What is the latest Post Office Interest Rates April-June 2020? What are the latest Post Office interest rates on FDs, MIS, SCSS, NSC, KVP, PPF and SSY Schemes?

Earlier the interest rates used to be announced yearly once. However, from 2016-17, the rate of interest will be fixed on a quarterly basis. I already wrote a detailed post on this. I am providing the links to those earlier posts below.

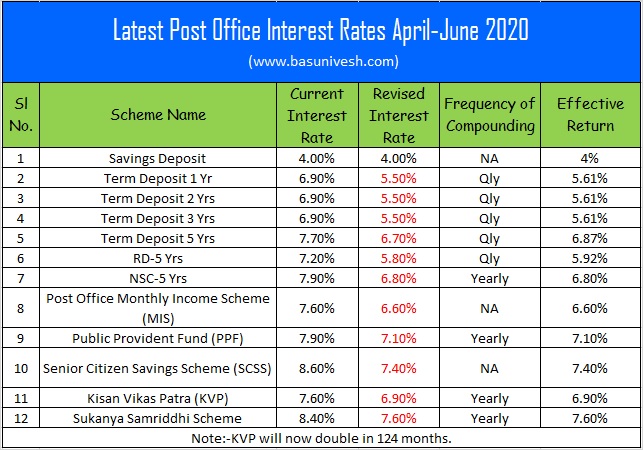

Below is the timetable for change in interest rates for all Post Office Savings Schemes.

As per the schedule, Government announced the interest rate applicable to all Post Office Savings Schemes from 1st April 2020 to 30th June 2020.

Latest Post Office Interest Rates April-June 2020

Ministry of Finance notified the applicable latest Post Office Interest Rates April-June 2020.

Just to quickly recap, since two quarters the Government unchanged the interest of all Post Office Small Saving Schemes Interest Rates.

You notice that there is a huge fall in the interest rates of all Post Office Saving Schemes. This is really a shocking to all those who are completely relying on Post Office Saving Schemes.

The trend of Post Office Interest Rates from April 2019 to April 2020

Below is the interest rate trend of last one year.

Features of Post Office Savings Schemes

# Post Office Savings Account

Like Bank Account, Post Office also offers you the savings account to its customers. The few features are as below.

- Minimum Rs.500 is required to open the account.

- Account can be opened single, jointly, Minor (above 10 years of age) or a guardian on behalf of minor.

- Minimum balance to be maintained in an account is INR 500/- , if balance Rs. 500 not maintained, a maintenance fee of one hundred (100) rupees shall be deducted from the account on the last working day of each financial year and after deduction of the account maintenance fee, if the balance in the account becomes nil, the account shall stand automatically closed.

- Cheque facility/ATM facility are available

- Interest earned is Tax Free up to INR 10,000/- per year from financial year 2012-13

- Account can be transferred from one post office to another

- One account can be opened in one post office.

- At least one transaction of deposit or withdrawal in three financial years is necessary to keep the account active, else account became silent (Dorment).

- Intra Operable Netbanking/Mobile Banking facility is available.

- Online Fund transfer between Post Office Savings Accounts/Stop Cheque/Transaction View facility is available through Intra Operable Netbanking/Mobile Banking.

- Facility to link with IPPB Saving Account is available.

- Funds Transfer (Sweep in/Sweep out) facility is available with IPPB Saving Account.

# Post Office Fixed Deposits (FDs)

- Minimum of Rs.1,000 and in multiples of Rs.100. There is no maximum limit.

- FD tenure currently available are 1 yr, 2 Yrs, 3 Yrs and 5 Yrs.

- Account can be opened single, jointly, Minor (above 10 years of age) or a guardian on behalf of minor.

- Account can be opened by cash /Cheque and in case of Cheque the date of realization of cheque in Govt. account shall be date of opening of account.

- Account can be transferred from one post office to another

- Single account can be converted into Joint and Vice Versa .

- Any number of accounts can be opened in any post office.

- Interest shall be payable annually, No additional interest shall be payable on the amount of interest that has become due for payment but not withdrawn by the account holder.

- The annual interest may be credited to the savings account of the account holder at his option.

- Premature encashment not allowed before expiry of 6 month, If closed between 6 month to 12 month from date of Opening, Post Office Saving Accounts interest rate will be payable.

- 5 Yrs FD is eligible for tax saving purposes under Sec.80C.

# Post Office Recurring Deposit (RD)

- Minimum is Rs.100 a month and in multiple of Rs.10. There is no maximum limit.

- Account can be opened single, jointly, Minor (above 10 years of age) or a guardian on behalf of minor.

- Tenure of RD is 5 years.

- Account can be opened by cash / Cheque and in case of Cheque the date of deposit shall be date of clearance of Cheque.

- Premature closure is allowed after three years from the date of opening of the account.

- Account can be transferred from one Post Office to another Post Office.

