENS ARE NOT AN ORGANISED COMMUNITY AND ALWAYS AT THE MERCY OF GOVT.

LET US UNITE AND DEMAND THE CAP FOR 30 LAKH WITH TAXFREE INTEREST !!

HON’BLE MADAM FM, ARE YOU LISTENING !!?!

Dear Mitra,

True and all your views are genuine.