LIC Jeevan Utkarsh Plan 846 is going to launch on 6th September 2017. This policy will be available to purchase for 270 days from the date of launch. Let us see its features, benefits and review it.

LIC Jeevan Utkarsh Plan 846 is a single premium, non-linked, with-profits, savings cum protection plan wherein the risk cover is ten times of Tabular Single Premium.

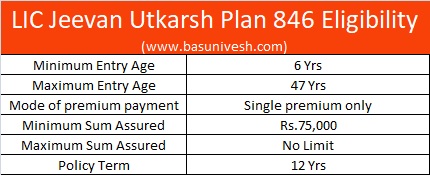

Eligibility of LIC Jeevan Utkarsh Plan 846

I will explain you about the eligibility from below the table.

In case the age at entry of the Life Assured is less than 8 years, the risk under this plan will commence from one day before the policy anniversary coinciding with or immediately following the completion of 8 years of age. For those aged 8 years or more, the risk will commence immediately.

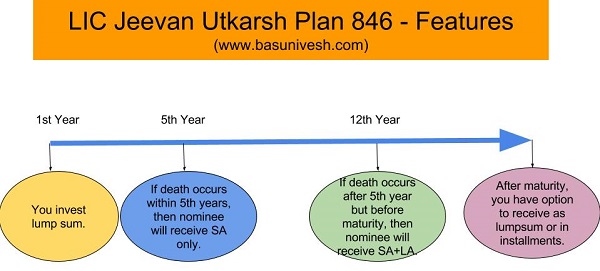

Features of LIC Jeevan Utkarsh Plan 846

# It is a single premium close ended plan.

# It is a typical endowment plan.

# You can avail riders like LIC’s Accidental and Disability rider.

# This plan offers unique settlement feature (explained below in detail).

# You can surrender the policy at any point of time during policy period (as per some conditions).

# Loan facility is available after 3 months from the policy start period.

Benefits of LIC Jeevan Utkarsh Plan 846

There are two types of benefits in LIC Jeevan Utkarsh Plan 846.

# Maturity benefits of LIC Jeevan Utkarsh Plan 846

If the Life Assured surviving to the end of the policy term, “Sum Assured on Maturity” along with Loyalty Addition (LA), if any, will be payable. Where “Sum Assured on Maturity” is equal to Basic Sum Assured.

# Death Benefits of LIC Jeevan Utkarsh Plan 846

a) If death occurs within the first 5 years of policy

If death occurred before the commencement of risk, then LIC will refund the single premium without any interest on it. Also, this refund of single premium will not include any taxes, extra premium chargeable under the policy due to underwriting decision and rider premium, if any.

If death occurred after the commencement of risk, Sum Assured will be payable to nominee without any additional benefits.

b) If death occurs after the 5th years of policy and before maturity

Sum assured which is equal to 10 times of your single premium and Loyalty Addition will be payable to the nominee.

Sum Assured at death will be highest of the below

-125% of the single premium; or

-Guaranteed Sum Assured on Maturity i.e. Basic Sum Assured; or

-10 times of Single Premium

Loyalty Addition of LIC Jeevan Utkarsh Plan 846

Along with Sum Assured, this plan offers you the benefit of Loyalty Addition or LA. You will be eligible for LA after the completion of five policy years in the form of Death during the policy term or Maturity.

Settlement option of LIC Jeevan Utkarsh Plan 846

This feature I think first time introduced by LIC. You can receive the settlement amount (death or maturity) in installments over the chosen periods like 5 Yrs, 10 Yrs or 15 Yrs instead of a lump sum one-time settlement.

The policy holder has to choose this option but not the nominee. You can receive this maturity installment settlement either in monthly (Minimum Rs..5,000), Quarterly (Minimum Rs.15,000), Half-Yearly (Rs.25,000) or yearly (Minimum Rs.50,000).

If your chosen option is below the above-said minimum limits, then you will receive it as a lump sum settlement only.

For death claim settlement option-During the policy period, the policy holder has to select this option either of the one-time lump sum or the settlement option explained above.

For maturity claim settlement option-Policyholder has to inform to LIC 3 months before the policy maturity.