- Subsequent deposit can be made up to 15th day of next month if account is opened up to 15th of a calendar month and up to last working day of next month if account is opened between 16th day and last working day of a calendar month.

- If subsequent deposit is not made up to the prescribed day, a default fee is charged for each default, default fee @ 1 Rs for every 100 rupee shall be charged. After 4 regular defaults, the account becomes discontinued and can be revived in two months but if the same is not revived within this period, no further deposit can be made.

- If in any RD account, there is monthly default amount , the depositor has to first pay the defaulted monthly deposit with default fee and then pay the current month deposit.

- There is rebate on advance deposit of at least 6 installments, Rs. 10 for 6 month and Rs. 40 for 12 months Rebate will be paid for denomination of Rs. 100.

- One loan up to 50% of the balance allowed after one year. It may be repaid in one lumpsum along with interest at the prescribed rate at any time during the currency of the account.

- Account can be extended for another 5 years after it’s maturity.

# Post Office Monthly Income Scheme (MIS)

- Maximum investment is Rs.4.5 lakh in a single account and Rs.9 lakh jointly.

- Account can be opened single, jointly, Minor (above 10 years of age) or a guardian on behalf of minor.

- Any number of accounts can be opened in any post office subject to maximum investment limit by adding balance in all accounts (Rs. 4.5 Lakh).

- Single account can be converted into Joint and Vice Versa.

- Maturity period is 5 years.

- Interest can be drawn through auto credit into savings account standing at same post office,orECS./In case of MIS accounts standing at CBS Post offices, monthly interest can be credited into savings account standing at any CBS Post offices.

- Can be prematurely en-cashed after one year but before 3 years at the discount of 2% of the deposit and after 3 years at the discount of 1% of the deposit. (Discount means deduction from the deposit.).

- Interest shall be payable to the account holder on completion of a month from the date of deposit.

- If the interest payable every month is not claimed by the account holder such interest shall not earn any additional interest.

# Post Office Senior Citizen Savings Scheme (SCSS)

I have written a detailed post on this. Refer the same at ” Post Office Senior Citizen Scheme (SCSS)-Benefits and Interest Rate“.

# Public Provident Fund (PPF)

I have written various posts on PPF. Refer the same:-

- PPF (Public Provident Fund) Scheme 2019 – 5 Important Changes

- PPF Investment and Deposit Rules – Beware your Banks are unaware of it!

- Online deposit in Post Office PPF, Sukanya Samridhi, RD – How to do?

- PPF Account for Minor and Wife – Rules, Tax Benefits and Tricks

- Premature closure of PPF account – New Rules 2016

- PPF withdrawal rules & options after 15 years maturity

- All about Public Provident Fund (PPF)

- PPF-Loan and Withdrawal

- PPF-When to contribute to get higher returns?

# National Savings Certificate NSC (VIII Issue)

- Minimum Rs.1,000 and in multiple of Rs.100.

- No maximum limit.

- Account can be opened single, jointly, Minor (above 10 years of age) or a guardian on behalf of minor.

- Tax Benefit under Sec.80C is available.

- Tenure is 5 years.

# Kisan Vikas Patra (KVP) Account

- Minimum Rs.1,000 and in multiples of Rs.100. There is no maximum limit.

- Account can be opened single, jointly, Minor (above 10 years of age) or a guardian on behalf of minor.

- The money will be double at maturity. However, as the interest rate changes on a quarterly basis. The maturity period also varies once in a quarter.

# Sukanya Samriddhi Account Yojana (SSY)

I have written various posts on this. Refer the same:-

- Sukanya Samriddhi Account-An investment scheme for your girl child

- Difference of Sukanya Samriddhi Account Vs PPF (With Tax Benefits)

- Sukanya Samriddhi Account -When to invest to earn more returns?

- 5 unknown facts about Sukanya Samriddhi Yojana (Account) Rules

- Online deposit in Post Office PPF, Sukanya Samridhi, RD – How to do?

Sir,

I am an NRI aged 65 years and now Im returning back to my country. Please advise the safest investment for me to have a regular monthly income for my living.

Regards,

Salman

Dear Salman,

It is hard for me to suggest anything blindly.

sir

what about Tamil Nadu power finance fd scheme 2020 ? is this good bet to invest as this is 100% govt product.

pls advise on this and comment pls

Dear Ankita,

You may try if the requirements are matching with bond features like time horizon, taxation and liquidity.

Dear sir, please take my heartly salute, please tell me about sip,is there any market risk to invest in sip.

Dear Ramachandra,

SIP is the way of investment. Risk depends on in which asset class or product you invest.

Is post office cheque book issued to its customer is valid for bank clearing house?

Dear Siddhartha,

Yes.

w.e.f April 2020 it is not better to invest in Post Office Schemes as they are giving less interest compared to Pvt.bank.Investment up to rs. five lac are insured in the banks, & giving more than 1% of interest. Then why go to the Post office where work is done very slowly. Preference is given to post office Agents. Am I right. Lastly, the checkbook issued by the Post office to its customer not is Valid in banks clearing House .

