Latest IRDA Claim Settlement Ratio 2022 was released on 22nd December 2021. Which is the best Life Insurance Company in 2022 (based on claim settlement ratio)? The majority of Life Insurance Companies nowadays lure buyers based on the IRDA Life Insurance Claim Settlement Ratio. However, is it the right data to look into?

What is the meaning of Claim Settlement Ratio?

Claim Settlement Ratio is the indicator of how many death claims Life Insurance Company settled in any financial year. It is calculated as the total number of claims received against the total number of claims settled. Let us say, Life Insurance Company received 100 claims and among those, it settled 98, then the claim settlement ratio is said to be 98%. The remaining 2% claims the Life Insurance Company rejected.

Based on this, we can easily assume how customer-friendly they are in dealing with death claims. However, I warn you that this claim settlement ratio is raw data.

It will not give you a clear picture of what types of products they settled. They may be Endowment plans, ULIPs, or Term Insurance Plans. Hence, this is not the sole criterion in judging the performance of a life insurance company.

More than that we don’t know for what reasons the insurance company rejected the claims.

Latest IRDA Claim Settlement Ratio 2022

Below is the IRDA Claim Settlement Ratio 2020-21 or up to 31st March, 2021. Few points to notice from this Annual Report are as below.

# Claim settlement ratio of LIC was at 98.62%% as at March 31, 2021, when compared to 96.69% as at March 31, 2020. The proportion of repudiations has decreased to 0.1% in 2020-21 compared to that of 1.9% in the previous year.

# For private insurers, the settlement ratio had increased to 97.2% during 2020-21 when compared to 97.18% during the previous year. The proportion of repudiations came down to 2% in the year 2020-21 when compared to that of 2.5% in the previous year.

# The industry’s settlement ratio increased to 98.39% in 2020-21 from 96.76% in 2019-20 and the repudiation ratio decreased to 1.14% compared to that of 1.28% in 2019-20.

# Women comprise roughly 49% of the total population in India. However, policies issues on women stand for 33% of the total policies issued.

# Claims of Life Insurers is as per the below table.

# Death Claims of Life Insurers for FY 2020-21 can be classified as below.

You noticed that compared to last year, LIC improved it’s data for this year.

# Let us see the types of complaints insurers received during last year.

The interesting thing to notice is the majority of the complaints are related to policy service, unfair business, and survival claims. However, death claims-related complaints are just around 3%.

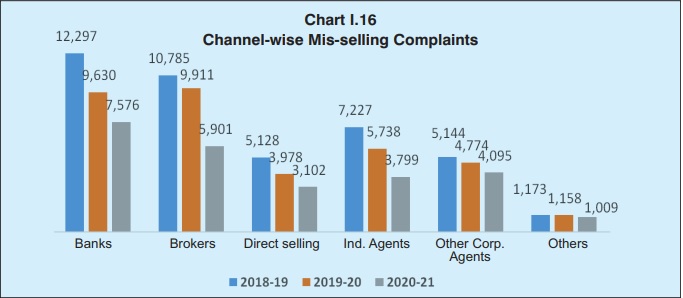

# Let us now look into the complaints side. The highest complaints about mis-selling are against the banks. Then comes the brokers. The break-up is as below. BEWARE OF BANKERS!!

# Causes of Mis-Selling are listed as below:-

a. Incorrect explanation of product features and benefits by sales person sourcing the business.

b. Incorrect premium paying term and policy term is explained to policyholder especially in cases

where regular premium paying product is sold as single premium product.

c. Policy is sold to gullible prospects assuring Loan / Bonus / Medical Benefits/ Gold coins/Mobile Towers/other benefits upon purchase of insurance policy.

d. Tampering, forgery of proposal/ other related documents.

e. High attrition rate amongst Sales team

f. Pressure on the sales person to meet sales target.

g. Free look cancellation requests are rejected by sales personnel who are not authorized to take such decisions.

h. Splitting of policies wherein multiple policies are issued to the same proposer at the same time.

i. Life Insurance policies are sold only as Tax saving/ Investment plans.

j. Sales personnel lack proper knowledge /are inadequately trained, thereby recommending unsuitable products to prospects.

k. Improper/Incorrect financial needs assessment of Prospect is done while sourcing the policy by the sales personnel.

l. Charges under the policy and lock in period are not properly explained while sale of Unit Linked Insurance Policies.

m. Churning of policies.

n. Contact numbers updated on the proposals are tampered, which restricts the success of the pre-issuance verification calls.

o. Lack of awareness on insurance on the policyholder’s part thus being misled into buying the insurance policy.

p. Policyholders failing to cross-check details.

q. Financial Problems/incapacity of the policyholder to pay future premiums.

r. Bundling and making it conditional for availing bank services.

s. Sale without proper consent of customer t. Insurance is sold to clients who were not present in India at the time of sourcing along with premium being funded without customer consent through bank accounts held with the bank.

u. Instigation by employees, advisor, channel partners, others who are no longer sourcing new business for the insurer.

