LIC Bachat Plus (Plan No.861) is available from 15th March 2021 and available for sale online as well as offline for a maximum period of 180 days.

LIC‘s Bachat Plus plan is a Non-Linked, Participating, Individual Life Assurance Savings plan. Under this plan, the premium can be paid either as Lumpsum (Single Premium) or as Limited Premium with a Premium Payment Term of 5 years. Under each of these premium payment options the proposer will have two options to choose “Sum Assured on Death”.

As I said above, the plan is available online and offline also.

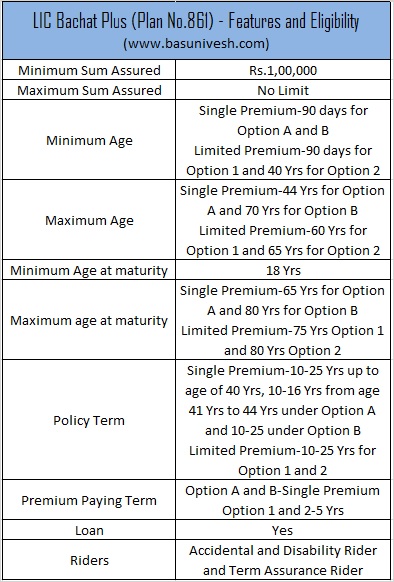

LIC Bachat Plus (Plan No.861) – Features and Eligibility

Let us see the features and eligibility for LIC Bachat Plus plan.

LIC Bachat Plus (Plan No.861) – Benefits

Let us now look into the benefits of LIC Bachat Plus Plan.

a) Maturity Benefit

If the Life Assured survived till the maturity of the policy, he will receive Sum Assured at maturity and Loyalty Addition (LA) is payable. Here, sum assured at maturity means basic sum assured.

Note that LA is not payabe if you convert your policy to paid up.

b) Death Benefit

Here, the sum assured on death benefits can be available to choose for the policyholder at the time of buying the policy. The premium and benefits will vary based on the option you choose here. The benefits are as below.

Death benefits along with the above sum assured on death benefits are as below:-

a) Death during the first 5 years-

If death occurs before the commencement of risk, LIC will refund the premium without any interest.

If death occurs after the commencement of risk, then LIC will pay the nominee Sum Assured on Death.

b) Death after 5 years but before the maturity-

Sum Assured on Death+Loyalty Addition.

Other featurs of LIC Bachat Plus (Plan No.861)

1) Settlement Option for maturity-Under this, one can receive the paid-up as well as maturity benefits in installments like 5 yrs, 10 years or 15 years.

2) Settlement Option for death-Under this, nominee can receive the death benefits as installements for 5 yrs, 10 years or 15 years.

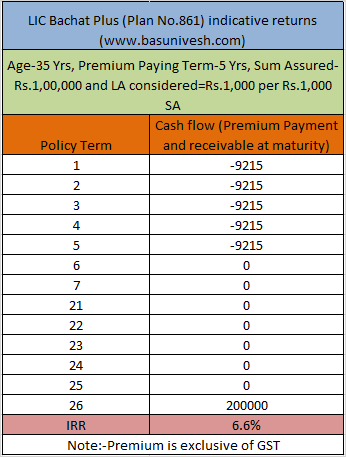

LIC Bachat Plus ( Plan No.861) – Should you invest?

Let me take an example. I have taken an example of Age-35 Yrs, PPT-5 Yrs, Sum Assured-Rs.1,00,000, Policy Period-25 Yrs, LA Rate-Rs.1,000 per Rs.1,000 Sum Assured.

Considering the current LIC bonus or LA trend, and assuming the highest LA rates, you noticed that the returns are around 6.6%. Do remember that I have not considered the GST Tax. If you consider GST, then returns may be lesser than 6.6%.

Hence, if you feel by investing around 25 years and looks 6.6% is FANTASTIC returns, then go ahead. However, if you are looking for real returns (returns beating the inflation), then stay away from this product.

Dear Basu Sir,

is this plan better than Recurring Deposit scheme? because, interest rates are falling and postal RD is 5.5% now. Can this be considered as an alternative to RD?

Thank you sir,

Dear Rajesh,

Use RD for short-term goal accumulation. Don’t use RD or such LIC plans for your long term goals.

Hi Sir ,

Kindly explain the surrender value for 25 years policy with example

Regards ,

Nagaraj

Dear Nagaraj,

Values changes and I can’t give example to each individual.

Sir,

I think you are only analyzing this plan.But any one who wish to buy this plan you are discouraging him with your comments. It seems you have made up your kind first and the have analyzed this plan.

Surprising.

Dear Milind,

If I am wrong, then please correct me with valid points. I am ready to accept it.

Does medical require for 59 years business women in 861 plan 5 years ppt

Dear Jeetender,

I think YES. But check with the concerned branch.

Sir

Don’t you think that considering L.A. of 1000/- per thousand is too high, projecting it for next 25 years, considering various economic scenarios. I feel that L.A. of 500/- per thousand would also be on higher side, considering LIC’S investments patterns in various instruments as on today and in future., if we consider L.A. of 500/- per thousand it would work out to 3.3% , of course on this platform we cant project and predict what would be the L.A. scenario going ahead for next 25 years, but a fair estimate will definately help us to derive at calculations.,

Dear Ramachandra,

My point of considering higher LA is to show that even after such exaggerated considerations, returns are not so great 🙂

Good discussion also informative about Lic return on current Bachat Plus plan

Dear Dipu,

My pleasure 🙂

Dear sir

I want to know that. This policy is are stand alone policy or not

Dear Chaturbhuji,

Yes, it is a standard and standalone policy.

