LIC is introducing its new offline term life insurance LIC’s Jeevan Amar (No.855) from 5th August, 2019. It is claimed that it is going to be one of the best cheapest term life insurance plan designed by LIC. Let us see the benefits and how it is beneficial for all of us.

Note:-Along with this plan, LIC also launched an online term life insurance and read more about this at “LIC’s Tech-Term (No.854) – Online Term Life Insurance Review”.

LIC’s Jeevan Amar (No.855) is a Non-Linked, Non-Participating Term Life Insurance Plan. After a long gap, LIC launching a term life insurance. It is mainly because of the competition in this field of product.

Under this plan, there two categories of premium 1) Non-Smoker and 2) Smoker Rates. You can choose anyone option. However, if you have chosen the Non-Smoker category, then you have to undergo the additional medical examination like Urinary Cotinine Test. Based on the findings of the Cotinine Test, the premium will be applicable for Non-Smoker proposer.

LIC’s Jeevan Amar (No.855) – Features

# It is an OFFLINE Term Life Insurance from LIC.

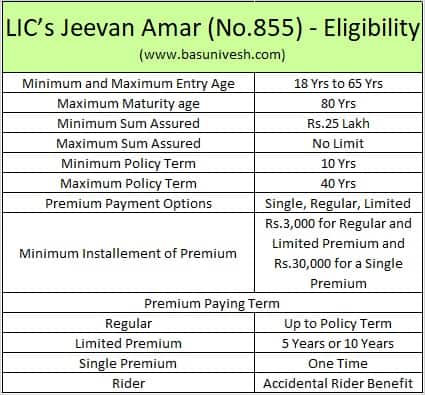

# Minimum Sum Assured is Rs.25 lakh and there is no limit for maximum sum assured.

# You can pay the premium as regular, single or limited.

# You can opt for a level sum assured, where the sum assured you opted will remain the same throughout the policy period.

# You can opt for an increasing sum assured also, where the death benefit will remain the same up to 5 years of the first policy period. After that, it will increases at a rate of 10% for the next 10 years (up to it will turn double of the basic sum assured). From the 16th year, it will remain the same i.e double of the basic sum assured.

# Death Benefits can be taken in installments also of 5 years, 10 years or 15 years.

# Coverage up to 80 years of age.

# You can opt for Accidental Rider also.

# Lower rates for Non-Smokers and special rates for women.

# For regular premium policies, there is no surrender value as it is a term life insurance. However, for a single premium policy and limited premium policy, the surrender value is calculated based on the formula set by LIC.

LIC’s Jeevan Amar (No.855) – Eligibility

Let me share with you the eligibility for buying LIC’s Jeevan Amar (No.855).

LIC’s Jeevan Amar (No.855) – Premium

I have limited information about this policy. However, I have received this below premium example.

Sum Assured-Rs.1 Cr

Term-10 Years.

Premium Paying Term-10 Years.

Mode-Yearly

Sum Assured Option-Level Sum Assured

Age-20 Years-Male-Rs.8,080, Age-20 Years-Female-Rs.7,760 (Yearly)

Age-30 Years-Male-Rs.9280, Age-30 Years-Female-Rs.8720 (Yearly).

Age-40 Years-Male-Rs.16065, Age-40 Years-Female-Rs.13260 (Yearly)

(The above rates are exclusive of GST).

LIC’s Jeevan Amar (No.855) – Death Benefit Options

Death Benefit Sum Assured

As I have mentioned in the above post, there are two death options under LIC’s Jeevan Amar (No.855). You have to choose the type of death benefit sum assured option at the time of buying only. You can’t change the option in the middle of the policy period. They are as below.

# Level Sum Assured

Your nominee will receive the Sum Assured you opted while buying the policy. It will remain the same throughout the policy period.

# Increasing Sum Assured

Under this feature, your sum assured increase as below.

- Under this feature, the death benefit will be the same as that of the initial sum assured you have chosen for the first five years.

- From 6th policy year to 15th year, it will increase at the rate of 10% per year till it becomes the double of the basic sum assured. The increase in the sum assured will continue under an inforce policy till the end of the policy term, till the date of the death of the policyholder or till the 15th year, whichever is earlier.

- From 16th policy year, the sum assured payable at death will be constant and i.e double of the sum assured you opted initially.

As per the chosen option, your nominee will receive the death benefit during which period of the policy your death occurs.

Death benefit payment option to the nominee

Your nominee can receive the death benefit as a lump sum or in installments. If you opted for installments, then LIC will pay the death benefit installments in 5 years, 10 years or 15 years.