Dear Vipan,

In Banks, up to Rs.5 lakh is secured. Here, the whole amount 🙂 If you are ready to take 1% risk, then please go ahead.

Sir bank gives upto 5% & post office upto 6.6%

Dear Rajinder,

Choose which is better for you. Post Office is more safer.

Sir

I want to do FD rs 16 lakh, which was matured on 20th march 2020 in state bank of india. My father has invested the amount three years ago.

Now my father has expired on 8th january 2018. He was a professor of history in university. So plz kindly suggest me where it is to invested

in SBI bank or post office. I want to FD for 1 year. shall i invest it lump sum or break up the money. Finally my question is that which is better

bank or post office

Dear Siddhartha,

Go with Post Office and break into 2 lakh each FD.

Sir

why are you my question answer properly i can’t understand that.

Dear Siddhartha,

What part of my answer is not understood by you?

Sir,

i want to do FD rs 16 lakh. but i can’t understand where to invest it bank or in postoffice. Plz suggest me

rs 16 lakh shall i invest in lump sum or split the amount, if split the amount then what should it be?

Dear Siddhartha,

What is your requirement?

Respected

Sir

I want to TD in post office for 5 years of rs 13-14 lakh.

So Kindly suggest me it is suitable for me. My current age is

now 45 years.

Dear Siddhartha,

How can I say your suitability without knowing your financial life?

I had given cheque and it got claered before 23rd March 2020. but due to lockdown post office could not done the investment. So at what rate will i get:? Will i get at old rate or new rate?

Dear Shilpi,

If they realized the money on 23rd or before 1st April, then they have to give you as per the old rates.

Sir,

I had deposited the cheque and filled up the required form around 11th march 2020 . but due to post office’s technical issue they delayed in realizing my cheque and they realized it on 23rd April and it got credited in my SB account on 24th april,2020. But the new rate is effective from April. What rate they will provide me? Though it is not my fault. Due to post office’s technical issue they could not realize my cheque for clearance.

Dear Shilpi,

Sadly it is the new rates applicable from 1st April 2020.

Hi sir good morning my self Damodar.

Sir, i want to do FD/MIS in post office/SBI. My question is the interest rate will be applicable fixed throughout the year/maturity date or changed quaterly if increase/decrease.

And interest will be credited quaterly or annually…

Dear Damodar,

For Post Office FDs, MIS and SCSS, the interest is fixed. The applicable interest rate is the one that is there at the time of account opening.

Sir, I have completed my investments for FY 2019-20 as under: Rs.1,50,000/- in PPF and Rs.50,000/- in NPS under Sec 80 CCD (1B). I would now like to invest the same for the FY 2020-21. i.e; Rs.1,50,000/- in PPF and Rs.50,000/- in NPS under Sec 80 CCD (1B). Can I invest the same before June 2020 or should wait and invest it after July 2020? Please advice.

Dear Vasavan,

If your Sec.80C limit is fulfilled for FY 2019-20, then why this JUNE waiting?

Sir, I deliberately said July 2020 for investing for FY 2020-21 because if I invest before June 2020 I am afraid whether they will consider it for FY 2019-20 which I have already fulfilled. Otherwise I have no issue in investing before June 2020 for FY 2020-21. Can I invest before June 2020. Please advice.

Dear Vasavan,

For taxation purposes, it is YOUR CHOICE to consider either for the last FY or current FY. For product features, there is no change in limits or period.

Hi,

What about RPLI interests?

Dear Karkera,

PLI is an Insurance product, not investment product. Hence, don’t compare those.PLI returns varies based on the bonus Post Office declare.

Dear Sir, If I invest in PPF today, then it will be considered in FY 2020-2021 or in 2019-2020?

Dear Kapil,

Obviously it is considered for FY 2020-21.

Dear Sir, I suppose the revised interest are applicable for any new / fresh deposits from 01st Apr’20 & not for deposits prior to 01st Apr’20 .

Also, does this interest rate change effective from 01st Apr’20 be applicable to RBI bonds too ?

Please clarify both above points .

Thanks & best regards

Chandrashekar.K

Dear Chandrashekar,

If you already invested in products like SCSS, MIS, Fixed Deposits, NSC or KVP, the old rates will continue. However, any fresh investments in SCSS, MIS, FDs or KVP will attract the new interest rates. Also for the products like PPF and SSY, the rate change will affect for this quarter. RBI Bond is a different product which will not come under Post Office.

Thank you for the valuable information, sir

Sir,

In case of Point 1(# Post Office Savings Account), below features are not available as per my experience/understanding.

•Intra Operable Netbanking/Mobile Banking facility is available.

•Online Fund transfer between Post Office Savings Accounts/Stop Cheque/Transaction View facility is available through Intra Operable Netbanking/Mobile Banking.

Dear Krishan,

I think you have apply personally to use those features. In terms of service, Post Office is still living in 1947.