Recently LIC declared the bonus rates for the year 2021 – 2022 (As per March 2021 valuation). Let us see the complete details about LIC Bonus Rates – 2021- 22 and how they affect your life insurance returns.

LIC of India has declared the latest bonus rates for the valuation period 1 st April 2020 to 31st March 2021.

Update – The latest LIC Bonus Rates for 2022 – 2023 is declared by LIC. Refer to the latest bonus rates “LIC Bonus Rates – 2022- 2023 | Complete List“

Meaning of bonus for LIC policies

When you buy a traditional with profit product from LIC, then your returns from such policy mainly depend on what will be the rate of bonus. LIC declares bonus on the yearly basis. Usually, you will not find any such drastic change. But it is always better to track the bonus rates.

Let us say you bought LIC’s Jeevan Anand for the term of 20 years and the sum assured as Rs.5,00,000. If LIC declared a bonus as Rs.45 for this product, then the calculation will be as below.

The bonus rates will be based on three criteria.

# Term of policy-Higher the tenure means higher the rate.

# Sum Assured-LIC bonus depends on per Rs.1,000 of Sum Assured. Hence, if you bought higher sum assured policy, then your bonus accumulation will be at the higher end.

So from above example, if LIC declared you Rs.45 as bonus per Rs.1,000 sum assured for 20 years policy, then the bonus accumulation for that year will be as below.

Rs.22,500=(Rs.45 x Rs.5,00,000)/Rs.1,000.

Remember this Rs.22,500 will not be payable to you. But it will be with LIC and you receive this amount during the time of death claim or maturity. The most important point to note is that they will not add any amount on this Rs.22,500. It will remain the same till the period of death claim or maturity date.

There are various types of benefits LIC policies offer you like Bonus, Loyalty Addition or Final Additional Bonus.

Types of LIC benefits

# Simple Reversionary Bonus

LIC will declare this on yearly basis and added to your policy account. You will get it either at maturity or if there is a death claim. If you decide to exit from the policy during the policy period by surrendering it, then a certain portion of such accrued bonus will be payable to you. Do remember that this type of bonus does not compound every year and hence it is called a simple reversionary bonus.

# Final Additional Bonus (FAB)

Final Additional Bonus (FAB) is a one-time additional bonus, which is paid along with the maturity amount. It is an additional one-time bonus along with the simple reversionary bonus and added to the policy account. As I told you, it is a one-time payment you will receive at maturity, death claim if you surrender it (one year preceding the date of maturity).

# Loyalty Bonus (LA)

Based on the policy features, certain LIC policies are eligible to avail this LA. LA is also a one-time payment kind of benefit. Unlike the simple reversionary bonus, which becomes a part of the policy benefits as and when it is declared, loyalty additions shall be available to the policyholder only at the time of exit from the policy. Hence, they became the part of policy benefit at once during the policy exit (due to maturity, death, or surrender)

How to calculate returns for your LIC policy?

In simple, I explained how to calculate bonus for a year. But LIC offers different products like the endowment, limited endowment or money back plans. In such a situation, you may find it difficult to calculate returns on your LIC plan. Hence, I created a video about this.

The below video will explain to you how to calculate returns on your LIC plans using an excel sheet. It is too simple and convenient for you to calculate.

LIC Bonus Rates – 2021- 22 | Complete details

Hope you got clarity about the importance of bonus rates for your traditional plans. Now let us concentrate on recently declared LIC Bonus Rates – 2021- 22.

The below reversionary bonus rates are applicable for the policy year entered upon during the inter valuation period i.e. 01/04/2020 to 31/03/2021 and in force for full sum assured as on 31/03/2021. It would apply to policies resulting into claims by death or maturity (including those discounted within one year of maturity) or surrendered on or after 01/01/2021.

The interim bonus rates are applicable to policies in respect of each policy year entered upon after 31/03/2021 and result into claims by death or maturity (including those discounted within one year of maturity) or are surrendered during the period commencing from 01/01/2021 and ending 9 months from the date of next valuation.

This time, I separated the plans in two ways. One for the old policies which are closed and another list for the new policies which are currently available for purchase.

The below bonus rates are for the old plans.

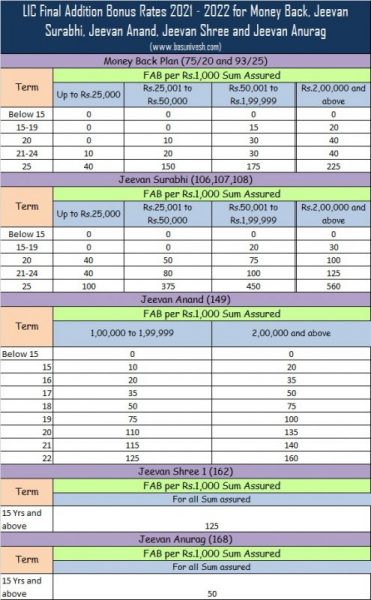

LIC Final Additional Bonus Rates – 2021- 22

As explained above, Final Addition Bonus (FAB) is a one-time additional bonus paid along with the final payment of the policy. The minimum term required for the eligibility of the Final Additional Bonus as per the current valuation is 15 years also, FAB rates increase with the increase in sum assured of the policy.

