Many of us investing in NPS (National Pension Scheme). But have you ever checked NPS Returns for 2019? Whether you analyzed who is the best NPS Fund Manager for 2019 or which is the best NPS Scheme for 2019?

Note:-I have written a post with respect to NPS Returns 2020. Refer the same at “NPS Returns for 2020 – Who is best NPS Fund Manager?

NPS now slowly turning to be one of the major investment choices for many of us. It may be due to default option provided to Government employees, tax benefits at the time of investment or to create a retirement corpus.

What is Scheme Preference in NPS Account

In NPS, there are two types of options available to create your portfolio. They are as below. Remember this scheme preference is not available for Government Employees Tier 1 Account Type. However, they have the freedom to choose scheme preference in their Tier 2 account. For rest of all investors, you have an option to choose scheme preference.

# Active choice – You will decide on the asset classes in which the contributed funds are to be invested and their percentages (Asset class E-Maximum of 50%, Asset Class C, and Asset Class G ).

# Auto choice – Lifecycle Fund– This is the default option under NPS and wherein the management of investment of funds is done automatically based on the age profile of the subscriber. At the age of 18 years, the auto choice will invest 50% of pension wealth in E Class, 30% in C Class and 20% in G-Class. These ratios of investment will remain fixed for all contributions until the participant reaches the age of 36 yrs. From age 36 yrs onwards, the weight in E and C asset class will decrease annually and the weight in G class will increase annually till it reaches 10% in E, 10% in C and 80% in G class at age 55 yrs.

At the age of 18 years, the auto choice will invest 50% of pension wealth in E Class, 30% in C Class and 20% in G-Class. These ratios of investment will remain fixed for all contributions until the participant reaches the age of 36 yrs. From age 36 yrs onwards, the weight in E and C asset class will decrease annually and the weight in G class will increase annually till it reaches 10% in E, 10% in C and 80% in G class at age 55 yrs.

Such changes will be done on the birth date of the subscriber. Such changes can be done once in a financial year.

What are the types of funds available in NPS?

There are three types of NPS funds available. They are as below.

- Asset Class E : Invest in equity market instruments. This is the riskier asset class among all three.

- Asset Class G : Invest in fixed income instruments. The best example of this is the central government bond. This is secured among all three.

- Asset Class C : Invest in fixed income instruments. Examples of these are bonds issued by firms or companies. this neither risky like Asset Class E nor safe like Asset Class G.

Recently a new fund category by name Alternate investment has been introduced.

List of NPS Fund Managers

Currently, there are 8 Fund Managers who are managing our NPS corpus and they are as below.

- Birla Sun Life Pension Scheme

- HDFC Pension Fund

- ICICI Prudential Pension Fund

- Kotak Pension Fund

- LIC Pension Fund

- Reliance Capital Pension Fund

- SBI Pension Fund

- UTI Retirement Solutions

The Government employees NPS accounts and contributions are managed by LIC Pension Fund, SBI Pension Fund and UTI.

Under this category, up to 15% of the corpus can only be invested in Equity Fund. The remaining corpus is allocated to Corporate Bonds and Govt securities.

The private sector employees and other individuals can also invest in NPS. The Equity fund threshold limit is 75% in this case. These individuals can select any of the two investment options to select scheme preferences.

NPS Tax Benefits 2019

Many of us invest in NPS mainly because of tax saving options. But sadly many fail to understand the different sections one can avail by investing in NPS.

I am explaining the same from the below image.

I have written a detailed post on this. You can refer the same at “NPS Tax Benefits 2019 – Sec.80CCD(1), 80CCD(2) and 80CCD(1B)“.

NPS Returns for 2019 – Who is best NPS Fund Manager?

Now let us concentrate on NPS Returns for 2019 and try to find who is the best NPS Fund Manager for 2019 or which is the best NPS fund for 2019.

NPS Returns for 2019- Best NPS Fund under Central Government Scheme

As I said above, this scheme is meant for Central Government Employees only. Here, we can find only three fund managers and the returns are as below.

