LIC launched its new pension plan LIC New Jeevan Shanti on 21st October 2020. It is a single premium, deferred pension plan. The pension rates are guaranteed at the time of buying itself.

Few days back, LIC launched Jeevan Akshay VII, an immediate annuity plan (LIC Jeevan Akshay VII Pension Plan (857) – Features, Benefits, and Eligibility). Due to falling interest rates, LIC closed the earlier Jeevan Shanti Plan and launched the new Jeevan Shanti. Let us see it features.

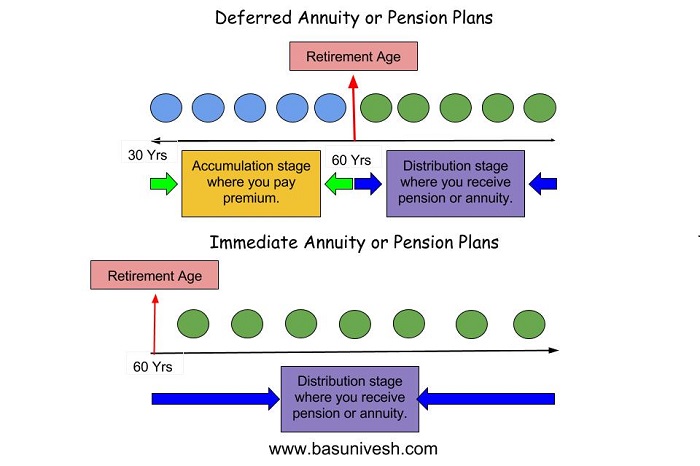

What do you mean by deferred pension plan?

Let me give you an example. Assume that you are 40 years old. You are buying this product with the intention that you start your retirement life at the age of 50 years. Then this 40 years to 50 years period is called as a deferment period. From 50 years onwards it is called as a retirement period of the post deferment period. You can refer to the below image for clarity.

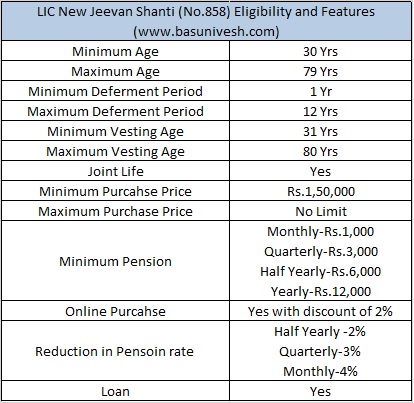

LIC New Jeevan Shanti (No.858) Eligibility

Let us now look into the eligibility conditions for buying LIC New jeevan Shanti (No.858).

You noticed that the maximum deferment period is 12 years and the maximum vesting period is 80 years. The second point you have to notice is the reduction in pension if you opted for a half-yearly, quarterly, or monthly pension. The policy is eligible for surrender also.

Benefits of LIC New Jeevan Shanti (No.858)

Annuity Benefits:-

# Deferred Annuity for Single Life:- Nothing is payable during the deferment period. After the deferment period, you will receive the pension as per the option you have selected as long as you are alive.

# Deferred Annuity for Joint Life:-Nothing is payable during the deferment period. After the deferment period, you will receive the pension as per the option you have selected as long as the primary or secondary holder alive.

Death Benefits during deferment period

Higher of the below will be payable:-

# Purchase Price+Additional Benefit on Death-The total annuity amount payable till date of death

OR

# 105% of Purcahse price.

(Additional benefit on Death=(purchase price*Annuity rate per annum payable monthly)/12)

This Additional benefit on death is applicable only during the deferment period but not while you are issuing the pension.

Death benefit options after defermnet period

You have an option to choose three types of death benefit to be payable to your nominee.

a) Lump Sum Death Benefit:-Your nominee will receive the lump sum amount in one go.

b) Annuatisation of Death Benefit:-Under this option, the nominee can purchase the LIC New Jeevan Shanti (No.858) in his name. Your nominee can opt for full purchase or partly he can purchase this pension plan.

c) In Installment:-Your nominee can receive the death benefit in installments like 5, 10 or 15 years. Such installments can be receivable in monthly, quarterly, half-yearly or yearly.

LIC New Jeevan Shanti (No.858) – Should you purchase?

In India to sell a financial product if you tag two lines GUARANTEED or TAX-FREE, then people buy such products like hot cake. In this product, LIC mentioned it as a GUARANTEED pension. Hence, obviously, investors look at this feature itself. However, consider the below factors before you buy such annuity products.