The policyholder can change the option of receiving it as a lump sum after the maturity period and the start of settlement frequency also. In that case, LIC will calculate the remaining amount to be payable to him based on the calculation.

If policyholder option settlement option which is not a lump sum, and if death occurs during this settlement period, then the future settlement installments will be payable to his nominee. In this case, nominee can’t alter the settlement rules.

Review of LIC Jeevan Utkarsh Plan 846

# This is a typical endowment plan where insurance and investments are mixed. Hence, you can’t expect around 5% to 6% returns.

# If you are very much eager to go for lump sum investments, then you have many many options available. Then why one must lock money here?

# LIC first time instroduced the settlement option. This I think is the first of it’s kind from LIC. However, do remember that each facility you get will comes with cost.

# In case of settlement option, the policyholder dies means the nominee can’t alter the settlement feature. This I think a bit rigid feature.

# I think this plan is made for thos who are eager to save the tax under Sec.80C benefits.

Note-This is the limited information which I am having right now. I will update the blog post as and when I get the updates regarding this plan.

Who should sign the form if it is invested for a child age of 7?, what form numbers are used for child?

For Jeevan Utkarsh plan

Abel-It is the proposer (parents like a guardian) has to sign the form. Visit the branch regarding other information.

For whose “Utkarsh” LIC brought this product? Returns won’t even beat inflation rate.

Ritesh-Obviously for AGENTS 🙂

Does 10(10D) exemption apply if the insured is less than 8 years old for Jeevan Utkarsh ? The commencement of Risk is only when the insured is 8 years old. That means for a 6 / 7 years old, first two years or first year the sum assured value is ONLY equal to the single premium paid which is against the clause of 10(10D) exemption :

actual sum assured simply means the sum assured which is least in “ALL” the policy years

Can you please clarify ?

Babu-Any death claim amount is tax-free in the hand of a nominee. Your doubt is correct. But here in first risk free years, insurance is not comes into picture. Hence, it is still treated as tax-free.

Thanks for the clarification . So, it holds good ( tax exemption ) even for the survival benefit – maturity proceeds . Right ?

Thanks again for your time & comments. I appreciate sincerely.

Babu-Maturity proceeds will be as per the Sec.10(10D).

Basavaraj,

Grateful for your guidance.

Right . So , if the insured is 6 / 7 years years old , the first 2/1 years what will be the effective SA as per 10D ?

Since the ‘risk’ is not commenced will it be considered just the premium paid ?

In that case for 6/7 years old, it cannot comply for tax exemption because 10D expect SA to be minimum 10 times of annual premium for ALL policy year.

Or , as you said earlier since there are no insurance in initial years for 6/7 years – they will not be considered in 10D hence maturity proceeds will remain tax free ( for 6 / 7 years old) for Jeevan Utkatrsh.

Please clarify.

Thanks a lot for your comments & time.

Babu-Yes, your understanding is correct.

SIR,

GOOD SUGGESTION GIVEN BY YOU FOR JEEVAN UTKASH 846 PLAN,I WANT TO KNOW BENIFITS IN ACCIDENTAL CASE ,CAN WE GET DOUBLE AMOUNT OF S/A OF ACCIDENTAL CASE,PL. EXPLAIN.

Bharat-If you opted for an accidental rider, then you will get that benefit. Otherwise, LIC will pay you only the Sum Assured and LA (if any declared).

YOU HAVE SAID THIS IS THE FIRST TIME THAT LIC HAS INTRODUCED SETTLEMENT OPTION. THIS SPEAKS HOW MUCH YOU ARE IGNORANT ABOUT LIFE INSURANCE PRODUCTS. PLEASE HAVE A SOUND KNOWLEDGE ABOUT LIFE INSURANCE AND THEN, SPEAK OUT. PLS UPDATE YOUR KNOWLEDGE.

Mazibar-Thanks 🙂 May I know which other plan offers such flexible settlement option? I am ignorant and want to learn from the knowledgeable person like you. Can you share it??

Sir,

I want to Invest 150000/- for batter returns for my future . Requesting to suggest best plan. My Age 35 years.

Hardik-May I know the meaning of BETTER return and your TIME HORIZON?