You can choose the full death claim amount be payable in installments or a certain portion of death claim in installments.

You can choose this installment option either at the time of buying or during the policy period.

The installments will be payable to nominee in advance at yearly or half-yearly or quarterly or monthly as one has opted for. But make sure that these minimum installment payment rules.

- For monthly payment, the minimum installment amount is Rs.5,000.

- For quarterly payment, the minimum installment amount is Rs.15,000.

- For half-yearly payment, the minimum installment amount is Rs.25,000.

- For yearly payment, the minimum installment amount is Rs.50,000.

If the net claim amount is less than the required amount payable in installment, then LIC will pay as a lump sum one-time payment to your nominee.

LIC’s Jeevan Amar (No.855) – Review

Considering the market competition in online term life insurance plans, LIC launched this plan with the utmost care and including the many features which are already available in the market.

# It is an OFFLINE term life insurance. Hence, the premium will be higher than their newly going to be launched plan LIC’s Tech-Term (No.854). Also, it looks upfront that LIC’s Jeevan Amar (No.855) premium is much cheaper than it’s earlier offline term life insurance. Hence, it is a big benefit for those who are desperate to buy the term life insurance from trusted LIC. However, I strongly suggest you to buy it online. Because agents commission under this plan is 25% for 1st year, 7.5% in 2nd and 3rd year, 5% in subsequent years (for the policy period of 15 years or more). Hence, why not pay more than opting the same from the online?

# Coverage of the policy is up to 80 years of age. Even though Life Insurance is not required up to 80 years of your age, but LIC added this feature to compete with private players. Hence, this is an attractive move.

# This plan comes with an accidental rider. It’s an earlier version of term life insurance was without any rider. Hence, this time LIC added accidental rider benefit. This is one more positive.

# Special discounts for a female is unique and attractive to all-female who are looking for online term life insurance from LIC.

# Premium paying option is too flexible with options like Single, Limited Period and Regular Period. This gives us flexibility.

# Increasing Sum Assured option is first time added by LIC. Where for the first 5 years it will not increase. However, after 5th year to 15th year it will increase at the rate of 10% (up to this increasing sum assured double the basic sum assured). From 16th years onward, it will remain the same throughout the policy period. This is the big relief for those who have to review their life insurance coverage and avoid having multiple life insurance products. However, keep one thing in mind that the maximum benefit one avail under this plan is DOUBLE of basic sum assured you availed at the start of the policy period. Hence, consider the actual need and take a call.

BUT WHY IS LIC LAUNCHING AN OFFLINE PRODUCT WITH the SAME FEATURE, WHEN IT JUST LAUNCHING ONLINE TERM LIFE INSURANCE WITH THE SAME FEATURE?

IS IT JUST TO CATER TO THEIR AGENTS FORCE? OR THOUGHT OF TO CATER TO THOSE WHO ARE NOT WELL VERSED WITH ONLINE BUYING? I DON’T THINK SO. BECAUSE WITH THE KIND OF SMARTPHONES, ONLINE BUYING AND ONLINE PAYMENT THE PEOPLE ARE ACCUSTOMED, IT IS USELESS TO BUY COSTLY OFFLINE PLAN WITH THE SAME FEATURE OF ONLINE (except lower minimum sum assured).

I strongly suggest you go for online term life insurance LIC’s Tech-Term (No.854) rather than this offline product.

Dear sir i tried but could not find why jeevan amulya 2 is costly than amar jeevan, as policy is made up.adding risk factors. What risk we carry more by paying less in jeevan amar?

Dear Parag,

NO risk at all as the product features are different.

Sir, I am availing LIC Jeevan Amulya Term Plan for Rs. 50.00 Lacs. But its premium is very high. Around 15k yearly. Is there any option to change this plan to Jeevan Amar?

Dear Fahad,

Why OFFLINE and why not ONLINE?

Sir , will u prefer this LIC term plan over other private company Term plan.

I am asking ur personal opinion… because once I read ur article over term plans …where u mentioned-“Always go for Simple Vanilla plan”.

Thanks in advance sir

Dear Aaditya,

Why OFFLINE?

My question was For online plan only….sir.

Will u prefer LIC over other private term plan (online)??

Dear Aaditya,

I look for premium and features. If it is suitable to my requirement, then why NOT?

Will it not be good to buy private company e-term insurance which are much cheaper than LIC such as HDFC life, ICICI proud. etc.

Will there be much difficulty while realizing the claim amount, at the time of claim settlement. (After the death of insured person). Please guide and give your opinions.