# Fund Managers managing the scheme since 1st April 2008.

# SBI Manages the highest AUM (38,804.26 Cr) followed by UTI (36,894.41 Cr) and LIC (34,357.17 Cr).

# When you compare 10 years returns, SBI tops with almost 10% returns (9.86%) and then LIC and UTI almost generated around 9.5% returns.

#All Fund Managers debt portfolio hold Govt Bonds which maturing from 2030 to around 2045. Hence, any interest rate fluctuation will impact the return badly. Because of longer the maturity period higher the interest rate impact on bond.

# Top 3 holdings of SBI Fund Manager is G-Sec, Banking and Financial Institutions. LIC Fund Manager holding is Govt. Sec, Finance, Banks. However, with UTI, it is Banks, Other credit granting, Housing credit Institutions.

# Benchmark return for 5 years is 10.05%, 3 years is 8.27%, 2 years is 6.65% and for 1 year it is 9.07%. Hence, all three fund managers have beaten the benchmark consistently for 5 years.

NPS Returns for 2019- Best NPS Fund under State Government Scheme

Now let us go with NPS Returns for 2019 under State Government Scheme. Here also you will find 3 fund managers like central government NPS. Let us see the performance.

# Fund Managers managing the scheme since 25th June 2009.

# SBI Manages the highest AUM (54,585.94 Cr) followed by UTI (53,521.21 Cr) and LIC (52,644.86 Cr).

# When you compare 9 years returns, LIC tops with 9.56% returns and then UTI (9.5%) and SBI (9.46%).

#All Fund Managers debt portfolio hold Govt Bonds which maturing from 2030 (UTI holding bond maturing in the year of 2029) to around 2045. Hence, any interest rate fluctuation will impact the return badly. Because of longer the maturity period higher the interest rate impact on bond.

# Top 3 holdings of SBI Fund Manager is G-Sec, Banking, and Financial Institutions. LIC Fund Manager holding is Govt. Sec, Finance, and Banks. However, with UTI, it is Banks, Other credit granting, Housing credit Institutions.

# Benchmark return for 5 years is 10.05%, 3 years is 8.27%, 2 years is 6.65% and for 1 year it is 9.07%. Hence, all three fund managers have beaten the benchmark consistently for 5 years.

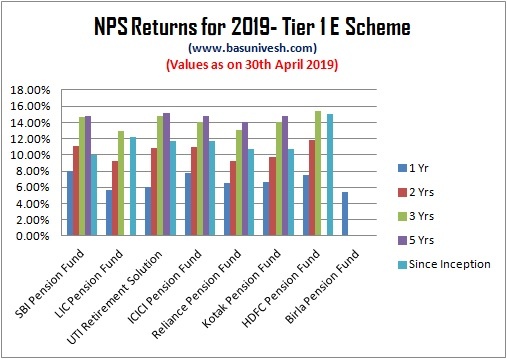

NPS Returns for 2019 – Best Performing NPS Tier 1 – Scheme E Fund Returns

Now let us concentrate on NPS Returns for 2019 in Tier 1 Scheme E. The returns are as below.

# The best performing NPS Pension Fund manager under NPS Tier-1 Scheme E is HDFC PF. This scheme has generated returns of around 13.22% in the last 5 years. Also, since inception, it is 15.02%.

# Also, weightage of top 5 holdings is less in case of UTI. It constitutes 27.52% of the overall portfolio.

# Last year Kotak Fund was holding Mutual Funds like Birla Sunlife Top 100, Birla Sunlife Frontline Equity and SBI Magnum Multiplier. Seems strange to me as how they managing the expenses. Because there will be double expenses like Kotak expenses and also the Mutual Fund Expenses. But this time, I think they reduced their exposure or not holding. Hence, I have not seen this in the NPS report.

# The clear winner in this category is HDFC followed by UTI.

NPS Returns for 2019 – Best Performing NPS Tier 1 – Scheme C (Corporate) Fund Returns

Now let us concentrate on NPS Returns for 2019 in Tier 1 Scheme C. The returns are as below.

# The best performing NPS Pension Fund manager under NPS Tier-1 Scheme C is ICICI. This scheme has generated returns of around 10.10% in the last 5 years. Also, since inception, it is 10.33%.

