LIC today launched a new plan LIC Dhan Varsha 866. It is a GUARANTEED and single premium plan. LIC’s Dhan Varsha is a Non-Linked, Non-Participating, Individual, Savings, Life Insurance plan which offers a combination of protection and savings. This plan offers up to Rs.75 per Rs.1,000 as guaranteed addition.

This plan provides financial support for the family in case of unfortunate death of the life assured during the policy term. It also provides a guaranteed lump sum amount on the date of maturity for the surviving life assured.

This plan is available in ONLINE and OFFLINE modes. Hence, at your convenience, you can buy this plan.

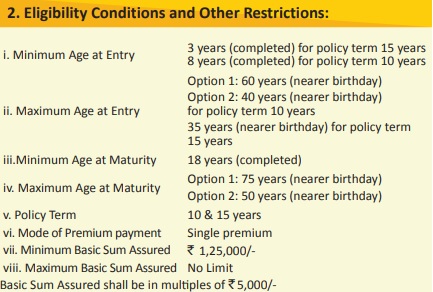

LIC Dhan Varsha No.866 Eligibility

Let us first understand the eligibility criteria of this plan.

Date of commencement of risk: In case the age at entry of the Life assured is less than 8 years, the risk will commence either 2 years from the date of commencement of the policy or from the policy anniversary coinciding with or immediately following the completion of 8 years of age, whichever is earlier. For those aged 8 years or more at entry, risk will commence immediately from the date of acceptance of the risk i.e. from the Date of issuance of policy.

This plan offers riders like Accidental death and disability rider, Term Assurance riders, and settlement option for maturity (instead of receiving the maturity in a lump sum, you can opt for 5 years installment and the interest will be 5 years of Gsec semi-annual interest rate minus 2%).

LIC Dhan Varsha No.866 Benefits

There are three types of benefits for all the in-force policies.

# Death Benefit – If the death of the policyholder happens to post the commencement of risk, then his nominee will receive “Sum Assured on Death” + Accrued GUARANTEED ADDITION. “Sum Assured on Death” shall depend on the option chosen by the policyholder as under –

Option 1 – 1.25 times of Tabular Premium for the chosen Basic Sum Assured

Option 2 – 10 times of Tabular Premium for the chosen Basic Sum Assured

You have to choose these two options at the time of buying the policy itself. Later on this option can’t be altered.

If the death happened before the commencement of the risk, the Death Benefit payable shall be a refund of premium(s) paid (excluding taxes, extra premium, and rider premium(s), if any), without interest.

# Maturity Benefit – If the life assured survived till the maturity of the policy, then he will receive “Basic Sum Assured” along with accrued Guaranteed Additions.

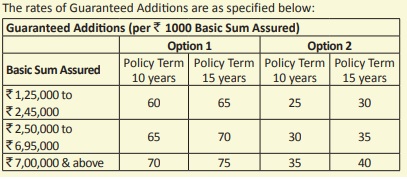

# Guaranteed Addition – The Guaranteed Additions shall accrue at the end of each policy year, throughout the policy term, and shall depend on the Option Chosen, Basic Sum Assured and the Policy Term.

LIC Dhan Varsha No.866 Guaranteed single Premium Plan – Should you invest?

Let us now understand the basic purpose of this post. Should you invest in this product? The answer as usual is NO. The reasons are as below.

# Why has LIC launched this product now?

If you are tracking the LIC history, one thing is sure LIC always launches single premium policies during the months of October to February. The primary purpose is to catch the salaried customers who are in a desperate mode to save the tax.

Many easily turn scapegoats to this logic.

# Death Benefits

If death happens before the commencement of risk for minors, then LIC will return just the premium paid without any interest. This looks funny to me. Whether LIC think that people are so desperate or illiterate to blindly invest?

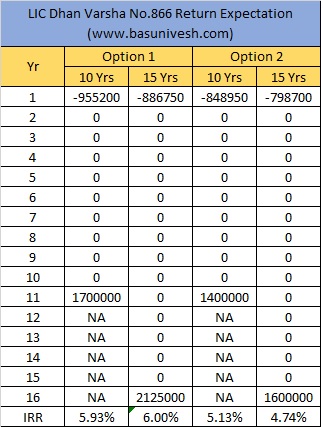

# Returns

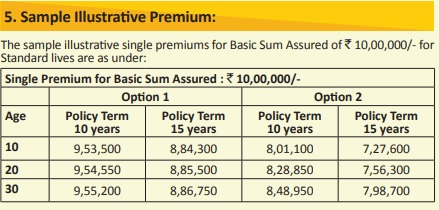

Let us take an example of premium from the LIC brochure itself.