These Final (Additional) Bonuses are applicable In the case of Plans of Groups 1, 2, 8, 9, and 10 mentioned below.

- (Group 1) Whole Life type (Plans 2, 5, 6, 8, 10, 28 (Before Conversion), 35, 36, 37, 38, 49,77,78, 85 & 86)

- (Group 2) Endowment type (Plans 14, 17, 27 (After Conversion), 28 (After Conversion), 34, 39 40, 41, 42, 50, 54, 79, 80, 81, 84, 87, 90, 91, 92, 95, 101, 102, 103, 109, 110 & 121)

- (Group 8) Jeevan Mitra (Double Cover plan), Jeevan Saathi (Plans 88 & 89)

- (Group 9) Jeevan Mitra (Triple Cover Plan: Plan 133 )

- (Group 10) Limited Payment Endowment (Plan 48)

Let us now see the FAB rates for special plans where the FAB is different from the above rates.

LIC’s Jeevan Saral – Loyalty addition rates 2021-22

LIC Jeevan Saral plan was one among the popular many where many investors invested. Hence, let me share the LA rates of this plan.

LIC Bonus Rates – 2021- 22 – Is it really add value?

Look at the current and past bonus rates of LIC. They are not increasing drastically. In fact, for many policies, the bonus rate is the same for many years. Obviously because of this and no additional return on such declared bonus will erode your return part. Let me share with you one of my client’s real experiences and this seems to be the classic example of how low-yielding such policies will result in a difficult time for you in the future. I am not pointing LIC alone here. It is the case with all insurer’s products where if you invest in such endowment or money back kind of products.

Think and act wisely rather than just running behind someone’s recommendation. If you still feel such 5% or 6% returns are fantastic for your long-term wealth creation, then please go ahead and buy these products. Otherwise, you have to think seriously.

To give you more clarity on how this bonus in a traditional plan works and erodes your wealth, let me take an example. Assume that you took a traditional plan of Rs.5 lakh Sum Assured and the term is 20 years. Let us assume that the bonus rate for this plan is Rs.50 per Rs.1,000 Sum Assured. Hence, each year the insurance company will declare the bonus for your policy of Rs.25,000 (Rs.50*Rs.5,00,000/Rs.1,000). As this declared bonus will not participate in any future growth its value will depreciate with each passing year. If we assume 6% inflation rate, then the first year’s bonus of Rs.25,000 will be worth just Rs.7,715 after the 20th year. Because as it is not earning anything, its value depreciating by each year. If we consider the depreciation of such each year’s bonus, then the same can be graphed as below.

At the policy tenure end, you feel that the insurance company giving you Rs.5,00,000 as a bonus (Rs.25,000*20). However, due to inflation of around 6% and its zero return on each year’s such bonus, it will be just around Rs.2,95,782 (sum of each year’s final value on 20th-year post 6% depreciation). The final difference between the total bonus to the depreciation value due to inflation is a whopping of around 40%. Due to low yielding nature, such products are not suitable for your long-term wealth creation.

Hence, whether it is LIC or some other insurers, never combine your insurance with investment and think of real returns than the plain return numbers.

This man is against LIC policies and support of MF don’t believe his explanations and surrender the insurance plans you will lose money and risk cover which protects your income for your family in emergency and no other instruments like MF ,shares FD’s give those benefits!

Dear Damodar,

By staying against LIC and supporting MF, I will not get a single penny 🙂 However, it looks like you have conflict of interest when you are saying don’t stop the LIC policies.

Dear Sir

I have Bima Gold Policy – 174. It is SA for 15 lacs and for 20 years. Can you suggest what is the LA rate for this?

Dear Subinoy,

The latest LA for this plan for the mentioned term is Rs.150 per Rs.1,000 SA.

So where to invest with no risk of loss, an regular investment plan wherein it can beat inflation with Guranteed returns.

Dear Chetan,

Frist be realistic with your expectation.

Sir i purchased Jeevan umang and paid 2 premium so far, i felt the return is not more than 4.5 percent . My premium is 1.25lakh/15yrs and sum assured is 15lakh. Is my calculations right sum assured+ bonus + final addition is less than 5percent after 30yrs. Is it worth to continue or pay another term and make it paid up and switch to mutual funds?

My aim is wealth creation.

Dear Vivekananda,

It is hard for me to say that better you forget of what you paid rather than paying one more premium and get less than what you paid. But this is the hard truth.