# SBI’s AUM is highest here with around 1,572.49 Cr followed by HDFC (1,232.35 Cr) and ICICI (834.05 Cr).

# The clear winner in this category is ICICI followed by SBI.

NPS Returns for 2019 – Best Performing NPS Tier 1 – Scheme G (Govt Securities) Fund Returns

Now let us look for NPS Returns for 2019 in NPS Tier 1 and Scheme G (Govt Securities).

# In this category, the higher and consistent performer is LIC.

# Have you noticed the higher returns of all these funds for a year? The reason for underperformance by all these funds is that easing interest rate since a year or so. Due to this, the fund performance increased drastically. Because these funds holding longer maturity Government bonds which are prone to interest rate movement.

NPS Returns for 2019 – Best Performing NPS Tier 2 – Scheme E Fund Returns

Let us now move to Tier 2 performance of NPS Returns 2019.

# The best performing NPS Pension Fund manager under NPS Tier-1 Scheme E is SBI. This scheme has generated returns of around 12.81% in the last 5 years. Also, since inception, it is 9.7%%.

# The clear winner in this category is SBI followed by UTI.

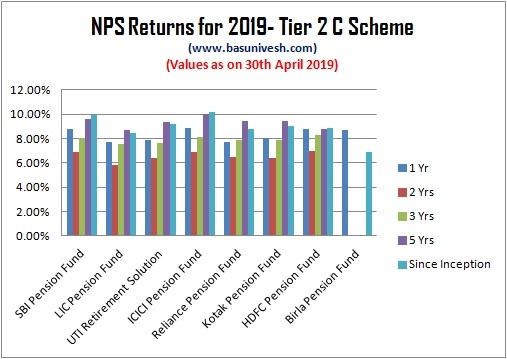

NPS Returns for 2019 – Best Performing NPS Tier 2 – Scheme C (Corporate) Fund Returns

Now let us concentrate on NPS Returns for 2019 in Tier 2 Scheme C. The returns are as below.

# In this Scheme the winner is ICICI pension fund with 5 years return 9.98% and followed by Reliance Pension Fund.

# The highest AUM is managed by SBI Pension Fund and followed by ICICI Pension Fund.

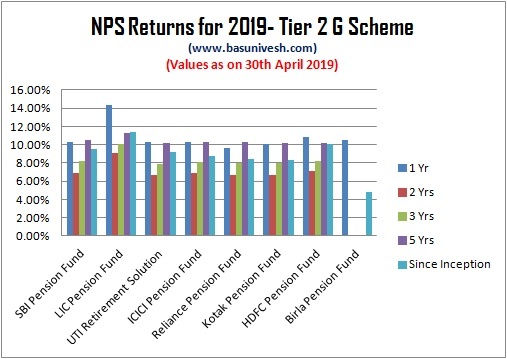

NPS Returns for 2019 – Best Performing NPS Tier 2 – Scheme G (Govt Securities) Fund Returns

Let us not check the NPS Returns for 2019 for Tier 2-Scheme G (Government Securities).

# In this category the winner is LIC.

Who is the best NPS Fund Manager for 2019?

In the above charts we the NPS Returns for 2019. Now based on those performance returns, who is the best NPS Fund Manager? To identify the best NPS fund manager, I considered the last 5 years returns of each scheme.

In the below chart, I show you the highest return generated fund manager for each asset class for a different time period of 1 year, 3 years and 5 Yrs returns. The data looks like below.

Hope this much information is enough for you to judge how your NPS is performing. Do remember that NPS comes with lock-in, annuity you buy will be taxable and you have to stick to limited fund managers. Never invest in NPS with the sole intention of tax saving.

Refer our other posts related to NPS:-

- NPS Tax Benefits 2019 – Sec.80CCD(1), 80CCD(2) and 80CCD(1B)

- Latest NPS Withdrawal Rules 2018

- National Pension Scheme (NPS) – 5 Biggest Disadvantages

I am a state govt employee and I have GPF. I also have PPF account. My age is 30. Now I want to open an NPS account contributing 5000/- per month only for investment purpose not for tax saving. Which is the best pension fund Lic or Sbi? Will I get profitable return from NPS after retirement?