Let us take an example of a 30-year-old guy opting for Rs.10,00,000 Sum Assured. Then the returns look horrific.

The above premium that you pay to LIC is exclusive of tax. If you add the tax you pay while purchasing this policy means, the return will again reduce.

But…the biggest question mark is – When LIC is claiming Rs.75 per Rs.1,000 Sum Assured as Guaranteed Addition, then how come the returns are so low? The reason is that LIC declares the GA. But it will not give you. Instead, they will keep with them without adding a single penny to your money on that yearly accrued GA. Because of this, the end return on investment will be less than typical bank FD rates.

# Maturity benefit in installment

This is one more LIC’s biggest blunders. If you notice it cautiously, what it was mentioned in the brochure is “For all the installment payment options commencing during the 12 months’ period from 1st May to 30th April, the interest rate used to arrive at the amount of each installment shall be annual effective rate not lower than 5-year semi-annual G-Sec rate minus 200 basis points; where the 5-year semi-annual G-Sec rate shall be as at last trading day of the previous financial year. Accordingly, for the 12 months period commencing from 1st May 2022″.

When the current G-Sec 5 year yield (as of today) is at 7.3%, I don’t know why one must madly opt for this feature.

Considering all these features, I strongly suggest you to stay away from this product. However, if you are fond of LIC, running behind the concept of GUARANTEED and eager to save the tax, then please go ahead!!

Dear Sir ,

I have been reading your articles since last few years and find them very informative.

I am 54 years old and a working professional. My income is Rs. 80,000 per month.

Can you please suggest a few low premium and guaranteed High Maturity / High Return LIC POLICIES or a few COMBINATION POLICIES which can give me a NET RETURN OF 45 TO 50 LACS .

I can invest a total of 10 lacs premium over a period of 10 to 12 years . I NEED NET 45 TO 50 LACS AFTER 12 TO 15 YEARS FOR MY SON AND DAUGHTER’S MARRIAGE.

THE LIC POLICIES CAN BE TAKEN

BY MY ELDER SON WHO IS 22 YEARS OLD. I CAN GIFT HIM 10 LACS WHICH IS PERMISABLE AS PER INCOME TAX.

KINDLY HELP ME AND ADVISE WITH YOUR EXPERT OPINION FOR WHICH I SHALL BE TRULY OBLIGED.

KIND REGARDS ,

MANOJ

7992287230

[email protected]

Dear Sir,

I have replied to your email.

Many thanks for the clear picture…was thinking of investing just to help an acquaintance!!!..Would you suggest any other Lic scheme which is beneficial,apart from PMVVY of course?

Dear Shobha,

Always buy Life Insurance only for protection purpose but not as an investment purpose.

LIC is bullshit . They are fooling people giving them very less gain from the investment and also you will need run around LIC offices to get the funds settled after maturity. My personal opinion invest in Mutual funds and stocks directly if you are looking for good returns.

Dear Raghavendra,

I don’t want to comment on your views about LIC. However, one must have debt part also in investment and never put all your money in single asset class just because they generate high returns.

please publish article on Long Term capital gains related to Land sale. Options for saving tax like buying a house or another land, putting money in capital gains account and any other options.

i spoke to you too. i am waiting for a very long time for this article

REgards

TS Sridhar

M-9449929936

Dear Sridhar,

Yes, it is a long pending work. Will soon write.

calculation completely ignores the benefit of insurance cover one will get. It will be indirect return every year till the the time policy is active. If we add that, then return across different options will go up by approximately by 1.5 to 2%. Am I missing something ?

Dear NA,

Do you think this benefit of INSURANCE inch up the return even of around 0.5%? Check the term insurance rates (including LIC), they are available at cheapest rates. Don’t misguide the people with such illogical ideas to showcase the returns. Whether IRDA ever considered your way of calculating the returns in it’s indicative returns calculation?

Sir, I am comparing this plan with bank FD. Also I am planning to take this on behalf of my 6 yr old daughter, who will receive the money as tax free ( for 15yr plan option 1).Do you think bank FD around 6% after 15 years? Is there any better idea?

Dear Himadri,

Do you think for your 6-year-old daughter, this plan is SUPERIOR? Think twice, especially when the education inflation is more than 8% and such products give you around 5% to 6% returns. SSY is a far better option than this.

How you say LIC won’t give Rs 75 per 1000/-, instead they will keep?

Dear Himadri,

They will keep this GA with them without adding a single penny to such yearly accrued GA up to maturity. I hope you understood the concept of TIME VALUE OF MONEY.