I am sharing these reasons mainly to make you aware of the ways mis-selling may happen in the Life Insurance space.

Let me share you now the latest IRDA Claim Settlement Ratio 2022.

You noticed that 14 out of 25 companies have a claim settlement ratio of more than 98%.

Average Claim Settlement Amount of Life Insurance Companies in 2020-21

It is hard to find what type of products these insurers settled. Hence, I always try to look into the average claim settlement amount of these insurers. Even though it may not give us a clear picture, but a better indicator of the types of policies they settled.

If you look at this data, then you noticed that Aegon is a topper and Sahara with LIC is at lower. LIC’s average claim settlement amount is Rs.1,95,901. It means the majority of the claims are traditional plans.

Top 5 Best Life Insurance companies in India for 2022

Based on the IRDA Claim Settlement Ratio 2020-21, which are the Top and Best Life Insurance Company in 2022? I select only five based on the above data. You may differ in my view and come up with a different set of ideas. But these are my choices.

- LIC

- HDFC Standard Life

- ICICI Pru Life

- Max Life

- Aegon

Few important points before jumping into selecting of Life Insurance Companies

# Claim Settlement Ratio is raw data

As I pointed above, the claim settlement ratio is just raw data. It will not give us the specific data. Hence, never rely on this single data alone while shortlisting the insurance company.

# Concentrate on Product rather than company

Choose the product which suits your requirement and premium affordability. Declare the facts properly. Never hide any material facts. If all these you do, then an insurance company will have to accept your claim. Never give a room of suspicious on you to reject the claim.

# Section 45 of the Insurance Act will guard YOU

According to Section 45 of Insurance Act “No policy of life insurance shall be called in question on any ground whatsoever after the expiry of three years from the date of the policy, i.e. from the date of issuance of the policy or the date of commencement of risk or the date of revival of the policy or the date of the rider to the policy, whichever is later”.

It says a lot. Even if you shared wrong information or hid some material facts, then also it is purely life insurance Company’s responsibility to dig deep and find out faults WITHIN 3 YEARS ONLY. After 3 years, they cannot question. Note the period of 3 years, it is from the date of issuance of the policy, or the date of commencement of risk or the date of revival of the policy or the date of a rider to the policy, WHICHEVER IS LATER. So let us say if you took the policy today and after a few years, the policy lapsed due to non-payment of premium. However, you thought to renew it again and paid all dues. In such a situation, this 3-year period starts from such revival date, but not from the original policy issued date.

Read the complete details about this IMPORTANT act of Life Insurance in my earlier post at “Term Insurance-Claim Settlement Ratio no more a big criteria”.

# Disclose the facts Properly

While buying Life Insurance products, you must fill the proposal form on your own. Never allow any agent or Life Insurance Company representative to fill it. Disclose the facts properly without hiding anything. This will really help you in a big way. Also, it will not give any room for insurers to reject your claim.

Do the things properly which are in your hand. Rest HOPE for the best.

I want to opt medical insurance for my family which one would be better please suggest?

Dear Sai,

It is hard to suggest without knowing your background.

Nice article to rule out most confusions. I am looking for term insurance for myself, 34 years, non smoker. The premium with ICICI is around 5k less than HDFC. Should I opt for ICICI? Personally I have more trust in HDFC life as a brand, but as suggested by many PPL, that term insurance is not an investment and one should go with plan with lower premium from any good company. What do you suggest?

Dear Tarun,

Don’t listen to anyone. None have control over the company claim. The only thing that you can control is disclosing the facts properly. Go with the one with whom you are comfortable.

Thank you for sharing detailed review.. It is very helpful. I am following your articles regularly.

I have question.

I am now 45 years old and i took Aegon Life iTerm Plan many years back. Now seems Aegon discontinued this plan. Do you still suggest to continue with Aegon Life iTerm Plan? or do i need to switch to other companies term insurance?