Why so much wrong information in the comments and author of the blog is not clarifying clearly?

I took the policy last week. For 10 lk investments returns are 16.5lks guaranteed and LA.. so expecting about 17.5 lks after 10 years. This works out to be about 6.6%

BUT THIS DOES GOT GIVE 10 times life coverage. It will be 1.25 times your premium which is about 13.5 lks life coverage..

I feel it’s a good debt plan and surplus money can be kept in this after post office plans, ppf, kvp, nsc and 7.15% floating bonds…

Dear Santosh,

If you feel 6.6% is the BEST returns then go ahead. None can hold you 🙂

Hello Sir,

It seems LIC has introduced this limited period product to make up for comparatively lower FPI this year. It will directly compete with Bank FD and RD where rates are going down over the years. In that case return of 6.6% looks attractive.

But how did you arrive at LA of 1000??? Isn’t it on a higher side??

Dear Ritesh,

It is the habit of LIC to launch such limited period offers (product) during tax-saving period. No surprising in this 🙂 I assumed the highest LA rate of Rs.1,000. Hence, don’t think 6.6% is what you get. In my view, it is less than that.

Hi,

What is the Loyalty Bonus trend of LIC from their past products for a term of 10 Years? From your blogs, I can see that you have good statistics of LIC Plans, if not the private insurers. Kindly share. I am looking for various debt investment options.

Dear Ram,

Check the article related to LIC Bonus.

Thanks for the information Mr.Basavaraj. I checked the loyalty additions information from your blog for year 2020-21. In Jeevan Saral, the loyalty addition for 10 years for annual premium more than 50,000 was Rs.475. Since Bachat Plus is single premium, the loyalty could be different. If I invest Rs.50LAKHS, I get a sum assured of 69.50 Lakhs (Thanks to Smart LIC App). With assumed loyalty bonus of Rs.350 per 1000 Sum, the bonus amount is 24.325 Lakhs and the maturity is 93.825Lakhs. The returns rate is coming out to be 6.75%. Is it not a good one if not great? I know ‘good’ is a very subjective term. Your capital ‘GOOD’ is different from my ‘good’. But with 5 Crores insurance cover and tax-free 6.75%, can it not be considered is the question?

Am I assuming a high loyalty bonus, though I have assumed way less than what statistics you have shown in your blog? Kindly guide me.

Dear Ram,

With HIGHEST expectation itself the returns are around 6.6% (excluding the tax). Hence, don’t assume any 8th wonder from this product.

Hi,

Why is it 6.6% excluding tax? If the life insurance cover is 10 times or more than the invested amount, then is the maturity not tax-free? Again, 6.6% as you have mentioned may be the HIGHEST but is it not good enough considering it is debt. We cannot compare it to equity returns. But I am talking from a conservative investor point of view. Because, if I invest the same 50Lakhs in best of Debt Mutual Funds (with high credit rating) which might give me 9% p.a. returns, I might end up getting only 5% returns considering the long-term capital gains tax post inflation-indexation. And, I do not get any life cover too. I am not expecting any 8th wonder. But let me know where am I wrong in calculating.

Dear Ram,

SIR JI, when I said excluding tax, I meant about GST not the tax-free returns that you get either at maturity or death 🙂 Who is comparing this product with equity or debt mutual funds?? So as per you if the total returns from debt funds is 9%, then post tax returns after indexation benefit at 5%? Can you elaborate more how the indexation benefit and 20% tax on debt fund took away 4% returns?

We get 5% post-tax returns if we do a huge human calculation error 🙂 Thanks for pointing it out. Still, not a FANTASTIC or HIGHEST or any other “CAPITAL” letter adjective Return, but considerable debt product return. Not for 25 Years like you have taken as an example in your blog. The readers would have been happy if you had mentioned this as a considerable option for a debt basket for a 10 Year period to park a surplus just to give a neutral viewpoint.

Dear Ram,

Is it wise when you say consider as debt part? What if one need to rebalance the portfolio once in a while?

Sir i have bought 5 lacs insurance & term limited primium term 25 yrs so whats is maturity at 25 yrs

Dear Imran,

Please calculate like how I calculated above (using excel).

Helpful information

In which policy does LIC pay highest IRR?

Dear Rushit,

As per you, what do you mean by HIGHEST?

Thank you so much for sharing such useful information on LIC. I never knew LIC has such a wonderful product which gives 6.6% return, 10 times insurance cover and tax-free return. I plan to invest 1 crore in my name and my spouse. I am also planning the same for kids age 5, and 9, each Rs.75 Lakhs. Kindly guide me how to go ahead with this plan. Is there nay last date?

Dear Naresh,

WONDERFUL PRODUCT???? I have considered the highest LA rate and excluded the GST you pay with premium. Hence, its looking at 6.6% returns for you. Otherwise, it is below 6%. However, if you feel this 6.6% (which is not sure and below 6% in reality), is the BEST returns, then go ahead and buy NOW!!