What are the new online EPF advance rules 2020? Due to Coronavirus outbreak, EPFO offering the advance of 3 months wages or 75% of EPF balance. Let us see the procedure and who are eligible for this withdrawal.

New online EPF Advance Rules 2020 -Features

- All the employees who are contributing to EPF are eligible to avail this advance.

- It is NON-REFUNDABLE ADVANCE.

- As Coronavirus is declared as Pandemic by the Appropriate Government for the entire country, all the EPF contributors are eligible for this withdrawal.

- You no need to submit any documents or certificates for this advance withdrawal.

- You can get non-refundable withdrawal to the extent of the Basic+DA for three months or up to 75% of the amount standing to your credit in the EPF account, whichever is less. Since withdrawal is non-refundable, there is no requirement to refund the amount.

- Suppose your Basic+DA per month is Rs.15,000 and your EPF balance is 40,000, then you will get 75% of Rs.40,000 i.e Rs.30,000. Because your three months Basic+DA is more than Rs.40,000 (Rs.45,000). The condition of whichever is LESS applies here.

New online EPF Advance Rules 2020 – How to take advance of 3 months wages or 75% of EPF?

Now let us see how to avail this advance online using UAN portal.

Step 1-Visit the EPFO UAN Member Portal. Login to your UAN portal with your User Name and Password.

Step 2-Under the “Online Services”, select the dropdown of Claim (FORM-31,19,10C&10D).

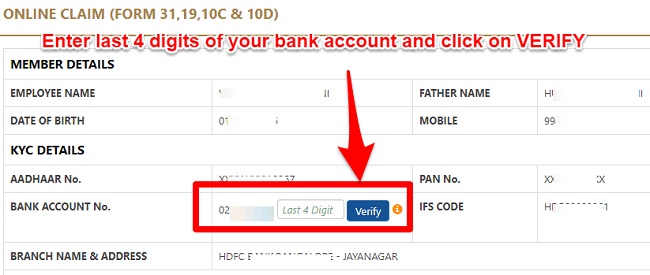

Step 3:-Here, you have to enter your Bank Account’s last four digits and click on the tab VERIFY. Then click on “Proceed for Online Claim”.

Step 4-Select drop down of “I want to apply for “ and select ‘PF Advance (Form 31)’.

Step 5-You will find many options here. However, select purpose as “Outbreak of pandemic (COVID-19)” from the drop down.

Step 6- Enter the amount required and Upload a scanned copy of the cheque/Passbook and enter your address. Then click on “Get Aadhaar OTP”. Enter the OTP received on Aadhaar linked mobile. That’s it. Your claim is submitted.

Let me know if you have doubts in availing this EPF Advance.

Conclusion:- Is it wise to withdraw this advance? Your EPF is meant for your retirement goal. It is a wonderful debt product of your retirement portfolio. Hence, even though the Government is offering by considering the difficulty many are facing, I strongly suggest you not to touch your EPF.

Only if all other options of managing your money fail, then as a last option touch EPF. But never disturb this wonderful long term tax free yearly compounding product just for the sake of few months of difficulty.

- EPF Scheme 2026: EPF, EPS and EDLI Rules Explained Fully

- Financial Freedom Without Health? You’ll Regret It Later

- The Peltzman Effect: Why Playing It Safe Can Make You Poor

- Your Retirement Success Depends on Luck, Not Skill

- Never Compare Nifty 50 Index Funds Vs Active Large Cap Funds!

- Nifty 500 Multicap 50:25:25 vs Nifty 500: Which Is Best?

Hello, This is Arun, I want to withdraw my EPF amount during covid-19 pandemic. Is there any interest for this amount. Please let me know.

Dear Arun,

There is no interest on this advance.

Hii, I am Bhavika Kakkad. I have served from 1/12/2015 to 31/05/2017. When I apply for 10 c it shows rejected on the clause that either short service or not eligible… i want to know the exact reason for such..

Dear Bhavika,

Whether you are requesting for withdrawal for above-shared reason?

Very patient and detailed article. Thank you!

Dear Poonam,

Pleasure 🙂

I am getting AADHAAR is not authenticated from UIDAI. Please authenticate your AADHAAR by visiting the nearest EPFO office. How can I make a withdrawal

Dear Chera,

Follow as they suggested.

Hai.

I withdraw a amount from the PF in last November 2019. am i eligible for the 75% withdrawl

Dear Rahulpr,

If you withdraw and there is no balance, then how you will be eligible?

Hi Basu,

I do VPF too. Where I can track the VPF amount? is it the same EPF passbook? EPF and VPF have different rate of interest, so I believe we should have a separate tracker for it.

Dear Balaji,

EPF Passbook also considers the VPF. Hence, there is no separate interest rate or passbook.

There is 3 colum in passbook 1.Employer share, 2.employee share, 3.pension contribute.

My question is will i get 75% from this three contribution or I Will get only from employee and employer share only.. How long ii take for settlement

Dear Basha,

You will get advance ONLY from EPF but not from EPS.

Hi Basu

Will this policy applies to PPF too?

When I see last few month’s statements are really scary n disappointing with regards to my SIP’s!

All my SiP’s were started from 2nd anniversary of Basu nivesh

With your advice n interaction.

Please advice what should I do

Is it ok if we withdraw but continue with sip or just continue with dwindling accumulated corpus?

Dear Saleem,

This rule is only for EPF. Regarding the investments, whether you did the yearly asset allocation with respect to equity and debt? Whether you followed the changes as and when I wrote on yearly basis?

Yes it was a good mix of equity n debt I sticked to only three funds and was yearly updated list followed ,Even when fund didn’t make to your yearly list then still sought your advice and then continued till now

Returns were attractive n I was satisfied very much…

But now suddenly changed world wide phenomena funds are taking hit…

Franklin India equity,Franklin ultra short n HDFC hybrid are my three funds

Dear Saleem,

I have not suggested Franklin India Equity. Regarding debt funds, due to the ongoing default or downgrade issues, better to stick to Liquid Funds. Regarding Hybrid Fund, it’s better to continue.