Regards

Venkatesh

Dear Venkatesh,

Please continue.

Very detailed and exhaustive information on term plan. Thanks!

Dear Sanjit,

Thanks.

Dear Basunivesh,

Reading your post on your blog about best life insurance gave me the proper perspective on the matter for the first time in my fairly long life!! Thank you so much for the well analysed and fine details in your offerings.

Would greatly value your opinion and suggestion for a policy suitable for my 18yr old granddaughter. I’m thinking of a total (?lump sum) investment of 12 lakhs for a 20 yr policy. In anticipation of your kind advice.

Dear Suzoy,

Whether she is earning? Whether someone is financially dependent on her? If so, then go for Life Insruance. Otherwise, it is useless.

Hi sir, the post is useful in selecting insurance companies of our choosing. I request you to share your opinion of selecting premium payment options as in 5yrs/7yrs/10yrs or till 60 years monthly/yearly sir.

Thank you

Dear Prabhu,

Your premium payment should be up to the policy period (no more limited or single premium).

Iam ,40 years old iam interested Saral jeevan bhima yojana pls suggest top insurance companies with consistent track record

Dear Prasad,

As it is a standard product, just go with any insurer of your choice and check the premium.

I’m 31 year old, I want to purchase a best health insurance policy for my wife 25 years old & my daughter 1.5 month old, suggest me the best health insurance policy in all manner having best network near Patna Bihar & Udhampur (J&K) & also having best Claim settlement ratio & Incurred ratio.

Dear Ranjit,

May I know why you wish to separate your wife and kid in separate plan and why not you also be part of that?

Please suggest a good health insurance policy for family of three. Self. (42 yrs), spouse(38 yrs) and a child of one year.I have been searching difnt sites. Calls coming from various sources. I m literally very confused. Please suggest

Dear Manjit,

You can check with ICICI, HDFC or MaxBupa.

Great article as usual. I see mis-selling mis-spelt as mis-spelling.

Dear Ashok,

Thanks for pointing the error. Corrected it.

I m 45 yeara old…looking forward to buy term insurance policy… Kindly suggest me the best company

Dear Abhi,

Refer the above post.

Sir, sincerely waiting for Health Insurance blog and the last blog based on health insurance was soo long ago. Kindly please check if its possible. Many Thanks.

Dear Rohit,

Incurred Claim Ratio is not much relevant to health insurance buying and hence dropped the idea of writing a post on it. However, soon I will write my choice of health insruance products.

Sir ,

1.What is the definition of “Arm Forces” in Life & health insurance. Local Police include in “Arm Forces” Catagory. I’m belong to Mumbai Police but my health insurance agent advice me say NO while filling from . Now when I’m calling he replied diplomatically. Main aap kaa claim pass kar dunga.

2. What is the definition of Materialistic Fact in insurance industry.

Thank You.

Dear Suni,

1) In my view as you belong to Mumbai Police, you are not defined as Armed Forces. Hence, no worries.

2) Any facts which may impact the claim are considered as materialistic facts.

Maxlife is no 1 in claim settlement name is not in the list

Dear Bali,

In the list means the overall list? The data of Maxlife is also mentioned in above table. Please check.

Very nice analysis Mr Basu. Very useful.

Dear Venkatesh,

My pleasure.

Very detailed analysis, keep it up

Dear Manoj,

Thanks.

Sir ,

In 7th, January I’ve purchased Tata AIA term insurance, wheather it’s good or else I need to shift any other insurance company. Pls reply.

Dear Sobhan,

As you already purchased it, go ahead.

Dear Basu Sir,

Nice analysis of data and superb explanation of all relevant facts. Article has come out exceptionally well.

Sir, does Sec 45 mean that, after 3 years, policy has to be settled irrespective of wrong information or hiding facts etc?

regards

Dear Rajesh,

Thanks for your kind words. Sec.45 is meant for protection from unnecessary questioning. However, it does not mean that we have to hide true material facts. If it is impacting the claim, then still insurers can question and reject it.

Superb

Dear Vembu,

Thanks.

Hello Sir,

Appreciate the efforts that you have done over the last 10 yrs thru’ your blog. I was curious as why you are yet to publish the top MFs (across categories) that you usually post at beginning of every year. Looking forward to it.

Dear Dev,

Thanks. I will publish soon.