Government of India is offering the longest bond of 50 years “New Government Security 2073”. This Government of India Bond 2073 is available at a 7.52% yield. Who can invest?

The bond details as per RBI Retail Direct are as below.

Security Name – NI GOVT. STOCK 2073

Maturity Date – 6th November 2073

Indicative Yield (as of 1st October 2023) – 7.52%

ISIN Number – IN0020230127

You can buy this bond in RBI Retail Direct Platform without any cost involved. (“RBI Retail Direct – Invest In Government Bonds Online).

As of now, the longest bond offering by the Government Of India is 40 years. First-time government is offering a 50-year maturing bond. Two more auctions of 50-year tenure bonds will also be announced at later dates for the second half of FY2024.

New Government Of India Bond 2073 – Who can invest?

Just because it is offered by the Government Of India and default or downgrade risk is almost NIL does not mean it is SAFE. You can avoid the default or credit downgrade risk as it is issued by the Government. However, you can’t run away from interest rate risk.

Hence, let us try to understand the pros and cons of investing in the New Government Of India 2073 Bond.

# Interest or Coupon Income

Interest will be payable on half yearly basis. It is not like your Bank FD where you accrue the accumulated interest and get back maturity. Hence, if you are in need of such frequent income, then you can opt for it. If you are in the accumulation phase of your life and trying this bond just for diversification or as a debt part, then it is of no use for you.

Many may argue that they can reinvest the same. However, note that this interest income is taxable for you. Hence, post-tax you have to invest, and reinvestment risk is always on your head. When you buy a debt mutual fund, the fund manager also receives the coupon. However, he reinvests which will not alter your taxation. But if you wish to do the same, then you have to pay the tax and then reinvest.

# Taxation

As I mentioned above, the interest or coupon you receive is taxable as per your taxable. Hence, look at post-tax returns than the pre-tax returns.

Along with this, if you sell the bonds in the secondary market before maturity, then you have to pay the tax on capital gains.

If you sell bonds within a year of purchasing them, the gains will be treated as short-term capital gains and will be taxed at your income tax slab rate. However, if you sell your bonds after a year of holding them, the gains will be treated as long-term capital gains and will be taxed at a lower rate of 10% (without indexation benefit).

# Interest Rate Risk

I wrote a detailed post on this “Part 3 – Debt Mutual Funds Basics” or I pasted the same here for your reference.

Assume that Mr.A is holding a 10-year bond that offers him 8% interest with a face value of Rs.100. Mr.B is holding a 10-year bond that offers him 6% interest with a face value of Rs.100. Assume that the Bank FD rate is at 7%.

Let us assume that for various reasons Mr.A and Mr.B are willing to sell their bonds in the secondary market.

As the Bank FD rate is currently at 7%, many will try to buy Mr.A’s bond rather than Mr.B’s bond. Even few may be ready to pay more than what Mr.A invested (assuming he invested Rs.100). Mainly because the bank is offering 7% and Mr.A’s bond is offering higher than this (8%).

Because of this, Mr.A may sell at a premium price than he actually invested. Say for Rs.106. Now, the buyer of the bond from Mr.A will think differently. As Rs.100 face valued bond is available at Rs.106, which offers 8% interest for the next 10 years, and at maturity, the buyer of the bond will get back Rs.100 back, then he starts to calculate the RETURN ON INVESTMENT. For the buyer, his investment is Rs.106, he will receive 8% interest on Rs.100 face value and after 10 years he will receive Rs.100 face value. His return on investment is 7.14%. This is obviously a little bit higher than the Bank FD rate. Hence, he may buy it immediately.

Suppose the same buyer wishes to buy Mr.B’s bond, to make it attractive to the buyer, Mr.B has to sell his bond at Rs.92 (with a loss of Rs.8). Rs.92 priced bond, 6% interest, face value of Rs.100 and tenure 10 years will fetch the same 7.14% returns for a buyer.

You noticed that the determining factor in both transactions is the Bank FD rate of 7%. Hence, the interest rate policy of RBI is the most important factor for the bond market. Bond prices change on a daily basis based on such interest rate movement.

This risk is applicable to all categories of bonds (including Central Government or State Government Bonds).

In simple, whenever there is an interest rate hike from RBI, the bond price will fall and vice versa. From the above example, indirectly you learned two concepts. One is interest rate risk and the second one is YTM (Yield To Maturity). YTM is nothing but the return on investment for a new buyer of the bond from the secondary market. In the above example, the buyer’s return on investment is nothing but a YTM. As the price of the bond changes on a daily basis, this YTM also changes on a daily basis.

# Yield To Maturity (YTM)

For this also, I wrote a detailed post “Part 4 – Debt Mutual Funds Basics“. However, I will explain the same in detail.

For a new bond investor, yield to maturity in a simple way say is the return on investment if he holds the bond till maturity. You know that when you buy a bond, then you will get interest at a certain interval (in the majority of bonds) and at maturity, you will get back the face value of the bond.

Let us assume that a 10-year bond is currently trading at Rs.105, the time horizon is 10 years and the coupon (interest rate) is 8%, then the buyer has to calculate the return on investment. The buyer will pay Rs.105 (for Rs.100 face value bond), he will receive 8% (on Rs.100 face value but not on Rs.105) every year, and at maturity after 10 years, he will receive Rs.100 (face value but not the invested amount of Rs.105).