Dear Anita,

You can choose any one as both are equally good. Regarding the return, it is a market-linked product. Hence, no one can give you a guarantee.

Hi

I have selected ICICI Prudential Pension fund and Asset allocations in Tier-1 are scheme-E-46.52%, Scheme-E-17.16, and Scheme-G-36.32%. And i am depositing 4000 Per month in the same. Is this the right allocation & will this fund give me at least 10% return after 20 years.

Dear Dinesh,

Expect 10% from equity and from debt around 6% to 7%.

Hi Basu,

I have been investing in nps for last 3 years with HDFC as pfm and ECG as 50,25,25%.

Given the current market scenario, is it good to change the PFM and scheme to ECG as 75,10,15%?

Dear Deepak,

Refer my latest post (link shared in the post at the beginning itself).

Hi Basu I just open nps account my age is 44 I M working in private sector. please suggest me which fund manager i have to choose and % of E C and G .

Dear Manoj,

Wait for my next article.

Dear sir I’m 23 year old my salary is 33000 per month and I’m considering to invest 5000 per month in NPS scheme but I don’t which fund manager to choose..can you please guide me through I was considering to choose auto-moderate since I’m not knowledgeable enough to manage it myself..

Dear Soumya,

If you are investing just because of tax saving, then stay away.

Hello Mr. Vasavraj,

I would need guidance on financial planning for my family. My age is 37yrs+. Here are the plans..

1.PPF-5000/- per month. Already running.

2. NPS-5000/- per month. Already running. But hardly made 4 times contribution in last 2 years . Now want to contribute every month.

3. LIC for 5 yrs Daughter and 4 Months Son …Total 5k per month. Already running.

4.LIC for wife(Pension scheme)… 5k/month …yet to start.

5.Sukanya Account for Daughter… 5k/month. Already running.

6. Mutual Fund… Want to invest in mutual fund 5k/month. But need guidance. Can I start directly without any portfolio manager to save money.

Actually I need guidance on NPS and Mutual fund, what amount should I invest every month keeping liquidity option in mind. Also which stock/share to invest in and percentage of contribution in different asset class.

I work in a private organization.

Regards

Dear Sujan,

The whole financial planning for your life can’t be done with a mere few lines of sharing. It is more harmful to you than me.

Hi Sir, I works for a private company, I have invested LIC pension fund scheme E, C, G @ 71%,11% and 18% and regularly investing since 2018 in tier-1, but noticed now that I hardly gained any profit in last 2 years, Should I change my fund and if yes to which is the best PFM?

Please guide.

Regards

Vivek Jain

Dear Vivek,

Please stick to it.

Hi Basavaraj,

Kudos for the very informative article. I am an NRI and want to invest in an instrument where i do not have to check every now and then. I am looking for long term investment for various reasons.

1. I want my money to help Indian Market grow

2. I need better returns then western markets, which are restricted to single digit growth.

NPS was one of the many options, but as i read i think you do not recommend NPS for investing. I am not worried about tax saving at this time. What should be a good instrument to invest in long term which offer decent ROI.

Thanks , looking forward for your opinion.

Dear Manu,

There is no such product where you no need to check and open eyes only when you need it. Continues (at least once in a year) monitoring is must to protect your money.

Dear Basavaraj,

I was just reading various conversations between you and NPS Interesting contributors.

And observed that you do not like NPS and suggesting investor to stay away from NPS. Specially if objective is for tax saving only.

Why so ? do you recommend any other instrument. pls. explain reason…

What is harm if investor want to save tax and at the same time, accumulating retirement corpus…. We know that this is non-liquid instrument but non liquidity will be benefiting us only at old age.

Dear Gurpreet,

TAX SAVING MUST NOT BE YOUR SOLE IDEA OF INVESTING. Also, due to change in tax regime, if you think NPS is a great product, then cross check.

