LIC is launching a new plan from 2nd March 2020. This LIC Nivesh Plus (Plan No.849) is a ULIP Single Premium Plan. Let us see the LIC Nivesh Plus (Plan No.849) features, benefits and review.

Features and Eligibility of LIC Nivesh Plan (Plan No.849)

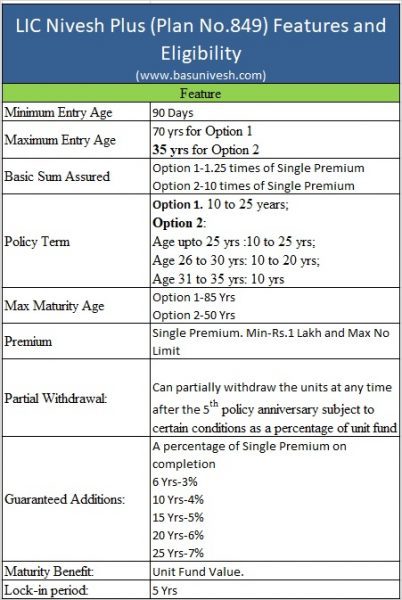

Let us first try to understand the eligibility and features of this LIC Nivesh Plan (Plan No.849).

You noticed that it is a SINGLE PREMIUM ULIP PLAN. However, as this is a ULIP Plan, charges also matter to us. Hence, let us look for the charges under this plan.

The plan proposes to offer you the four types of fund choices with equity components ranging from 0% to 80%.

LIC Nivesh Plus (Plan No. 849) – Should you invest?

I feel pity with the kind of the product LIC luanching. Let us review the features one by one.

# Tax Saving RUSH-LIC knows the blood of Indian investors. Hence, usually during the peak period of the tax-saving rush of salaried, usually, LIC will launch such single premium plans. However, this time they came out with ULIP.

Hence, it is mainly a product to those salaried who are in RUSH of TAX SAVING by hook or crook.

# Expenses-When you are investing in any product, then the first thing you have to concentrate on is the expenses. Look at the expenses of this ULIP. Even though LIC claims there are NO POLICY ADMIN CHARGES, but you have to bear the initial Premium Allocation Charges (which is 3.3% for Offline and 1.5% for Online) and Fund Management Charges (1.35% of Unit Fund).

It is just pathetic the way LIC is thinking that by charging 1.35% Fund Management Charges, it can claim LESS expenses. Look at the total expense ratio of DIRECT Mutual Funds to this 1.35%. It is still high. If you look at Index Mutual Funds or ETF, LIC’s this Fund Management Charge is around 1% higher.

If you look at charges, I don’t think it is a worth product to consider.

# GUARANTEED ADDITION-As I said above, LIC knows the blood of the Indian investors. We are fond of a product which gives us Tax Benefits and GUARANTEE. However, look at what is GUARANTEED here. It is the maximum of 7% Guaranteed Addition for 25 years of the policy. Also, this is a % of Single Premium what you paid initially.

# Life Risk Coverage-The maximum coverage one can get is 10 times of your single premium. Suppose you are looking for Rs.1 Crore Life coverage, then you have to invest Rs.10 Lakh. Instead, why not buy the LIC’s online Tech Term Policy to cover your life risk than combining Insurance with Investment?

# Death Benefit-Under this plan, if death occurs before the commencement of risk, then the nominee will receive the FUND VALUE ONLY. However, if death occurs after the commencement of the risk, then the nominee will receive HIGHER of RISK COVERAGE or FUND VALUE.

But if you separate the Investment and Insurance, then in case of death at any point of time, you will receive the fund value from whatever you invested and also from term life insurance the full coverage amount.

Hence, thinking that it covers your life risk is a MYTH.

Conclusion:-As I pointed above, this product is launched with an intention to garner those customers who are desperate to save their tax by hook or crook. Stay away from such products as they neither be considered as best for Life Insurance nor for Investment purposes.

LIC launching one more new plan on 2nd March 2020. Take a look of that plan at “LIC SIIP (Plan No. 852) – Eligibility, Benefits and Review

Yeh basu nivesh ke hisaab se chalenge toh kabhi kuch nahi kar paaoge..

People like basu nivesh Only want people to invest in shares and stocks…

He recommends Lic tech term plan coz he knows if he goes against all plans, people will not believe him…

Once u buy a mutual fund from any company there are N number of charges and when u go to withdraw that mutual fund you get less than peanuts..

Invest only and only in LIC, I would recommend SIIPS of Lic is better than those nonsense mutual fund available in market

Dear Kapil,

Where I recommended investing in stocks?? 🙂 Come out from that mindset, please 🙂

I don’t intend to oppose Mr Basu’s review but I didn’t see a single review of Mr Basu which recommends any any LIC policy.

Every instrument has pros and cons, be it shares MF so all LIC policies are not bad.

Indians have a poor risk appetite so LIC is not something which should be altogether rejected.

Dear Anonymous,

Thanks for your views 🙂 I am fond of LIC’s Online Term Life Insurance and I recommend all my clients as the first choice among Term Life Insurance (even though it is costliest in the market).

when LIC sell a policy to a policyholder , except policy holder LIC and agent both earn profits . In long run LIC provides only 4% – 5% return . Any amount of money will double = 72/ Interest rate . If you assume only 6 % return then 72/6= 12 , In 12 years your Initial investment would be double . LIC return Check IRR in excel , any Life insurance company will provide only 4-5% return . They invest in BOND market and G sec , they generate 8-10% cagr . 4-5% gets policy holder and agent and LIC both makes profit .

LIC alternative take any Debt Mutual Fund . Hold for 25 years you will get more return then LIC .

professionally making customer fool is called business and LIC is no1 in this segment .

Dear Ghosh,

Thanks for airing your views.

Its a market driven long term investment option like the erstwhile Future Plus. Its not an insurance option. Take only minimum insurance cover (1.25 times). The maturity amount is free from any capital gains tax (unlike amounts received on redemption of mutual funds) as the law stands today. Wonderful opportunity to invest on behalf of minors (grand children) and to create a corpus for them in a tax effective way. Minimum age at entry is only 90 days.

For example Future Plus which was launched in March 2005 has a NAV of 43.5 in March 2020 (growth plan) giving an average annual yield of 16.75%. What more do you want?

I think it is a great product.

Dear Iyer,

What about the cost? If you are pointing about the taxation, then why not you discuss about the high cost of such products? Take ONLY MINIMUM INSURANCE COVER??? When you approach the Life Insurance Company, it must be to BUY LIFE INSURANCE but not an INVESTMENT PRODUCT.

Hello Basu,

I am looking for a saving plan to make some corpus in next 5 years. I can invest 50,000/- per annum. My current age is 38 years.

Can you please suggest me any good option for it.

Thanks

Dear Rajneesh,

Use either Bank RDs, FDs or Liquid Funds.

LIC has launched excellent ULIP products keeping in mind the attributes people like to have in a financial product .Analysis is biased and full of ignoranve

Dear N,

Let me know your analysis also that on what basis you are claiming this to be EXCELLENT ULIP KEEPING IN MIND THE ATTRIBUTES OF PEOPLE. Can you come out with certain points or ideas rather than BLIND FOLLOWING OF LIC?