The YTM calculation is a little bit complicated to understand for many investors. Instead, there are online readymade calculators available to understand the YTM. If we go by the above example, then the yield to maturity for a buyer or return on investment for a buyer is 7.8% IF HE HOLD THE BOND UP TO MATURITY.

Obviously, buyers by calculating the YTM compare with the current prevailing interest rate. If YTM is better then he will buy otherwise he will negotiate the price with the seller to make it more profitable for him.

Now in the above example, you noticed that rate of interest on the bond is 8% but YTM is 7.8%. It is mainly because if a buyer is buying at face value, then for him the YTM will be 8%. However, in the above example, as he is buying at a higher than the face value, his return on investment is proportionately reduced.

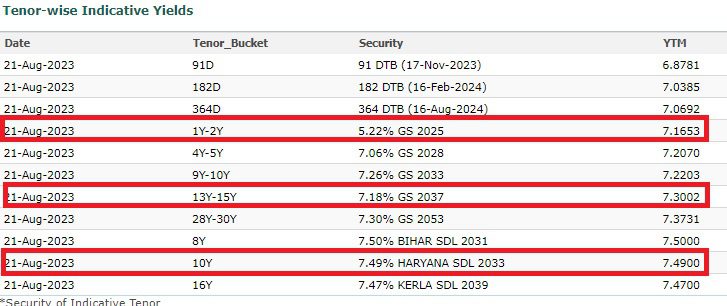

Hence, whenever someone buys a bond, it is YTM matters a lot more than the coupon rate. However, if someone is buying the bond at issuing price, then YTM equals to the coupon rate. To understand this concept in a better way, let us take into consideration the current YTM of the various maturing bonds.

The above list includes the latest YTM of various maturing bonds. Just concentrate on the bonds that I have highlighted.

The 2025 maturing bond YTM is now at 7.16%. But the coupon rate is 5.22%. It obviously indicates that the bond is available at a lower than the face value. If we calculate the price, then the bond is available at around Rs.97 (the face value is Rs.100).

Same way, if look into the 15-year maturing bond, you notice that the YTM is 7.3% but the interest rate is 7.18%. this again shows that the bond is available at a discounted price.

However, if you look at the 10-year Haryana state government bond (which is usually called SDL), the YTM is equal to the interest rate. It means the bond is available at face value.

Now, your debt mutual fund is holding a bunch of bonds, right? Then how the fund will arrive at the YTM of the fund? The fund manager will calculate the weighted average of bonds is calculated. It means that based on the weightage of the particular bond in a fund’s portfolio, the YTM is considered proportionately to arrive at the total YTM of the fund.

Important Points About YTM

- YTM is a return a bond investor can expect IF he is holding the bond till maturity. However, if he is selling it before maturity, then his YTM will differ based on the prevailing price of the bond (do remember that bond price changes on a daily basis and hence the YTM too) at the time of selling.

- YTM will not take into consideration the taxation part.

- Also, YTM will not take into the buying and selling costs.

- Few argue that higher YTM means risky and lower YTM means non-risky. I don’t believe in this plain judgment. Instead, we have to look for the credit quality of the bond and the time horizon left to mature. Of course, the lower YTM bond may be less volatile. However, what matters is the quality of the bond and the time horizon for maturity.

# Volatility

The biggest concern especially when you invest in bonds is volatility. As I mentioned above, if the bond tenure is long-term, then volatility will increase drastically. Just to give you an example, I have taken the last 20 years’ bond yield movement of the 10-year government of India bond (usually it is a benchmark that is considered in many fields of the investment world).

The below chart shows the yield movement of the same of last 20 years.

You noticed that the yield was around 5% during 2003 and it went up to more than 9% during 2008 and again came down.

However, you may not visualize the volatility so easily. Hence, instead of the above chart, I created a drawdown chart of the yield of the last 20 years. Drawdown means how much % it has fallen from its earlier peak.

Notice the sharp fall in yield of almost 40% during the 2008-2009 period and the next big fall is during the 2020 period.

Imagine the volatility of the New Government Of India Bond 2073 as its 50-year maturing bond. I thought of showing the existing 40 years of Government Bond volatility. However, as the 40-year maturing bond was first time introduced in 2015, I thought that may not provide a clear picture as data points are not much. Hence, compared with 10 years bond.

# Liquidity

Liquidity is the biggest concern for such long-term bonds. Hence, with the current attractive yield if you invest and if you need the money before maturity, then you have to struggle a lot to sell the bonds in the secondary market. Also, as I mentioned above, based on the interest rate cycle, you may gain or lose.

Conclusion – Never invest in this bond just because the yield is attractive and with fear of missing this current yield in the future. Try to first look at your requirements, taxation, risk, volatility, and liquidity. Then take a call. Such long-term bonds are typically meant for Employees Provident Fund Organisation (EPFO), insurance companies, pension funds and even charitable trusts.

However, if you are SURE to hold this bond for the next 50 years, then think of entering into this bond as risk is minimal in such a situation. Are you SURE?? If answer is YES, then go ahead.