My name is Hemant and I am a central government employee. I am considering investing in NPS Tier 2 with 3 year lock in. As Finance Minister announced NPS Tier 2 Tax Benefits for the central government employee. Is it the right thing to do considering Stock Market is over valued as of now?

Dear Hemant,

Refer my last post “NPS Tax Benefits 2020 – Sec.80CCD(1), 80CCD(2) and 80CCD(1B)“.

Sir,

I’m a central government employee.. me and c govt contribute 10000+ in NPS tier 1.. right now on default scheme… Could you suggest me the best fund manager and the best scheme for me…. Thanks in advance..

My age is 28.

Dear Rajesh,

Stick to default.

Hi Basu,

Thanks for the informative post.

In most of the replies, you have been suggesting to stay away from NPS in a long term perspective as the prospects don’t seem bright given the current info.

Would you mind helping me understand why it can’t serve the purpose?

Also, can you kindly suggest some good investment options to beat the inflation.

PS: My age is 34 and I fall in the 30% bracket.

Dear Guru,

Refer my post “National Pension Scheme (NPS) – 5 Biggest Disadvantages“. Good investment option depends on many considerations. It is hard for me to say BLINDLY.

Dear Sir,

I have invested 100000 in NPS tair 1 from last 2 years.

Currently the distribution structure is SBI Pension fund scheme

1. 50 % in scheme E

2. 20% in scheme G

3. 30% in scheme C

Could you please suggest if I can change my scheme and it’s percentage so that I can get best return

Thanks

Giri

My age is 40 years. Could you please suggest

Dear Giri,

If possible inter change the % between C and G.

i am about to invest in NPS. I will opt for Auto choice with weightage 50- E , 30 – Cand 20 – G .

Please could you suggest what scheme/fund manager to select for this option

As a long term outlook, should i look what total corpus has any fund management company accumulated like SBI and HDFC

or going through return since inception would really be other factor which we should look for long term returns Ex. ICICI , SBI or HDFC

Dear Raj,

What prompted you to select this product?

Hi Basavaraj,

I was looking for a long term retirement investment. It attracted my attention somewhat and looks like some ELSS scheme with additional tax benefits as of today.

And also the current trend of absolute return i see in such tax saving instrument is also what attracted towards NPS

Dear Raj,

Never invest in an instrument just because there are tax benefits.

Hi Basu,

I took your recommendation from other replies that not to invest just because of tax benefits.

I am thinking to invest for long term in this instrument.

Can you please advise to my original question if total corpus managed by fund management company matters when it comes to giving return is long term

I see SBI, HDFC and ICICI some potential to start my investment with. What will you suggest ?

Dear Raj,

Now you have decided that you are not going to invest for the sake of tax saving, then why to invest in such a huge ILLIQUID product?

Hi Basu, I wont say it is highly illiquid. I still have way to premature exit in 3 years if i want. I still know the fact i can only get 20% of the amount on maturity and 80% will still be allocated to annutiy plan which i can clear off in 5 years ( minimum ) plan if i want.

But thats not the idea i am even thinking off. In any case if i am thining 15 years down the line, is there any product as compared to NPS that can offer as good return as NPS ?

P.S i already have investments in mutual funds with such long term goals and high anticipated returns

Dear Raj,

Betting either on NPR or on any other product depends on your gut feeling. I will not suggest any product which LOCKS my money. Also, your performance with NPS is like marriage between you and fund manager where there is no freedom.

Thanks a lot Basu. This explains a lot 🙂

Hello Sir,

I am 27 years old and work in private sector. I want to start NPS account of Tier-1.

I am thinking to opt for SBI pension fund for this. Can you tell if this is the best fund manager for highest returns. Also how should I distribute the percentage among E,G and C

Dear Kanchan,

May I know why you wish to invest in NPS?

Hi Sir, I also have the same question as Kanchan. I want to invest 5k per month and I can’t risk high. But can take a medium risk as I have other family commitments and solo earning person of the family. From the above post, I understood that NPS can give 9-10% returns in long term investment along with tax benefit. Right now I don’t have any tax benefit from my side. That’s the reason I want to invest in NPS. So, can you suggest me whether I need to invest or not? Right now I am investing 2k per month in mutual funds and will continue that although it is in a loss for now(Started one year ago). This 5k is additional to that 2k. Will be waiting for your reply.