Respected Sir

I took Jeevan Anand 2 policy each 40 lakh sum assured at age 34 with term of 35. I have to pay around 2.5 lakh premium annually now. What can I do now?

Dear Akshayy,

Depends on when you purchased it.

Dear Sir,

I have taken Jeevan Saral 165 plan from LIC since 2013. Paying monthly around 6K as premium. Should I continue to invest or hold for some more time.? Please advice.

Dear Ganesh,

Continue for another one year and once it completes 10 years, then surrender it.

Hi Sir,

Many thanks for your post. I am having LIC Endowment plan 814 from 2015 onwards. Premium is Rs 4218 per month, Sum Insured is Rs 10 lakh and term is 20 years. I’ve paid premium now for 7 years. Is it advisable to stop now and make this like a paid up policy or continue the policy. For insurance purposes I’ve taken another term insurance now. Request your valuable opinion.

Dear Bharat,

Better convert to paid up.

Final additional bonus termed as FAB is very high for more than 20 years of policies please mention all details. Some policies after maturity gives you more than sum assured as Final additional bonus .some have life time insurance after maturity.

Dear Anil,

What matters to investors is WHEN they give this FAB than how much. I hope you understand the concept of time value of money.

Hello sir, what is current loyalty rate for Jeevan Shree plan 112? The maturity date is sept, 2026 and the sum assured is 500000. Insurance term is 25 and premium term is 16. All premium completed. How much loyalty should I expect beside the sum assured 500000 and guaranteed addition 937500?

Hello Basu Sir,

I’m investing 3062 per month in Jeevan Saral 165 since 2010 when I was 21 years old, took the policy for 35 years, maturity in 2045. There’s no Loyalty Bonus for 35 year term? What should I do? Should I continue or surrender.

Dear Kabir,

As you completed more than 10 years, better to close it. LA is available for your policy.

What about Bhima Gold , table no 174 Loyality addition

Dear Kripa,

It is Rs.130.

Hello Sir, what is loyalty addition rate of LIC New Bima Gold (179), term 16 years?

Dear Prithi,

As it is a new policy, as of now LIC not declared LA.

Hello Sir, when will LIC declare loyalty addition rate of LIC New Bima Gold (179), term 16 years?

Any Guess work on how much it is going to be.

Best Regards

Dear Syam,

Let us wait.

Hi Mr Basu / Mr Prithi , Now that I reckon that 16 yrs should have been completed, would you share some insight about the LA for the policy. Any inputs will be immensely helpful in planning.

Dear Tej,

Refer my latest posts in this regard. I have already shared.

I have Jeevan saral where my 10 years are getting completed on 15th Dec 2021. i feel I will withdraw as not getting good returns.. would u know how much loyalty addition I will get as 10 yrs completed and what would be the amount I get …my monthly premium is 10208 rs for 25 l sum assured..there is additional 25 l of accident insurance

Dear Akash,

Yes, better to surrender. Regarding the LA rate, refer above post.

Dear Mr Basu,

Thanks for this greaet informatiom. I want to understand what would be the maturity amount for Jeevan Shree 112 policy with Sum assured 5L, payment term of 16 years and maturity of 25 years. I am not sure if Final Addition Bonus and Loyalty Bonuses are applicable here.

Dear Kanv,

Please refer above post and you can easily calculate it.

Dear Sir,

What is the bonus for the lic policy 113?

My policy matures this here

Dear Shalin,

You can check the same easily on LIC website by login.

Thank you sir…guess you are suggesting should I just leave it till end of term or surrender after 2-3 yrs. Please advice

Dear Ramesh,

Better opt for Paid Up (leave it till maturity without further premium payment).

Dear Sir

Had invested two Jeevan Tarun policy for my 2 kids in 2016 – had paid 3 yrs and later stopped due to some circumstances.

1) Son – 10yrs – Premium Rs 49962/- 2) Daughter – 5 yrs – Premium Rs 31997 (both with PWB rider) now am in dilemma (a) Should I continue or (b) surrender and invest in mutual fund. Kindly advice

Dear Ramesh,

Better to stop the premium payment and let the policy be in paid-up mode.

Dear Sir , What is the LA of Jeevan shree Plan 112 for 2021-22 ? You mentioned LA of only Jeevan Saral not for Jeevan Shree.

Dear Abhishek,

May I know your policy’s term?

Dear Sir, Policy term is of 20 year.

Dear Abhishek,

It is Rs.550.

Dear Sir,

My father has 3 policies that will expire in September 2023. Only 1 more premium is left in 2022. Then it will mature. So, should I wait for the maturity (which is just 2 years left) or surrender it?

Dear Ankur,

Better to wait till maturity.

Dear sir, I have a lic jeevan shree(plan 112)(20 y) policy maturing on Feb 2022. Is the current Loyalty addition rates declared applicable on my policy?

Dear Shreyasg,

Yes.