# Inflation:- Do remember that in this product, the pension will not increase as you grow older. It will remain fixed. Hence, the pension of what you will get today may have no value after few years due to inflation.

# Taxation:-Whatever the pension you receive from this product is taxable as per your tax slab. Hence, post-tax returns may be much lesser than actually what you receive. If you are under the highest tax bracket, then such products are not suitable for you.

# Annuity Age:-If one plan to enter into this plan at 30 years of age, then he has to opt for a pension when he reaches 42 years (to the maximum). Do you need a pension during your 42 years of age?

# Features in question:-If you choose monthly, half-yearly, and quarterly annuity options, then you receive less pension than opting for yearly. I think this is the biggest hurdle. Because people buy such products only to get a constant monthly income. The maximum deferment period set as 12 years. It means after 12 years you have to start receiving the pension. What if you are extending your working age?

Such products are suitable for those who are desperately looking for a GUARANTEED income stream and who not bother about taxation, inflation and ready to locking their money.

It is hard to predict the returns from annuity plans. Because it all depends on how many years you survive after the deferment period. Also, if this plan is purchased by the young guy, then obviously the returns will be lesser and for those who are elders, for them, the rates may look attractive.

Conclusion:-Annuity products are best for those who are actually looking for a constant stream of income rather than worrying about the market or interest rate movements. However, it is not worthy to rely on such products as such products fail to beat the index in long run. Hence, my suggestion is that rather than completely relying on such products, you may explore the products like PMVVY, SCSS, Tax-Free Bonds, and RBI Floating Rate Bonds for your immediate needs. At the same time, if you are looking for an income stream after 10 years or so, then the combination of equity and debt as per your risk appetite will be the best hedge against inflation.

Refer our latest posts:-

- Flexi Cap Funds: Why Your 10-Year Return Chart Is Lying

- EPF Scheme 2026: EPF, EPS and EDLI Rules Explained Fully

- Financial Freedom Without Health? You’ll Regret It Later

- The Peltzman Effect: Why Playing It Safe Can Make You Poor

- Your Retirement Success Depends on Luck, Not Skill

- Never Compare Nifty 50 Index Funds Vs Active Large Cap Funds!

Mr.Basu,

I am at 59 yrs of age. Suggest a policy of LIC to get immediate pension by 1 or 2 yrs.

Dear Chalraborty,

You can look for Jeevan Akshay and you can buy the same online also.

I have invested Rs 12 lakhs and after two years including the interest @7% the totai amount would be Rs 128980 . For this amount the interest is Rs Rs90291 .60. But LIC pay85080 0nly after two years.

Less than the interest. What is the benefit?. Can I close the same

Dear Roy,

Please understand the product feature. I am unsure of from where you assumed that this policy will pay you 7% interest.

Hello Basu,

I am your fan and an avid follower of your articles.

For this policy how do we know what is the IRR for the amount invested in the Jeevan Shanti policy.

These days there is a growing concern regarding safety of money in banks. Can you post an article to help your followers in taking a decision which banks not to keep money in?

Regards,

Soumya

Dear Soumya,

As this policy is meant for a lifelong annuity, hard to predict. But you can predict to a certain extent the IRR by assuming the life expectancy as around 80 Years.

Thank you Sir! What is the rough IRR for New Jeevan Shanti assuming 80 years life expectancy?

Dear Soumya,

It may be around 6% to 7% (Pre Tax).

Thanks once again. Also, please provide guidance regards which banks to keep money in and which ones not to keep money in. Maybe a top 10 or top 15 kind of analysis. Thanks in advance.

Dear Soumya,

Surely I will do. Thanks.

Which is the best LIC policy?

Jeevan Saral or Jeevan Anand

Dear Abhishek,

The best must depend on your requirement. First, try to understand your requirements.

I don’t understand your rationale for posting on LIC products just to conclude that they are not good or suitable. Are you being paid to right such article against LIC. Why such bias towards LIC

Dear Naresh,

Whether it is LIC or some other products, if I say the reality, then am I against LIC? 🙂 I am not saying that one MUST NOT BUY. But making them aware of the pitfalls. If they are OK with this, then they have all rights to buy right? 🙂

I noticed that interest rates are not mentioned on the LIC website also. I think that also plays a key role.

Dear Raju,

Such policies will not offer any interest rates. They just offer annuity rates.