Dear Kumar,

How you arrived at the conclusion that NPS will not take high risk?

Sir please suggest how to move from Karvy to others such as NSDL.

Also i am not happy with HDFC Pension Fund please suggest how to move to SBI/etc..

Dear Vineet,

What is an issue with Karvy? Regarding fund managers, you can change it.

Hi,

I am a software professional, I am looking for NPS option under 80CCD, for additional 50 thousand rupees over 80c section.

Please suggest the best fund manager and options to be opted.

Thank you.

Dear Guruhema,

Never invest in a product just because of tax saving.

Hi Basu,

Could you please suggest, if i want to activate tier ii , which is the best fund manager for tier two, and in which category i have to contribute the % as i did for tier 1. Please suggest

for tier 1 i have selected sbi pension fund with % 50, 30, 20 in E, G, C respectively. is it the best fund manager or i can select diff one which returns more interest for tier 1.

Thanks

Dear Aurobindo,

Refer the Tier 2 performer list and accordingly you can select.

Dear Sir,

I have invested 98000 in NPS time 1.

Currently the distribution structure is SBI Pension fund scheme

1. 50 % in scheme E

2. 20% in scheme G

3. 30% in scheme C

Could you please suggest if I can change my scheme and it’s percentage so that I can get best return

Thanks

Aurobindo Nayak

My age is 35 years. Could you please suggest

Dear Aurobindo,

Enough. Instead, I suggest you 30% in G and 20% in C.

Thanks for replying.

you mean, I will keep 50% as it is and change 30% to G and 20% to C.

Normally how many years I have to invest this, and what is the rate of interest I will get finally.

diff % form diff schemes like E, G, C or a single % I will get..

could you please suggest, please let me know the exact figure

Dear Aurobindo,

you mean, I will keep 50% as it is and change 30% to G and 20% to C.-YES.

How many years I have to invest?-It is a Retirement product and hence you have to invest for your retirement. It is a market linked product and hence no such kind of interest (like bank FDs).

Thanks for your suggestion. based on your previous estimation, normally what will be the interest rate as we are getting 7% as FD in SBI like what will be the rate amount in NPS SBI pension found

Dear Aurobindo,

NPS will not provide you interest. Because it is a market linked product.

Hi Basu,

I have opened my NPS amount with Karvy, what is the difference between owing an NPS amount through Karvy or NSDL?

Just heard about the issue with Karvy fintech and was a little worried.

Regards

Sandip

Dear Sandip,

Karvy just act like a facilitator. You no need to worry as your money is with fund managers but not with Karvy.

I am a self-employed person and 36 years old. I want to invest in NPS for retirement corpus. Which NPS should I choose?

Dear Amit,

Stay away.

Then according to u , why should 1 invest in NPS .

Dear Sachet,

I never said you to invest in NPS.

pl suggest the best NPS for a retired employee like me who has never invested in NPS schemes.

Dear Kamalkar,

For retired employee, NPS is not suitable. NPS is a product to accumulate retirement corpus.

As per valueresearchonline.com research report HDFC Pension Fund is topper in NPS Tier-1 and Tier-2 both. Your report differs whereas your graph shows HDFC is topper. Why this disparity in reseach reports of valueresearchonline and basunivesh, which is correct?

Dear Tapas,

Check the date I have written to the date you have checked.

Whether we can exit before 60 year of age and opt all amount to buy annuity, suppose i am 36 year and want to invest till 55 and opt out at 60, will i get all tax benefits in that case?

Dear Kush,

Are you investing for tax saving purpose?

Dear sir,

I am a Bank employee. N NPS us mandatory. My contribution to NPS including employers is 15000 per month. Should I opt for Active Choice? If yes, what should be my allocation in E G and C and in which funds? My age is 31.

Dear Aniket,

Choosing which option best suitable to you depends on your requirement. It is hard for me to suggest BLINDLY.

Sir,

Can NPS be considered as a good scheme for private sector employees ? As we mainly think for tax relaxation over it and neither for the long term investment of our fund nor the maturity part.