My son is 20 years, My intention is Investment. How about investing in Jeevan Uthkarsh?

Ramachandra-May I know the tenure?

20 Years

Ramachandra-Then why this 12-year product? Also, why to mix insurance with investment?

If i invest one lakh in this jeevan utkarsh plan, how much guaranteed amount shall i get after 12 years

Avtar-The guaranteed part in this plan is ONLY the SUM ASSURED but not LA. Hence, you may expect around 5% to 6% returns.

Sir,

If i invest one lakh in this jeevan utkarsh plan, how much guaranteed amount shall i get after 12 years ( investment)

Bindu-NOTHING is guaranteed except the Sum Assured. Because LA depends on the LIC’s declaration. But we may assume around 5% to 6% returns.

Dear Mr Basu,

Ref lic jeevan utkarsh plan.

Would it be advisable to invest about 270000/- for a 9 yrs old child, for maturity @21yrs, as indicated in this plan? against investing the same amount in about 80-90 gms of gold today, with the intention of needing the gold around 22yrs age of child?? With safety of investment, point of view. Ppf, ssa already invested in.

Kindly read reference salutation as ‘Dear Mr Basavraj’. instead of Mr Basu. Typo error is regretted.

Patole-It’s alright.

Patole-I neither support the idea of investing in this plan for long 12 years nor the idea of investing in PHYSICAL gold for future usage.

I seems it is good plan for above 6 years childrens

Virupaksha-May I know what sense? Also, kids need INSURANCE?

Please tell me about an investment scheme where a little risk can come but could expect good returns for 5 to 10 years

Dheeraj-May I know the exact meanings of LITLE RISK and the exact tenure of investment? There is a huge 5 years gap in your assumptions. Investment not works in this way.

Dear Basu sir,

This policy is just a copy + paste of old JEEVAN SHIKHAR policy to lure one time investors who search insurance at the year end to save tax. The biggest drawback of this policy is maturity returns are taxable ( premium of < 5% SA per annum or policy term of more than 20 years are eligible for maturity proceedings tax exemption). If final returns are taxed at 30% what is left for investor? it is just like bank Fixed deposits with a life cover.

regards

RAJESH PAI

Rajesh-It is tax-free maturity amount. As per rule of Sec 10(10D), if the premium is 20% of sum assured and issued on or before 31st March 2012, then it is tax-free. Same way if the premium is 10% of the sum assured for policies issued on or after 1st April 2012. Hence, it is tax-free maturity amount. LIC is clever in this. Because this is meant for end time tax saving individuals who run behind plans to save tax at any cost. Every year LIC floats such plans to trap such individuals.

Hello Sir, I am Hareesh Babu and I have two daughters aged about 7 Years and 9 Years. If I purchased Jeevan Uthkarsh Policy for them for Rs.2,00,000/- (Two Lakhs) for each child. How much amount will come after 12 years? and give full details.

Bachu-Whether your intention is INSURANCE or INVESTMENT?

INSURANCE

Bachu-Then buy pure Life Insurance (Term Life Insurance) either from LIC or from other insurers.

SIR I M 21 YEARS OLD PLEASE SUGGEST ME TO THAT POLICY WHICH WILL HELP ME AFTER 12 YEARS

Balakrishna-What is your requirement, INSURANCE or INVESTMENT?

I think this is a good plan who do not want to take a tension for every year premium. The period is also goods only for 12 year. One time investment and more benifit thanks lic

Vimal-May I know what do you mean by MORE BENEFIT? May I know how much one can expect? In my view, not more than 5% to 6%.

Sir. Please, tell me what is the fixed L.A after maturity for this plan.

Biswanath-It is new plan. LIC will announce once this plan completes at least 3 years.

sir,I m sr.citizen.is there any LIC plan like this for sr.citizen?

Sureshchandra-You can check LIC’s Jeevan Akshay VI or “Pradhan Mantri Vaya Vandana Yojana -LIC’s 8% Guaranteed Pension Plan“.

Sir how is the Loyalty Addition (LA) for this plan?

Kamlesh-It is usually not disclosed during policy launch. They declare it usually during the course of the policy period.