Dear Heera,

Yes, LIC’s premium is still costlier. If a premium is the concern for you, then you can check with private players also.

What should be the premium for the following criteria?

Policy Term – 40 Years

Sum Assured – 1.5 Cr

Premium Paying Term – 10 Years

Mode – Yearly

What kind of death will not be cover under this term plan?

Dear Hiren,

Please check the same on LIC Website. Regarding the death, all-natural and accidental deaths are covered.

What should be the premium for the following criteria?

Policy Term – 40 Years

Sum Assured – 1.5 Cr

Premium Paying Term – 10 Years

Mode – Yearly

Dear Hiren,

Please check with LIC portal.

diff with lic 855 and lic e term

Dear Prateek,

855 is an offline plan and e-Term is an online plan with more coverage.

Thanks for sharing this information.It’s really good.

Jeevan Amar is a very good term insurance policy even though it is marginally costly compared to online policy you will get valuable service of agent

Dear Jogur,

What is the guarantee that the agent will SERVE ME FOREVER? Why not one go for online plan?

In online plan, for sure and rest assured, the nominee will face lots of issues while realizing the claim amount (in the case of death of the policy holder) for many a broad based reasons.

One more thing, agent does not mean, the only agent from whom through you have enrolled the policy, agent means in a wider meaning in this case, every official of LIC as per IRDA rules.

Dear Rajeeb,

Rightly said, and hence, no worry of buying a costly OFFLINE.

Sir I open SCSS account in PNB on 08/03/2019. But they give interest of only April to till June. Is i eligible for March month interest.

Dear Rajinder,

Yes.

But bank ne kaha hai ki nahin milega. 4 months ho gaye. Even April to June ka interest bhi nahin lagaya tha . 15 din chakkar lagakar Mila.

Dear Rajinder,

Raise a complaint.

Where sir? Even bank says we are not responsible for SCSS account. Kehte hai bank mein FD karwao. Even post office service is better than banks in our city. Very disappointed

Dear Rajinder,

I can’t predict their service 🙂

What about need for medical examination?

Dear Shivaprasad,

That depends on case to case, which will be informed by LIC.

There is a clause that “Insurance company can not reject the claim after 3 years”. However the count of 3 years will restart after every change in policy.

In this policy, Sum assured is changing between 5 to 15 years. Does that mean that 3 years count has to restart every time?

Dear Ashok,

Sum assured increasing in this policy is within the same policy. Hence, you must not consider it as a new policy every year when there is an increase in sum assured. Hence, your assumption is wrong.

Dear Basavaraj,

In term insurance, the premium amount will remain the same till the policy period( eg, 5yrs, 10yrs) or the premium amount change for every year?

Dear Aravind,

In the case of Life Insurance, the premium will remain the same throughout the policy period.

PREMIUM WILL BE SAME TILL TERM

Please avoid offline financial planner, go for robo-advisor who are very cheap. Why pay hefty fees for a offline financial planner.

Dear Naresh,

Here we are discussing about Term Life Insurance 🙂

Hello Sir,

Why is it that premium of term policy in LIC is more than other private company?

Dear PM,

We can’t ask the reason or why it is so. Because premium arrival depends on many business theories of the Life Insurance Companies. Hence, it is hard to say WHY it is costly.

SIR GO THROUGH FULL DETAILS OF CLAIM SETTELMENT RATIO NOT ONLY BY NO OF CLAIMS BUT THE AMOUNT WISE ALSO

LIC has to give 8000 crores this year to IDBI bank for them to give loans. So they are collecting higher premium.

Dear Pradeep,

I feel pity of your knowledge. At first, LIC is used as a scapegoat by the central government to fund such unhealthy banks or institutes. But you are claiming that premium is higher because LIC gave money to IDBI 🙂 Please update your knowledge.

Basu,

You are right. Centre made LIC buy that bank. Now the bank need recapitalisation so that they can do bad loans again. LIC as a promoter is forced to fund them. Where will LIC get money to splash it at IDBI. It’s the policy buyers.

I hope you get the idea.

Dear Pradeep,

Yes, you are right 🙂

VERY GOOD SIR BUT WHO WILL SUPPORT AT TIME OF CLAIM IF Y FAMILY WILL GET HELPLESS & WHO WILL GUIDE ME

Dear Barunkumar,

Why LIC Officials are there? Will they not HELP? Only advisers HELP?

Dear Basu Sir,

LIC official will not give door to door service which an Insurance advisor can give.

Dear Kamal,

Do we need door to door service in the current life of online? Also, what is the guarantee that the agent will remain in this industry as long as I need?