Dear Chirag,

Better to stay away and never invest or choose any product just for tax saving purpose.

Some portion of fund should be provided to the employee so that they can directly buy equity and generate higher return

Dear Hemant,

How many of NPS contributors aware about equity volatility? Majority of NPS investors are tax savers.

Yes sir I believe NPS is best product when you plan this along with rest like equity ppf VPF EPF and fixed deposit.

Dear Ram,

Let me know in what sense it is the BEST?

If we consider the tax benefit(both 80CCD(2) and 1(B) and we are in 30% tax slab then straight away we are getting 30% return which would have in the tax, apart from this the average return on NPS is ~10% which is very good compared to other investment option.

Additionally at the time of retirement 60% of the corpse is tax free and remaining 40% will be used to buy annuity which will provide regular income in the old age.

Considering all these points I think this is one of the best product for retirement planning.

As always advisable never keep all the eggs in one basket so individual should invest in other available avenues like mutual funds, PPF, FDs, GSB etc.

Dear Abhishek,

If taxation is a major reason for investing in NPS and you are comfortable with product feature, then please go ahead.

Hi Basu, Thanks for your reply.

Its not just taxation but other aspects as well like return, safety etc. for someone in 30% tax bracket , when he/she gets an opportunity to save over and above 80C then it becomes attractive as just by investing in this product he/she is getting 30% return straight away which he would have paid in taxes.

I am interested to know and appreciate if you can write some blog and provide the unique insight that why people who fall in 30% tax brackets should not invest in NPS and what are other comparable investment options on the parameters of taxation(EEE), safety, return etc.

Dear Abhishek,

NPS gives you SAFETY? Check your facts. Forget about their equity part, check how volatile the debt part of NPS due to their holding in long term bonds. You are concentrating on TAX and IMMEDIATE tax saving. However, I am concerned with other aspects more. I have written an article about the disadvantages of NPS. You can refer the same. National Pension Scheme (NPS) – 5 Biggest Disadvantages

Respected sir,

I am a central government employee and am eligible for the old pension scheme. I have taken tax benefits up to 1.5 lakh under 80C through my GPF. Am I eligible for additional tax benefit under 80CCD(1B) by investing Rs 50000 in NPS tier2 ?

Kindly guide me.

Dear Ravindra,

Refer the latest post “NPS Returns for 2020 – Who is best NPS Fund Manager?“.

sir could you suggest which fund manager is good for T2. i set E-50%, C-30% and G-20% when it comes to T1 i set opposite where G-50%,C 30% and E20%. currently im using LIC as T1 fund manager where as choosen kotak as T2 manager. since my exposure to G is more in T1 want to stick with LIC but thinking to change my T2 fund manager to SBI/HDFC. your suggestion please. my plan is invest 50,000 in T1 and 1 lakh in T2 would like to continue for long term retirement.no plans of withdrawing money from T1/T2 till retirment as i already planned for emergency fund of 20lakh in bank deposit

Dear Ram,

I have already shared who is best. It is you who has to take a call. Do you feel NPS is a right product?

Sir, I have some savings in LIC T2 Govt bonds(72%) and in T2 Corp bonds (28%). Considering interest rate cur is ahead, is it the time to rebalance or suggest where to invest this savings. Last 1 year, I got 15% returns from nos t2 account

Dear Murali,

Sadly their debt part holding long term bonds which are highly sensitive to interest rate movements.

Great post. Is it not equity share now increased to 75% under active choice recently?

Dear Nanda,

Yes, it is increased in the latest updates.

sir, can you throw a light on nps corporate scheme for bank employees

Dear Dheeraj,

It comes under Tier 1 Scheme

Hi Sir,

I have all my investments through 80 ccd(1b) and 80ccd(2) In UTI Retirement Solutions (75 % E, 10% C, 15% G)… A corpus of around 1.7 Lacs. I am 27 years old and have done investment since March 2019.

Please suggest if I should change the scheme fund manager or the percentage of contributions in three schemes.

Dear Akshay,

Let it be like that.